cpm precious metals advisory 2012 12-06

DESCRIPTION

In depth Analysis on precious metalsTRANSCRIPT

Palladium..….………......……...p.27

Rhodium.…….….......……….…p.32

Precious Metals Price Table......p.33

Equities and Metrics Table..p.34-35

Next Scheduled Issue: 10 January 2012

Copyright CPM Group 2012. Not for reproduction or retransmission without written consent of CPM Group. Precious Metals Advisory is published monthly by CPM Group and is distributed via e-mail.

The views expressed within are solely those of CPM Group. Such information has not been verified, nor does CPM make any representation as to its accuracy or completeness. Any statements non-factual

in nature constitute only current opinions, which are subject to change. While every effort has been made to ensure that the accuracy of the material contained in the reports is correct, CPM Group cannot

be held liable for errors or omissions. CPM Group is not soliciting any action based on it. Information contained here should not be relied on as specific investment or market timing advice. At times the

principals and associates of CPM Group may have long or short positions in some of the markets mentioned here.

Market Data (Data as of 6 December; changes from 8 November)

Open Interest1 oz ∆ oz

Nymex/Comex Inventories oz ∆ oz

Nymex/Comex Nearby Active Prices % ∆ $∆

Precious Metals Advisory 6 December 2012 Vol. XXV, No. 12

Report Contents

Gold 1,701.80 ↓ -1.4% -24.20

Silver 33.11 ↑ 2.7% 0.87

Platinum 1,600.70 ↑ 3.8% 58.20

Palladium 697.05 ↑ 13.5% 82.70

Rhodium* 1,100.00 ↓ -4.3% -50.00

Gold

Eligible 8,800,826 ↑ 119,225 8,681,601

Registered 2,602,693 ↑ 15,114 2,587,579

Total 11,403,519 ↑ 134,339 11,269,180

Silver

Eligible 105,456,690 ↓ -1,141,470 106,598,160

Registered 39,836,930 ↑ 3,428,100 36,408,830

Total 145,293,620 ↑ 2,286,630 143,006,990

Platinum - Total 207,850 ↑ 9,350 198,500

Palladium - Total 531,100 ↓ -2,000 533,100

DJIA 13,074.0 ↑ 2.1% 263

FT World Stock Index 383.6 ↑ 3.0% 11.07

FT Gold Mines Index 2,777.8 ↓ -11.2% -351.79

CRB Index 297.9 ↑ 2.1% 6.07

T-Bills 0.09% ↑ 5.6% 0.01%

ICE Dollar Index 80.24 ↓ -0.7% -0.55

$ / Euro 1.30 ↑ 1.8% $0.023

*Rhodium price is BASF daily settlement price.

There is a tremendous amount of uncertainty in the mar-

ket regarding the economy and the future for precious

metals prices. As a result precious metals investors may

wait on the sidelines in December. Many price-moving

factors appear already priced into the market, such as de-

mand expectations for the PGMs and silver, a continua-

tion of the recession in Western Europe, China’s reduced

economic growth trajectory, and sovereign debt handling

in Europe. The approaching U.S. fiscal cliff may have

contributed to precious metals price increases in Novem-

ber and may continue to influence prices through the end

of the year.

Precious metals prices typically move higher in the first

few months of the year due to seasonal factors. Overall,

however, prices are expected to average modestly lower

in 2013 relative to 2012 levels. Investment demand vol-

umes for gold and silver are expected to come off further

next year, which will be the primary driver behind lower

gold and silver prices. Investors are expected to continue

to welcome opportunities to buy at price dips. That ten-

dency to view dips in prices as buying opportunities

could dissipate as the year progresses if sell-offs are not

followed by significant rallies, as investors would begin

to re-evaluate their longer term bullish sentiments in light

of weaker prices. The platinum group metals may trade

modestly higher on an annual average basis, with weak

fabrication demand limiting the upside and constrained

supply keeping prices well supported.

The primary concern at present in the precious metals

markets is when to expect demand growth to strengthen.

In 2010 and 2011, assessing demand was fairly easy –

these were recovery years so demand was rising rapidly

for cars and electronics containing PGMs and silver and

for gold jewelry in the booming Chinese and Indian mar-

kets. In 2012, demand expectations for all the precious

metals came off. India’s economy slowed and its govern-

ment raised import taxes on gold in order to reduce its

current account deficit, which weighed on gold jewelry

sales. Europe’s auto market contracted, weighing on ex-

pectations for PGM demand growth. China’s economic

growth slowed, adding further pressure to demand expec-

tations. The demand picture in 2012 is expected to spill

into 2013, will no material changes to prospects for

growth.

Precious Metals Prices May Lack Direction in 2013

Prices in 2013…...…......……….....p.1

Price Targets...………....…………p.3

Macroeconomic Indicators………p.5

Gold……...……….……...….…….p.8

Silver………………...…………..p.16

Platinum………………………...p.22

Gold

February 27,853,400 ↑ 21,074,800 6,778,600

Total 42,851,800 ↓ -2,187,500 45,039,300

Silver

March 426,995,000 ↑ 318,450,000 108,545,000

Total 704,615,000 ↑ 15,535,000 689,080,000

Platinum

January 2,724,400 ↓ -79,200 2,803,600

April 344,950 ↑ 154,100 190,850

Total 3,091,700 ↑ 86,450 3,005,250

Palladium

March 2,362,200 ↑ 2,074,900 287,300

Total 2,377,100 ↑ 200,700 2,176,400

1Data as of 5 December; changes from 7 November.

Indicators %∆ $∆

6 December 2012 Page 2 Precious Metals Advisory

Commodities Research and Consulting,

Asset Management, and Investment Banking

CPM Group, founded in 1986, is an authoritative commodities research and consulting company. It is independent of all

producers, processors, financial institutions, and other companies having commercial positions in commodities. CPM

Group has extensive experience in commodities research, trading, and finance, equipping the company to provide finan-

cial advice and consulting grounded in hands-on experience.

email: [email protected]

Telephone 212-785-8320

www.cpmgroup.com

The lack of demand upside in 2013, especially through

the first three quarters, is expected to weigh on precious

metals prices. If the European and U.S. economies begin

to pick up later in the year, industrial demand for pre-

cious metals could help to improve price appreciation

prospects.

Precious Metals Prices May Lack Direction in 2013 (cont.)

6 December 2012 Page 3 Precious Metals Advisory

Key

Top of Range

Forecast Average

Bottom of Range

1-Month

Projection

2nd & 3rd Month

Projections

Average

Price Targets Nearby active Comex/Nymex prices. Rhodium prices

are daily BASF prices. All prices are US$/ounce.

SILVER

GOLD

PLATINUM

Continued

Near Term Outlook — Prices may trend higher

over the next three months. Concerns about supply

remain high, but strike activity in South Africa’s

platinum mining sector has abated significantly in

recent months, which may weigh on prices. Anglo

Platinum restarted operations at its mines where

illegal strikes were taking place. The company has

lost about 200,000 ounces of potential platinum

output since the illegal strikes began in Septem-

ber. Fresh concerns about power supply in the

country as well as the potential for new strikes are

expected to keep prices above $1,540 in the near

term in even the worse price scenario. The first

few months of the year are typically a seasonally

strong period for platinum prices, which may keep

platinum above $1,560 (?) and could help push

prices toward $1,700 in January and February.

26

28

30

32

34

36

38

J-12 J-12 A-12 S-12 O-12 N-12 D-12 J-13 F-13

32.79

33

30

35

33.45

31

35.50

1,300

1,350

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

1,800

J-12 J-12 A-12 S-12 O-12 N-12 D-12 J-13 F-13

1,560

1,650

1,540

1,700

1,635

1,5951,579

Near Term Outlook — Prices are expected to

move sideways to lower this month, as the level of

uncertainty regarding the approaching U.S. fiscal

cliff pushes and pulls at prices. Prices could head

higher in January and February of 2013 due to

index and portfolio rebalancing activity as well as

the approach of the Comex March futures delivery

period at the end of February. Seasonal demand

for silver is typically stronger in the first few

months of the year. Prices may stay above $30

over the next three months. There is a lot of sup-

port at $30, but a move toward this level could

trigger a spike lower, possibly toward $26. Indus-

trial demand remains weak, which will weigh on

silver, but investors continue to buy on price dips.

Near Term Outlook — Gold prices could poten-

tially move in a wide range between $1,620 and

$1,780 during December. If prices settle below

$1,680, prices could decline toward $1,650 or

even $1,620. A decline in prices or consolidation

at present low levels could induce bargain buying

by various market participants including investors,

central banks, and fabricators. Prices could show

some seasonal strength in the first few months of

the year . Fiscal tightening in the United States is

expected to reduce economic growth during the

first few months reducing concerns about infla-

tion, which could weigh on gold prices. In such an

environment gold prices could slip toward $1,550. 1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

J-12 J-12 A-12 S-12 O-12 N-12 D-12 J-13 F-13

1,780

1,620

1,550

1,800

1,721

1,710 1,715

6 December 2012 Page 4 Precious Metals Advisory

Key

Top of Range

Forecast Average

Bottom of Range

1-Month

Projection

2nd & 3rd Month

Projections

Average

Price Targets Nearby active Comex/Nymex prices. Rhodium prices

are daily BASF prices. All prices are US$/ounce.

RHODIUM

PALLADIUM Near Term Outlook — Palladium prices could

potentially decline as a result of profit taking and

the possibility of weaker real demand for the

metal in the near to medium term. Prices have

risen sharply in recent weeks, which could result

in investors booking profits in their positions, es-

pecially toward the end of December. There also

is the possibility that fabrication demand for the

metal will soften during the first half of 2013 due

to fiscal tightening in the United States. This

could potentially push prices toward $580. Prices

should find support on the downside because of

the constant possibility of supply disruptions

from South Africa.

Near Term Outlook — Rhodium prices are ex-

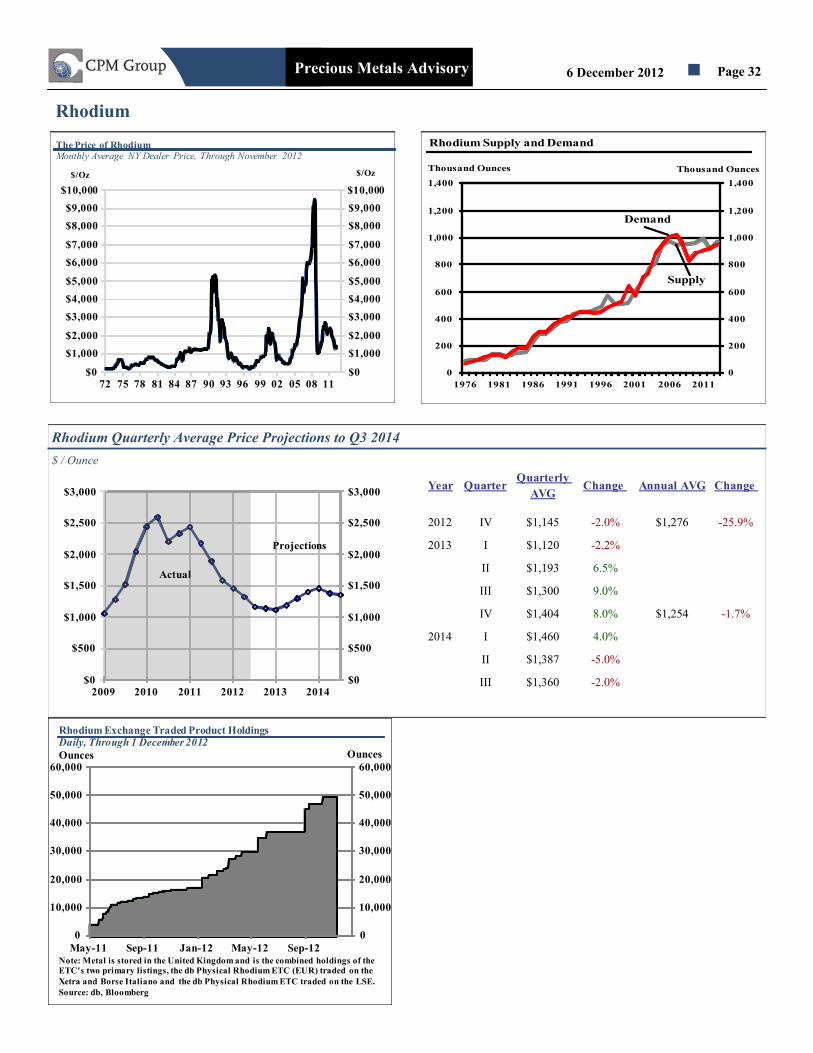

pected to remain weak over the next three months.

Rhodium prices are expected to average lower in

December, at $1,105, from November, when

prices averaged $1,142, as some of the supply

constraints supporting prices have eased. Prices

could decline toward $1,000 over the next few

months. Some seasonal price strength could help

buoy prices in January and February. Demand

prospects remain bleak, however, which has been

weighing heavily on rhodium prices since 2011

and may continue to do so. There is scope for fur-

ther declines in rhodium prices, but investors may

view prices below $1,000 or even $1,100 as a tre-

mendous buying opportunity.

450

500

550

600

650

700

750

800

J-12 J-12 A-12 S-12 O-12 N-12 D-12 J-13 F-13

750

610

725

638

580

642650

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

J-12 J-12 A-12 S-12 O-12 N-12 D-12 J-13 F-13 M-13

1,150

1,050

1,200

1,000

1,1051,130

1,142

6 December 2012 Page 5 Precious Metals Advisory

Macroeconomic Indicators

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

05 06 07 08 09 10 11 12 13

Euro zone United States

United Kingdom Japan

Unemployment Rates in Developed Economies

PercentMonthly Data, through October 2012

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Euro zone

United States

United Kingdom

Japan

Industrial Production in Developed Economies

Monthly through October 2012, Year-over-Year Percentage Change

-20%

-10%

0%

10%

20%

30%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Brazil China India

Industrial Production in Developing Economies

Monthly through August 2012, Year-over-Year Percentage Change

-4%

-2%

0%

2%

4%

6%

8%

05 06 07 08 09 10 11 12

Euro zone United Kingdom

Japan United States

Inflation - Developed Countries

Monthly CPI, Year-over-Year Percentage Change, through October 2012

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

05 06 07 08 09 10 11 12

Brazil India

China

Inflation -Developing Countries

Monthly CPI, Year-over-Year Percentage Change, through October 2012

-10

-5

0

5

10

15

Jun-96 Nov-98 Apr-01 Sep-03 Feb-06 Jul-08 Dec-10

USA China

Japan Brazil

India EU

Real Gross Domestic Product

Quarterly Data, Quarter-over-Quarter Percentage Change

Percent

Note: China and India is Quarterly data, with percentage change on a year-over-year basis. Note: U.K. data is through September 2012.

Note: Euro Zone data is through September 2012. Note: Chinese. data is through July 2012.

6 December 2012 Page 6 Precious Metals Advisory

Macroeconomic Indicators (cont)

-3

-1

0

1

3

4

6

7

8

10

11

-10

-5

0

5

10

15

20

25

30

35

40

Nov-81 May-86 Nov-90 May-95 Nov-99 May-04 Nov-08

MZM Money Supply (LHS)

U.S. Inflation (CPI)

MZM Money Supply and U.S. Inflation

Percent Percent

Correlation: negative 0.11

Monthly Data, through September 2012

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

Percent

10-Year Nominal Treasury Yield minus 10-Year TIPS Yield

Daily Data, through 4 December 2012

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

J-82 J-85 J-88 J-91 J-94 J-97 J-00 J-03 J-06 J-09 J-12

10-Year Treasury minus Three-Month Treasury

Daily Data, through 4 December 2012

Percent

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-86 Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10

Corporate Baa-rate bond minus Ten-year Treasury

Daily Data, through 4 December 2012

Percent

0

10

20

30

40

50

60

70

80

90

Jan-04 Apr-05 Jul-06 Oct-07 Jan-09 Apr-10 Jul-11 Oct-12

CBOE Volatility Index: VIX

Percent

Daily Data, through 5 December 2012

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

60

70

80

90

100

110

120

130

140

150

Jan-73 Oct-78 Jul-84 Apr-90 Jan-96 Oct-01 Jul-07

Trade-Weighted Dollar (LHS) Gold PricesIndex $/Oz

Trade-Weighted Dollar and Gold Prices

Monthly Data, through November 2012

6 December 2012 Page 7 Precious Metals Advisory

U.S. Macroeconomic Indicators

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

O-49 F-57 J-64 O-71 F-79 J-86 O-93 F-01 J-08

Total U.S. Consumer Debt

Quarterly End of Period Data, through 1 July 2012

Trillion of Dollars

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

J-93 J-95 J-97 J-99 J-01 J-03 J-05 J-07 J-09 J-11

Billions of Dollars

Total Construction Spending

Monthly Data, through October 2012

100

120

140

160

180

200

220

240

260

F-92 J-94 O-96 F-99 J-01 O-03 F-06 J-08 O-10

Manufacturers' New Orders: Durable Goods

Monthly Data, through October 2012

Billion of Dollars

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

J-60 J-66 J-72 J-78 J-84 J-90 J-96 J-02 J-08

Percent

Real Personal Income

Monthly Data, through October 2012

30

35

40

45

50

55

60

65

70

75

F-92 J-94 O-96 F-99 J-01 O-03 F-06 J-08 O-10

New Orders: Nondefense Capital Goods Excluding Aircrafts

Monthly Data, through October 2012

Billion of Dollars

0

500

1000

1500

2000

2500

3000

J-59 J-64 J-69 J-74 J-79 J-84 J-89 J-94 J-99 J-04 J-09

Housing Starts

Monthly Data, through October 2012

Thousands of Units

6 December 2012 Page 8 Precious Metals Advisory

Gold Quarterly Average Price Projections to Q3 2014

$ / Ounce

Gold Outlook

Gold prices may be expected to move between $1,620

and $1,780 in December. There have been a couple of

sharp declines in gold prices in the past two weeks, re-

flecting investor profit taking and nervousness on the part

of long investors. It may be that investor attitudes toward

the state of the world and the outlook for gold are con-

tinuing to shift, away from fear of major problems toward

a view that economic and political problems remain unre-

solved but are less likely to trigger a major collapse than

investors had expected earlier

Gold settled at $1,716.50 on 28 November, down $25.80

from the previous day and prices had declined to

$1,695.80 on 4 December, down $25.30 from the prior

trading session. Part of the selling on 28 November was

investors who had bought December Comex calls earlier

at lower prices, who had exercised these calls at the close

of trading the day before, on options expiration day.

These investors then sold the futures contracts at the

opening of trading the next day. Additional selling is be-

lieved to have been prompted by stop loss selling by

nervous longs. The sharpness of these declines is likely to

have made other remaining investors nervous, and kept

fresh investors on the sidelines, which could drive prices

lower. That said, some physically backed exchange

traded products (ETPs) saw an increase in their holdings

on both of those days, with ETP holdings reaching a re-

cord high 86.5 million ounces on 4 December. Even

though holdings are at record levels, the net additions to

holdings have not been particularly large. The strength in

incremental demand is more important in pushing prices

higher.

As this is being written gold prices have fallen to levels

just above support at $1,680. If prices decisively break

below this level they could slip toward $1,660. Or, they

could cascade sharply lower, to $1,650 or even $1,620. If

prices hold above $1,680 the sense that a low has been

made at least on a temporary basis could lead to increased

demand from fabricators, central banks, and investors, all

of whom have become extremely sensitive to the price of

gold.

India is presently in the midst of its marriage season and

any weakness in prices should be supportive of fabrica-

tion demand there. The Indian rupee has also been

strengthening lately, reducing the cost of imports, which

could further boost fabrication demand for the metal from

India.

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

2009 2010 2011 2012 2013 2014

Projections

Actual

Year QuarterQuarterly

AVGChange Annual AVG Change

2012 IV $1,726 4.2% $1,675 6.7%

2013 I $1,718 -0.4%

II $1,667 -3.0%

III $1,608 -3.5%

IV $1,641 2.0% $1,659 -1.0%

2014 I $1,673 2.0%

II $1,623 -3.0%

III $1,599 -1.5%

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Gold Prices: 1 January 2009 to 5 December 2012

$ / Oz

6 December 2012 Page 9 Precious Metals Advisory

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

75 78 81 84 87 90 93 96 99 02 05 08 11

Monthly, Through November 2012

Gold Price Volatility

0

10

20

30

40

50

60

70

80

90

100

110

120

0

10

20

30

40

50

60

70

80

90

100

110

120

77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11e

Million Ounces

Jewelry, Developing Countries

Dental

Jewelry, Developed

Million Ounces

Annual Total Fabrication Demand

Electronics

Other

Demand from central banks also might be expected to

rise if gold prices soften. During the first 10 months of

2012, central banks had added 10.76 million ounces of

gold to their reported holdings, on a net basis. Some of

the strongest net additions by central banks were seen in

months when prices softened or were at relatively low

levels. Central banks added on a net basis 2.95 million

ounces of gold to their holdings in July, when the price of

gold was at the lower end of its trading range for the year.

This was the highest monthly net additions made by cen-

tral banks during 2012. Central banks were also seen add-

ing 2.3 million ounces of metal to holdings when prices

slipped lower in March 2012.

For a variety of reasons investors remain interested in

owning gold and should be expected to step in as buyers

when prices soften. There is a lot of uncertainty sur-

rounding the handling of the current U.S. fiscal deficit

situation, which if not addressed would trigger automatic

federal spending cuts and tax increases in January 2013

(the fiscal cliff). We expect that the U.S. government will

patch together a relatively superficial agreement at the

11th hour, with most of the proposed tax increases and

budget cuts in the years beyond 2014. However, there are

likely to be some increases in taxes and reductions in

government spending, so the question is how much weak-

ness should be expected in the first half of 2013, regard-

less of the outcome of the political discussions. More im-

portant for the matters at hand, the gold market, along

with broader financial markets and economic conditions

around the world, will be held hostage to a bathetic politi-

cal melodrama over the remainder of December.

In a scenario where the fiscal cliff is averted, market sen-

timent should improve driving gold prices, along with

other markets, higher at the beginning of 2013. Any com-

promise reached on the fiscal deficit issue, which would

be positive for market sentiment, would still hurt eco-

nomic growth, only less than if all of the fiscal tightening

were to occur. As a result of this the present loose mone-

tary policy is expected to remain in place, to offset eco-

nomic weakness arising from any fiscal tightening. This

might provide slight support to gold prices, but probably

would not drive prices significantly higher from current

levels.

In the less likely scenario, where no deal is reached on

how to address the U.S. fiscal situation gold prices should

be expected to decline alongside other assets as investors

move into cash. In such a scenario monetary accommoda-

tion is likely to be increased significantly to support eco-

nomic growth, which could be supportive of gold prices.

Prices

Volatility in gold prices rose during November, with

prices both rising and declining sharply on various

occasions during the month. Monthly average price

volatility was 20.8%, which was the highest level of

monthly price volatility since July of this year. Price

volatility should be expected to continue rising dur-

ing December, as markets focus on the fiscal cliff

issue in the United States. November began with gold

prices declining sharply. Prices settled at $1,675.20

on 2 November, down from a settlement price of

$1,715.50 the previous day. Prices recovered from

Gold Price Volatility and Gold Fabrication Demand

6 December 2012 Page 10 Precious Metals Advisory

this sharp decline over the next two trading session,

reaching an intraday high of $1,720.9 on 6 November

and settling at $1,715 that day. Prices began to soften

toward the end of the month, with the sharpest de-

cline seen on 28 November, when prices settled at

$1,716.50 (around where they were at the beginning

of the month), down $25.80 from the previous day.

The weakness in prices continued into the first few

days of December.

Fabrication Demand

India is presently in the middle of its marriage sea-

son, traditionally a strong gold buying season. The

recent weakness in the price of gold coupled with

some strength in the Indian rupee is likely to help

increase demand for gold from India. The strength in

the Indian rupee helps to reduce the cost of importing

gold. These factors could collectively result in some

strength in gold fabrication demand from India.

Official Transactions

Central banks added on a net basis, 1.61 million

ounces of gold to their holdings in October. Gross

additions to holdings during the month were 1.75

million ounces, and gross reductions were 141,000

ounces.

The central bank of Turkey added 564,000 ounces of

gold to its holdings in October, making it the largest

central bank buyer of gold during the month. The

Turkish central bank’s holdings reached 10.28 mil-

051015202530354045505560657075808590

05

1015202530354045505560657075808590

73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 0911e

Indonesia

Canada

Peru

Australia

United States

Million Ounces Million Ounces

South AfricaOther Market Economies

Total World Mine Production

Transitional EconomiesChinaRussia

940

960

980

1,000

1,020

1,040

1,060

1,080

1,100

1,120

1,140

1,160

940

960

980

1,000

1,020

1,040

1,060

1,080

1,100

1,120

1,140

1,160

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12p

Million Ounces Million Ounces

Official Sector Gold Reserve Levels

Official Transactions and Supply

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

04 05 06 07 08 09 10 11 12

Million Ounces Million Ounces

Gross Additions

Gross Reductions

Net Additions/Reductions

Official Sector Changes In Gold Holdings

2012 Through October

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-09 Aug-09 Mar-10 Oct-10 May-11 Dec-11 Jul-12

Gross Additions

Gross Reductions

Net Additions/Reductions

Million Ounces Million Ounces

Official Sector Changes In Gold Holdings in 2009 - October 2012

Excludes China, India and IMF Transactions,

6 December 2012 Page 11 Precious Metals Advisory

lion ounces, a record high, in October. The central

bank of Brazil added 552,000 ounces of gold to its

holdings in October, taking total holdings of gold to

1.69 million ounces. This was the second consecutive

month that the central bank added gold, after making

no additions to holdings between October 2001 and

August 2012. The central bank of Kazakhstan re-

sumed purchasing gold after being a seller of the

metal in September. The central bank purchased

242,000 ounces of gold in October, raising its hold-

ings to a record high 3.6 million ounces.

The Bank of International Settlements’ gold holdings

rose by 371,429 ounces in October. Other central

banks that added gold to their holdings included the

central bank of Russia (13,000 ounces), Mongolia

(1,000 ounces), Greece (1,000 ounces), and Belarus

(2,000 ounces).

The central banks of Germany reduced its holdings

by 135,000 ounces in October to 109.03 million

ounces. This was the second time that Germany re-

duced its holdings this year, with the first reduction

made in June. The central bank of Mexico reduced its

holdings for the sixth consecutive month in October,

taking its total holdings of gold to 4.01 million

ounces. This level of gold holdings is still 600,000

ounces higher than levels at the end of 2011.

Reported net additions to central bank gold holdings

during the first 10 months of the year were 10.76 mil-

lion ounces, driven entirely by an increase in gross

purchases made by central banks. Gross additions to

central bank gold holdings were 11.06 million ounces

during the first 10 months with gross reduction of

290,000 ounces.

Supply

The global production-weighted cash cost for gold

mining continued to rise during the third quarter of

2012 reaching $733/ounce, up from $730/ounce in

the second quarter of 2012 and $662/ounce in the

third quarter of 2011. On average the global gold

mining industry is still enjoying a healthy margin

between cash costs and gold prices. The average

price of gold during the third quarter of 2012 was

$1,654.37. The price of gold has not been rising in

the same fashion as it was in the past few years. This

coupled with continuing increases in cash costs is

squeezing producer margins. During the third quarter

of 2011 the average price of gold was $1,700 and

cash costs were $662/ounce, giving producers an av-

erage margin of $1,038/ounce in that quarter.

Investment Demand

Gold exchange traded product holdings continued to

rise in November. Total holdings reached 86.3 mil-

lion ounces at the end of the month, up 932,050

ounces from 85.4 million ounces at the end of Octo-

ber. Holdings continued to rise during the first few

days of December, reaching a record high 86.5 mil-

lion ounces on 4 December. Even though holdings

are at record levels, the net additions to holdings have

Investment Demand

-4

-2

0

2

4

6

8

-20%

-10%

0%

10%

20%

30%

40%

Jan-07 May-08 Sep-09 Jan-11 May-12

Change in ETF Gold Holdings

Gold Price %Change M-t-M

Million Ounces% Change

Month-end Change in ETF Gold Holdings and % Change in Gold Price

Through November 2012

Note: Data as of 30 November 2012

0

10

20

30

40

50

60

70

80

90

100

-

10

20

30

40

50

60

70

80

90

100

20032004 2005 2006 2007 2008 2009 2010 2011 2012

Japan HDFCReligare SBIQuantum RelianceKotak UTIAUUSA CSGLDECSGLDC CSGOLDSGLD SGLNAGOL GLTRCGL GBEESSprott GermanTurkey SGBSGOLD NYSEJB ETFZKB IAUGLD GLDGBS GOLDCGT CEF

Million OuncesMillion Ounces

Exchange Traded Funds' Physical Gold Holdings

6 December 2012 Page 12 Precious Metals Advisory

not been very strong. The strength in this incremental

demand is more important to price increases.

Investors in exchange traded funds were seen adding

to their holdings when the price of gold was declin-

ing or was relatively depressed. This shows that in-

vestors remain interested in the metal but are also

price sensitive and are reluctant to purchase the metal

when prices rise.

Markets and Inventories

Total open interest in the Comex gold futures con-

tract rose to 49.3 million ounces on 23 November,

from 45.7 million ounces at the end of October. Total

open interest softened over the remainder of Novem-

ber and into the first few days of December. At the

end of November, total open interest was 44.3 mil-

lion ounces and was down to 43.4 million ounces by

4 December.

Open interest in the December Comex contract de-

clined over the course of November as market par-

ticipants either rolled forward or closed out their po-

sitions. Open interest in this contract slipped from

29.7 million ounces at the beginning of November to

462,300 ounces at the end of the month. Open inter-

est in the nearby active February Comex contract was

at 28.6 million ounces on 4 December, down from

29.3 million ounces at the end of November.

Gold delivered via the December Comex contract

totaled 240,100 ounces as of 5 December. Comex

registered inventories rose by 67,830 ounces on 5

December from 2.53 million ounces at the end of

November. Total eligible stocks meanwhile declined

-10

-5

0

5

10

15

20

25

30

35

-10

-5

0

5

10

15

20

25

30

35

A-95 D-96 J-98 M-00O-01 J-03 J-05 S-06 A-08 D-09 A-11

Long

Short

Net Fund Position in Comex

Million OuncesMillion Ounces

Gross Long and Short Positions of Non-Commercial Positions Comex Gold Futures & Options.Weekly Data,through 27November 2012

0

10

20

30

40

50

60

70

0

1

2

3

4

5

6

7

8

9

10

11

12

13

J-06 A-06 A-07 D-07 J-08 M-09O-09M-10 J-11 A-11M-12N-12

O

Eligible Stocks

Registered Stocks

M

Million Ounces Million Ounces

Total Open Interest (Right Scale)

Comex Gold Inventories & Total Open Interest

Daily, Through 5 December 2012

20

25

30

35

40

45

50

55

60

65

70

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Million Ounces$/Ounce

Gold

Total Open Interest

Gold Price and Total Open Interest

Daily, Through 5 December 2012

-10

-5

0

5

10

15

20

25

30

35

-10

-5

0

5

10

15

20

25

30

35

Jun-06 Apr-07 Mar-08 Jan-09 Nov-09 Oct-10 Aug-11 Jun-12

Money Managers

Other Traders

Net Position

Long

Short

Gross Long and Short Positions of Comex Disaggragated Non-Commercial Positions

Comex Gold Futures and Options. Weekly Data, Through 27 November 2012

Million Ounces Million Ounces

Markets and Inventories

6 December 2012 Page 13 Precious Metals Advisory

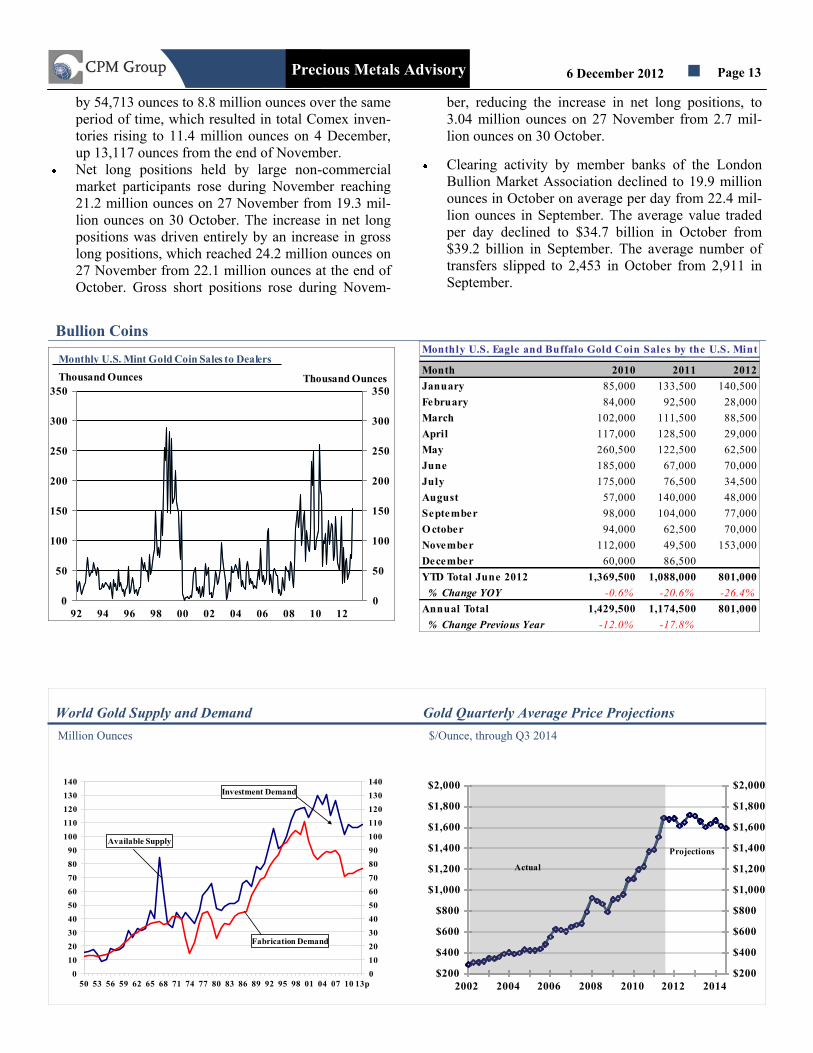

Bullion Coins Monthly U.S. Eagle and Buffalo Gold Coin Sales by the U.S. Mint

Month 2010 2011 2012

January 85,000 133,500 140,500

February 84,000 92,500 28,000

March 102,000 111,500 88,500

April 117,000 128,500 29,000

May 260,500 122,500 62,500

June 185,000 67,000 70,000

July 175,000 76,500 34,500

August 57,000 140,000 48,000

September 98,000 104,000 77,000

O ctober 94,000 62,500 70,000

November 112,000 49,500 153,000

December 60,000 86,500

YTD Total June 2012 1,369,500 1,088,000 801,000

% Change YOY -0.6% -20.6% -26.4%

Annual Total 1,429,500 1,174,500 801,000

% Change Previous Year -12.0% -17.8%

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

92 94 96 98 00 02 04 06 08 10 12

Thousand OuncesThousand Ounces

Monthly U.S. Mint Gold Coin Sales to Dealers

by 54,713 ounces to 8.8 million ounces over the same

period of time, which resulted in total Comex inven-

tories rising to 11.4 million ounces on 4 December,

up 13,117 ounces from the end of November.

Net long positions held by large non-commercial

market participants rose during November reaching

21.2 million ounces on 27 November from 19.3 mil-

lion ounces on 30 October. The increase in net long

positions was driven entirely by an increase in gross

long positions, which reached 24.2 million ounces on

27 November from 22.1 million ounces at the end of

October. Gross short positions rose during Novem-

ber, reducing the increase in net long positions, to

3.04 million ounces on 27 November from 2.7 mil-

lion ounces on 30 October.

Clearing activity by member banks of the London

Bullion Market Association declined to 19.9 million

ounces in October on average per day from 22.4 mil-

lion ounces in September. The average value traded

per day declined to $34.7 billion in October from

$39.2 billion in September. The average number of

transfers slipped to 2,453 in October from 2,911 in

September.

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

50 53 56 59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07 10 13p

Available Supply

Investment Demand

Fabrication Demand

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2002 2004 2006 2008 2010 2012 2014

Projections

Actual

Gold Quarterly Average Price Projections

$/Ounce, through Q3 2014

World Gold Supply and Demand

Million Ounces

6 December 2012 Page 14 Precious Metals Advisory

Bullion Coins

U.S. Mint gold coin sales reached 153,000 ounces in

November, the highest level reached since July 2010

when sales had totaled 175,000 ounces. Sales during

the first 11 months of 2012 totaled 801,000 ounces,

down 26.4% over the same period in 2011. On a year

-on-year basis, sales during November 2012 were up

209%, however.

U.S. Mint American Eagle gold coin sales reached

136,500 ounces during November 2012, the highest

level of sales for these coins since July 2010. Sales of

these coins during the first eleven months of the year

reached 677,000 ounces, down 27.6% from the corre-

sponding period in 2011.

American Buffalo gold coin sales continued to rise in

November reaching 16,500 ounces during the month.

This was up from 8,500 ounces from the same period

in 2011 and up from 11,000 ounces in October 2012.

Sales during the first 11 months of 2012 declined to

124,000 ounces, down 19.2% from the same period

in 2011.

Premiums on both the American Eagle and American

Buffalo gold coins remained mostly flat during No-

vember. This suggests that the market was well sup-

plied and could potentially result in softening in de-

mand from dealers in December.

6 December 2012 Page 15 Precious Metals Advisory

Million Ounces

Gold Statistical Position

*Million Ounces; Source: CPM Group; Notes: There may be discrepancies in totals and percent changes due to rounding; Net official sales are indicated by negative numbers; The price

is the Comex nearby active settlement, 2012 Through 11 October. Longer term projections are available in CPM Group's Gold Supply, Demand, and Price: 10-Year Projections report; e

-- estimates; p -- projections; NM -- Not meaningful; December 5, 2012

Supply 2007 2008 2009 2010 2011 2012p 2013p

Mine Production

China 8.7 9.1 10.1 11.0 11.6 12.3 13.0

Australia 7.9 6.9 7.2 8.4 8.3 8.1 8.4

United States 7.7 7.5 7.2 7.4 7.6 7.2 7.4

South Africa 8.2 7.1 6.6 6.2 6.0 5.3 5.1

Peru 5.5 5.8 5.9 5.3 5.3 5.4 5.5

Indonesia 3.7 2.1 4.0 3.4 2.5 1.8 2.0

Canada 3.3 3.1 3.1 2.9 3.2 3.2 3.1

Other Market Economies 20.4 21.5 23.1 24.6 25.0 26.0 28.0

Total 65.3 62.9 67.1 69.2 69.4 69.3 72.6

% Change Year Ago -0.7% -3.6% 6.6% 3.1% 0.3% -0.2% 4.8%

Secondary Supply 33.8 39.8 41.2 40.3 40.6 40.7 38.3

% Change Year Ago 22.5% 17.8% 3.7% -2.1% 0.5% 0.3% -6.0%

Transitional Economy

Sales 11.3 12.0 10.5 9.7 9.0 7.5 7.0

% Change Year Ago 9.7% 6.2% - -7.6% - - -

Total Supply 110.3 114.7 118.8 119.2 119.0 117.6 118.1

% Change Year Ago 6.5% 4.0% 3.6% 0.3% -0.2% -1.2% 0.4%

Fabrication Demand

Industrial Demand

Electronics 9.1 9.1 7.9 8.5 8.5 8.4 8.6

Dental/Medical 2.5 2.4 2.2 2.2 2.1 2.1 2.1

Other 3.9 4.6 4.1 4.1 4.7 4.8 4.9

Total 15.4 16.1 14.2 14.8 15.3 15.3 15.6

% Change Year Ago 15.6% 4.2% -11.9% 4.6% 3.1% 0.0% 1.8%

Jewelry

Developed Countries 14.9 12.4 9.4 8.7 8.4 8.2 8.1

Developing Countries 60.0 58.4 48.0 49.6 49.1 51.0 53.8

Total 74.9 70.8 57.3 58.3 57.5 59.2 61.8

% Change Year Ago -0.8% -5.5% -19.0% 1.7% -1.4% 3.0% 4.5%

Total Fabrication Demand 90.4 86.9 71.4 73.1 72.7 74.5 77.4

% Change Year Ago 1.7% -3.9% -17.8% 2.4% -0.5% 2.4% 3.9%

Stock Demand

Total Official Transactions -16.0 0.2 16.8 10.1 12.7 11.0 9.0

% Change Year Ago 37.2% NM NM -39.9% 25.9% -13.6% -18.2%

Net Private Investment

Official Coins 4.4 5.0 6.0 6.3 4.5 4.1 3.6

Bullion 28.8 18.1 20.1 24.7 26.0 25.4 25.6

Medallions 2.8 4.5 4.5 5.0 3.0 2.7 2.4

Total 36.0 27.6 30.6 36.0 33.5 32.1 31.7

% Change Year Ago 36.5% -23.3% 10.7% 17.8% -6.9% -4.1% -1.4%

Total Stock Demand 20.0 27.8 47.4 46.1 46.3 43.1 40.7

% Change Year Ago 36.0% 39.3% 70.4% -2.7% 0.3% -6.7% -5.6%

Total Demand

(Fabrication Plus Stock Change) 110.3 114.7 118.8 119.2 119.0 117.6 118.1

Price Per Ounce YTD

High $842.70 $1,004.30 $1,218.30 $1,421.40 $1,889.70 $1,796.50

Low 606.90 705.00 807.30 1,052.80 1,318.40 1536.60

Average 700.11 872.82 974.70 1,228.63 1,572.00 1669.27

% Change Year Ago 15.4% 24.7% 11.7% 26.1% 27.9% 6.5%

6 December 2012 Page 16 Precious Metals Advisory

Silver Quarterly Average Price Projections to Q3 2014

$ / Ounce

Silver Outlook

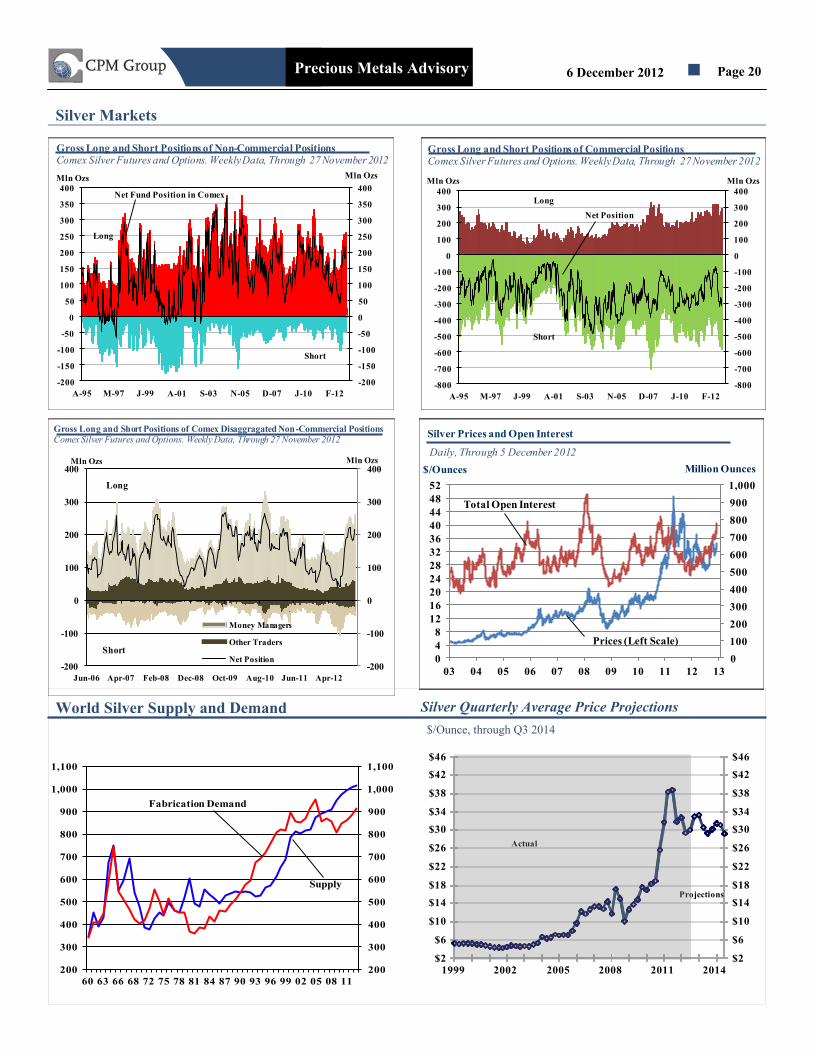

Silver prices rose last month, after trending lower in Oc-

tober. The roll of the December contract into the March

and forward month contracts helped boost prices. This

coupled with seasonal demand for the metal ahead of Di-

wali, contributed to the 11.3% trough-to-peak increase in

settlement prices between 2 and 29 November.

Silver prices have been trending lower since April of last

year. Each price rally has ended at lower highs. Intraday

peaks went from $49.82 in April 2011 to $44.09 in Au-

gust 2011 to $37.48 in February 2012 to $35.45 in Octo-

ber 2012 to the most recent peak of $34.35 on 29 Novem-

ber. Price support throughout this period has been firmly

positioned at $26.25. Going forward CPM Group expects

further declines in silver prices, driven by continued

weakness in industrial demand and rising supply. These

future declines, however, may be limited. Over the past

year, despite a broad decline in the price of the metal,

investors have remained relatively interested in silver as a

form of investment. Investors have purchased a net of

40.6 million ounces of silver exchange traded products

(ETPs), more than reversing the 24.4 million ounces of

silver ETPs sold during 2011. Last month, the U.S. Mint

witnessed a spike in November bullion coin sales, selling

3.2 million ounces of silver Eagle bullion coins, up

128.3% from last November, to authorized dealers. Also,

net long positions held by non-commercial Comex mar-

ket participants in silver futures and options have been

increasing since July and open interest in Comex silver

futures rose above levels seen in April of last year when

prices peaked last month.

Even though investment demand has been positive this

year thus far, 2012 pales in comparison to 2011. Trading

volumes in the Comex silver futures market are down

about 30%, clearing volumes in the London interbank

market are 20% lower this year than last year, silver Ea-

gle bullion sales are down 15% year-to-date, and silver

ETP net purchases are the lowest seen since 2005

(excluding 2011 when investors sold a net of 24.4 million

ounces of silver ETPs). CPM Group is projecting invest-

ment demand for silver to fall to 124.3 million ounces in

2012 from 133.2 million ounces last year. A further de-

cline in investment demand to 102.0 million ounces in

projected for 2013 while prices may come off by 8%

from 2012 levels.

Silver prices are projected to move sideways to lower this

month amid reduced trading activity during the holiday

season in the Western hemisphere. Investor concerns

about the fiscal cliff so far have appeared immaterial to

the silver market. It seems investor views about the ap-

Year QuarterQuarterly

AVGChange Annual AVG Change

2012 IV $32.72 9.7% $31.32 -6.0%

2013 I $29.47 0.9%

II $30.08 -8.0%

III $32.99 -4.0%

IV $33.28 3.0% $30.89 -1.3%

2014 I $30.62 4.0%

II $29.40 -1.0%

III $30.28 -6.0%

$8

$12

$16

$20

$24

$28

$32

$36

$40

$44

$48

$8

$12

$16

$20

$24

$28

$32

$36

$40

$44

$48

2009 2010 2011 2012 2013

Projections

Actual

8

12

16

20

24

28

32

36

40

44

48

52

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Silver Prices: 1 January 2010 to 5 December 2012

$ / Oz

6 December 2012 Page 17 Precious Metals Advisory

and Australian output is up 19.1% so far this year.

Chilean and Bolivian output both declined strongly

this year relative to 2011.

Approximately 25 new silver-producing mines began

production this year so far, four of which are primary

silver mines. The largest mine by annual silver ca-

pacity is Aurcana’s Shafter mine in the United States,

which started production in the first half of the year.

The second largest was Mawson West’s Dikulushi

mine in the Democratic Republic of Congo. These 25

mines will add around 15.0 million ounces to silver

mine production capacity once fully ramped up.

Fabrication Demand

Net imports of silver in China fell to 5.7 million

ounces in October, down from 6.2 million ounces in

Silver Prices

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

75 78 81 84 87 90 93 96 99 02 05 08 11

Monthly, Through November 2012

Silver Price Volatility

proaching fiscal cliff are mixed, resulting in no net im-

pact on price direction. Prices may rise in January and

February, ahead of the March contract delivery period at

the end of February and due to portfolio rebalancing.

Prices are expected to trade above $30 and below $35.50

over the next three months.

Prices

Silver prices trended higher in November. Continu-

ing a decline that began in October, silver prices fell

during the first three days of the month. Silver traded

to an intraday low of $30.66 on 5 November, the

lowest price since the first half of September. Prices

began to rise thereafter, touching an intraday peak of

$34.40 on 29 November, a 12.2% increase from the 5

November intraday trough. Silver settled at $33.20

on 3 November, down 3.3% from the previous day.

Prices averaged $32.82 last month, down 1.1% from

the previous month, despite rising prices.

Silver price volatility rose last month to 29.0% from

19.0% in October. This was the highest monthly

volatility rate since June.

Supply

Silver mine production fell to 68.1 million ounces in

September from 69.2 million ounces the previous

month, according to the World Bureau of Metal Sta-

tistics. Silver output from mines rose to 608.5 million

ounces this year through September, up 8.3% from

562.0 million ounces in the same period in 2011.

Output in Mexico, China, Peru, and Australia rose

during the first nine months of the year relative to

2011. Chinese silver mine production is up 37.1%

Silver Supply

World Silver Mine Production

Million Troy Ounces

% ∆

2011 2012

Mexico 113.1 122.5 8.3%

China 77.9 106.9 37.1%

Peru 81.0 83.4 3.0%

Australia 40.0 47.6 19.1%

Chile 31.3 27.2 -13.1%

Bolivia 29.3 26.4 -9.8%

Subtotal 372.6 414.0 11.1%

Other Countries 189.4 194.5 2.7%

Total 562.0 608.5 8.3%

Source: WBMS

Note: Russia, the sixth largest silver-producing country, was

excluded due to lack of comparable data.

Jan- Sept

55

57

59

61

63

65

67

69

71

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12

Monthly Silver Mine ProductionThrough September 2012

Mln Oz

6 December 2012 Page 18 Precious Metals Advisory

September and 6.1 million ounces in October 2011.

Gross imports were lower and gross exports were

higher last month relative to September.

Demand for silver in India for Diwali and the wed-

ding season benefited from high gold prices last

month, but overall demand may have been flat to

lower year-on-year. Gold and silver sales in cities

appeared positive, but rural areas posted weak de-

mand, mostly due to the delay of harvesting. Adverse

monsoon weather delayed harvesting activities by

approximately a month. This limited the buying ca-

pacity of farmers, which make up about 70% of In-

dia’s work force.

Investment Demand

Silver exchange traded product holdings increased by

1.1% of 6.7 million ounces last month from 601.4

million ounces at the end of October. Holdings rose

to a monthly peak of 612.2 million ounces on 15 No-

vember, just shy of the record high of 615.1 million

ounces reached on 25 April 2011. Holdings declined

Silver Investment Demand

Note: CEF-Central Fund of Canada traded on the Toronto Stock Exchange. SLV-iShares Silver

Trust traded on the American Stock Exchange. ZKB-Zurich Cantonal traded on the Swiss Exchange.

ETF-ETF Securities traded on the London Stock Exchange and Australian Securities Exchange, and

New York Stock Exchange. Julius Baer traded on the Swiss Exchange. SIVR-ETF Securities traded

on the New York Stock Exchange. MSL-ETF Securities traded on the Australian Stock Exchange.

GLTR—ETF Securities traded on NYSE. WITE—ETF Securities traded on NYSE. SSLN—iShares

ETP traded on the London Stock Exchange. SSLV—Source ETP traded on the London Stock Ex-

change. Silver Mitsubishi—Mitsubishi’s silver ETP traded at the Tokyo Stock Exchange.

Silver Demand

-25

-20

-15

-10

-5

0

5

10

15

20

25

-25

-20

-15

-10

-5

0

5

10

15

20

25

J-05 S-05 M-06 J-07 S-07 M-08 J-09 S-09 M-10 J-11 S-11 M-12

Gross Imports

Gross Exports

Net Trade

Monthly, Through October 2012

Chinese Silver Imports and Exports

0

100

200

300

400

500

600

700

02 07 08 09 10 11 12

Japan SSLV

SSLN WITE

GLTR PSLV

SVR.UN SBT.U

Julius Baer SIVR

MSL PHAG

SLV

CEF

ZKB

Silver Exchange Traded Product HoldingsThrough 30 November 2012

Mln Oz

-15%

-10%

-5%

0%

5%

10%

15%

2005m01 2006m04 2007m07 2008m10 2010m01 2011m04 2012m07

Production-Weighted World Industrial ProductionPercentage Change from a Year Ago, Through September 2012

Source: CPB Netherlands Bureau for Economic Policy Analysis

Silver ETP Holdings

Data as of 30 November, Changes from 31 October

Month-end Holdings % ∆ Ounce ∆

CEF 76,964,103 - 0.0% 0

SLV iShares 314,448,448 ↓ -1.4% -4,589,504

ETF - ETFS 28,649,144 ↑ 2.6% 733,212

ZKB Silver 88,742,680 ↑ 1.6% 1,367,048

Silver MSL 2,267,399 ↓ -1.3% -30,852

SIVR - ETFS 18,417,787 ↓ -0.6% -103,618

Julius Baer S ilver 17,222,990 ↑ 3.1% 515,000

GLTR - ETFS 3,143,830 ↓ 0.0% 0

WITE - ETFS 3,347,751 ↓ -2.8% -95,306

PSLV 49,287,863 ↑ 21.8% 8,814,961

SVR 2,335,561 ↑ 2.3% 52,647

SBT 740,423 ↓ -0.1% -1,052

SSLN -iShares 487,905 ↓ 0.0% -230

SSLV 319,641 ↑ 64.6% 125,468

Silver Mitsubishi 1,652,548 ↓ -6.9% -122,173

Total 608,028,073 ↑ 1.1% 6,665,602

YTD Net Additions to Total ETF Holdings* ↑ 7.2% 40,596,837

*YTD data through 30 November. Percentage change is from end of

previous year.

6 December 2012 Page 19 Precious Metals Advisory

thereafter, to 608.0 million ounces on 30 November.

Silver ETP holdings are up 7.2%, or 40.6 million

ounces, this year so far.

Coins

The U.S. Mint delivered 3.2 million ounces of silver

Eagle bullion coins to authorized dealers in Novem-

ber, up 128.3% from 1.4 million ounces delivered in

November 2011. Coins sales by the U.S. Mint are

down 15.5% so far this year from the same period in

2011.

Markets and Inventories

Open interest in Comex silver futures rose from

696.2 million ounces on 31 October to 774.4 million

ounces on 23 November, an 11.2% increase. Open

interest in Comex silver futures has been increasing

since December of last year. The 23 November peak

was higher than the April 2011 peak of 764.7 million

ounces. Open interest came off after 23 November,

falling to 722.1 million ounces on 3 December.

Open interest in the most active nearby March con-

tract was 446.1 million ounces on 30 November. This

was 3.1 times the amount of metal stored in Comex

warehouses.

Daily trading volumes of Comex silver futures aver-

aged 326.7 million ounces in November, 71.7%

higher than the daily average rate of 190.1 million

ounces in October.

Large non-commercial market participants’ net long

positions increased 11.7% from 192.9 million ounces

on 30 October to 215.5 million ounces on 27 Novem-

ber, according to CFTC data. Net long positions held

by these market participants have been trending

higher since the beginning of July. Gross long posi-

tions rose by 26.1 million ounces while gross short

positions increased 3.5 million ounces during the pe-

riod.

The daily average number of ounces transferred in

the London interbank market during October was

98.1 million ounces, down from 124.3 million ounces

in the previous month. The daily value of ounces

transferred averaged $3.26 billion, down from $4.18

billion in September and the number of transfers fell

to 757 from 967 in the previous month.

Bullion Coins

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

92 9394 95 96 97

U.S. Mint Silver Coin Sales

Million Ozs Million Ozs

0

100

200

300

400

500

600

700

800

900

1,000

0

100

200

300

400

500

600

700

800

900

1,000

J-06 O-06 A-07 M-08 M-09 D-09 S-10 J-11 M-12

O

Registered Stocks

M

Total Open Interest

Comex Silver Inventories & Total Open InterestDaily, Through 5 December 2012

Mln Ozs Mln Ozs

Eligible Stocks

Monthly U.S. Eagle Silver Coin Sales by the U.S. Mint

Month 2010 2011 2012

January 3,592,500 6,422,000 6,107,000

February 2,050,000 3,240,000 1,490,000

March 3,381,000 2,767,000 2,542,000

April 2,507,500 2,819,000 1,520,000

May 3,636,500 3,653,500 2,875,000

June 3,001,000 3,402,000 2,858,000

July 2,981,000 2,968,000 2,278,000

August 2,451,000 3,679,500 2,870,000

September 1,880,000 4,460,500 3,255,000

O ctober 3,150,000 3,064,000 3,153,000

November 4,260,000 1,384,000 3,159,500

December 1,772,000 2,009,000

YTD Total June 2012 18,168,500 37,859,500 32,107,500

% Change YOY 351.4% 108.4% -15.2%

Annual Total 34,662,500 39,868,500 32,107,500

% Change Previous Year 48.1% 15.0%

Silver Markets

6 December 2012 Page 20 Precious Metals Advisory

Silver Quarterly Average Price Projections

$/Ounce, through Q3 2014

0

100

200

300

400

500

600

700

800

900

1,000

0

4

8

12

16

20

24

28

32

36

40

44

48

52

03 04 05 06 07 08 09 10 11 12 13

$/Ounces

Silver Prices and Open Interest

Million Ounces

Daily, Through 5 December 2012

Total Open Interest

Prices (Left Scale)

$2

$6

$10

$14

$18

$22

$26

$30

$34

$38

$42

$46

$2

$6

$10

$14

$18

$22

$26

$30

$34

$38

$42

$46

1999 2002 2005 2008 2011 2014

Projections

Actual

200

300

400

500

600

700

800

900

1,000

1,100

200

300

400

500

600

700

800

900

1,000

1,100

60 63 66 68 72 75 78 81 84 87 90 93 96 99 02 05 08 11

Supply

Fabrication Demand

-200

-150

-100

-50

0

50

100

150

200

250

300

350

400

-200

-150

-100

-50

0

50

100

150

200

250

300

350

400

A-95 M-97 J-99 A-01 S-03 N-05 D-07 J-10 F-12

Long

Short

Net Fund Position in Comex

Mln Ozs

Gross Long and Short Positions of Non-Commercial Positions Comex Silver Futures and Options. Weekly Data, Through 27 November 2012

Mln Ozs

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

A-95 M-97 J-99 A-01 S-03 N-05 D-07 J-10 F-12

Mln Ozs

Long

Short

Net Position

Gross Long and Short Positions of Commercial PositionsComex Silver Futures and Options. Weekly Data, Through 27 November 2012

Mln Ozs

-200

-100

0

100

200

300

400

-200

-100

0

100

200

300

400

Jun-06 Apr-07 Feb-08 Dec-08 Oct-09 Aug-10 Jun-11 Apr-12

Money Managers

Other Traders

Net Position

Gross Long and Short Positions of Comex Disaggragated Non-Commercial PositionsComex Silver Futures and Options. Weekly Data, Through 27 November 2012

Mln Ozs Mln Ozs

Long

Short

Silver Markets

World Silver Supply and Demand

6 December 2012 Page 21 Precious Metals Advisory

Million Ounces

Silver Statistical Position

*Million Ounces; Notes: Totals may not equal the sum of categories due to rounding. Mine production in Poland, Bulgaria, Romania, Hungary, the Czech Republic, and Slovakia is included in "other" mine

production; Photography, jewelry and silverware, electronics, and 'other' industrial use reflects demand in Europe, the United States, and Japan.; These sectors include Canada from 1979, Mexico from 1982,

Hong Kong from 1985, Thailand from 1986, India from 1987, Australia, Brazil, Peru, Colombia, Argentina, Chile, Korea, Pakistan, and Bangladesh from 1989, and Taiwan from 1990; Demand excludes the

transitional economies, except for imports.; The price is the Comex nearby active settlement, percent change from year earlier period. 2012 through 6 December. There may be discrepancies due to rounding; p

- projections; NM - Not meaningful; Source: CPM Group 6 December 2012.

Supply 2007 2008 2009 2010 2011 2012p 2013p

Mine Production

Mexico 99.5 104.1 114.3 128.6 152.8 160.9 161.3

United States 39.0 40.2 39.9 40.8 36.0 34.3 35.4

Peru 112.3 118.5 126.1 116.9 109.8 109.0 111.4

Canada 27.7 24.3 20.3 19.2 18.4 17.8 18.8

Australia 60.5 61.9 52.5 60.4 55.5 57.0 58.2

China 97.9 96.3 107.9 112.5 128.6 135.4 142.7

Other 190.2 189.6 212.8 207.8 212.6 208.5 217.4

Total 627.1 634.8 673.8 686.2 713.6 722.9 745.1

% Change Year Ago 5.0% 1.2% 6.1% 1.9% 4.0% 1.3% 3.1%

Secondary Supply

Old Scrap 242.2 251.5 249.9 262.8 270.8 263.0 255.0

Coin Melt 5.0 4.0 4.0 2.0 1.5 3.0 3.0

Other Supply 0 1 2 3 4 5 6

Indian Scrap 16.1 17.5 21.7 15.7 4.8 13.8 10.0

Total 263.3 273.0 275.6 280.5 277.1 279.8 268.0

% Change Year Ago -1.9% 3.7% 1.0% 1.8% -1.2% 1.0% -4.2%

Other Supply

Government Disposals 8.0 0 0 3.8 2.4 0 0

Net Exports from

Transitional Economies 5 3 1 2 2 2 2

Total 13 3 1 5.8 4.4 2 2

% Change Year Ago -45.8% -76.9% -66.7% 480.0% -23.5% -55.0%

Total Supply 903.4 910.8 950.4 972.5 995.1 1,004.7 1,015.1

% Change Year Ago 1.5% 0.8% 4.3% 2.3% 2.3% 1.0% 1.0%

Fabrication Demand

Photography 161.5 133.5 119.4 110.9 102.6 96.8 93.1

Jewelry & Silverware 284.7 278.9 276.5 286.5 290.9 296.1 308.0

Electronics and Batteries 195.9 204.3 201.1 212.8 221.8 234.4 248.4

Solar Panels 6.3 15.5 22.6 48.6 59.8 60.2 64.0

Other Uses 212.3 213.5 176.4 178.3 178.8 183.2 189.5

Other Countries 8.2 9.7 7.5 6.5 8.0 9.7 10.0

Net Imports into the

Transitional Economies

Total Fabrication Demand 869.0 855.3 803.6 843.5 861.9 880.4 913.0

% Change Year Ago 1.3% -1.6% -6.1% 5.0% 2.2% 2.1% 2.6%

Net Surplus or Deficit 34.4 55.5 146.8 129.0 133.2 124.4 102.0

Addenda

Coinage 29.2 54.4 66.2 82.5 98.7 79.7 70.9

Price Per Ounce YTD

High $15.55 $20.79 $19.33 $30.94 $48.58 $37.14

Low 11.50 8.79 10.44 14.83 26.81 26.25

Average 13.45 14.97 14.67 20.31 35.29 31.15

% Change Year Ago 15.9% 11.3% -2.0% 38.4% 73.8% -12.8%

6 December 2012 Page 22 Precious Metals Advisory

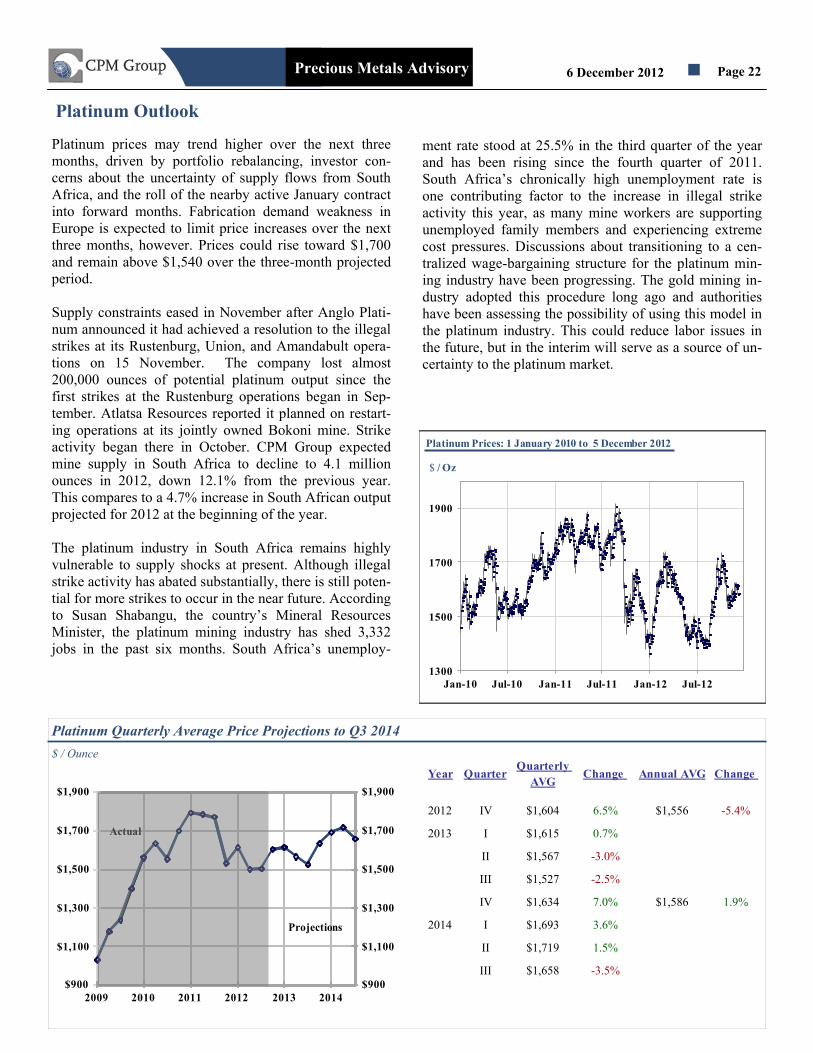

Platinum Outlook

Platinum prices may trend higher over the next three

months, driven by portfolio rebalancing, investor con-

cerns about the uncertainty of supply flows from South

Africa, and the roll of the nearby active January contract

into forward months. Fabrication demand weakness in

Europe is expected to limit price increases over the next

three months, however. Prices could rise toward $1,700

and remain above $1,540 over the three-month projected

period.

Supply constraints eased in November after Anglo Plati-

num announced it had achieved a resolution to the illegal

strikes at its Rustenburg, Union, and Amandabult opera-

tions on 15 November. The company lost almost

200,000 ounces of potential platinum output since the

first strikes at the Rustenburg operations began in Sep-

tember. Atlatsa Resources reported it planned on restart-

ing operations at its jointly owned Bokoni mine. Strike

activity began there in October. CPM Group expected

mine supply in South Africa to decline to 4.1 million

ounces in 2012, down 12.1% from the previous year.

This compares to a 4.7% increase in South African output

projected for 2012 at the beginning of the year.

The platinum industry in South Africa remains highly

vulnerable to supply shocks at present. Although illegal

strike activity has abated substantially, there is still poten-

tial for more strikes to occur in the near future. According

to Susan Shabangu, the country’s Mineral Resources

Minister, the platinum mining industry has shed 3,332

jobs in the past six months. South Africa’s unemploy-

ment rate stood at 25.5% in the third quarter of the year

and has been rising since the fourth quarter of 2011.

South Africa’s chronically high unemployment rate is

one contributing factor to the increase in illegal strike

activity this year, as many mine workers are supporting

unemployed family members and experiencing extreme

cost pressures. Discussions about transitioning to a cen-

tralized wage-bargaining structure for the platinum min-

ing industry have been progressing. The gold mining in-

dustry adopted this procedure long ago and authorities

have been assessing the possibility of using this model in

the platinum industry. This could reduce labor issues in

the future, but in the interim will serve as a source of un-

certainty to the platinum market.

1300

1500

1700

1900

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Platinum Prices: 1 January 2010 to 5 December 2012

$ / Oz

Platinum Quarterly Average Price Projections to Q3 2014

$ / Ounce

$900

$1,100

$1,300

$1,500

$1,700

$1,900

$900

$1,100

$1,300

$1,500

$1,700

$1,900

2009 2010 2011 2012 2013 2014

Projections

Actual

Year QuarterQuarterly

AVGChange Annual AVG Change

2012 IV $1,604 6.5% $1,556 -5.4%

2013 I $1,615 0.7%

II $1,567 -3.0%

III $1,527 -2.5%

IV $1,634 7.0% $1,586 1.9%

2014 I $1,693 3.6%

II $1,719 1.5%

III $1,658 -3.5%

6 December 2012 Page 23 Precious Metals Advisory

In addition to wage issues, fresh concerns about the sup-

ply of electricity surfaced last month. Eskom, the main

utility provider in the country, reported that its supply/

demand balance of electricity was extremely narrow due

to unplanned outages. This fresh uncertainty may be sup-

portive of prices over the next few weeks.

Prices

Prices trended higher last month, from an intraday

low of $1,534.50 on 7 November to an intraday high

of $1,626.60 on 23 November, a 6.0% increase. Plati-

num traded sideways after 23 November, mostly be-

tween $1,580 and $1,625. Prices averaged $1,579.40

for the month, down 3.5% from the previous month.

The monthly volatility rate fell to 15.7% in Novem-

ber from 19.7% the previous month. This was lower

than the 24.9% rate in November of last year and was

the lowest monthly rate since July of 2011.

Supply

Anglo Platinum restarted operations on 15 November

at its Rustenburg mines, where an illegal strike had

halted mining activities since 13 September, and its

Union and Amandelbult operations, where strike ac-

tion began in early October. These operations ac-

count nearly 60% of the company’s South African

platinum production capacity and roughly 30% of

total South African platinum production capacity. In

the company’s 15 November press release, Anglo

Platinum reported it had lost 191,359 ounces of po-

tential output during the strike, which is about 4.1%

of South African platinum output in 2011. Workers

accepted Anglo’s wage offer, which increased

monthly base salaries by 400 South African rand and

included a one off allowance payable upon returning

to work. CPM Group estimates that Anglo Platinum’s

output could be around 12% lower in 2012 from the

previous year.

Impala Platinum reported results for the quarter

ended 30 September last month. The company pro-

duced 454,000 refined ounces of platinum during the

quarter, up 17.0% from 388,000 ounces produced in

the same quarter in 2011. The company decided to

defer its phase 2 expansion plants at Zimplats to 2015

as part of its capital preservation measures. Cash

costs at Impala mines increased by around 15%, due

to poor mining quality at its Rustenburg operations,

wage pressures, and adverse exchange rates.

The strike that began at the Bokoni mine, jointly

owned by Atlatsa Resources and Anglo Platinum, on

1 October may have ended or will come to an end

soon. Atlatsa reported in its 3 December press release

that it was currently in the process of “re-hiring

workers with the view to re-commencing operations

as soon as possible.” The Bokoni mine is one of the

highest cost mines in the industry and only produces

about 100,000 ounces of platinum a year.

Renewed concerns about South Africa’s power sup-

ply surfaced in the first week of December. Eskom,

the main power provider in the country, reported it

only had about 2% of excess supply of electricity.

The narrow margin was attributed to unplanned out-

ages. About four years ago, the country experienced

rolling blackouts due to an electricity shortage. These

blackouts halted PGM mining operations and contrib-

uted to the PGM price spikes of 2008.

Platinum Prices

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

75 79 83 87 91 95 99 03 07 11

Monthly, Through November 2012

Platinum Price Volatility

6 December 2012 Page 24 Precious Metals Advisory

Fabrication Demand

Commercial vehicle demand in the United States and

Japan are up 10.0% and 21.5% this year through Oc-

tober from the same period a year ago. Commercial

vehicle sales in Western Europe and China are down

10.6% and 7.9%, respectively. Commercial vehicles

have large engines, which holding other factors con-

stant requires higher PGM loadings in the fitted auto

catalysts. These auto catalysts typically are more

platinum intensive, due to the sulfur content of the

diesel fuel often used.

Passenger car demand in Western Europe was 6.9%

lower in 2012 through October from the same period

a year ago. Sales in the major auto markets last

month were lower than last year’s sales levels. Ger-

many’s auto market worsened last month. Sales fell

to 259,846 vehicles, down 3.5% from a year ago.

Auto sales in France, Italy, and Spain all showed

double-digit declines in November from the previous

year. Sales this year through November in Germany,

France, Italy, and Spain are down 1.2%, 13.7%

20.0%, and 12.8% year-on-year.

Gross imports of platinum in China are up 2.5% this

year through October from the same period in 2011.

Trading volumes of platinum on the Shanghai Gold

Exchange are down 1.3% this year through Novem-

ber from 2011 levels. Trading volumes in November

fell to 161,525 ounces, down 0.9% from November

2011.

Investment Demand

Investors were net sellers of platinum exchange

traded products in November, reducing their holdings

by 19,365 ounces or 1.3% from the end of October.

Holdings totaled 1.5 million ounces on 30 November,

up 15.0% from the end of 2011. Holdings are down

2.8% from a peak of 1.6 million ounces reached in

late September.

Platinum Fabrication Demand

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 YTD

China USA Europe Japan

Y-o-Y % Chg. Y-o-Y % Chg.

Commercial Vehicle Sales in Major Auto MarketsChange over same period a year ago

Note: 2012 Through October

Annual Growth in New Car Registrations in Europe

2009 2010 2011 2012YTD

Germany 24.4% -23.2% 8.2% -1.2%

France 10.9% 1.4% -2.5% -13.7%

Italy -0.9% -10.4% -10.7% -20.0%

United Kingdom -6.6% 2.2% -4.9% 4.7%

Spain -16.8% 3.9% -17.9% -12.8%

Western Europe -1.7% -5.1% -1.3% -6.9%

Source: ACEA via Bloomberg.

Note: Country data through November, except for the U.K.,

which is through October. Western Europe data through

October.

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

2009 2010 2011 2012YTD

Germany

France

Italy

United Kingdom

Spain

Western Europe

Annual Change in European Passenger Car Sales

Note: 2012 through November Western Europe and U.K. throughOctober.

6 December 2012 Page 25 Precious Metals Advisory

Platinum Investment Demand

Note: PHPT-ETF Securities’ platinum ETF traded on the London Stock Exchange. ZKB-Zurich

Cantonal's platinum ETF traded. PPLT-ETF Securities’ platinum ETF traded on the New York

Stock Exchange. Julius Baer’s platinum ETF traded on the Swiss Exchange. MSL-Metals Securities

Australia platinum ETF. GLTR-ETF Securities’ Precious Metals Basket ETF traded on the New

York Stock Exchange. WITE-ETF Securities’ white metals basket ETF traded on the New York

Stock Exchange. SPLT-iShares platinum ETC traded on the London Stock Exchange. SPPT-

Source’s platinum ETP traded on the London Stock Exchange. Tokyo-Mitsubishi’s Japanese

Platinum ETC.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

20-Apr-07 20-Apr-08 20-Apr-09 20-Apr-10 20-Apr-11 20-Apr-12

SPPT - LSE Source

SPLT-LSE iShares

WITE-NYSE ETFS

GLTR-NYSE ETFS

Julius Baer Platinum

MSL ASX

Tokyo Mitsubishi

Platinum Exchange Traded Product HoldingsDaily, through 30 November 2012

Mln Oz Mln Oz

PHPT LSE

ZKB Platinum

PPLT NYSE

Markets & Inventories

Open interest in Nymex platinum futures fell from

3.06 million ounces on 31 October to a monthly low

of 2.98 million ounces on 20 November. Open inter-

est began rising thereafter, touching 3.10 million

ounces on 3 December.

Open interest in the nearby active January contract

trended lower last month, from 2.87 million ounces at

the end of October to 2.73 million ounces on 4 De-

cember, a 5.0% decrease.

Daily trading volumes of Nymex platinum futures