corporate presentationjuly2011

TRANSCRIPT

U.S. Silver Corporation July 2011

TSXV : USA US OTC Markets : USSIF

Forward Looking Statements

Certain statements contained in or incorporated by reference into this presentation constitute forward-looking statements. The words "may", "would", "could", "will", "intend", "plan", "anticipate", "believe", "estimate", "expect" and similar expressions as they relate to U.S. Silver or its management, are intended to identify forward-looking statements, however, other information may also constitute forward-looking statements. Such statements reflect the current views of U.S. Silver with respect to future events and are subject to certain risks, uncertainties and assumptions. Many factors could cause the actual results, performance or achievements of U.S. Silver that may be expressed or implied by such forward-looking statements to vary from those described herein should one or more of these risks or uncertainties materialize. U.S. Silver does not intend, and does not assume any obligation, to update these forward-looking statements.

Page 2

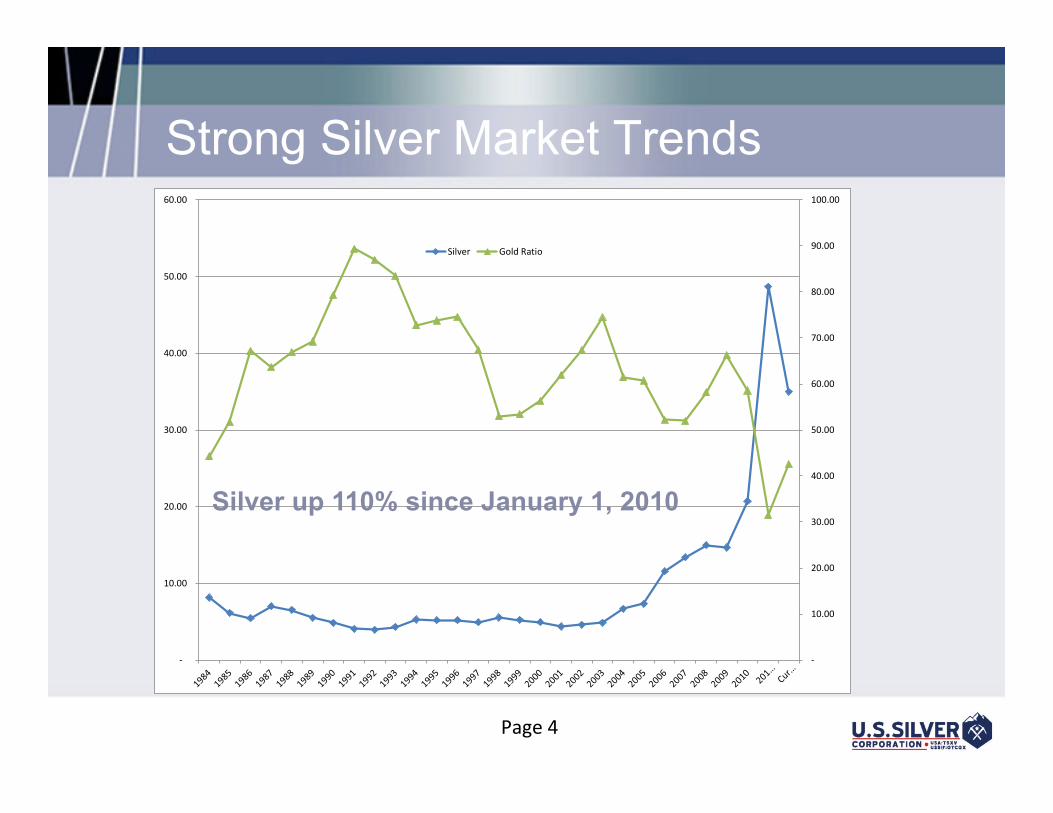

Strong Silver Market Trends

In 1980, when Nelson Bunker Hunt was asked as to why he had developed a passion for silver, he said; "Silver looked safer than overseas oil concessions, the way things were going. And precious metals were a good hedge against paper money".

Silver Demand – Industrial and Investment

Page 3

-‐

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

-‐

10.00

20.00

30.00

40.00

50.00

60.00

Silver Gold Ratio

Strong Silver Market Trends

Silver up 110% since January 1, 2010

Page 4

Million oz Ag Annual production 85% of revenue from silver

Company Overview

2.4

Established producer in prolific Silver Valley in Northern Idaho

Low cost incremental growth potential (excess capacity)

Revenue of $85 million at current prices

Page 5

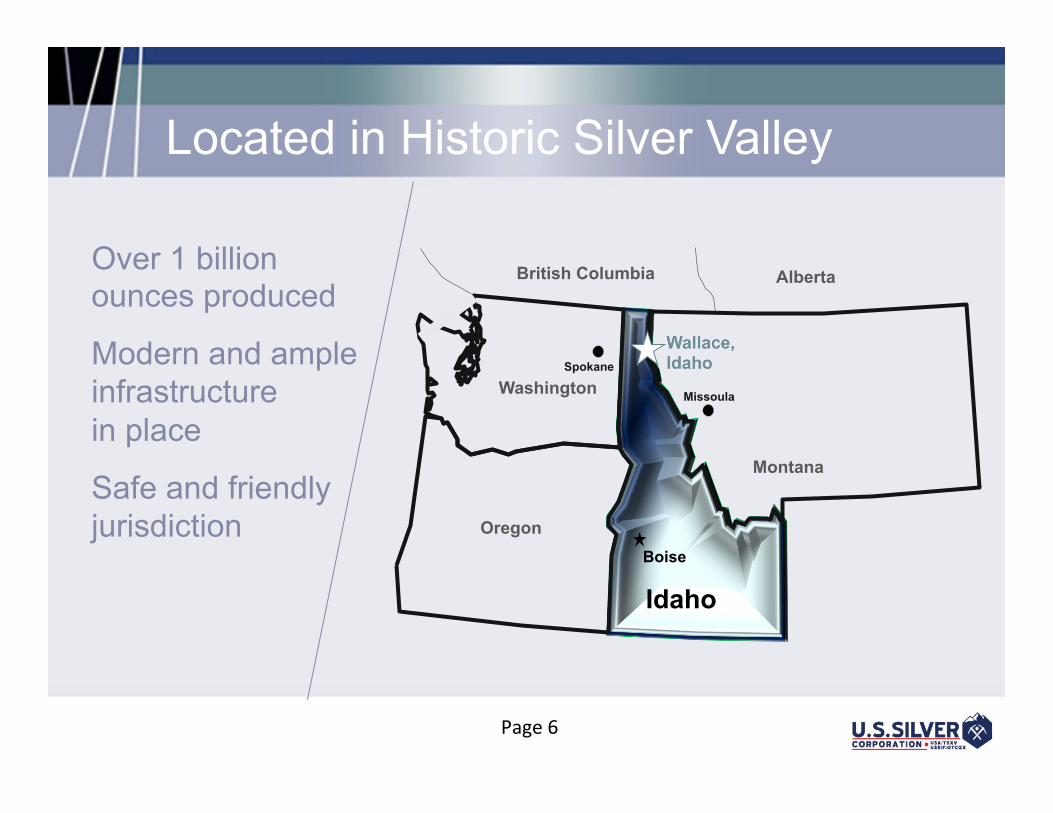

Located in Historic Silver Valley

Montana

Oregon

Washington

British Columbia

Spokane

Alberta

Missoula

Boise

Idaho

Over 1 billion ounces produced

Modern and ample infrastructure in place

Safe and friendly jurisdiction

Page 6

Company Overview • 100% interest in the producing Galena silver-copper-lead mine

– High grade narrow vein mining operation, opened in 1953

• 100% interest in the Coeur Silver mine – Redevelopment plans underway

• 2 mills (Galena and Coeur) – Both in use, excess capacity available

• Dominant land position in the Silver Valley – Large under explored property

• No historic environmental liability with EPA – Settled in 2001

• Hedged 20% of production in 2011 to protect CapEx program • 80% unhedged, 100% unhedged in 2012 and after

Page 7

Million oz Ag

Proved & Probable Reserves

21.9

86 Million lbs. lead

11 Million Lbs. copper

Provides a 7 year mine life

Exploration consistently replaces annual production

Has produced for almost 60 years and still keep finding ore

Page 8

Recent Results

Page 9

• Q1 2011revenue lower due to two rail cars shipped but not received un@l early Q2

• Q2 will have record revenue and profit as a result

!"#$%"" $%"% $%%&

'()(*+( "&," -$,.################# ./,&#################01(2345*6#127854 9,$ "%,.################# :,%###################;2(#43<#5*=7>( -,$ .,&################### $,%###################?3@A#827>#01@ B,$ "/,%################# 9,:###################

C5D)(2#127E+=457* .&.F:-:########### $F$B/F9"B####### $F.$BF"/-#######G(3E#127E+=457* "F$BBF$%"####### /F-":F-9&####### -F..-F-/-#######?711(2#127E+=457* $/&F.%"########### "F%%%F:"&####### "F%B/F:%B#######?3@A#=7@4#H#7+*=(#I6 "B,&B############### ":,/%############### "",-B###############

Million

Market Data

$193

Current Market Cap (July 14, 2011)

52 week hi-lo $0.83 - $0.15

292.4 million shares outstanding

335.3 fully diluted

TSX.V and OTCQX average daily volume 1 Million

Undervalued vs. peers on key metrics

Page 10

Galena Mine

Page 11

Galena Mine – an impressive history

High grade, narrow vein, copper-silver & lead-silver mine

Short term variability in operating results, long term proven producer

No historic environmental liability

2nd largest

Primary silver producer in the U.S.

Page 12

Galena – Past & Present

Focusing on higher grade zones to increase head grade Examining production expansion options with high prices Continued exploration success and mine life extension

1 million

Ounces produced

7 9

Page 13

Mining Operations

No.

3 S

haft

Gal

ena

Shaf

t

Cal

aday

Sha

ft

Coe

ur S

haft

2400

Sea Level

3700

5500

Cal

laha

n Sh

aft

4900

483 356 400

Coeur 3700

2800 3000

3400

1200

Silver Vein 117-215

72

Ag - Pb Veins Ag - Cu Veins

5200

4600 4300 4000

LEGEND

175

Page 14

Galena Performance

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2007 Actual 2008 Actual 2009 Actual 2010 Actual 2011 Forecast

Silver ounces produced

Page 15

Milling Operations

Excess Capacity Galena Mill 900 tons/day and Coeur Mill 500 tons/ day = total capacity of 1,400 tons/day

Ores 2 ore types (silver-copper and silver-lead) have separate crushing, milling and flotation circuits

Recoveries Consistent mill recovery rates of 96% for silver-copper and 92% for silver-lead ores

Smelters Silver-copper concentrates railed to Quebec and silver-lead cons trucked to Trail, BC

Page 16

Reserves Detail

• Current 43-101 based mine life of approximately 7 years

• U.S. Silver continues to cost effectively add reserves well in excess of its production, continually extending mine life

• Reserves increased by 115% since 2006

Ag Lead CopperTons Ag (oz/t) (MM oz) (MM lb) (MM lb)

Proven & Probable Reserves 1,615,700 13.6 21.9 85.6 11.1Measured & Indicated Resources 560,600 15.6 8.7 14.4 4.8Inferred Resource 1,026,300 13.4 13.7 103.3 5.4Total 44.4 203.3 21.3

Contained

Page 17

Coeur Redevelopment

Page 18

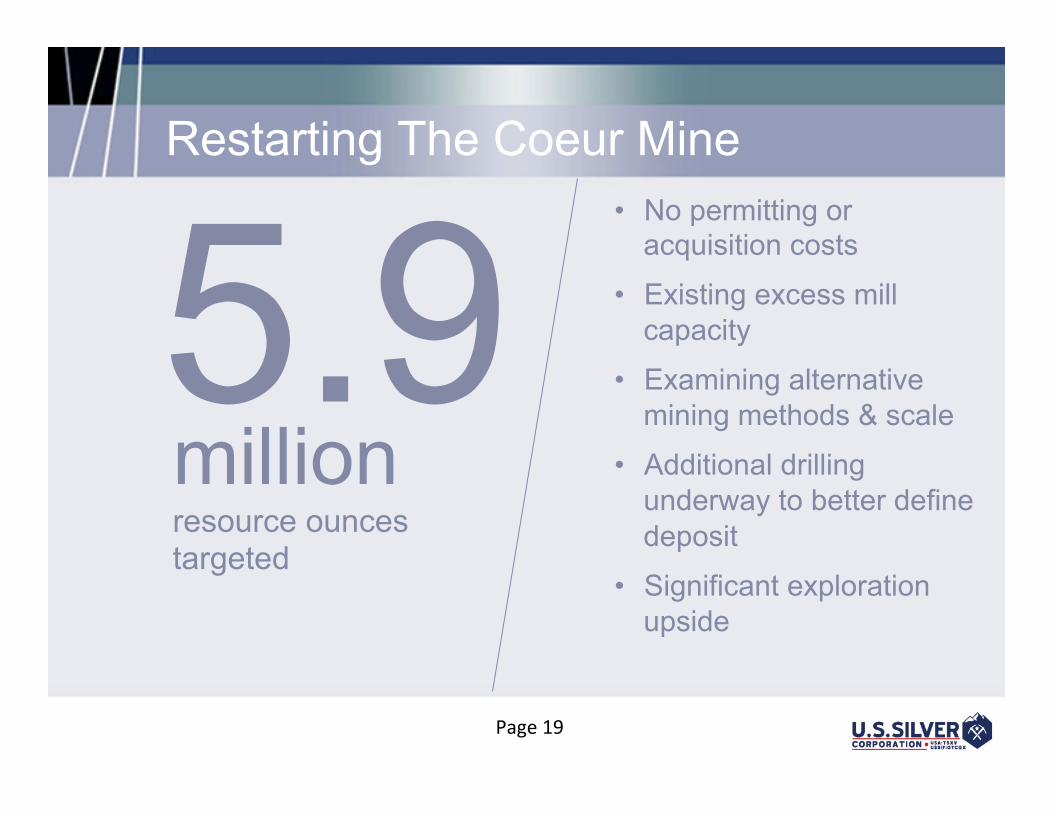

Restarting The Coeur Mine

• No permitting or acquisition costs

• Existing excess mill capacity

• Examining alternative mining methods & scale

• Additional drilling underway to better define deposit

• Significant exploration upside

5.9 million

resource ounces targeted

Page 19

Exploration Potential

Page 20

• Dominant land position • Under explored, accessible • Strong cash flow funding all

plans, 50% increase in footage in 2011

• Identified 6 surface & underground targets that are ready for drilling

• Historical success of increasing reserves well in excess of production

14 Thousand

acres of land

Exploration Potential

Page 21

Significant Reserve Growth

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2005 2006 2007 2008 2009 2010

Proved and Probable Silver Reserves

Page 22

Surface and Underground Drill Targets

CDA “GAP”

Western Coeur Mine

Argentine Vein

Deep Coeur Mine

Deep Silver Vein

Calady Mine Lead-Silver

Page 23

Surface Drilling Targets

Commencing 12,000 foot surface drilling program • CDA Gap • Argentine Vein Drill ready targets identified by • Surface and underground showings • Geochemical profile matching that of Galena/Coeur • Strong correlation between surface tetrahedrite

showings and deeper silver vein systems

Page 24

Underground Drilling Targets

• Targets: Western Coeur Mine Deep Coeur Mine Deep Silver Vein Caladay Lead-Silver

• Targets are extensions of known vein systems

Page 25

The Right People in Place

Page 26

Experienced and Stable Workforce

33 with over 20 years of experience Additional 30 contract miners

237 employees

Page 27

The Right Management Team Gordon E. Pridham Chairman

• Over 25 years experience in investment banking, capital markets, and corporate banking • President and CEO of Edgewater Capital and Chairman of Titanium Corporation

• Serves as a Director for Newalta Income Fund

• Formerly with Chemical Bank and National Bank, in the energy and minerals sector in New York, Calgary, and Toronto

• Formerly with Merrill Lynch Canada and Midland Walwyn and managed the Investment Banking groups at Deutsche Morgan Grenfell, Research Capital, and Raymond James

Tom H. Parker President , CEO & Director

• Mining engineer with over 40 years experience in the mining industry • Former President and CEO of Gold Crest Mines and High Plains Uranium

• Worked for 10 years as an Executive VP of Anderson and Schwab, a New York based management consulting firm

• Former CEO of Contain Minerals which owned 22 coal mines, the Brewer gold mine, and Montana Talc

• Worked for 10 years for ARCO where he was President of Beaver Creek Coal Mines, General Manager of Nevada Molly, President of Thunder Basin Coal and VP for Engineering, Exploration and Business Development

• Former General Manager of Jacobs Ranch mine for Kerr McGee Coal and served as Project Manager for Conoco

Steven Long Chief Operating Officer

• Over 33 years experience in mine engineering and management • Direct senior management of underground mining operations for Newmont Mining Corporation in Elko, Nevada and Barrick

Gold, Echo Bay and Homestake Mining

Chris J. Hopkins CFO

• Chartered Accountant with over 25 years experience in financial management, strategic planning, mergers and acquisitions, corporate finance and financing and management reporting

• Formerly with Rio Algoma, Suncor, and several junior mining and oil & gas companies

Mine Management • Many long service management end employees provide knowledge and continuity • New management bring new thinking and approaches

Page 28

The Right Board

John S. Brock Director

• Geologist with over 40 years experience as an executive for 20 public, junior exploration companies • Participated in 12 major mineral deposit discoveries in north and western Canada, Nevada, Mexico, and Ecuador

• Served six years as governor of the Vancouver Stock Exchange (TSX Venture Exchange) and CDNX Exchange and 2 years on the TSX Venture Exchange Advisory Board

• Currently CEO of Pacific Ridge Exploration and Senior Consultant to the Manex Resources Group

James M. Macintosh Director

• Geologist and mining analyst with over 15 years experience • Served as an executive and a director of numerous public and private companies in Canada and the United States

• President and COO of Innovium Capital, a company that invests in innovative opportunities

Kevin D. Stulp Director

• Served on the board of Aurora Oil & Gas since 1997 • Worked as a consultant with Forte group,

• Held various positions with Compaq Computer Corporation, including industrial engineer, new products planner, manufacturing manager, director of manufacturing and director of worldwide manufacturing reengineering

Alan R. Edwards • Board of directors for Gammon Gold Inc., Entrée Gold Inc., and Copper One Inc. • President and Chief Executive Officer of Copper One Inc.

• Senior management positions with Frontera Copper, Apex Silver Mines, Kinross, Cyprus Amax, Phelps Dodge

• Mr. Edwards holds an MBA from the University of Arizona and a B.S. Mining Engineering also from the University of Arizona.

Page 29

Summary

Opportunity to Capitalize on a proven and established asset • Produc@on growth • Reserve Growth • Explora@on Expansion

Increased Strength

Page 30

Summary

• Highly leveraged silver producer,

85% revenue from silver, strong cash flow • Stable and consistent production • Infrastructure in place with excess capacity • Dominant land position with significant

exploration upside with in a highly prospective region • No debt, sufficient financial capacity to execute

growth plan

• No historic environmental liability

Page 31