corporate real estate challenges in 2013 · pdf filecorporate real estate challenges in 2013 3...

TRANSCRIPT

Corporate Real Estate Challenges in 2013

95.2%

30%

While 95.2% of respondents believe the workplace has an impact on employee productivity ...

... only 30% measure how the workplace impacts productivity.

Financial Services

CORPORATE REAL ESTATE CHALLENGES IN 2013 SURVEY SUMMARY

In the ever-changing financial services industry, corporate real estate (CRE) teams face myriad challenges in maintaining increasingly distributed/global portfolios. Mergers and acquisitions, as well as corporate dissolutions have confronted CRE teams with portfolios that can literally change overnight. Despite this volatility, portfolio managers are expected to demonstrate strong value in sustainability, speed-to-market, cost reduction and operational efficiency.

Building on the findings of Gensler’s 2010 Global Portfolio Management and Planning Survey, we conducted a survey last year to delve deeper into CRE challenges. The questions specifically looked at growth, information tools, and workplace strategies.

This summary highlights the survey results. The findings offer insights into the types of tools and processes that can assist CRE teams in better managing their real estate portfolio.

1

2

Highlights

Corporate Real Estate Challenges in 2013 2

METHODOLOGY

Gensler issued this survey to senior leaders of top financial services firms:• 90% were at the VP level or above—SVP, Executive Director, Managing Director,

C-Level—and report to the most senior levels of their organizations• 81% represent US-headquartered firms

Approximately how many square feet of total real estate does your company have in its entire portfolio?

Over which geographies do you have direct responsibility?

Which of the following statements best describes the scope and responsibilities of your role?

50 to 100 million sf 23.8%20 to 50 million sf 9.5%5 to 20 million sf 28.6%2 to 5 million sf 9.5%Less than 2 million sf 28.6%

Workplace Decisions 53% Both Real Estate andWorkplace Decisions 33%Real Estate Decisions 14%

(%)

0

100

50

75

25

RESPONDENT PROFILE

Global ScopeRespondents were responsible for understanding and directing global portfolio holdings with very diverse local workplace and real estate conditions.

Portfolio Size60% of the companies surveyed had portfolios of more than 5 million square feet.

Real Estate and Workplace Responsibility Just over half of respondents reported responsibility for workplace decisions. A third reported responsibility for both real estate and workplace decisions.

United States 90%Canada 30%Central/South America 30%Asia-Pacific 30%Western Europe 25%United Kingdom 25%Australasia 20%Eastern Europe 20%Middle East 20%Africa 20%

Corporate Real Estate Challenges in 2013 3

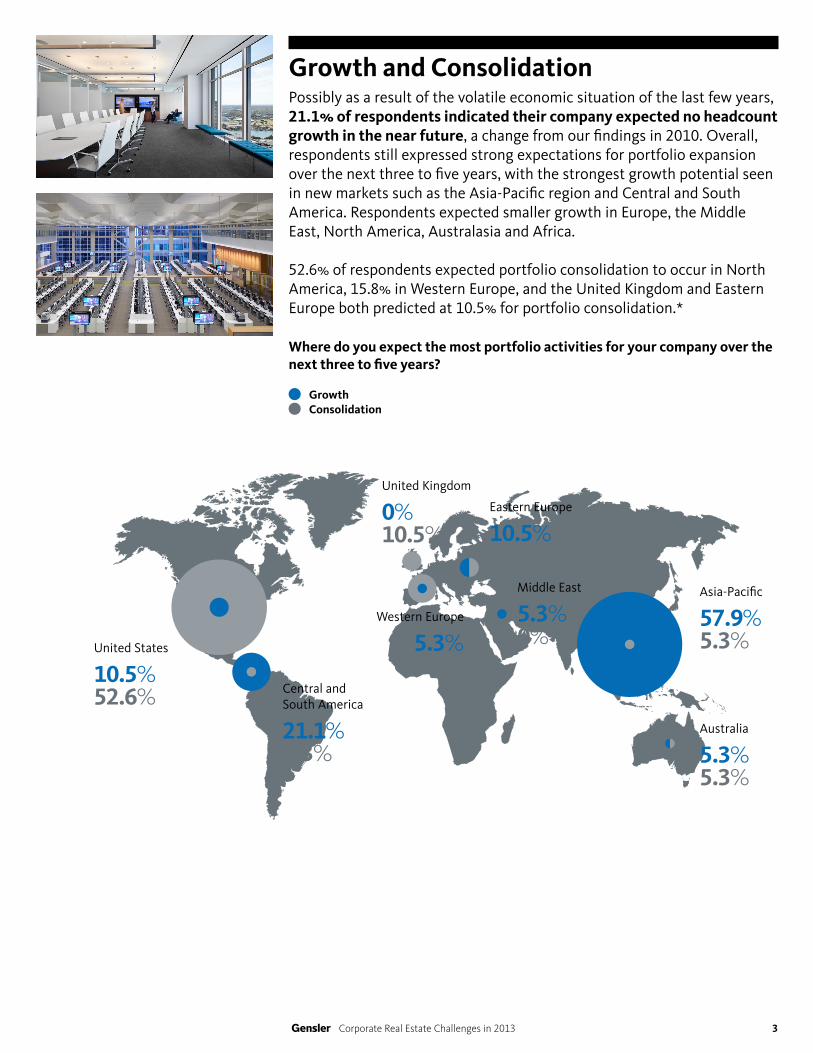

Growth and ConsolidationPossibly as a result of the volatile economic situation of the last few years, 21.1% of respondents indicated their company expected no headcount growth in the near future, a change from our findings in 2010. Overall, respondents still expressed strong expectations for portfolio expansion over the next three to five years, with the strongest growth potential seen in new markets such as the Asia-Pacific region and Central and South America. Respondents expected smaller growth in Europe, the Middle East, North America, Australasia and Africa.

52.6% of respondents expected portfolio consolidation to occur in North America, 15.8% in Western Europe, and the United Kingdom and Eastern Europe both predicted at 10.5% for portfolio consolidation.*

Where do you expect the most portfolio activities for your company over the next three to five years?

United Kingdom

0%10.5%

Eastern Europe

10.5%10.5%

Western Europe

5.3%15.8%

Middle East

5.3%0%

Australia

5.3%5.3%

Asia-Pacific

57.9%5.3%

GrowthConsolidation

Central and South America

21.1%5.3%

United States

10.5%52.6%

Corporate Real Estate Challenges in 2013 4

Planning for the factors above is done on a relatively tight schedule, with 63.2% of respondents saying planning for change happens less than three years out. Another 31.6% of respondents said they plan three to five years out.

Within what timeframe do you generally plan for business changes or headcount growth?

Less than 3 years out 63.2%3 to 5 years out 31.6%11 to 15 years out 5.3%

84.2%

77.8%

72.3%

61.1%

44.4%

38.9%

29.4%

15.8%

Economic volatility

Changing business models

Growth in new markets/geographies

Talent availability

Cyber security

Political risks/uncertainy in emerging markets

Generational shifts

Climate change

For the factors listed below, please indicate the level of impact you believe each will have on the future of real estate and the workplace in the financial services industry. (percent citing high or very high)

Economy Still Looms LargeWhen asked to rate various factors for potential impact on the industry, concerns about the economy dominated the responses. Economic volatility took the top spot—84% of respondents were concerned about its impact on the industry, with business models and growth in new markets claiming second and third (78% and 72%, respectively).

Talent availability was also a consideration for almost 2/3 of respondents, while generational shifts and climate change rounded out the list.

Corporate Real Estate Challenges in 2013 5

83.3%

83.3%

77.8%

68.8%

61.1%

55.5%

52.9%

33.3%

How would you rate the importance of the following information for making effective real estate/workplace decisions? (percent citing quite important or very important)

Informing the Right ChoicesTimely access to information is vital for CRE decisions. Survey respondents indicated better understanding of space utilization and business unit workflow/processes would be most helpful. At the opposite end of the spectrum, benchmarking against peers was seen as important by only 1/3 of respodents.

Space utilization

Better understanding of business unit workflow/work processes

Electronically available occupant information—who sits where

Employee satisfaction with physical environment

Employee work patterns/work styles (i.e., mobility)

Cultural variances —differences in workplaces across regions

ROI for sustainability strategies

Peer comparisons

Confidential Financial Services Client, Minneapolis, MN, USA

Corporate Real Estate Challenges in 2013 6

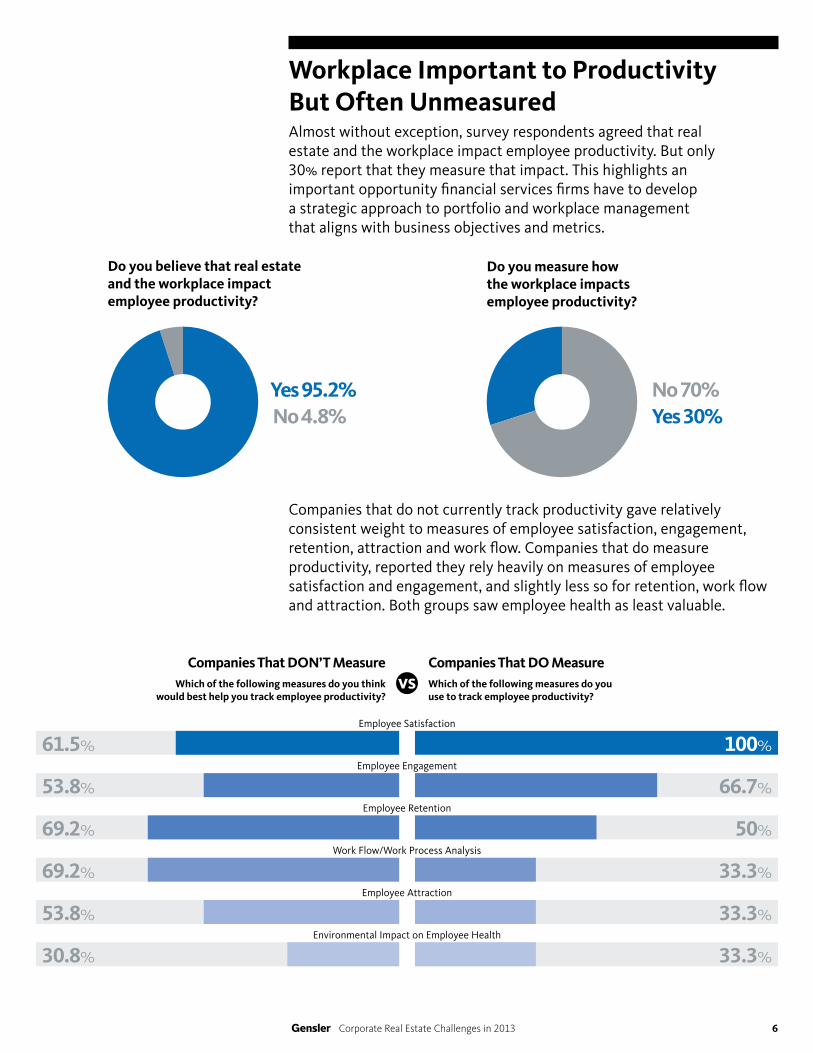

Workplace Important to Productivity But Often UnmeasuredAlmost without exception, survey respondents agreed that real estate and the workplace impact employee productivity. But only 30% report that they measure that impact. This highlights an important opportunity financial services firms have to develop a strategic approach to portfolio and workplace management that aligns with business objectives and metrics.

Companies That DON’T MeasureWhich of the following measures do you think

would best help you track employee productivity?

Do you believe that real estate and the workplace impact employee productivity?

Do you measure how the workplace impacts employee productivity?

Companies that do not currently track productivity gave relatively consistent weight to measures of employee satisfaction, engagement, retention, attraction and work flow. Companies that do measure productivity, reported they rely heavily on measures of employee satisfaction and engagement, and slightly less so for retention, work flow and attraction. Both groups saw employee health as least valuable.

Companies That DO MeasureWhich of the following measures do you use to track employee productivity?

100%

66.7%

50%

33.3%

33.3%

33.3%

Employee Satisfaction

Employee Engagement

Employee Retention

Work Flow/Work Process Analysis

Employee Attraction

Environmental Impact on Employee Health

61.5%

53.8%

69.2%

69.2%

53.8%

30.8%

vs

Yes 95.2%No 4.8%

No 70%Yes 30%

Corporate Real Estate Challenges in 2013 7

Least

Most

Which of the following alternative workplace strategies do you believe are of greatest interest to the financial services industry? (percent citing quite interested or very interested)

Strong Interest in Alternative Workplace StrategiesWhen asked about interest in a variety of alternative workplace strategies, respondents indicated strong interest in nearly all options, pointing to their openness for new approaches to traditional workplace design.

In terms of drivers of alternative workplace strategies, repondents cited cost as the number one driver, but followed closely by the desire to attract and retain talent with flexible work arrangements.

Which of the factors below do you think are the biggest drivers of alternative workplace strategies? (rank each factor where 1 has the biggest impact and 7 the least)

1. Need to reduce real estate costs

2. Flexible work strategies to attract and retain talent

3. Advancements in technologies that support virtual communication

4. Business emphasis on collaboration

5. Differences in how employees work today

6. Preferences younger workers have for space

7. Digitization of information storage and retrieval

79%

73.7%

72.2%

66.6%

57.9%

Open, collaborative spaces with solutions for addressing privacy

Design strategies based upon work flow (i.e., activity-based settings)

Consolidation—smaller offices/smaller workstations

Mobility programs (no desks/shared desks)

Employee work-at-home solutions

For more information, contact:

Rocco [email protected]+1 (212) 492-1539

Rockefeller Center1230 Avenue of the AmericasSuite 1500New York, NY 10020USA

Dianne [email protected]+1 (949) 260-8551

4675 MacArthur CourtSuite 100Newport Beach, CA 92660USA

© Gensler 2013. The information contained within this brochure is and shall remain the property of Gensler. This document may not be reproduced without prior consent from Gensler.

www.Gensler.comTwitter.com/GenslerOnWorkwww.GenslerOn.comFacebook.com/GenslerDesignYouTube.com/user/GenslerTV

Key Takeaways• Corpore Real Estate Executives (CREs) remain focused on

the bottom-line. They are looking for opportunities to cut costs even as they recognize the need to retain talent and evolve in response to changing business models.

• Information is at a premium. There is a growing interest in work flow and process analysis alongside continued interest in traditional data such as space utilization and employee satisfaction.

• Measures of workplace productivity are strongly desired but rarely used.

• Alternative workplace strategies are on the table. Cost and flexibility are the top factors driving interest in new ways of working.