cost segregation

TRANSCRIPT

Cost Segregation

Engineering StudiesEngineering Studies

AmCorp Management, Inc. is the Nation’s most successful Expense Analysis Firmmost successful Expense Analysis Firm

A Company with a singular focus.

AmCorp Management, Inc. offers a RISK FREE analysis to help companies locate and recover revenue that has been lost through improper billing practices. Our auditing team’s sole practice is to identify and secure overcharges

We ha e the highest reco er rate in the ind strWe have the highest recovery rate in the industry

AmCorp’s Examiner's and Auditors have‐ 20+ years experience‐ 20+ years experience‐ helped over 20,000 clients‐ recover almost 2 billion in savings

AmCorp Management, Inc. has been highlighted by the following media outletshighlighted by the following media outlets.

Plus many more…

AmCorp Management, Inc. is the Nation’s most successful Expense Analysis Firm

What is Cost Segregation?Cost Segregation is the process of identifying personal property

most successful Expense Analysis Firm

Cost Segregation is the process of identifying personal property assets that are grouped with real property assets, and separating out personal assets for tax reporting purposes. A cost segregation study identifies and reclassifies personal property assets to shorten h d i i i f i hi h ithe depreciation time for taxation purposes, which increases annual deductions, reduces current income tax obligations, thus increasing income and cash flow.

Personal property assets include a building’s non‐structural elements, exterior land improvements and indirect construction costs.

U.S. Treasury Department, 2004 “Cost Segregation is a lucrative Tax Strategy that should be used in almost every major purchase of Commercial Real Estate.”

Cost Segregation Engineering Opportunities

What qualifies for Cost Segregation opportunitiesN t ti– New construction

– Purchase of existing property– Renovations or expansions– Leasehold improvements– Leasehold improvements– Existing property placed in service after 1986

(“look‐backs”)– Real property stepped‐up through estate

Each $100,000 in assets reclassified from a 39‐year recoveryperiod to a five‐year recovery period results in approximately$$22,000 in net present value savings, assuming an 8% discountate and a 40% marginal tax rate.

Journal of Accountancy Copyright 2005 by the AICPAJournal of Accountancy, Copyright 2005 by the AICPA

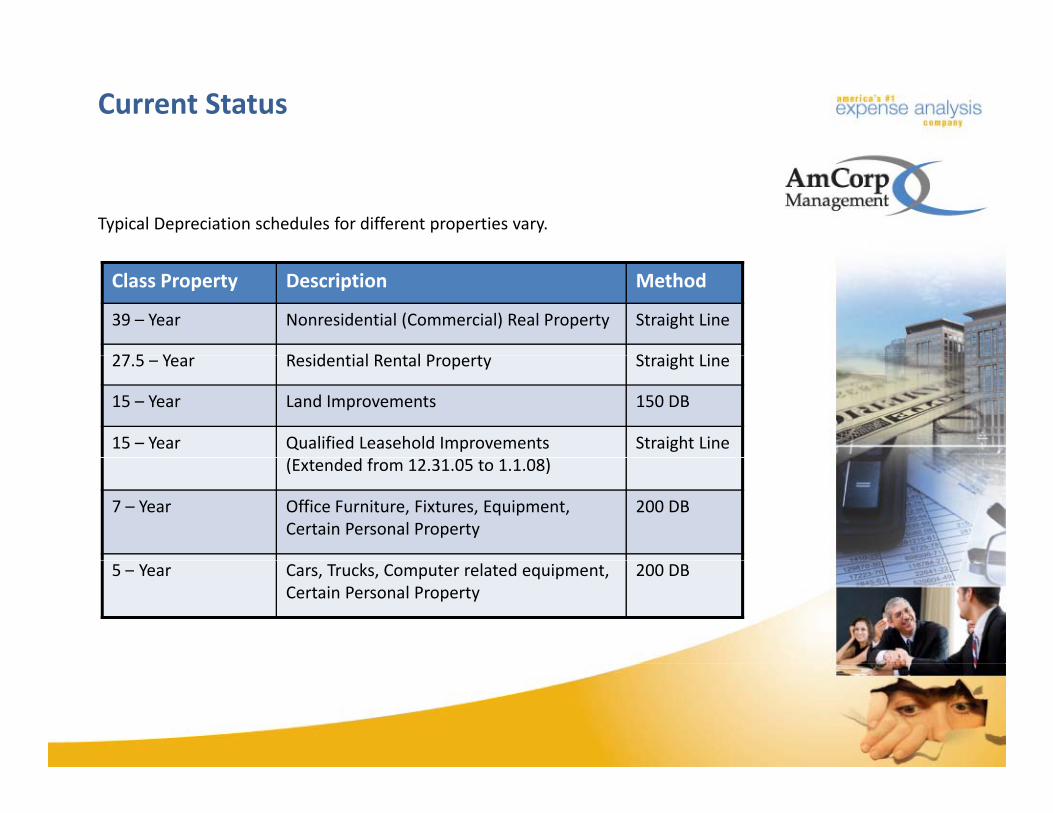

Current Status

Typical Depreciation schedules for different properties vary.

Class Property Description Method

39 – Year Nonresidential (Commercial) Real Property Straight Line

27 5 Y R id ti l R t l P t St i ht Li27.5 – Year Residential Rental Property Straight Line

15 – Year Land Improvements 150 DB

15 – Year Qualified Leasehold Improvements( )

Straight Line(Extended from 12.31.05 to 1.1.08)

7 – Year Office Furniture, Fixtures, Equipment, Certain Personal Property

200 DB

5 – Year Cars, Trucks, Computer related equipment, Certain Personal Property

200 DB

Cost Segregation Reclassification Opportunities

Experience has shown that an average of 32% is typically eligible for Cost Segregation.

The Reclassification Process

The IRS wrote the Standard:• Mandates 3rd party study• Mandates 3rd party study

• Recommends engineering based studies

• Enforces Audit Techniques Guide of 2004Enforces Audit Techniques Guide of 2004

• Regulates compliance to Circular 230

SIMPLE TAX TREATMENT:SIMPLE TAX TREATMENT:1. Catch‐up depreciation is taken in one year by filing IRS Form 3115

(Change of Accounting Method)

f2. There are NO amended tax returns to file.(File a new depreciation schedule)

3. Payments accompanying quarterly tax filings may be immediately reduced.

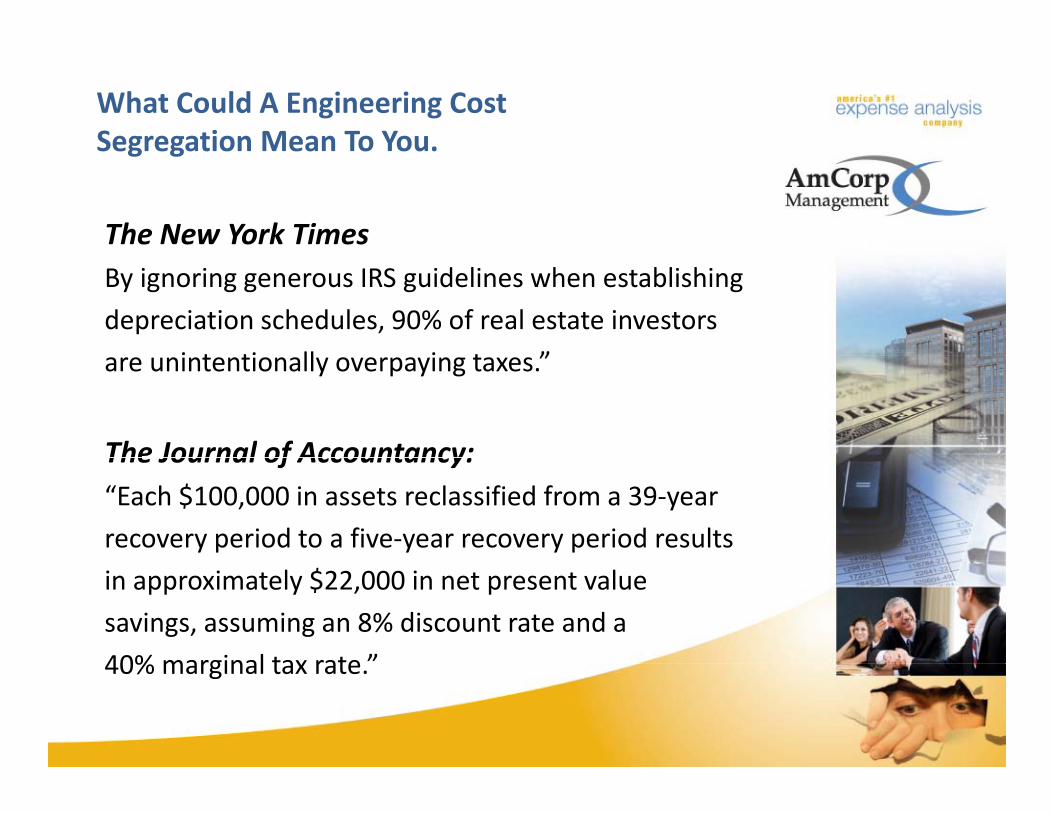

What Could A Engineering Cost Segregation Mean To You.Segregation Mean To You.

The New York TimesBy ignoring generous IRS guidelines when establishingdepreciation schedules, 90% of real estate investors

i t ti ll i t ”are unintentionally overpaying taxes.”

The Journal of Accountancy:The Journal of Accountancy:“Each $100,000 in assets reclassified from a 39‐yearrecovery period to a five‐year recovery period resultsin approximately $22,000 in net present valuesavings, assuming an 8% discount rate and a40% marginal tax rate ”40% marginal tax rate.

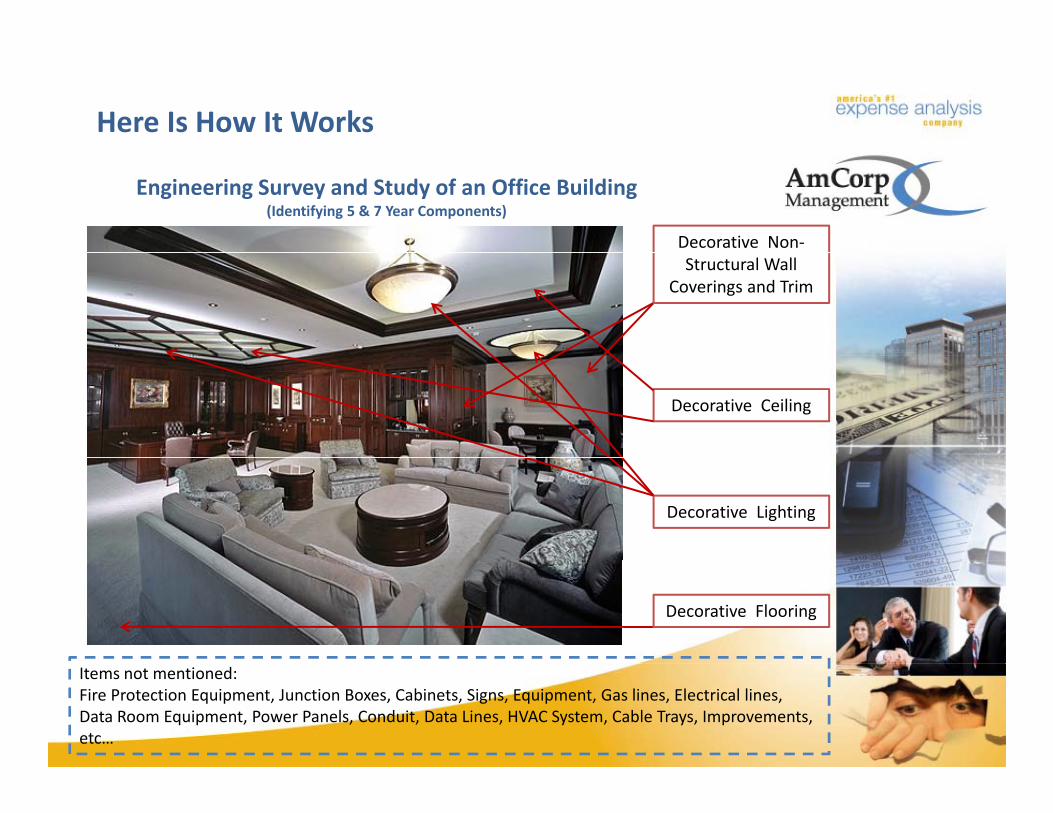

Here Is How It Works

Decorative Non‐

Engineering Survey and Study of an Office Building(Identifying 5 & 7 Year Components)

Structural Wall Coverings and Trim

Decorative Ceiling

Decorative Lighting

Decorative Flooring

Items not mentioned: Fire Protection Equipment, Junction Boxes, Cabinets, Signs, Equipment, Gas lines, Electrical lines, Data Room Equipment, Power Panels, Conduit, Data Lines, HVAC System, Cable Trays, Improvements, etc…

Partial List Of Other Components That Can Be Re‐Classified To Accelerate Tax BenefitsRe Classified To Accelerate Tax Benefits

• Communication• Systems Transformers

• Emergency Fixtures • Waste Interceptors

• Mezzanines Stairs • Platforms

• Hospitality Fixtures • TV Outlets & Wiring • Distribution Panels• Distribution Wiring • High Voltage Switchgear

• Security Systems• Monitoring Systems • Conduit/Wiring for specialty Systems • Flex Space

• Structural Steel • Task Lighting • Vents Beams Columns • Gas Systems• Vacuum SystemsHigh Voltage Switchgear

• Data Jacks • Miscellaneous Outlets • Emergency Power • Computer Data/Power S l /E h t

Flex Space • Demountable Power Systems• Shower/Deluge Fixtures• Supply & Waste Systems • Gas/Compressed Air Mill k Fl C i

Vacuum Systems• Exhaust Systems • Waste Interceptors • Audio/Visual Systems • Buss Ducts N t li ti B i• Supply/Exhaust

• Kitchens• HVAC Systems • Environmental Controls • Computer Environ. Control

• Millwork Floor Coverings• Window Treatments • Wall Coverings • Demountable Walls • Decorative Lighting

• Neutralization Basins • Humidity/Temp. Control • Site Utilities • Specialty refrigeration units• Sewer

• Communications • Fire Protection Systems • Specialized Air Systems• Filtration/Sensing• Break/Coffee Stations

• Signage • Sidewalk & Curbing • Parking Lots & Curbing • Landscaping Fencing• Swimming Pools

• Drainage Systems • Outdoor Lighting • Much more…

reak/Coffee Stations• Sinks Drains• Specific‐Use Structures

Swimming Pools• Foundations

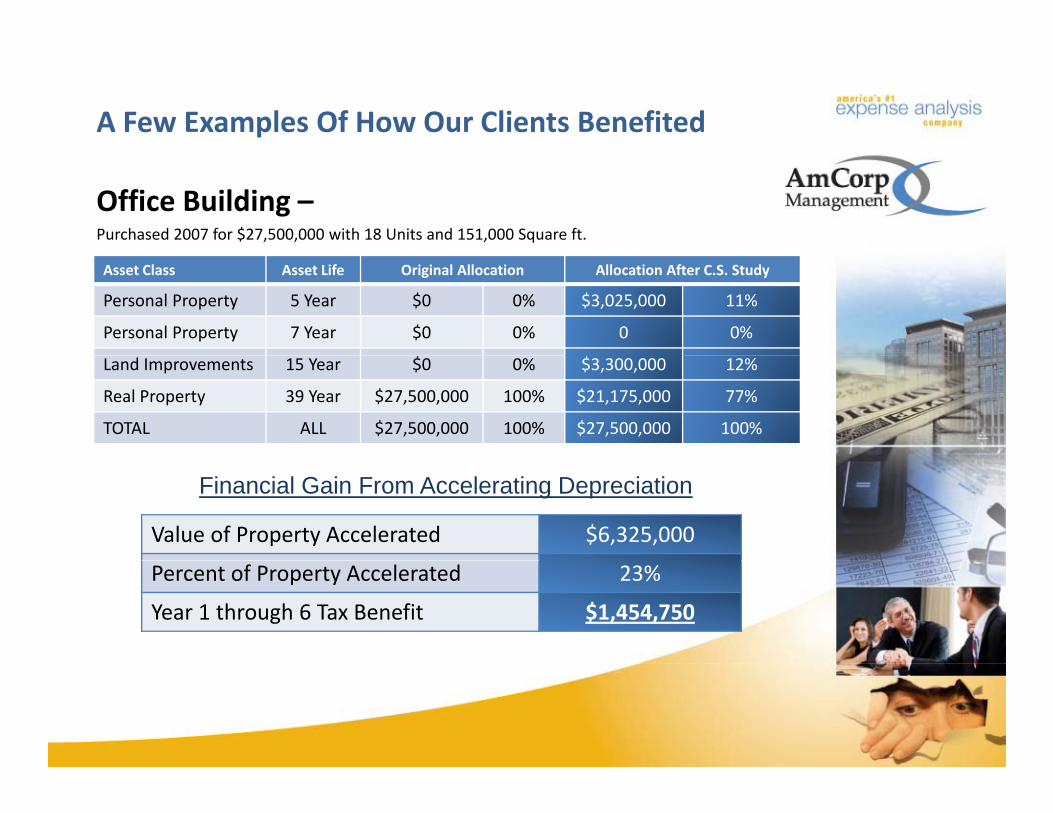

A Few Examples Of How Our Clients Benefited

Office Building –Purchased 2007 for $27,500,000 with 18 Units and 151,000 Square ft.

Asset Class Asset Life Original Allocation Allocation After C.S. Study

Personal Property 5 Year $0 0% $3,025,000 11%

Personal Property 7 Year $0 0% 0 0%

Land Improvements 15 Year $0 0% $3,300,000 12%

Real Property 39 Year $27,500,000 100% $21,175,000 77%

TOTAL ALL $27,500,000 100% $27,500,000 100%

Value of Property Accelerated $6,325,000

Financial Gain From Accelerating Depreciation

Percent of Property Accelerated 23%

Year 1 through 6 Tax Benefit $1,454,750

A Few Examples Of How Our Clients Benefited

Motel ‐Purchased 2005 for $10,925,000 with 32,000 Square ft.

Asset Class Asset Life Original Allocation Allocation After C.S. Study

Personal Property 5 Year $0 0% $2,294,250 21%

Personal Property 7 Year $0 0% 0 0%

Land Improvements 15 Year $109,250 1% $437,000 4%

Real Property 39 Year $10,815,750 99% $8,193,750 75%

TOTAL ALL $10,925,000 100% $10,925,000 100%

Value of Property Accelerated $2,731,250

Financial Gain From Accelerating Depreciation

Percent of Property Accelerated 25%

Year 1 through 6 Tax Benefit $682,912

Who Needs A Cost Segregation Study?

Anyone who:

1. Owns a building with over $1,000,000 in property value.

2. Has net income and is a profitable tax paying entity.

Qualifying Properties:

1. Purchased or Built their facility within the last 12 months.

2. Purchased or Built their facility since 1987.

3. Facility with Renovations or Additions.

4. Any Change of Ownership.(Including Estates)

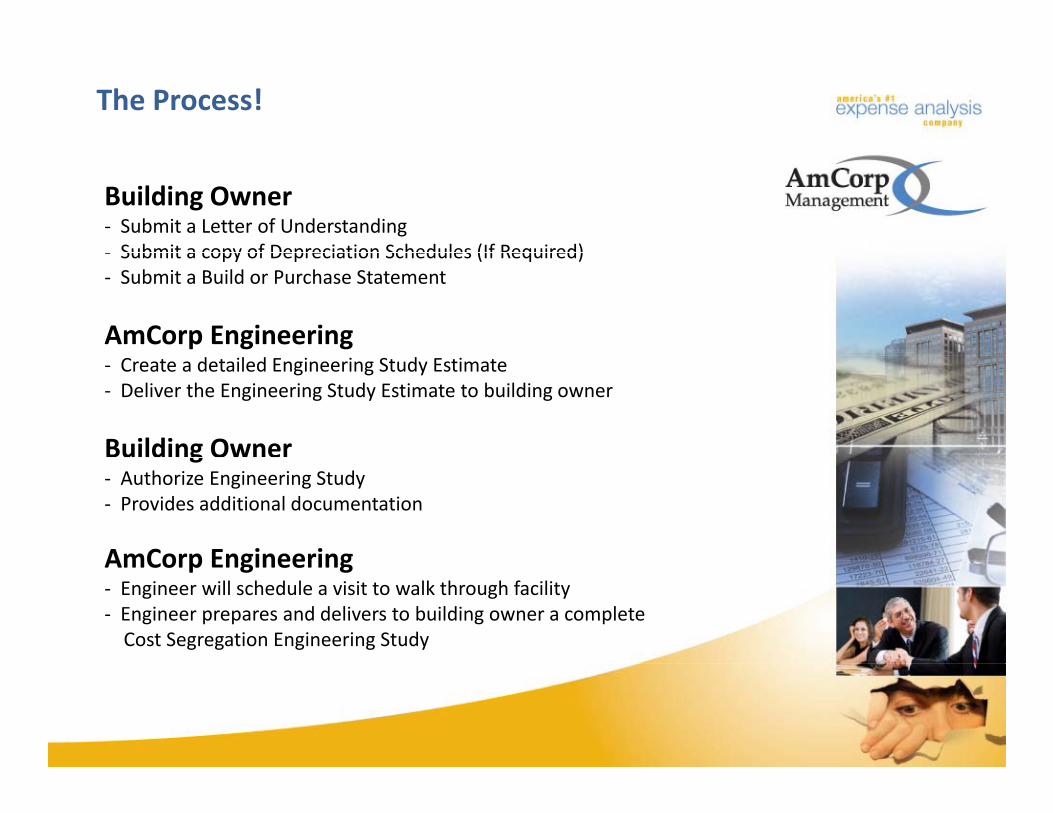

The Process!

Building Owner‐ Submit a Letter of Understanding‐ Submit a copy of Depreciation Schedules (If Required)‐ Submit a copy of Depreciation Schedules (If Required)‐ Submit a Build or Purchase Statement

AmCorp Engineering‐ Create a detailed Engineering Study Estimate‐ Deliver the Engineering Study Estimate to building owner

Building Ownerg‐ Authorize Engineering Study‐ Provides additional documentation

AmCorp EngineeringAmCorp Engineering‐ Engineer will schedule a visit to walk through facility‐ Engineer prepares and delivers to building owner a complete Cost Segregation Engineering Study