cpfl energia presentation morgan stanley final

TRANSCRIPT

• Energy market is concentrated in the most developed regions of Brazil (South/Southeast)

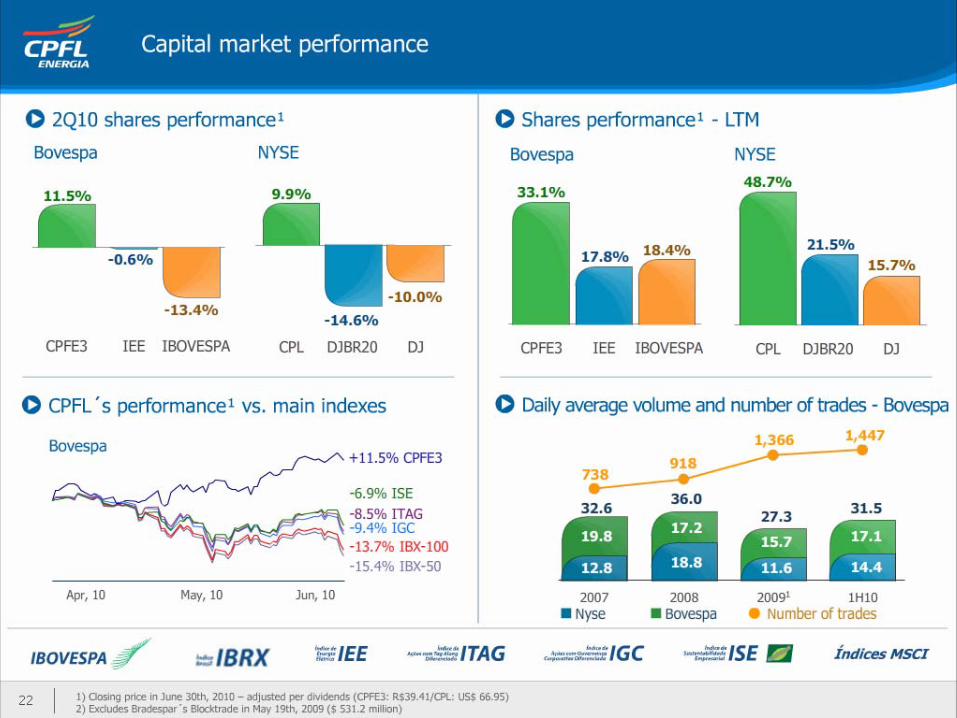

• Market cap of R$ 20 billion in August, 20101

• Listed on Bovespa’s Novo Mercado and NYSE’s ADR Level III

• Differentiated Dividend Policy: minimum payment of 50% of the net income on a semi-annual basis

• Strong growth in the generation installed capacity in the last few years

• Long term generation and distribution concessions

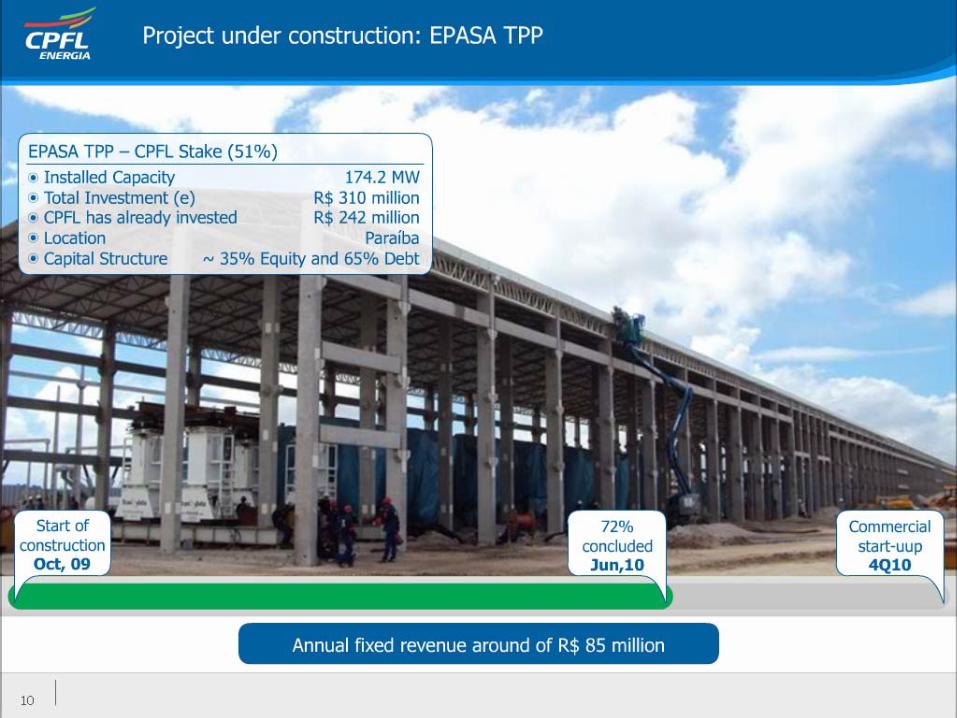

• 5 distribution companies’ acquisition, 9 SPP’s and RGE’s stake (33%), Foz do Chapecó HPP’s stake (11%), Lajeado HPP’s stake (7%) and EPASA TPP’s stake (51%) in the last 3 years

• First company in the Brazilian electric sector to negotiate carbon credits, through a run-of-stream HPP

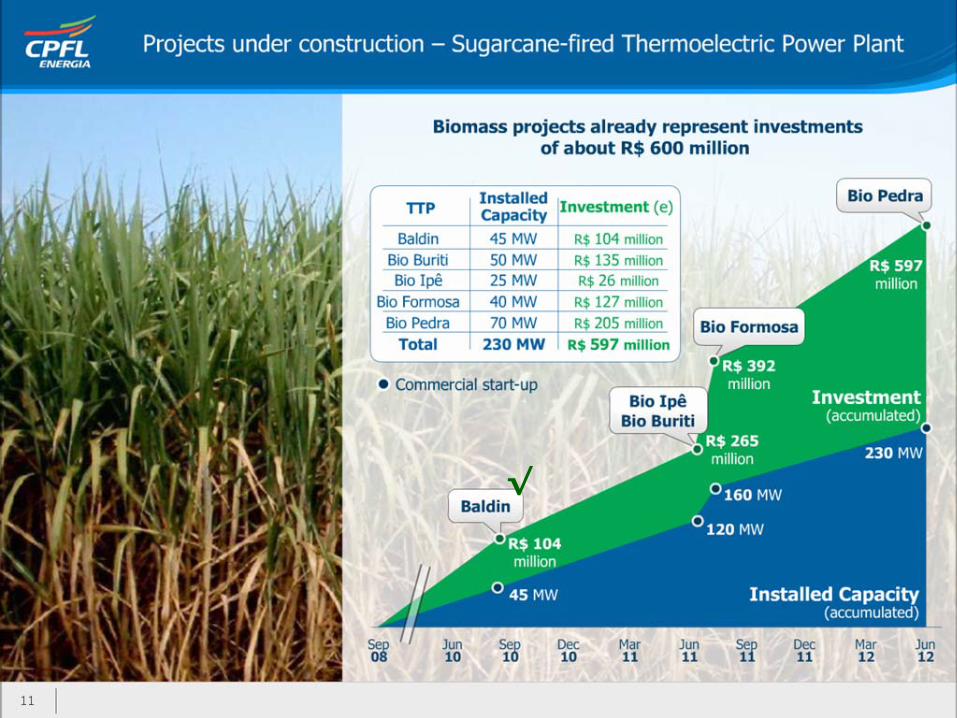

• Investments in energy generation from biomass: Baldin Biomass TPP, Baía Formosa Biomass TPP, Pedra Biomass TPP, Buriti Biomass TPP and Ipê Biomass TPP

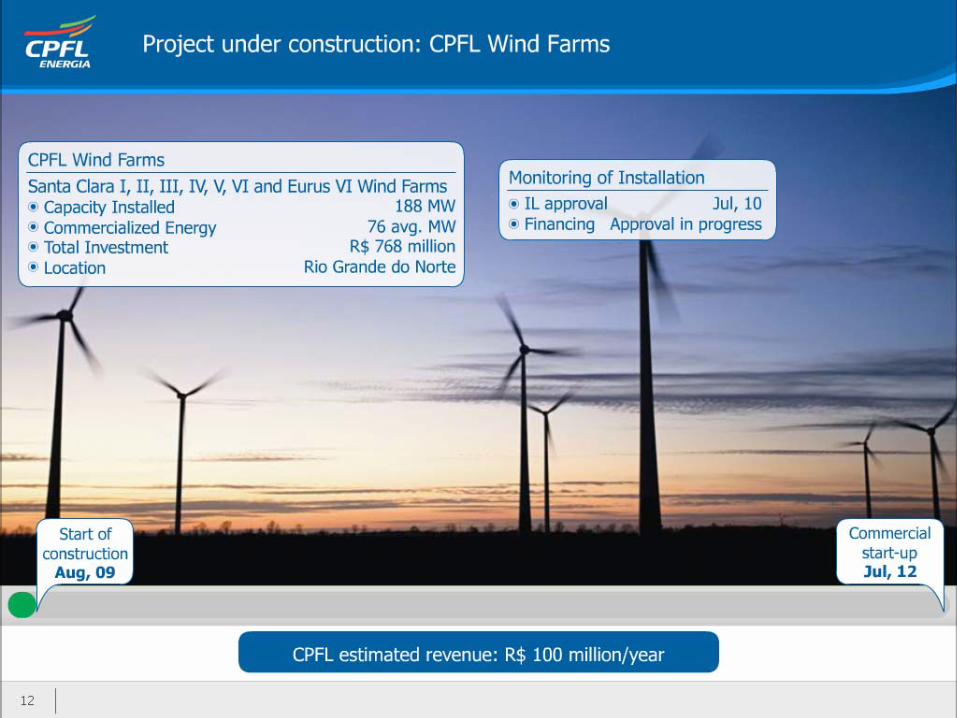

• 188 MW sold in the Wind Energy Auction in Dec, 2009 and 30 MW in Aug, 2010

Highlights

The largest private player in the Brazilian Electric Sector

1) Share price Aug 13th 2010: R$ 41,23/ON2

100%

100%

100%

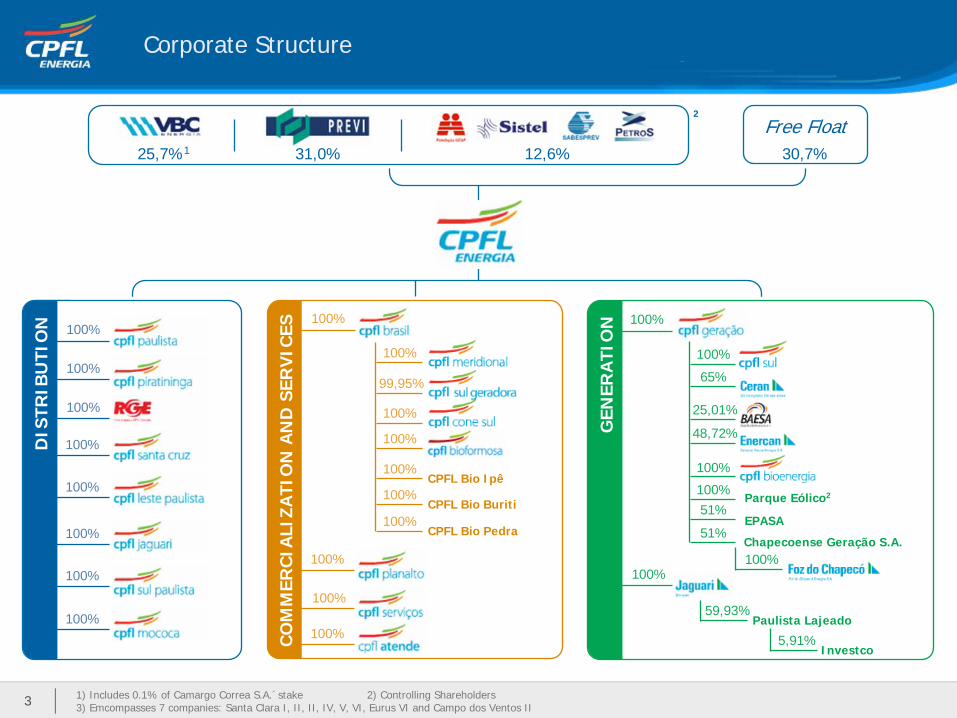

Corporate Structure

31,0% 12,6%25,7%1

DIS

TRIB

UTI

ON 100%

100%

100%

100%

100%

100%

100%

100%G

ENER

ATI

ON 100%

100%

100%

65%

25,01%

48,72%

100%

51%

59,93%

5,91%

100%

51%

100%

Paulista Lajeado

Investco

Parque Eólico2

EPASA

Chapecoense Geração S.A.

CO

MM

ERC

IALI

ZATI

ON

AN

D S

ERV

ICES

100%

100%

100%

100%

100%

100%

100%

CPFL Bio Ipê

CPFL Bio Buriti

CPFL Bio Pedra

30,7%

Free Float2

99,95%

1) Includes 0.1% of Camargo Correa S.A.´stake 2) Controlling Shareholders3) Emcompasses 7 companies: Santa Clara I, II, II, IV, V, VI, Eurus VI and Campo dos Ventos II3

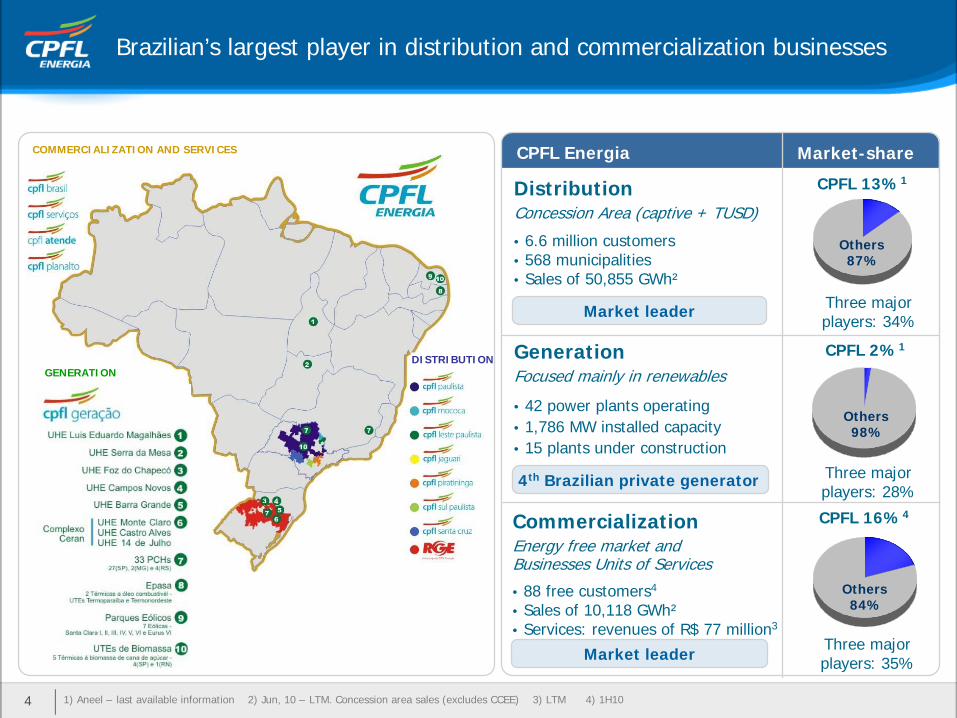

Brazilian’s largest player in distribution and commercialization businesses

CPFL 2%1

CPFL Energia

CPFL 16%4

CPFL 13%1

Market-share

DistributionConcession Area (captive + TUSD)

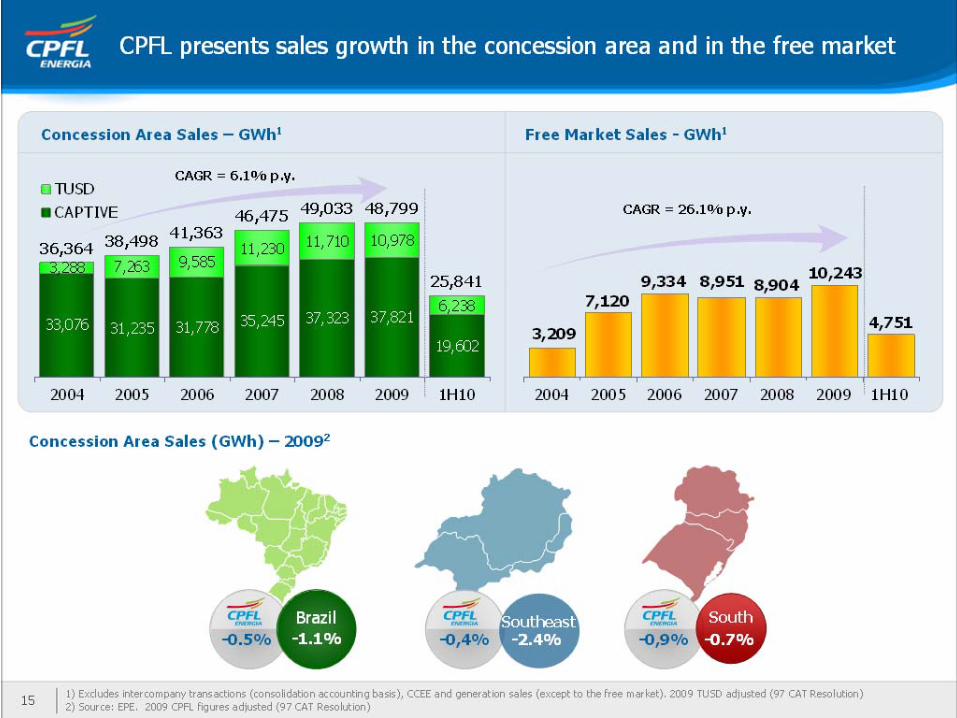

• 6.6 million customers• 568 municipalities• Sales of 50,855 GWh²

GenerationFocused mainly in renewables

• 42 power plants operating• 1,786 MW installed capacity• 15 plants under construction

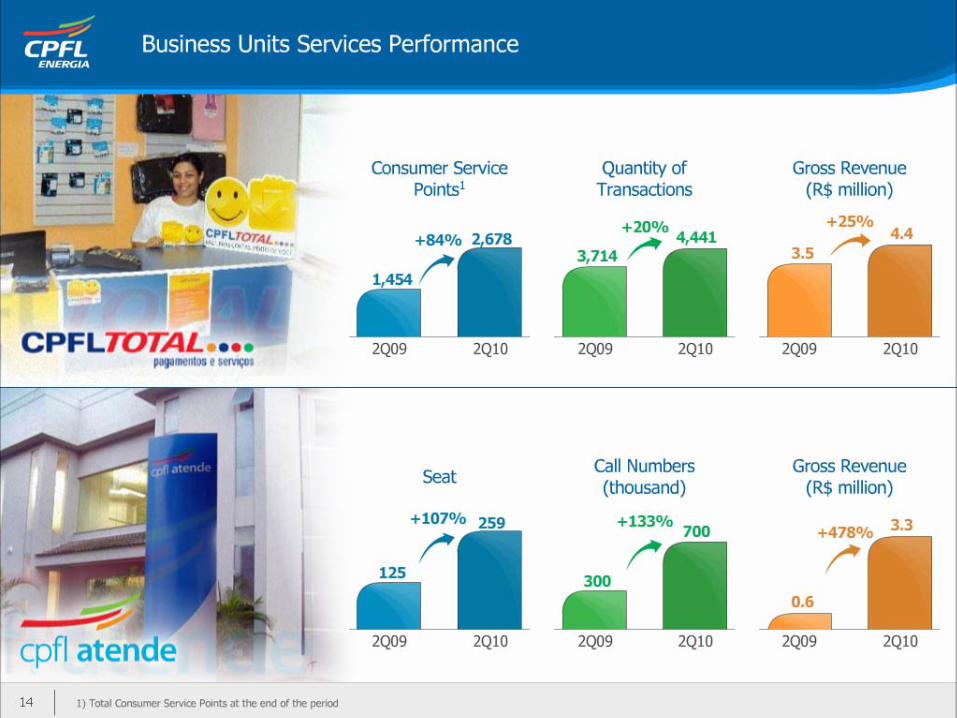

CommercializationEnergy free market and Businesses Units of Services

• 88 free customers4

• Sales of 10,118 GWh²• Services: revenues of R$ 77 million3

Market leader

4th Brazilian private generator

Market leader

GENERATION

COMMERCIALIZATION AND SERVICESCOMMERCIALIZATION AND SERVICES

DISTRIBUTION

1) Aneel – last available information 2) Jun, 10 – LTM. Concession area sales (excludes CCEE) 3) LTM 4) 1H104

Three majorplayers: 34%

Others 87%

Others 98%

Others 84%

Three majorplayers: 28%

Three majorplayers: 35%

1,3161,851

1,645

1,051 957 912746

570794

1,057961

684

761

290

936

22

893

192009 actual

2010(e) 2011(e) 2012(e) 2013(e) 2014(e)

746

1,057961

761893

516936

370

376 470

586 512

448

445

316420

497

396

2009 Actual

2010(e) 2011(e) 2012(e) 2013(e) 2014(e)

570

794684

290

19222009 actual

2010(e) 2011(e) 2012(e) 2013(e) 2014(e)

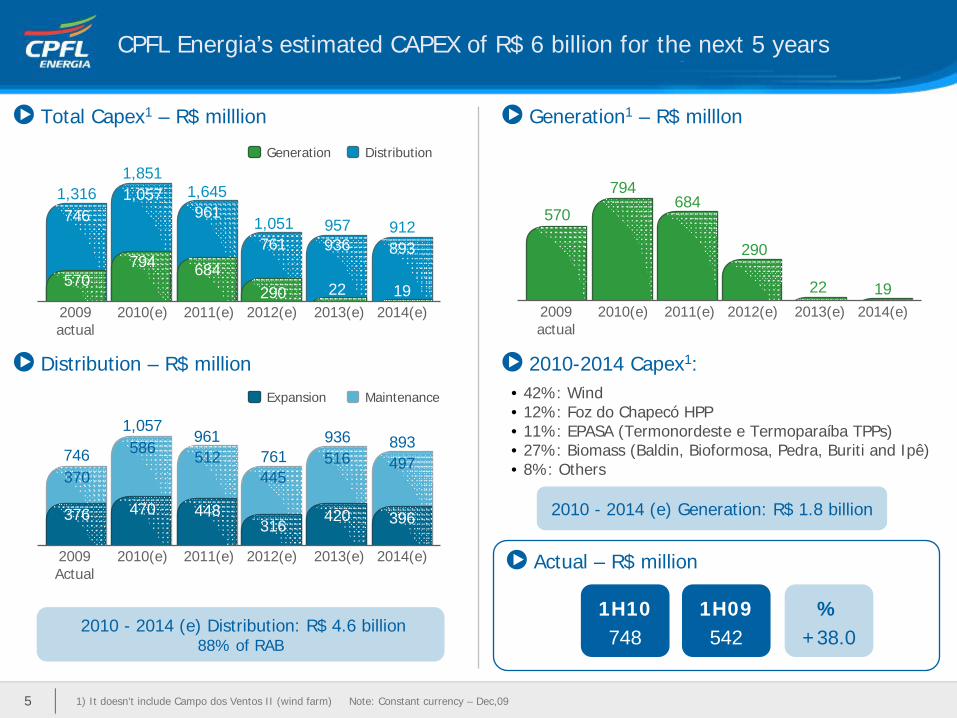

Total Capex1 – R$ milllion

Distribution – R$ million

Generation1 – R$ milllon

2010-2014 Capex1:

Actual – R$ million

2010 - 2014 (e) Distribution: R$ 4.6 billion88% of RAB

2010 - 2014 (e) Generation: R$ 1.8 billion

• 42%: Wind• 12%: Foz do Chapecó HPP• 11%: EPASA (Termonordeste e Termoparaíba TPPs)• 27%: Biomass (Baldin, Bioformosa, Pedra, Buriti and Ipê)• 8%: Others

Generation Distribution

Expansion Maintenance

1) It doesn’t include Campo dos Ventos II (wind farm) Note: Constant currency – Dec,09

1H10748

%+38.0

1H09542

CPFL Energia’s estimated CAPEX of R$ 6 billion for the next 5 years

5

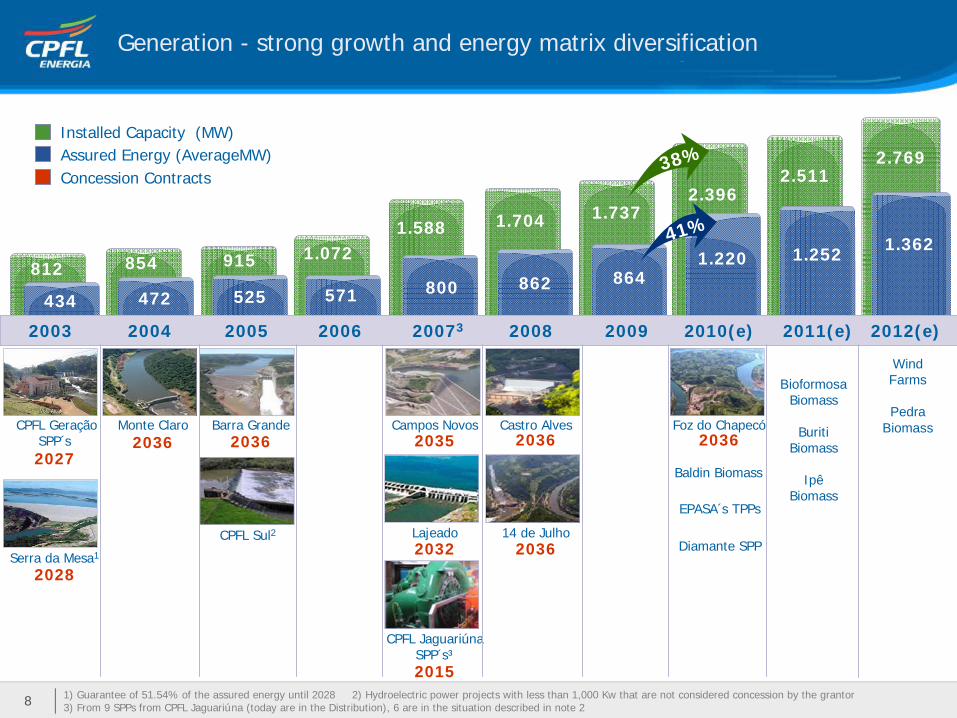

2.511

1.252812 854 915 1.072

1.588 1.704 1.7372.396

8641.220

Serra da Mesa1

CPFL GeraçãoSPP´s

Monte Claro Barra Grande

14 de Julho

Castro Alves Foz do ChapecóCampos Novos

CPFL Sul2 Lajeado

CPFL Jaguariúna SPP´s³

20272036 2036 2036 20362035

2028

20362032

2015

Baldin Biomass

EPASA´s TPPs

BioformosaBiomass

BuritiBiomass

IpêBiomass

7.3%38%

41%

Installed Capacity (MW)Assured Energy (AverageMW)Concession Contracts

2.769

1.362

434 472 525 571 800 862

2011(e)2003 2004 2005 2006 20073 2008 2009 2010(e)

Wind Farms

PedraBiomass

2012(e)

Diamante SPP

Generation - strong growth and energy matrix diversification

1) Guarantee of 51.54% of the assured energy until 2028 2) Hydroelectric power projects with less than 1,000 Kw that are not considered concession by the grantor3) From 9 SPPs from CPFL Jaguariúna (today are in the Distribution), 6 are in the situation described in note 28

√√

√

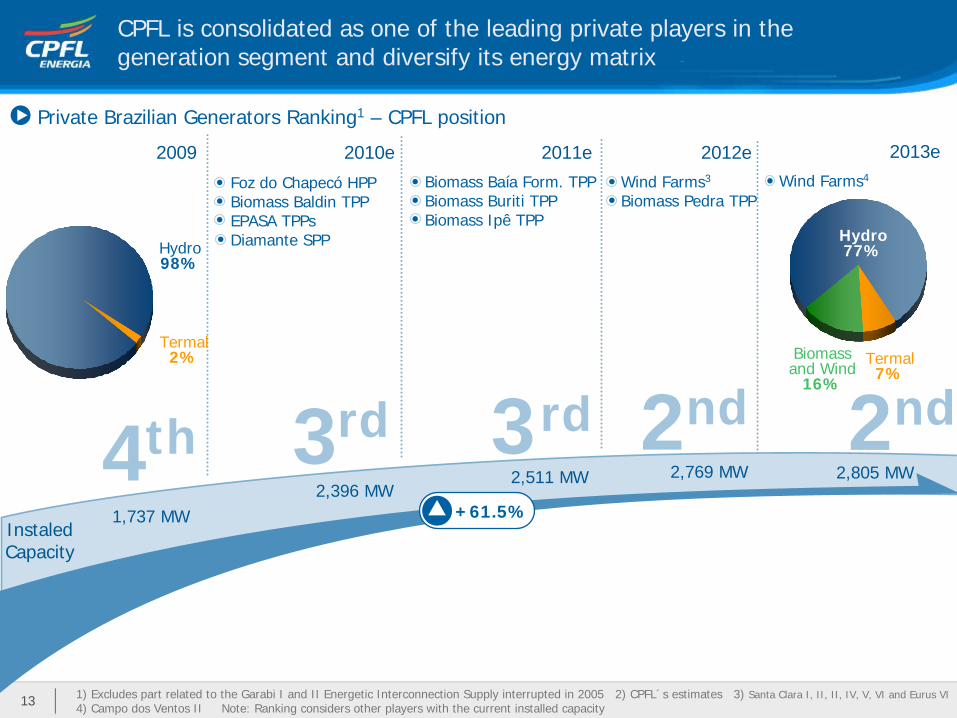

4th 3rd 3 2nd

InstaledCapacity

1,737 MW2,396 MW

2,511 MW 2,769 MW

+61.5%

Private Brazilian Generators Ranking1 – CPFL position

2009 2010e 2011e 2012e

Foz do Chapecó HPPBiomass Baldin TPPEPASA TPPsDiamante SPP

Biomass Baía Form. TPP Biomass Buriti TPPBiomass Ipê TPP

Wind Farms3

Biomass Pedra TPP

1) Excludes part related to the Garabi I and II Energetic Interconnection Supply interrupted in 2005 2) CPFL´s estimates 3) Santa Clara I, II, II, IV, V, VI and Eurus VI4) Campo dos Ventos II Note: Ranking considers other players with the current installed capacity

Termal2%

Hydro98%

Termal7%

Hydro77%

Biomass and Wind

16%

CPFL is consolidated as one of the leading private players in the generation segment and diversify its energy matrix

rd

13

2013eWind Farms4

2nd2,805 MW