course cover 16 - calcpa/media/event materials/january...calcpa education foundation programs and...

TRANSCRIPT

Copyri

ght 2

016-1

7Federal and California Tax Update

Kathleen K. Wright, MBA, CPA, JD, LLM

Learning today. Leading tomorrow.

Copyri

ght 2

016-1

7

Notice to Readers

CalCPA Education Foundation programs and publications are designed to provide CPAs and financial professionals current, accurate information concerning the subject matter covered. However, the CalCPA Education Foundation gives no assurance that such information is comprehensive in its coverage of a subject matter or that it is suitable in dealing with specific client problems or business-related circumstances. Accordingly, information published or provided by the CalCPA Education Foundation should not be relied upon as a substitute for independent research to original sources of authority. The CalCPA Education Foundation does not render any accounting, legal or other professional advice, nor does it have any responsibility for updating or revising any programs or publications which it may present, distribute or sponsor. CPE Credit Policies Course, Conference, Onsite—The California Board of Accountancy (CBA) grants one CPE credit hour for each 50 minutes of class time. To qualify for CPE, a program must be at least 50 minutes in length. The CBA tracks CPE in 25-minute segments after the first 50 minutes. For each additional 25-minute segment completed, 0.5 CPE credit hours will be granted. To accurately track participation, registrants are required to legibly sign your name on the official sign-in sheet prior to the start of the event. If you arrive late, you must note your arrival time on the sign-in sheet. If you need to leave early, you must initial and note your departure time on the sign-in sheet to receive partial credit. The CBA requires CPE providers to closely monitor attendance during CPE. If you are not in the room during a portion of the CPE event, you will not receive credit. Your official record of attendance for the event is available via the My Events section of the website within one week. The host provider must retain the record of attendance, written educational goals and specific learning objectives, as well as a syllabus, which provides a general outline instructional objective and a summary of topics for the course for a period of five years. A copy of the educational goals, learning objectives, and course syllabus shall be made available to the CBA upon request. Webcast—For webcast participants to receive credit, three times every hour, you will be required to respond to an attendance question that appears on the screen. If viewing the webcast as part of a group, the group leader is required to answer the attendance questions on behalf of all participants. Group attendance is verified and documented by the group attendance form the day of the event. The CalCPA Education Foundation archives attendance records as required by the CBA to verify your CPE attendance in the event your CPE records are audited. Webcast are broadcast via the internet to those individuals who have registered for the webcast. The CalCPA Education Foundation takes all reasonable efforts to maintain the camera on the speaker, but does on occasion pan across the audience while following a speaker around the room. Furthermore, as the broadcast requires the use of microphones and other devices to amplify the speaker to both the live and webcast audience, an attendee’s voice may be broadcast during the webcast and, no attendee should have an expectation of privacy as to potentially being identifiable in the webcast. Self-Study—An online exam is included with your purchase. After studying the materials, to take the exam please go to www.calcpa.org/MySelfStudy. You may be asked to log in. Once you have logged in, find this product and click “Take Exam.” You will have a total of (3) attempts to take the final exam. Once you have completed the online final exam, you will be notified if you have passed or failed. To pass, you need a minimum passing grade of 70% (except for California regulatory review courses where the minimum passing grade is 90% as specified in Reg. Sec. 87.9(3)). You will be able to download your certificate of completion documenting the number of CPE credits earned for the course through your CPE Tracker at www.calcpa.org/CPE_Tracker. Please monitor the time it takes to complete the course. Record your total time and your comments about the course on the evaluation e-mailed to you. In accordance with the Standards of the National Association of State Boards of Accountancy (NASBA), one credit hour is granted for each 50 minutes of interactive self-study completed. Recommended credit hours are included in each course description. However, state boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Self-study courses must be completed by one year from date of purchase. If you have any problems or questions using your online course, please e-mail [email protected]. If you move before completing this course, please contact Member Services at (800) 922-5272 with your new address. Materials Terms and Conditions—CalCPA Education Foundation program materials, both hardcopy and electronic, are protected by U.S. copyright law. Materials are provided only for use by the participant registered for the program. You agree that you will not sell, distribute, transmit, or otherwise transfer all or any portions of the content of program materials without written permission from the author(s). Please contact the CalCPA Education Foundation course materials coordinator at [email protected] or (650) 522-3208 to obtain permission. eBook FAQs—Visit www.calcpa.org/ebooks to view frequently asked questions. Be sure to save your annotations made throughout the course. The CalCPA Education Foundation Guarantee—If any continuing education product fails to meet your expectations, or if you are not satisfied for any reason, you may return it within 30 days for an exchange or refund. (Shipping and handling fees are nonrefundable). Call Member Services at (800) 922-5272 for return instructions.

Copyright © 2016 Kathleen K. Wright, CPA, JD, LLM

No copyright claimed in U.S. Government materials.

FDCLU _________________________________________________________________________________________________________www.calcpa.org (800) 922-5272 rev 03/2015

Copyri

ght 2

016-1

7

CalCPA Education Foundation www.calcpa.org (800) 922-5272

This page intentionally left blank.

Copyri

ght 2

016-1

7

1

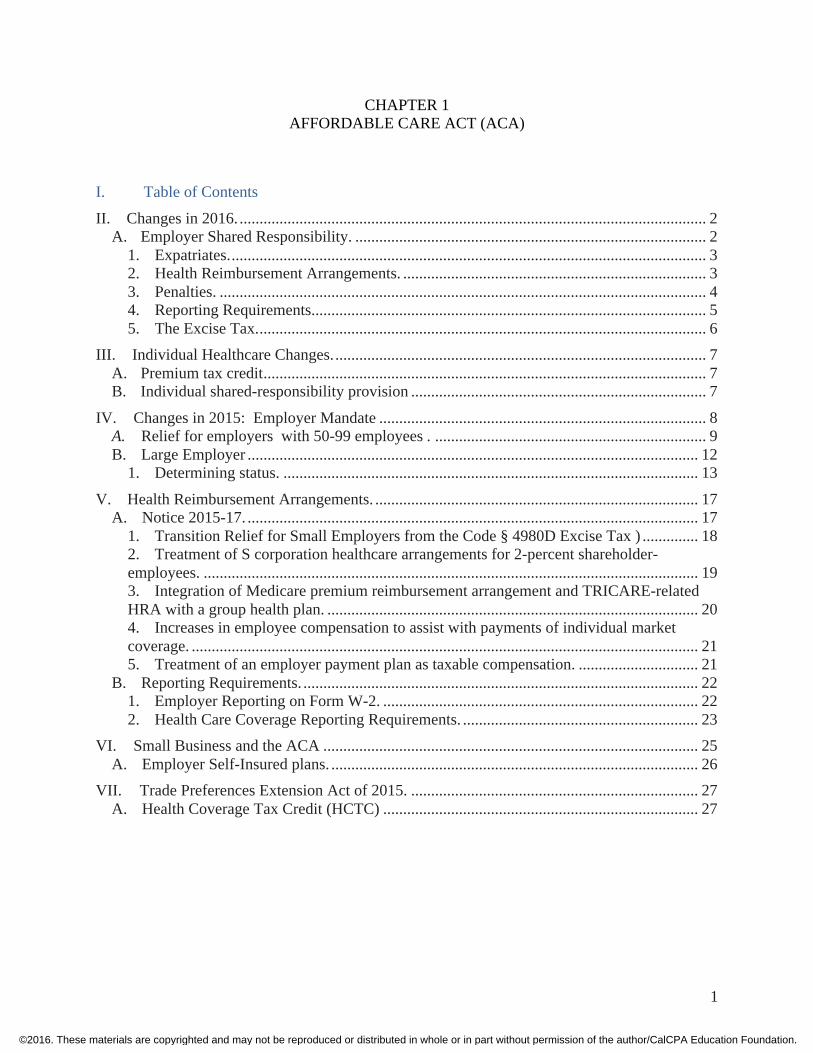

CHAPTER 1 AFFORDABLE CARE ACT (ACA)

I. Table of Contents

II. Changes in 2016. ..................................................................................................................... 2 A. Employer Shared Responsibility. ........................................................................................ 2

1. Expatriates. ....................................................................................................................... 3 2. Health Reimbursement Arrangements. ............................................................................ 3 3. Penalties. .......................................................................................................................... 4 4. Reporting Requirements ................................................................................................... 5 5. The Excise Tax. ................................................................................................................ 6

III. Individual Healthcare Changes. ............................................................................................. 7 A. Premium tax credit ............................................................................................................... 7 B. Individual shared-responsibility provision .......................................................................... 7

IV. Changes in 2015: Employer Mandate .................................................................................. 8 A. Relief for employers with 50-99 employees . .................................................................... 9 B. Large Employer ................................................................................................................. 12

1. Determining status. ........................................................................................................ 13

V. Health Reimbursement Arrangements. ................................................................................. 17 A. Notice 2015-17. ................................................................................................................. 17

1. Transition Relief for Small Employers from the Code § 4980D Excise Tax ) .............. 18 2. Treatment of S corporation healthcare arrangements for 2-percent shareholder-employees. ............................................................................................................................ 19 3. Integration of Medicare premium reimbursement arrangement and TRICARE-related HRA with a group health plan. ............................................................................................. 20 4. Increases in employee compensation to assist with payments of individual market coverage. ............................................................................................................................... 21 5. Treatment of an employer payment plan as taxable compensation. .............................. 21

B. Reporting Requirements. ................................................................................................... 22 1. Employer Reporting on Form W-2. ............................................................................... 22 2. Health Care Coverage Reporting Requirements. ........................................................... 23

VI. Small Business and the ACA .............................................................................................. 25 A. Employer Self-Insured plans. ............................................................................................ 26

VII. Trade Preferences Extension Act of 2015. ........................................................................ 27 A. Health Coverage Tax Credit (HCTC) ............................................................................... 27

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2

II. Changes in 2016.

A. Employer Shared Responsibility.

The employer shared responsibility provisions—also known as the employer coverage mandate—are the employer penalty provisions under the ACA. Penalties apply if an employer fails to offer minimum essential coverage that is affordable and provides minimum value to full-time employees working at least 30 hours per week.

• Employers with 100 or more full-time or equivalent employees (when adding together part-time employees' hours) are subject to the employer shared responsibility provisions in 2015.

• Employers with between 50 and 99 full-time or equivalent employees (“mid-size employers”) are subject to employer shared responsibility in 2016.

These employers must submit ACA information reporting forms to the IRS on or before Feb. 29 by mail (Feb. 28 being a Sunday), or file electronically by March 31. Employers filing 250 or more forms must do so electronically.

To prepare for employer shared responsibility, mid-size employers should:

• Identify full-time employees based on the ACA definition of full-time (those who average 30 hours of work per week in one month), considering special classifications such as staffing employees, independent contractors, temporary or short-term employees and even interns.

• Assess whether the monthly measurement method or look-back measurement method to determine full-time status is best based on the nature of the company’s workforce.

• Update plan documents and summary plan descriptions (SPDs) if necessary for the measurement method selected.

• Determine the appropriate safe harbor the company will use for the affordability calculation: W-2, rate of pay, or federal poverty line.

Example:

In January Company A has 40 full-time employees and 15 part-time employees who each worked 24 hours per week (96 hours per month). The total number of hours worked by part-timers is 1,440 hours (15 x 96). This is equal to a full time equivalent of 12 employees (1,440 / 120 hours = 12). The total employees for purposes of the ACA employer mandate is 52 (40 + 12).

Employers who do not know in advance how many hours an employee will work in a given time period can use a look-back period, called a standard measurement period, to measure full-time employees. The period cannot be less than three months nor exceed 12 months.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

3

Under recent legislation, individuals who have medical coverage under the TRICARE program or the Veteran’s Administration are not considered “employees” in determining whether an employer meets the 50-employee threshold to be an applicable large employer (IRC sec. 4980H( c)(2)(F).

Large employers subject to the ACA’s employer shared responsibility provisions this year should closely monitor their processes to ensure accurate implementation of the ACA’s measurement method and affordability calculation and document offers and waivers of coverage. Penalties will not be assessed until after employer reporting and individual tax filings in 2016, but once a penalty is assessed, there is no retroactive correction. If an employer finds a gap in its processes or a mistake, it should take steps to correct immediately to reduce the amount of potential penalties.

1. Expatriates.

Until further guidance, expatriate health plans do not have to comply with the market reforms as long as they continue to comply with the pre-Affordable Care Act group plan rules. For purposes of this relief, an “expatriate health plan” is an insured group health plan with respect to which enrollment is limited to primary insureds who reside outside of their home country for at least six months of the plan year and any covered dependents, and its associated group health insurance coverage (Notice 2015-43). The Expatriate Health Coverage Clarification Act of 2014 (Div. M, P.L. 113-235) provides generally that the ACA generally does not apply to:

(1) expatriate health plans; (2) employers with respect to expatriate health plans but solely in their capacity as plan sponsors of these plans; and (3) expatriate health insurance issuers with respect to coverage offered by such issuers under expatriate health plans.

The ACA continues to apply to expatriate health plans with respect to the employer shared responsibility rules of Code Sec. 4980H, the reporting requirements of Code Secs. 6055 and 6056, and the excise tax provisions of Code Sec. 4980I. Expatriate health plans can satisfy individual shared responsibility requirements either as an eligible employer sponsored plan or as a plan in the individual market depending on the arrangement.

2. Health Reimbursement Arrangements.

The IRS has taken the position that an arrangement under which an employer pays the premiums for current employees’ individual health coverage or reimburses them for such coverage violates the ACA market reforms that limit cost sharing. As a result, such a plan can cost an employer a $100 per day per affected employee in penalties. Under transition relief for 2014 and the first half of 2015 for small employers, the IRS agreed not to assert the excise tax solely for violation of this rule.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

4

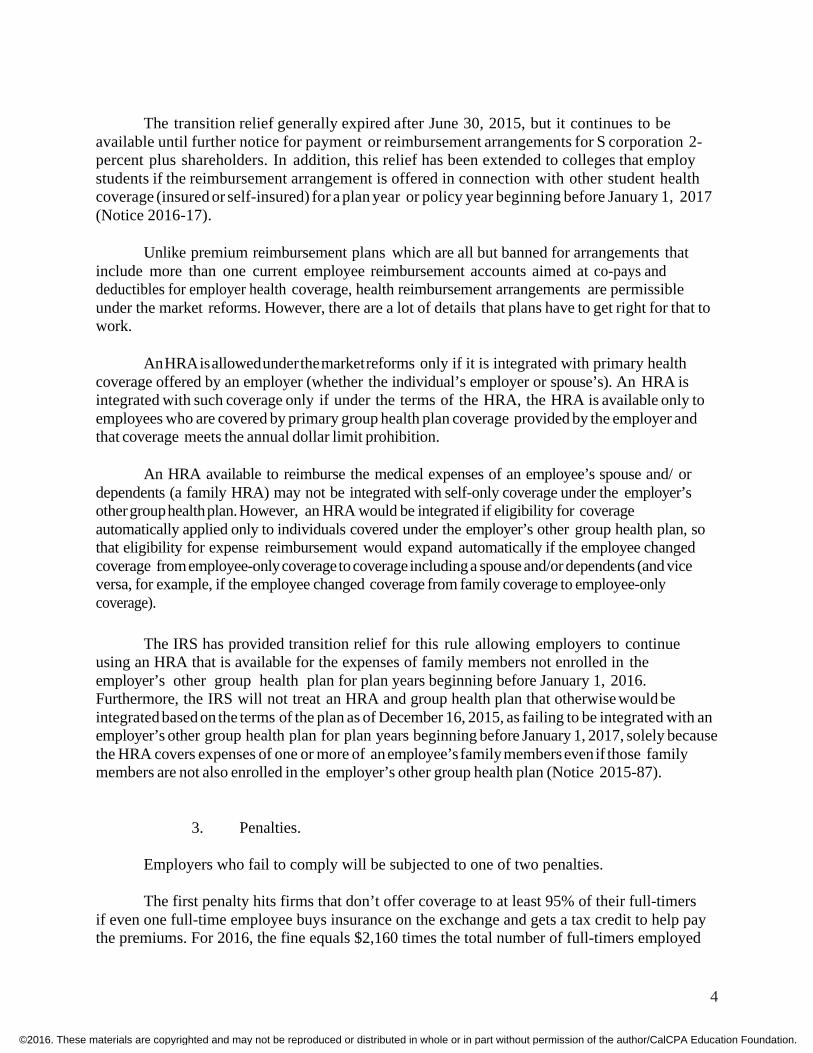

The transition relief generally expired after June 30, 2015, but it continues to be available until further notice for payment or reimbursement arrangements for S corporation 2-percent plus shareholders. In addition, this relief has been extended to colleges that employ students if the reimbursement arrangement is offered in connection with other student health coverage (insured or self-insured) for a plan year or policy year beginning before January 1, 2017 (Notice 2016-17). Unlike premium reimbursement plans which are all but banned for arrangements that include more than one current employee reimbursement accounts aimed at co-pays and deductibles for employer health coverage, health reimbursement arrangements are permissible under the market reforms. However, there are a lot of details that plans have to get right for that to work. An HRA is allowed under the market reforms only if it is integrated with primary health coverage offered by an employer (whether the individual’s employer or spouse’s). An HRA is integrated with such coverage only if under the terms of the HRA, the HRA is available only to employees who are covered by primary group health plan coverage provided by the employer and that coverage meets the annual dollar limit prohibition. An HRA available to reimburse the medical expenses of an employee’s spouse and/ or dependents (a family HRA) may not be integrated with self-only coverage under the employer’s other group health plan. However, an HRA would be integrated if eligibility for coverage automatically applied only to individuals covered under the employer’s other group health plan, so that eligibility for expense reimbursement would expand automatically if the employee changed coverage from employee-only coverage to coverage including a spouse and/or dependents (and vice versa, for example, if the employee changed coverage from family coverage to employee-only coverage). The IRS has provided transition relief for this rule allowing employers to continue using an HRA that is available for the expenses of family members not enrolled in the employer’s other group health plan for plan years beginning before January 1, 2016. Furthermore, the IRS will not treat an HRA and group health plan that otherwise would be integrated based on the terms of the plan as of December 16, 2015, as failing to be integrated with an employer’s other group health plan for plan years beginning before January 1, 2017, solely because the HRA covers expenses of one or more of an employee’s family members even if those family members are not also enrolled in the employer’s other group health plan (Notice 2015-87).

3. Penalties.

Employers who fail to comply will be subjected to one of two penalties. The first penalty hits firms that don’t offer coverage to at least 95% of their full-timers if even one full-time employee buys insurance on the exchange and gets a tax credit to help pay the premiums. For 2016, the fine equals $2,160 times the total number of full-timers employed

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

5

(less 30). 2015’s rules were more lenient: The fine was $2,080 per full-timer, 80 employees were disregarded, and the coverage rate was just 70%. Companies that offer unaffordable health insurance will owe a fine for 2016 equal to $3,240 for each full-timer who gets a subsidy for exchange-bought insurance. 2015’s fine was $3,120. For 2016, coverage is affordable if the required premium payin from a worker for self-only coverage doesn’t exceed 9.66% of total household income. Employers can base the 9.66% calculation on an employee’s rate of pay, W-2 wages or the federal poverty line, instead of household income. The employer’s health plan must also be designed to pay at least 60% of the cost of covered health benefits and provide substantial coverage of inpatient hospital and physician services. Some employers have started to receive subsidy notices from the exchanges. The letters let firms know that an employee got a subsidy to help buy health coverage on the exchange for 2015 because his or her employer didn’t offer affordable insurance. But the notices are going out to a limited number of firms...those whose employees provided the exchange with the employer’s address when they bought health coverage. The employer can appeal the findings in the letter if it disagrees with its contents. These notices are completely separate from IRS’s assessment of fines. The Internal Revenue Service will let employers know whether they owe a penalty. IRS will first send out a preliminary notice to employers of their potential liability and give them a chance to respond before officially assessing the monetary payment. The agency hasn’t yet begun sending its letters. It is still in the process of reviewing the information from the exchange, the data on Form 1095 health returns that were required to be filed for the first time this year by large employers, and the income tax returns of employees who claimed the premium credit.

4. Reporting Requirements

Employers received some welcome relief last December when the IRS extended employee notification and IRS filing deadlines for Affordable Care Act (ACA) information reporting on tax year 2015.

That could pose a challenge going forward, especially for employers that must provide 1095-Cs to employees by the end of January, indicating month-by-month coverage provided through the end of the previous December.

That won't leave much time, and HR should be prepared to act quickly:

ACA Information Reporting Forms

2015 Tax Year Deadlines (forms filed in 2016)

2016 Tax Year Deadlines (forms filed in 2017)

Forms 1095-B and 1095-C due to employees (to be postmarked if mailed, or sent by e-mail if

March 31, 2016 Jan. 31, 2017

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

6

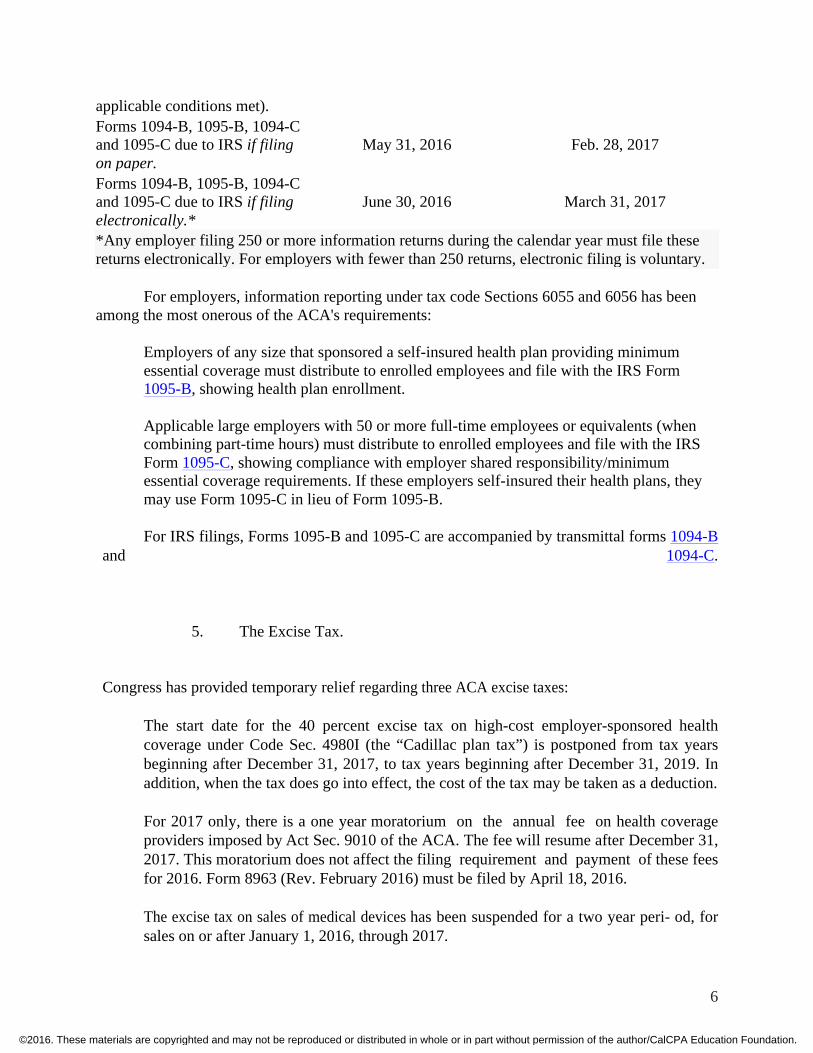

applicable conditions met). Forms 1094-B, 1095-B, 1094-C and 1095-C due to IRS if filing on paper.

May 31, 2016 Feb. 28, 2017

Forms 1094-B, 1095-B, 1094-C and 1095-C due to IRS if filing electronically.*

June 30, 2016 March 31, 2017

*Any employer filing 250 or more information returns during the calendar year must file these returns electronically. For employers with fewer than 250 returns, electronic filing is voluntary.

For employers, information reporting under tax code Sections 6055 and 6056 has been among the most onerous of the ACA's requirements:

Employers of any size that sponsored a self-insured health plan providing minimum essential coverage must distribute to enrolled employees and file with the IRS Form 1095-B, showing health plan enrollment.

Applicable large employers with 50 or more full-time employees or equivalents (when combining part-time hours) must distribute to enrolled employees and file with the IRS Form 1095-C, showing compliance with employer shared responsibility/minimum essential coverage requirements. If these employers self-insured their health plans, they may use Form 1095-C in lieu of Form 1095-B.

For IRS filings, Forms 1095-B and 1095-C are accompanied by transmittal forms 1094-B and 1094-C.

5. The Excise Tax.

Congress has provided temporary relief regarding three ACA excise taxes:

The start date for the 40 percent excise tax on high-cost employer-sponsored health coverage under Code Sec. 4980I (the “Cadillac plan tax”) is postponed from tax years beginning after December 31, 2017, to tax years beginning after December 31, 2019. In addition, when the tax does go into effect, the cost of the tax may be taken as a deduction. For 2017 only, there is a one year moratorium on the annual fee on health coverage providers imposed by Act Sec. 9010 of the ACA. The fee will resume after December 31, 2017. This moratorium does not affect the filing requirement and payment of these fees for 2016. Form 8963 (Rev. February 2016) must be filed by April 18, 2016. The excise tax on sales of medical devices has been suspended for a two year peri- od, for sales on or after January 1, 2016, through 2017.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

7

III. Individual Healthcare Changes.

A. Premium tax credit

The premium tax credit (PTC), a refundable tax credit that can be paid to qualifying taxpayers in advance, applied beginning in 2014. It is intended to make health insurance affordable for individuals who do not have coverage from other sources, such as an employer or the government. The PTC amount is computed using the cost of the second lowest cost silver plan (SLCSP) less the amount the insureds are deemed to be able to contribute based on their income (IRC sec. 36B).

To qualify for the PTC, the individual must have household income (Sec. 36B(d)(2)) of at least 100% of the federal poverty line (FPL) and not more than 400% of the FPL. The FPL figures are included in the instructions to Form 8962, Premium Tax Credit, and are also provided by the Department of Health and Human Services (HHS). The prior year FPL figures are used. In addition, the individual must not have minimum essential coverage offered by the employer that also qualifies as affordable. For 2015, affordable means the self-only coverage offered cost the employee no more than 9.56% of household income (Rev. Proc 2014-37). In addition, the individual is not eligible for government-sponsored coverage, such as Medicare.

In 2016 the federal poverty levels change annually, as do the “applicable percentage” and the affordability factor. For 2016, a policy offered by an employer will be considered unaffordable if it costs the employer more than 9.66% of household income.

B. Individual shared-responsibility provision

Sec. 5000A imposes a penalty on individuals who do not have health coverage for any month of the year and are not exempt for that month. This payment, first effective in 2014, is referred to as the individual shared-responsibility provision (ISRP). To comply with the ISRP the taxpayer must determine whether all members of the “shared responsibility family” (Regs. Sec. 1.5000A-1(d)(4)) had coverage for all months of 2015. If yes, check the box on line 61 of Form 1040 (or equivalent on Form 1040-A or 1040-EZ), and nothing more is needed.

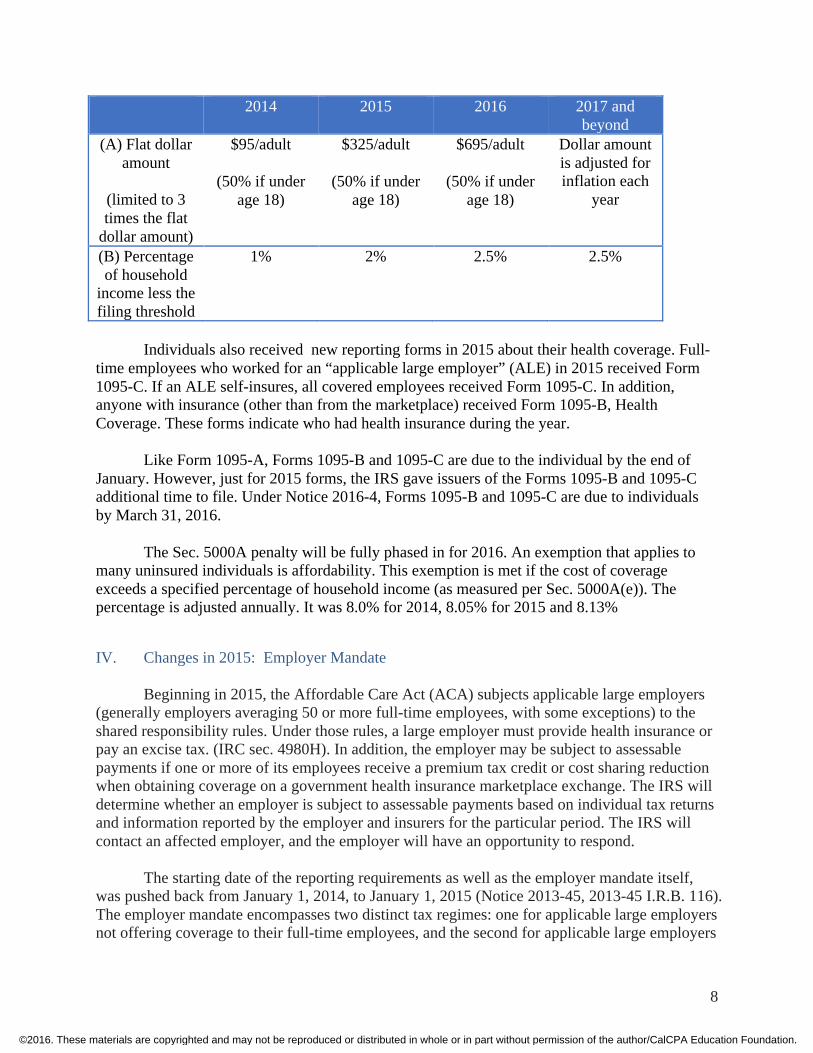

For any months when someone did not have coverage, determine whether an exemption is met. If yes, complete Form 8965 and file it with the return. For any month with no coverage or exemption, a payment is owed. The payment amount is phased in for 2014 and 2015. The penalty calculation is the greater of (A) or (B) below. The maximum penalty amount is capped at the national average bronze premium amount. For 2015, this amount is $207 per individual per month (Rev. Proc. 2015-15).

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

8

2014 2015 2016 2017 and beyond

(A) Flat dollar amount

(limited to 3 times the flat

dollar amount)

$95/adult

(50% if under age 18)

$325/adult

(50% if under age 18)

$695/adult

(50% if under age 18)

Dollar amount is adjusted for inflation each

year

(B) Percentage of household

income less the filing threshold

1% 2% 2.5% 2.5%

Individuals also received new reporting forms in 2015 about their health coverage. Full-time employees who worked for an “applicable large employer” (ALE) in 2015 received Form 1095-C. If an ALE self-insures, all covered employees received Form 1095-C. In addition, anyone with insurance (other than from the marketplace) received Form 1095-B, Health Coverage. These forms indicate who had health insurance during the year.

Like Form 1095-A, Forms 1095-B and 1095-C are due to the individual by the end of January. However, just for 2015 forms, the IRS gave issuers of the Forms 1095-B and 1095-C additional time to file. Under Notice 2016-4, Forms 1095-B and 1095-C are due to individuals by March 31, 2016.

The Sec. 5000A penalty will be fully phased in for 2016. An exemption that applies to many uninsured individuals is affordability. This exemption is met if the cost of coverage exceeds a specified percentage of household income (as measured per Sec. 5000A(e)). The percentage is adjusted annually. It was 8.0% for 2014, 8.05% for 2015 and 8.13%

IV. Changes in 2015: Employer Mandate

Beginning in 2015, the Affordable Care Act (ACA) subjects applicable large employers (generally employers averaging 50 or more full-time employees, with some exceptions) to the shared responsibility rules. Under those rules, a large employer must provide health insurance or pay an excise tax. (IRC sec. 4980H). In addition, the employer may be subject to assessable payments if one or more of its employees receive a premium tax credit or cost sharing reduction when obtaining coverage on a government health insurance marketplace exchange. The IRS will determine whether an employer is subject to assessable payments based on individual tax returns and information reported by the employer and insurers for the particular period. The IRS will contact an affected employer, and the employer will have an opportunity to respond.

The starting date of the reporting requirements as well as the employer mandate itself, was pushed back from January 1, 2014, to January 1, 2015 (Notice 2013-45, 2013-45 I.R.B. 116). The employer mandate encompasses two distinct tax regimes: one for applicable large employers not offering coverage to their full-time employees, and the second for applicable large employers

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

9

whose coverage fails one or more full-time employee on affordability or minimum value grounds. The first regime is meant to generate a higher assessment than the second, and the second is capped so that it can never result in a higher assessment than the first regime for a particular employer in a particular period. The two regimes have different rates as well as different ways of counting employees for their calculations.

An employer is never liable under both regimes for the same period.

There are two threshold issues. First, is the employer an applicable large employer for the pertinent year. An employer is an applicable large employer if it employed an average of at least 50 full-time employees on business days during the preceding calendar year. A second threshold issue is whether a full-time employee enrolled in an insurance exchange and received a health insurance premium tax credit or cost sharing reduction during the period in question. If the answer to both of these questions is yes, then the tax will probably apply barring an explanation from the employer such as compliance with the affordability safe harbor. IRS has issued final regs that provide guidance to employers that are subject to the employer mandate for health coverage under Code Sec. 4980H, which was enacted by the Affordable Care Act (ACA). For months beginning after Dec. 31, 2014, an applicable large employer is liable for an annual assessable payment if any full -time employee is certified to receive an applicable premium tax credit or cost-sharing reduction and either the employer:

(1) fails to offer to its full -time employees (and their dependents) the opportunity to enroll in minimum essential coverage (MEC) under an eligible employer -sponsored plan (Code Sec. 4980H(a) liability); or (2) offers its full -time employees (and their dependents) the opportunity to enroll in MEC under an eligible employer -sponsored plan that, with respect to a full -time employee who has been certified for the advance payment of an applicable premium tax credit or cost-sharing reduction, either is unaffordable or does not provide minimum value as these terms are defined in Code Sec. 36B(c)(2)(C) (Code Sec. 4980H(b) liability).

A stop-gap bill provides that an individual is not taken into account as an employee for the month if the individual has medical coverage for the month under a program for members of the U.S. Armed Forces (TRICARE) or a VA health care program. This provision may be applied retroactively, to months beginning after December 31, 2013. (See the Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 (H.R. 3236)

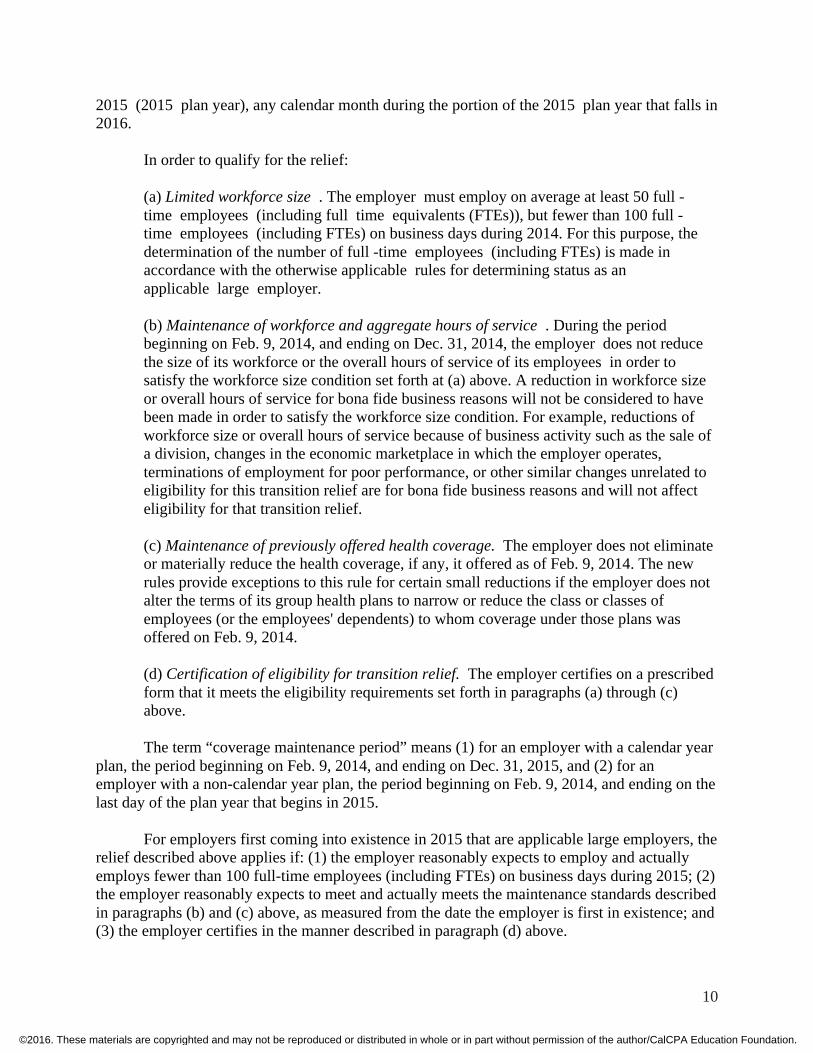

A. Relief for employers with 50-99 employees . For employers with 50-99 employees , who meet requirements (a) through (d) below, no assessable payment under Code Sec. 4980H(a) or Code Sec. 4980H(b) will apply for any calendar month during 2015 or, in the case of any non-calendar plan year that begins in

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

10

2015 (2015 plan year), any calendar month during the portion of the 2015 plan year that falls in 2016. In order to qualify for the relief:

(a) Limited workforce size . The employer must employ on average at least 50 full -time employees (including full time equivalents (FTEs)), but fewer than 100 full -time employees (including FTEs) on business days during 2014. For this purpose, the determination of the number of full -time employees (including FTEs) is made in accordance with the otherwise applicable rules for determining status as an applicable large employer. (b) Maintenance of workforce and aggregate hours of service . During the period beginning on Feb. 9, 2014, and ending on Dec. 31, 2014, the employer does not reduce the size of its workforce or the overall hours of service of its employees in order to satisfy the workforce size condition set forth at (a) above. A reduction in workforce size or overall hours of service for bona fide business reasons will not be considered to have been made in order to satisfy the workforce size condition. For example, reductions of workforce size or overall hours of service because of business activity such as the sale of a division, changes in the economic marketplace in which the employer operates, terminations of employment for poor performance, or other similar changes unrelated to eligibility for this transition relief are for bona fide business reasons and will not affect eligibility for that transition relief. (c) Maintenance of previously offered health coverage. The employer does not eliminate or materially reduce the health coverage, if any, it offered as of Feb. 9, 2014. The new rules provide exceptions to this rule for certain small reductions if the employer does not alter the terms of its group health plans to narrow or reduce the class or classes of employees (or the employees' dependents) to whom coverage under those plans was offered on Feb. 9, 2014. (d) Certification of eligibility for transition relief. The employer certifies on a prescribed form that it meets the eligibility requirements set forth in paragraphs (a) through (c) above.

The term “coverage maintenance period” means (1) for an employer with a calendar year plan, the period beginning on Feb. 9, 2014, and ending on Dec. 31, 2015, and (2) for an employer with a non-calendar year plan, the period beginning on Feb. 9, 2014, and ending on the last day of the plan year that begins in 2015.

For employers first coming into existence in 2015 that are applicable large employers, the relief described above applies if: (1) the employer reasonably expects to employ and actually employs fewer than 100 full-time employees (including FTEs) on business days during 2015; (2) the employer reasonably expects to meet and actually meets the maintenance standards described in paragraphs (b) and (c) above, as measured from the date the employer is first in existence; and (3) the employer certifies in the manner described in paragraph (d) above.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

11

Code Sec. 4980H(a) transition relief. The preamble to the regs provides two types of Code Sec. 4980H(a) transition relief:

... For purposes of Code Sec. 4980H(a), the final regs provide that an applicable large employer member (i.e., one of multiple related entities that, due to the application of the aggregation rules, make up an applicable large employer ) would be treated as offering coverage to its full -time employees for a month if, for that month, it offers coverage to all but 5% or, if greater, 5, of its full -time employees . As provided in Reg. § 54.4980H-4(a), an employee is treated as having been offered coverage only if the employer also offered coverage to that employee's dependents. But see (7) below for transition relief for a failure to offer coverage to dependents for the 2015 plan year. Under the transition rule, for each calendar month during 2015 and any calendar months during the 2015 plan year that fall in 2016, an applicable large employer member that offers coverage to at least 70% of its full -time employees (and, to the extent required under Reg. § 54.4980H-4(a) and the transition relief referred to at (7) below, their dependents) will not be subject to an assessable payment under Code Sec. 4980H(a). ... In general, an assessable payment under Code Sec. 4980H(a) is equal to the number of all full -time employees (excluding 30 full -time employees ) multiplied by one-twelfth of $2,000 for each calendar month. For purposes of the liability calculation under Code Sec. 4980H(a), with respect to each calendar month, an applicable large employer member's number of full -time employees is reduced by that member's allocable share of 30. Accordingly, an applicable large employer with 50 full -time employees that is subject to an assessable payment under Code Sec. 4980H(a) may be subject to an assessable payment based on 20 employees (that is, 50 minus 30) times one-twelfth of $2,000 for each calendar month. Under the transition rule, for 2015 plus any calendar months of 2016 that fall within the employer's 2015 plan year, if an applicable large employer with 100 or more full -time employees (including FTEs) on business days during 2014 (or an applicable large employer member that is part of such an applicable large employer ) is subject to an assessable payment under Code Sec. 4980H(a), the assessable payment under Code Sec. 4980H(a) with respect to the transition relief period will be calculated by reducing an applicable large employer member's number of full -time employees by that member's allocable share of 80 rather than 30.

Shorter period permitted for determining applicable large employer status for 2015 . An applicable large employer is, with respect to a calendar year, an employer that employed an average of at least 50 full -time employees (including FTEs) on business days during the preceding calendar year. (Code Sec. 4980H(c)(2); Reg. § 54.4980H-2)

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

12

Under the transition rule, an employer may determine its status as an applicable large employer by reference to a period of at least six consecutive calendar months, as chosen by the employer , during the 2014 calendar year (rather than the entire 2014 calendar year). Thus, an employer may determine whether it is an applicable large employer for 2015 by determining whether it employed an average of at least 50 full time employees (including FTEs) on business days during any consecutive six-month period in 2014. Coverage for January 2015 . The final regs provide, in general, that if an applicable large employer member fails to offer coverage to a full -time employee for any day of a calendar month, that employee is treated as not offered coverage during that entire month. (Reg. § 54.4980H-4(c)) Recognizing that many employers offer coverage for a new year effective as of the first day of the first pay period beginning on or after the first day of the year, the transitional rule provides that, if an applicable large employer member offers coverage to a full -time employee no later than the first day of the first payroll period that begins in January 2015 , the employee will be treated as having been offered coverage for January 2015 . Coverage for dependents. In order to avoid a potential assessable payment under Code Sec. 4980H, an applicable large employer member must offer coverage to its full -time employees and the full -time employees ' dependents. To provide employers sufficient time to expand their health plans to add dependent coverage, the transitional rule, extending a provision that was in the proposed regs, provides that any employer that “takes steps” during its 2015 plan year toward satisfying the Code Sec. 4980H provisions relating to offering coverage to full -time employees ' dependents, will not be liable for any assessable payment under Code Sec. 4980H solely on account of a failure to offer coverage to the dependents for that plan year. The relief is not available to the extent the employer offered dependent coverage during either the plan year that begins in 2013 (2013 plan year) or the 2014 plan year (meaning the relief is not available to the extent the employer had offered dependent coverage during either of those plan years and subsequently dropped that offer of coverage).

B. Large Employer Only applicable large employers are subject to the employer mandate, and to be an

applicable large employer an employer must employ at least 50 full-time employees or a combination of full-time and part-time employees that equals at least 50. For example, 40 full-time employees employed 30 or more hours per week on average plus 20 half-time employees employed 15 hours per week on average are equivalent to 50 full-time employees. Employers will determine each year, based on their current number of employees, whether they will be considered a large employer for the next year. For example, applicable large employer status for 2015 is determined based on the number of full-time employees the employer averages in 2014. Employers average their number of employees across the months in the year to see whether they

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

13

meet the large employer threshold. The averaging can take account of fluctuations that many employers may experience in their work force across the year. (IRS Q&A on Employer Shared Responsibility Dec. 31,2012 Q&A 4).

Applicable large employer status is determined on a calendar year-by-calendar year basis. An employer is an applicable large employer for a particular calendar if it employed an average of at least 50 full-time employees on business days during the preceding calendar year. An employer is not subject to the shared responsibility assessable payment if:

Its work force exceeds 50 full-time employees for 120 or fewer days during the calendar year, and

The employees in excess of 50 employed during the 120-day period are seasonal workers. (IRC 4980H(c)(2)(B)(i)).

The shared responsibility rules apply to non-profit and government employers as well as for-profit employers. For purposes of determining whether an employer is an applicable large employer, an employer generally will take into account only work performed in the U.S. For example, if a foreign employer has a large workforce worldwide, but less than 50 full-time (or equivalent) employees in the U.S., the foreign employer generally would not be subject to the shared responsibility rules. A company that employs U.S. citizens working abroad generally would be subject to the shared responsibility rules only if the company had at least 50 full-time employees (or the equivalent combination of full-time and part-time employees), determined by taking into account only work performed in the U.S. Employees working only abroad, whether or not U.S. citizens, generally will not be taken into account for purposes of determining whether an employer meets the 50 full-time employee (or equivalents) threshold. Furthermore, for employees working abroad the time spent working for the employer outside of the U.S. would not be taken into account for purposes of determining whether the employer owes an shared responsibility payment or the amount of any such payment. (IRS Q&A on Employer Shared Responsibility, Dec. 31, 2012 Q&A 6).

Related employers and predecessor employers are treated as a single employer under aggregation rules. These include controlled groups of corporations, partnerships and proprietorships under common control, and affiliated service groups. In addition, if the employer was not in existence throughout the preceding calendar year, the determination of whether that employer is an applicable large employer is based on the average number of employees that it is reasonably expected the employer will employ on business days in the current calendar year. Employer for these purposes includes the employer's predecessors.

If the combined total meets the threshold, then each separate company is subject to the shared responsibility rules, even those companies that individually do not employ enough employees to meet the threshold. However, the rules for combining related employers do not apply for purposes of determining whether an employer owes a shared responsibility payment or the amount of any payment.

1. Determining status.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

14

An employer's status as an applicable large employer for a calendar year is determined by taking the sum of the total number of full-time employees (including any seasonal workers) for each calendar month in the preceding calendar year and the total number of full time equivalents (FTEs) (including any seasonal workers) for each calendar month in the preceding calendar year, and dividing by 12. If not a whole number, the result is rounded down to the next lowest whole number. If the result of the calculation is less than 50, the employer is not an applicable large employer for the current calendar year. If the result of this calculation is 50 or more, the employer is an applicable large employer for the current calendar year, unless the seasonal worker exception applies. An employer not in existence throughout the preceding calendar year is an applicable large employer for the current calendar year if it is reasonably expected to employ an average of at least 50 full-time employees (taking into account FTEs) on business days during the current calendar year and it actually employs an average of at least 50 full-time employees (taking into account FTEs) on business days during the calendar year. (Reg. 54.4980H-2(b)(3)).

The shared responsibility rules were originally scheduled to go into effect on January 1, 2014, with transition relief provided with that date in mind (the start date has been postponed a year). Under transition relief for 2013 for employers that are close to the 50 full-time employee threshold, rather than being required to use the full twelve months of 2013 to measure whether it has 50 full-time employees (or an equivalent number of part-time and full-time employees), an employer may measure using any six-consecutive-month period in 2013. So, for example, an employer could use the period from January 1, 2013, through June 30, 2013, and then have six months to analyze the results, determine whether it needs to offer a plan, and, if so, choose and establish a plan.

Seasonal worker exception. If the sum of an employer's full-time employees and FTEs exceeds 50 for 120 days or less during the preceding calendar year, and the employees in excess of 50 who were employed during that period of no more than 120 days are seasonal workers, the employer is not considered to employ more than 50 full-time employees (including FTEs) and the employer is not an applicable large employer for the current calendar year. For purposes of this rule only, four calendar months may be treated as the equivalent of 120 days. The four calendar months and the 120 days are not required to be consecutive. A seasonal worker is a worker who performs labor or services on a seasonal basis and retail workers employed exclusively during holiday seasons.

Although seasonal workers who work more than 30 hours a week do not count for purposes of counting full time employees to determine applicable employer status, they do count as full time employees for purposes of determining shared responsibility payment amounts.

Full-time employees. A full-time employee with respect to any month is an employee who is employed on average at least 30 hours of service per week. Under proposed reliance regulations, 130 hours of service in a calendar month is treated as the monthly equivalent of at least 30 hours of service per week, provided the employer applies this equivalency rule on a reasonable and consistent basis.

Full time equivalents. Although part-time employees do not count for purposes of determining shared responsibility payments, they nevertheless do count for purposes of determining large employer status. An employer must include full-time equivalent employees

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

15

(FTEs) determined by dividing the aggregate number of hours of service of employees who are not full-time employees for the month, by 120. Under proposed reliance regulations, all employees (including seasonal workers) who were not employed on average at least 30 hours of service per week for a calendar month in the preceding calendar year are included in calculating the employer's FTEs for that calendar month. The number of FTEs for each calendar month in the preceding calendar year is determined by calculating the aggregate number of hours of service for that calendar month for employees who were not full-time employees (but not more than 120 hours of service for any employee) and dividing that number by 120. In determining the number of FTEs for each calendar month, fractions are taken into account.

Example: Assume that Diva Corp. has, in addition to full-time employees, five part-time employees for the month. The part-time workers' aggregate number of hours of service for the month is 480. Based on the service hours of its part-time workers, Diva must add four full-time equivalent employees (480 aggregate hours of service / 120) to the number of its full-time employees for that month in determining if it is an applicable large employer.

Example: For 2015 and 2016, ParentCo. owns 100 percent of all classes of stock of Sub1 and Sub2, and they are a controlled group of corporations. ParentCo has no employees at any time in 2015. For every calendar month in 2015, Sub1 has 40 full-time employees and Sub2 has 60 full-time employees. Because ParentCo, Sub1 and Sub2 have a combined total of 100 full-time employees during 2015, they are an applicable large employer and each is treated as an applicable large employer member for 2016.

Example: During each calendar month of 2015, the employer company has 20 full-time employees (each averages 35 hours of service per week), 40 part time employees (each averages 90 hours of service per month), and no seasonal workers. Each of the 20 employees who average 35 hours of service per week count as one full-time employee for each month. To determine the number of FTEs for each month, the total hours of service of the employees who are not full-time employees (but not more than 120 hours of service per employee) are aggregated and divided by 120. The result is that the employer has 30 FTEs for each month (40 × 90 = 3,600, and 3,600 ÷ 120 = 30). Because the company has 50 full-time employees (the sum of 20 full-time employees and 30 FTEs) during each month in 2015, and because the seasonal worker exception is not applicable, the company is an applicable large employer for 2016.

Example: During 2015, the employer 40 full-time employees for the entire calendar year, none of whom is a seasonal worker. In addition, the company has 80 seasonal full-time workers who work for the company from September through December, 2015. The company has no FTEs during 2015. Before applying the seasonal worker exception, the company has 40 full-time employees during each of eight calendar months of 2015, and 120 full-time

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

16

employees during each of four calendar months of 2015, resulting in an average of 66.5 employees for the year (rounded down to 66 full-time employees). However, the company’s workforce equaled or exceeded 50 full-time employees (counting seasonal workers) for no more than four calendar months (treated as the equivalent of 120 days) in calendar year 2015, and the number of full-time employees would be less than 50 during those months if seasonal workers were disregarded. Accordingly, because after application of the seasonal worker exception, the company is not considered to employ more than 50 full-time employees and it is not an applicable large employer for 2016.

Example: Same facts as in Example 4, except that the employer company has 20 FTEs in August, some of whom are seasonal workers. The seasonal worker exception does not apply if the number of an employer's full-time employees (including seasonal workers) and FTEs equals or exceeds 50 employees for more than 120 days during the calendar year. Because the employer has at least 50 full-time employees for a period greater than four calendar months (treated as the equivalent of 120 days) during 2015, the exception does not apply. The employer averaged 68 full-time employees in 2015: [(40 × 7) + (60 × 1) + (120 x 4)] ÷ 12 = 68.33, rounded down to 68, and accordingly, the employer is an applicable large employer for calendar year 2016.

Example: The employer is incorporated on January 1, 2015. On January 1, 2015, it has three employees. However, prior to incorporation, its owners purchased a factory intended to open within two months of incorporation and to employ approximately 100 employees. By March 15, 2015, the employer has more than 75 full-time employees. Because the employer can reasonably be expected to employ on average at least 50 full-time employees on business days during 2015, and actually employs an average of at least 50 full-time employees on business days during 2015, the employer is an applicable large employer. (Reg. 54.4980H-2(d) Examples 1 through 5).

For employees paid on an hourly basis, an employer must calculate actual hours of service from records of hours of service and hours for which payment is made or due. For employees paid on a non-hourly basis, an employer must calculate hours of service by using one of the following methods:

Using actual hours of service from records of hours of service and hours for which payment is made or due;

Using a days-worked equivalency whereby the employee is credited with eight hours of service for each day for which the employee would be required to be credited with at least one hour of service in accordance with the rule for hourly employees; or

Using a weeks-worked equivalency whereby the employee is credited with 40 hours of service for each week for which the employee would be required to be credited with at least one hour of service in accordance with the rule for hourly employees.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

17

An employer must use one of these three methods for calculating the hours of service for non-hourly employees, but an employer is not required to use the same method for all non-hourly employees. The employer may apply different methods for different classifications of non-hourly employees, provided the classifications are reasonable and consistently applied. Similarly, an applicable large employer member is not required to apply the same methods as other applicable large employer members of the same applicable large employer for the same or different classifications of non-hourly employees, provided that in each case the classifications are reasonable and consistently applied by the applicable large employer member.

An assessable payment for an employer that does not offer coverage to at least 95 percent (70% in 2015) of its full-time employees is based on the total number of full-time employees (minus 30). An assessable payment for an employer that does offer such coverage is based only on the number of full-time employees that claim a premium tax credit. An employer may use a look-back method for determining in advance whether or not an employee is to be treated as a full-time employee, based on the hours of service credited to the employee during a previous period.

V. Health Reimbursement Arrangements. A common question to emerge after enactment of ACA relates to the consequences to the employer if the employer does not establish a health insurance plan for its own employees, but reimburses those employees for premiums they pay for health insurance (either through a qualified health plan in the Marketplace or outside the Marketplace). Under IRS Notice 2013-54, such arrangements are described as employer payment plans. An employer payment plan generally does not include an arrangement under which an employee may have an after-tax amount applied toward health coverage or take that amount in cash compensation. As explained in Notice 2013-54, these employer payment plans are considered to be group health plans subject to the market reforms, including the prohibition on annual limits for essential health benefits and the requirement to provide certain preventive care without cost sharing. Notice 2013-54 clarifies that such arrangements cannot be integrated with individual policies to satisfy the market reforms. Consequently, such an arrangement fails to satisfy the market reforms and may be subject to a $100/day excise tax per applicable employee (which is $36,500 per year, per employee) under section 4980D of the Internal Revenue Code. In 2015, the IRS issued Notice 2015-17, which provides relief from the excise tax penalty. Both Notices are discussed here.

A. Notice 2015-17.

This notice reiterates the conclusion in previous guidance addressing employer payment plans, including Notice 2013-54, 2013-40 I.R.B. 287, that employer payment plans are group health plans that will fail to comply with the market reforms that apply to group health plans under the Affordable Care Act (ACA). For this purpose, an employer payment plan as described in Notice 2013-54 refers to a group health plan under which an employer reimburses an

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

18

employee for some or all of the premium expenses incurred for an individual health insurance policy or directly pays a premium for an individual health insurance policy covering the employee, such as arrangements described in Revenue Ruling 61-146, 1961-2 C.B. 25. This notice also provides transition relief from the assessment of excise tax under Internal Revenue Code (Code) § 4980D for failure to satisfy market reforms in certain circumstances. The transition relief applies to employer healthcare arrangements that constitute:

(1) employer payment plans, as described in Notice 2013-54, if the plan is sponsored by an employer that is not an Applicable Large Employer (ALE) under Code § 4980H(c)(2) and §§ 54.4980H-1(a)(4) and -2;

(2) S corporation healthcare arrangements for 2-percent shareholder-employees;

(3) Medicare premium reimbursement arrangements; and

(4) TRICARE-related health reimbursement arrangements (HRAs).

Certain questions/answers from Notice 2015-17 are reproduced below with comment:

1. Transition Relief for Small Employers from the Code § 4980D Excise Tax )

Small employers have in the past often offered their employees health coverage through arrangements that would constitute an employer payment plan as described in Notice 2013-54. If an employer offered coverage through such an arrangement, will the employer owe an excise tax under Code § 4980D?

In general, yes; however, this notice provides limited transition relief for coverage sponsored by an employer that is not an ALE under §§54.4980H-1(a)(4) and -2.

Notice 2013-54 concludes that the arrangements constituting employer payment plans as described in that notice fail to comply with the market reforms and may subject employers to the excise tax under Code § 4980D. At the same time, the Departments understand that some employers that had been offering health coverage through an employer payment plan may need additional time to obtain group health coverage or adopt a suitable alternative.

The SHOP Marketplace addresses many of the concerns of small employers. However, because the market is still transitioning and the transition by eligible employers to SHOP Marketplace coverage or other alternatives will take time to implement, this guidance provides that the excise tax under Code § 4980D will not be asserted for any failure to satisfy the market reforms by employer payment plans that pay, or reimburse employees for individual health policy premiums or Medicare part B or Part D premiums (1) for 2014 for employers that are not ALEs for 2014, and (2) for January 1 through June 30, 2015 for employers that are not ALEs for 2015. After June 30, 2015, such employers may be liable for the Code § 4980D excise tax.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

19

For purposes of this Q&A-1, an ALE generally is, with respect to a calendar year, an employer that employed an average of at least 50 full-time employees (including full-time equivalent employees) on business days during the preceding calendar year. See Code § 4980H(c)(2) and §§ 54.4980H-1(a)(4) and -2. For determining whether an entity was an ALE for 2014 and for 2015, an employer may determine its status as an applicable large employer by reference to a period of at least six consecutive calendar months, as chosen by the employer, during the 2013 calendar year for determining ALE status for 2014 and during the 2014 calendar year for determining ALE status for 2015, as applicable (rather than by reference to the entire 2013 calendar year and the entire 2014 calendar year, as applicable).

Employers eligible for the relief described in this Q&A-1 that have employer payment plans are not required to file IRS Form 8928 (regarding failures to satisfy requirements for group health plans under chapter 100 of the Code, including the market reforms) solely as a result of having such arrangements for the period for which the employer is eligible for the relief. This relief does not extend to stand-alone HRAs or other arrangements to reimburse employees for medical expenses other than insurance premiums.

2. Treatment of S corporation healthcare arrangements for 2-percent shareholder-employees.

IRS Notice 2008-1, 2008-2 I.R.B. 1, provides that if an S corporation pays for or reimburses premiums for individual health insurance coverage covering a 2-percent shareholder (as defined in Code § 1372(b)(2)), the payment or reimbursement is included in income but the 2-percent shareholder-employee may deduct the amount of the premiums under Code § 162(l), provided that all other eligibility criteria for deductibility under Code § 162(l) are satisfied. (This arrangement is referred to in this notice as a 2-percent shareholder-employee healthcare arrangement.) Is a 2-percent shareholder-employee healthcare arrangement subject to the market reforms?

The Departments are contemplating publication of additional guidance on the application of the market reforms to a 2-percent shareholder-employee healthcare arrangement. Until such guidance is issued, and in any event through the end of 2015, the excise tax under Code § 4980D will not be asserted for any failure to satisfy the market reforms by a 2-percent shareholder-employee healthcare arrangement. Further, unless and until additional guidance provides otherwise, an S corporation with a 2-percent shareholder-employee healthcare arrangement will not be required to file IRS Form 8928 (regarding failures to satisfy requirements for group health plans under chapter 100 of the Code, including the market reforms) solely as a result of having a 2-percent shareholder-employee healthcare arrangement.

The guidance provided in this Q&A-2 (including the guidance provided in the preceding paragraph) does not apply to reimbursements of individual health insurance coverage with respect to employees of an S corporation who are not 2-percent shareholders (but see Q&A-1).

The Treasury Department and the IRS are also considering whether additional guidance is needed on the federal tax treatment of 2-percent shareholder-employee healthcare arrangements. However, unless and until additional guidance provides otherwise, taxpayers may

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

20

continue to rely on Notice 2008-1 with regard to the tax treatment of arrangements described therein for all federal income and employment tax purposes. To the extent that a 2-percent shareholder is allowed both the deduction under Code § 162(l) and the premium tax credit under Code § 36B, Revenue Procedure 2014-41, 2014-33 I.R.B. 364, provides guidance on computing the deduction and the credit with respect to the 2-percent shareholder.

Code § 9831(a)(2) provides that the market reforms do not apply to a group health plan that has fewer than two participants who are current employees on the first day of the plan year. Accordingly, an arrangement covering only a single employee (whether or not that employee is a 2-percent shareholder-employee) generally is not subject to the market reforms whether or not such a reimbursement arrangement otherwise constitutes a group health plan. If an S corporation maintains more than one such arrangement for different employees (whether or not 2-percent shareholder-employees), however, all such arrangements are treated as a single arrangement covering more than one employee so that the exception in Code § 9831(a)(2) does not apply. For this purpose, if both a non-2-percent shareholder employee of the S corporation and a 2-percent shareholder employee of the S corporation are receiving reimbursements for individual premiums, the arrangement would be considered a group health plan for more than one current employee. However, if an employee is covered under a reimbursement arrangement with other-than-self-only coverage (such as family coverage) and another employee is covered by that same coverage as a spouse or dependent of the first employee, the arrangement would be considered to cover only the one employee.

3. Integration of Medicare premium reimbursement arrangement and TRICARE-related HRA with a group health plan.

If an employer offers to reimburse Medicare premiums for its active employees, does this arrangement create an employer payment plan under Notice 2013-54? If so, may the employer payment plan be integrated with another group health plan to satisfy the annual dollar limit and preventive services requirements? Similarly, does an arrangement under which an employer reimburses (or pays directly) some or all of medical expenses for employees covered by TRICARE constitute an HRA subject to the market reforms? If so, may the HRA be integrated with another group health plan to satisfy the annual dollar limit and preventive services requirements?

An arrangement under which an employer reimburses (or pays directly) some or all of Medicare Part B or Part D premiums for employees constitutes an employer payment plan, as described in Notice 2013-54, and if such an arrangement covers two or more active employees, is a group health plan subject to the market reforms. An employer payment plan may not be integrated with Medicare coverage to satisfy the market reforms because Medicare coverage is not a group health plan. However, an employer payment plan that pays for or reimburses Medicare Part B or Part D premiums is integrated with another group health plan offered by the employer for purposes of the annual dollar limit prohibition and the preventive services requirements if (1) the employer offers a group health plan (other than the employer payment plan) to the employee that does not consist solely of excepted benefits and offers coverage providing minimum value; (2) the employee participating in the employer payment plan is actually enrolled in Medicare Parts A and B; (3) the employer payment plan is available only to

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

21

employees who are enrolled in Medicare Part A and Part B or Part D; and (4) the employer payment plan is limited to reimbursement of Medicare Part B or Part D premiums and excepted benefits, including Medigap premiums. Note that to the extent such an arrangement is available to active employees, it may be subject to restrictions under other laws such as the Medicare secondary payer provisions. An employer payment plan that has fewer than two participants who are current employees (for example, a retiree-only plan) on the first day of the plan year is not subject to the market reforms and, therefore, integration is not necessary to satisfy the market reforms.

Notice 2015-17 also explains health reimbursement arrangements with respect to TRICARE (the health care program for uniformed service members (the Military Health System).

4. Increases in employee compensation to assist with payments of individual market coverage.

If an employer increases an employee's compensation, but does not condition the payment of the additional compensation on the purchase of health coverage (or otherwise endorse a particular policy, form, or issuer of health insurance), is this arrangement an employer payment plan?

No. As described in Notice 2013-54, an employer payment plan is a group health plan under which an employer reimburses an employee for some or all of the premium expenses incurred for an individual health insurance policy or directly pays a premium for an individual health insurance policy covering the employee, such as arrangements described in Rev. Rul. 61-146. The arrangement described in this Q&A-4 does not meet that description. In addition, because the arrangement described in this Q&A-4 generally will not constitute a group health plan, it is not subject to the market reforms. Providing employees with information about the Marketplace or the premium tax credit under Code § 36B is not endorsement of a particular policy, form, or issuer of health insurance.

5. Treatment of an employer payment plan as taxable compensation.

Notice 2013-54 provides that the payment arrangement described in Rev. Rul. 61-146 is an employer payment plan. May the reimbursements or payments under an arrangement described in Rev. Rul. 61-146 be provided on an after-tax basis and, if so, will this cause the arrangement not to be a group health plan (and accordingly not to be subject to the market reforms)?

No. Rev. Rul. 61-146 holds that under certain conditions, if an employer reimburses an employee's substantiated premiums for non-employer sponsored hospital and medical insurance, the payments are excluded from the employee's gross income under Code § 106. This exclusion also applies if the employer pays the premiums directly to the insurance company. The holding in Rev. Rul. 61-146 continues to apply, meaning only that payments under arrangements that meet the conditions set forth in Rev. Rul. 61-146 are excludable from the employee's gross income under Code § 106 (regardless of whether the employer includes the payments as wage

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

22

payments on the Form W-2). However, Rev. Rul. 61-146 does not address the application of the market reforms and should not be read as containing any implication regarding the application of the market reforms. As explained in Notice 2013-54, an arrangement under which an employer provides reimbursements or payments that are dedicated to providing medical care, such as cash reimbursements for the purchase of an individual market policy, is itself a group health plan. Accordingly, the arrangement is subject to the market reform provisions of the Affordable Care Act applicable to group health plans without regard to whether the employer treats the money as pre-tax or post-tax to the employee. Such employer health care arrangements cannot be integrated with individual market policies to satisfy the market reforms and, therefore, will fail to satisfy PHS Act §§ 2711 (annual limit prohibition) and 2713 (requirement to provide cost-free preventive services) among other provisions.

B. Reporting Requirements.

1. Employer Reporting on Form W-2.

Employers are required to disclose the aggregate cost of employer-sponsored health insurance coverage provided to their employees on the employee's Form W-2. Contributions to any health savings account (HSA) or Archer medical savings account (MSA) of the employee or the employee's spouse or salary reduction contributions to a flexible spending arrangement under a cafeteria plan will not be included. This employer disclosure requirement was to begin with the Form W-2 for the 2011 tax year. However, the IRS deferred the requirement, making it optional for 2011 Forms W-2, and generally effective for 2012 Forms W-2. Until the IRS issues further guidance, smaller employers that are required to file fewer than 250 Forms W-2 for the preceding calendar year are not subject to the reporting requirement. Employers are required to disclose the aggregate cost of "applicable employer-sponsored coverage" provided to employees annually on the employee's Form W-2 (IRC 6051(a)(14)). Regardless of whether the employee or employer pays for the coverage, the aggregate cost of the coverage reported is determined under rules similar to those used in IRC 4980B(F)(4) to determine the applicable premiums for purposes of the COBRA continuation coverage requirements of group health plans. They are determined on an annual basis, and may be based on the information available on December 31 of the year (Notice 2012-9) For purposes of the new reporting requirement, "applicable employer-sponsored coverage" means, with respect to any employee, coverage under any group health plan made available to the employee by the employer that is excludable from the employee's gross income under IRC 106. Coverage is treated as applicable employer-sponsored coverage regardless of whether the employer or employee pays for the coverage. Applicable employer-sponsored coverage does not include coverage for long- term care, accidents, or disability income insurance. Nor does it include coverage that applies to only a specified disease or illness, hospital indemnity, or other fixed indemnity insurance, the payment for which is not excludable from gross income and deductible under IRC 162(l).

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

23