cost allocation sponsored by: california association for coordinated transportation presented by...

TRANSCRIPT

Cost Allocation

Sponsored by:

California Association for Coordinated Transportation

Presented by

Rich Garrity, Senior AssociateRLS & Associates, Inc.

September 23-24, 2008Sacramento, CA

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 2 of 175

Session Objectives1. Develop a Standard Approach to “Cost Allocation”1. Develop a Standard Approach to “Cost Allocation”

2. Identify Special Issues in Cost Allocation 2. Identify Special Issues in Cost Allocation

3. Build a Cost Allocation Model3. Build a Cost Allocation Model

4. Understand the Difference Between Cost and Price 4. Understand the Difference Between Cost and Price

5. Automating the Cost Allocation Process5. Automating the Cost Allocation Process

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 3 of 175

Target Audience

This Session is Designed for: Organizations That Need an Approach to

Cost Individuals Service Components Transit Organizations that Provide

Service Under a Purchase of Service Arrangement to Other Users/Groups

Multi-Purpose Human Service Agencies Supported by Multiple Federal Grants

Defining a Standardized Approach to Cost Allocation IssuesModule 1

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 5 of 175

Issues in Cost Allocation

The Term “Cost Allocation” Has Been Used to Describe a Wide Range of Allocation Needs Among Public Transit Operators

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 6 of 175

Issues in Cost Allocation

In Transit, “Cost Allocation” Can Refer to a Series of Distinct Management/Accounting Practices

Each Cost Allocation Problem Requires a Separate Methodology, Typically Referred to As “Cost Allocation”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 7 of 175

Types of Cost Allocation

Financial Based Cost Allocation

Service Based Cost Allocation Plans

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 8 of 175

Financial Based Cost Allocation

Central Service Cost Allocation Plans

Indirect Cost Allocation Plans

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 9 of 175

Financial Based Cost Allocation #1

Central Services Cost Allocation Plan A Publicly Sponsored Transit Program

Benefits from the Services of Other Governmental Units and Desires to Claim Costs Incurred by these Units Under its Various Federal Awards

The Public Entity or Governmental Unit Must Prepare a “Central Services Cost Allocation Plan”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 10 of 175

Financial Based Cost Allocation #2 Indirect Cost Allocation Plan

An Entity (Public or Private Nonprofit) Provides Multiple Program Services

Certain Overhead and Administrative Costs Incurred by the Entity Benefit All Programs and Services, Including Transit

The Agency Seeks to Recoup These Costs in Their Billings to Various Federal Agencies

The Entity Requires an Approved “Indirect Cost Allocation Rate” in Order for Such Costs to be Reimbursable by the Federal Government

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 11 of 175

Service Based Cost Allocation

Allocate Costs to Various Types/Modes/Services

Urban/Rural Cost Allocation Required by FTA

Charter Cost Allocation Local Match Allocation Plan

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 12 of 175

Service Based Cost Allocation #1

Service Based Cost Allocation A Public Transit Agency Coordinates

Service With Various Human Service Agencies In The Area

The Transit Provider Has A Policy That Public Transit Funds Cannot Be Used To Subsidize Human Service Agency Client Transportation

The Transit Agency Needs A “Fully Allocated Cost Analysis” To Determine How To Price Contract Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 13 of 175

Service Based Cost Allocation #2

Service Based Cost Allocation A Transit Agency Receives Funding Under

Both FTA Section 5307 And Section 5111 FTA Expects the Grantee to Develop a

Reasonable Basis for Allocating Operating Costs Between the Two Funding Sources that is Related to the Service Provided

FTA Requires a “Grant Allocation Plan” to Distribute Costs to the Two Different, But Related Programs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 14 of 175

Service Based Cost Allocation #3

Service Based Cost Allocation A Transit Agency Provides Charter

Service in Accordance with 49 CFR part 604

The Transit Agency Must Demonstrate That it Fully Recovers the Cost of Charter Service

The Agency Requires a “Charter Service Allocation Plan”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 15 of 175

Service Based Cost Allocation #4

Service Based Cost Allocation A Regional Transit Authority Provides

Service Over a Multi-Jurisdictional Service Area

Each Participating Local Entity Must Share Responsibility for Funding a Portion of the Local Share

The Authority Must Allocate Local Funding Needs In An Equitable Manner To All Participating Jurisdictions

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 16 of 175

Multiple Cost Allocation Needs

Some Public Transportation Projects May Require Multiple Types of Cost Allocation

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 17 of 175

Multiple Cost Allocation Needs

Municipal or County Government

Central Service Departments

Central Service Departments Operating Departments

Individual Operating Departments

Public Works & Transit

Central Service Cost Allocation Plan

Allocable Portion of Central Service Costs

Departmental Administration

Approved Indriect Cost Rate Approved Indriect Cost Rate

Allocable Portion of Departmental Indirect Costs

Allocable Portion of Departmental Indirect CostsTransit Public Works

Management

Transit Direct Costs:Shared Functions

Dispatch

Allocated on Basis of Service Units

Allocable Portion of

Transit Direct Costs:Direct Functions

Operations Maintenance

Fixed Route JARC Demand Response

Modes

Transit Management Costs (Fixed Costs)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 18 of 175

Multiple Cost Allocation Needs

Nonprofit Organization

Direct Expenses

Home Care TransportationCongregate Meals

Indirect Expenses

Approved Indirect Cost Rate

Allocable Portion of Indirect Costs

Management

Transit Direct Costs:Shared Functions

Dispatch

Allocated on Basis ofService Units

Allocable Portion of

Transit Direct Costs:Direct Functions

Operations Maintenance

Medicaid Contract Transit

Rural Public Transit

Title III Client Transit

Services

Transit Management Costs (Fixed Costs)

Embracing the Concept of Full Cost Identification Module 2

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 20 of 175

Why Full Cost Identification?

Our Goal - To Answer the Questions: How Much Does the Transportation

Service Cost? How are We Going to Pay For It?

In Order to Achieve These Goals, Agency and Program Managers Must Use Financial Planning

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 21 of 175

Why Full Cost Identification?

Assess Performance Measure Progress Toward the

Achievement of Goals and Objectives

Consider Actions Which May Change the Course of Future Events

Modify Policies, Procedures, and Processes

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 22 of 175

Why Full Cost Identification?

Make Operational Changes, Including Those Leading To: Service Expansion, Reduction, Or

Cessation Increases Or Decreases In Services,

Revenues, And Staff Changes Or Modifications In

Procedures Or Other Activities (Such As Marketing Or Public Relations)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 23 of 175

Why Full Cost Identification?

Transportation Systems Need Complete and Accurate Financial Data in Order to: Manage the System So That its

Goals and Objectives are Met Efficiently

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 24 of 175

Why Full Cost Identification?

Know the True Cost of Operating the System so that Costs May be Billed or Allocated Appropriately to the System's Users

Report to the Funding Sources or Purchasing Agencies How Money was Spent, What Revenues were Realized, and the Financial Status of the Organization

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 25 of 175

Issues in Full Cost Accounting

Lack of Sufficient Account Detail In Organizational Accounting Systems

Failure to Capture and/or Allocate Agency Indirect or Overhead Costs

There Is A Lack Of Common Definitions For Accounts (Non-FTA Programs)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 26 of 175

Issues in Full Cost Accounting

Lack of Common Definition of Service

Failure to Capture Service Unit Data

Blended Program Expenditures Use of Capitated Payments

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 27 of 175

Financial Planning:Why is This Important?

Planning for Change Changes We

Institute Changes

Forced Upon Us

Political Climate

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 28 of 175

Financial Planning:Why is This Important?

Consider the Example: A Manufacturer Produces Two

Consumer Products What are Some of the Costs That

Will Be Incurred by this Company?

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 29 of 175

Exercise No. 1

Exercise No. 1 - Take a Minute or Two to Jot Your Ideas Down on Paper

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 30 of 175

Identifying Transportation Costs Now Consider ….

Since the Ingredients Used are Basically the Same as Product 2, the Product 1 Manager Opts to Include them all In Product 2 and Does Not Include Them in Calculating His Cost

Since Product 1 is Delivered on the Same Trucks as Product 2, the Product 1 Manager Does Not Include Them in Calculating His Cost

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 31 of 175

Identifying Transportation Costs

Product 1 Research,

Development, & Testing

Purchase of Ingredients

Production Quality Control Distribution Marketing Profit

Product 2 Research,

Development, & Testing

Purchase of Ingredients

Production Quality Control Distribution Marketing Profit

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 32 of 175

Identifying Transportation Costs Do You Disagree with this

Approach? Strongly Disagree Disagree Not Sure Agree Strongly Agree

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 33 of 175

Identifying Transportation Costs What is this Product Line

Manager Doing Wrong? ? ? ?

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 34 of 175

Identifying Transportation Costs Let’s Talk About a Transportation

Related Situation What About this Example?

A Transportation Provider Reports Their Transportation Expenses as Follows: Fuel Maintenance Insurance

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 35 of 175

Identifying Transportation Costs Financial Planning Begins by

Establishing (or Reaffirming) Overall Strategies and Goals Mission Statement

WHAT Will the Transit Service Do? HOW Will the System Operate?

This Starts the Financial Planning Process

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 36 of 175

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 37 of 175

Identifying Transportation Costs Cost Analysis is a Key Element

of Financial Planning Knowing the Costs of Individual

Routes or Services is Useful for Your Management Purposes and for Billing Your Client Agencies

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 38 of 175

Identifying Transportation Costs The Basic Approach

Recommended and Used by Successful Business Operations and Transportation Systems is Called “Full Cost Accounting”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 39 of 175

Identifying Transportation Costs

To Use this Approach Requires an Understanding of Basic Cost Concepts and the Use of a Consistent Costing Method

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 40 of 175

Identifying Transportation Costs Using “Full Cost Accounting”

Means that the Total Costs of Providing Transportation Services are Considered

Total Costs Include Any Commitment or Use of Time, Money, Physical Resources, and Other Assets of the Agency in the Delivery of Transportation Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 41 of 175

Identifying Transportation Costs

In Full Cost Accounting, a Value is Given to These Commitments Whether or Not They Result in Immediate Out-of-Pocket Expenditures

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 42 of 175

Identifying Transportation Costs Full Cost Accounting Will:

Assist the Manager in Understanding the TRUE Cost of Providing Service

Determine Needed Revenues -- Immediate and Long-Term

Allow Allocation of Costs to System Users

Compare Costs of Service with Other Systems (Peer Analysis)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 43 of 175

Identifying Transportation Costs Full Cost Accounting Will

Assist in Making Decisions to Participate in a Coordinated Services Program

Recognize Value of Donations (Time, Materials, and Supplies)

Permit Accurate Financial and Performance Monitoring/Evaluation

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 44 of 175

Identifying Transportation Costs Analyze the Various Functions

and Activities that Your Transportation Program Carries Out on a Day-to-Day Basis

Management’s Responsibility is to Identify All Activities That Your Agency Performs in the Delivery of Transportation Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 45 of 175

Identifying Transportation Costs Understand HOW the Activity

Creates Costs for the Transportation Program Your Transit Program DOES

Something Your Transit Program BUYS

Something Use a Functional Approach to

Cost Recognition

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 46 of 175

Identifying Transportation Costs Functional Areas of Transportation:

Operations Maintenance Non-Vehicle Maintenance General Administration

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 47 of 175

Identifying Transportation Costs The Agency’s Chart of Accounts

is the Basic Tool Used to Ensure that All Transportation Costs are Reflected in the Agency’s Accounting System

Issues in Cost Allocation

Module 3

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 49 of 175

Special Issues in Cost Allocation

Direct and Indirect Costs

Operating and Capital Costs

Fixed and Variable Costs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 50 of 175

Direct and Indirect Costs

Direct Costs Those Expenses Incurred by the Grantee

That Are Directly Related and Strictly Benefit Only the Public Transportation Program

Generic Examples: Compensation of Employees for the Time

Devoted and Identified Specifically to the Performance of the Grant

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 51 of 175

Direct and Indirect Costs Direct Costs

Generic Examples: Cost of Materials Acquired, Consumed, or

Expended Specifically for the Purpose of Providing Public Transit Service

Equipment and Other Approved Capital Expenditures

Travel Expenses Incurred Specifically to Carry Out the Award

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 52 of 175

Direct and Indirect Costs Direct Costs

Transit Examples: 501.01 – Operator's Salaries & Wages 501.03 – Dispatcher's Salaries & Wages 503.05 – Contract Vehicle Maintenance 504.01 – Fuel & Lubricants Consumed 504.02 – Tires and Tubes Consumed 508.00 – Purchased Transportation

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 53 of 175

Direct and Indirect Costs Indirect Costs

Generic Examples Certain Central Service Costs General Administration of the Organization Accounting and Personnel Services Performed

Within the Organization the Delivers Public Transit Services

Costs of Operating and Maintaining Facilities

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 54 of 175

Direct and Indirect Costs

Indirect Costs Transit Examples

501.04 – Administrative Salaries & Wages

512.12 – Other Administrative Facilities

505.02 – Telephone

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 55 of 175

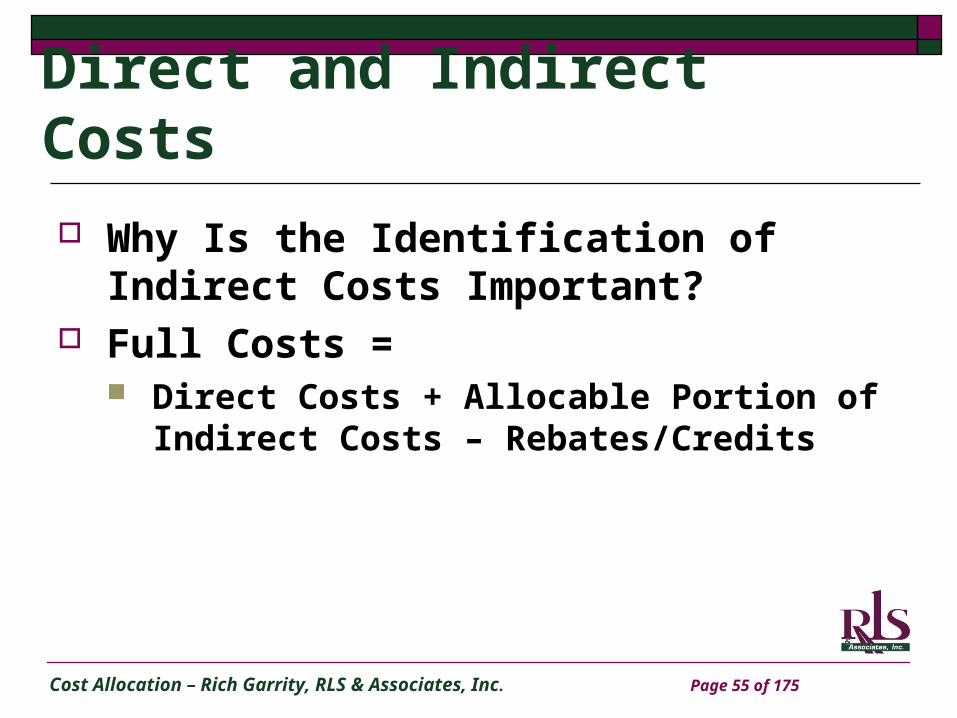

Direct and Indirect Costs Why Is the Identification of

Indirect Costs Important? Full Costs =

Direct Costs + Allocable Portion of Indirect Costs – Rebates/Credits

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 56 of 175

Direct and Indirect Costs Will All Transit Agencies Incur

Indirect Costs? No

Independent Transit Authorities Other Units That Do Not Rely on

Central Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 57 of 175

Direct and Indirect Costs How Can We Tell if We Need An

Indirect Cost Allocation Plan? If a Transit System Incurs Costs That Are: Accumulated in the Accounts of Another

Department or Division of the Organizations

Incurred by Nonprofit Agency Management That Benefits Multiple Programs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 58 of 175

Direct and Indirect Costs

Indirect Costs Must Be Allocated in a Manner Consistent with Procedures Set Forth in OMB Circulars A-87 or A-122

Facility Expenses

Transportation

Meals

Vocational Services

Homemaker Services

FunctionExpense

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 59 of 175

Direct and Indirect Costs How are Indirect Costs Claimed

Under Federal Awards? OMB Circular A-87, Attachment A,

“General Principles for Determining Allowable Costs,” paragraph C3(d) states:

Where an accumulation of indirect costs will ultimately result in charges to a Federal award, a cost allocation plan will be required

OMB Circular A-122 contains similar language

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 60 of 175

Indirect Cost Allocation

You MUST Have An Indirect Cost Allocation Plan or Indirect Cost Rate in Order to Claim Reimbursement Under Federal Awards

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 61 of 175

Indirect Cost Allocation

Indirect Cost Rate Proposals or Cost Allocation Plans Must Either: Be Submitted to a Federal Cognizant

Agency; or Be Maintained on File by the

Governmental Unit Similar Rules Apply to Nonprofits

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 62 of 175

Indirect Cost Allocation

"Cognizant Agency" Means the Federal Agency Responsible for Reviewing, Negotiating, and Approving Cost Allocation Plans or Indirect Cost Proposals Developed on Behalf of All Federal Agencies

OMB Publishes a Listing of Cognizant Agencies

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 63 of 175

Indirect Cost Allocation

Negotiation and Approval of Rates Generally, the Federal Agency with the

Largest Dollar Value of Awards to the Nonprofit Organization Will be Designated as the Cognizant Agency for the Negotiation and Approval of the Indirect Cost Rates

The Designation Is Not Changed Unless There is a Major Long-Term Shift in the Dollar Volume of Federal Awards

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 64 of 175

Indirect Cost Allocation

In No Case Shall an Indirect Cost Allocation Plan or Indirect Cost Rate Proposal Be Acceptable Unless it Has Been Certified by the Governmental Unit Using the Certificate of Cost Allocation Plan or Certificate of Indirect Costs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 65 of 175

Indirect Cost Allocation

The Certification Must be Signed on Behalf of the Governmental Unit by an Individual at a Level No Lower than Chief Financial Officer of the Governmental Unit that Submits the Proposal or Component Covered by the Proposal

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 66 of 175

Indirect Cost Allocation

Where a Local Government Only Receives Funds as a Subrecipient, the Primary Recipient Negotiates the Indirect Cost Rates and/or Monitors the Subrecipient's Plan

Section 5311 Primary Recipient: Caltrans Subrecipient: Grantee

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 67 of 175

Indirect Cost Allocation

Indirect Cost Rates and Cost Allocation Plans Have Specific Documentation Requirements: Organization Chart Comprehensive Annual Financial

Report Certification

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 68 of 175

Indirect Cost Allocation

Indirect Cost Rates and Cost Allocation Plans Where an Organization’s “Central Services” are Included Must: Identify the Unit Rendering the

Service and the Operating Agencies Receiving the Service

Detail the Items of Expense Included in the Cost of the Service

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 69 of 175

Indirect Cost Allocation

Indirect Cost Allocation Plans Must: Describe the Method Used to

Distribute the Cost of the Service to Benefitted Agencies

Contain a Summary Schedule Showing the Allocation of Each Service to the Specific Benefitted Agencies

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 70 of 175

Indirect Cost Allocation

Guidelines for Nonprofits are Similar to Those for Government Agencies

Procedures for Nonprofits Are Prescribed in OMB Circular A-122, Attachment A, Paragraph C

Procedures for Educational Institutions Different – Consult A-21

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 71 of 175

Indirect Cost Allocation

Prescribed Methodologies Simplified Allocation Method Multiple Allocation Base Method Direct Allocation Method

(Nonprofits Only) Special

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 72 of 175

Indirect Cost Allocation

A-122 States that Indirect Costs be Classified within Two Broad Categories: Facilities Administration

A-21 Provides Similar Classification

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 73 of 175

Indirect Cost Allocation

A Nonprofit Organization Which Has Not Previously Established an Indirect Cost Rate with a Federal Agency Shall Submit its Initial Indirect Cost Proposal Immediately After the Organization is Advised that an Award will be Made and, in No Event, Later Than Three Months After the Effective Date of the Award

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 74 of 175

Indirect Cost Allocation

Use of a Standardized Chart of Accounts Is Essential to Indirect Cost Allocation Modify or Expand the Chart of

Accounts to Meet Needs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 75 of 175

Indirect Cost Allocation Plan Preparation Guide

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 76 of 175

Indirect Cost Allocation Plan Preparation Guide

HHS Guide Can be Downloaded at:

http://rates.psc.gov/fms/dca/asmb%20c-10.pdf

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 77 of 175

Capital vs. Operating Costs Operating Costs are Consumed in

Less Than One Year (e.g., Wages, Fuel) and Generally Have a Unit Acquisition Cost of Less Than $300.00

Capital Costs are Expenses for Long-Term Assets (e.g., Vehicles, Garages)

Definitions May be Set by the Grantor Agency

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 78 of 175

Capital vs. Operating Costs

Under the Section 5311 Program, Capital Expenses are Defined in FTA Circular 9040.1F, Chapter III, Paragraph 2e(2)

This Document Can Be Obtained at http://www.fta.dot.gov/documents/FTA_C_9040.1F.pdf

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 79 of 175

Capital vs. Operating Costs Defining Capital Costs is

Important, as OMB Circular A-87 States that Depreciation Will Exclude: Any Portion of the Cost of

Buildings and Equipment Borne by or Donated by the Federal Government Irrespective of Where Title was Originally Vested or Where it Presently Resides

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 80 of 175

Capital vs. Operating Costs What Does this Mean?

If the Cost of the Vehicle (Asset) Was Paid for by a Federal Program, You May NOT Include Depreciation of that Asset in Your Charges to Other Federal Programs in the Cost of Service Provision Source: OMB Circular A-87,

Attachment B, Paragraph 15c(2); and OMB Circular A-122, Attachment B, Paragraph 11c(2).

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 81 of 175

Fixed vs. Variable Expenses

Variable Costs Change Relative to the Amount of Service Provided (e.g., Drivers' Wages)

Fixed Costs Do Not Vary with the Amount of Service Provided (e.g., Administrative Salaries)

Fixed

Variable

Total

Output

Co

st

Developing a Cost Allocation Model

Module 4

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 83 of 175

Why Cost Allocation? Fad or Management Necessity?

An Understanding of Fully Allocated Costs Provides Management with: The Ability to Accurately Price Services

Provided Under Contract An Assessment Tool to Evaluate

Changes in Service For Example, the Cost of Adding or

Losing a Contract Service Could Be Estimated

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 84 of 175

Why Cost Allocation?

General PublicRidership

More GrantFunds From Caltrans??

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 85 of 175

Why Cost Allocation?

To Determine How Much It Costs to Provide A Specific Transit Service

$6.80Per

Trip

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 86 of 175

The Cost Allocation Process

Why Do We Need a Model to Determine Cost? Why Can’t We Simply Divide

Total System Cost by Total System Miles?

Or Total System Cost by Total System Hours?

Consider the Following:

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 87 of 175

The Cost Allocation Process Do These Trips Cost the Same?

5 Miles

5 Miles

10Minutes

5 Miles

5 Miles

20Minutes

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 88 of 175

The Cost Allocation Process Do These Trips Cost the

Same?8 Miles

5 Miles

20Minutes

5 Miles

5 Miles

20Minutes

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 89 of 175

The Cost Allocation Process

Transportation Costs are Driven by Two Critical Factors: Time AND Distance

Our Model Must Take Both Factors Into Account When Costing Transportation Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 90 of 175

Developing a Cost Allocation Model How Do We Allocate Costs?

Don’t Worry, This Process is Not Complicated!

Another Program Mandate???? Aaaaaagh!!!

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 91 of 175

Cost Allocation Model

Cost Allocation Assumes: Total System Costs Can be

Allocated to Service Based on the Level of Service Provided

System Average Unit Costs Can Be Used to Estimate Service Costs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 92 of 175

Overview of Cost Allocation Process

Assemble Data

Assign Expense Line Items

Calculate Unit Costs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 93 of 175

Issues in Assembling Data

Where Do We Get Cost Data?

What Time Period Should be Used?

Projected vs. Actual?

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 94 of 175

Required Data Twelve (12) Months Actual or

Projected Transit Expense Data Expense Data Will be Classified as

Either: Fixed Expense Variable Expense

Service Data Vehicle-Miles Vehicle-Hours Passenger Trips

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 95 of 175

Assigning Cost to Categories Cost Allocation Involves Taking

Each Expense Line Item and Assigning It to Either the Fixed or Variable Category

Variable Expenses are Further Broken Down as Varying Either by: Hour Mile

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 96 of 175

Assigning Cost to Categories

Fixed Costs are Those Costs that Will Not Change As a Result of an Increase or Decrease in Service Levels

Variable Expenses are Those Costs that Will Change if There is a Change in Service Levels

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 97 of 175

Assigning Cost to Categories There are No Hard and Fast

Rules…..But: Project Administration Costs are

Almost Always Fixed Understand the Basis of Each

Cost Item and Assign Accordingly Be Logical BE CONSISTENT

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 98 of 175

Exercise No. 2, Part A

Using the Provided Budget, Classify Each Line Item Expense as Either: Fixed Variable (by Hours) Variable (by Miles)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 99 of 175

Exercise No. 2, Part B

Now that We Have Classified Each Expense Line Item, We Want to Total All Fixed Expenses, All Variable - Hours Expenses, and All Variable - Miles Expenses

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 100 of 175

Calculation of Unit Costs We Now Have a Total of Fixed and

Variable Costs We Need to Calculate Our Unit Costs.

There are Three (3) Calculations: Allocated Hours Cost Allocated Miles Cost Allocated Fixed Expense

Demand Response: Ratio Fixed Route: Fixed Cost Per Vehicle

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 101 of 175

Calculation of Unit Costs

Allocated Hours Cost:

Total Allocated Hours Cost ÷Annual Projected Vehicle Hours

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 102 of 175

Calculation of Unit Costs

Allocated Miles Cost:

Total Allocated Miles Cost ÷Annual Projected Vehicle Miles

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 103 of 175

Calculation of Unit Costs What Do We Do With Fixed

Expenses? There Are Different Approaches -

For Most Demand Response Systems in Rural Areas, Fixed Expenses are Expressed as a Percentage or Ratio of Allocated Variable Expenses (Hours Cost + Miles Cost)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 104 of 175

Calculation of Unit Costs

In Rural Systems, Fixed Expenses are Expressed as a Percent of Variable Expenses: Fixed Cost Factor =

Total Fixed Expenses ÷ (Total Allocated Hours Expenses + Total Allocated Miles Expenses)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 105 of 175

Calculation of Unit Costs

In Urban Systems, Fixed Expenses are Expressed as Follows:(Total Fixed Expenses ÷ Total

Vehicles In Maximum Revenue Service)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 106 of 175

Exercise No. 3

Calculate the Unit Rates Allocated Hours Cost Allocated Miles Cost Fixed Cost Ratio

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 107 of 175

Completing the Computations The Fully Allocated Cost of Service is

Equal to:

{(Total Annual Projected Hours x Allocated Hours Cost)

+(Total Annual Projected Miles x Allocated Miles Cost)}

+ {Fixed Cost Factor x [(Total Annual Projected Hours x Total Allocated Hours Cost) + (Total Annual Projected Miles x Allocated Miles Cost)]}

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 108 of 175

Completing the Computations

To Test our Unit Average Costs, Plug in Total Annual Projected Hours and Total Annual Projected Miles into the Above Equation to Ensure the Result = Total Annual Expenses

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 109 of 175

Completing the Computations

Congratulations … You Have Just Developed a Cost Allocation Model

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 110 of 175

Applying the Model

Now that We Have Our Model, We Will Put it to Work

We'll Sort Through The X's and O's By Looking At Allocating the Costs

of Various System Users

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 111 of 175

Exercise No. 4

Using the Parameters Given, and Our Cost Model Unit Costs, We Will Calculate How Much it Costs to Provide Service to the Five Different Users of Our Transit System

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 112 of 175

Exercise No. 4

This Exercise is Comparable to the Process a Transit Manager Would Use to Determine What Each Agency Should Pay to Purchase Service from the Provider of Services

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 113 of 175

Exercise No. 4 In this Exercise, Management Has Made an

Estimate of the Resources (Hours & Miles) of Service that Each User Will Consume

The Allocated Hours Cost and the Allocated Miles Cost is Applied to Each User

Fixed Costs are Then Added, Then the Three (3) Costs are Summed to Arrive at the Provider’s Fully Allocated Cost of Service

Let’s Walk Through the Computation for the First Agency User

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 114 of 175

Review We Built a Cost Allocation Model

that Uses Generally Accepted Accounting Principles to Allocate Transportation Costs Among Various Agency Users

We Learned How to Use the Model to Determine or Project the Costs for Individual Agency Users

Pricing Fully Allocated Services

Module 5

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 116 of 175

Using the Model to Price Contract Services We Will Examine the Ways in Which

A Transit System Can Use Fully Allocated Costs to Develop Unit Pricing for Contracted Services Various Types of “Unit” Costs Pro’s and Con’s of Each Unit Cost Type

We Will Calculate Various Units Costs for Our Transit System

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 117 of 175

Objectives in Our Rate Structure

Our Objectives in the Process: Simple Equitable Reflect Actual Cost of Service

Provision Appropriate Use of Public

Subsidies

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 118 of 175

Alternative Rate Structures

Per Trip Per Mile Per Hour Per Passenger Mile Per Zone

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 119 of 175

Price Per Trip

Price Per Trip Computed as Follows:

Fully Allocated Costs of the Service ÷ No. Projected Passenger Trips

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 120 of 175

Characteristics of Per Trip Pricing Simple Shared Ride Equity Assumes That Are Trips Have

Similar Characteristics Works Best in Small Service Areas Greater Risk for Service Provider Short Trips Subsidize Long Trips

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 121 of 175

Price Per Mile

Price Per Mile Computed as Follows:

Fully Allocated Costs of the Service ÷ No. Projected Miles of Service

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 122 of 175

Characteristics of Per Mile Pricing Customers Understand Miles Requires Recordkeeping by Drivers Cost Per Mile Varies Based on

Route Path Driven on a Given Trip Does Not Address Travel and Wait

Time Dead Head Mileage Shared Ride Equity Issues

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 123 of 175

Price Per Hour

Price Per Hour Computed as Follows:

Fully Allocated Costs of the Service ÷ No. Projected Vehicle Hours

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 124 of 175

Characteristics of Per Hour Pricing Requires Recordkeeping by

Drivers Cost Per Hour Varies Based on

Route Path Driven on a Given Trip

Addresses Travel and Wait Time Shared Ride Equity Issues

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 125 of 175

Price Per Passenger Mile

Price Per Passenger Mile Computed as Follows:

Fully Allocated Costs of the Service ÷ No. Projected Passenger Miles

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 126 of 175

Characteristics of Per Passenger Mile Pricing

Equitable Addresses Shared Ride Some Shared Ride Equity

Issues Generally Requires Automation

to Assist in Billing Computations

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 127 of 175

Price Per Zone

Price Per Zone Zones are Artificial Grids

Overlaid on a Map of the Service Area

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 128 of 175

Price Per Zone

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 129 of 175

Price Per Zone

Computed as Follows:

Fully Allocated Costs of the Service ÷ No. Projected Zones of Travel

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 130 of 175

Price Per Zone Counting Zones Zones are Counted on a Straight-Line Basis,

Up and Down, Left or Right (No Diagonal Movement)

33

7

1

2

5

6

B H JIDC ME F G K L

1 2 3 4

10

8

9

3

4

6

7

5

A

Columbus

Dublin

Hilliard

Upper Arlington

Worthington

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 131 of 175

Characteristics of Zone Pricing Sometimes Difficult to Explain Relatively Simple to Administer Easy to Predict Trip Cost if User is

Familiar with Zone Map Requires Initial Estimate of Zones

Traveled in Order to Set Rate Short Trips Will Generate

Problems in Cost Recovery Sensitive to Zone Size

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 132 of 175

Rate Setting Complexities

Ridesharing Wait Time Out-of-County Trips Mixed Fleet (e.g., Different Sized

Vehicles) Brokerage: Trips Assigned to Other

Providers Contracted Services Subsidies

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 133 of 175

Ridesharing

Occurs When the Clients of Two or More Agencies that Contract for Service Ride the Same Vehicle

Some Rate Structures Will Require Sub-Allocation of Costs Per Hour and Per Mile Pricing

Methods

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 134 of 175

Ridesharing

Suggested Approaches Pro-Rate Trip Costs Based on:

Percent of Agency “A” Passengers as Percent of All Passengers (Percent x Overall Route Cost)

Calculate Trip Cost Based on Total Number of Passengers ((Overall Trip Cost ÷ No. of Passengers) x Passengers Agency “A”)

Problems Assumes Uniform Trip Characteristics Gives Appearance of Uniform Rate

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 135 of 175

Wait Time

Labor Costs Associated with Wait Time is a Problem

Suggested Approach Adopt Time-Based Pricing

Cost Per Hour Added Wait Time Charges on Top of

Existing Pricing Strategy (e.g., $10.00 per Hour)

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 136 of 175

Out-of-Service Area Trips

Use The Cost Allocation Model as the Pricing Structure

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 137 of 175

Mixed Fleets

Different Operating Cost Structure of Large Buses over Minivans/Standard Vans

Options: Adopt Tiered Pricing Structure Use Uniform Structure

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 138 of 175

Brokered Trips

Adopt Uniform Rate Structure Despite Differential Costs/Charges Among Multiple Providers

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 139 of 175

Contracted Services

Fully Allocated Cost Pricing Means System Administration Costs Plus Contractor’s Rate are Incorporated Into the Pricing Structure

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 140 of 175

Subsidies

Deduct Subsidy Amount Prior To Calculating Average Unit Rates in Your Cost Allocation Model

Run Cost Model With and Without Subsidy so Users Understand True Cost of Service

Automating the Cost Allocation ProcessModule 5

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 142 of 175

Overview

As You Can See from the Cost Allocation Model Built Earlier in this Workshop Cost Allocation Can be Repeated

on an Annual Basis The Process Lends Itself to

Spreadsheet Application

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 143 of 175

Cost Allocation Model

The Course CD-ROM Contains a Generic Cost Allocation Model

Let’s Take A Look at the Model

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 144 of 175

Cost Allocation Model

Copy the File “Cost Allocation Model.xls” to a Folder on Your Computers Local or Network Drive

Start MS Excel Navigate to Folder and Open

the Model

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 145 of 175

Cost Allocation Model

Cautions Excel Will Generate One of Two

Messages, Depending on Your Security Level Excel Will Not Permit You to Open the

File Action:

Reset Security Level to Medium From the Menu, Click on Tools, Options,

Security Tab, Click on the Macro Security Button and Select Medium

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 146 of 175

Cost Allocation Model

Cautions Once Set to Medium, Excel Will

Permit You to Open the File, But Will Generate a Warning Message

You Must Click on “Enable Macros” in Order for the Cost Allocation Model to Work

You are Not Jeopardizing Your Computer or Network Security

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 147 of 175

Cost Allocation Model:Macro Warning

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 148 of 175

Cost Allocation Model:Opening Screen

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 149 of 175

Cost Allocation Model:Opening Screen Opening Screen

The Cost Allocation Model Will Always Open to This Screen (Rather Than Last Place)

To Continue, Click the “Begin” Button

This Will Advance You to the “Table of Contents” Worksheet

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 150 of 175

Cost Allocation Model:Table of Contents

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 151 of 175

Cost Allocation Model:Opening Screen First Step – Enter System

Service Data Vehicle Hours Vehicle Miles Vehicles Used in Peak Revenue

Service Click On “Step 1 – Enter ……”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 152 of 175

Cost Allocation Model:Opening Screen

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 153 of 175

Cost Allocation Model:Enter Service Data What Time Period For Data?

Analysis of Past Performance Historical Data

Projected Costs for a Future Period Budgeted or Projected Data

Enter System Hours and Miles For Fixed Route Systems, Enter

Peak Vehicles In Revenue Service

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 154 of 175

Cost Allocation Model:Enter Service Data:

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 155 of 175

Cost Allocation Model:Next Step Once You Have Entered System

Service Data, Click on “Back to Table of Contents”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 156 of 175

Cost Allocation Model:Next Step

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 157 of 175

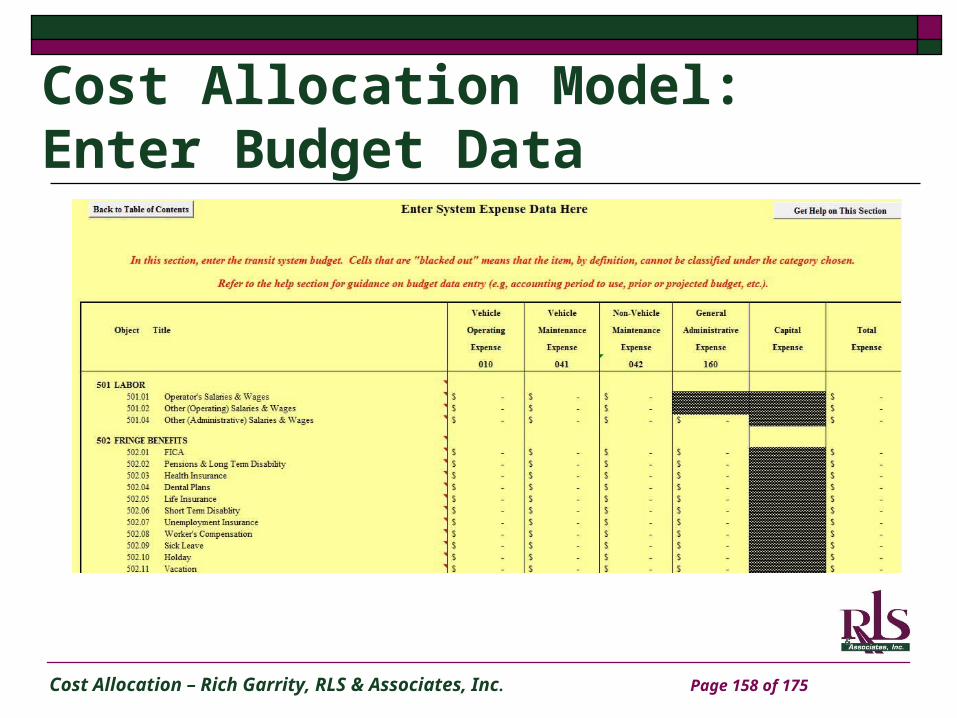

Cost Allocation Model:Enter Budget Data From the Table of Contents,

Click on Step 2 – Enter Budget Data for Your Transportation System

This Will Take You To a Worksheet Where You Will Enter Budget Data

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 158 of 175

Cost Allocation Model:Enter Budget Data

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 159 of 175

Cost Allocation Model:Enter Budget Data The Chart of Accounts is

Generic, Based on the FTA Uniform System of Accounts (USOA)

The Chart Requires You To Enter Data in Accordance With Four Basic Function Codes

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 160 of 175

Cost Allocation Model:Enter Budget Data Four Basic Function Codes

Operations Vehicle Maintenance Non-Vehicle Maintenance General Administration

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 161 of 175

Cost Allocation Model:Enter Budget Data Enter Budget Data

Each Function Code Has Its Own Column

Columns Automatically Total for Each Function Each Line Item

Where the Cells are Shaded, It Means That, By Definition, the System Cannot Have Expenses in That Line Item

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 162 of 175

Cost Allocation Model:Enter Budget Data If You are Unfamiliar With the

USOA Chart of Accounts, Help is Available

By Moving Your Mouse Cursor Over the Tiny Red Triangle on the Ride Side of the Account Column

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 163 of 175

Cost Allocation Model:Enter Budget Data

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 164 of 175

Cost Allocation Model:Compute Fully Allocated Costs Once You Have Enter Budget

Data, Click the Button on the Top of the Worksheet and Go Back to the Table of Contents

Click on “Step 3: Calculate the Fully Allocated Cost of Any Service Component”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 165 of 175

Cost Allocation Model:Compute Fully Allocated Costs A Final Data Entry Sheet Will

Appear You Will Need to Specify The

Mode of Service Fixed Route Demand Response

Fixed Expenses Are Allocated Differently in Each Mode

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 166 of 175

Cost Allocation Model:Compute Fully Allocated Costs You Then Enter the Estimated

or Actual Vehicle Hours or Vehicle Miles

If Costing a Fixed Route Service, Also Enter the Number of Peak Vehicles Used for the Proposed Service

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 167 of 175

Cost Allocation Model:Compute Fully Allocated Costs

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 168 of 175

Cost Allocation Model:Compute Fully Allocated Costs Once You Enter the Required

Service Data, The Fully Allocated Cost Will Automatically be Computed and Shown in the Bottom Box!

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 169 of 175

Cost Allocation Model:Other Elements The Model Works Because Once

the Budget Information, Standardized Assignment of Each Line Item Has Already Been Established

You DO NOT Have to Assign Each Line Item to the Fixed, Variable-Hours, or Variable Miles Category

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 170 of 175

Cost Allocation Model:Other Elements You Can View the Assignment of

Costs From the Table of Contents, Click on

“View the Assignment of Cost Categories” Your Total Budget Information Appears An “X” Indicated How the Model

Classifies Each Line Item, By Function Code

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 171 of 175

Cost Allocation Model:Other Elements You Can Also View the Total

Computations of Fixed and Variable Expenses

From the Table of Contents Click on “View the View the Cost

Computations”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 172 of 175

Cost Allocation Model:Other Elements Finally, Some Additional

Explanation, Help, or Tips are Available from All Screens

Click on the “Get Help on This Section to Get Context Sensitive Help”

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 173 of 175

Cost Allocation Model:Other Elements

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 174 of 175

Adjourn

Good Luck in Using this Information at Your Own Transit Programs

Please Complete the Course Evaluation!!

Cost Allocation – Rich Garrity, RLS & Associates, Inc. Page 175 of 175

Presenter

Richard Garrity, Senior AssociateRLS & Associates, Inc.

3131 S. Dixie Highway, Suite 545Dayton, OH 45439

(937) 299-5007

Direct Line: (910) [email protected]