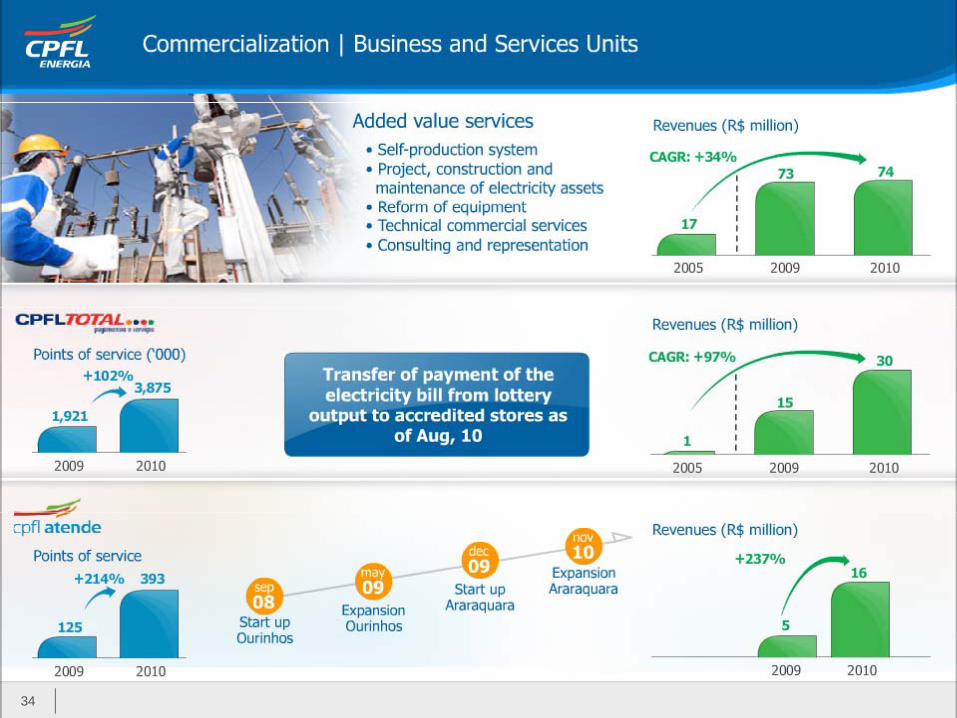

cpfl energia institucional jun11_eng_final

TRANSCRIPT

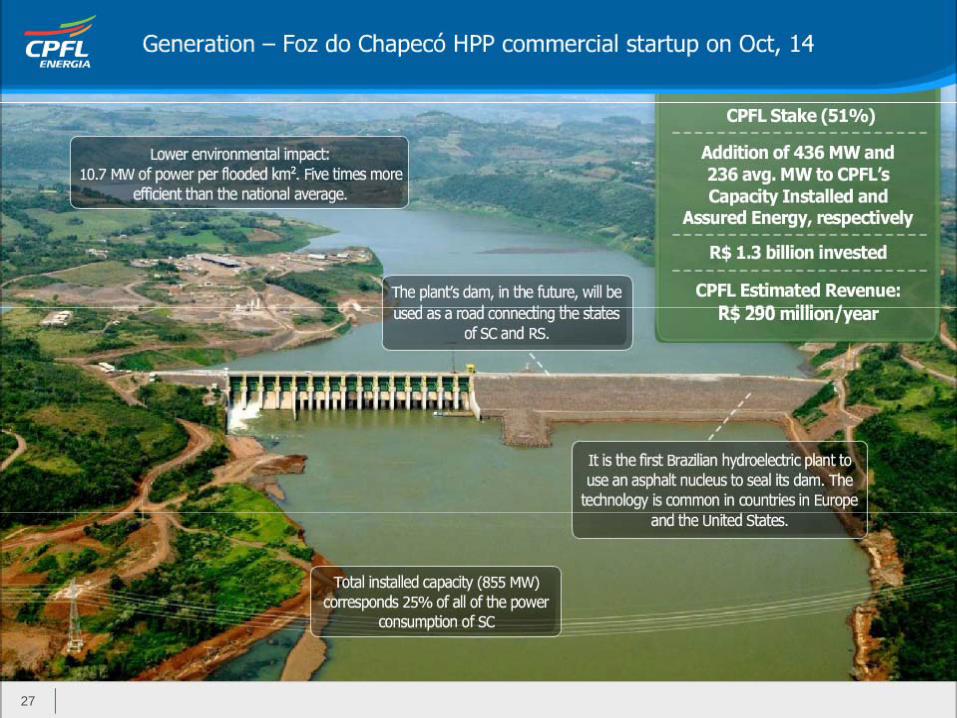

Foz do Chapecó HPPOverview: dam | reservoir

Disclaimer

This presentation may contain statements that represent expectations about future events or results according to Brazilian

and international securities regulators. These statements are based on certain assumptions and analyses made by the

C t t it i d th i i t k t diti d t d f t tCompany pursuant to its experience and the economic environment, market conditions and expected future events, many

of which are beyond the Company's control. Important factors that could lead to significant differences between actual

results and expectations about future events or results include the Company's business strategy, Brazilian and international

economic conditions, technology, financial strategy, developments in the utilities industry, hydrological conditions, financial

market conditions uncertainty regarding the results of future operations plans objectives expectations and intentionsmarket conditions, uncertainty regarding the results of future operations, plans, objectives, expectations and intentions,

among others. Considering these factors, the Company's actual results may differ materially from those indicated or implied

in forward-looking statements about future events or results.

The information and opinions contained herein should not be construed as a recommendation to potential investors and no

investment decision should be based on the truthfulness, timeliness or completeness of such information or opinions. None

of the advisors to the company or parties related to them or their representatives shall be liable for any losses that may

result from the use or contents of this presentation.

This material includes forward-looking statements subject to risks and uncertainties which are based on currentThis material includes forward looking statements subject to risks and uncertainties, which are based on current

expectations and projections about future events and trends that may affect the Company's business. These statements

may include projections of economic growth, demand, energy supply, as well as information about its competitive position,

the regulatory environment, potential growth opportunities and other matters. Many factors could adversely affect the

estimates and assumptions on which these statements are based.est ates a d assu pt o s o c t ese state e ts a e based

2

Agenda

Corporate Overview

Operational Efficiency

Growth in the Generation Business

Wide Portfolio of Services

1 t i l M k C

Corporate overview – Highlights

1st private player in the electric sector in terms of Market Cap (R$ 22 billion in Mar, 2011)

R$ 3.4 billion EBITDA and R$ 1.6 billion Net Income in 2010

The largest private player

in the BrazilianMain player in Renewable Energy in Latin America

Leadership in the distribution business through 8 distributors. Energy market is concentrated in the most

in the Brazilian Electric Sector

d bu o gy a co ce t ated t e ostdeveloped regions of Brazil

2,640 MW(e) generation installed capacity in FY11, 93% renewable sources. 17 wind farms, 5 biomass

S ll P Pl t d t tiplants and 1 Small Power Plant under construction

Successful strategy in the commercialization business

B ’ Novo Mercado d NYSE’ ADR Level IIIBovespa’s Novo Mercado and NYSE’s ADR Level III

Differentiated Dividend Policy: minimum 50% of the net income semi-annually. Practices 95%

Most sustainable electricity company in Latin America for the3rd consecutive year by Management & Excellence

4

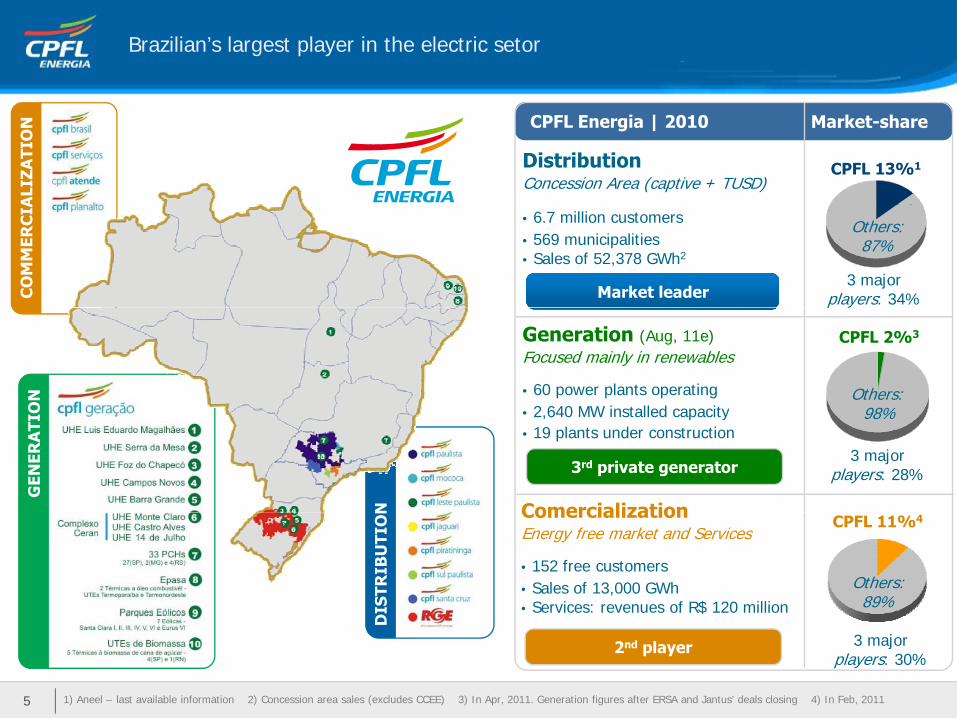

Brazilian’s largest player in the electric setor

CPFL Energia | 2010

CPFL 13%1

Market-share

DistributionConcession Area (captive + TUSD)

ALI

ZATI

ON

Others: 87%

• 6.7 million customers• 569 municipalities• Sales of 52,378 GWh2

Market leader3 major

players: 34% CO

MM

ERC

IA

CPFL 2%3Generation (Aug, 11e)Focused mainly in renewables

• 60 power plants operating2 640 MW installed capacity

Others: 98%

p y

ON

• 2,640 MW installed capacity• 19 plants under construction

Comercialization

3rd private generator

98%

3 majorplayers: 28%

N

GEN

ERA

TIO

CPFL 11%4ComercializationEnergy free market and Services

• 152 free customers• Sales of 13,000 GWh• Services: revenues of R$ 120 million

Others:89%

DIS

TRIB

UTI

ON

1) Aneel – last available information 2) Concession area sales (excludes CCEE) 3) In Apr, 2011. Generation figures after ERSA and Jantus’ deals closing 4) In Feb, 20115

$

2nd player 3 majorplayers: 30%

D

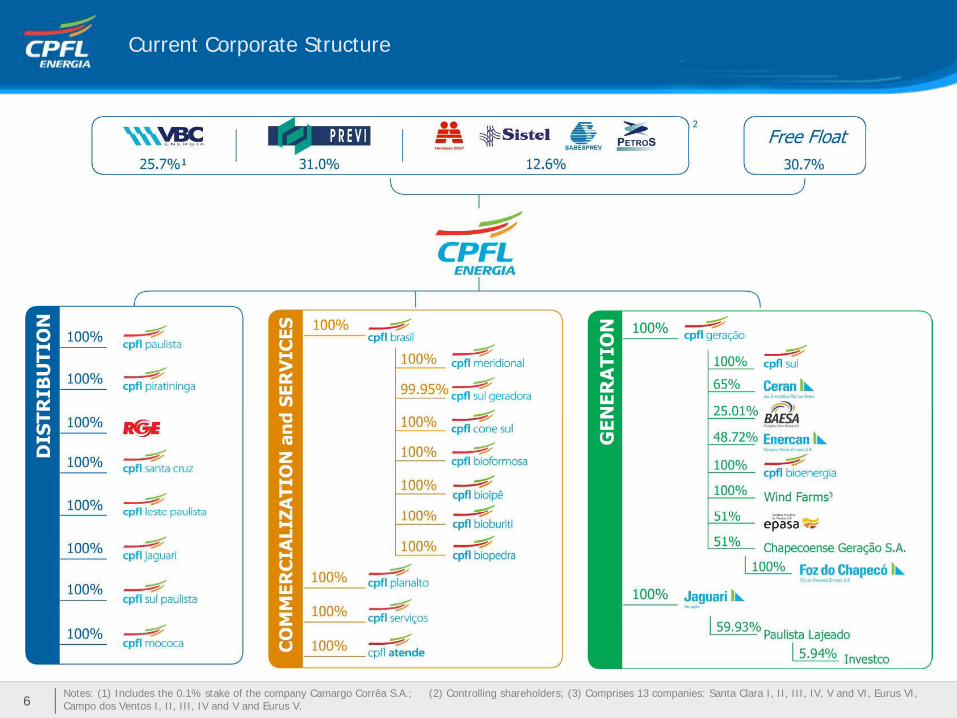

Current Corporate Structure

Notes: (1) Includes the 0.1% stake of the company Camargo Corrêa S.A.; (2) Controlling shareholders; (3) Comprises 13 companies: Santa Clara I, II, III, IV, V and VI, Eurus VI, Campo dos Ventos I, II, III, IV and V and Eurus V.6

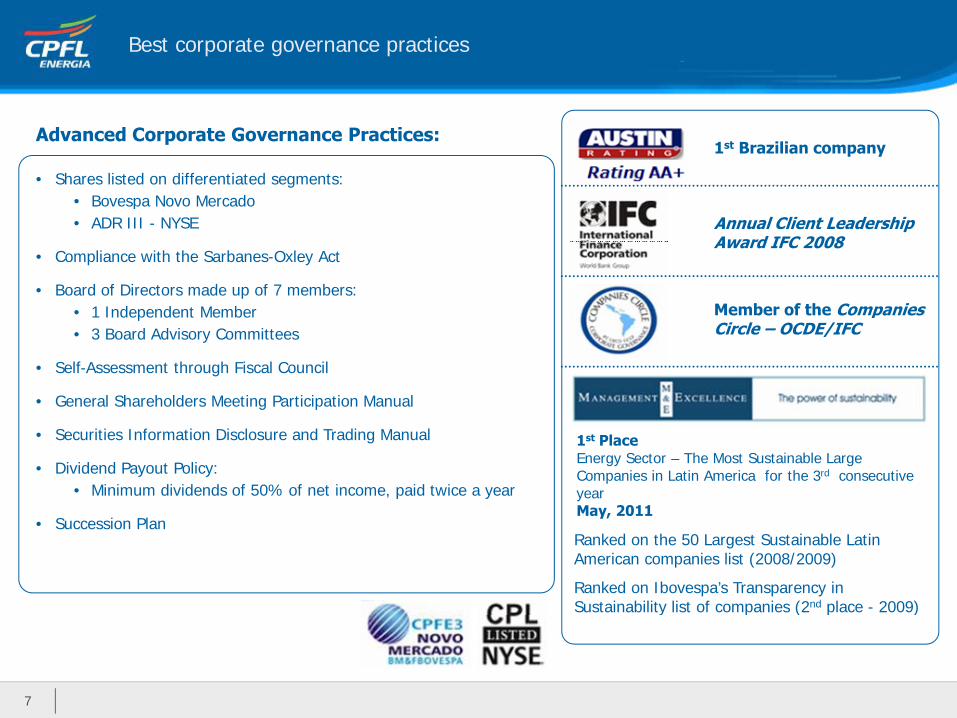

Best corporate governance practices

• Shares listed on differentiated segments:• Bovespa Novo Mercado

1st Brazilian companyAdvanced Corporate Governance Practices:

Bovespa Novo Mercado• ADR III - NYSE

• Compliance with the Sarbanes-Oxley Act

• Board of Directors made up of 7 members:1 I d d t M b

Annual Client Leadership Award IFC 2008

Member of the Companies• 1 Independent Member• 3 Board Advisory Committees

• Self-Assessment through Fiscal Council

• General Shareholders Meeting Participation Manual

Member of the Companies Circle – OCDE/IFC

• Securities Information Disclosure and Trading Manual

• Dividend Payout Policy:• Minimum dividends of 50% of net income, paid twice a year

1st PlaceEnergy Sector – The Most Sustainable Large Companies in Latin America for the 3rd consecutive yearMay 2011

• Succession PlanRanked on the 50 Largest Sustainable Latin American companies list (2008/2009)

Ranked on Ibovespa’s Transparency in Sustainability list of companies (2nd place - 2009)

May, 2011

y p ( p )

7

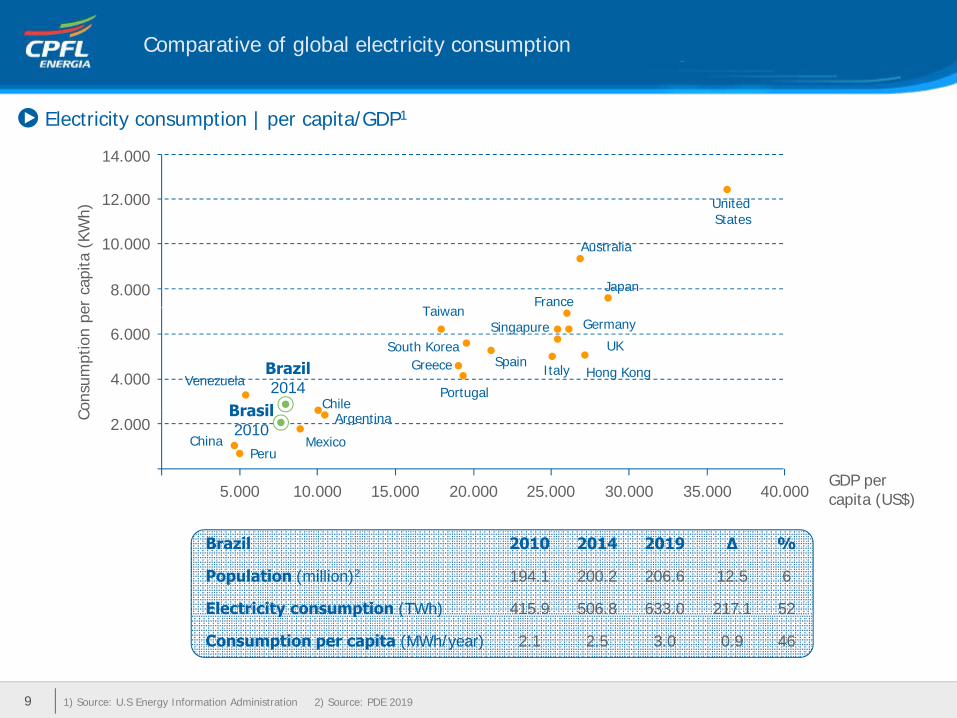

Comparative of global electricity consumption

Electricity consumption | per capita/GDP1

) 12.000

14.000

United

er c

apita

(KW

h)

8.000

10.000

000

T iFrance

Australia

Japan

United States

onsu

mpt

ion

pe

4.000

6.000

Venezuela

ChileBrasilPortugal

GreeceSouth Korea

Taiwan

Spain

Singapure

Italy

Germany

UK

Hong KongBrazil2014

Co

5.000 10.000 15.000 20.000 25.000 30.000 35.000 40.000

2.000China

PeruMexico

ArgentinaBrasil2010

GDP per capita (US$)

Brazil 2010 2014 2019 ∆ %

Population (million)2 194.1 200.2 206.6 12.5 6

Electricity consumption (TWh) 415.9 506.8 633.0 217.1 52

1) Source: U.S Energy Information Administration 2) Source: PDE 2019

y p ( )

Consumption per capita (MWh/year) 2.1 2.5 3.0 0.9 46

9

10

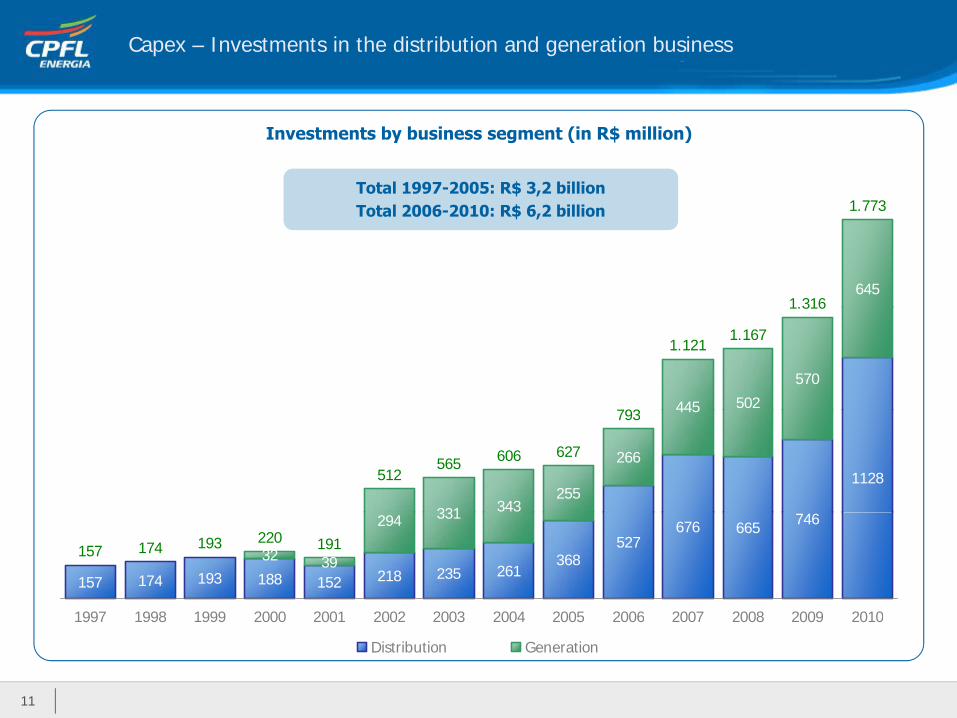

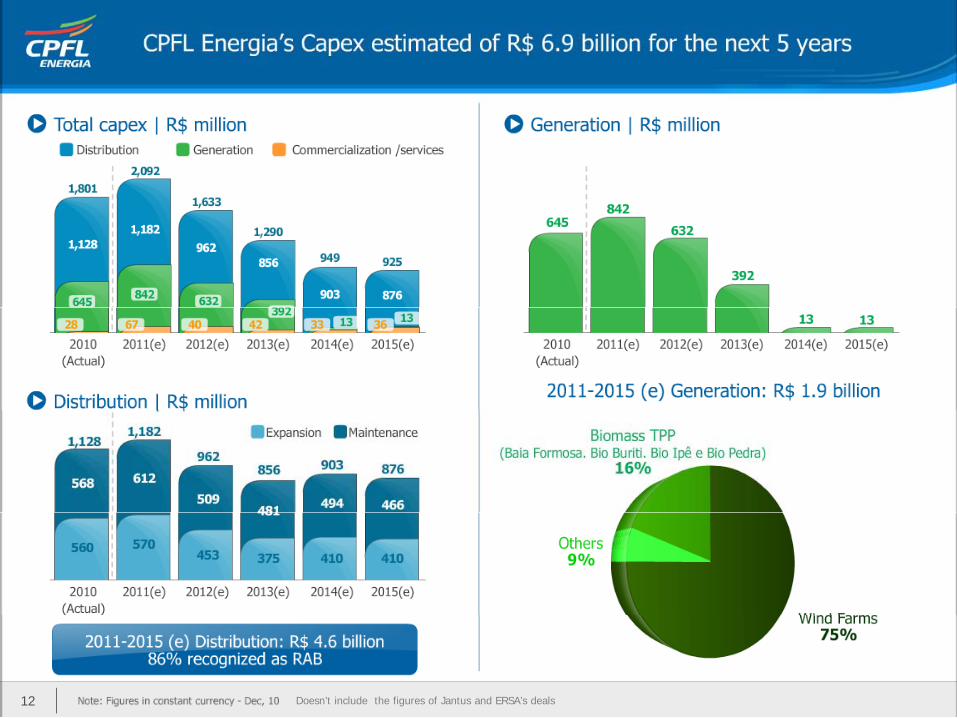

Capex – Investments in the distribution and generation business

1 773

Investments by business segment (in R$ million)

Total 1997-2005: R$ 3,2 billionT l 2006 2010 R$ 6 2 billi

6451.316

1.773Total 2006-2010: R$ 6,2 billion

445 502

570

793

1.1211.167

1.316

1128

331 343255

266

445

512565 606 627

793

157 174 193 188 152 218 235 261368

527676 665 746

32 39

294 331

157 174 193 220 191

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20101997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Distribution Generation

11

12 Doesn’t include the figures of Jantus and ERSA’s deals

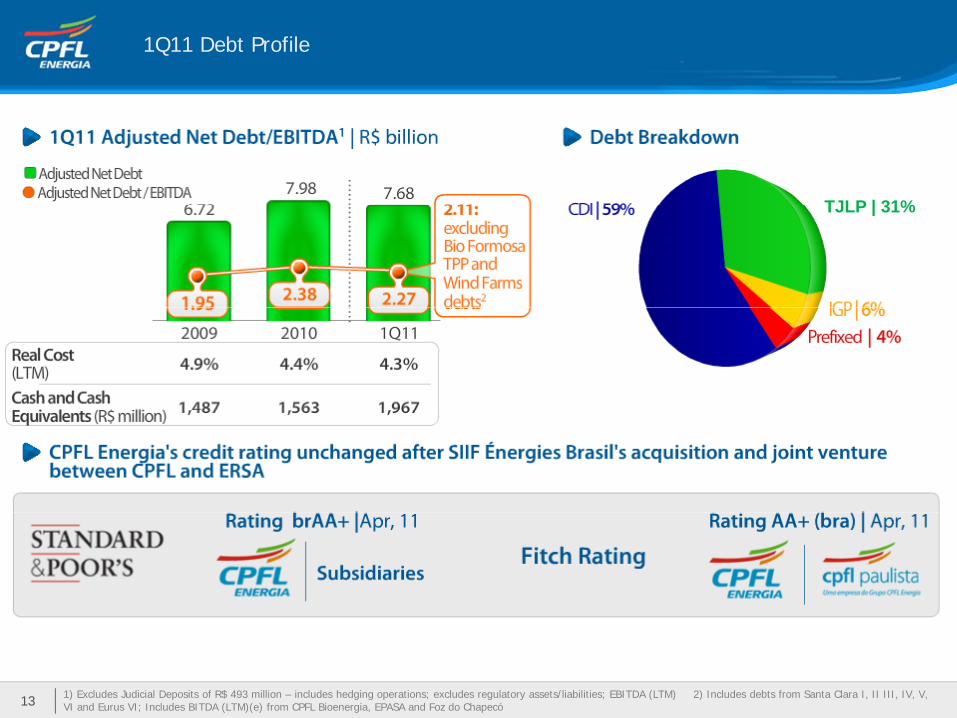

1Q11 Debt Profile

The largest private player

in the Brazilian TJLP | 31%in the Brazilian Electric Sector

TJLP | 31%

13 1) Excludes Judicial Deposits of R$ 493 million – includes hedging operations; excludes regulatory assets/liabilities; EBITDA (LTM) 2) Includes debts from Santa Clara I, II III, IV, V, VI and Eurus VI; Includes BITDA (LTM)(e) from CPFL Bioenergia, EPASA and Foz do Chapecó

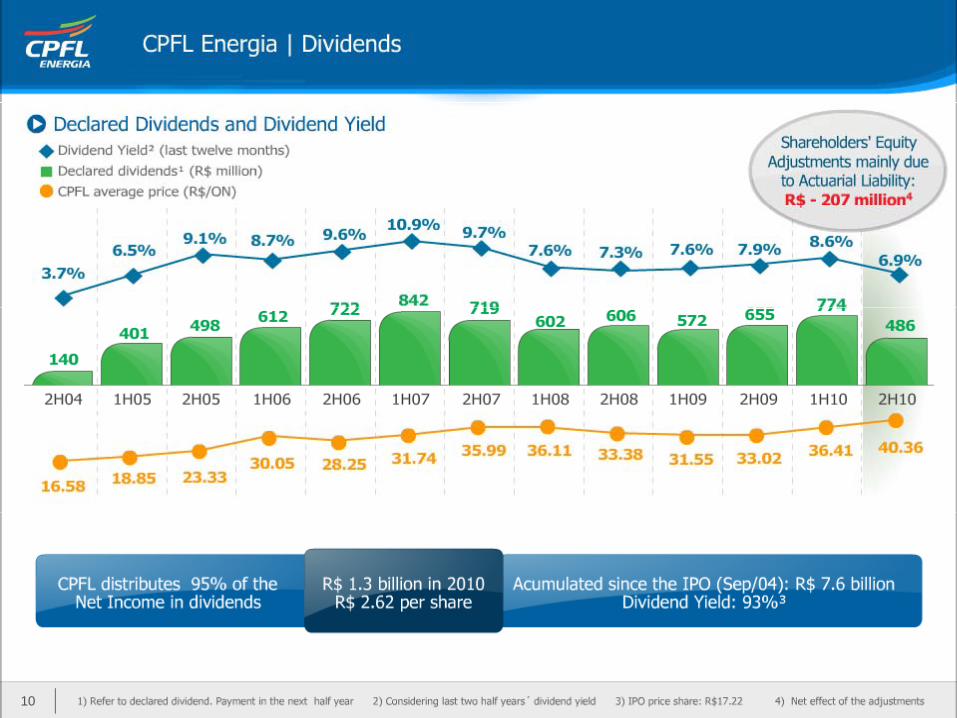

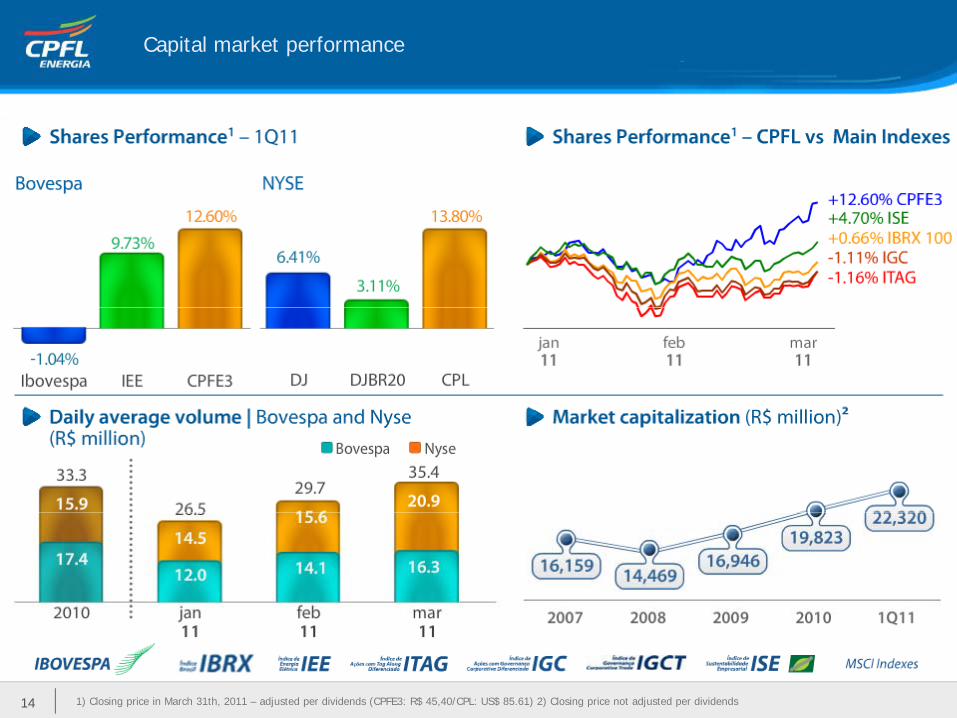

Capital market performance

1) Closing price in March 31th, 2011 – adjusted per dividends (CPFE3: R$ 45,40/CPL: US$ 85.61) 2) Closing price not adjusted per dividends14

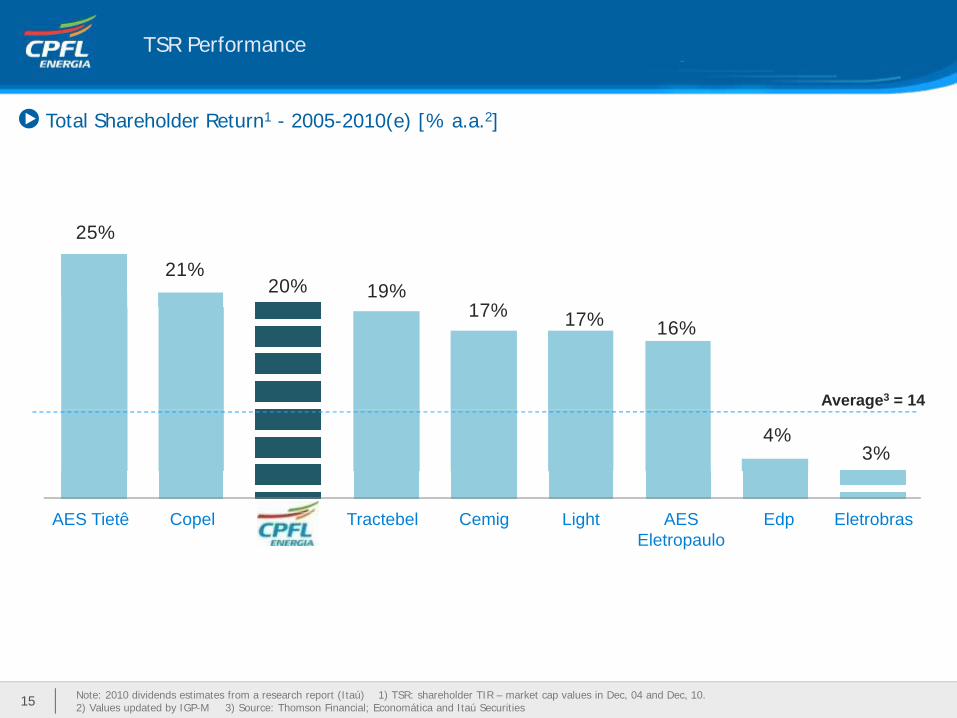

TSR Performance

Total Shareholder Return1 - 2005-2010(e) [% a.a.2]

25%

21%20% 19%

17%17% 17% 16%

Average3 = 14

4%3%

AES Ti ê C l T b l C i Li h AES Ed El bAES Tietê Copel Tractebel Cemig Light AES Eletropaulo

Edp Eletrobras

Note: 2010 dividends estimates from a research report (Itaú) 1) TSR: shareholder TIR – market cap values in Dec, 04 and Dec, 10. 2) Values updated by IGP-M 3) Source: Thomson Financial; Economática and Itaú Securities15

Agenda

Corporate Overview

Operational Efficiency

Growth in the Generation Business

Wide Portfolio of Services

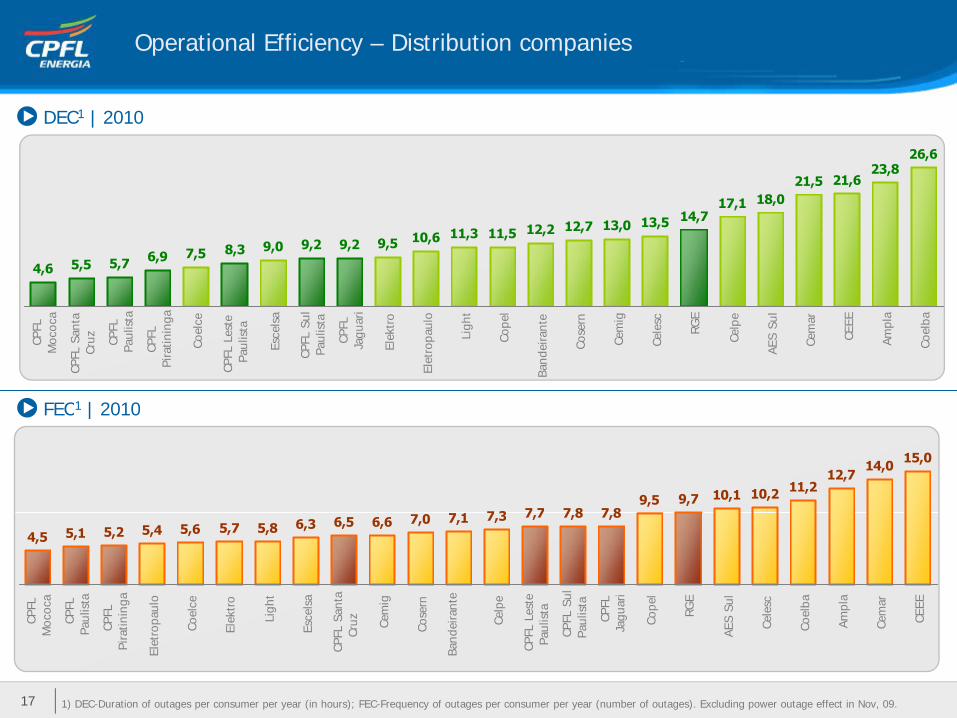

Operational Efficiency – Distribution companies

17 1 18,021,5 21,6

23,826,6

DEC1 | 2010

4,66,9 7,5 8,3 9,0 9,2 9,2 9,5 10,6 11,3 11,5 12,2 12,7 13,0 13,5 14,7

17,1 ,

5,75,5

CPFL

Moc

oca

CPFL

San

taCr

uz CPFL

Paul

ista

CPFL

Pira

tinin

ga

Coel

ce

CPFL

Les

tePa

ulis

ta

Esce

lsa

CPFL

Sul

Paul

ista

CPFL

Jagu

ari

Elek

tro

Elet

ropa

ulo

Ligh

t

Cope

l

Band

eira

nte

Cose

rn

Cem

ig

Cele

sc

RGE

Celp

e

AES

Sul

Cem

ar

CEEE

Ampl

a

Coel

ba

FEC1 | 2010FEC | 2010

7 3 7 7 7 8 7 89,5 9,7 10,1 10,2 11,2

12,714,0 15,0

4,5 5,4 5,6 5,7 5,8 6,3 6,5 6,6 7,0 7,1 7,3 7,7 7,8 7,85,25,1

PFL

coca

PFL

lista

FL inga

aulo

elce

ktro

ight

elsa

anta

z emig

sern

ante

elpe

Lest

est

a L Su

lis

ta

CPFL uari

opel

RGE

Sul

lesc

elba

mpl

a

mar

EEE

1) DEC-Duration of outages per consumer per year (in hours); FEC-Frequency of outages per consumer per year (number of outages). Excluding power outage effect in Nov, 09.17

CP

Moc C

PPa

u

CP F

Pira

tini

Ele

trop

a

Coe

Ele

k

Li

Esc

CPF

L S

Cruz Ce

Cos

Ban

deira Ce

CPF

L L

Paul

is

CPF

LPa

ul C Jag

Co R

AES

Ce l

Coe

Am

Cem CE

Operational Efficiency – Distribution companies

Dec 09 1Q11

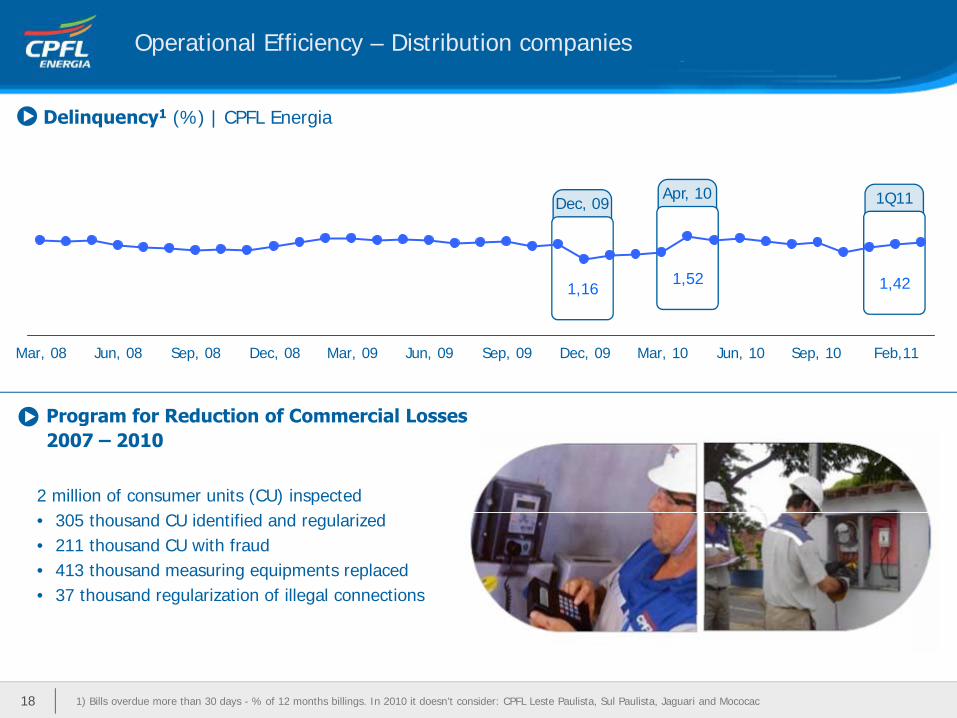

Delinquency1 (%) | CPFL Energia

Apr, 10Dec, 09

1,16

Q

1,421,52

P f R d ti f C i l L

Mar, 08 Jun, 08 Sep, 08 Dec, 08 Mar, 09 Jun, 09 Sep, 09 Dec, 09 Mar, 10 Jun, 10 Sep, 10 Feb,11

Program for Reduction of Commercial Losses2007 – 2010

2 million of consumer units (CU) inspected• 305 thousand CU identified and regularized• 211 thousand CU with fraud• 413 thousand measuring equipments replaced• 37 thousand regularization of illegal connections

18 1) Bills overdue more than 30 days - % of 12 months billings. In 2010 it doesn’t consider: CPFL Leste Paulista, Sul Paulista, Jaguari and Mococac

CPFL Energia Group’s Awards

Abradee

Best Electric Energy Distribution Company in Brazil: CPFL Paulista 2000|2003|2006|2008|2009

Economic-Financial Management: CPFL Paulista – 1999|2000|2008CPFL Piratininga 2004|2007CPFL Paulista–2000|2003|2006|2008|2009

RGE – 2010

Best Electric Energy Distribution Company in the South RegionRGE – 2003|2009|2010

CPFL Piratininga – 2004|2007

Management Quality: CPFL Paulista – 2005|2006|2008|2009CPFL Piratininga – 2010

RGE 2003|2009|2010

Operational Management: CPFL Paulista – 2001|2003|2005|2007|2008RGE – 2010

Best Social Responsibility:CPFL Paulista – 2002|2003|2004|2005|2008RGE – 2009|2010

PNQ® – National Quality Award

19

Awarded Awarded Finalist

Agenda

Corporate Overview

Operational Efficiency

Growth in the Generation Business

Wide Portfolio of Services

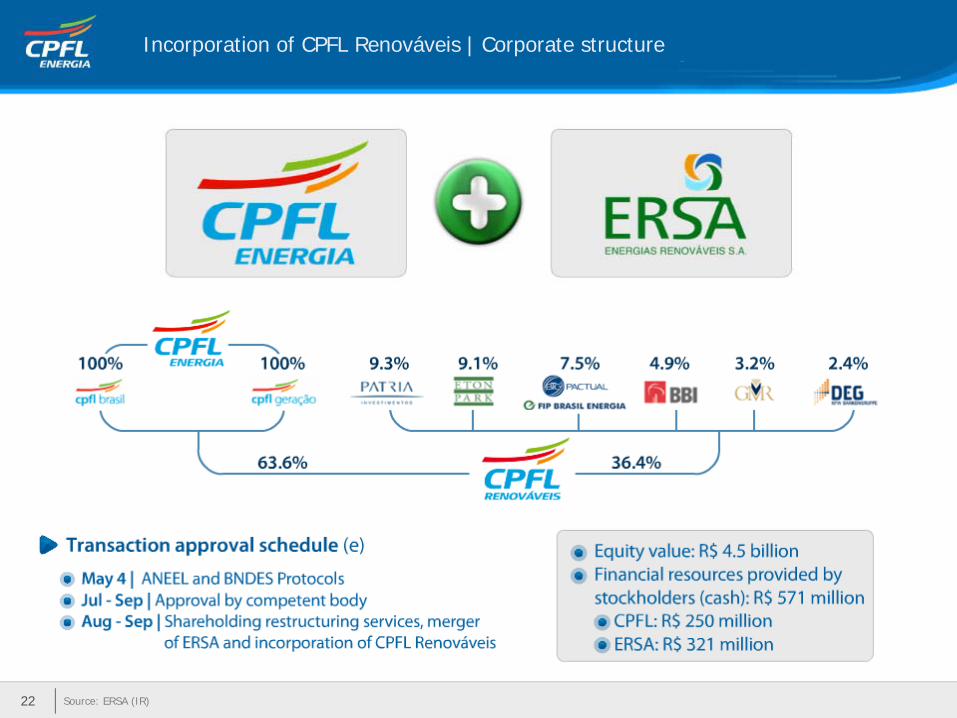

Incorporation of CPFL Renováveis | Corporate structure

Source: ERSA (IR)21

Incorporation of CPFL Renováveis | Corporate structure

Source: ERSA (IR)22

á

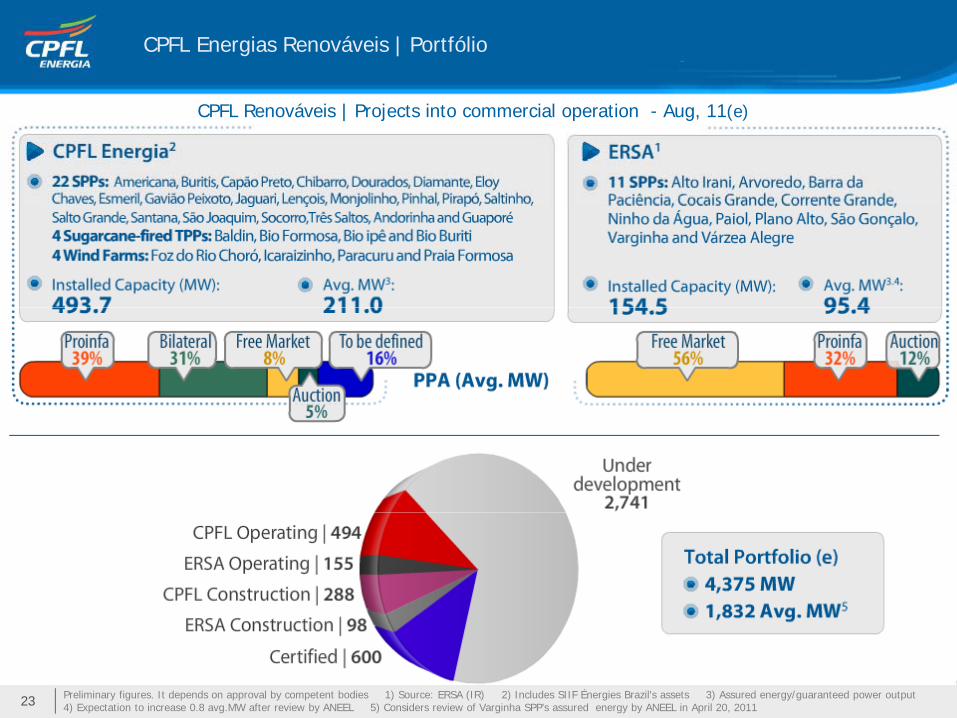

CPFL Energias Renováveis | Portfólio

CPFL Renováveis | Projects into commercial operation - Aug, 11(e)

Preliminary figures. It depends on approval by competent bodies 1) Source: ERSA (IR) 2) Includes SIIF Énergies Brazil's assets 3) Assured energy/guaranteed power output 4) Expectation to increase 0.8 avg.MW after review by ANEEL 5) Considers review of Varginha SPP’s assured energy by ANEEL in April 20, 201123

CPFL Energias Renováveis | Portfolio

SPP

Installed capacity(Total: 4,375 MW)3,341 4,375

Installed capacity (MW)Assured energy (AvgMW)

Bio36%

18%

Wind648

386

1,359 1,832

45%648

Operating (Aug, 11) Under construction

TotalUnder development

306 167

Estimated EvolutionInstalled capacity (MW)Assured energy (AvgMW)

Assured Energy(Total 1,832 AvgMW)

SPP25%2 092

4,375

Bio31%

25%

Wind44%

648306

907410

1,174538

1,692

742

2,092

920

1,832

2011 2012 2013 2014 2015 Total

24

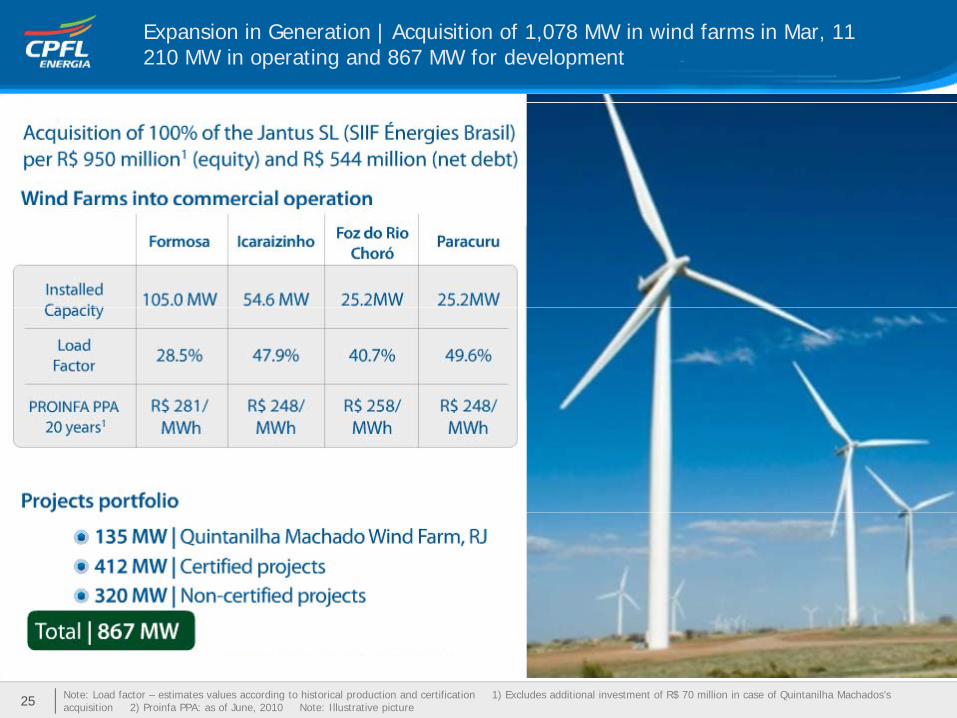

Expansion in Generation | Acquisition of 1,078 MW in wind farms in Mar, 11210 MW in operating and 867 MW for development

Note: Load factor – estimates values according to historical production and certification 1) Excludes additional investment of R$ 70 million in case of Quintanilha Machados’s acquisition 2) Proinfa PPA: as of June, 2010 Note: Illustrative picture25

26

27

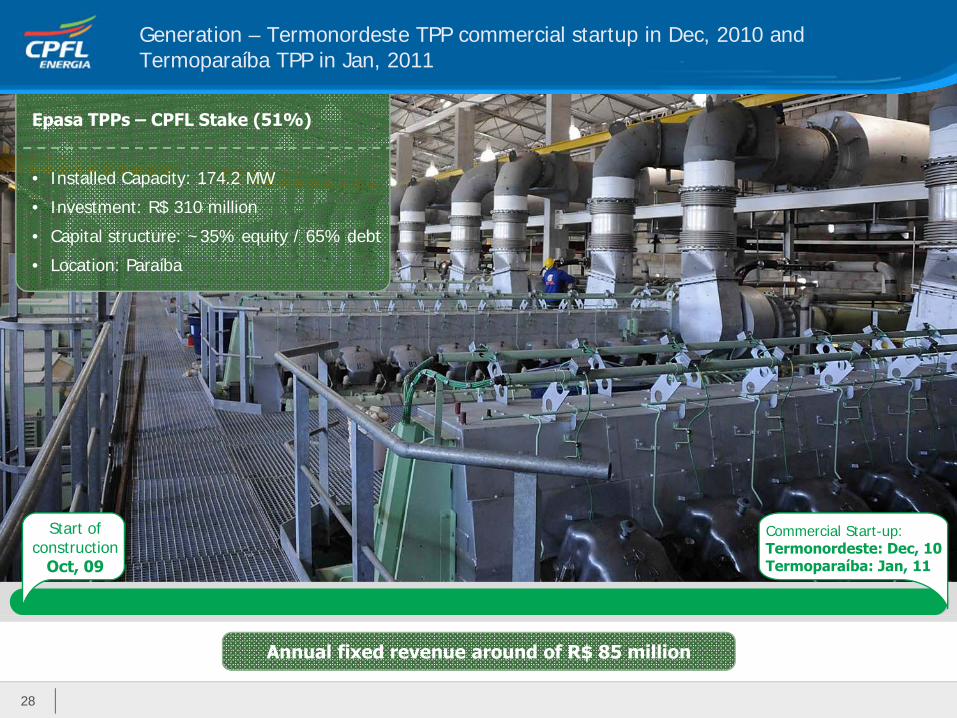

Generation – Termonordeste TPP commercial startup in Dec, 2010 and Termoparaíba TPP in Jan, 2011

Epasa TPPs – CPFL Stake (51%)

• Installed Capacity: 174.2 MW

• Investment: R$ 310 million• Investment: R$ 310 million

• Capital structure: ~35% equity / 65% debt

• Location: Paraíba

Start of construction

Oct, 09

Commercial Start-up:Termonordeste: Dec, 10Termoparaíba: Jan, 11

28

Annual fixed revenue around of R$ 85 million

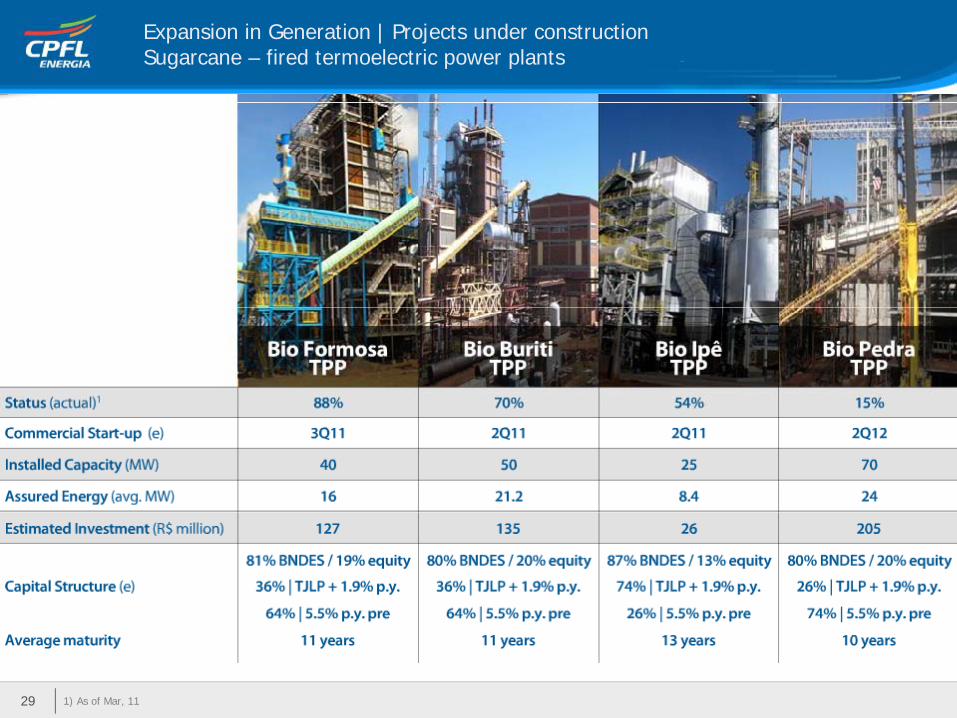

Expansion in Generation | Projects under construction Sugarcane – fired termoelectric power plants

1) As of Mar, 1129

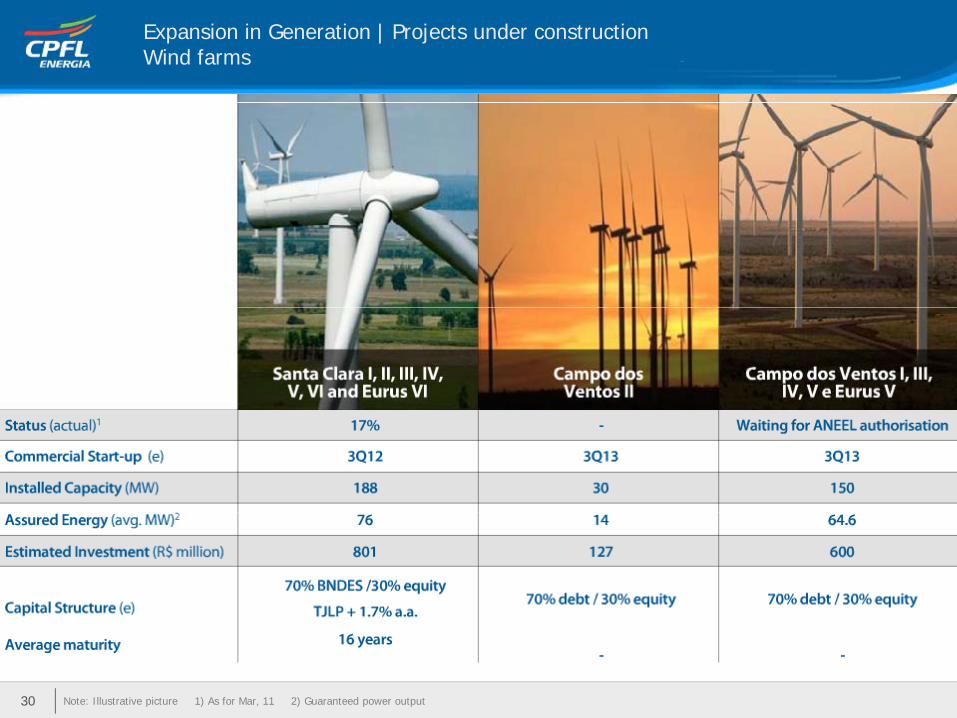

Expansion in Generation | Projects under construction Wind farms

Note: Illustrative picture 1) As for Mar, 11 2) Guaranteed power output30

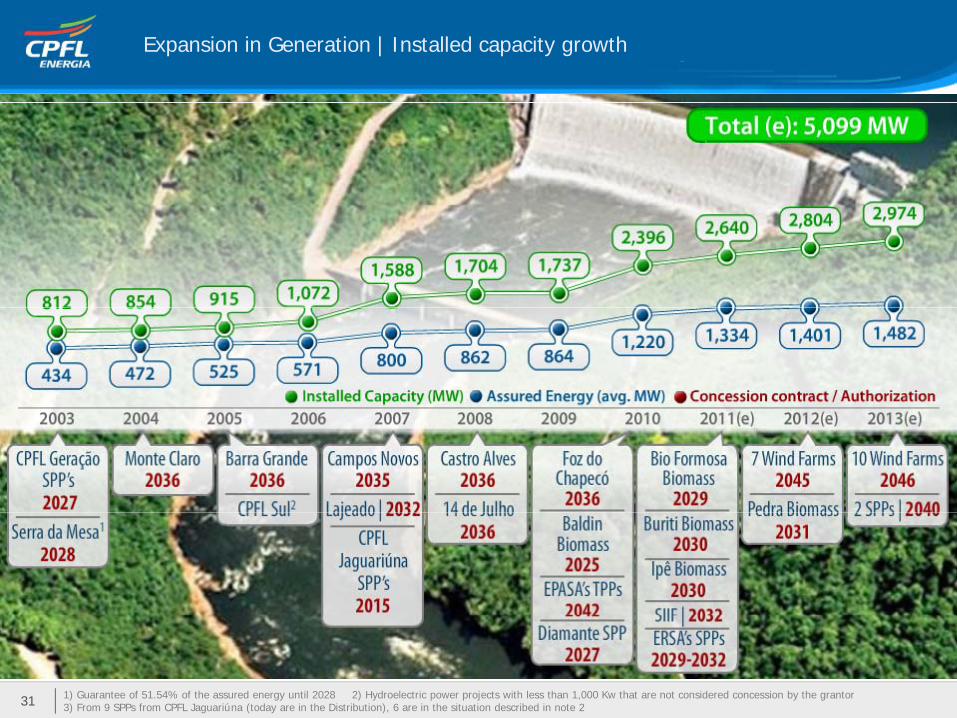

Expansion in Generation | Installed capacity growth

1) Guarantee of 51.54% of the assured energy until 2028 2) Hydroelectric power projects with less than 1,000 Kw that are not considered concession by the grantor3) From 9 SPPs from CPFL Jaguariúna (today are in the Distribution), 6 are in the situation described in note 231

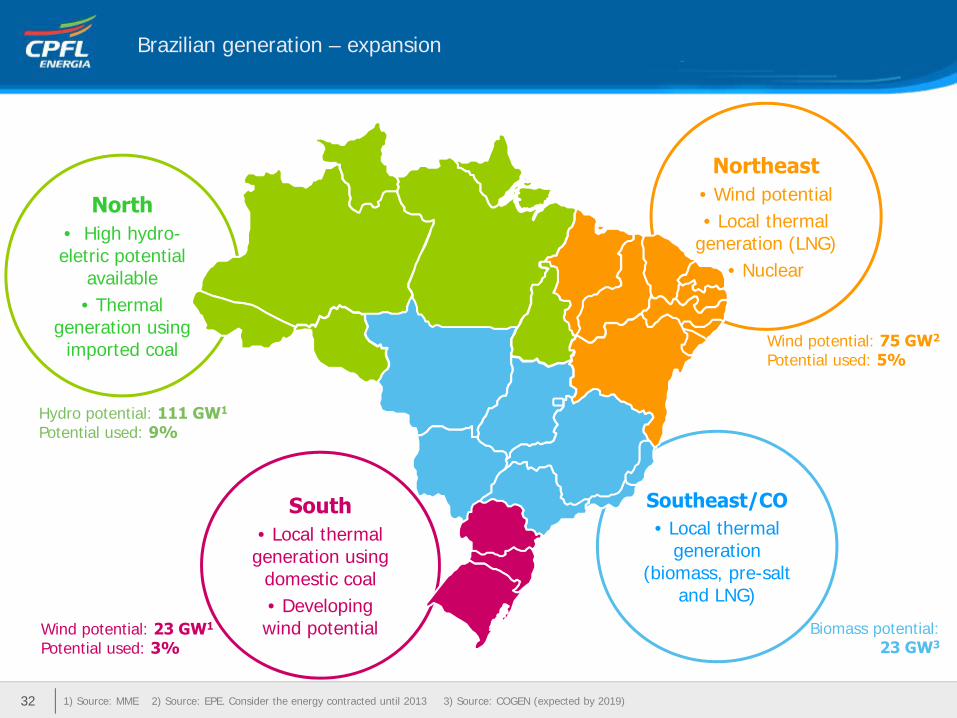

Brazilian generation – expansion

Northeast• Wind potentialNorth• Local thermal

generation (LNG)• Nuclear

North• High hydro-eletric potential

available• Thermal• Thermal

generation using imported coal

Hydro potential: 111 GW1

Wind potential: 75 GW2

Potential used: 5%

Southeast/COSouth

Hydro potential: 111 GW1

Potential used: 9%

• Local thermal generation

(biomass, pre-salt and LNG)

South• Local thermal

generation using domestic coal• Developing p gwind potentialWind potential: 23 GW1

Potential used: 3%Biomass potential:

23 GW3

1) Source: MME 2) Source: EPE. Consider the energy contracted until 2013 3) Source: COGEN (expected by 2019)32

Agenda

Corporate Overview

Operational Efficiency

Growth in the Generation Business

Wide Portfolio of Services

34

Foz do Chapecó HPPOverview: dam | reservoir