could maastricht convergence criteria be...

TRANSCRIPT

COULD MAASTRICHT CONVERGENCE CRITERIA BE APPLIED FOR THE ASEAN MONETARY UNION (AMU)?

OLEH:

ZAENAL MUTAQIN 6605810235

TESIS

Diajukan sebagai salah satu syarat guna mempcrolch gelar Magister Sains Ekonomi

Pada Program Studi Ilmu Ekonomi Program Pascasarjana Fakultas Ekonomi Universitas Indonesia

DEPOK,2007

Nama NPM Kekhususan Judul

PERSETUJUAN TESIS

: Zaenal Mutaqin : 6605810235 : Ekonomi Intemasional :COULD MAASTRICHT CONVERGENCE CRITERIA BE APPUED FOR THE ASEAN MONETARY UNION (AMU)?

Depok, 21J J uli 2007

ABSTRAK TESIS

COULD MAASTRICHT CONVERGENCE CRITERIA BE APPLIED FOR THE ASEAN MONETARY UNION (AMU)?

ZAENAL MUTAQIN 6605810235

Program Studi Ilmu Ekonomi Program Pascasarjana Fakultas Ekonomi Universitas Indonesia

KlasifikasiJEL: E61, F02, F42, 052, 053,057 Kata kunci: 1. Maastricht Convergence Criteria

2. ASEAN monetary union 3. Cronbach alpha 4. Reliability index 5. Korelasi

Beberapa literatur tentang konvegensi ASEAN dan kemungkinan pembentukan mata uang bersama menghasilkan beberapa kesimpulan. Beberapa diantaranya membuktikan bahwa pembentukan mata uang bersama bagi ASEAN tidaklah menguntungkan sementara penelitian yang lain menunjukan hasil bcdawanan. Tesis ini mencoba untuk menyeldiki kemungkinan penerapan Kriteria Konvergensi Maastricht di ASEAN pada tahun 2006 yang meliputi scluruh anggota ASEAN berdasarkan data dari IMF, Bank Dunia, Sekretat:iat ASEAN dan CIA untuk periode 2002-2006. Dengan menggunakan Alpha Cronbach (Reliability Index), penelitian ini menunjukkan bahwa dari 5 Maastricht Convergen criteria, ASEAN hanya memenuhi kriteria utang publik dan deficit anggaran. Sementara tiga criteria yang lain tidak tet:penuhi. Berdasarkan Kriteria Konvergensi Maastricht, syarat pembentukan mata uang bersama tidak terpenuhi. Meskipun demikian perbandingan Uni Eropa pada tahun 1992 dengan ASEAN pada tahun 2006 menunjukkan dari 12 negara komunitas eropa hanya Prancis dan Luxembourg yang memenuhi semua kritet:ia dan diikuti oleh Swiss. Semcntara itu tidak satu negara ASEANpun yang dapat mcmenuhi semua kritcria. Meskipun dcmikian mengcluarkan Brunei dan Singapura dari analisis menghasilkan perspektif yang lebih optimis, Thailand dan Kambodia mampu memenuhi semua kriteria. Kritet:ia Maastricht bisa digunakan oleh ASEAN sebagai alat untuk membentuk mata uang bersama berdasarkan beberapa alasan: Pengalaman EMU memberikan pelajaran untuk melakukan bebern.pa langkah. Dalam jangka pendek pembentukan mata uang bersama membutuhkan ket:ja dan upaya yang keras untuk mencapai system keuangan yang stabil sebagai fondasi untuk semua pembangunan dan kemajuan. Memperhatikan . kondisi tet:kini, ASEAN harus berani untuk memulai kesatuan mata uang sebagaiaman EU melakukannya pada permulaan langkah pertama dalam Treaty Maastricht. Didorong oleh komitmen politik, ASEAN harus membuat sebuah skenario sebagaimana tiga langkah Perjanjian Maastricht yang sejalan dengan tujuan untuk mencapai visi ASEAN pada tahun 2020. Olehkarenanya akan lebih baik buat ASEAN jika pada tahun 2010 untuk mendeklarasikan pet:janjian serupa dengan Pet:janjian Maastricth yang diikuti dengan deklarasi kesatuan mata uang ASEAN pada tahun 2020 bersamaan dengan target AEC.

111

ABSTRACT

The literatures on ASEAN convergence and the possibility to create a common currency in ASEAN yield a number of findings. Some studies prove that ASEAN was not favorable to create a common currency, but others find another evidence. This study tries to investigate the possibility to apply Maastricht Convergence criteria in ASEAN in 2006. Covering all ASEAN members for period 2002-2006 data taken from IMF, World Bank, ASEAN Secretary and CIA, the result using Cronbach alpha (reliability index) shows that from five Maastricht convergence criteria, ASEAN could only satisfy the public debt and government deficit criteria (fiscal criteria). There is little evidence that it meets the three other criteria (monetary criteria). Therefore according to Maastricht convergence criteria, ASEAN is not favorable to create a common currency. However, the comparison of EU in 1992 with ASEAN 2006 shows only two of the 12 EC countries - France and Luxembourg satisfied all criteria, thus are followed by Switzerland that was candidate country for the EC and none of ASEAN members satisfy all Maastricht criteria excluding Brunei and Singapore, the imposition of Maastricht criteria gives more optimistic perspective that. Thailand and Cambodia satisfy all criteria. ASEAN can use Maastricht criteria as a tool to form a common currency for following reason: EMU experience gives a lesson to propose some actions to be taken as an ex post example. In a short term, this requires hard works and efforts to reach financial system stability as a foundation for all development and progress. Looking at the current situation, ASEAN should not be abrupt in starting a monetary union as EU did in the beginning of stage I in Maastricht treaty. Guided by political commitment, ASEAN should create a scenario as three stages of Maastricht treaty in line with the targets to attain ASEAN vision in 2020. Therefore it will be better for ASEAN, if in 2010 ASEAN declares a similar treaty as the Maastricht Treaty followed the declaration of ASEAN monetary union in 2020, the same time with AEC targets.

Key words: Maastricht Convergence Criteria, ASEAN monetary union, alpha

Cronbach alpha, reliability index, correlation.

IV

Table of Contents

Olapter I. Introduction 1-1

1.1 Introduction 1-1

1.2 Research Methodology 1-3

1.3 Structure ofWriting 1-4

Chapter 2. Integration, Convergence, and Economic Monetary Union (EMU) 2-1

2.1 Literature Review 2-1

2.1.1 Regional Integration 2-1

2.1.2 Definition and Welfare Effects of Convergence 2-5

2.1.3 Economic of Monetuy Union 2-6

2.2 Empirical literature 2-13

22.1 Maastricht Convergence Criteria 2-13

2.2.2 Convergence and Forming a Common Currency 1n ASEAN 2-18

Chapter 3. ASEAN Economic Integration 3-1

3.1 Basic Facts 3-1

3.2 The Development of ASEA..N Economic Integration 3-3

Chapter 4. Empirical Analysis 4-1

4.1 Model Specification 4-2

4.2 Data for Estimation 4-2

4.3 Empirical Result 4-3

4.3.1 Inflation 4-3

4.3.2 Interest Rate 4-4

4.3.3 Exchange Rate 4-6

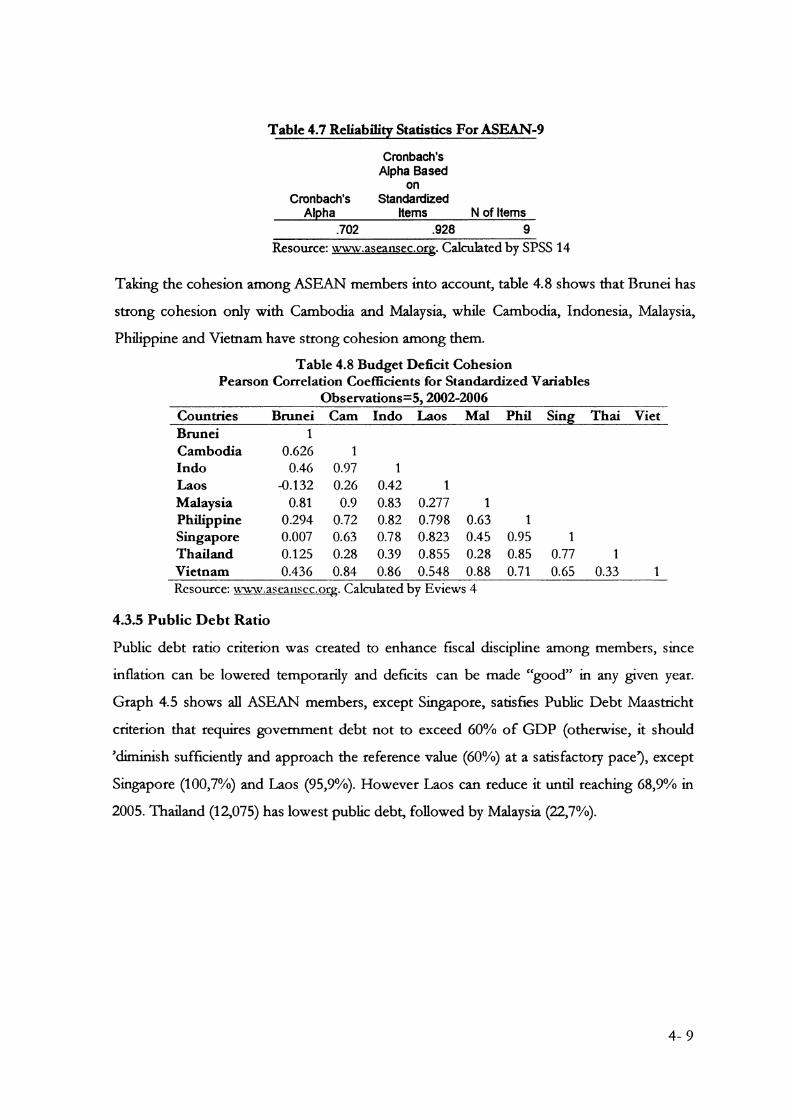

4.3.4 Government Budget Deficit 4-8 -----4.3.5 Public Debt Ratio 4-9

4.4 Empirical Analysis 4-11

4.4.1 Comparing EU (1992) and ASEAN (2006) 4-12

4.4.2 The Usefulness and the benefit of Maastricht Convergence Criteria for ASEAN 4-17

Chapter V. Conclusion 5-1

References

v

ABSTRACT

The literatures on ASEAN convergence and the possibility to create a common currency in ASEAN yield a number of findings. Some studies prove that ASEAN was not favorable to create a common currency, but others f:md another evidence. This study tries to investigate the possibility to apply Maastricht Convergence criteria in ASEAN in 2006. Covering all ASEAN members for period 2002-2006 data taken from IMF, World Bank, ASEAN Secretary and CIA, the result using Cronbach alpha (reliability index) shows that from five Maastricht convergence criteria, ASEAN could only satisfy the public debt and government deficit criteria (fiscal criteria). There is little evidence that it meets the three other criteria (monetary criteria). Therefore according to Maastricht convergence criteria, ASEAN is not favorable to create a common currency. However, the comparison of EU in 1992 with ASEAN 2006 shows only two of the 12 EC countries - France and Luxembourg satisfied all criteria, thus are followed by Switzerland that was candidate country for the EC and none of ASEAN members satisfy all Maastricht criteria excluding Brunei and Singapore, the imposition of Maastricht criteria gives more optimistic perspective that. Thailand and Cambodia satisfy all criteria. ASEAN can use Maastricht criteria as a tool to form a common currency for following reason: EMU experience gives a lesson to propose some actions to be taken as an ex post example. In a short term, this requires hard works and efforts to reach fmancial system stability as a foundation for all development and progress. Looking at the current situation, ASEAN should not be abrupt in starting a monetary union as EU did in the beginning of stage I in Maastricht treaty. Guided by political commitment, ASEAN should create a scenario as three stages of Maastricht treaty in line with the targets to attain ASEAN vision in 2020. Therefore it will be better for ASEAN, if in 2010 ASEAN declares a similar treaty as the Maastricht Treaty followed the declaration of ASEAN monetary union in 2020, the same time with AEC targets.

Key words: Maastricht Convergence Criteria, ASEAN monetary umon,

alpha Cronbach alpha, reliability index, correlation.

11

Table of Contents

Chapter I. Inttoduction 1-1

1.1 Introduction 1-1

1.2 Research Methodology 1-3

1.3 Structure of Writing 1-4

Chapter 2. Integration, Convergence, and Economic Monetary Union (EMU) 2-1

2.1 Literature Review 2-1

2.1.1 Regional Integration 2-1

2.1.2 Definition and Welfare Effects of Convergence 2-5

2.1.3 Economic of Monetary Union 2-6

2.2 Empirical Literature 2-13

2.2.1 Maastricht Convergence Criteria 2-13

2.2.2 Convergence and Forming a Common Currency in ASEAN 2-18

Chapter 3. ASEAN Economic Integration 3-1

3.1 Basic Facts 3-1

3.2 The Development of ASEAN Economic Integration 3-3

Chapter 4. Empirical Analysis 4-1

4.1 Model Specification 4-2

4.2 Data for Estimation 4-2

4.3 Empirical Result 4-3

4.3.1 Inflation 4-3

4.3.2 Interest Rate 4-4

4.3.3 Exchange Rate 4-6

4.3.4 Government Budget Deficit 4-8

4.3.5 Public Debt Ratio 4-9

4.4 Empirical Analysis 4-11

4.4.1 Comparing EU (1992) and ASEAN (2006) 4-12

4.4.2 The Usefulness and the benefit of Maastricht Convergence Criteria for ASEAN 4-17

Chapter V. Conclusion 5-1

References

lll

COULD MAASTRICHT CONVERGENCE CRITERIA BE APPUED FOR THE ASEAN MONETARY UNION (AMU)?

1.1. Introduction

Chapter1 Introduction

There was a fundamental change in international relations after World War 111• The

partnership, cooperation and integration approaches replaced the colonialism approach,

which was no longer accepted2• The emergences of United Nation Organization (UNO),

World Bank, International Monetary Fund (IMF), World Trade Organization (WTO), G-8,

EU, ASEAN, NAFfA (North America Free Trade Area), APEC (Asian Pacific Economic

Cooperation) and others indicate this trend

The regionalization as a part of economic integration among neighboring countries has been

a cooperation trend. Its target is to improve the welfare of all state members concurrendy.

The most successful cases of regionalization in the world is EU, which almost reaches an

economic union, and ASEAN, which is the highest rapid growth area in the world in 90's

outside East Asia Qapan, South Korea, Taiwan and Hongkong).

There have been debates and efforts to enhance the cooperation of EU, whose vision of a

united Europe were primarily guided by political and economic considerations. Established

in 1957 by 6 original members (Belgium, Germany, France, Italy, Luxembourg, and

Netherlands) those signed the Rome treaty, the 27-membered EU almost achieves a full

economic integration since January 1st 2007. The important stage is the signing 'The Treaty

of Maastricht in 1992 when introduced a new form of co-operation among its member

states. The Maastricht Treaty, which was signed on February 7, 1992, states five convergence

conditions (Afxentiou, 2000):

•!• the country's inflation rate is not more than 1.5% higher than the average of the three

lowest inflation rates in the European monetary system

•!• its long term interest rate is not more than 2% higher than the average experiential in the

three low inflation countries

1 Since World War II was an arena of scrambling the impression among countries resulted in the deaths of over 72 million people and making it the deadliest conflict in human history (http:/ I en.wikipedia.org/wiki/World_ War_II_casualties). 2Since colonizing nation generally dominate the resource, labor, and market of colonial territory (http:/ /www.answers.com/topic/colonialism)

1- 1

•:• it has not practiced devaluation during the two years preceding the entrance into the

Union its government budget deficit is not higher than 3% of its Gross Domestic

Product (if it is it should be declining continuously and substantially and come close to

the 3% norm, or alternatively

•:• the deviation from the reference value (3%) should be exceptional and temporary and

remain close to the reference value

•:• its government debt should not be exceed 60% of Gross Domestic Product (if it does, it

should diminish sufficiendy and approach the reference value (60%) at a satisfactory

speed Implementing the 5 criteria will ensure the sustainability of EU to absorb

asymmetric shock).

These criteria guided the introduction of a common currency in line with the principle "One

Market, one Currency." The convergence criteria in The Maastricht Treaty are needed since

the macroeconomic situation differed widely from one country to another (De Grauwe,

2005). Therefore, the Treaty described in detail on how the system was expected to work,

including the statutes of the ECB and the condition under which monetary union would

start (http:// europa.eu/ scad plus/leg/ en/lvb/l25007.htm).

ASEAN is large far behind EU with regard to the integration progress. While EU has been

implementing the European Monetary Union, ASEAN is still struggling in process to

implement the ASEAN Monetary Union (AMU) and has only started initial steps m

implementing ASEAN Free Trade Area (AFTA). However, it is quite interesting to know

whether current condition of ASEAN was favorable to form a common currency as that

when EU was releasing EMU with Maastricht criteria. Geographically, ASEAN is one of the

most important crossroads of world trade. However, it is difficult to create an ASEAN

economic integration because of the huge difference in the size and level of development

among member states as well a number of social issues such as language, history, religion

and culture Govanovic, 2005).

However after the economic crisis m 1997, ASEAN has been indicating its interests to

develop policies to set up greater regional exchange rate stability. It is in this background

that ASEAN policy-makers are considering a regional monetary arrangement for ASEAN

that provides flexibility with regard to the three main global currencies (the dollar, euro and

yen) for its importance in diversified direction of trade provides no obvious single currency

against which to peg (Bayoumi, Eichengreen and Mauro, 2000).

1-2

Measuring current condition of ASEAN as a whole3 with Maastricht criteria and comparing

it with EU condition before the sign of Maastricht Treaty will give the message whether

ASEAN will be appropriate to create a common currency. Although some debates would be

arising whether Maastricht Treaty Criteria as tools to enhance the level of convergence in

EU will be appropriate in ASEAN or other criteria will be more feasible since it was huge

difference between EU and ASEAN.

Kawai (2005) acknowledges the limitation of institutional supports in forming a deeper

integration in ASEAN. However, ASEAN has great potencies to form further economic

integration through various types of institutional cooperation, including the establishment of

an Asia FTA, founding a stronger device for regional financial stability, relative stability of

intra-regional exchange rates and stipulation of various types of regional public goods.

It is remain to be seen whether ASEAN members will be able to maintain their political

commitment strong especially in creating a common currency, like EU members did, to

achieve their vision. Politically, ASEAN has made some efforts to set-up a fundamental

stage as a foundation to form an ASEAN Economic Community. ASEAN has also agreed

to create an ASEAN Economic Community (ASEAN-EC) by 2020 to achieve a greater

economic integration of the region as stipulated in the ASEAN Vision 2020.

Therefore, I am attempting to analyze the feasibility to form a common currency in ASEAN

for the current development based on Maastricht convergence criteria. Therefore, some

questions below are based on Maastricht criteria:

1. What does the Maastricht Criteria need, why have they been beneficial to the EU?

2. To what extent do ASEAN countries in 2006 satisfy The Maastricht Criteria?

3. Would a similar treaty as the Maastricht Treaty be appropriate for the ASEAN countries,

and what would be the best criteria to be included in the treaty?

1.2. Research Methodology

To explore the possible outcomes, I use literature review and empirical study. I carry out the

standardized coefficient cronbach a (reliability index) and correlation to know convergence

and cohesion in ASEAN. This is meant to examine the actual dynamic condition empirically,

apart from the descriptive statistic. The data for the analysis were taken from the World

3 all members (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippine, Singapore, Thailand, and Vietnam).

1- 3

Bank, the International Monetary Fund (IMF), the ASEAN secretary, the European

Commission, the European Central Bank (ECB), and the Central Intelligence Agency (CIA).

1.3. The Structure ofWriting

This thesis consists of four chapters:

-Chapter 1 Introduction, which is the proposal of this research paper

- Chapter 2: Integration, Convergence, and Economic Monetary Union (EMU)

(Literature Review and Theoretical Analysis).

- Chapter 3; ASEAN Economic Integration. This part attempts to explore the

development of ASEAN, starting from its establishment until recent development with

emphasis on economic aspects.

- Chapter 4: Empirical Studies. This part explains the procedure of study, data and study

results.

- Chapter 5: Conclusion

1- 4

Chapter2 Integration, Convergence, and Economic Monetary Union (EMU)

The development of regional integration becomes a world trend for the consequence of

greater reliance on market forces, increased openness, and integration into world economy.

These same forces are expected to generate faster economic growth especially for poorer

countries, and leading to convergence of incomes neighboring countries. Integration among

neighboring countries was characterized by loose and speculative discourse. The analysis of

integration, convergence and EMU centers on possibility to apply a common currency. This

chapter outlines some of review about the analytical and empirical arguments linking

integration, convergence and EMU.

2.1 Literature Review

2.1.1 Regional Integration

Until recendy economic integration has been an important debate among economists. Both

theoretical and empirical works have been inspired by the development of regionalism issue

such as EU, ASEAN, NAFf A and others. Jovanovic (2006) summaries economic

integration as a process and a means by which a group of cow1tries attempts to increase their

level of welfare where strong partnership make achievement of goals more easily. The

integration process will pursue the member states to be concerned about other members

within the group than outside the group. De Rosa (1998) defines economic integration

broadly as the equalization of relative prices for traded goods among countries. Jovanovic

(2006) segregates international economic integration between at least two countries into

seve~ theoretical views: a preferential tariff agreement ~owering tariff among members

compare to non-members), a partial custotns union (retaining the tariff among members and

introducing common external tariff), a free trade area (the agreement to eliminate tariff and

quantitative restriction), a custom union (removing all tariffs and quantitative restriction

among members and introducing common external tariff with non-members), a common

market (free mobility of factor production among members with common regulation or

restriction with non-members), an economic union (synchronization of fiscal, monetary,

industrial, regional, transport and other economic policies), a total economic union (an union

with a single economic policy and a supranational government with great economic

authority).

2- 1

According to Agenor (2001 ), the basic reason for the increase in the number of integration

around world is the increase in the globalization spurred by investors who search the places

where give them the highest return. Bretschger and Steger (2004) state thus econormc

integration will affect economic participation in direct effect on the income level and

dynamic effect

Baldwin and Forslid (2000) propose two major mechanisms by which economic integration

influence evolution of an economy dynamically. First, a scale-effect channel as the result of

positive spill-over effects and growth rate of the integrated economic area; second, factor

reallocation channel as the result of share of resources allocated to the dynamic economic

sectors and therefore changes the growth rate. Integration can also be viewed from the

agglomeration effect as firstly developed by LOsch 1944 (m Neibuhr and Stiller, 2002). He

develops a consistent, albeit rather unknown, model dealing with spatial effects of economic

integration. According to his model, consumers and production factors are assumed

immobile and equally distributed in space. LOsch considers economies of scale and

imperfect competition by which firms descend where spatially dispersed demand can be

served best while profits are maximized. Therefore, the transportation costs for goods

should be proportional to the distance between consumers and producers. The main idea of

LOsch is the development of a regional system theory of market areas. Since all points in

space have to be supplied with goods found out by regular hexagonal market areas for fu:ms

in the equilibrium As the result border regions will have only little economic activities and

will have only firms requiring a small market area.

Based on LOsch, Hoover (1963) fmds out the significance of borders in traditional location

theory. He shows that tariffs and other restraints on international trade raise transportation

costs, distort market areas and supply networks, and increase the costs of producers located

near borders. Therefore, producers will turn away from the territory near a trade barrier that

would restrict their market or supply area and prefer to choose the location in more central

relative area to domestic markets. For this border effect firms orientate both towards the

interior of an area enclosed by borders since the network of a fu:m's demand and supply

relations are denser in the geographical centre of a country than in its periphery.

Supporting LOsch, Hoover suggests that the aperture of a border for trade may change the

economic situation in border regions dramatically. Attractiveness will be gained from border

regions through the reduction of barriers to international trade and low-cost access to the

2-2

foreign market This condition will spur the relocation of firms close to the national border.

When the national market is not large, new products can be supplied profitably from the

integrated market area where a firm is located near the centre of the common market

Therefore, border regions at the boundary of the domestic and the foreign market attract

production within the process of integration.

Viner (1950) shows that integration will reduce the trade barriers and increase international

trade which affects the international pattern of specialization in production. Intra-country

reallocation of production among sectors will drive economic adjustment as production

factors assumed to be mobile within countries and among sectors, although they are

completely immobile on an international scale. Thus countries have ftxed factor endowments

and trade serves as a substitute for factor mobility. Moreover transportation costs, whether

exist or not on a national or an international level, will be treated as a single geographic

location. The assumption that spatial distance is irrelevant for the intensity of trade relations

strongly contrast with the fact that empirical estimations of gravity models have proved that

distance is a very important determinant of international bilateral trade volumes. Finally an

inherent factor of integration is omitted as long as trade models neglect international factor

mobility.

Krugman (1991) proposes the new economic geography which deals with the distribution of

economic activities across space and explains regional disparities by entirely endogenous

location decisions. Krugman's model is called core-periphery model. The model generally

has a combination of elements of traditional regional science and new trade theory. The

characteristics of Krugman's models are an explicit spatial structure, interregional trade costs,

economies of scale in production and monopolistic competition. Spatial equilibrium resulted

from the location decisions of firms, workers and consumers, then the balanced distnbution

of workers and firms across space depends on the relative strength of centripetal forces

(which promote the geographic concentration of economic activities) and centrifugal forces

(which promote the geographic dispersion of economic activities). If centripetal fotces

dominate workers and firms will be unequally distributed across space. In this case, there are

agglomerations with a high density of economic activities as well as regions that only have a

few ft.rmS or no industry at all.

Niebuhr and Stiller (2001), based on the spatial impact of integration, show two results of

new economic geography models which are highly relevant

2-3

First, eliminating both international trade costs and liberalizing cross-border labor

movement will affect the balance of centripetal and centrifugal forces on the international

level. The integration will change the distribution of population, production factors and

firms among countries. Therefore, spatial impact of integration may increase labor migration

among countries. The labor migration not only will alter the national factor endowments but

also the international location of industrial activities.

Second, eliminating international trade costs will change the balance of centripetal and

centrifugal forces on a national level since foreign markets become more important for

buyers and suppliers. Thus, integration will change the distribution of population,

production factors and firms within countries. It implies that opening goods markets might

affect the economic geography within a country. The argument is when the location of

economic activities within a closed economy is strongly inward-oriented, it partially changes

to an outward orientation in an open economy. Finally, the domestic market becomes less

important and less attractive. This might cause a reallocation of economic resources within a

country away from previous centers to new locations.

Niebuhr and Stiller state that the integration has a positive impact on the access to foreign

demand, potential market, and the development of cross-border backward and forward

linkages. But these developments in favor of an economic activity of border regions are

countered by forces which tend to preserve pre-integration geography of economic activities.

Hence economic theory only allows very vague conclusions about the spatial effects of

integration; the relative weight of these counteracting forces is ambiguous from the

theoretical perspective in which depends on specific circumstances, border regions might

benefit, lose or not be affected by integration.

Baldwin and Wyplosz (2006) defme integration effects of growth into medium and long

term. Medium effect will be that economic integration sequentially will improve efficiency,

higher GDP per worker, and fmally higher investment per worker. From this point, capital

per labor ratio starts to rise towards new, higher equilibrium value and faster growth of

output per worker. While long term effect resulted from economic integration is faster

knowledge creation and absorption. This result arises from an increase in investment in

knowledge that leads to a permanent increase in the growth rate.

From fmancial side, Agenor (2001) mentions some benefits of fmancial integration as

following: consumption smoothing (a country can borrow money in recession and lend

2-4

money when booming), domestic investment and growth (openness gives the access for

domestic investment, furthermore contribute to growth), enhanced macroeconomic

discipline (free flow of capital will punish the bad policy and give reward for the good

policy), and increase banking system efficiency and fmancial stability (foreign bank will

improve overall quality and quantity of financial system). On the other hand, possible cost

may also arise from: concentration of capital flows and lack of access, domestic

misallocation of capital flows, loss of macroeconomic stability, pro-cydicality of short term

flows, herding, corruption and volatility of capital flows, and risk of entry by foreign bank.

2.1.2 Defmition and Welfare Effects of Convergence

Convergence can be defined into two definitions: first, the process in which less developed

countries can catch up developed countries in terms of economic productivity and growth,

second, the equality of long terms forecasts at a fuced time (Bernard and Durlauf, 1994).

To describe convergence phenomena within or among countries, many economists use neo

classical framework as the most famous approach. Escot and Galindo (2000), based on

Solow model), concludes the steps in convergence in various analyses: First, closed economy,

where a poorer country with lower initial income will achieve higher growth and equalize it's

income with a richer country in steady state level and the possibility to increase long run

growth rate only through technological progress. The condition will happen if production

function is in constant return to scale and diminishing in each productive function, perfect

competitive market where such condition will push into steady state and full employment in

the long term. Second; opened economy, where the small country will jump immediately to its

steady state of output, and the level of growth rate only determined by technological

progress. This condition will be hold when capital mobility is perfect and fmancial market is

integrated. Third, opened economy with extended Solow Model, where the model is no much

different with first model. Under the assumption imperfect capital mobility with credit

restriction, the long-term per capita growth rate is firmed solely by the technological

progress and economic policy to increase total factor productivity could improve long-term

growth. As in the ftrst model, the absence of international capital flow makes the velocity of

convergence equals the rate of convergence derived from the closed model with the rate of

convergence is 0,

De la Fuente (2002) defmes that the necessary conditions for convergence are the presence

of decreasing return to scale of capital and the presence of technological progress. The

2- 5

fundamental factors that detennirte the level of convetgettce ate investment in physical

capital and technological capital. Once a country suffers from a divergence in fundamental

factors, it will be difficult for this country to catch up growth process experienced by higher

incom~ count.ty. This vi~w was supported by David (1997), who divides the world into

world's wealthiest countries (the convergence is the result of catch-up by poorer countries)

and world's poorest countries (the convergence is the result of downward by richer

countries. Tilis division is the result from the positive relal.ion between saving rale and level

of development. The richer the countries, the higher the saving will be. Therefore th~ level

of development wili be higher. Taylor (1996) found the importance of factor mobility in

delenni:ni:ng lhe convergence and Lhe speed of il. in influencing the convergence process.

The factors are capital, labor, and land.

2.1.3 Economic of Monetary Union

The Theory of Optimum Currency Areas (OCA)

Mongelli (2002) defm~s OCA as the optimal geographic ar~a of a single currency, or of

several currencies, whose exchange rates are irreversibly pegged and might be unified The

single currency, or the pegged currencies, can fluctuate only in agreement against the rest of

the world. Furthermore Mungdli ddin~s optimality in terms of sev~ral OCA properties as

the mobility of labor and other production factors, price and wage flexibility, economic

openness, diversification in production and consumption, similarity in inflation rates, fiscal

i:nl.egra.lion and polil.ica.l inl.egra.t.ion. Distributing above properties will reduces Lhe value of

nominal exchange rate adjustments within the currency area by fostering internal and

external balance, and will reduce the impact of some types of shocks or facilitate the

adjusttnent thereafter. Comttries would form a currency area in expectation that curren.t and

future benefits exceed costs.

The theory of OCA firsdy initiated by Mundell (1961) whose paper illustrates a simple model

of two countries which were initially itt full employment and balance of payments

equilibrium. When the equilibrium is disturbed by a shift in demand from th~ goods in

country B to the goods in country A with underlying assumption that wages and ptices

cannot be reduced in the short run without causing unemployment, the monetary authorities

act to prevenl inflation. The existence of more t:h.a.n one OCAin the world implies variable

exchange rates. Suppose the demand shifts from the products of country B to the products

of Country A, a depreciation by country B or an appreciation by country A would correct

2-6

the external imbalance and also relieve unemployment in country B and restrain inflation in

country A This is the most positive case for flexible exchange rates based on national

currenoes.

Based on Munden•s concept on OCA (1961), many studies determine OCA criteria which

are the extents of international trade among integration members, similarity of economic

structures especially regional shock and business cycle, the degree of mobility, and the

availability of fiscal federalism insurance system to absorb regional shock. From them are

Baldwin and Wyplosz (2006) who mention some OCA criteria as followed: Labor mobility

(people move easily because the cost of sharing the same currency could be eliminated, if the

factors of production, capital and labor were fully mobile across borders), production

diversification (countries whose production and exports are widely diversified, structure

form are similar, and asymmetric shock happen only rarely, therefore overall costs are small

while the benefits accumulate every day), openness (countries which are very open to trade

and trade heavily with each other form an OCA because when the economy is small and

very open to trade, it has little ability to change the prices of its goods on the international

markets), ftScal transfer (countries that agree to compensate each other for adverse shock

form an OCA as shocks occur randomly, today's provider of help will be tomorrow's

beneficiary), homogeneous preferences (currency union member countries must share a

wide consensus on the way to deal with shocks because otherwise each of them will want the

common central bank to pursue different policies), solidarity vs nationalism (when the

conflict arises within a country, the countries that form a currency are need to accept the

costs in the name of a common destiny. This because when separate countries consider the

formation of a currency area, they need to realize that there will be disagreements times

following national lines, especially if the shocks are asymmetric or produce asymmetric

effects).

Eichengreen (1997) following Mundell's paradigm states that policymakers balance the

saving in transactions costs from creating single money against the consequences of

diminished policy autonomy. The decrease in autonomy is arising from the loss of the

exchange rate and of an independent monetary policy as instruments of adjustment The loss

will be more costly when macroeconomic shocks are more asymmetric, when monetary

policy is a more powerful instrument for offsetting them, and when other adjustment

mechanisms like relative wages and labor mobility are less effective.

2-7

Krugman (1991) states that trade mtegration which occurs as a result of economies of scale

leads to regional concentration of mdustrial activities. His basic argument is when

impediments to trade decline, thus will have two opposmg effects on the localization of

industries. It not only makes it possible to produce closer to the fmal markets, but it also

makes it possible to concentrate production so as to profit from economies of scale. 'Ibis

explains why trade integration in fact may lead to more concentration of regional activities

rather than less.

De Grauwe (2006) proposes another argument thus other costs of monetary union are

included: the difficulty to face asymmetric shock (In the absence of flexibility and mobility in

the labor market and the mechanisms to allow for income transfer when a country suffer

from asymmetric shock, the cost of monetary union may become high), different

preferences of countries about inflation and unemployment (some countries may less allergic

to inflation than others), differences in labor market institutions (Some labor markets are

dominated by highly centralized labor union while others are decentralized), difference in

legal system (the difference run deep and sometimes have profound effects on the way

markets function), difference in growth rate (some countries grow faster than others which

may lead to a trade balance problem) and difference in fiscal system and seigniorage problem

(it leads countries to use different combinations of debt and money for financing the

government deficit. When countries join monetary union, they will be constrained in the way

of fmancing their budget deficit).

Furthermore Mongelly (2002) defined benefits and costs of Monetary Integration based on

OCA theory as followed:

- Benefits from improvements in microeconomic efficiency resulted principally from the

increased usefulness of money.

- Benefits from increased macroeconomic stability (and growth) resulted from improved

overall price stability, broader access and more transparent financial markets increasing the

availability of external fmancing, reputation gains for those members with a history of higher

inflation that benefit from an anti-inflationary anchor, the reduction of some types of

fluctuations of output and employment across the currency area due, possibly, to different

economic policies.

- Benefits from positive external effects resulted principally from: savings on transaction

co.sts resulting from a wider international circulation of the single currency, revenues from

2-8

international seignorage, the reduced need for foreign exchange reserves, and simplified

international co-ordination.

- Costs from the deterioration in microeconomic efficiency resulted from change-over costs

(administrative, legal and hardware such as re-denominating contracts and adapting vending

machines) from switching to a new currency and psychological costs resulting from a new

enumerative.

- Costs from decreased macroeconomic stability resulted from membership in a currency

area that narrows the menu of policy instruments direcdy available to national governments.

As the responsibility for setting monetary policy and exchange rates is transferred to a

supranational central bank, no country can pursue some real adjustment in the wake of

asymmetric disturbances (and if its prices and wages are downward sticky).

- Costs from negative external effects. Eventually some pecuniary externalities might ripple

through the currency area if one or more member countries were to run sizeable and

protracted budget deficits, accumulating an unsustainable public debt.

Finally De Grauwe (2005) concludes the costs and benefits of monetary union based on EU

experience to the following conclusions: First, Not all EU members have the same interest

in surrendering their national currencies in adhering to EMU as monetary unification in EU.

Second, the number of countries that benefit from monetary union is probably larger than

most economists though as the process of integration moves on. Third, even net gainer

countries take risk by joining the union as the result from large shock. Fourth, the

enlargement of the Eurozone creates serious challenges. And fifth, the implementation of a

common currency area was the topic in other world areas.

Monetary Union and the Transition to a Monetary Union (a lesson from EU)

Monetary integration is a subject where real economic integration among countries is tested

Therefote, the creation of EMU among the 12 EU countries is the greatest achievement in

the history of The EU. Even though the creation of the EU is very important step towards

completing Single European Market, the EMU has always been an essentially political, rather

than a predominandy economic project One of the expected consequences of the creation

of the EMU is that member countries have similar prices for traded goods. EMU carefully

passes Maastricht Treaty, a map that specifies how and when the single currency would be

launched and laid down a precise set of institutional arrangement (Baldwin and Wyplosz,

2006).

2-9

Toward Maastricht

1970 Werner Plan

Table 2.1 EMU Timetable Between Maastricht and the single currency 1994 European Monetary

Institute 1979 European Monetary 1997 Stability and Growth

Pact System starts

The single currency

1999 Monetary Union starts

2001 Greece joins

1989 Delors Committee 1998 on 2002 Decision membership Conversion rates set

Euro coins and notes introduced

1991 Maastricht signed

1993 Maastricht ratified

Treaty 1998

Treaty 1998

Source: Baldwin and W_;plosz (2006: 380)

Creation of ECB

In December 1991, the Maastricht treaty was signed by the heads of state based on two

principles: the transition toward monetary union in EU that was seen as a gradual one,

extending over a period of many years and the entry into the union that was made

conditional on satisfying convergence criteria (De Grauwe, 2005). The treaty pursues that

the transition to the final stage of monetary union was conditional on a number of

<convergence criteria' which are:

1. Its inflation rate is not more than 1.5% higher than the average of the three lowest

inflation rates among the EU-member states;

2. Its long-term interest rate is not more than 2% higher than the average observed in these

three low-inflation countries;

3. It has joined the exchange rate mechanism of the EMS and has not expenence

devaluation during the two years preceding the entrance into the union;

4. Its government budget deficit is not higher than 3% of its GDP (if it is, it should be

declining continuously and substantially and come close to the 3% norm, or alternatively,

the deviation from the reference value (3%) should be exceptional and temporary and

remain close to the reference value;

5. Its government debt should not exceed 60% of GDP (if it does it should 'diminish

sufficiently and approach the reference value (60%) at a satisfactory pace').

In May 1998, 11 of 15 EU countries (Belgium, Germany, Spain, France, Ireland, Italy,

Luxembourg, the Netherlands, Austria, Portugal and Finland) joined EMU and satisfied

these convergence criteria. Furthermore, Greece on 1 January 2002 satisfied convergence

criteria. While Denmark, Sweden and UK, which satisfied convergence criteria, decided not

2-10

to join the Eurozone. The UK obtained the right to opt-out; Denmark is to subject its entry

to a national referendum; and Sweden decided not to join and used a dodge in the Treaty.

The monetary union was fully worked out with the irrevocable decision to adopt a single

currency by 1 January 1999. The Treaty descnbed in great detail how the system would

work, including the statutes of the ECB and the condition under which monetary tmion

would start (http:/ /europa.eu/scadplus/leg/en/lvb/l25007.htm). When the Treaty was

under preparation, the macroeconomic situation differed widely from one country to

another. For example, German was hit by price instability. It pursues the admission to the

monetary union would not be automatic, therefore why some convergence criteria are

needed (De Grauwe, 2005):

1. Inflation convergence

The reason to satisfy this criterion is the fear of inflationary bias in future monetary union.

Suppose two countries (Germany and Italy) have identical condition except difference in

preference authorities. The German authorities stresses on reducing inflation while Italian

authorities does not stress on it while natural unemployment rate was the same in both

countries. Creating a monetary tmion establishes welfare reduction (resulting from higher

inflation) in Germany as the tmion's central bank is likely to reflect the average preferences

of the participating countries. Since Germany loses when joining monetary union with Italy,

therefore it should impose the condition in which union's central bank should have same

preferences as the German central bank. However, it will be difficult to be implemented,

since majority voting in the council may put German in a minority position and Italian will

suffer from an inevitable high interest rate as the result of fighting inflation. For these

reasons The Maastricht treaty pursues that candidate member countries were asked to

provide a low inflation rate as the same objectives of inflationary stability.

2. Budgetary Convergence

High government debt creates incentive to increase inflation surprisingly for government

bond in the long term. Bonds' interest rate was fixed in a previous period based on the

existing expectations of inflation. If the government creates an unexpectedly higher inflation

the real value of these bonds will be eroded and the bondholders will obtain insufficient

compensation hence bond's interest rate does not reflect the rise of inflation. Therefore

bondholders lose and the government gains. The problem also arises from a monetary

union between low and high debt countries since the low-debt country will be confronted

2-11

with a partner who have a tendency to push for more inflation although if these countries

have the same preferences regarding inflation. The higher debt-GDP ratio is the higher the

probability to create higher inflation and finally the low-debt country continues loosing. The

low-debt country will insist that the debt-GDP ration should be reduced before joining

monetary union by imposing the decrease in government deficit Therefore when it was

achieved, the incentives to create high inflation are disappear. Another argument to insist

this criterion is a large debt will create a higher default risk. If it was allowed into the union,

the pressure for a bailout in the event of a default crisis will increase.

3. Exchange Rate Convergence

The basic idea for this criterion is to prevent countries from manipulating their exchange

rates in order to force entry a more favorable exchange rate with the target is the increase in

the competitiveness. Based on the Treaty, countries should maintain their exchange rate

within the normal band of fluctuation during the two years preceding their entry into the

EMU (normal band was 2x2.25% and since august 2003 become 2x1.5%).

4. Interest rate convergence

The argument for this criterion based on justification that extremely large differences in the

interest rate before joining could lead to large capital gains and losses at the moment of

entry. Hence the exchange rate is irrevocably ftxed there is no exchange risk involved in such

an arbitrage until return on euro and other currencies are equalized, as a result bondholder

will be attracted to sell low-yield euro bonds and to buy high yield other currencies bonds.

Finally this could create large disturbances in national capital market. After some countries

are expected to join EMU, long term interest rates converged automatically as the result

from the peculiarity of this rule is its self-fulfilling nature. Therefore at the start of the union,

the inevitable capital losses and gains will be very small until the long term bond rate will

start converging before entering.

To fully implemented EMU, Delors' report divides Maastricht treaty implementation into

three stages as descnbed below (http:/ /www.ecb.int/ecb/history/emu/html/index):

-The first stage of the realisation of economic and monetary union should begin on 1 July

1990. All restrictions on the movement of capital between Member States were abolished

and the first step was to identify all the issues which should be examined at an early stage, to

establish a work programme by the end of 1993 and to deftne accordingly the mandates of

the existing sub-committees and working groups established for that purpose.

2-12

- The second stage is the establishment of the European Monetary Institute (EMI) on 1

January 1994. The EMI's main tasks are to strengthen central bank cooperation and

monetary policy coordination, to make the preparations required for the establishment of

the European System of Central Banks (ESCB), to perform as the agent of the single

monetary policy and for the creation of a single currency in the third stage, to carry out

preparatory work on the future monetary and exchange tate relationships between the euro

area and other EU countries. To complement and to specify the Treaty provisions on EMU,

the European Council adopted the Stability and Growth Pact in June 1997 with aims to

ensure budgetary discipline in respect of EMU and suplemented by a Declaration of the

Council in May 1998. On 2 May 1998 the Council of the European Union - in the

composition of Heads of State or Government - unanimously decided that 11 Member

States (Belgium, Germany, Spain, France, Ireland, Italy, Luxembourg, the Netherlands,

Austria, Portugal and Finland) had satisfied the criteria to participate the third stage of EMU

and to adopt the single currency on 1 January 1999. With the establishment of the ECB on 1

June 1998, the EMI had completed its tasks and all the preparatory work entrusted to the

EMI was devoted by the ECB to the final testing of systems and procedures.

-The third stage, begining on 1 January 1999, commenced with the irrevocable fixing of the

exchange rates of the currencies of the 11 Member States initially participating in Monetary

Union and with the conduct of a single monetary policy under the responsibility of the ECB.

The number of participating Member States increased to 12 on 1 January 2001, when Greece

entered the third stage of EMU.

2.2 Empirical Literature

2.2.1 Maastricht Convergence Criteria

De Grauwe (1996) states that the convergence criteria in Maastricht treaty are neither

necessary nor sufficient to create a successful monetary union since economic structure in

each member country may be similar. Therefore not only asymmetric shock will not be

happen but also the interest rate convergence and no devaluation two years before entry in

the union are neither necessary nor sufficient to form a successful monetary union. The

reason is that if the monetary union at the same time does not involve some degree of

centralization of national budgets, imposing budgetary convergence requirements will

deteriorate the management of the union. Further critic of De Gtauwe is that the Maastricht

requirement about inflation convergence before the union starts is a technique that

2-13

maximizes the cost of convergence (without guaranteeing success). For example, Italy was

forced to reduce its inflation rate before joining the union, which would carry to the burden

of a low reputation. &onomic agents will be skeptical and inflationary expectations do not

decline easily. Suppose the Italian government fails to attain the same low inflation

reputation as the German government, Italy would never reach the same low inflation

equilibrium as Germany that the Maastricht Treaty required Italy to peg its exchange rate.

Therefore, lira's experiences in increasing real appreciation during the transition direct to

doubts that this disinflation process can be sustained

For debt's criteria, De Grauwe shows several pressures on the central bank to create surprise

inflations in order to reduce the real burden of the debt. When two countries intend to form

a monetary union, a problem arises. For example, the Italian government has the same

preferences for low inflation as that of the German government. They will still have stronger

incentives to create surprise inflations because the Italian government debt exceeds that of

the German government. This incentive does not disappear when Italy is in the union and

creates a problem for Germany. The need to have budgetary convergence criteria is a

different nature. It is necessary to achieve low inflation in the union and to convince

Germany to be a part of the union, even if preferences with respect to inflation are identical.

However, these convergence conditions also bring greater risks that can split the European

Union apart. The division of the European Union will create problems not only for the

countries left out, but also for those who started the union since it will be volatile, create

distortions in trade flows, and undermine the single market program. Imposing these

countries into the monetary union would make it easier to reduce their budget deficits to a

level close to the 3% Maastricht norm. However, imposing the Maastricht convergence

conditions makes convergence difficult Letting highly indebted countries like Italy and

Belgium into the union would put price stability at risk in the future union and will ease

them to reduce their government debt and to eliminate the risk of a deep division of the

European Union.

De Grauwe suggests shifting the focus from convergence requirements towards institutional

strengthening of Europe's future monetary institutions. The future European monetary

union will be in a zone of monetary stability and reduce the risk of a great and permanent

division of the European Union. Such a division would not be in the interest of those who

are allowed in the monetary union, let alone of those who are left out

2-14

Artus (1993) supports De Grauwe's argument that although imposing Maastricht

convergence criteria is to restrict club membership for countries that had demonstrated their

commitment to price stability and fiscal responsibility and to postpone the beginning of the

union to give adequate time for all members of the EC to demonstrate their commitment, a

greater chance of success is limited to countries that have already converged The treaty also

does not stimulate much the integration and flexibility of labor markets. Although legal

obstacles of labor mobility have largely been removed, linguistic and cultural differences are

bound to keep mobility relatively low since the structure and strength of labor unions and

institutional aspects of wage negotiations differ widely in the various EC countries. The

fundamental issue is that some countries could still qualify for membership by cutting

inflation through a severe recession without fundamentally changing their inflationary

proclivity. If the transformation does not take place, the monetary union, or at least its

objective of price stability, will be endangered.

From his study Artus shows that according to the preliminary estimates for 1992, only two

from the 12 EC countries, France and Luxembourg, satisfy all Maastricht criteria. From the

other European countries that could soon join the EC, only Switzerland satisfies the criteria.

Four other EC countries, Denmark, Germany, Ireland, and the Netherlands, and two other

non-EC countries, Austria and Norway, would probably pass the test For Germany and

Norway have close to 3 percent deficit and the excess could be viewed as temporary. For

Denmark and Ireland, the debt ratio is decreasing in a significant pace, and in the

Netherlands, the excess deficit is small and the debt ratio is decreasing; two other EC

countries, Belgium has a low inflation country for many years but the deficit remains high

and the debt ratio is very high. The United Kingdom has a large part of its deficit due to the

severe economic recession; the other countries, Greece, Italy, Portugal, and Spain, and the

two remaining non-EC countries, Finland and Sweden, are clearly far from having

converged

Guldager (1996) divides the five criteria of the Maastricht Treaty into inflation and public

debt performance. Based on these criteria, five EU Member States (France, Ireland, Spain,

Portugal and the United Kingdom) show some convergence towards the EMU requirements

in the period 1986 to 1990. During 1986 to 1993 Denmark improved its position with regard

to inflation performance with the expense of its public debt. The economic performance of

Greece deteriorated, whereas that of the other Member States remained largely stationary.

2-15

Poor debt performance restrains some Member States from participating in the EMU. Italy

and Greece in particular appear to be in a non-sustainable long run situation, with debt-GDP

ratios that are steadily deteriorating. Belgium and Ireland also have no better situation, where

the debt rate has stopped increasing, but remains at a high level. In 1993 Greece, Italy and

Belgium faced a serious problem of excessive public deficit and public debt. Countries with

this complicated problem face serious obstacles on the road to the EMU.

Furthermore Casario and Dadkhah (1998), measuring the benefits and costs of monetary

union, examine the effects of replacing multiple currencies with a single currency by

employing fuzzy1 analysis to measure the degree of compliance of the individual countries in

meeting the convergence criteria in the period 1984 to 1994. The countries included in their

analysis are nine EU countries: Germany, France, Italy, the United Kingdom, Belgium,

Denmark, Ireland, The Netherlands, and Spain. The result shows that the convergence

inflation rate fell from 3.8 percent in 1992 to 3 percent in 1993 and rose to 3.5 percent in

1994; the convergence of interest rates measured on the basis of long-term government

bonds has fallen from 10.9 percent in 1992 to 9.8 percent in 1993 to 9.7 percent in 1994.

Interest rates have demonstrated significant convergence throughout the period under study,

two fiscal criteria show that EU faces considerable difficulty. Only German in 1994 meets

both. With respect to the budget deficit target, the first 6 years of the period showed a

gradual increase in the degree of convergence;

The EU has experienced the least degree of convergence with respect to the government

debt ratio. The number of countries has steadily declined throughout the period from a high

of six between 1984 and 1986 to five between 1987 to 1992 to four in 1993 and 1994. The

membership ratings also declined between 1990 and 1992, and then again between 1993 and

1994. These two countries, Italy and Belgium (the ratio of debt to GDP continues to

diverge), have government debt ratio more than double of the amount specified by the

Maastricht criteria The normal bands of fluctuation within the ERM were widened from

62.25 percent to 61.5 percent. In every year, excluding 1988, at least seven of the EU

countries have achieved a high degree of exchange rate stability. In four separate years all

countries achieved complete fulfillment of the exchange rate goal. In 1994, all currencies,

except the Italian lira maintained their currencies within the acceptable band of fluctuation.

1Potential of aiding economic analysis tremendously, yet it has found most favor with engineers who have applied it to a host of forecasting and control problems

2-16

Finally, it was found that European countries have shown considerable progress toward

meeting the convergence criteria of the macroeconomic variables. Some have been more

willing and able to achieve the preconditions of EMU.

Krugman (1992) criticizes The Maastricht treaty that the sound like unusual as entry criteria

although it was proposed to constrict exchange rate band, and essentially tests the discipline

and effectiveness of each country's central bank. It also tests the ability of governments to

do precisely the one thing that they will never need to do again. Hence under Stage 2

countries will in effect have no independent monetary policies, their inflation rates will have

nothing to do with monetary policy. Therefore the criterion on inflation is also somewhat

doubtful. The obvious concern is at countries will be penalized for success since a country

whose booming economy attracts large voluntary capital inflows, leads to a real appreciation

and fmally, the last two criteria, both of which relate to fiscal policy, make somewhat more

sense. But it remains somewhat vague why fiscal probity is a key issue for monetary union.

He also points to the adverse effects of German reunification deficit as a demonstration that

fiscal policy carries strong externalities; however the German case is a very special one for

the Bundesbank is in the peculiar position of making European monetary policy while

serving only German interests, while under EMU nobody will be in that position, so the case

for collectively policed fiscal policy will be much weaker. Since German monetary leadership

in Europe is not a natural consequence of German size the success and effectiveness do not

rest on firm foundations. German dominance of European monetary policy is by no means

inevitable by sheer economic weight The EMS as now constituted is a kind of a lucky

accident, since it has fortuitously evolved into an effective device for monetary co

ordination. Originally EMS was designed as a system with few teeth (a system without a clear

mechanism for decision making), but it has evolved into a de facto Deutsche mark area in

which a stem-willed Bundesbank exerts control and EMS in principle gave way to German

monetary hegemony in practice. Although Germany is the largest economy by a margin that

will have been slighdy increased once the East has been absorbed, its size advantage is not

huge. Krugman also wavers whether European nations are actually sure that they want EMU

which is reasonable, since it is unclear whether it. is really a good idea. He argues that it is not

clear whether EMU is actually such a great idea, at least from an economic point of view, but

that if it will be done, it should be done quickly. The economics of EMU are straightforward

in principle: They involve a tradeoff of macroeconomic flexibility for microeconomic

2-17

efficiency. The problem is that the macroeconomic costs of EMU are hard, and the

microeconomic benefits impossible, to quantify. Therefore he hesitates whether EMU is

such a good idea Europe has accidentally stumbled into a system of voluntary acceptance of

German monetary leadership, which has made the EMS a surprise success. But Germany is

neither large enough nor representative enough to play that role indefinitely.

2.2.2 Convergence and Forming a Common Currency in ASEAN

Lim and MeAler (2004) used data from 1965-1992 to find out income convergence in

ASEAN 52• Using test of J3 convergence3, the result found negative correlation between the

average growth rate in income and in its initial level for ASEAN 5, but the estimate was not

significant For the cross country income deviations for ASEAN 4 and ASEAN 5, there

were no reduction in income dispersion. The simple test of Verspagen 4 (1994) indicates that

ASEAN 3 are converging where only Indonesian is converging in ASEAN 4. However, the

test of DF-type for output differences between two countries and co-integration found no

evidence of convergence in ASEAN.

Another pessimistic view about setting up a common currency is delivered by study of Xu,

Ward and Gan (2006). Using annual data from 1970-2004 and structural vector auto

regression (SVAR) model and Kalman Filter5, the scholars propose the following model in

which Japan and the USA are chosen as reference countries in testing economic convergence

among ASEAN 5 countries. The state-space model used in their paper is presented as

follows:

Measurement Equation: [X A -X 8 l = a1 + b1x[X A -X c ]+ e1 and the transition Equation:

2 Indonesia, Malaysia, Philippine, Singapore, and Thailand 3 The most common test of convergence to regress the average growth rate on the initial level of real output per capita using cross section data. A negative estimate of f3 indicates absolute convergence and vice versa. But if we include other variables, a negative estimate indicates conditional convergence and vice versa. 4 The model is W;t=lny.t-lny*t where yit is real GDP per capita for country i at time t, yt is average GDP per capita for s countries in the sample and it is assumed that w changes according to the following process Wit+1='1'Wit If '¥>1, per capita income in country i diverges from sample group and if'¥<1 convergence is taking place. 5 an a1gorithm for sequentially updating a linear projection for a state-space form and when applied to a model in state-space form provides an a]gorithm for producing prediction errors ut and prediction error variances Ft.

2-t8

Where XA and Xc represent the set of economic indicators for Japan and the USA

respectively, and X8 represents the economic indicators of the five respective ASEAN-5

countries. In transition equation a, and b, are time-varying coefficients. The model is used to

test the convergence of each indicator separately. If Japan and the ASEAN-5 countries'

series have converged, br would be expected tend to be zero, while if the series of the

ASEAN-5 countries and the U.S have converged, bt is expected to equal one.

Mathematically, this relationship can be expressed as followed, when br = 0, transition

equation can be written as: [X A -X 8 1 = a, + e,, indicating that XA and X8 series have

converged. However, when b, =1, transition equation can be written as:

[xA -X8 ], =a, +lx[XA -Xc]+e, and [Xc -X8 1 =a, +e,, indicating that Xc and X8

series have converged. From their model, it was found that nominal exchange rate in

Malaysia, Singapore, Thailand and Philippine have converged among themselves, and

inflation rate has converged among three countries Malaysia, Singapore and Thailand. For

real GDP, there is no convergent evidence among ASEAN 5. For SVAR analysis, they

follow the process provided by Bayoumi and Eichengreen (1993, 1994), the ftrst step for

SV AR ts estimation of a Standard V AR model, taking the form of

X 1 = lf/1Xt-I + lf/2X 1_ 2 + ..... +If/ PX,_P + e1 = lfi(L )X1 • ~ is a vector of differences of

endogenous variables, the 'Pi are (3x3) matrices of reduced form parameters, e, is the

residuals having Gaussian process and L is the polynomial lag operator. Before estimating

the V AR model, unit root tests of the three endogenous variables will be conducted. The

unobserved structural shocks~ takes the following form: ~=B-1Aer. Since Eviews requires

all restrictions to be linear in the elements of A and B, to specify a long-run restriction, the A

matrix must be the identity matrix. The B matrix can be estimated from the V AR model by

imposing long-run restrictions C. The long-run identifying restrictions are specifted in terms

of the elements of the C matrix in Equation (6). It was assumed that the domestic supply

shocks have long-run effects on domestic output and prices, while the demand shocks only

have effects on domestic prices. Only external shocks have long-run effects on the world

output Taking into account these restrictions, the C matrix can be provided as followed:

[~:: ~22 ~ l From this SV AR model, the result shows a high degree correlation in

(;31 (;32 (;33

2-t9

inflation and growth, positive correlation in external shock among ASEAN 5 and highly

correlated demand, supply shock and high correlation of response to shock among

Singapore, Thailand and Malaysia. Final conclusion is that forming single currency within

ASEAN is favorable just for Singapore, Thailand and Malaysia.

Bayoumi, Eichengren, and Mauro (2000) evaluate regional monetary arrangement for

ASEAN especially after hit by economic crises in 1998 by using data from ASEAN-5. They

find that ASEAN is less suitable for a regional monetary arrangement than EU before

Maastricht treaty. Although intra-regional trade as a share of GDP is similar to EU and the

composition of ASEAN's trade highly weight toward manufacture, aggregate supply

disturbance is highly correlated across member countries. Vector auto-regression systems of

industrial production, interest rates, and prices suggest that the transmission mechanism of

monetary policy is only slighdy more diverse within ASEAN than in the euro area, and the

speed of adjustment is higher than EU; but, the level of development across members is

difference much more significant than in EU. It gives a more complicated future integration

if at the same time; it is likely that inclusion of the less fmancially developed countries in

ASEAN would imply much greater diversity in this respect as well.

Madhur (2002), analyzing cost and benefit of single currency for ASEAN based on OCA

theory, specifies that AMU faces several constrains, including huge diversity in income

among countries, weakness in fmancial sector in some countries, lack of resource pooling

mechanism and constitution to manage a common currency, and lack of political

precondition to implement a common currency. Comparing to EU experience, the old

debate has been replaced with a discussion of political integration that shows the important

of political precondition to get common compromise to achieve convergence. However, the

ASEAN's practice in launching AFf A gives a positive message that ASEAN can implement

a common currency.

In terms of factor mobility, ASEAN compares favorably with the European Union (EU) at

the time of the Maastricht Treaty. ASEAN has relatively high labor mobility as well as capital

mobility as workers from Indonesia, Malaysia, Philippines, and Thailand account for 10

percent of the employment in Singapore. Emigration has been as much as 2 percent of the

labor force of the sending countries. Compared to the EU, ASEAN also ranks quite high in

terms of wage and price flexibility. In fact, traditionally they are known for their flexibility

and speed of adjustment to shocks. Almost all of the change in output and prices in

2-20

response to a shock in East Asia takes place in about two years. By comparison, in Europe,

only about half the adjustment occurs in the ftrst two years after a shock. These results are

consistent with the general impression that labor markets are more flextble in ASE.AN than

in Western Europe. Many ASEAN countries have trade-to-GDP ratios as well as trade

intensity ratios (which normalize bilateral trade by the relative share of the countries in total

world trade to elirnmate size effects) that are higher than in Western Europe.

Bayoumi and Mauro (1999) support Madhnur idea that at close to 25 percent, the share of

intraregional trade in ASEAN total trade, although lower than in the EU ( 40 percent), is

significant and rising. It is much higher than in some of the other currency unions such as

the Eastern Carribean Currency Union (about 10 percent), the Western Africa Economic

and Monetary Union (about 10 percent), and the Central African Economic and Monetary

Community (about 3 percent). Although there are inter-country differences, the symmetry in

shocks among the countries in the region is comparable to the EU. The region wide

economic slowdown in 2001 in response to the global economic downturn is another

evidence of the high degree of shock symmetry among these countries. The high degree of

shock symmetry reflects both the high degree of openness in export orientation, capital

flows, and the similarities in the production structures among these economies.

Green (1994), using data over the period 1970 to 1990, examines the extent to which the

ASEAN- economies; Indonesia, Malaysia, Philippines, and 'Ibailand with the Maastricht

treaty emphasizes the achievement of a set of standards at one point in time. The model

developed in his paper is a reliability index, the standardized coefficient a. (Cronbach's

standardized coefficient alpha) which commonly used in psychometrics and in educational

testing, arises from looking at the collection of national measures for each variable as

separate and distinct measures of some underlying «true" variable. Coefficient a. is calculated

k

k l:var(x;) as: a = -- 1- -=-'=....:.1-~-

k-1 k var:Lx;

i=l

Var refers to sample variance, k=4 (the number of countries estimated), and a. value is close

to 1 when individual measures convergence and can have large negative value when

divergence. To make the calculation more reliable it is common in this form of analysis to

use standardized variables-variables deflated by the sample standard deviations. In this case,

2-21

the coefficient becomes a relatively simple transformation of the average bilateral correlation

coefficient where a = kr , r is the av~rage value of the correlation coefficients, Pii I+ (k -I)r

2 k k

across the different pairs of countries (Xi and X), and r = L L piJ . The result k(k -1) a/lij i<j

shows that exchange rate stability is the likely focal point for any future economic integration

in the ASEAN region. The data suggests that there is considerable cohesion in nominal as

well as real exchange rates. However, increasingly deregulated and open fmancial markets

imply that, in the future, exchange rates will have to be consistent with broader fmancial

market variables. Looking at comparative monetary policy, strictly speaking little

convergence in trends for interest rates can be seen. Somewhat more cohesion can be seen

for money supply growth rates. However, in both cases, the underlying institutional structure

is clearly changing and the past results may not be indicative of future tendencies. Looking

beyond variables that can have an immediate impact on exchange rate structures, fiscal

policy variables exhibited considerable divergence in the late 1980s. However, three of the

ASEAN-5 have relatively limited Government fiscal imbalances, and would appear to pass

the kind of tests for greater economic integration that the European countries have adopted.

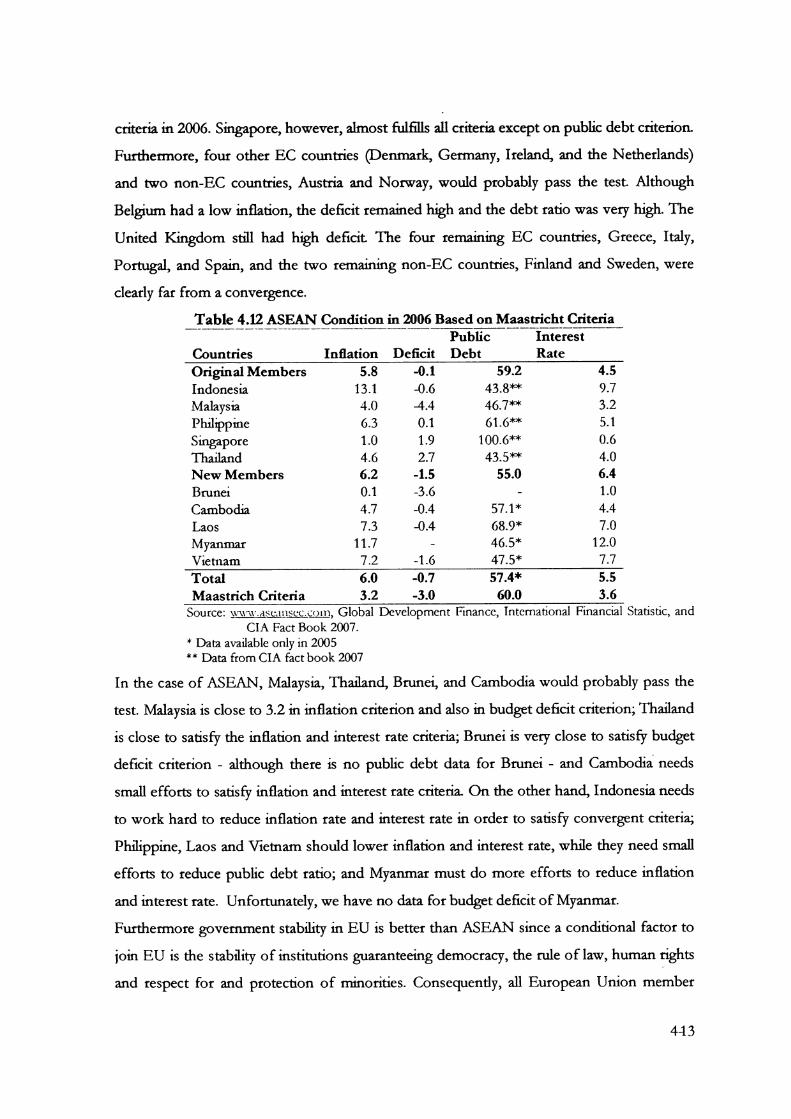

With respect to performance indicators, including real growth rates and inflation, the