corporate tax avoidance and public debt costs

TRANSCRIPT

1

Corporate Tax Avoidance and Public Debt Costs *

Terry Shevlin University of California – Irvine

Oktay Urcan London Business School

Florin Vasvari London Business School

August 2013

Abstract We investigate the impact of corporate tax avoidance on the cost of public debt and provide evidence on the channels through which it affects the cost of debt. Although corporate tax avoidance increases current after-tax cash flows thus lowering default risk, it amplifies the uncertainty by negatively affecting future cash flows and it facilitates more opaque reporting. Using a large sample of US corporate bonds, we document that corporate tax avoidance is associated with higher bond offering yields. We also find that tax avoidance predicts lower and more volatile future cash flows and that approximately one third of the total effect of tax avoidance on the cost of public debt is explained through the negative effect of tax avoidance on future cash flows levels. Consistent with the lasting negative impact of tax avoidance activities on bondholders' wealth, we find that insurance companies, who are long term buy-and-hold bond investors, are less likely to own the bonds of the firms engaging in these activities. Additional cross sectional analyses indicate that corporate tax avoidance increases the cost of public debt especially when equityholders and the management have incentives to expropriate bondholders’ wealth and when the probability of an IRS audit is high. JEL Classifications: G31, G32, M10, O16 Keywords: Corporate Tax Avoidance, Cost of Public Debt, Bond Ownership, Governance * We appreciate helpful comments from Atif Ellahie, Scott Richardson, Texas Tax Readings Group, and seminar participants at London Business School. We gratefully acknowledge the support of London Business School RAMD Fund. We thank Michelle Hanlon for generously supplying the names of their tax shelter firms.

2

1. Introduction

An expanding literature has analyzed the consequences of corporate tax avoidance in

capital markets focusing mainly on equity pricing (e.g., Hanlon and Slemrod, 2009; Wilson,

2009; Koester, 2011; Hutchens and Rego, 2012; Goh et al., 2013). We add to this literature

by examining the association between corporate tax avoidance and offering yields of public

bond issues and investigating the determinants of this association. The analysis of the effect

of tax avoidance on the cost of debt is relevant given the inconclusive findings of its effect on

the cost of equity, the conflicts of interest between equityholders and debtholders and the fact

that, in contrast to the cost of equity, the cost of debt is affected by idiosyncratic risk factors.1

In addition, corporate tax avoidance is potentially another determining factor of the cost of

public debt financing which affects the use of public bonds in the capital structure of the

firm.2 Understanding the drivers of the cost of public debt is important given that the U.S.

corporate bond market provides one of the largest sources of capital to public corporations:

the average annual corporate bond issuance in the U.S. over the last six years exceeded $950

billion, compared to an average of about $200 billion raised through common equity

issuances (SIFMA, 2012).

Prima facie, corporate tax avoidance reduces cash taxes, increasing current after-tax

cash flows available to service the debt, and thus reducing the risk of default. This argument

suggests that we should observe an inverse relation between debt offering yields and tax

avoidance: firms exhibiting more corporate tax avoidance should receive lower bond offering

yields. However, two main countervailing forces lead to the opposite prediction suggesting

that it is an empirical issue as to whether increased corporate tax avoidance is associated with

lower or higher bond yields. First, corporate tax avoidance activities could induce higher

1 The classical Merton (1974) model suggests that debt investors demand compensation for exposure to total asset volatility risk which is affected by both systematic and unsystematic risk factors. Corporate tax avoidance is likely to affect asset volatility through its impact on the firm’s cash flows. 2 In a recent paper, Rauh and Sufi (2010) document that bond debt represents approximately 20% of total assets for a random sample of U.S. non-financial corporations.

3

uncertainty about the magnitude and volatility of the firms' future profits and cash flows.

Lower and more volatile future cash flows are viewed negatively by debt holders. This future

cash flow uncertainty can be due to elevated tax risk which comes about because of an

increased probability of IRS audits, penalties and interest charges but also due to managerial

rent extraction. Complex tax structures can be used by firm managers to enable and obscure

the expropriation of firm resources (e.g., Desai et al., 2007; Dhaliwal et al. 2011; Hanlon et

al., 2012).

Second, in the spirit of Scholes et al. (2008), corporate tax avoidance activities may

decrease the quality and transparency of the financial statements. Desai and Dharmapala

(2006) and Desai et al. (2007) argue that tax avoidance, especially that involving more

aggressive positions, often involves opaque reporting. Consistent with this argument,

Balakrishnan et al. (2012) find that firms with tax planning activities are characterized by a

less transparent information environment due to these activities' role in increasing the

complexity of the firm.3

We test these arguments using a sample of approximately 7,000 individual bond

issues from 962 U.S. domiciled non-financial firms over the period 1990-2007. We employ a

number of proxies to capture corporate tax avoidance. Our first measure, ETR5, is the ratio of

total tax expense scaled by total pre-tax income net of total special items averaged over a five

year period just prior to the bond issue (Dyreng et al., 2008). This measure captures the

average GAAP effective tax rate (ETR) and reflects tax planning activities that lower taxable

income but have no effect on past, current or future book income thus giving rise to

permanent differences between the two incomes.4 Our second measure is the ratio of taxes

3 On the other hand, Wang (2010) documents that more transparent firms engage in more tax avoidance, suggesting that tax avoidance enhances shareholders' wealth. 4 Shevlin (2002) argues that tax activities that give rise to permanent differences represent the ideal tax shelter because the lowering of taxable income but not book income avoids the book-tax trade-off when firms undertake conforming tax activities (meaning both taxable and book income are lowered). In contrast, tax

4

paid in cash to pre-tax income net of total special items averaged over the same five year

period (CETR5). This measure captures the effect of all cash tax savings, whether they are

temporary or permanent.5 Our third corporate tax avoidance proxy is a composite tax

avoidance measure, CTA, computed as the average of the annual decile ranks of ETR5 and

CETR5. We standardize the average to be between zero (high tax avoidance) and one (low

tax avoidance).

We find that offering bond yields are higher for firms avoiding more taxes.

Specifically, we document a significant negative relation between bond offering yields and

the three corporate tax avoidance measures (higher values indicate less tax avoidance).

Although the economic magnitudes of these average effects seem small, we investigate the

impact of factors that are potentially associated with a larger economic impact in additional

analyses. To better isolate the effect of corporate tax avoidance on bond offering yields, we

control for an aggregate measure that captures several accepted proxies of information quality

throughout all multivariate analyses in our study. Therefore, the effect of corporate tax

avoidance on bond offering yields is incremental to the effect of information quality.

We run three additional robustness analyses. First, we address the issue that corporate

tax avoidance measures, despite being lagged for up to five years, are potentially endogenous.

Following the approach of Dittmar and Mahrt-Smith (2007), we use tax avoidance measures

computed in the first year they are available in our sample period, thus removing the time

variation in these measures, and find similar results. Second, we replace the bond yields with

a measure of the distance to default, expected default frequencies (EDFs), provided by

Moody’s/KMV. In contrast to bond offering yields, EDFs are not affected by bond illiquidity

or the tax position of the bond investors in the secondary bond market that are difficult to

control for in the bond analyses. As a certified rating agency, Moody’s has preferential access activities giving rise to temporary differences lower taxable income in the current period relative to book income but lower book income in some future period. 5 We have replicated our results using yearly effective tax rate measures and our inferences are similar.

5

to private information about borrowers when issuing ratings and uses sophisticated

information processing methodologies, relative to the marginal bond investor. Therefore, the

EDFs are less likely to reflect issues with the information quality of firm’s public reports. We

continue to find that tax avoidance measures are negatively and significantly associated with

EDFs suggesting that Moody's is concerned about the uncertainty of future cash flows

triggered by tax avoidance.

Third, we examine changes in the five year credit default swap (CDS) spreads to the

public announcement of a firm’s participation in a corporate tax shelter using the sample of

tax shelters identified by Hanlon and Slemrod (2009). CDS spreads provide a market

assessment of the probability of default and have the advantage of trading far more frequently

than the underlying bond securities (e.g., Hull et al., 2004).6 CDS spreads are also much less

affected by liquidity problems, changes in interest rates, tax issues and contract design

features that are specific to bond securities. Most importantly, prior research suggests that

CDS spreads incorporate information faster than equity markets because dealers in this

market enjoy lower information asymmetry due their access to private information (Acharya

and Johnson, 2007; Norden and Weber, 2004). We compute market adjusted changes in the

CDS spreads over a five day period centered on the tax shelter announcement dates. We find

a positive and statistically significant change in the CDS spreads of the announcing firms

suggesting that credit market participants react negatively to tax shelter announcement

events. This result provides further evidence that credit markets view corporate tax avoidance

activities negatively, likely to be due to the uncertainty generated by tax avoidance with

respect to future cash flows.

Supporting our interpretations above, we document that firms engaging in corporate

tax avoidance activities experience significant cash flow shortfalls and greater cash flow

6 The low frequency of bond trade data makes it difficult to conduct short-window tests in bond markets (e.g., Goodhart and O’Hara, 1997; Hotchkiss and Ronen, 2002).

6

volatility five years ahead. For instance, a decrease in the composite tax avoidance (CTA)

measure from the 90th percentile to the 10th percentile of its sample distribution decreases the

average cash flow from operations scaled by total assets by 0.7%, an economically

meaningful effect given that the average cash flow ratio is about 11% in our sample. The

ability of the tax avoidance measures to predict lower cash flow levels and higher cash flow

volatility suggests that bond investors view corporate tax avoidance as an early indicator of

lower and more volatile future cash flows instead of an indicator of future information

opacity that impairs monitoring efforts. We test this statement directly by implementing a

path analysis methodology. We examine three mechanisms, future cash flow levels, future

cash flow volatility and information quality, through which corporate tax avoidance

potentially increases the cost of debt. We document that corporate tax avoidance has both

direct and indirect effects on bond offering yields, with the main indirect effect arising

through lower future cash flows. This effect explains approximately one third of the total

effect of tax avoidance on the cost of public debt. Information quality is not a very important

mediating factor; the indirect effect on bond offering yields through information quality is

very small relative to the total effect.

Given that the negative impact of corporate tax avoidance on future cash flows takes a

few years to materialize, we test whether long term bond investors indeed consider this effect.

Specifically, we test whether insurance companies, the largest and most important bond

investors, are less likely to own bonds issued by firms engaging in tax avoidance activities.7

Because regulators impose strict capital requirements that increase with the portfolio's credit

riskiness, insurance companies are expected to avoid bonds issued by firms engaging in tax

avoidance activities that potentially generate future drops in credit quality due to lower and

more volatile cash flows. Consistent with our expectation, we find that greater tax avoidance 7 Because these investors have access to a stable supply of capital, relative to other investors such as mutual funds or hedge funds, they are typically long term holders of bonds. The average bond in our sample has a mean insurance company ownership (number) of 20% (10).

7

lowers the bond ownership of insurance companies. This finding reinforces our results that

corporate tax avoidance activities are viewed negatively by the bond market, and suggests

that the lasting impact of corporate tax avoidance on credit risk affects the investment

decisions of long term buy and hold investors.

In the last set of analyses, we further investigate the role of two sets of factors that

affect the positive association between corporate tax avoidance and bond yields through their

effect on future cash flows available to service the debt: debtholder wealth expropriation

incentives, which reflect the conflicts of interest between equityholders and debtholders, and

the probability of an IRS audit, which reflects tax risk. We find that proxies that capture

incentives to expropriate debtholders' wealth such as poor corporate governance, more

concentrated equity ownership, high risk-taking incentives of management and high credit

risk result in stronger associations between corporate tax avoidance and bond offering yields.

The impact of these variables is economically large. For instance, the coefficient estimates

for poorly governed firms indicate that a drop in the composite tax avoidance measure from

the 90th percentile to the 10th percentile of its distribution increases the bond offering yields

by 37 basis points, a 5.3% reduction in the average bond yields. We similarly find a stronger

relation between tax avoidance and bond yields when the probability of an IRS audit is high,

suggesting that bondholders are concerned about increased tax payouts resulting from IRS

audits.

Our paper makes a number of contributions. First, we contribute to the emerging

literature that examines how capital suppliers view corporate tax avoidance activities. The

current research provides mixed results with respect to how equityholders view tax avoidance

activities. On the one hand, Hanlon and Slemrod (2009) find that a company’s stock price

drops around news of the firm involvement in tax shelters and Hutchens and Rego (2012)

find that higher tax reserves are associated with a higher cost of capital. On the other hand,

8

Goh et al. (2013) find that less aggressive forms of corporate tax avoidance are associated

with a significantly lower cost of equity while Koester (2011) finds that shareholders value

uncertain tax avoidance positively. We add to this literature by documenting how corporate

tax avoidance is viewed by public bondholders, another set of stakeholders with often

conflicting incentives from shareholders and with a focus on downside risk protection given

their capped payoffs. Similar mixed results have been found in debt settings. Kim et al.

(2010) and Lisowsky et al. (2011) find that corporate tax avoidance and tax aggressiveness

respectively are associated with lower interest costs while Crabtree and Maher (2009) and

Ayers et al. (2010) find that book-tax differences, a proxy for higher tax avoidance, are

associated with lower ratings. While these papers focus on a different set of debt market

participants, bank lenders or rating agencies, that have preferential access to private

information, we examine the effect on the pricing of public debt where individual investors

have less ability and incentives to monitor and have access only to public information. We

contribute to this literature not only by showing the impact of corporate tax avoidance on the

actual cost of public debt but also by documenting that its indirect effect on the cost of public

debt is through lower future cash flows not information quality. Most importantly, we

provide novel insights into how corporate tax avoidance affects the investment decisions of

long term investors in public debt securities.

Second, we add to the rapidly developing literature that investigates the impact of the

reported financial information and its quality on the cost of debt securities (e.g., Yu, 2005;

Francis et al., 2005; Sengupta, 1998; Bharat et al., 2008; Easton et al., 2009; Ghosh and

Moon, 2010; Shivakumar et al., 2011; DeFond and Zhang, 2011). We show that measures of

corporate tax activities inferred from the firm's reported income statement, are relevant

variables that are also priced in the public debt market not because of their impact on the

quality of the accounting information but because they are a lead indicator of future cash

9

flows problems.

Third, our results provide an explanation on why more firms do not engage in tax

shelters and corporate tax avoidance given the possibility of substantial tax savings (e.g.,

Weisbach, 2002). Our evidence suggests that a major provider of capital, public debtholders,

view corporate tax avoidance in a negative light especially when incentives to expropriate

their wealth are in place and the probability of an IRS audit is high.

Fourth, the evidence we provide is consistent with Graham and Tucker (2006) and

Wilson (2009) who document a strong negative relation between leverage and the incidence

of tax shelter activity concluding that the two are substitutes. The findings of prior work by

Kim et al. (2010) and Lisowky et al. (2011) that tax avoidance reduces the cost of private

debt and interest expenses suggest that firms should issue more debt, increasing leverage,

thus contradicting the substitutability result. In contrast, our findings support the substitution

between leverage and corporate tax avoidance by showing that one potential explanation is

that tax avoidance makes borrowing more expensive thus incentivizing the firms to have

lower leverage.

The remainder of the paper is organized as follows. Section 2 develops our

hypotheses and summarizes the prior literature. Section 3 discusses the sample selection,

variables and the research design. Section 4 presents our findings and Section 5 concludes.

2. Hypothesis development and prior literature

2.1. Hypotheses development

Corporate tax avoidance activities significantly reduce taxes thus saving cash flows

that can be used to service the firm’s debt. For our sample firms (described more fully

below), the mean one year cash ETR (CETR) is 25.0%, a rate that is 10% below the U.S.

corporate statutory rate of 35%. Given that the mean pre-tax book income is approximately

$1,160 million, the lower rate implies average annual cash savings of $116 million ($1,160

10

million × (0.35 − 0.25)) for the average firm in our sample.8 Such relatively large annual cash

savings from tax avoidance potentially improve the solvency of the firm and reduce its

default risk. Thus, firms pursuing more corporate tax avoidance should receive lower yields

on debt issues.

However, corporate tax avoidance activities, particularly the more aggressive ones,

could reduce future cash flows and increase cash flow volatility due to tax risks or escalated

managerial rent extraction. Tax risks come about because of higher probability of IRS audits,

interest and penalties. For example, Wilson (2009) reports that, among his sample of tax

shelter participants, the median savings from the tax shelters is $66.5 million with the IRS

assessing interest and penalties on the tax shelters of $58 million. Also, complex tax

structures allow firm managers (and others) to expropriate firm resources which may or may

not include the cash tax savings from the tax avoidance activity. For instance, Dhaliwal et al.

(2011) argue that tax avoidance allows managerial rent extraction that contributes to lower

cash holdings. Such wealth expropriation reduces the after-tax cash flows to debtholders and

increases the volatility of the cash flows. Both effects (reduced level and more volatile cash

flows) will lead debtholders to require ex ante price protection via higher yields.

Second, in the spirit of Scholes et al. (2008), there are non-tax costs associated with

corporate tax avoidance activities such as lower quality and transparency of the financial

statement numbers that potentially impair bondholders’ ability to monitor the borrowers.

Desai and Dharmapala (2006), Desai, Dyck and Zingales (2007), Balakrishnan, Blouin and

Guay (2012) argue that aggressive tax avoidance often involves opaque reporting so as to

conceal either the purpose of the underlying transaction or the very existence of the

transaction to escape detection by tax authorities.9 In the same spirit, Frank, Lynch and Rego

(2009) document that tax aggressiveness is associated with the reporting of more 8 A similar calculation using the sample median indicates annual cash savings of $39.5 million. 9 Balakrishnan et al (2012) also show that firms increase other disclosures to reduce the opacity problem with shareholders. IRS could use these disclosures to go after tax avoiding firms.

11

discretionary accruals while Kim, Li and Zhang (2011) find that corporate tax avoidance

activities are strongly associated with firm-specific stock price crash risk, consistent with tax

avoidance introducing opacity by facilitating the hoarding and accumulation of bad news for

extended periods.10 Given the higher sensitivity of bond prices to negative news, tax avoiding

firms are likely to experience negative bond returns in the future, when bad news is

released.11 Therefore, if corporate tax avoidance increases the opacity of the financial

information, bondholders will face higher adverse selection and moral hazard problems that

should be reflected in higher bond offering yields.

In summary, there are arguments suggesting that public debtholders view corporate

tax avoidance either favourably or negatively. Thus it is an empirical issue as to whether

increased corporate tax avoidance is associated with lower or higher debt yields at the time

when public debt is issued. In addition, it is unclear which factors are likely to influence the

relation between the bond yields and the corporate tax avoidance. The possible agency costs

associated with tax avoidance activities discussed above are more likely to arise among firms

whose equityholders and managers have incentives to expropriate debtholders' wealth or

firms that face high IRS audit risk. We investigate the role of several mechanisms that likely

facilitate debtholders' wealth expropriation: (1) Corporate takeover markets, (2) Large

blockholders, (3) CEO's high equity risk-taking incentives and (4) High credit risk. We

discuss below the impact of these factors on debtholder wealth expropriation activities that

potentially affect the association between corporate tax avoidance activities and bond yields

at issuance.

We expect that strong antitakeover provisions, coded using the methodology of

Gompers, Ishii and Metrick (2003), are an indication of poor governance, since they shield

10 A recent line of research argues that firms with aggressive financial reporting are less likely to be tax aggressive to avoid the suspicion of investors, SEC, or IRS (e.g., Erickson et al., 2004; Lennox et al., 2013). 11 Easton, Monahan, and Vasvari (2009) document that bad earnings news are the main drivers of bond returns in the secondary bond market.

12

the firm from the market for corporate control which is viewed as a strong external

disciplining mechanism.12 Ineffective monitoring by the corporate takeover market could

allow entrenched managers to exploit tax avoidance activities for personal gains (Desai and

Dharmapala, 2006). However, the adoption of antitakeover amendments is not necessarily a

sign of debtholder wealth expropriation. Avoiding takeovers that are motivated by wealth

transfers from bondholders to stockholders (Shleifer and Summers, 1988) or increasing the

credit risk of the firm by adding debt (Warga and Welch, 1993) while preserving cash

through corporate tax avoidance schemes can be beneficial to bondholders.

Lisowsky et al. (2011) argue that debtholders view large blockholders negatively

since these shareholders have both the incentive and ability to expropriate resources and tax

avoidance activities, particularly the more aggressive ones, offer them an opportunity for

expropriation (e.g., Desai and Dharmapala, 2006; Desai et al., 2007). If this is the case, then

we expect any positive association between debt yields and tax avoidance to be stronger for

firms with large blockholders. An alternative argument can be made for the role of

blockholders as outside monitors of the management of the firm (Jensen, 1993; Shleifer and

Vishny, 1997). These shareholders have the incentives (due to the large size of their

investment) and resources to uncover managerial opportunism that also negatively impact

debtholders.

Coles, Daniel and Naveen (2006) document that a higher sensitivity of CEO's wealth

to stock volatility (vega) is associated with riskier policy choices, including relatively more

investment in R&D, less investment in property, plant and equipment, more focus on fewer

lines of business, and higher leverage. All these activities are detrimental to bondholders'

wealth because they increase the riskiness of the underlying assets and facilitate wealth

expropriation. However, another effect of increased vega is to expose managers to more risk. 12 We acknowledge the likely endogeneity of the corporate takeover index. For example, a growing firm with large needs for outside debt financing has more incentives to adopt better governance practices in order to lower its cost of debt.

13

If CEOs are undiversified with respect to firm-specific wealth, they are exposed to more risk

than diversified shareholders. Accordingly, CEOs will engage in less risky activities, which

benefit bondholders, to preserve their wealth.

Easton et al. (2009) argue that if firms are credit risky (i.e., have speculative grade

debt) then equityholders have strong incentives to engage in risky activities that expropriate

bondholders' wealth. This is because they hold a call option that is relatively close to being

out-of-the-money vis-à-vis the call option embedded in an investment grade bond. As a

result, we expect the relation between corporate tax avoidance and bond yields to be stronger

when firms are credit riskier.

Finally, several recent papers propose and test the role of the IRS as a monitor of

firm’s tax avoidance behaviour. As a monitor, the IRS reduces the ability of managers to act

opportunistically via their tax planning activities, thus protecting debtholders’ wealth.

Guedhami and Pittman (2008) examine the role of the IRS as a monitor in the pricing of

public debt (nonconvertible 144A bond issues) for private firms and find that the probability

of an IRS audit decreases bond yields among private firms. They conclude that IRS

monitoring plays a valuable corporate governance role by reducing information asymmetry

embedded in borrowing costs. Further, Hoopes et al. (2012) find that IRS audits deter

corporate tax avoidance. These arguments suggest a weaker association between tax

avoidance and bond yields when the probability of an IRS audit is higher. However,

bondholders could be concerned about the risks associated with an IRS audit of a firm’s tax

avoidance activities since such an audit can trigger large payouts introducing uncertainty

about firms’ future cash flows (Wilson, 2009).

2.2 Prior literature

Prior literature has investigated extensively how the quality of accounting numbers

(Francis et al., 2005; Bharath et al., 2008; Zhang, 2008; Bhojraj and Swaminathan, 2009;

14

Ghosh and Moon, 2010) and corporate disclosures (Sengupta, 1998; Shivakumar et al., 2011)

affect credit spreads. Another stream of literature has documented a strong relation between

accounting earnings and credit spreads (Datta and Dhillon, 1993; Hotchkiss and Ronen, 2002;

Easton et al., 2009; DeFond and Zhang, 2012). We extend this work by examining how

corporate tax avoidance, as reflected in the reported accounting numbers, affects bond yields

in the primary bond market. We show that it is the impact of corporate tax avoidance on

future cash flows rather than on information quality that is driving the association between

tax avoidance and bond offering yields.

While there have been a number of studies investigating the relation between

corporate tax avoidance and the pricing of equity, we could identify only a few studies

examining the relation between corporate tax avoidance and debt pricing that provide mixed

results. We briefly summarize these studies and highlight our incremental contribution.

Kim et al. (2010) predict and find evidence that firms exhibiting greater tax avoidance

obtain bank loans with lower interest rates and fewer covenant restrictions.13 They argue that

the cash tax savings arising from tax avoidance is likely to be viewed favorably by banks

because they have privileged access to private information and greater abilities and incentives

to monitor borrower’s activities compared to other outside capital providers. In contrast to

Kim et al. (2010), we investigate the effect of corporate tax avoidance on the cost of a

different set of contracts which are long term debt securities (average maturity is almost 12

years for bonds versus only 3-4 years for loans). Also, investors in the bond market, in

contrast to syndicate banks, rely only on publicly available information including the firm’s

financial statements, have limited monitoring incentives and cannot renegotiate their claims.

This choice also motivates our use of public financial statement based measures of corporate

tax avoidance.

13 Kim et al. (2010) proxy for corporate tax avoidance using a factor analysis of various book-tax difference measures, the 5-year cash ETR, and a tax shelter probability score based on Wilson (2009).

15

Lisowsky et al. (2011) examine the relation between measures purported to capture

the more extreme end of corporate tax avoidance (referred to as corporate tax aggressiveness)

and the interest expense of outstanding debt.14 They document that more tax aggressive firms

have lower interest rates. Lisowsky et al. (2011) examine interest expense reported in firms’

financial statements which reflects interest on both private (e.g., bank loans) and public debt

as well as other contracts such as leasing contracts and commercial paper. Thus for much of

this debt, the lenders are likely to be banks and finance companies that have incentives to

closely monitor the borrower. Additionally, there is a likely timing mismatch between the

actual cost of debt paid by the firm and the interest expense reported in the current period.

The interest expense is affected by changes in both benchmark rates (e.g. LIBOR rates) and

borrower’s credit quality since debt was issued. It is thus difficult to make inferences about

the extent to which debtholders price corporate tax avoidance in the credit risk premium at

the time of issuance.15 Finally, the use of interest expense does not allow controlling for other

debt security specific characteristics that lenders trade off at the time of issuance. We use the

bond yields on the date of issuance of the public debt and a slew of bond specific

characteristics which are known to affect bond yields to overcome these problems.16

Two papers examine the relation between book-tax differences (BTDs, both

temporary and total) and corporate bond ratings. Crabtree and Maher (2009) find that firms in

the extreme quintiles of BTDs (defined on an industry-year basis) are rated as riskier by 14 Lisowsky et al. (2011) use confidential reportable transaction tax shelter data from the IRS Office of Shelter Analysis, firms’ unrecognized tax benefits as disclosed in their financial statements, the 5-year cash effective tax rate (from Dyreng et al., 2008) and the discretionary portion of annual permanent book-tax differences (from Frank et al., 2009) to develop proxies for corporate tax aggressiveness. Because we do not have access to confidential tax return data and unrecognized tax benefits are only available since 2007, we limit ourselves to measures that can be constructed from publicly available sources such as cash and GAAP effective tax rates. Both measures capture general tax avoidance including aggressive tax positions. 15 A large portion of the debt, especially bank loans, is priced as floating rate thus the interest expense reflects current market conditions (e.g., current LIBOR rates above which loan spreads are typically set). However, these debt spreads are based on the firm’s characteristics, including tax avoidance behavior, at the borrowing date, not at the current financial statement date. 16 If these other bond-specific characteristics are in part determined by the firm’s tax avoidance activities, our results will understate the effect of corporate tax avoidance on bond yields. However, observing a significant association between corporate tax avoidance and bond yields will indicate the incremental (and direct) role of corporate tax avoidance on bond yields.

16

rating agencies. In particular, they find that firms classified as tax planners (those in the

lowest quintile ranked on 5-year ETR) have lower ratings and argue that these firms are

viewed negatively by rating agencies due to concerns about transparency and earnings

persistence. Ayers et al. (2010) also examine the same general research question by looking

at changes in corporate bond ratings as a function of changes in book-tax differences. Their

results are consistent with Crabtree and Maher (2009). We add to these papers by

investigating the impact of corporate tax avoidance on the actual cost of debt. Most

importantly, we examine the mechanisms (uncertainty of future cash flows versus

information quality) through which corporate tax avoidance activities affect bond yields. We

also investigate how insurance companies, the most important investors in the bond market

that are long term investors by typically following buy and hold investment strategies, invest

as a function of corporate tax avoidance.

3. Sample selection and variable definitions

In this section, we first present our bond sample selection process and provide

background information on the data sources to build our sample. We then describe our main

variables of interest: the cost of public debt (bond) financing, and the tax avoidance

measures. Finally, we discuss the research design and the set of bond attributes and firm-

specific characteristics used as controls in the multivariate tests.

3.1 Sample selection

We start our sample selection process with the universe of bonds in the Mergent Fixed

Income Securities Database (FISD) issued between 1990 and 2007. FISD provides bond-

specific information such as bond size, issue date, rating, coupon rate and frequency, and

other features as well as borrower-specific information. We eliminate bond issues that have

missing ratings and bond-specific information, pay variable coupon payments (a minority in

the database), are convertible into common stock, are not issued by firms incorporated in the

17

United States, or are privately placed under Rule 144A.17

We apply several additional filters to this initial dataset to obtain our final bond sample.

First, we select all bonds for which the U.S. borrower could be manually matched to

Compustat based on company name and industry membership. Second, we exclude financial

companies (i.e., those whose SIC code is between 6000 and 6999). These companies tend to

issue a large number of bonds to finance their operations or off-balance sheet trusts they

sponsor, and are highly regulated. Finally, we require bond issuers to have available data in

Compustat for relevant firm-specific variables and the tax avoidance measures. Our final

sample contains 6,905 individual bonds issued that cover 2,612 firm-years (962 firms)

between 1990 and 2007.

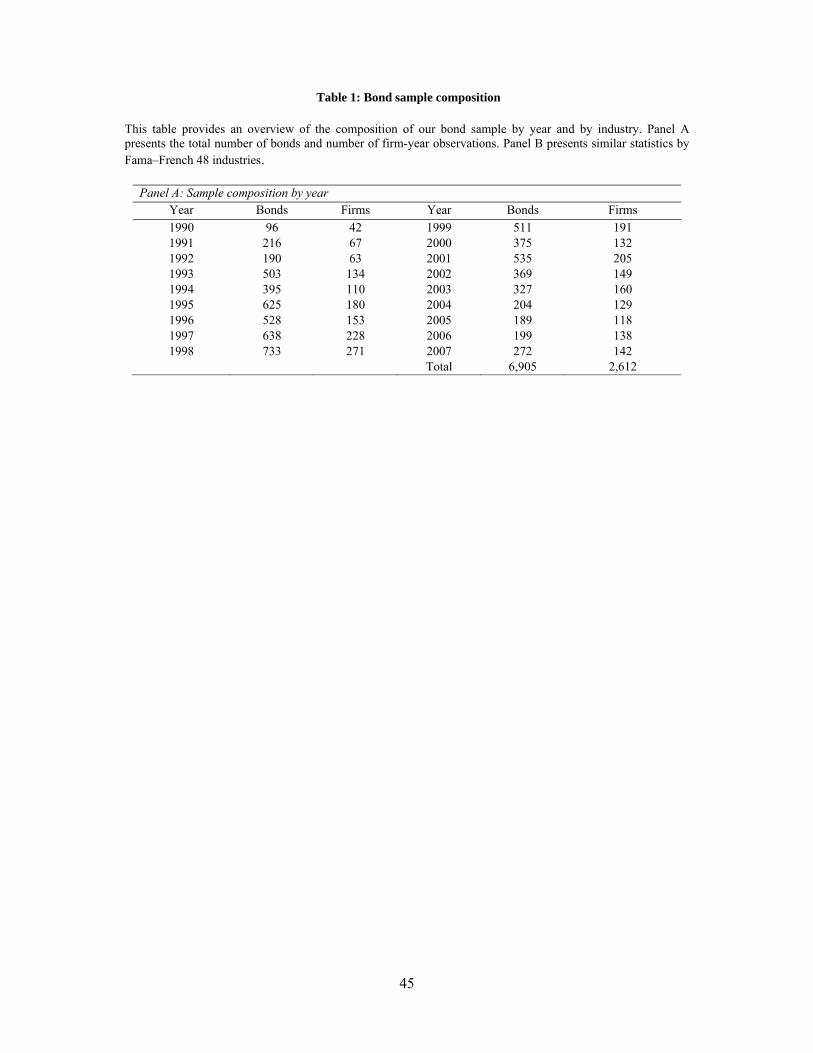

Table 1 provides an overview of the composition of our bond sample by year and

industry. Panel A presents the total number of bond and firm-year observations, and Panel B

presents similar statistics by Fama–French industries. We note some clustering in our bond

sample over time and across industries. In particular, most public bonds in our sample were

issued during the mid-1990s, with a decline in issues starting in year 1999. Finally, most

bonds were issued by firms in the utilities (24%), transportation (10%), petroleum and natural

gas (6%), business services (6%) and retail (6%) industries.

3.2. Measures of tax avoidance

We use three measures of tax avoidance. Our first measure is the effective tax rate

computed as the ratio of total tax expense over the last five years scaled by total pre-tax

income net of total special items over the same period prior to the bond issuance date

(ETR5).18 This measure reflects aggressive tax planning through permanent book-

tax differences. Examples of such tax planning are investments in tax havens with lower

17 Rule 144A does not require bonds to be registered with the SEC. Thus, borrowers under Rule 144A might not provide U.S. GAAP financial statements. Further, these bonds are less liquid than public bond issues because they can be purchased by only a limited set of qualified financial institutions. 18 Dyreng et al. (2008) argue that single-year ETR suffers from significant year-to-year variation and is a poor proxy of long-run tax avoidance.

18

foreign tax rates (provided that foreign source earnings are classified as permanently

reinvested), investments in tax exempt or tax-favored assets, and participation in tax shelters

that give rise to losses for tax purposes but not for book purposes (e.g., Wilson, 2009).

Our second measure is the cash effective tax rate computed as the ratio of total taxes

paid in cash scaled by total pre-tax income net of total special items over the last five years

prior to the bond issuance date (CETR5). This measure reflects both permanent and

temporary book-tax differences. By focusing on cash taxes paid, this measure avoids the

overstatement of current tax expense due to the accounting for the income tax benefits of

employee stock options during our pre-SFAS 123R sample period (see Hanlon and Shevlin,

2003). For both tax measures, we remove observations with negative total pre-tax income net

of total special items over the last five years and truncate the measures to the range [0, 1].

We also calculate a composite tax avoidance measure to reduce the potential effects of

noise and errors in ETR5 and CETR5. We first rank both measures into deciles in every year.

We then compute an average rank across the two measures and standardize the averages to be

between zero (high tax avoidance) and one (low tax avoidance). We label this composite tax

avoidance measure as CTA.

Panel A of Table 2 reports descriptive statistics for the tax avoidance measures. The

mean long-run effective tax rate is 32% while the mean cash effective tax rate over the last

five years preceding the bond issuance is 25%. This evidence suggests that firms pay 7%

lower taxes than their effective tax rates imply. In unreported analyses, we find that the two

effective tax rate measures are positively correlated with a Pearson correlation of 45%. The

relatively low magnitude of the correlation coefficient indicates that these measures capture

different aspects of tax avoidance and/or may be affected by measurement errors.

3.3 Research Design

We estimate the following OLS regression model, which relates offering bond yields to

19

our proxies for tax avoidance as well as bond- and firm-specific control variables:

,

∝ ∝ , ∝ ,

∝ , ∝

∝ ,

(1)

Offering bond yield is the yield to maturity of bonds computed at the time of issuance. We

include U.S. Treasury bill rates (Tbill Rate) to control for shifts in benchmark interest rates

and the time preference for money. We choose the contemporaneous yield of a U.S. Treasury

bill that has the same maturity and is the closest (in absolute value) with respect to the stated

coupon rate. In Table 2, we report descriptive statistics on the bond’s offering yield, and its

corresponding matched Treasury bill rate. The average offering yield for sample bonds is

7.03%, whereas the average matched Treasury bill rate yield is 5.73%.

Tax avoidance is a proxy for a firm's tax avoidance prior to the bond issuance (defined

above).

We control for a number of bond-specific characteristics in our empirical models. Rating

measures the credit quality of the bond issue as assessed by one of the three main certified

rating agencies (i.e., Standard and Poors, Fitch or Moody’s). Prior research has shown that

credit ratings provide information on the bonds’ default risk additional to what is available in

the public information set (e.g., Ederington, Yawitz, and Roberts, 1987; Ziebart and Reiter,

1992). We convert the letter ratings retrieved from FISD into numbers, so that a “AAA”

rating is coded as 1, a “AA+” rating is coded as 2, and so on. Hence we expect a positive

association between Rating and the bond offering yield.19 Life of the Bond is the maturity of

the bond in years. Bonds with longer maturities are usually exposed to greater interest

19 As discussed earlier, Crabtree and Maher (2009) and Ayers et al. (2010) show that credit ratings are a function of book-tax differences. Thus, by including credit ratings, we are documenting that the association between bond issuance yields and tax avoidance is incremental to the effect of tax avoidance effects on bold yields via credit ratings.

20

fluctuations and credit risks, and therefore are expected to be priced at higher yields (e.g.,

Ziebart and Reiter, 1992). Amount of issue is the total dollar face value of the bond issue.

Larger issues are usually more liquid and marketable, thus these issues might receive lower

yields (e.g., Sengupta, 1998). On the other hand, a larger issue implies a higher debt burden

for the borrower, and therefore a higher probability of default (e.g., Shi, 2003). Hence the

impact of issue size on the bond offering yield is ambiguous. Subordinated is an indicator

variable that takes the value 1 if the bond is subordinated to other debt securities, and 0

otherwise. Subordinated bonds are junior debt, and relatively riskier (Ziebart and Reiter,

1992). We therefore expect a positive association between Subordinated and bond offering

yields. Callable is an indicator variable that takes the value 1 if the bond is callable, and 0

otherwise. Callable bonds have prepayment risk, thus bondholders are likely to demand

higher yields for bonds with a call provision (Datta, Datta, and Patel, 1999). Putable is an

indicator variable that takes the value 1 if the bond is putable, and 0 otherwise. Putable bonds

minimize the downside risk to bondholders by allowing them to sell the issue back to the

company at a predetermined price. We therefore expect a negative association between bond

yields and Putable. Sinkingfund is an indicator variable that takes the value 1 if a sinking

fund exists, and 0 otherwise. Dyl and Joehnk (1979) and Boardman and McEnally (1981)

have shown that yields on bonds with sinking fund provisions are significantly lower.

However, the establishment of complex sinking fund agreements has been shown to be an

indicator of issuers’ high level of riskiness (Smith and Warner, 1979; Ziebart and Reiter,

1992).

Table 2 provides descriptive statistics for the bond-specific characteristics. The average

rating of the bonds in our sample is 8.2, which is equivalent to a Standard and Poor’s “BBB”

rating. Sample bonds have, on average, a time until maturity of about 12 years, and a face

value of US$192 million. About 4% of the sample bonds are subordinated, 53% of bonds are

21

callable, 2% are putable, and 3% have a sinking fund provision in place. These averages are

similar to the characteristics of the average bond in Mergent suggesting that our filters pick a

relatively representative sample of bonds.

We further control for several firm-specific characteristics that are measured in the fiscal

year immediately prior to a given bond’s issuance. We use Market to book, as measured by

the firm’s market-to-book ratio at the end of the fiscal year prior to the bond issuance, to

capture firm growth opportunities. If high-growth firms pursue high risk activities (e.g.,

Bhojraj and Sengupta, 2003), the firm’s market-to-book ratio should be positively associated

with its cost of debt. On the other hand, Fama and French (1995) argue that high market-to-

book ratios can signal sustained earnings performance, thus the association with the bond

spreads could be negative. Return on asset is pretax income before extraordinary items,

scaled by total assets at the end of the fiscal year prior to the bond issuance; it is included in

our models to control for profitability, and is expected to be negatively associated with the

cost of debt financing, since profitable firms are less likely to default. Leverage is the sum of

the firm’s debt in current liabilities and long-term liabilities, scaled by total assets at the end

of the fiscal year prior to bond issuance. The higher the leverage ratio is, the heavier the

firm’s financial burden is suggesting that firm leverage is positively related to the firm’s cost

of debt. Log(Assets) is the natural logarithm of firm’s total assets at the end of the fiscal year

prior to the bond issuance. Larger firms should obtain more favorable debt terms, given their

stable cash flows and larger tangible asset base. We therefore expect a negative association

between Log(Assets) and the cost of debt financing. Finally, we include the coefficient of

variation of the firm’s net operating cash flows (scaled by total assets) calculated over the

five years prior to the bond issuance, CV(Cash Flows). Since high cash flow volatility is

associated with a higher risk of default (e.g., Minton and Schrand, 1999), we expect a

positive association between CV(Cash Flows) and the cost of debt financing.

22

Finally, we also control for firm characteristics that prior literature suggests are

correlated with our tax avoidance measures to make sure that our results are incremental to

these factors that might drive fundamental differences in our sample firms (e.g., Mills, 1998;

Manzon and Plesko, 2002; Rego, 2003; Dyreng et al., 2008, Frank et al., 2009). Loss carry

forward is an indicator variable taking the value of 1 if loss carry forward is positive and 0

otherwise while Change in loss carry forward is change in the loss carry forward scaled by

lagged assets. Loss carry forwards could be used to reduce future tax payments and can be

positively viewed by debtholders. Foreign income is foreign income scaled by lagged assets.

We expect firms with sizable foreign operations to be more geographically diversified and

pay lower bond offering yields (Franco et al., 2012). PPE is property, plant, and equipment

scaled by lagged assets. PPE could be used as collateral in borrowing agreements reducing

yields, and hence we expect a negative coefficient on PPE. Intangible assets is intangible

assets scaled by lagged assets. Similarly, intangible assets could also be used as collateral in

borrowing agreements (e.g., Loumioti, 2012) resulting in a negative relationship with bond

offering yields. Equity income is income in earnings from investments accounted for under

the equity method scaled by lagged assets. Firms with high equity income are more likely to

be diversified and thus likely pay lower yields at the time of bond issuance.

Information quality is our composite measure of information quality. Prior research

(Frank et al., 2009; Balakrishnan et al., 2012) documents that tax planning results in less

transparent financial reporting and information environments. We construct a composite

measure of Information quality using the following seven financial reporting / information

quality proxies: 20 a) the ratio of annual research and development expense (coded as 0 if

missing) to sales averaged over the last five years. R&D expense is used by prior research to

proxy for the presence of intangible assets, which are associated with higher information 20 We obtain qualitatively similar results when we control for information quality proxies individually in separate regressions. Also, our results are similar if we control for different combinations of information quality proxies rather than combining all seven of them.

23

asymmetry (Barth and Kasznik, 1999; Barth, Kasznik, and McNichols, 2001). b) the accrual

quality measure calculated as the standard deviation of residuals over the last five years from

an industry-year level Dechow and Dichev (2002) model augmented with fundamental

variables from the Jones model (McNichols, 2002). c) the performance adjusted discretionary

accruals calculated from the Jones Model averaged over the last five years (Kothari et al.,

2005). d) the absolute analyst forecast error calculated as the absolute value of the difference

between actual reported earnings and the latest IBES median consensus analyst forecast

(reported immediately before the earnings announcement) scaled by the absolute value of the

latest IBES median consensus analyst forecast. To be consistent with other information

quality proxies we average AFE over the last five years. e) the analyst forecast dispersion

calculated as standard deviation of the forecasts included in the latest IBES consensus

forecast scaled by the absolute value of the latest IBES median consensus forecast and

averaged over the last five years. f) the number of forecasts included in the latest IBES

consensus analyst forecast and averaged over the last five years. We multiply this measure

with -1 so that it captures a less transparent information environment. g) the average monthly

bid – ask spread scaled by the average of the absolute value of bid and ask prices and

calculated over the last 60 months (five years). We rank each of the seven information quality

proxies into deciles annually and standardize these deciles to be between 0 (high information

quality) and 1 (low information quality). Information quality is the average of these seven

standardized ranks. We expect Information quality to result in higher borrowing costs.21

Including the information quality measure reduces the ability of tax avoidance to influence

bond yields through the information opacity channel.

All models include year fixed-effects to capture structural changes in the bond market’s

21 Our sample consists of bonds issued by large firms (average firm size is about $11.5 billion). On the other hand, previous research examining the impact of tax avoidance on bank loans (Kim et al., 2010) and interest expense (Lisowsky et al., 2011) deal with smaller firms. Average firm size in Kim et al. (Lisowsky et al., 2011) is $915 million ($111 million). Therefore, compared to these studies, we expect that the impact of Information quality in our tests to be less pronounced.

24

liquidity as well as general debt market conditions over time. We also include industry fixed

effects (defined per Fama and French 48 industry definitions) to mitigate industry related

time-invariant factors which might drive our results.

The bottom part of Table 2 presents descriptive statistics on the firm-specific

characteristics for our sample. The average bond issuer in our sample has a market-to-book

ratio of 3.18, a return on assets of 10.3%, and leverage of about 41%.

4. Empirical findings

4.1. Main results

In Table 3, we present our empirical analyses of the net effects of tax avoidance on the

cost of public debt financing. The table reports coefficient estimates from OLS regression

models together with t-statistics (in parentheses). To control for autocorrelation in the errors,

we compute standard errors clustered at the firm level. The explanatory power of our model

(adjusted R2) is relatively high at 78% suggesting that the variables included are important

drivers of the bond offering yields. We find a significant and negative association between

our proxies of effective tax rates and the bond offering yields, with a coefficient varying from

−0.435 (t-statistic = −2.67) to −0.247 (t-statistic = −2.99). In terms of economic significance,

going from the 90th percentile to the 10th percentile of CTA's distribution increases the bond

offering yields by 15 basis points. Although the economic magnitude this effect seems small,

we investigate the impact of factors that are potentially associated with a larger economic

impact in additional analyses. Overall, these results are consistent with the hypothesis that

corporate bondholders view corporate tax avoidance activities negatively and, as a result,

they increase the offering bond yields.

Results on our control variables are consistent with our expectations. We find that the

coefficient on the sinking fund provision indicator is negative suggesting that the

establishment of a sinking fund lowers the lenders' risk. We also document that the

25

coefficient on market-to-book ratio is negative supporting Fama and French (1995)’s

argument that high market-to-book ratios can signal sustained earnings performance. Lastly,

we find that, consistent with prior findings (e.g., Francis et al., 2005; Bharath et al., 2008),

the coefficient on the composite information quality proxy is positive and significant.

4.2. Robustness tests

In this section, we investigate the robustness of our main results to the endogeneity of

tax avoidance activities and to an alternative dependent variable that captures the probability

of default. We also run an event study methodology which allows us to make causal

inferences.

4.2.1. Endogeneity

One might argue that corporate tax avoidance is endogenous because of a correlated

omitted variable which influences both tax avoidance and the cost of debt. Thus, as a

robustness test, we use tax avoidance proxies that are measured in the first year when this

computation is possible. For example we calculate CTA in year 1987 for a particular firm and

use it for all bonds issued in any year after 1987 by the same firm. Thus there is no time

variation in tax avoidance proxies within the same firm. Dittmar and Mahrt-Smith (2007)

adopt a similar approach when testing the impact of corporate governance on firm value and

argue that it is appropriate when the potentially endogenous variable of interest changes over

time very slowly. Over our sample period, the autocorrelation in the tax avoidance measures

is between 82% and 88% suggesting that indeed the tax avoidance measures are quite sticky.

The results reported in Panel A of Table 4 show that our main result is robust to endogeneity:

when we use tax avoidance proxies calculated many years before the bond issuance, we

continue to find that tax avoidance results in higher bond offering yields.

4.2.2. The impact of tax avoidance on expected default frequency

26

As an alternative to bond offering yields, we use monthly expected default

frequencies (EDFs) provided by Moody’s/KMV.22 Moody’s has preferential access to private

information about borrowers when issuing ratings and uses sophisticated information

processing methodologies, relative to the marginal bond investor. Therefore, the EDFs are

less likely to reflect issues with the information quality of firm’s public reports. We estimate

the following model to check robustness of our main results:

, ∝ ∝ , ∝ ,

∝ ∝ , (2)

where EDF is the expected default frequency calculated on the month earnings are

announced. Our results are reported in Panel B of Table 4. Consistent with Table 3, we find

that the coefficients on all tax avoidance proxies are negative and significant; more tax

avoidance is associated with a greater expected probability of default. An increase in tax

avoidance as measured by CTA measure from the 90th percentile to the 10th percentile of its

sample distribution increases EDF by 0.11%. This number is economically large given that

average EDF in our sample is 0.58%. The strong association suggests that Moody's is likely

to be concerned about the long term implications of corporate tax avoidance activities on the

uncertainty of future cash flows. This concern is reflected through assigning a higher

estimated expected default frequency.

4.2.3. CDS spread changes around tax shelter announcements

In this sub-section, we test the effect of tax avoidance on the cost of public debt by

looking at Credit Default Swap (CDS) market reactions to announcements of tax shelters (see

22 Moody’s estimates the asset values and volatilities using information from stock prices and financial statements. This measure of the distance to default is empirically mapped to a large set of corporate default data (e.g., Crosbie and Bohn, 2003). The main advantage of using EDFs, as opposed to bond spreads, is that they are not affected by illiquidity and we do not have to control for bond contractual features (e.g., covenants, seniority, etc).

27

Hanlon and Slemrod, 2009).23 We use CDS data from Markit because these default spreads

are theoretically linked to bond spreads and form the basis of pricing bonds in the secondary

market. Moreover, CDS data is available daily allowing us to perform an event study. CDS

spreads are less affected by liquidity problems, changes in interest rates, tax issues and

contract design features that are specific to bond securities. Most importantly, prior research

suggests that CDS spreads incorporate information faster than equity markets because dealers

in this market enjoy lower information asymmetry due their access to private information

(Acharya and Johnson, 2007; Norden and Weber, 2004). Thus we expect changes in CDS

spreads to reflect updates in the expectations about future cash flows as opposed to changes

in the information quality triggered by corporate tax avoidance activities.

We compute ∆Raw CDS Spread as the percentage change in 5-year CDS spread

around the tax shelter announcement date over a five-day window ([−2, 2]). We then compute

∆Abnormal CDS Spread which is the difference between raw and market CDS spread

changes (the change in spreads of the same credit rating group during the same five-day

window). The sample of Hanlon and Slemrod (2009) has 112 tax shelter announcements

between 1990 and 2004. However, because the Markit CDS database coverage starts in year

2001, we end up with only 20 announcements between 2002 and 2004. Although this sample

size is small, the event study provides clean evidence on how creditors view announcements

of serious tax avoidance activities.

We present results of this event study analysis in Panel C of Table 4. We find that the

average (median) market-adjusted CDS spreads increase by 3.84% (2.19%) around tax

shelter announcements. These changes are economically significant given that average

(median) 5-year CDS spread in our sample is 1.94% (0.74%). The positive and statistically

significant changes in market-adjusted CDS spreads suggest that debtholders respond 23 CDSs are in essence insurance contracts that provide buyer protection against losses arising from borrower-defaults. In a typical CDS contract the buyer pays to the seller a periodic fee (i.e., the CDS spread) to insure against default of any debt security issued by a third party, called the reference entity.

28

negatively to tax shelter announcements. Moreover, the evidence highlights that tax

avoidance activities cause greater credit spreads and the reaction is triggered by updated

expectations about lower and more uncertain future cash flows.

4.3. The impact of tax avoidance on future cash flow level and volatility

We further examine the potential reason for why tax avoidance increases cost of public

debt. As we have discussed earlier, corporate tax avoidance activities could make future cash

flows more uncertain due to tax risk or by facilitating managerial rent extraction. We test

directly the impact of corporate tax avoidance on future cash flows by estimating the

following regression:

, ,

∝ ∝ , ∝ ,

∝ ∝ ,

(3)

The dependent variable in equation (3) is either Cash flow level, defined as the average

of cash flow from operations scaled by total assets over the next five years, or Cash flow

volatility, defined as the coefficient of variation of cash flow from operations scaled by total

assets over the next five years.

We report the results of estimating equation (3) in Table 5. The dependent variable in

columns 1-3 is Cash flow level. Consistent with the conjecture that tax avoidance increases

uncertainty in future cash flow levels, we find that tax avoidance is negatively and

significantly related to the level of future cash flows from operations. An increase in tax

avoidance, as measured by CTA measure, from the 90th percentile to the 10th percentile of its

sample distribution decreases future cash flow levels by 0.7%; an economically large effect

given that the average cash flow level in our sample is 11.1%. The dependent variable in

columns 4-6 is Cash flow volatility. We find significant and positive coefficients on our tax

avoidance proxies suggesting that tax avoidance increases also the future cash flow volatility.

29

Moreover, an increase in tax avoidance as measured by CTA from the 90th percentile to the

10th percentile of its sample distribution increases Cash flow volatility by 0.218. This number

is economically significant given that the average Cash flow volatility in our sample is 1.019.

The ability of the tax avoidance measures to predict future lower cash flow levels and higher

volatility indicates that corporate tax avoidance activities are associated with significant tax

risks and managerial rent extraction that are detrimental to bondholders' wealth. These results

suggest that bond investors see tax avoidance behaviour as an early indicator of problems in

the future cash flow level and volatility, two variables that are first order determinants of a

firm's cost of debt financing.

4.4. Path Analysis

In the prior section we document that corporate tax avoidance activities potentially

increase the uncertainty about the magnitude and volatility of the firms' future cash flows.

This analysis suggests a relationship between tax avoidance and cost of public debt through

future cash flows levels and volatility channels but it is silent on the importance of these

channels. In particular, we cannot conclude whether the relationship between tax avoidance

and the cost of bond debt is completely explained by the impact on future cash flow levels

and volatility given that tax avoidance could also affect bond yields through its impact on

future information quality. We perform a path analysis in this section to shed more light on

this issue. 24

Path analysis is a structural equation model used to decompose the correlation between

two variables into a direct path and an indirect path through a mediating variable. In our

paper, the path analysis decomposes the relationship between tax avoidance and the cost of

public debt into a direct path between these two variables and an indirect path through the

24 A path analysis is used to answer how a variable (corporate tax avoidance in our case) affects another variable (i.e., bond yields). The impact is through a third mediating variable. In contrast, an interaction analysis is used to answer when a variable impacts another variable. This is usually the case when a third variable, the moderating variable, is high or low. Baron and Kenny (1986) provide a discussion on mediation versus moderation.

30

cash flows level or volatility. We employ a recursive (all paths flow in only one direction)

path model with observable variables. A direct path includes only one path coefficient while

an indirect path includes a path coefficient between the source variable and the mediating

variable (in our paper, it is the path between tax avoidance and the cash flows level or

volatility) and a path between the mediating variable and the outcome variable (in our paper,

it is the path between the cash flows level or volatility and the cost of public debt). The total

magnitude of the indirect path is the product of these two path coefficients. The analysis

automatically standardizes all variables in the model with a mean of zero and a standard

deviation of one allowing a comparison between direct and indirect path coefficients. We

estimate the following model:

,

∝ ∝ ,

∝ , ,

∝ , ∝ ,

∝ ∝ ,

(4)

, ,

, , (5)

In this model, the path coefficient ∝ is the magnitude of the direct path from tax

avoidance to the cost of public debt. On the other hand, the path coefficient ∝ * is the

magnitude of the indirect path from tax avoidance to the cost of debt mediated through the

cash flow level or volatility. We report the path coefficients of interest in Table 6.25 Panel A

(Panel B) of Table 6 reports path coefficients when we use the cash flow level (cash flow

volatility) as the mediating factor. Panel A shows that the direct path between tax avoidance 25 All models have a Bentler’s comparative fit index (CFI) greater than 0.9 suggesting that they have a good fit.

31

and cost of debt is negative and statistically significant for all three measures of tax

avoidance. A path coefficient of -0.039 on CTA indicates that a one standard deviation

decrease in CTA increases the bond offering yield by 0.039 times the standard deviation of

the bond offering yield. The path coefficient between tax avoidance and the cash flow level is

positive and significant suggesting that higher tax avoidance results in a lower future cash

flow level (consistent with Table 5). Moreover the path coefficient between the cash flow

level and the offering yield is negative and significant. The total mediated path (product of

the path coefficient between tax avoidance and cash flow level and the path coefficient

between cash flow level and offering yield) is negative for all three proxies of tax avoidance.

In terms of economic magnitude, a one standard deviation decrease in CTA increases bond

offering yields by 0.019 times the standard deviation of bond offering yields through CTA’s

impact on the future cash flows level. This economic magnitude is about half of the direct

impact of CTA on the bond offering yields and about a third of the total impact of CTA on the

bond offering yields (the total effect is the sum of the direct and the indirect effect).26

We also examine the role of future cash flow volatility as a mediating factor on the

relationship between tax avoidance and bond offering yields in Panel B of Table 6.

Consistent with Panel A, the direct path between tax avoidance and bond offering yields is

negative and significant for all three proxies of tax avoidance. When we look at components

of the indirect path, the path between tax avoidance proxies and cash flow volatility is

negative and statistically significant (except for ETR5) while the path between cash flow

volatility and the bond offering yield is positive and significant. However the total magnitude

of the mediated path when we use cash flow volatility as a mediating factor is quite small.

For example, the magnitude of the total mediated path coefficient is -0.005 when we use CTA

as our tax avoidance measure. This result suggests that a one standard deviation decrease in

26 The total effect is not comparable with the effect we show in Table 3 because the variables used in the path analysis are standardized.

32

CTA increases bond offering yields only 0.005 times the standard deviation of bond offering

yield.27 In unreported analyses, we also employed information quality separately as a

mediating factor. We find that the maximum magnitude of mediated path for Information

Quality is 0.005 suggesting that it is not a very important mediating factor.

Overall, the path analysis results indicate that there is a statistically significant direct

path between tax avoidance and bond offering yields regardless of the mediating factor we

employ. We also find that future cash flow uncertainty is a more economically important

mediating factor than the information quality in explaining the relationship between tax

avoidance and bond offering yields.

4.5 Bond ownership

We further analyze the impact of corporate tax avoidance on bond yields from a

supply-side perspective. In particular, we examine whether long term investors in the bond

market take into account the long term effect of corporate tax avoidance when making

investment decisions. We focus on the bond ownership of insurance firms, the largest

investors in the bond market that typically follow a buy and hold investment strategy. We test

whether firms which engage in corporate tax avoidance attract lower bond investments from

insurance companies using the following model:

, ,

∝ ∝ , ∝ ,

∝ , ∝

∝ ,

(6)

Equation (6) mirrors equation (1) except we use Percentage of bonds owned (annual

average of the quarterly percentage of bonds owned by insurance firms) or Number of

bondholders (annual average of the quarterly number of insurance firms) as dependent

27 We did not employ both cash flow level and volatility at the same time as mediating variables due to their high correlation (Pearson correlation is 50% in our sample).

33

variables. We obtain bonds holdings information from the National Association of Insurance

Commissioners (NAIC) starting with year 2001 and match this data with bond specific data

in the Mergent Fixed Income Securities Database (FISD). This dataset allows us to compute

the percentage of ownership and number of bondholders by insurance firms in a particular

bond throughout its life. In our sample, this group of investors holds, on average, 20% of the

par value. The remaining variables in equation (6) are defined in Section 3.3.

We report the results of estimating equation (6) in Table 7. We find that bond

ownership of insurance firms is negatively associated with corporate tax avoidance

suggesting that they are less likely to invest in bonds of firms which avoid paying taxes. The

coefficient estimates indicate that going from the 90th percentile to the 10th percentile of the

CTA distribution decreases the average bond ownership by insurance firms by 4%. This effect

is economically meaningful given that the average bond ownership in our sample is 20%. We

also document a significant reduction in the number of insurance firm bondholders as tax

avoidance increases. In terms of economic significance, going from the 90th percentile to the

10th percentile of CTA distribution decreases the number of bondholders by 1.3. This effect is

large given that the average number of insurance firm bondholders in our sample is 10.

This evidence indicates that long term investors such as insurance firms are reluctant to

own bond of firms with high tax avoidance, potentially due the long term impact on future

cash flows of tax activities. Thus insurance companies view tax avoidance activities as an

early signal of decreases in future credit performance that can trigger an expensive portfolio

rebalancing due to capital regulation requirements.

4.6. Cross-sectional analyses

In the previous set of analyses, we have shown that corporate tax avoidance activities

are negatively associated with bond offering yields mainly due to the negative consequences

of these activities on future cash flows. In this section, we investigate directly whether the

34

negative association is a function of ex ante proxies for rent extraction and tax risk.

Specifically, we partition our sample based on several variables that capture incentives for

debtholder wealth expropriation (poor corporate governance, more concentrated equity

ownership, high risk-taking incentives for management and high credit risk) and tax risk (the

probability of an IRS audit).

4.6.1. Corporate takeover market

We use Gompers, Ishii and Metrick’s (2003) G-Index as our proxy for poor corporate

governance since it provides an indication of the extent to which the management of the

company is protected from the corporate takeover market. We split the sample into two

groups according to the median G-Index every year. Observations which have higher (lower)

than median G-Index scores are characterized by lower (greater) management monitoring by

the takeover market. We estimate the empirical specification in Equation (1) separately for

high and low G-Index sub-samples.28 Panel A of Table 8 reports regression results for the

high and low governance quality sub-samples. We find no evidence of an association

between our proxies of tax avoidance and bond offering yields in the high monitoring (high

governance) group. However, we note that our results in Table 3 are generally driven by the

low monitoring group. The coefficient estimates indicate that going from the 90th percentile

to the 10th percentile of the CTA distribution increases the bond offering yields by 37 basis

points. We conclude that tax avoidance negatively impacts the cost of public debt for firms

characterized by poor management monitoring; these firms are more likely to expropriate

wealth from bondholders and report lower future cash flows.

4.6.2. Ownership concentration

We investigate the impact of ownership concentration on our results by splitting the