cost transformation

TRANSCRIPT

1

Our study began with a mapping of all profitability

drivers for a wireless carrier, with greater focus on

defining the expense levers

Profit =

f (ARPU * Subscribers) f (CCPU * Subscribers, CPGA* gross adds, D&A)

-

ARPU Subscribers

CPGA

(Cost per Gross

Acquisition)

CCPU

(Cash Cost per

User)

Depr. & Amort

Revenue Expenses

Wireless Profitability Tree

Acquisition ChurnHardwareVoice Data Services

& Features

Voluntary Involuntary

• Care

• Billing

• General & Administration

– Credit & Collections

– IT

– Human Resources

– Finance & Admin

– Device Supply Chain

Management

• Base Marketing/Retention

• Network Operations

• Acquisition Marketing

• Sales Operations

• Acquisition Subsidies

2

CPGA

Acquisition

Marketing

Other

G & ABillingCare

= In Scope

= Out of Scope

Base

Marketing /

Retention

Network

(Variable)

Sales

Operations

OpEx

CCPU1Cost per Gross

AcquisitionCash Cost

per User

Wireless Operating Expense Cost Tree*

Credit &

CollectionsIT HR F & A

Device

SCM

• Depreciation / Amortization

Acquisition

Subsidies

* Users

*

Gross

Ads

Note: 1-CCPU should also include cost of content such as licensing fees for video or games and procurement costs.

They are not listed here due to their small percentages in CCPU compared to other cost components.

*For a higher level profitability tree, see appendix

Key F

un

cti

on

s

An in-depth analysis of the Operating Expense

drivers provides a framework for value targeting

around a number of key functions

3

CPGA

Acquisition

Marketing

Other

G & ABillingCare

= In Scope

= Out of Scope

Base

Marketing /

Retention

Network

(Variable)

OpEx

CCPUCost per Gross

AcquisitionCash Cost

per User

Wireless Operating Expense Cost Tree

Credit &

CollectionsIT HR F & A

Sales

Operations

Acquisition

Subsidies

Device

SCM

• Depreciation / Amortization

7% 3% 14% 4% 29% 8% 7% 9%

19% 57% 24%

3.5% 5% 0.3% 1.5% 4%

Cost Breakdown % of OPEX*

Source: US DB Data Book 2005, Major US wireless companies’ financials

Note: Payroll and training costs are included in functional areas.

*For a cost breakdown as a percent of revenue, see Appendix

* Users

*

Gross

Ads

A benchmark of key components of OpEx has been

created based on large US carriers’ financials and

compared across major markets of the world.

4

10-20%

Savings

5-15%

Savings

CPGA

Acquisition

Marketing

Other

G & ABillingCare

= In Scope

= Out of Scope

Base

Marketing /

Retention

Network

(Variable)

OpEx

CCPUCost per Gross

AcquisitionCash Cost

per User

Wireless Operating Expense Cost Tree

Credit &

CollectionsIT HR F & A

Sales

Operations

Acquisition

Subsidies

Device

SCM

• Depreciation / Amortization

7% 3% 14% 4% 29% 8% 7% 9%

19% 57% 24%

3.5% 5% 0.3% 1.5% 4%

15-20%

Savings

20-25%

Savings

12-19%

Savings

25-35%

Savings

20-25%

Savings

30-35%

Savings

15-20%

Savings

15-20%

Savings

15-20%

Savings

15-20%

Savings

35-40%

Savings

20-25%

Savings

20-30%

Savings

15-25%

Savings

Savings % of Cost Element*

Source: US DB Databook 2005, Large US Wireless Companies’ Financials

*For savings percentage ranges as a percent of overall OpEx, see Appendix

* Users*

Gross

Ads

A target range of average savings potential within

each operating expense component was developed

using cost take-out leading practices

5

The Care function operates all points of service to

resolve customer issues including the use of

agents, self-service portals, and IVR systems.

— Cost Reduction Trends —

— Definition —

• Inbound and Outbound Care Centers

– Agents and Outside Agencies

• Agent, IVR, Face-to-Face, Mail/Fax, and Web Care Channels

• Prepaid & Postpaid contacts

Care Includes:

— Functional Interdependencies —

Key Cost KPIs:

• Calls per Customer

• Agent First Call Resolution Rate

• Average Handle Time

• Misdirects

• Service level

• Repeat Call rate

• IVR Percent Complete

• Web Percent Complete

CCPU - Care

• Credit & Collections (separate tree)

• Outbound Sales (Covered in tree under CPGA)

Care does not Include:

• Billing

– Multiple bills per customer will trigger more volume in the

care channel

• Marketing

– An easy to understand offer or campaign will drive down

volume in Care

• Network

– Dropped calls or other network downtime will increase

contacts to the Care channels

Emerging vendor offerings are driving customer contact management infrastructure to outsourcers and to offshore locations (e.g., India, Philippines)

Technology advances create significant opportunities to fundamentally shift cost structure

– Advances in voice recognition have the potential to reduce traffic to agents

– Intelligent call routing and balancing reduces queues and improves close-out rate

The move towards web care is enabling substantial cost savings

– 80% of Fortune 1000 companies involved with some form of Web care (Yankee Group Survey)

The mobile handset will increasingly serve as a supplemental customer care platform

– SMS provides simple care features today (already in place in Europe)

– Mobile Web provides more dynamic care features in future

– Proliferation of handset types and carriers’ desire to retain control over customer data may limit growth of mobile care in the near term

Customer care services bureaus, managed by third party service providers, will increasingly become an attractive option for carriers to deliver care at reduced costs without compromising proprietary customer information

6

• Company owned Retail

vs Third Party

• # of contacts

• AHT

• Labor costs1

• Service Level

• Agent utilization

The Care function decomposes into various levers

driving the overall cost of the operation

Phone

Care

Application

Maintenance

Operations

Support

# Contacts

IVR

Agent Handled

• # of contacts

• AHT

• Agent utilization

•Cross train

• Call mix

• Labor costs1

• Outsourcing

• Abandon rate

• Service level

• Agent Performance

Web

Web

Self-Service

Other eChannels

(Agent+Automated)

eChat

• # of contacts

• AHT

• Labor cost1

• Agent utilization

• Service level

• Abandon rate

• Simultaneous chats

• “Bad Volume” rates3

• Rep Search Functionality4

• Non-company issue training5

• # of contacts

• AHT

• Labor cost1

• Agent utilization

• Service level

• Contact rate – Volume / Type (Voice, Data, Content)

• Call Triggers or Events (i.e. Billing Issue, Network, etc…)

• # subscribers

• Repeat contacts (done rate) contact resolution

• Segment based Treatment Strategy

• # of applications

• # /mix

locations/sites/

geographies

• # of employees

• # of offers

• Regulatory

• HQ / OverheadFace-to-Face

• # of contacts

• % Automated Capability2

• # (%) of transactions

completed

• Ease of Use / Service

Level

• # of contacts

• Abandon

• Completes

• % Automated Capability2

• Redirect

• Ease of Use / Service

Level

IVR

Self-Service

1. Fully Loaded Labor Costs: Includes: Wages, Benefits, Training, Facilities, Supervision, Space, etc…

2. Refers to the scope of SS capability (e.g. the number of transaction types supported)

3. “Bad Volume” refers to eChats that cannot be resolved through this channel

4. This refers to the ability given to the rep to search for standard phrases that resolve issues

5. This refers to issues that do not relate to the company’s product or service

Mail / Fax

Other CareRepair /

Tech Services• Company owned Retail

vs Third Party

• # of contacts

• Labor costs1

• Service Level

• Agent utilization

Variable

Operations

Infrastructure

• Telecom costs

• Reporting

Cost drivers are in Maroon

7

Detailed Analysis of the Cost Drivers of the Care

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Number of Contacts

• Call volume

• Contact rate

• Misdirected calls

• Repeat calls

Understanding and proactive management of 'Call Drivers' can

eliminate significant segments of call volume, via:

– Automation of common inquiries (e.g., Payments) via self service

channels (IVR and Web)

– Reduction of mis-directs, and repeat calls

• Universal Agents (or universal serviceability of common

inquiries)

• First call resolution (supported by process, call reason

analysis, and workforce effectiveness tools)

• Customer insight driven routing

• Knowledge management application (operating procedures,

FAQs, etc.)

– Simplification of billing and product offerings (e.g., bundled and

single cost service packages)

– Incentives for self service (e.g., 'On-line' pricing)

– Offering directed/dynamic self service offerings for increased

adoption (e.g., offer restore service functionality to suspended

accounts ONLY)

– Proactive communication of customer impacting changes (e.g.,

Service, Regulatory, etc)

– Create a strong correlation between the reason of contacts and

business process impacted or causing the inbound call

– Identify inside the communication plan channels and events the

telco operator uses to contact the customer base that can cause an

inbound flow of contacts

– Identify business processes that create cases of interactions with

the customer base (e.g. invoicing process, new offerings, faults, ..)

– Create a correlation between incoming contacts and events

causing an information need to the clients

• BellSouth

• AT&T (SBC)

• Verizon

• Qwest

• AOL

• H3G

• Telecom Italia

• HP reduced misdirects

from 40% to 10%

Average client

experience:

• Decrease contact

volume in all channels

by 5-15% (key is agent

call volume)

• Increase first call

resolution by 5-15%

• Increase call

completion rates by 5-

15%

• Increase in

automated/self-redirect

rates by 5-15%

• Decrease cost to serve

overall

• First call resolution rate

• Call completion rate

• Automated/self redirect

rate

• Misdirects < 8%

8

Detailed Analysis of the Cost Drivers of the Care

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Web Self Service

• # of contacts

• % Automated

Capability

- Scope of

capability

- # (%) of

transactions

completed

• Ease of Use /

Service Level

Through channel optimization, drive more contacts to the Web for

self service vs. more expensive channels

– Provide more holistic, easily navigable and enjoyable web

experience by standardizing web infrastructure and

integrating customer insights

– Promote web self service through traditional channels

– Maximize number of simple transactions that can be

completed through web

– Improve completion rates

• Use queries with natural language understanding

capability

• Implement personalization, channel integration, dynamic

FAQs, remote diagnostics

– Over time, migrate more complex transactions to the web

• AT&T - Ask Allie: 70%

increase in self service

usage

• BEA: Self Service customer

retention improved 10%

• BellSouth: 200% increase in

web based sales and service

• Telia (Sweden): 10 fold

increase in time spent on the

web site for self service

• BT Spain, Telefonica

(Spain), Bell Canada, Virgin

Mobile, BT, MCI, Telecom

Italia, Telenor

• % self service 40+%

• % web self service 10+%

• Web completion rate

• Agent call volume

• Customer satisfaction

IVR Self Service

• Number of IVR

contacts

• Abandons

• Completes

• % Automated

Capability

- How many

transaction types

• Redirects

• - Ease of Use /

Service Level

Through channel optimization, drive more contacts to the IVR for

self service vs. the agent channel to reduce cost to serve

– Maximize self-service channel by enabling rules-driven,

differentiated treatment based on customer segmentation

– Use customer insight to expand breadth and depth of IVR

offerings and increase done rate

– Migrate platform to new lower cost technologies

– Multi-channel integration to complete portions of transactions

in IVR through CTI (Computer Telephony Integration)

• Reduce AHT when info is retained and passed on to

agents

• Lead to enhanced customer experience: Personalized

responses, Natural language speech recognition,

Announcements, Dynamic scripting, Customer centric

vs. industry centric offerings

• Telenor: 50% increase in

deflection of calls to self

service

• Verizon: Increase in self

service usage: 3% to 20%

• Virgin Mobile - 8.6%

reduction in callers

requesting an agent in IVR

Average client experience:

• Increase IVR complete rate

increase by 5-50%

• Increase in Automated/Self

Redirect Rates by 5 -15%

• % self service 40+%

• % IVR self service 25+%

• IVR completion rate

• Agent call volume

• First call resolution

• Call completion rate

• Automated/self redirect

rates

9

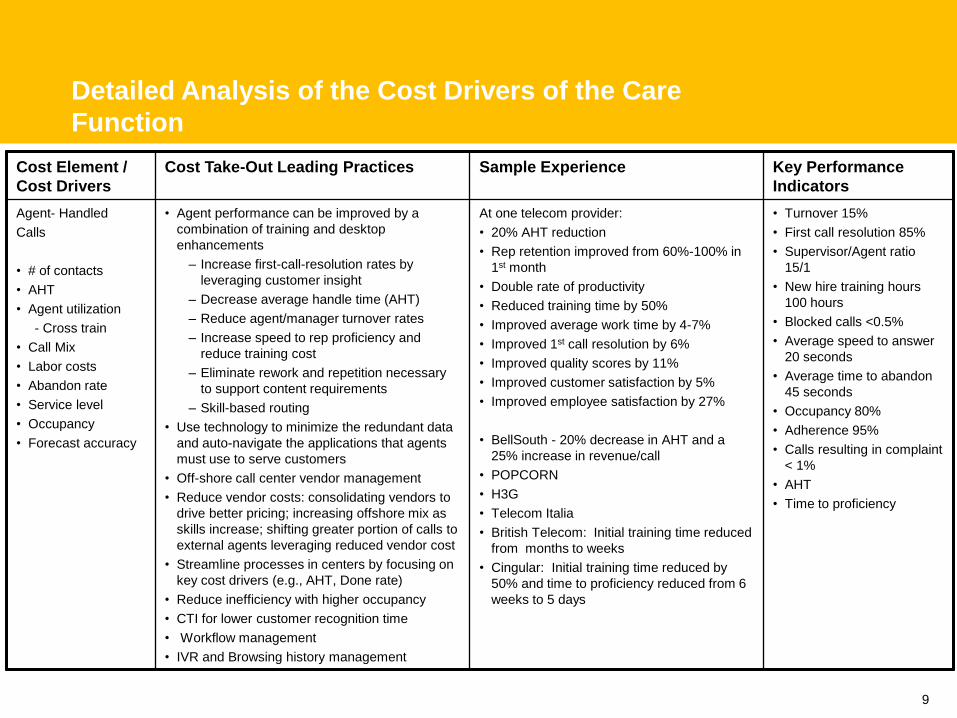

Detailed Analysis of the Cost Drivers of the Care

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Agent- Handled

Calls

• # of contacts

• AHT

• Agent utilization

- Cross train

• Call Mix

• Labor costs

• Abandon rate

• Service level

• Occupancy

• Forecast accuracy

• Agent performance can be improved by a

combination of training and desktop

enhancements

– Increase first-call-resolution rates by

leveraging customer insight

– Decrease average handle time (AHT)

– Reduce agent/manager turnover rates

– Increase speed to rep proficiency and

reduce training cost

– Eliminate rework and repetition necessary

to support content requirements

– Skill-based routing

• Use technology to minimize the redundant data

and auto-navigate the applications that agents

must use to serve customers

• Off-shore call center vendor management

• Reduce vendor costs: consolidating vendors to

drive better pricing; increasing offshore mix as

skills increase; shifting greater portion of calls to

external agents leveraging reduced vendor cost

• Streamline processes in centers by focusing on

key cost drivers (e.g., AHT, Done rate)

• Reduce inefficiency with higher occupancy

• CTI for lower customer recognition time

• Workflow management

• IVR and Browsing history management

At one telecom provider:

• 20% AHT reduction

• Rep retention improved from 60%-100% in

1st month

• Double rate of productivity

• Reduced training time by 50%

• Improved average work time by 4-7%

• Improved 1st call resolution by 6%

• Improved quality scores by 11%

• Improved customer satisfaction by 5%

• Improved employee satisfaction by 27%

• BellSouth - 20% decrease in AHT and a

25% increase in revenue/call

• POPCORN

• H3G

• Telecom Italia

• British Telecom: Initial training time reduced

from months to weeks

• Cingular: Initial training time reduced by

50% and time to proficiency reduced from 6

weeks to 5 days

• Turnover 15%

• First call resolution 85%

• Supervisor/Agent ratio

15/1

• New hire training hours

100 hours

• Blocked calls <0.5%

• Average speed to answer

20 seconds

• Average time to abandon

45 seconds

• Occupancy 80%

• Adherence 95%

• Calls resulting in complaint

< 1%

• AHT

• Time to proficiency

10

Detailed Analysis of the Cost Drivers of the Care

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Applications

Maintenance

Operations Support

• # of applications

• # of locations, sites,

and geographies

• # of employees

• # of offers

• Regulations

• Rationalize applications and associated overhead

• Rationalize call placement strategy to drive lower cost

while maintain customer satisfaction

• Implement hosted applications (i.e. salesforce.com)

• Application outsourcing

• Training, simulation, forecasting, & training the trainer

• BellSouth (AO)

–Outsourcing a full range of

applications software

development and maintenance

functions

–Covering a range of

information technology (IT)

applications including customer

care, network, billing,

marketing, etc. that support

BellSouth's local and Internet-

based communications

services to residential and

business customers in the US

Repair/Tech Services

(Face to Face)

• Company owned retail

vs. 3rd party

• AHT

• Labor costs

• Agent utilization

• Quality hardware and

network

• Reverse logistics

• Use business simulation for training

• Understand reasons for repair to address root-cause

of the repair visits

• Self-serve and self-diagnostics (including tech

service/bill payment kiosks in locations other than

company stores, device management)

• Enable store reps to answer care calls in stores

• Use cross-training to manage overflow from each

channel

• Incent mail in reverse logistics

- Dis-incent customers to go into store with reduced

hours

• Cingular POS

• Verizon

• Qwest

• Sprint Nextel

11

Detailed Analysis of the Cost Drivers of the Care

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

eMail (agent handled)

• # of contacts

• AHT

• Labor cost

• Agent utilization

• Service level

• Auto suggestion

settings

• Auto routing

• High propensity to outsource (no accent issues,

language barriers, or time zone issues; easily

distributed, natural filler work, non-real-time)

• Cross-train and gain efficiency through tools

• Use insight to achieve higher first contact resolution

%s

• Implement efficiency tools (i.e., agent can type

question into web or knowledge base to get pre-

scanned answers automatically sent back to

customers)

• Customer enabled case creation

• Earthlink

• H3G

• Telecom Italia

eChat

• Number of contacts

• AHT

• Labor cost

• Agent utilization

• Cross-train

• Abandon rates

• Simultaneous chats

• High propensity to outsource (no accent issues,

language barriers, or time zone issues; easily

distributed, natural filler work, non-real-time)

• Cross-train and gain efficiency through tools

• Use insight to achieve higher first contact resolution

%s

• Implement efficiency tools (i.e., agent can type

question into web or knowledge base to get pre-

canned answers automatically sent back to

customers)

• Intelligent routing

• Page pushing and collaboration tools

• Customer enabled case creation

• AOL eChat

– Workforce management not to

exceed two simultaneous chats

– Reduce chat volume and volume

to contact center

– Reduce billing contacts

redirected to phone

– Implemented frequently used

sayings

12

The Billing function encompasses the systems

and operations responsible for physical and

electronic processing, presentment and payment

— Definition —

• Billing Systems

– Biller

– Message Processing Systems

– EBPP Systems

– Remittance Processing Systems

– Management Systems

• Billing Operations

– Return Mail

– Message Processing

– Bill Rendering

– Billing Support Centers

– Remittance Processing/ Cash Application

• Printed Bill costs

– Include mail, presentment, and postage

• Greater complexity of voice services, data services and handsets making billing more complex

• Billing accuracy is a key element of the CRM cost structure

– 30-40% of customer care calls are related to billing

• Adoption of EBPP/ABP will significantly impact the billing cost structure

– By 2010, 52% of online households will pay bills online: a five-year increase of 75% from 2005. This amounts to over 47 million households in the US alone (Forrester Forecast)

– The average large company sending invoices to consumers via e-billing can save about 55 cents per invoice (Gartner)

• Greater integration between CRM, EBPP, and web-based self-service

• In software, shift from customized to standardized solutions, elimination of distinction between prepaid and postpaid customers, and increasing scope of functionality along value chain

• Billing accuracy

• # of bill cycles

• # of customers

• # of instances

• EBPP utilization

• Platform integration

• Electronic processing utilization

Billing includes: Key Cost KPIs:

CCPU – Billing

• Credit & Collections

– Quality level of credit approvals directly

impact Net Bad Debt

• Sales Operations

– Postpaid vs prepaid mix each have a

different billing cost structure

• Retention / Marketing

– Incentives (discounts) can complicate

Billing calculations and processing

– New product definitions and customer

plans require re-configuring processes to

ensure accurate billing

— Cost Reduction Trends —

— Functional Interdependencies —

13

• # of applications

• # of instances

• # of physical and logical markets

• # of bill cycles

• Complexity of architecture

• # /mix locations/sites/geographies

• # of employees:

• Testing and defect solving (H3G)

• CRM – Billing systems alignment

• # or % manual processing /automated

calculation processing

The Billing function decomposes into various levers

driving the overall cost of the operation.

Billing

Frequency

Billing

Calculation

Processing

Billing

Systems Application -

Maintenance

Operations

Support

Billing Operations

Presentment

Electronic Paper

Payment

Physical Electronic

Automated Pre-

authorized

One time

(single) TXIn PersonPayment

Consolidator

Check

Processing

• # of bills per year

• PC / web

• Mobile Handset

• Compensation

Costs

Postpaid Prepaid

PaymentPresentment Real Time

rating and

billing

• Content

• Messaging

• Voice

• Video

• Streaming

Recharge

• Electronic

• Physical

• PC / Web

OtherDebit

Card

Credit

Card

Web Kiosk Bank/ATM Other

Payment check and Consolidator

• PC / web

• Mobile Handset

Electronic

Cost drivers are in Blue

14

Detailed Analysis of the Cost Drivers of the Billing

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Frequency

• # of billing cycles

• # of customers

• Bill cycle optimization - trade off costs with increased load

to customer service and flexibility requirements with

customers

• Bill market optimization - trade off # of instances with IT

capacity, # of cycles, and market demands

• Balance the cost of bill creation and remittance processing

with impact on cash flow

• Potential impact: 50 FTEs

• Cingular cycle optimization

• WIND - implemented CSG/BP

real-time billing platform that

calculates rates and issues

bills for all services (mobile,

wireline, internet)

Application

Maintenance

Operations Support

• # of applications

• # of instances

• # of physical and

logical markets

• Complexity of

architecture

• # /mix

locations/sites/geogr

aphies

• # of employees

• Software

Development

Lifecycle

• Develop application architecture and design that aligns to

business strategy of optimal billing cycles and instances

• Application rationalization by finding synergies and

eliminating HW / SW through conversions and archiving

• Consolidate application software providers to reduce

diversity of applications and associated costs such as IT

maintenance and supporting headcount

• Develop business organization strategy for physical and

logical markets based on customer demand

• Storage rationalization to effectively optimize across

storage hardware

• Create application layer to get any data, any time,

anywhere to increase effectiveness of reporting

- Elimination of duplicate data

- Drive self service reporting

- Effective access to information reduces development

costs

• Data warehousing

• Albacom Billing Application

Maintenance - reduction of

billing backlog; ability to face

current growth; operation costs

optimization; treasury

optimization

• BellSouth

• ATL

• Cingular Billing Consolidation

15

Cost Element /

Cost Drivers

Cost Take-Out Leading

Practices

Sample Experience Key Performance

Indicators

Billing operations

• # of bill cycles

• Compensation

Costs

• # of employees

• Data retention and

archiving

• Software

Development

Lifecycle efficiency

• Technology

infrastrucutre

• PPE, power, etc..

• # of customers

• Assess SDLC to find gaps in efficiency

of doing development and testing

before production

• Organization workforce optimization to

align to future processes and # of bill

cycles

• Conduct process assessment for the

cost to automate vs headcount costs

for manual functions

• Design organization structure to

support 'to be' process which depends

on other CRM decisions such as rate

plans and data retention strategy

• Outsourcing to a third party is one

highly effective option to transform

billing operations:

- Third party services provider assumes

responsibility for operational functions

and improve performance through

business process realignment

initiatives

- Services provider guarantees

business results that address wireless

carrier’s specific needs

- Blended workforce of offshore /

onshore mix

• US Wireless provider recovered/accelerated a

significant amount of revenue

- Recovered billable Call Detail Records (CDRs):

US$90-110k per month

- 20-25% fewer CDR errors daily: US$960k per

month

- Improved CDR error correction: US$270-290k

per month

- Reduced backlog of rejected invoices: US$6-7m

• Malaysian mobile service operator retail/customer

billing project involved bottom line revenue

recovery and increased operational efficiency

– Revenue recovery through billing of 4m error

CDRs (worth about RM2 million) after 2 months

and subsequently timely resolution of ongoing

CDR errors

• Malaysian mobile service operator interconnect

billing project delivered

- Improved ICS revenue billed (revenue recovery)

by >30%

- Reduction in interconnect cost (over-charging

by other Telcos) by more than 5%

- Increased system performance and efficiency

(reduced processing time by >50%

Detailed Analysis of the Cost Drivers of the Billing

Function

16

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Electronic

Presentment

• Cost to provide

through: PC,

Mobile handset,

• Kiosks in stores

• Connectivity

• Support for HW /

SW maintenance

• A key differentiator will be providing incentive to eliminate paper

bills, otherwise benefit of electronic enablement will not be fully

realized

• Enable EBPP/ABP as the primary presentment and payment

channel for select customer segments.

• Drive adoption by incorporating and marketing EBPP as an

element of select offers (e.g. DSL).

• Partner with banks and other consolidators to co-market ABP

capabilities.

• Utilize leading software platforms and service provider

capabilities to accelerate capability development. Top EBPP

vendors include: Checkfree (BlueGill), Avolent (Just in Time),

eDocs (owned by Oracle)

• Reduce costs by shifting to a service provider (ASP model) to

leverage the provider’s economies of scale.

• Tightly integrate with the broader eCRM and traditional customer

operations capabilities to maintain an integrated customer

experience:

- Tightly integrate with eCare offers to manage Bill Inquiry

through the electronic channel

- Tightly integrate with eSales offer to upsell and cross-sell

through the electronic channel

• Drive customer adoption to the lower cost ABP channel by

incorporating electronic payment mechanisms in select offers.

• Utilize payment processing gateways to enable on-line payment.

- For global needs, focus on foreign-currency support

capabilities of leading vendors

• H3G EBP- built and delivered

EBP system in Sweden with

optimized invoicing database

• Cesky Telecom – required by

government to provide bill

over the Internet, developed

custom solution based on

J2EE technologies and

developed interfaces in

Ensemble, Geneva, and

Siebel

• Telenor – EBPP and

customer letter

• Verizon Advanced Data eBill

– developed, and operated an

end-to-end billing, taxation,

EBP, and dispute

reconciliation for host ISP

account

- Reduced average customer

balance outstanding from 90

to 33 days

• - Average receivables aging

>60 days reduced from 85%

to 8%

• - Cost of billing and

settlements per subscriber

<$0.15 per subscriber

Detailed Analysis of the Cost Drivers of the Billing

Function

17

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample

Experience

Key Performance

Indicators

Paper

Presentment

• # customers that

receive paper bill

• Print operations

• Postage scale

• Consolidate/outsource bill print operations contracts to scale-based

providers to optimize unit cost and secure variable pricing

- Utilize the highly specialized, non-occupational workforce of most

outsourcers

- Implement variable pricing that outsourcers can secure with their

vendors (e.g., high-speed printer manufacturers)

- Lock in contracted bill print rates for the life of the contract

• Postage consolidation to negotiate a preferential postage rate through

scale

• Optimize the invoice layout to balance bill clarity with consumption of

space to reduce paper and postage costs

• Utilize color print on the invoice to reduce the number of bill inquiries

Revenue uplift

• Take advantage of the physical interaction with customer for advertising

purposes.

• Leverage insight driven messaging for uplift

Detailed Analysis of the Cost Drivers of the Billing

Function

18

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample

Experience

Key Performance

Indicators

Payment (Remittance

Processing Mix)

• Physical

• Electronic

• Consolidate remittance processing contracts to a national provider or BPO

to optimize rate structure for processing

- Utilize the provider’s nationwide footprint to reduce mail float

- Utilize the highly specialized, non-occupational workforce of most

outsourcers

• Invest in advanced optical character recognition technology:

- Improve the throughput of standard remittance processing

- Reduce the number and cost of exception processing

• Align processes with emerging ACH standards for check clearing to

reduce processing costs

Order of lowest Processing Cost

• Debit

• Credit

• Other methods that involve people processes

• H3G: Review of

the

commissioning

area

processes/proce

dures (passive

invoicing vs

vendors – e-

incent platform)

• Check cost: 35-45 cents

/ check

• Debit cost: 0.001 cent

• Credit cost: 2-3% charge

Prepaid

• Distribution

• Revenue

assurance / theft

control

• # of customers

• Convergent pre/post payment to enable product bundling

- Apply discounts based on volume

- Integrate back-office systems to network

Recharge

• Drive physical recharge to electronic recharge to reduce costs associated

with activation, printing cards, and distribution

• Improve security with activation

• Shared distribution with vendors

• Retail process assessment

• 3PL for card inventory

• Verizon Wireless

Detailed Analysis of the Cost Drivers of the Billing

Function

19

The Credit and Collections function typically

manages credit policy, collections call centers,

fraud, and revenue assurance.

— Definition —

• Collections Call Centers

• Credit Policy and Scoring

• Pre-delinquency Usage Mgt

• Fraud Mgt

• Contra Revenue Mgt

• Application Development and Maintenance

– Predictive Dialer/IVR/CAD

– Credit Scoring Systems

– Collections Mgt and Workflow Systems

• Carriers typically operate in a reactive mode to collection problems

• Credit policy directly impacts churn in 3-12 months

• Prepaid products are aggressively being marketed to risky customer segments

• Faced with a saturated market, Net Bad Debt is likely to rise as carriers pursue less credit worthy customers

• Outsourcing (process, application and infrastructure) adoption is growing in the credit and collections process area

• Third party collection agencies are specializing in specific portfolio segments to enhance their recoveries

• Working capital mgt (DSO) is a priority for CFO as free cash flow is a key driver to shareholder value

• Technology enablers are continuing to grow more sophisticated allowing for increased effectiveness in the credit & collections processes while also

improving efficiency

• Percent of Net Bad Debt

• Delinquency Rate

• Acquisitions with credit policy

• C&C Expense as a percent of Revenue

• # of Employees per Billion in Revenue

• Loaded Payroll per Employee

• % of New Applications declined due to credit policy

Credit & Collections Includes: Key Cost KPIs:

CCPU G&A - Credit & Collections

• Billing

– Complicated or incorrect bills can disincent

customers to pay

• Sales Operations

– The postpaid vs prepaid mix influences the

workload of the credit department

– Targeting the customer profile that will pay

on time will reduce C&C expense

— Cost Reduction Trends —

— Functional Interdependencies —

20

G&A Credit &

Collections

Application

Maintenance

Operations Support

Credit &

Collections

Cost

The G&A Credit & Collections function decomposes

into various levers driving the overall cost of the

operation

Value of

Uncollectible

Bad Debt Credit

ScoringAdjustments

Inbound

IVR

Self-Service

Agent• # of calls

• AHT

• Agent

utilization

- Cross train

• Call Mix

• Internal vs.

External reps

• Labor costs

• Abandon rate

• Service level

Outbound

Mail Outs

• # of letters

• cost per

letter

Agent

• # of contacts

• Abandon

• Completes

• % Automated

Capability

• Redirects

• Completes

vs.

Voicemail

• AHT

• # Calls

• # Contacts • Desktop care

• Offshore development

Credit &

Collection

Strategy &

Management

Fraud &

Usage

Management

Collections

ManagementCorrections

to Charges

Unbillables

Write-offs

(Net of Tax)

Recoveries Change in

Reserve

Requirement

Fraud

Revenue

Assurance

NBD Is a result of the effectiveness of

the cost investment. In telcos, Credit

and Collections “cost” investment should

be viewed as a value creation

opportunity vs a pure cost saving target.

Web Self

Service

• # of contacts

• Ease of Use /

Service Level

Email IVR

• # of contacts

• AHT

• Labor cost1

• Outsourcing

• Agent utilization

• Cross train

• Service level

• Predictive

Dialer

Cost drivers are in Blue

21

Detailed Analysis of the Cost Drivers of the Credit

& Collections Function

Cost Element /

Cost Drivers

Cost Take-Out Leading

Practices

Sample Experience Key Performance

Indicators

Credit and

Collections

Strategy and Mgt

• Overall strategy

• FTEs

• Overall portfolio

performance

• Optimize the strategy of the Credit

and Collection Processes to

improve effectiveness and

efficiencies while driving bottom

line EBIT improvement

• Increase span of control to

leadership team to drive down

headcount

• Create value with management

team by focusing on effectiveness

and efficiency

• German Wireless Provider -- consolidated financial

operations into two centers

– Over $40m of receivables collected and Days Sales

Outstanding (DSO) reduced by 30% within the first year

– AR payback in 14 months

– Project savings: $144.7m from the Go-To-Market

proposition and $20.3m royalty payments

• SBC: Advanced Collections Environment - Defined future

operating environment for the C&C function

• North-American wireless company received a list of 35

improvement opportunities - a 10% reduction in workforce

• US Based Telecom - Identified and defined DSO reduction

opportunities of 10%-15%, resulting in an annual savings of

approximately $25m by improving invoicing cycle review

• NBD

• Cost per Customer

• Cost per Dollar

Collected

• AR as a % of Sales

• DSO

Credit Scoring

• Cost of scores/ risk

data

• Effectiveness of

data usage

• Supporting

technology

enablers

• Optimize the use of credit and

related capabilities to effectively

manage the risk of delinquent

payment and write-off

• Reduce cost per score by moving

from a multi-bureau to a single

bureau

• Identify repetitive debtor to

minimize credit scoring required

• Optimize the number of accounts

outside the credit agency

• Increase percentage of prepaid/risk

mitigating customers

• Cost per Score

• Effectiveness of the

scoring model

• Repetitive debtor

identification ratio

• Number of accounts

outside desired credit

tolerances

• Acceptance percentage

of prepaid/risk mitigating

offers

22

Detailed Analysis of the Cost Drivers of the Credit

& Collections Function

Cost Element /

Cost Drivers

Cost Take-Out Leading

Practices

Sample Experience Key Performance

Indicators

Fraud and Usage

Management

• Fraud

• Revenue leakage

• Usage levels

• Supporting technology

enablers

• Fraud mitigation and usage

monitoring and management

capabilties

• Implement a skip tracing

solution

• Implement fraud modelling

techniques to increase early

detection

• Implement limit and usage

management techniques, such

as prepaid accounts

• Malaysian mobile service operator stabilized and operated

day-to-day Fraud Management Operations

- Detected mobile prepaid fraud cases by internal staff

with revenue loss of more than RM10m per year

- Achieved post fraud savings of about RM33m per year

(reduced the RM exposure per fraudulent account by

more than 75%)

• Fraud component of NBD

• Unbilled/Unbillable

revenue

• "Never Pay Accounts &

Dollars as a % of Write-

offs

• Avg Balance per Never

Pay Account

Collections Management

• Collector sourcing

• Workplace location

• Method on contact -

inbound and outbound

• First party vs third

party performance

• Supporting technology

enablers

• Effectively balance the

investment in operating expense

to improve efficiencies while

improving the effectiveness of

the collections management

processes

• In most cases collections

effectiveness should be focused

on as a priority to drive reduced

NBD, customer churn, DSO

reduction, improve revenue and

reduce credit risk/fraud

• US-based Global Telecoms Provider -- Business Process

Outsourcing delivered 40% reduction in operating costs

– Collected over $60m in overdue receivables

– Reduced Days Sales Outstanding by 30% in the first

four months and sustained the improved DSO

– Consistent achievement of 99% service levels on

accuracy of cash processing and resolution of

misapplied payments prior to next invoice cycle

• German Wireless Provider

– Consolidate financial operations into two centers

– Over $40m of receivables collected and DSO reduced

by 30% within the first year

– AR payback in 14 months

– Project savings: $144.7m from the Go-To-Market

proposition and $20.3m royalty payments

• Inbound/outbound calls

per collector

Average handle and

answer time

• IVR completion

percentage

23

Detailed Analysis of the Cost Drivers of the Credit

& Collections Function

Cost Element /

Cost Drivers

Cost Take-Out

Leading Practices

Sample Experience Key Performance

Indicators

Net Bad Debt (NBD)

• Write-offs (net of

tax)

• Recoveries

• Change in reserve

requirements

• Affiliate allocation

• Driving efficiency and

effectiveness into the

strategy, credit scoring,

fraud, usage mgt and

collection management

processes will yield

improvements in NBD

• North-America-Based Wireless Company

– Identified opportunities provided a 3-year reduction in NBD

and DSO of over $40m

• US-based telecoms company received deliverables outlining

initiatives estimated to provide annual benefits of $118-189m

– Identified and defined Net Bad Debt reduction opportunities

of 7%-10%, resulting in a annual savings of approximately

$64m

– Identified and defined operating expense reduction

opportunities of 8%-18%, resulting in an annual savings of

approximately $26m

– Annual margin lift of $10-20m

• Major European Wireless Operator received bad debt

management assistance leading to >30% increase in the bad

debt amount collected after the roll-out of the new bad debt

capability

• Written Off Accounts as a

% of total accounts

• Average Balance per

Write-off Account

• Average Tenure of Written

off accounts

Application

Development &

Maintenance

• Desktop applications

• Development

sourcing

• Supporting

technology enablers

• Optimize the technology

enablers supporting the

credit and collections

processes

• Outsource to a lower cost

location

• Disparate, common

shared systems

• Implement hosting

solutions where applicable

• North-America-Based Wireless Company

– Installed treatment optimization modifications expected to

increase dollars collected by 10%

24

Detailed Analysis of the Cost Drivers of the Credit

& Collections Function

Cost Element /

Cost Drivers

Cost Take-Out

Leading Practices

Sample Experience Key Performance

Indicators

Revenue

Assurance

• Revenue

leakage

• Number of

personnel

• Level of system

complexity

• Level of control

• Number of

manual

processes

• Optimize the

processes around

revenue reporting

and reduce the

process cost to

achieve the same or

better results

• Implement an

integrated order 2

cash end-to-end

process with

appropriate

supporting people,

process, and

technology

• US Wireless Provider

– Identified out-collect file processing gaps : US$3-

4m

• US Based Telecom

– Identified Contra-Revenue reduction opportunity

of 7%-10%, resulting in an annual savings of

approximately $24m

• US wireless joint-venture developed airtime RA

process flows, control points and business

requirements as well as detailed procedures for

reconciling third party vendor bills

– US$1500 per month benefit achieved by adding

rigor to the process of reconciling third party

provider bills

• North American Based Telecom (Bell Canada)

– Received a list of 35 improvement opportunities

– Identified opportunities provided a 3-year

reduction in NBD and DSO of over $40M and a

10% reduction in workforce

25

NOTE: (1) Internal voice and data network used to support company operations only -- does not include core wireless network used to transport customer voice and data traffic

Information Technology includes all relevant labor,

software, hardware, network communications, and

facilities expenditures supporting wireless operations

• Percent on time delivery

• % in Budget delivery

• Average cost / person

• Mean time to repair

• Availability

In Scope: Key Cost KPIs:

CCPU G&A - Information Technology

• Labor – internal and external (contract

labor / external service providers)

Scope includes the following expenses

required to support Application Development

/ Maintenance and Production / Operations,

IT Management, IT Strategy and Account

Management.

• Increased pressure on IT to respond to rapidly changing business needs related to supporting more products, bundles (ordering / billing / product dev/intro), customer targeting, digital rights management

– Wireline: IPTV, VoIP

– Wireless: High speed data, music, gaming

• Business moving to simplify / rationalize product structure as new products come on-line

• The entry of new, lower cost players (VoIP, Wireless (including slim MVNOs and UMTS pure-plays) putting pressure on incumbents with expensive imbedded base to consolidate

– Wireline / wireless mergers in Europe– Rural “pure play” consolidation in US

• IT looking to upgrade primary legacy applications to IP-centric, COTS for Next-Gen billing, ordering, provisioning, etc.

• Renewed focus on “speed to market” within IT leading to co-sourcing, transformation of development capabilities

• Application architecture simplification / rationalization to increase responsiveness to business changes

• Application / infrastructure consolidation and rationalization post-merger / acquisition

• Software – Licenses,

maintenance expense, one time

fees, amortization/depreciation

(applications and operating

systems)

• Hardware – Leases and

maintenance fees for desktops,

servers, storage, and peripheral

• Network/Communications 1

– Voice and Data

• Facilities

• Other (e.g. one-time M&A

costs)

— Definition —

— Cost Trends — — IT Response —

26

The G&A Information Technology function

decomposes into various levers driving the overall

cost of the operation

G&A IT

Application

Development &

Maintenance 1

Production

Operations

IT Operations

(OpEx)

New Investment

(CapEx)

NOTES: (1) Includes all Development and Testing activities; (2) Includes Facilities and other one-time expenses (e.g. M&A costs); (3) Internal voice

and data network used to support company operations only -- does not include core wireless network used to transport customer voice and data

traffic

Hardware

Software

People

Governance

Mainframe

Operations &

Support

Server

Operations &

Support

Network

Operations &

Support 3

Desktop & End

User Support

Out of scope

IT

AdminR&D

Architecture

Strategy

Program,

Release,

Project

Mgmt

Account

Mgmt/

Service Mgmt

Other 2

Methods /

Processes

• Hardware right sizing and consolidation

• Software rationalization, optimization

• People – pyramid, cost, structure, skills / competency

• Governance – Strategic architecture, Business Alignment, Performance Management,

Roles/Responsibilities

• Methods / Processes – Leading practices, Continuous Improvement, Commonly defined / used

27

Detailed Analysis of the Cost Drivers of the IT

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Application

Development &

Maintenance (ADM)

• People (Cost,

Structure, HP)

• Technology

(Infrastructure &

Tools)

• Methods &

Processes (Usage

& C.I.)

• Governance

(Roles/Responsibilit

y, Alignment &

Port.Mgmt, Svc.

Level Management)

• For Development or Maintenance - IT Transformation

Diagnostic / Assessment of current spend (strategic

alignment, discretionary/non-discretionary), use of process,

application portfolio, infrastructure, etc.) leading to:

1. Reduce cost through

• a. Outsourcing portions of the Production Support, Break/Fix

code, Project/Release Detailed Design, Code, Test and

Deployment tasks to lower cost offshore resources

• b. Analysis of current organization structure / pyramid and

adjusting to leading practices

• c. Application Rationalization / Optimization - Rationalize,

Consolidate and Re-platform custom, legacy software/

platforms to less costly COTS-based solutions

2. Increase productivity through:

• a. Adoption / Implementation of Project Delivery Methods

replacing current client methods

• b. Assess culture related to use of standard methods,

standard processes and operational metrics to guide

delivery excellence; implement Human Performance

Offerings / Balanced Scorecard to shift behavior to common

process and metrics-based execution.

• c. Assessment of current Development / Maintenance

related skills with recommendations to address skill issues

• d. Adoption, Institutionalized, and Industrialized "Leading

Practices" across Maintenance / Development related

Processes; e.g. Requirements Management, Project

Management, Change Management, Release Management)

• 20-30% cost reduction, 20%

increase in productivity

(Orange,UK)

• 20-30% cost reduction, 20%

productivity increase (Telefonica

Argentina)

• 10-15% cost reduction (Telus)

• 15% Cost Reduction (One2One)

• 23% savings on outsourced

labor for development /

maintenance (AT&T Consumer)

• 25-30% Cost reduction / 20%

increased productivity (KPN

Netherlands)

TYPICAL SAVINGS:

• Application Rationalization - 15-

30% cost reduction (Savings

comes from: Labor-50-

75%,Facilities 10-35%,

Hardware 0-15%, Software 0-

15%)

• ADM Outsourcing - 20-35% cost

reduction from labor savings

28

Detailed Analysis of the Cost Drivers of the IT

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading

Practices

Sample Experience Key Performance

Indicators

Production Operations

• Mainframe Operations &

Support

• Server Operations & Support

• Network Operations & Support

• Desktop & End User Support-

Systems and Network Admin

(Voice and Data)

• Outsourcing - Shift portions of

operations, support, admin. through

lower cost labor

• Infrastructure Consolidation -

Rationalize, Consolidate Systems

(MF/Servers/Desktop Architecture,

Internal voice/data Network) and

associated storage, operating systems,

data bases, support staff and facilities)

• Process Optimization - Assess current

process execution vs. leading

practices; Adopt, Institutionalize, and

Industrialize ITIL based "Leading

Practices" across Operations, e.g.

Problem, Change and Configuration

Management, Vendor Management

• 50% Reduction in unplanned systems

downtime (Orange UK)

• 44% reduced downtime (Vodafone)

• 20% Reduced Operations Expense -

One2One

• 10-20% Cost Reduction from Supplier

Rationalization (One2One)

• 10-20% Cost Reduction Operations (KPN,

The Netherlands)

TYPICAL SAVINGS:

• Infrastructure Consolidation - 20-40% cost

reduction (Sys Platforms 20-35%,

Enterprise enabling infrastructure - 20-

35%, Application Enabling Infrastructure -

15-25%, Security Infrastructure - 5-10%,

Ops Management - 15-30%)

R&D & Architecture Strategy

• People (Cost, Structure, HP)

• Technology

(Infrastructure&Tools)

• Methods & Processes (Usage

& C.I.)

• Governance

(Roles/Responsibility,

Alignment&Port.Mgmt, Svc.

Level Management)

• Develop long term IT application /

infrastructure architectures and

migration planning to move to "next

generation" platforms

• Develop IT strategy, IT Organization

Design, IT Governance Design

• Telecom Italia - move to next generation

IP based platform

29

Detailed Analysis of the Cost Drivers of the IT

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading

Practices

Sample Experience Key Performance

Indicators

Program, Release,

& Project Management

• People (Cost, Structure, HP)

• Technology (Infrastructure &

Tools)

• Methods & Processes (Usage

& C.I.)

• Governance (Roles/Respon,

Alignment & Port.Mgmt, Svc.

Level Management)

• Process Optimization - Institutionalize /

Industrialize "Leading Practices" within

Release Management, Program/Project

Management

• Improve skills of existing client Program

/ Project Managers

• Improved governance and tracking of

requirements change management

• Implementation of standard tools to

measure and reinforce governance,

project management, change

management processes

• Implement and integrate

supply/demand balancing and resource

management

• 20-35% increased

productivity, improved

percent of commitments

met on schedule and

increased speed of

throughput in development

center

30

Detailed Analysis of the Cost Drivers of the IT

Function

Cost Element / Cost

Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Account Management &

Service Management

• People (Cost, Structure,

HP)

• Technology

(Infrastructure & Tools)

• Methods & Processes

(Usage & C.I.)

• Governance

(Roles/Responsibility,

Alignment&Port.Mgmt,

Svc. Level Management)

• Define IT Services, service levels and costs

associated with differentiated service levels

• Implement Demand Management processes to

control levels of low value / non -strategic

discretionary spend

• Service Level Management, Account

Management, Project Initiation)

• Refine and Implement rigorous governance

related to change management

• 25-30% Cost Reduction / 20%

increased productivity - KPN, The

Netherlands

TYPICAL SAVINGS:

• Demand Management / Resource

Management: Up to 20% budget

reduction from increased

workforce utilization

IT Management (CIO, HR,

Finance, Risk Mgt)

• People (Cost, Structure,

HP)

• Technology

(Infrastructure & Tools)

• Methods & Processes

(Usage & C.I.)

• Governance

(Roles/Responsibility,

Alignment&Port.Mgmt,

Svc. Level Management)

• IT Transformation Assessment re:-

• HR: hiring / retention / human performance /

training / career path development aligned to IT

Strategy, Resource Management, Demand

Management and sourcing

• Performance Management - Implementation of

"Leading Processes" and automation for a

balanced scorecard using integrated tools for

cost accounting, time reporting, charge back

mechanisms, performance reporting, etc.

• Vendor / Supplier Management - Consolidation of

number of suppliers/vendors and contracts to

leverage discounts, improve service levels and

reduce management expense

31

HR and Benefits Administration

• Companies are moving to outsource non-core HR transactional activities utilizing a shared service approach. Processes usually performed in a shared service model include: Recruiting, Staffing, Performance Management, Compensation, Benefits, and Payroll.

• Internal HR resources now focus on areas with huge business impact: Human Capital Strategy, Leadership, Employee Engagement, Talent Management, Workforce Performance and Knowledge Management.

Training

• Sales, Marketing, and Customer Care agents require continual training as product lines and complexity increase

• Integrating Workplace Performance Solutions which continually keep employees engaged and up-to-speed on products, service, and issues by using learning “nuggets” is a key trend.

Human Resources includes both core HR company-

wide processes such as benefits admin, and HR

processes in specific functional areas such as

retention and training

— Definition —

•Staffing and Support

– Employee Lifecycle: Recruiting, hiring, talent management, staffing, exiting, and alumni relations; Employee performance evaluation/management; Maintenance of employee information; Compensation & Benefits; Time & Attendance; Payroll

•Employee Management & Relations

– Employee communications; Grievance management; Employee services; Disciplinary activities

•Training, Development, and Knowledge Management (Internal)

– Development and delivery including online, instructor-led, and virtual aimed at employee development

– Knowledge Management

•Customer/Channel Partner Training

– Development and delivery including online, instructor-led, and virtual aimed at customer/partner development

•Vendor Management

•Application Development and Maintenance

– HR, Training, Benefits Administration, and KM Systems

• Cost of employee acquisition

• HR cost per employee served

• Cost of training each employee (time & expense to reach competency)

• Retention Rate of Key Talent

HR Includes: Key Cost KPIs:

CCPU G&A - Human Resources

• Care

– Labor issues (e.g., union) can strain the HR lifecycle management

– Offshore/Onshore Blend will affect HR support costs

• Marketing

– Rate of growth and new product introduction will affect hiring and training needs

• Sales Operations

– Proliferation of Outlets (Retail & Direct to Corporate) can increase HR expense and management required

— Cost Reduction Trends —

— Functional Interdependencies —

32

The G&A Human Resource function decomposes

into various levers driving the overall cost of the

operation

Risk

Management

Staffing &

Support

Training

Internal

Training

Customer/ Channel

Partner Training

Application

Development

& Maintenance

Benefits

Administration

G&A HR

- Training costs are part of loaded employee costs in each of the functional areas

• Desktop care

• HR ERP Solution

• Web-based Self-

Service

• Training Delivery

Technologies

• Learning

Management

System

• Performance

Workspace

Solutions

• % of Offshore

Development

• Talent Pipeline

Efficiency

• Retention

Rates

• % of

transactions

through self

service

• % of Online

Delivery

• # of Employees

• Retention Rate

• Time to Proficiency

• % of Online

Delivery

• # of Learners

• Sessions per Year

• Time to Proficiency

• % of Online

Delivery

• # of Learners

• Sessions per Year

• Time to Proficiency

• # of HR

Cases

Escalated

Cost drivers are in Blue

33

Detailed Analysis of the Cost Drivers of the HR

Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Staffing / Recruitment

• # Employees

• Retention Rate

• Growth Rate of Employee

Base

• Employee Segmentation

(locations, states,

countries)

• Frequency of Employee

Evaluation

• # of HRIS/ERP Systems

of Record

• Decrease cost to serve through the following

functions:

–Employee lifecycle: Recruiting, hiring, talent

mgt, staffing, exiting, and alumni relations

–Performance evaluation/management

–Maintenance of employee information

–Compensation & Benefit

–Time & Attendance

–Payroll

• Improve % of HR transactions that self served

• Decrease # of HR case escalation through

effective HR lifecycle management

• Achieve wage arbitrage and economies of scale

through global, multi-client service centers

• Standardize processes across areas, consolidate

vendors, and integrate with upstream and

downstream legacy systems

• Utilize the web to streamline benefits admin

• Seagate Technology LLC (Oracle HRMS)

–Improved employee productivity and

retention

–Reduced administrative/transactional HR

headcount by 30%

–Lowered HR transactional costs

–Increased global HR standardisation and

consistency

–Enhanced HR strategic focus and alignment

–Improved customer satisfaction with HR by

20%

–Reduced hiring costs and training/learning

costs

–Faster access to employee data

–Elimination of dual data entry

• Leading International Financial Services

Company (in-house HR Shared Services

implementation)

–4.5M HR cost reduction in one year

–reduced average costs per HR transaction

by 60%

– reduced number of processes by 40%;

–increased employee satisfaction by 50%

• Cost to serve per employee

• % of HR transactions that

are self-serviced

• Number of HR case

escalations

• Employee satisfaction

Employee Relations

• Employee #s

• Time to Competency by

Role

• Amount of Re-Training

required

• Cost of Delivery by

Medium (ILT vs online)

Costs to communicate and serve employees

includes: Employee communications, Grievance

management, Employee services, Disciplinary

activities, The number of "services" supplied to

employees (i.e. LifeWorks programs) will drive costs.

Also, process efficiency around disciplinary action

will also drive effectiveness.

• BT (Central helpdesk facility/web-based

solutions to deliver safety awareness)

– Absence reduced by 20%

• Number of employee

disciplinary cases

• Use of EAP programs per

1000 employees

• Communication Budget per

employee

34

Detailed Analysis of the Cost Drivers of the HR

Function

Cost Element / Cost

Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Training & Development

• Employee #s

• Time to Competency by

Role

• Amount of Re-Training

required

• Cost of Delivery by

Medium (ILT vs online)

• Create a rapidly scalable, customizable, and

low-cost means to develop and deliver training

to employees, channel partners and end

customers

• Consolidate and evaluate vendors for content

development and delivery.

• Incorporate strategic alignment and business

insight to better target content development

gaps

• Transform and shift instructor led course media

to less expensive, eLearning platforms

• Implement just-in-time embedded learning at

your desktop (real-time delivery of nuggets)

• Incorporate partner/customer insight to better

target content development and provide “just-in-

time” training.

• Deploy Knowledge Bases

• Ayava (centralization of admin to

Service Center)

– 30% reduction in training costs

• Training Costs per employee

• Number of employee

disciplinary cases

• Use of EAP programs per

1000 employees

• Communication Budget per

employee

Customer / Channel

Partner Training

• # of Partner/ Channel

Participants &

"Learners"

• Time to Competency

• Amount of Face Time

with each "Learner"

• BT (HRO)

– Migrated 29,000 instructor-led

safety training days to e-learning

– BT’s new learning capability

achieved ISO 9001 registration

• Number of employee

disciplinary cases

• Use of EAP programs per

1000 employees

• Communication Budget per

employee

Application Development

& Maintenance

•Desktop applications

•Self-Service vehicles

(web, kiosks, etc.)

•Offshore development

• Reduce costs by migrating portions of the ADM

offshore

• Re-platform custom, legacy software/ platforms

to less costly COTS-based solutions.

• FileNet (Comprehensive HRT)

– significantly enhanced reporting

capabilities

– faster and better-informed

decisions based upon quick

access to timely employee

information

– self-service capabilities boosted

employee satisfaction as they

streamlined operations and saved

costs

• Number of systems to

integrate

• Cost of ADM per man/year of

effort

35

Finance & Accounting includes processes such as

Accounting and Control, Financial Planning and Analysis,

Transaction Processing, Procurement, and other specialty

processes

— Cost Reduction Trends —

— Definition —

• Accounting & Control includes

– General & Cost Accounting

– GAAP/SEC/IAS Accounting

– Intercompany Accounting

– Consolidations/Eliminations

– Financial & Statutory Reporting

• Financial Planning & Analysis includes

– Strategic Planning, Budgeting, & Forecasting

– Enterprise Performance Management

– Profitability Reporting

• Transaction Processing includes

– AP/T&E; Fixed Asset Accounting; Project Accounting; Inventory Accounting; Payroll; Wholesale Credit, OM, BI, AR, Collection

• Center Of Excellence/Specialized Skills includes

– Tax; Treasury; Investor Relations; Risk Management; Finance Transformation

• Procurement– Vendors and Outside Agencies

• Sarbanes-Oxley and other control requirements have propelled the Finance and Accounting function to a top organizational priority

• Outsourcing is emerging as a means to significantly drive down costs for non-core functions by 20-40%

– Emergence of new low cost labor markets

– Maturity of business process outsourcing market

• ERP systems are not being fully utilized and run at only 26% of full capability (Hackett Group estimates)

• Emergence of Global Shared Services infrastructure

– Shared Services may reduce the cost of finance functions between by 10% - 30%

– Only 48% of companies (across industries) have implemented Shared Services

• F&A Expense as a Percent of Revenue (< 0.75% of revenue)

• Number of Employees per Billion in revenue (< 63 per Billion in revenue)

• Loaded payroll per Employee

• % Resource Allocation between Transaction Processing, Planning & Analysis, Compliance & Risk Management, and Management (no more than 50% focused on transaction processing)

• Days to perform close and report (4 days or less)

F&A Includes: Key Cost KPIs

CCPU G&A - Finance & Accounting

• Sales Operations

– Commission processing may be included in accounting

• SCM / Subsidies

– Sales and inventory levels place demands on the procurement and accounts payable

• Network

– Construction activity levels and movement of network components place demands on fixed asset and project accounting

• Billing/Care/C&C

– Timing of processing and interfaces with these functions to the General Ledger may impact performance and time to close

— Functional Interdependencies —

Trends indicate increasing significance of the Finance & Accounting function:

36

The Finance and Accounting function

decomposes into various levers driving the

overall cost of the operation

Financial Planning &

AnalysisAccounting &

Control

Application

Development

& Maintenance

GAAP/ SEC/ IAS Accounting

General & Cost Accounting

Financial & Statutory Reporting

Consolidations/ Eliminations

Inter-company Accounting

G&A Finance and Accounting1

Budgeting & Forecasting

Enterprise Performance Management

Channel/ Customer/ Product Profitability

Center Of

Excellence/

Specialized Skills

Tax

Treasury/Cash Management

Investor Relations

Risk Management

Finance Transformation

Strategic Planning

Transaction

Processing

Travel & Expense

Fixed Asset Accounting

Project Accounting

Accounts Payable

Inventory Accounting

Payroll

Wholesale Credit, OM, Billing, AR, Collections

Audit

Board/Audit Committee

• # of FTEs

• # of Entities

• # of Countries

• % Standardization of Processes

• Degree of Automation of Processes

• # of Financial Applications

• # of Transactions processed

Cost drivers are in Blue

• Desktop care

• Offshore development

Note: 1- Cost drivers are listed beneath G&A Finance and Accounting (F&A) because these drivers are common

for F&A’s major cost components.

37

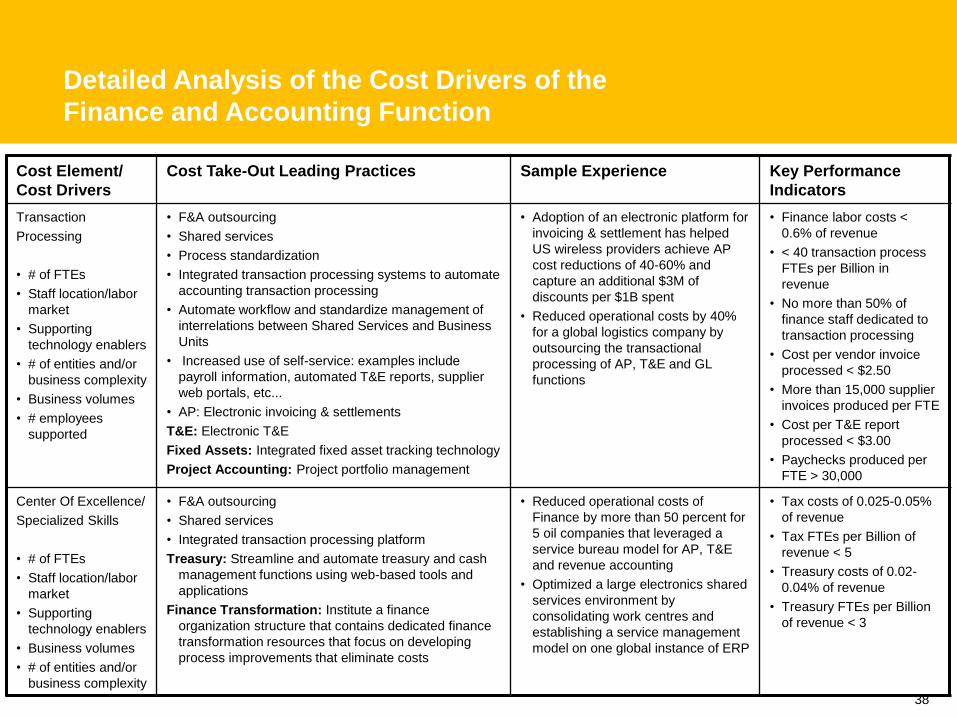

Detailed Analysis of the Cost Drivers of the

Finance and Accounting Function

Cost Element /

Cost Drivers

Cost Take-Out Leading Practices Sample Experience Key Performance

Indicators

Accounting & Control

• # of FTEs

• Staff location/labor market

• Supporting tech. enablers

• Business volumes

• # of entities and/or business

complexity

• F&A outsourcing

• Shared services

• Process standardization

• Integrated transaction processing systems to automate accounting

transaction processing

• Streamlined close cycle and reduction in manual close effort

• Integrated enterprise performance mgmt. platform

• At a global telecom,

reduced the close cycle

time by 50% through a

streamlined process

• Monthly close and report

cycle 4 days or less

• General accounting and

reporting costs 0.1-0.2% of

revenue

Financial Planning & Analysis

• # of FTEs

• Staff location/labor market

• Supporting tech. enablers

• Business volumes

• # of entities and/or business

complexity

• Budget model complexity

• F&A outsourcing

• Shared services

• Integrated transaction processing systems to automate accounting

transaction processing

• Integrated enterprise performance management platform that

enables self-service reporting, analysis, and information

distribution

Budgeting & Forecasting:

• Streamlined budget & forecasting process with rolling cycles and

web-based data collection to reduce manual effort

• At one of the world’s

largest electrical

engineering and

electronics companies

delivered reduction of

close cycle by 50% and

cost reduction of 25%

through a single global

web interface for all

Accounting and FP&A

teams

• Planning, performance

management, business

analysis function of 6-11

FTE per Billion of revenue

• Cost of 0.1-0.15% of

revenue

• Single reporting platform

Internal Audit

• # of FTEs

• Staff location/labor market

• Supporting tech. enablers

• # of entities and/or business

complexity to audit

Minimal opportunity to save in this area, but still

have best practices:

• Integrated transaction processing platform to reduce the cost of

performing audits

• Integrated enterprise performance management platform that

provides information which can be used to reduce the cost of

performing audits

• Proper controls and compliance measures

• At a large global telecom -

program management to

comply with Sarbanes

Oxley

• 3+ audits performed per

audit FTE

• 4-6 FTEs per Billion of

revenue

• Audit and compliance costs

of .005-.075% as a percent

of revenue

38

Detailed Analysis of the Cost Drivers of the

Finance and Accounting Function