©coursecollege.com 1 16 long term debt long term debt - liabilities with due dates greater than one...

TRANSCRIPT

©CourseCollege.com

1

16 Long Term Debt

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Long term debt -liabilities with

due dates greater than

one year.

Learning Objectives1. Explain accounting for long term

note origination and interest accrual

2. Describe various note types, repayment structures, collateral and loan agreements

3. Explain accounting for capital and operating lease obligations

4. Describe the structure of bonds, their issuance and interest payments

5. Analysis: Compute and explain debt coverage and times interest earned ratios

©CourseCollege.com

2

Objective 16.1: Explain accounting for long term note

origination and interest accrual

O16.1

Long term noteshave due datesbeyond the currentfiscal period*

*or the normal operating cycle whichever is longer

©CourseCollege.com

3

Written promise to pay

Long Term Notes

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Long term notes can be secured or unsecured

Maker is borrower and signs note

Payee is lender and holds note

O16.1

©CourseCollege.com

4

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

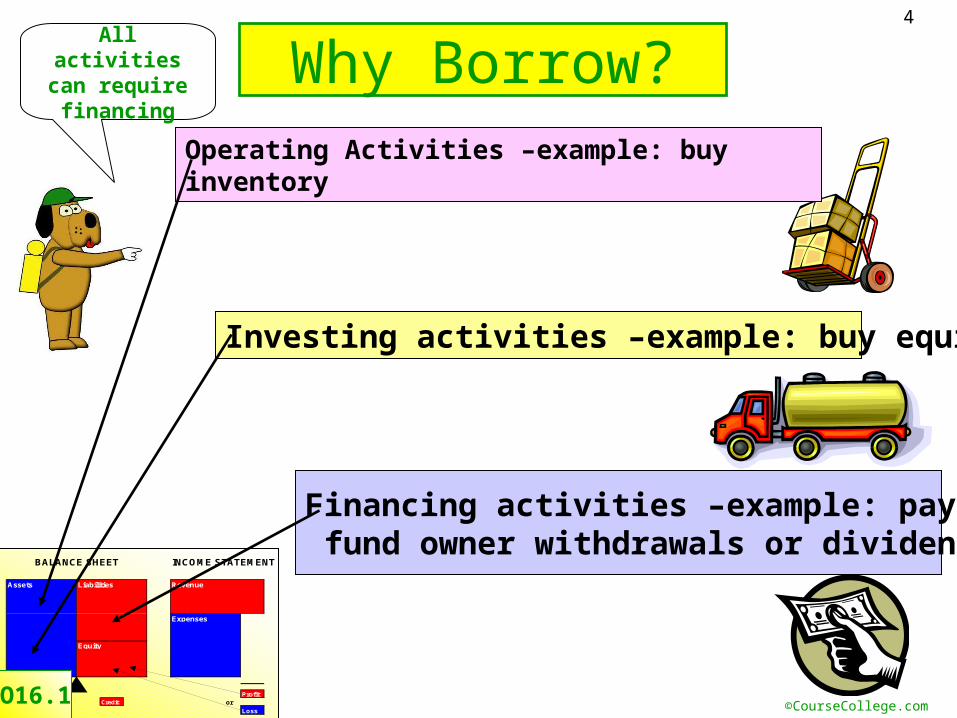

Why Borrow?All activities can require financing

Investing activities –example: buy equipment

Financing activities –example: payoff debt or fund owner withdrawals or dividends

Operating Activities –example: buy inventory

O16.1

©CourseCollege.com

5

Calculate interest accrued using the following formula:

Calculate interest accrued using the following formula:

With year end Dec 31, 2010, a 3 year note is signed Oct 1 for $100,000 at 8% with annual payments Oct

1

Interest expense and interest payable at year end:

$100,000 x .08 x 90/360 = $2000

With year end Dec 31, 2010, a 3 year note is signed Oct 1 for $100,000 at 8% with annual payments Oct

1

Interest expense and interest payable at year end:

$100,000 x .08 x 90/360 = $2000

Principal amount

Annual Interest

rate

Time Period

in yearsInterestX =

Long Term Notes Payable

Example

X

O16.1

©CourseCollege.com

6

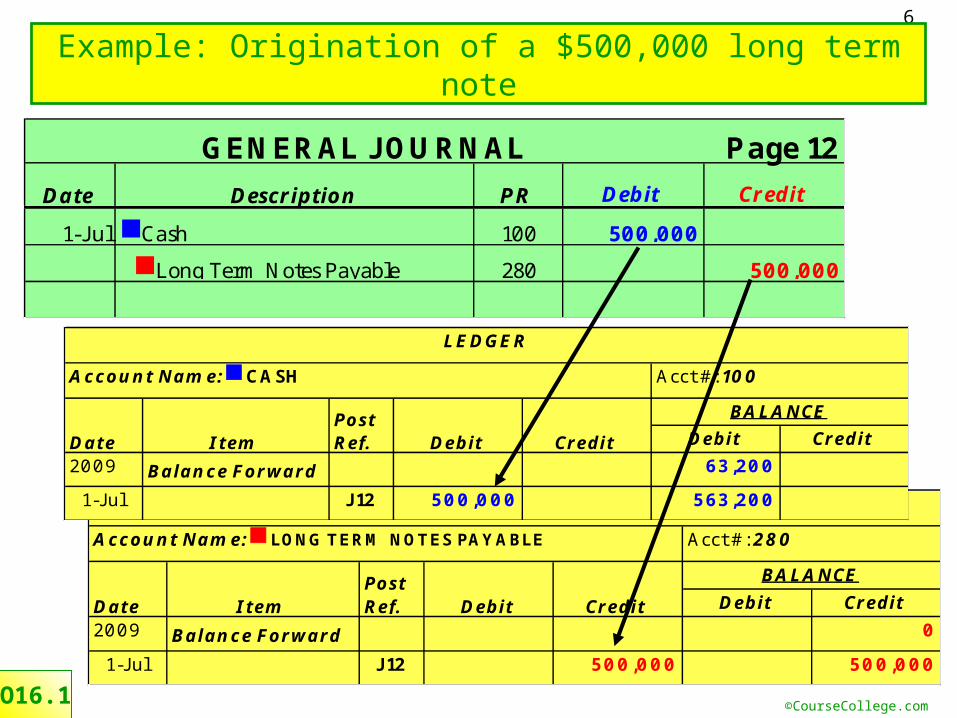

Debit Credit

2009 Balance Forward 0

1-Jul J12 500,000 500,000

LEDGER

Account Name: LONG TERM NOTES PAYABLE Acct #: 280

Date ItemPost Ref. Debit Credit

BALANCE

Debit Credit

2009 Balance Forward 63,200

1-Jul J12 500,000 563,200

LEDGER

Account Name: CASH Acct #: 100

Date ItemPost Ref. Debit Credit

BALANCE

O16.1

Page 12

Date Description PR Debit Credit

1-Jul Cash 100 500,000

Long Term Notes Payable 280 500,000

GENERAL JOURNAL

Example: Origination of a $500,000 long term note

©CourseCollege.com

7

Many note types

Objective 16.2: Describe various note types, repayment

structures, collateral and loan agreements

O16.2

Installment notes

Mortgage notes

Single Pay notes

Interest only notes

©CourseCollege.com

8

Some long term note types

O16.2

Installment notes

Mortgage notes

Single Pay notes

Interest only notesPeriodic interest payments with principal due at maturityPeriodic interest payments with principal due at maturity

Notes accompanying real estate mortgages which secure repaymentNotes accompanying real estate mortgages which secure repayment

Notes with a single payment of interest and principal at maturityNotes with a single payment of interest and principal at maturity

Notes with regular periodic payments of interest and principalNotes with regular periodic payments of interest and principal

©CourseCollege.com

9

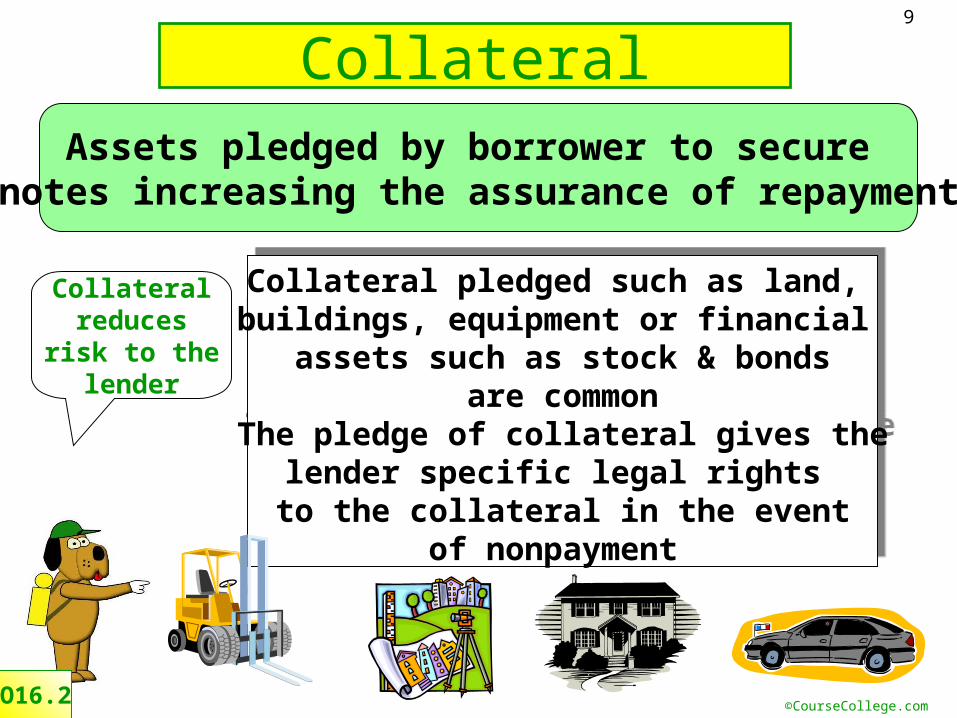

CollateralAssets pledged by borrower to secure

notes increasing the assurance of repayment

Collateral pledged such as land, buildings, equipment or financial

assets such as stock & bondsare common

The pledge of collateral gives thelender specific legal rights to the collateral in the event

of nonpayment

Collateral pledged such as land, buildings, equipment or financial

assets such as stock & bondsare common

The pledge of collateral gives thelender specific legal rights to the collateral in the event

of nonpayment

Collateral reduces

risk to the lender

O16.2

©CourseCollege.com

10

Installment Notes –equal principal payments

O16.2

$50,000

Principal Interest

$15,000

$50,000

$12,000

$50,000

$9,000

$50,000

$6,000

$50,000

$3,000

Declining total payments

Yr1

250,000 x .06 = 15,000

Yr2

(250,000-50,000)x .0

6 =12,000

Yr3

(200,000-50,000) x .06 = 9,000

Yr4

(150,000-50,000) x .06 = 6,000

Yr5

(100,000-50,000) x .06 = 3,000

Equal principal payments

©CourseCollege.com

11

Installment Notes –equal principal & interest payments

Original Annual Interest Principal Balance

Note amt payment Accrued reduction after payment

Year 1 $250,000 $59,349 - $15,000 = $44,349 $205,651

Year 2 $59,349 - $12,339 = $47,010 $158,641

Year 3 $59,349 - $9,518 = $49,831 $108,810

Year 4 $59,349 - $6,529 = $52,820 $55,990

Year 5 $59,349 - $3,359 = $55,990 $0

Original Annual Interest Principal Balance

Note amt payment Accrued reduction after payment

Year 1 $250,000 $59,349 - $15,000 = $44,349 $205,651

Year 2 $59,349 - $12,339 = $47,010 $158,641

Year 3 $59,349 - $9,518 = $49,831 $108,810

Year 4 $59,349 - $6,529 = $52,820 $55,990

Year 5 $59,349 - $3,359 = $55,990 $0

$44,349 $47,010

$15,000 $12,339

$49,831

$9,518

$52,820

$6,529$55,990 $3,359

Principal Interest

Yr1 Yr2 Yr3 Yr4 Yr5

Equal total payments

$59,3

49

©CourseCollege.com

12

O16.2

$44,349 $47,010

$15,000 $12,339

$49,831

$9,518

$52,820

$6,529$55,990 $3,359

Principal Interest

Yr1 Yr2 Yr3 Yr4 Yr5

Equal total payments

$59,3

49

Current Portion of Long Term Debt 44,349Long Term Debt 205,651 Total LTD 250,000

Year 1

Equity

Balance SheetAssets Liabilities

Current portion of long term debt

©CourseCollege.com

13

Objective 16.3: Explain accounting for capital and operating lease obligations

A lease is a rental agreement between the user and the owner of an asset

Depending on whether a transfer of ownership takes place, the lease may be

an operating lease or a capital lease

Accounting treatment is very different for the two types of leases

Depending on whether a transfer of ownership takes place, the lease may be

an operating lease or a capital lease

Accounting treatment is very different for the two types of leases

O16.3

©CourseCollege.com

14

Parties involved in a lease

O16.3

Lease Agreement

Lessor:__________Lessee:__________

Lease Agreement

Lessor:__________Lessee:__________ Lessee

Uses the AssetProvides the Asset

Lessor

Lessor

Lessee

©CourseCollege.com

15

Capital or Operating Lease?

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

O16.3

YES

Operating Lease

CapitalLease

NO

Virtually all benefits and risks of ownership transferred to

Lessee?

Capital lease is recorded

on the balance sheet

©CourseCollege.com

16

The 4 rules that qualify capital leases

1.The lease transfers ownership of the property to

the lessee.

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Record the leased asset and liability

on the balance sheet

It’s a capital lease if:

O16.3

©CourseCollege.com

17

The 4 rules that qualify capital leases

2.The lease contains a bargain purchase option.

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Record the leased asset and liability

on the balance sheet

It’s a capital lease if:

O16.3

©CourseCollege.com

18

The 4 rules that qualify capital leases

3.The lease term is 75% or more of the estimated

economic life of the leased asset.

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Record the leased asset and liability

on the balance sheet

It’s a capital lease if:

O16.3

©CourseCollege.com

19

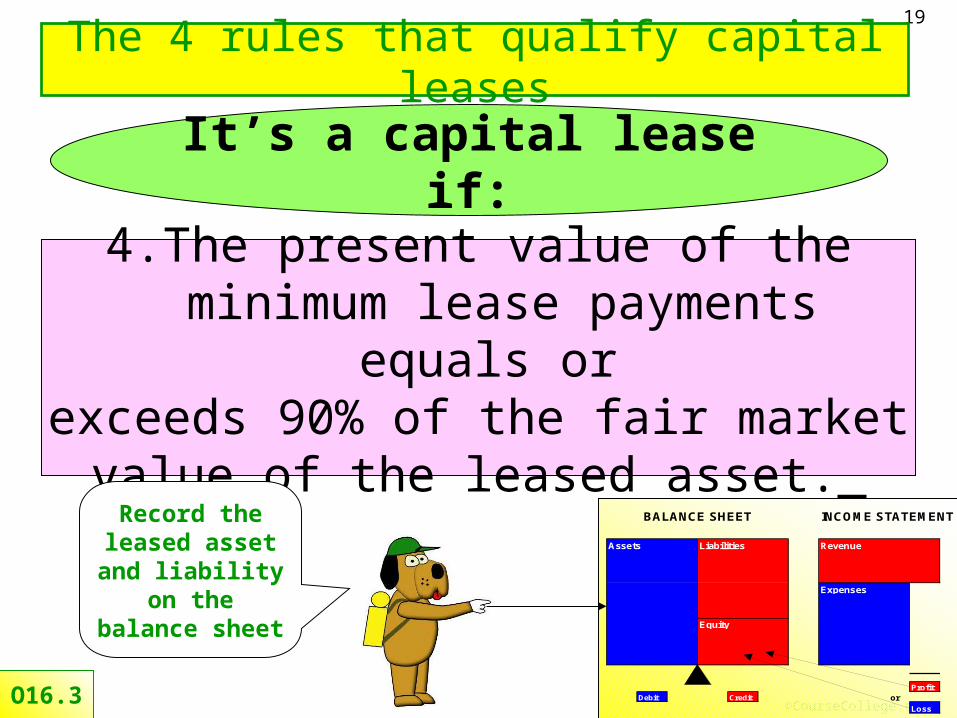

The 4 rules that qualify capital leases

4.The present value of the minimum lease payments equals

or exceeds 90% of the fair market

value of the leased asset.

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Record the leased asset and liability

on the balance sheet

It’s a capital lease if:

O16.3

©CourseCollege.com

20

Operating lease -example

O16.3

Cameron Construction signed a 24 month lease for a new compressor. There is no change in ownership and no bargain purchase option. The lease does not meet the 75% and 90% test as shown below. Therefore, this is an operating lease. No asset or liability is recorded, rental payments are expensed as incurred.

Page 4

Date Description PR Debit Credit

1-May Equipment Rental Expense 565 5,500

Cash 100 5,500

GENERAL JOURNAL

Compressor Lease DetailsLease Lease Fair Value Economic 75% of Econ Present 90% of

Payment Term of Equip Life Life Value Fair value706$ 2 years 24,000$ 10 years 7.5 years $15,000 21,600$

Compressor Lease DetailsLease Lease Fair Value Economic 75% of Econ Present 90% of

Payment Term of Equip Life Life Value Fair value706$ 2 years 24,000$ 10 years 7.5 years $15,000 21,600$

Date of first payment

©CourseCollege.com

21

Capital lease -example

O16.3

Boone Excavating signed a 48 month lease for a new backhoe. There is no change in ownership and no bargain purchase option. The lease meets the 90% test as shown below. Therefore, this is a capital lease. Therefore, the present value of the lease payments is recorded as the leased asset and the lease obligation on the balance sheet as the journal entry below illustrates.

Page 4

Date Description PR Debit Credit

1-Apr Leased Backhoe 565 65,000

Lease Obligation Payable 100 65,000

GENERAL JOURNAL

Backhoe Lease DetailsLease Lease Fair Value Economic 75% of Econ Present 90% of

Payment Term of Equip Life Life Value Fair value1,712$ 4 years 70,000$ 6 years 5 years $65,000 63,000$

Backhoe Lease DetailsLease Lease Fair Value Economic 75% of Econ Present 90% of

Payment Term of Equip Life Life Value Fair value1,712$ 4 years 70,000$ 6 years 5 years $65,000 63,000$

Present value is greater than 90% of fair value, therefore this is a capital lease

©CourseCollege.com

22

Objective 16.4: Describe the structure of bonds, their

issuance and interest payments

O16.4

Bonds are a common form of long term debt available, in general, to large publicly traded firms.

Bonds are a common form of long term debt available, in general, to large publicly traded firms.

The Securities and Exchange

Commission regulates bond

issuance by publicly traded firms

©CourseCollege.com

23

Bonds differ from direct commercial loans in that the source of funds for bonds can consist of a large number individual and institutional investors, each of which would own a portion of the total bond debt. With direct commercial loans, the source of loan funds are from a single financial institution.

Bonds differ from direct commercial loans in that the source of funds for bonds can consist of a large number individual and institutional investors, each of which would own a portion of the total bond debt. With direct commercial loans, the source of loan funds are from a single financial institution.

Bonds compared to commercial loans

O16.4

©CourseCollege.com

24

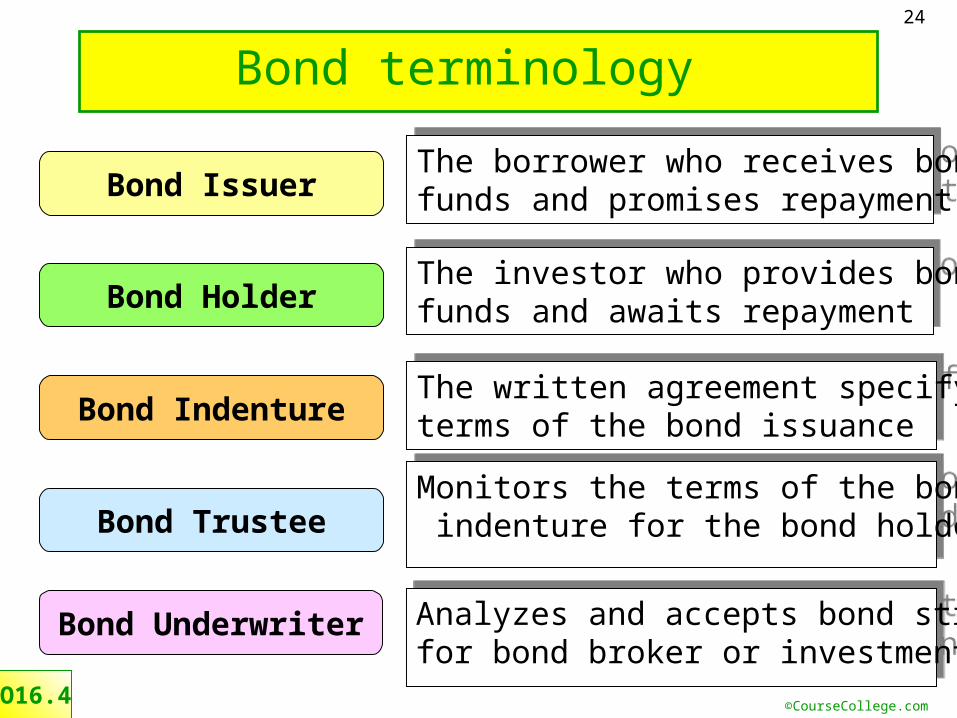

Bond terminology

O16.4

Bond Trustee

Bond Holder

Bond Indenture

Bond IssuerThe borrower who receives bond funds and promises repaymentThe borrower who receives bond funds and promises repayment

The investor who provides bondfunds and awaits repaymentThe investor who provides bondfunds and awaits repayment

The written agreement specifyingterms of the bond issuanceThe written agreement specifyingterms of the bond issuance

Monitors the terms of the bond indenture for the bond holdersMonitors the terms of the bond indenture for the bond holders

Bond Underwriter Analyzes and accepts bond structurefor bond broker or investment bankAnalyzes and accepts bond structurefor bond broker or investment bank

©CourseCollege.com

25

Floating a bond issue

O16.4

Trustee

Bond Holder(Investor)

Bond Issuer

Underwriter

Bond IndentureBond

Indenture

BondBond

©CourseCollege.com

26

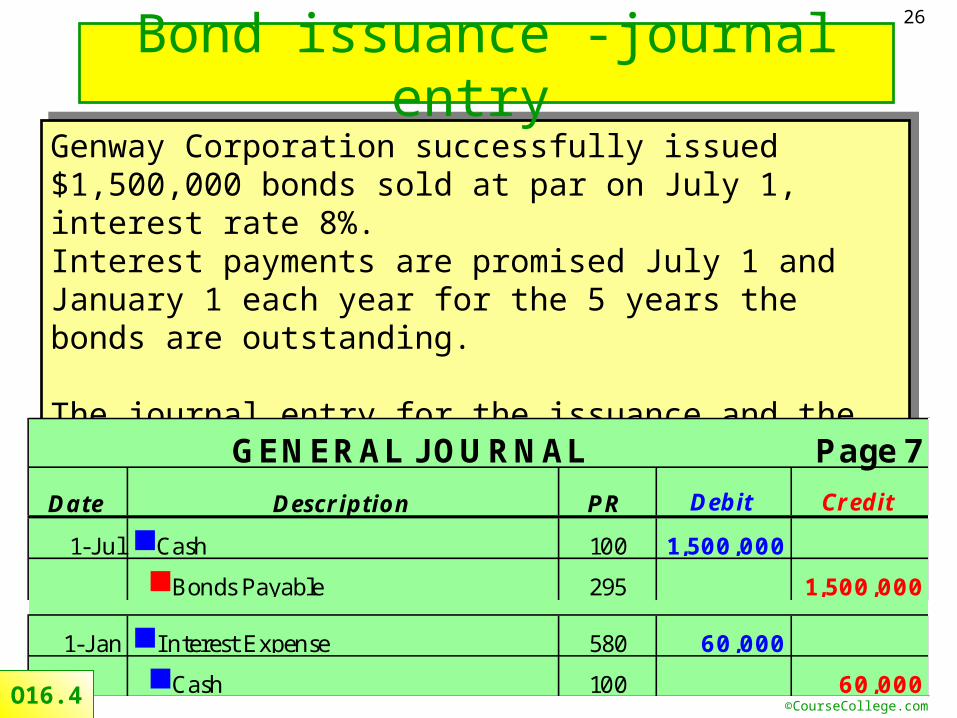

Genway Corporation successfully issued $1,500,000 bonds sold at par on July 1, interest rate 8%.Interest payments are promised July 1 and January 1 each year for the 5 years the bonds are outstanding.

The journal entry for the issuance and the first interest payment is shown below.

Genway Corporation successfully issued $1,500,000 bonds sold at par on July 1, interest rate 8%.Interest payments are promised July 1 and January 1 each year for the 5 years the bonds are outstanding.

The journal entry for the issuance and the first interest payment is shown below.

Bond issuance -journal entry

Page 7

Date Description PR Debit Credit

1-Jul Cash 100 1,500,000

Bonds Payable 295 1,500,000

1-Jan Interest Expense 580 60,000

Cash 100 60,000

GENERAL JOURNAL

O16.4

©CourseCollege.com

27

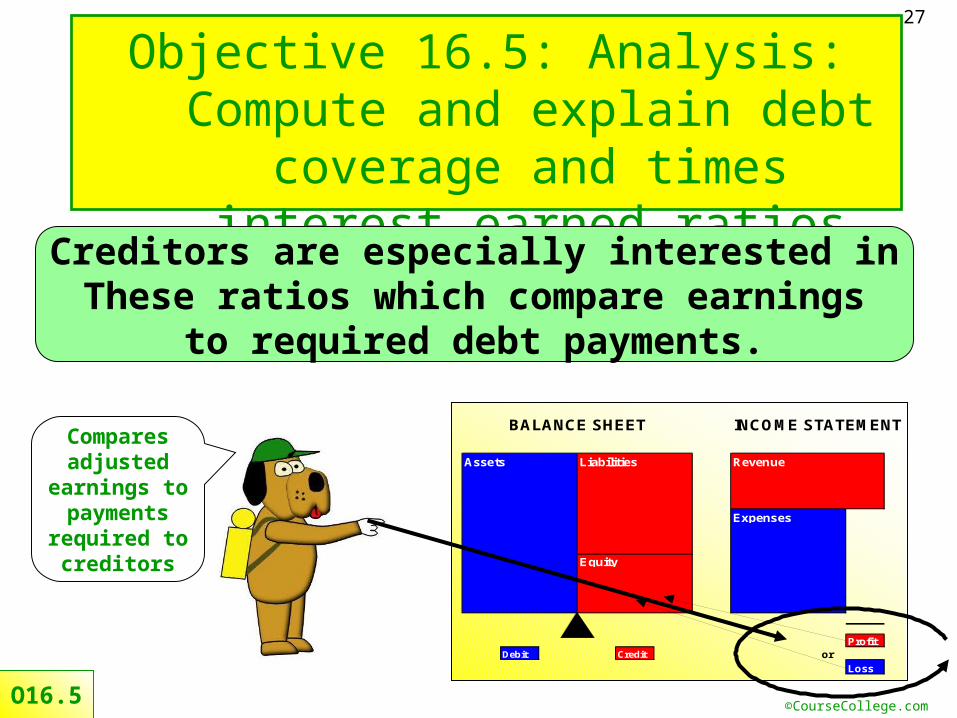

Objective 16.5: Analysis: Compute and explain debt

coverage and times interest earned ratios

ProfitDebit Credit or

Loss

Expenses

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Revenue

Equity

Compares adjusted

earnings to payments

required to creditors

O16.5

Creditors are especially interested inThese ratios which compare earnings

to required debt payments.

©CourseCollege.com

28

Times Interest Earned RatioAdjusted accrual income = the sum of accrual net income + interest expense + income tax expense + non cash expenses such as depreciation, amortization and depletion.

The higher the ratio, the more adequate earnings

are to cover interest expense

O16.5

Times interest earned

Interest expense

Adjusted accrual income=

©CourseCollege.com

29

Debt Coverage RatioAdjusted accrual income = the sum of accrual net income + interest expense + income tax expense + non cash expenses such as depreciation, amortization and depletion.

The higher the ratio, the more adequate earnings are to cover debt service

payments

O16.5

Debt Coverage Principal & Interest

payments

Adjusted accrual income=

©CourseCollege.com

30

Example -Times interest earned and Debt coverage ratios

O16.5

Assets LiabilitiesCash 123,000 Accounts Payable 536,700Accounts receivable 345,000 Current Portion Long Term Debt 138,600Inventory 410,500 Long Term Debt 823,400Property, Plant, Equipment 1,200,500 Total liabilities 1,498,700

Equity Total assets 2,079,000 Owner, Capital 580,300

Sales 2,347,000

Cost of Goods Sold 1,760,250 Adjusted accrual income 376,150Wages expense 210,600 (NP +Inc tax exp + Int exp + depr)Depreciation expense 60,025 Times Interest earned 4.3Interest expense 86,580 Adjusted accrual income / Interest expenseMisc expense 38,400 Debt Coverage 1.7

Net Profit 191,145

Balance Sheet -Ruiz RecyclingAs of 12/31 2009

Adjusted accrual income/ ( Principal + Interest exp)

Income StatementFor the year ended 12/31/09

X

X

©CourseCollege.com

31

End Unit 16