crÉdit foncier factbook 2013en · in 2013, the bank posted a non-recurring loss related to the...

TRANSCRIPT

FACTBOOK 2013ENCRÉDIT FONCIER

Message from the CEO 02

Groupe BPCE 03

Crédit Foncier at a glance 04

Crédit Foncier as a committed player 05

A strong local roots 06

Crédit Foncier gives helpful markets 07

insights and studies

The French housing market 08

The financing of Individuals 10

In a real estate market impacted by a rather unfavourable economic environment and a wait-and-see attitude from households and investors,

Crédit Foncier posted solid business performance in all of its markets in 2013, whether among individuals, real estate professionals or public entities.

This performance confirmed the accuracy of choices made when launching Crédit Foncier’s strategic plan (2012/2016). Our parent company, Groupe BPCE, reaffirmed these choices with its “Growing Differently” plan in November 2013, which implements them even more rapidly.

At the end of 2013, Crédit Foncier was ahead of its targets:

- with new real estate financing for individuals increasing by 17% compared to 2012 and a 46% market share on loans for low income families (PAS*), Crédit Foncier has confirmed its undisputed leadership position in the social home ownership sector in France;

- with e 9.8bn of international assets sold by end-2013, in almost two years, Crédit Foncier completed a higher asset disposal programme than the one forecasted at the end of 2011, which should have lasted four years. In 2013, the bank posted a non-recurring loss related to the asset disposal programme;

- with new ways of funding – syndication* and securitisation* - in addition to obligations foncières (French covered bonds*), Crédit Foncier maintains its commitment to its planned development business model, which will enable it to continue to support its clients while meeting new regulatory requirements;

- by reducing significantly its operating expenses, reaching after two years half of the e 90m forecasted over five years, Crédit Foncier proved its ability to evolve;

- with the “Growing Differently” plan, Crédit Foncier is fulfilling its role in Groupe BPCE’s development strategy. On the one hand by providing its expertise to serve the Group and making Compagnie de Financement Foncier, its wholly-owned subsidiary, available to all Group entities as a long term refinancing tool; on the other hand by continuing the policies of income and cost synergies with the

Group’s retail banks.

Bruno DeletréChief Executive Officer of Crédit Foncier

CONTENTS

12 The financing of real estate investors

and professional customers

14 The financing of public entities

16 Real estate services

18 Financial operations

20 Crédit Foncier 2013 results

21 Consolidated balance sheet

22 Contacts

23 Glossary

MESSAGE FROM THE CEO

CRÉDIT FONCIER FACTBOOK 2013

-2-

-3-* see glossary p.23

Groupe BPCE is the second largest banking group in France (1), with 115,000 employees serving 36 million customers, 8.8 of whom have decided to become cooperative shareholders.

Groupe BPCE pursues its activities in banking, insurance and real estate financing, tailoring its services as closely as possible to the needs of the individuals and regions they serve.

With its two historic brands - Banque Populaire banks and Caisses d’Epargne – and its specialized subsidiaries boasting expert knowledge in their particular areas of activity, the Group pursues all activities of a commercial bank and insurance specialist and provides financial solutions through its corporate and investment banking arm.

“Crédit Foncier, as a part of Groupe BPCE, has a unique

expertise that allows it to be the undisputed specialist in real estate financing and services

in France”.François Pérol

Chairman of the Groupe BPCE Management Board

KEY FIGURESLARGEST BANKING GROUP IN FRANCE

2 nd

MILLION CUSTOMERS36

8,8 MILLION COOPERATIVE

SHAREHOLDERS

115,000 EMPLOYEES

8,000 BANK BRANCHES

GROUPE

BPCE

Source: BPCE

ORGANISATIONAL STRUCTURE OF GROUPE BPCEAT DECEMBER 31, 2013

(1) Second in number of branches (source: database, banks 2013 website), second in market share for customer savings and customer lending (source: Bank of France Q3-2013), second in penetration rate among professionals and individual entrepreneurs (source: Pépites CSA survey 2011-2012).

100%

50%

28.04%

50%

71.96%(3)

100%(1)

• Crédit Foncier de France (100%)

• Banque Palatine (100%)• BPCE International

et Outre-mer (100%)• BPCE Assurances (46,38%)(2)

• Nexity (40.84%)(4)

• Coface (100%)

EQUITYINTERESTS

BPCECENTRAL INSTITUTION

COMMERCIAL BANKING& INSURANCE SUBSIDIAIRIES

GROUPE BPCE

NATIXIS

FREE FLOAT

BANQUESPOPULAIRES BANKS

19 CAISSESD’ÉPARGNE17

8.8 MILLION COOPERATIVE SHAREHOLDERS

Commercial Banking and Insurance

Wholesale Banking, Investment Solutions and Specialised Financial Services

(1) Indirectly through Local Savings Companies.(2) With the equity interest held by the Caisses d’Epargne in BPCE Assurances, the Group owns a 60% stake in the company.(3) Percentage of voting right held by BPCE.(4) Via CE Holding Promotion.

CRÉDIT FONCIER

AT A GLANCECRÉDIT FONCIER’S FIVE MAJOR BUSINESSESProperty finance for individuals

Financing real estate investors and professional customers

Financing public entities

Real estate services

Financial operations

A STRATEGY ANCHORED IN GROUPE BPCE Crédit Foncier’s strategy, laid out at end-2011, is focusing on five major axes:

1. the development of the core business in France (financing and real estate services) serving Crédit Foncier clients and those of the Group’s retail banking networks;

2. the discontinuation of international activities and the reduction of the balance sheet: deleveraging enabled Crédit Foncier to reduce its market footprint and thus improve its ability to fund its business under optimal conditions and plan ahead for compliance with the

Basel III leverage ratio;

3. the development of new funding tools alongside the obligations foncières, particularly syndication* and securitisation*;

4. cost savings that enhance the resilience of Crédit Foncier;

5. the development of synergies with Groupe BPCE: Crédit Foncier brings to the group its leadership position

in France on the social homeownership market as well as its reliable access to a debt capital markets as a source of medium and long term funding through its highly diversified investor base.

This strategy has been supported in November 2013 under the new Groupe BPCE strategic plan “Growing Differently”: Compagnie de Financement Foncier has been made available to all Groupe BPCE entities.

CRÉDIT FONCIER, A KEY PLAYER IN REAL ESTATE MARKETSCrédit Foncier is the leading specialist in real estate financing and services in France. As a wholly-owned subsidiary of Groupe BPCE, the second-largest banking group in France, Crédit Foncier serves all those who seek, for one reason or another, the expertise and unique insight that will help them find the answers to their real estate needs: individuals of course, but also professionals, investors and local authorities*.

Crédit Foncier provides, to all these players, its innovation and creativity as well as its market experience for over 160 years.

-4-

KEY FIGURES 1st*

LENDER TO LOW-INCOME FAMILIES

253BRANCHES

7,000BUSINESS PARTNERS IN THE REAL

ESTATE SECTOR**

* 46% market share on Loans for low-income families (PAS*)Source: SGFGAS** Developers, individual home builders, real estate brokers, property managersSource: Crédit Foncier

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

2,881EMPLOYEES (YEARLY FULL-TIME

AVERAGE HEADCOUNT)

-5-

AN ONGOING INNOVATION In offering a broader range of services, expanding communication, publishing studies, Crédit Foncier has proved to be an innovative player:

• rollout of Crédit Foncier’s “new generation” branch concept in order to upgrade its 253 branches;

• crédit Foncier’s new communication campaign to reaffirm its commitment to help French people become homeowners;

• development of the offer to high-end clients and non-residents;• offering a broader range of financing for jointly-owned

apartment buildings;• bond issuance programme marketed to investors by Compagnie de Financement Foncier (Public issuances and private placements);• term account;• contents delivery (studies, new website…) to strengthen

its reference position on the markets.

CRÉDIT FONCIER, A COMMITTED PLAYER

A HUMAN RESOURCE MANAGMENT ACTION-ORIENTED • An active policy of training: 6% of total payroll allocated to in-job training in 2013; nearly 90% of employees took part in more than 7,800 training days;• Quality of life in the workplace: working from home,

disability policy, gender equality, prevention of psychosocial risks.

A CORPORATE SPONSORSHIP STRATEGY FOCUSED ON THE CORE BUSINESS AND LOCAL RELATIONS Crédit Foncier’s sponsorship initiatives are focused around four areas:

• to confirm its commitment to society by building partnerships with associations providing solidarity-based and sustainable housing solutions;

• to involve its employees in general interest projects by offering skills sponsorship for existing partner associations or by enabling employees to support associations in which they are personally invested;

• to get involved with the local community;• to encourage and foster improved financial education for low-income households.

Created in 2009 and wholly-owned subsidiary of Crédit Foncier, ENFI is an approved training centre, whose mission is to assist all professionals interesting in learning new skills and knowledge related to real estate and its financing. Capitalising on the historical expertise of its parent company regarding real estate financing, ENFI is a recognised partner among real estate professionals, large banks and insurance companies.The ENFI’s areas of expertise cover a broad range of expertise

such as real estate financing, property valuation, law and regulation related to real estate, financial operations.

• Almost 1,000 customers

• 5,620 participants since the start of the programme in 2011

• Lectures from 220 professionals

THE CUSTOMER SATISFACTION AT THE CORE OF CRÉDIT FONCIER’S STRATEGY• 96% of customers have a positive image of

Crédit Foncier;• 98% of customers and partners trust Crédit Foncier; • 88% of customers and partners would recommend

Crédit Foncier.

Source: annual survey “customers and partners” of Crédit Foncier and G@links - 2013

ENFI (NATIONAL REAL ESTATE FINANCING INSTITUTE), THE FIRST SCHOOL/COMPANY DEDICATED TO REAL ESTATE PROFESSIONALS

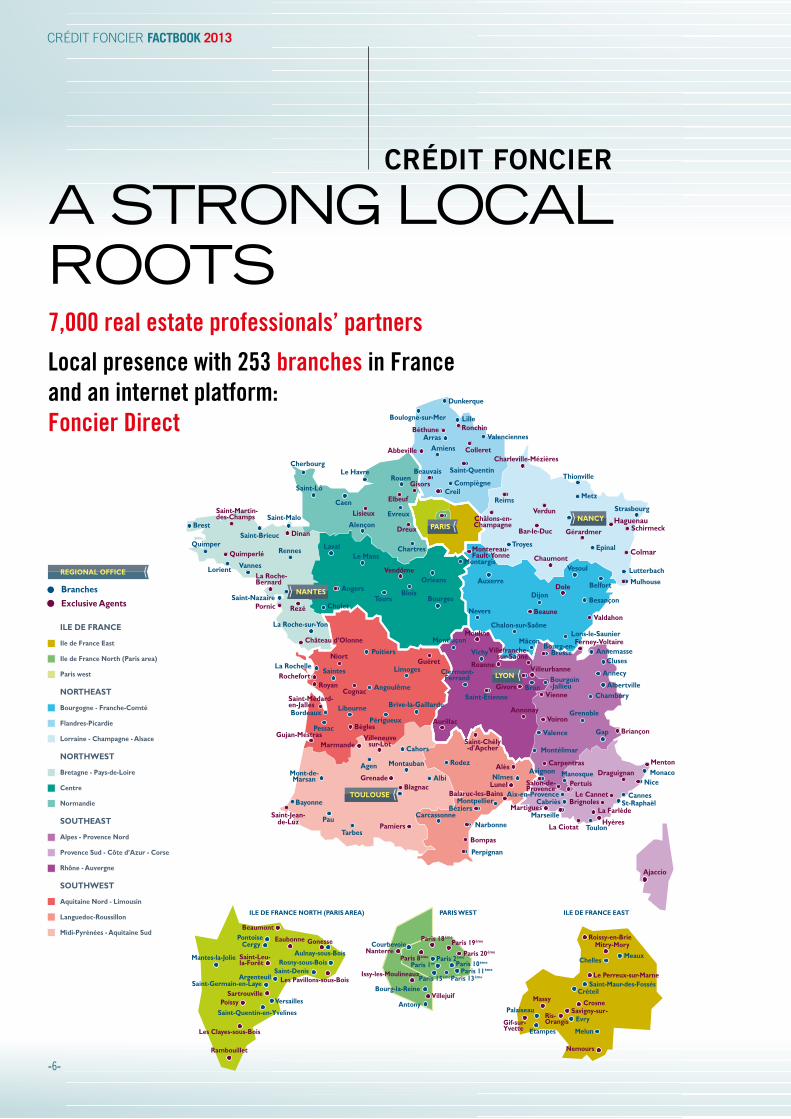

A STRONG LOCAL ROOTS

CRÉDIT FONCIER

-6-

7,000 real estate professionals’ partners

Local presence with 253 branches in Franceand an internet platform:Foncier Direct

CRÉDIT FONCIER FACTBOOK 2013

ILE DE FRANCE NORTH (PARIS AREA) PARIS WEST ILE DE FRANCE EAST

LYON

TOULOUSE

PARIS

NANTES

NANCY

Branches

Exclusive Agents

ILE DE FRANCE

Ile de France East

Ile de France North (Paris area)

Paris west

NORTHEAST

Bourgogne - Franche-Comté

Flandres-Picardie

Lorraine - Champagne - Alsace

NORTHWEST

Bretagne - Pays-de-Loire

Centre

Normandie

SOUTHEAST

Alpes - Provence Nord

Provence Sud - Côte d’Azur - Corsee

Rhône - Auvergne

SOUTHWEST

Aquitaine Nord - Limousin

Languedoc-Roussillon

Midi-Pyrénées - Aquitaine Sud

REGIONAL OFFICE

Cabriès

Marseille

Rennes

Tours

Clermont-Ferrand

Vichy

Limoges

Poitiers

Saintes

Mont-de-Marsan

Bayonne

Tarbes

Ajaccio

CarcassonneBéziers

Montpellier

Albi

Rodez

Nîmes

Toulon

St-RaphaëlCannes

NiceMonacoAvignon Manosque

Gap

Montauban

Cahors

Agen

Angoulême

LibourneBordeaux

La Rochelle

La Roche-sur-Yon

Saint-Nazaire

Lorient

Quimper

Brest

Vannes

Saint-Brieuc

Saint-Malo

Saint-Lô

Caen

CherbourgLe Havre

Alençon

Chartres

Evreux

Le MansLaval

Angers

Cholet

Blois

Orléans

Bourges

Montluçon

Auxerre

Nevers

Chalon-sur-Saône

Saint-Etienne

Mâcon

Montargis

Troyes

Reims Metz

Thionville

Valenciennes

Dunkerque

Périgueux

ArrasAmiens

Saint-Quentin

Pessac

Narbonne

Perpignan

Pau

Brive-la-Gaillarde

Montélimar

Cluses

Annecy

AlbertvilleChambéry

BronBourgoin-Jallieu

Bourg-en- Bresse Annemasse

Lons-le-Saunier

Besançon

Belfort Mulhouse

Lutterbach

Strasbourg

Vesoul

Epinal

Grenoble

Valence

Dijon

Boulogne-sur-Mer

RouenBeauvais

CreilCompiègne

Lille

Abbeville

RonchinBéthune

Colleret

Elbeuf

Gisors

Dreux

Lisieux

Pornic

Rochefort

Quimperlé

Dinan

Saint-Martin-des-Champs

Vendôme

Royan

Niort

Bègles

Marmande

Cognac

Château d’Olonne

Guéret

Saint-Médard-en-Jalles

Gujan-Mestras

Saint-Jean-de-Luz

Grenade

Aurillac

Blagnac

Pamiers

LunelLe Cannet

Hyères

La FarlèdeBrignoles

PertuisDraguignan

La Ciotat

Martigues

Alès

Saint-Chély-d'Apcher

Annonay

GivorsVienne

Voiron

Villeurbanne

Villefranche-sur-Saône

Moulins

BeauneValdahon

SchirmeckBar-le-Duc Gérardmer

Charleville-Mézières

Briançon

Menton

Bompas

Rezé

Balaruc-les-Bains

Meaux

Saint-Maur-des-FossésCréteil

Chelles

Melun

Evry

Etampes

Palaiseau

Roissy-en-BrieMitry-Mory

Le Perreux-sur-Marne

Gif-sur-Yvette

CrosneMassy

Savigny-sur-

Nemours

Ris-Orangis

Villejuif

Courbevoie

Paris 1er Paris 10ème

Paris 11ème

Paris 13èmeParis 15ème

Bourg-la-Reine

Antony

Paris 20ème

Paris 8ème

Paris 18ème

Paris 19ème

Nanterre

Issy-les-Moulineaux

Rosny-sous-BoisAulnay-sous-Bois

Saint-Denis

Versailles

Saint-Germain-en-Laye

Saint-Quentin-en-Yvelines

Mantes-la-Jolie

PontoiseCergy

Argenteuil

Beaumont

GonesseEaubonne

Saint-Leu-la-Forêt

Les Pavillons-sous-Bois

PoissySartrouville

Rambouillet

Les Clayes-sous-Bois

Carpentras

Roanne

Ferney-Voltaire

Dole

Colmar

HaguenauVerdun

Salon-de-Provence

La Roche- Bernard

Villeneuvesur-Lot

Châlons-en-Champagne

Aix-en-Provence

Chaumont

Paris 2ème

Montereau- Fault-Yonne

Branches

Exclusive Agents

ILE DE FRANCE

Ile de France East

Ile de France North (Paris area)

Paris west

NORTHEAST

Bourgogne - Franche-Comté

Flandres-Picardie

Lorraine - Champagne - Alsace

NORTHWEST

Bretagne - Pays-de-Loire

Centre

Normandie

SOUTHEAST

Alpes - Provence Nord

Provence Sud - Côte d’Azur - Corsee Rhône - Auvergne

SOUTHWEST

Aquitaine Nord - Limousin

Languedoc-Roussillon

Midi-Pyrénées - Aquitaine Sud

REGIONAL OFFICE

1 – Étude trimestrielle de CrÉdit FonCier immobilier – 2e trimestre 2013

un mArCHÉ loCAtiF Qui tourne Au rAlentiÉtude trimestrielle de Crédit Foncier Immobilier

Direction des Études

4e trimestre 2013

1,845 million de mètres carrés de bureaux ont été placés en Île-de-France en 2013. Le constat de fort ralentissement est sans appel, avec une inflexion des volumes commercialisés de 19 % par rapport à la moyenne décennale (proche de 2,3 millions de mètres carrés) et – 21 % sur un an.Le quatrième trimestre, meilleur que les trois premiers avec 511 700 m2 tertiaires placés (soit – 17 % par rapport au quatrième trimestre 2012), permet d’atténuer la baisse qui s’est établie à – 38 % au troisième trimestre sur un an glissant.

L’année 2013 restera marquée par l’essoufflement des grandes transactions, dont le volume se rétracte de moitié. Ce segment avait jusqu’ici porté entre 30 % et 40 % de l’activité locative, pour un nombre limité de signatures (moins de soixante-dix à l’année). Propriétaires de leur immobilier (vieillissant) et de leur siège historique prestigieux il y a encore quinze ou vingt ans, les entre-prises du CAC 40 sont aujourd’hui, pour la plupart, locataires. Une majorité ont par ailleurs transféré leurs activités en proche péri-phérie parisienne, dans un souci de modernisation, de regroupe-

ment et de rationalisation de l’outil immobilier, avec des exigences de meilleur rapport qualité/prix (flexibilité des espaces de travail, bonne desserte par les transports en commun, performance éner-gétique…). C’est ce mouvement de fond, initié il y a dix ans (avec par exemple l’implantation de Generali, en 2003, sur le pôle de la Plaine-Saint-Denis), qui semble se tarir, alors qu’il a contribué à porter le marché dans un contexte économique difficile. Autre facteur non négligeable, en 2013, les bailleurs, tout autant que les grands locataires, recherchent une plus grande sécurité. Ils utilisent largement le levier de la renégociation du bail, les uns pour pérenniser l’occupation de leur immeuble, les autres pour négocier facilement une réduction de leur loyer.

Autre pan du marché locatif tertiaire fragilisé, cette fois essen-tiellement à cause du contexte économique et de l’environnement anxiogène, celui des petites surfaces de bureaux de moins de 500 m2 à 1 000 m2. Les PME se sont montrées bien moins mobiles en 2013, mais continuent d’alimenter le moteur de l’activité pari-sienne dans le QCA.

Point de conjoncture bureaux – marché locatif Île-de-France

2013 : le levier des renÉgoCiAtions AssèCHe le niveAu de lA demAnde nouvelle

Contexte ÉConomIque et FInanCIer

FrAnCe 2010 2011 20122013

(chiffres provisoires) (1)

Évolution sur un an

indiCAteurs ÉConomiQues

Pib 1,4 % 1,7 % 0,0 % 0,2 %

taux de chômage 9,3 % 9,8 % 10,6 % 10,8 % (2)

inflation 1,7 % 2,3 % 1,5 % 0,8 % (3)

indiCAteurs FinAnCiers

taux directeur bCe 1,00 % 1,24 % 0,75 % 0,25 % (4)

taux euribor 3 mois France (5) 0,80 % 1,40 % 0,57 % 0,22 %

taux oAt 10 ans France (5) 3,10 % 3,33 % 2,54 % 2,20 %

(1) Source : Banque de France – Indicateurs conjoncturels France au 10 janvier 2014.(2) Donnée Eurostat, cvS à novembre 2013 (source Insee – estimations T3 2013 : 10,5 % en France métropolitaine).(3) IPcH – Insee – novembre 2013 en glissement annuel.(4) Taux directeur applicable depuis le 13 novembre 2013.(5) Moyennes annuelles calculées à partir des taux moyens mensuels (source Banque de France).

• Publication of quarterly macroeconomics reports on real estate markets.

• Key figures of the week, which covers both the property data of commercial or residential markets and users’ profile and behavior.

• Publication of detailed studies on issues regarding its markets: real estate market in Europe, individuals and rental investment…

• The Capacim indicator, created together with Paris-Dauphine University, quarterly determines the percentage of households’ ability to purchase a real estate property suited to their needs, based on sampling of 33 French cities.

CRÉDIT FONCIER GIVES HELPFUL MARKETS INSIGHTS AND STUDIES To gain a better insight into real estate markets, Crédit Foncier has developed several tools and market studies.

Le 7 avril 2014

DECOUVREZ LE CHIFFRE CLE DE LA SEMAINE DU CREDIT FONCIER

53 %

Il s’agit de la proportion de Français ayant acquis leur résidence principale, au bout d’un an de recherche.

Le saviez-vous ?

Seulement un Français sur deux a acquis sa résidence principale au terme d’un an de recherche. 28 % sont toujours en recherche et 19 % ont abandonné leur projet. Ces chiffres sont extraits de l’étude que le Crédit Foncier a dévoilée à la presse le 31 mars. Cette étude a été menée auprès de 3 700 Français visant à mieux appréhender le parcours d’acquisition de la résidence principale et à identifier les choix et arbitrages auxquels consent un acquéreur. Consultez l’étude : Parcours d’acquisition de la résidence principale : du rêve à la réalité. Retrouvez tous nos chiffres clés

** A propos du Crédit Foncier Le Crédit Foncier : un rôle central sur les marchés immobiliers. Le Crédit Foncier est aujourd’hui la première société spécialisée dans les financements et services immobiliers en France. Filiale à 100% du Groupe BPCE, 2ème groupe bancaire en France, le Crédit Foncier s’adresse à l’ensemble des acteurs qui, à un titre ou à un autre, ont besoin d’une expertise et d’une compétence uniques pour trouver une réponse à la mesure de leurs besoins immobiliers : les particuliers bien entendu, mais aussi les professionnels, les investisseurs et les collectivités locales. A tous, le Crédit Foncier apporte ses capacités d’innovation et de créativité, ainsi que son expérience d’un marché sur lequel il agit depuis plus de 160 ans. Le Crédit Foncier se déploie autour de cinq grands métiers : le financement immobilier des particuliers ; le financement des investisseurs et des professionnels de l’immobilier ; le financement des équipements publics ; les services immobiliers ; les opérations financières avec le refinancement.

Contacts Presse

Nicolas Pécourt

Directeur Communication externe et RSE Tél. : 01 57 44 81 07

Kayoum Seraly Responsable Communication Presse et Externe

Tel. : 01 57 44 78 34 [email protected]

Une étude issue du partenariat Chaire Ville et Immobilierentre l’Université Paris-Dauphine et le Crédit Foncier

Septembre 2013

2007 / 2012 Crise économique et pouvoir d’achat immobilier

des ménages : quels enseignements ?

Une étude du Crédit Foncier

Avril 2014

Parcours d’acquisitionde la résidence principale :

du rêve à la réalité

Une étude du Crédit Foncier

Décembre 2013

• Publication of research papers on major real estate issues.

• The “Observateur de l’immobilier”, a dedicated platform for real estate information on creditfoncier.com

-7-

2007/2012 Economic crisis and household purchasing power: Which lessons

can be drawn?

The European private real estate credit markets in 2012

Learning paths to acquire a principal residence:

makes dream come true

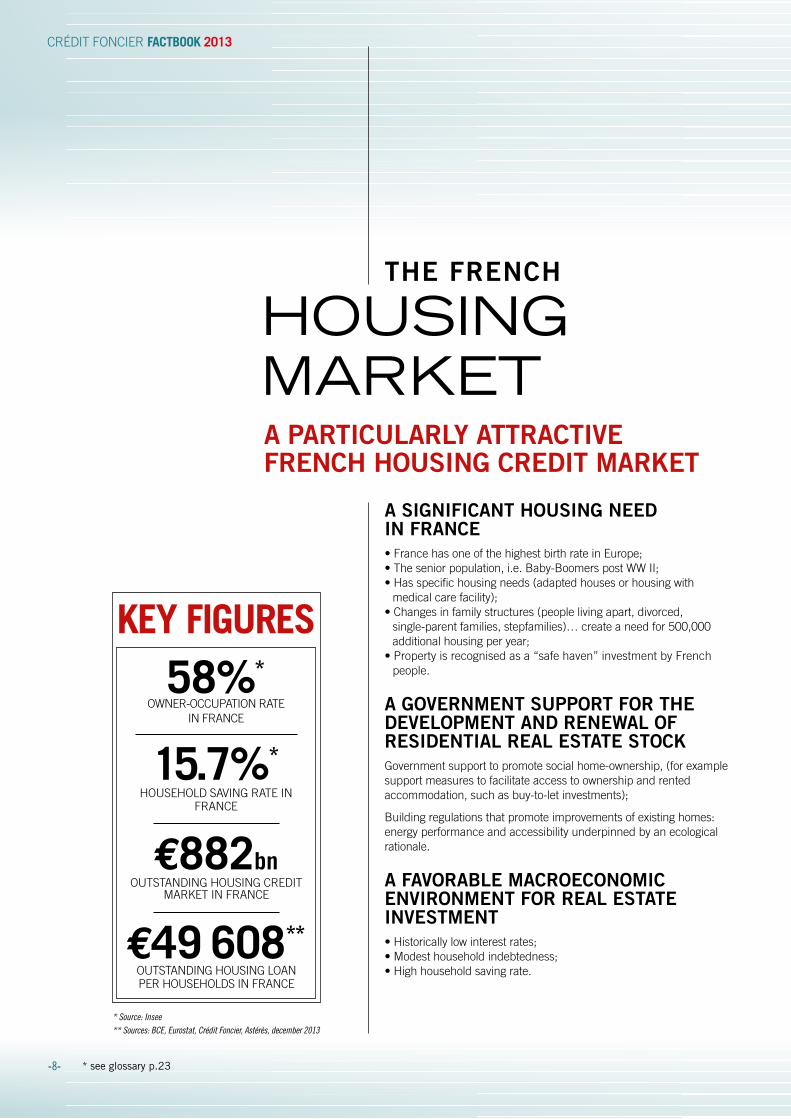

A SIGNIFICANT HOUSING NEED IN FRANCE• France has one of the highest birth rate in Europe;• The senior population, i.e. Baby-Boomers post WW II;• Has specific housing needs (adapted houses or housing with

medical care facility);• Changes in family structures (people living apart, divorced, single-parent families, stepfamilies)… create a need for 500,000

additional housing per year;• Property is recognised as a “safe haven” investment by French

people.

A GOVERNMENT SUPPORT FOR THE DEVELOPMENT AND RENEWAL OF RESIDENTIAL REAL ESTATE STOCKGovernment support to promote social home-ownership, (for example support measures to facilitate access to ownership and rented accommodation, such as buy-to-let investments);

Building regulations that promote improvements of existing homes: energy performance and accessibility underpinned by an ecological rationale.

A FAVORABLE MACROECONOMIC ENVIRONMENT FOR REAL ESTATE INVESTMENT • Historically low interest rates;• Modest household indebtedness;• High household saving rate.

A PARTICULARLY ATTRACTIVE FRENCH HOUSING CREDIT MARKET

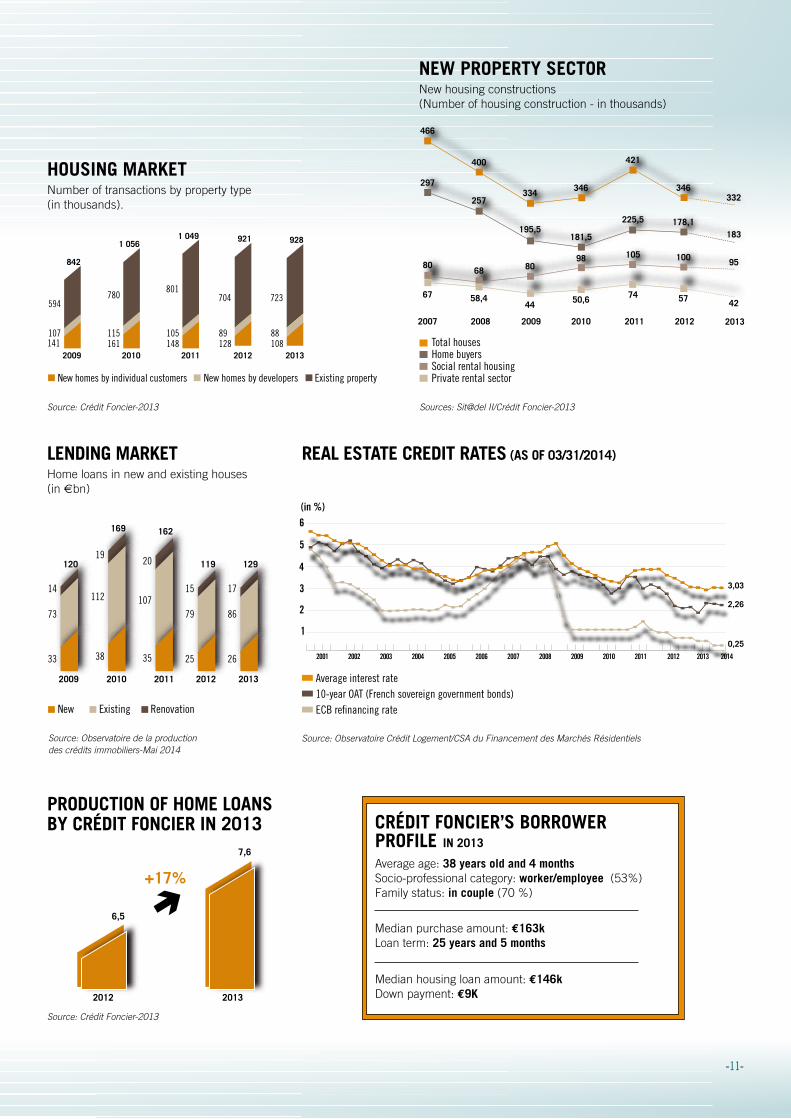

HOUSING MARKET

-8-

KEY FIGURES

OUTSTANDING HOUSING LOAN PER HOUSEHOLDS IN FRANCE

OUTSTANDING HOUSING CREDIT MARKET IN FRANCE

€49 608**

* Source: Insee** Sources: BCE, Eurostat, Crédit Foncier, Astérès, december 2013

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

58%*OWNER-OCCUPATION RATE

IN FRANCE

15.7%*HOUSEHOLD SAVING RATE IN

FRANCE

€882bn

THE FRENCH

2002 2003 2004 2005 2006 2007 2008 2009 2010 201130

36

42

48

54

60

2012

56%

A PARTICULARLY ATTRACTIVE FRENCH HOUSING CREDIT MARKET

-9-

REAL ESTATE LOANS BREAKDOWN: EUROPE AND FRANCE

Share of real estate loans as a percentage of household gross income

Share of outstanding real estate loans in the total indebtedness

63%

86%85%

69%

Sources: Banque de France, INSEE, national accounts-base 2005

FRENCH HOUSEHOLD DEBT AS % OF GDP DU PIB (2002-2012)

Multi-family housing

44%Single-family housing

56%

HOUSING TYPE33.5 million houses

Source: INSEE-2012

Sources: BCE, Eurostat, Crédit Foncier, Astérès-2013

2006 2007 2008 2009 2010 2011 2012 201360

70

80

90

100

110

120

SPAIN 67

GERMANY 114

FRANCE 106

UK 116

THE NETHERLANDS 85DENMARK 86

DEVELOPMENT OF REAL ESTATE PRICE INDICES (BASE 100 IN 2006)

Sources: Eurostat, Crédit Foncier, Astérès-2013

Other3%

Other40%

First-time homebuyers*

18%

Private housing22%Social

housing17%

Owners

58%Tenants

39%

European averageFrench average

A TAILOR-MADE CREDIT SOLUTION FOR ALL REAL ESTATE PROJECTS • Financing of principal or secondary residence, as well as

rental property, in new or existing property market;• Financing of seniors;• Financing of non-residents;• Financing of home improvements.

To finance these projects, Crédit Foncier develops a wide range of redeemable, bullet* and regulated loans.

LEADER OF FINANCING TO LOW-INCOME FAMILIES Crédit Foncier is the first lender to lowest-income households, commercialising almost half of the total loans for low-income families*. Crédit Foncier is also the leader in the distribution of PTZ +* with a market share of 25%.

Crédit Foncier is also a specialist in financing buy to let investment.

MULTI-CHANNEL DISTRIBUTION• 253 branches in France• 7,000 real estate professional partners (property agencies,

developers, constructors, real estate managers …)• An internet platform.

OF INDIVIDUALS THE FINANCING

For more than 160 years, the expertise of a specialist

Under French law, loans are granted depending on the borrowers’ creditworthiness, on justification and after review of the documentation:

• Required down payment in the financial plan prepared with the customer;

• Indebtedness is capped and doesn’t usually exceed 33% of the borrower’s net income;

• One of the two following guarantees: - Mortgage*, which can have an additional guarantee provided by FGAS* (Government fund promoting access to home ownership) for low income households, - Housing-loan sureties*.

• House and location value.

LOAN GRANTING IN FRANCE

-10-

253

KEY FIGURES

OUTSTANDING LOANS TO INDIVIDUALS

PRODUCTION OF LOANS TO INDIVIDUALS

MARKET SHARE IN LOANS FOR LOW-INCOME FAMILIES*

BRANCHES IN FRANCE

€49.9 bn

€ 7.6 bn

46%

Source: Crédit Foncier

CRÉDIT FONCIER PROVIDES FINANCING SOLUTIONS SUITED TO EVERYONE

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

-11-

2009 2010 2011

842

141107

594

1 056

161115

780

1 049

148105

801

2012

921

12889

704

2013

928

10888

723

HOUSING MARKET Number of transactions by property type (in thousands).

2009 2010 2011

120

33

73

14

169

38

112

19

162

35

107

20

2012

119

25

79

15

2013

129

26

86

17

LENDING MARKETHome loans in new and existing houses (in ebn)

20132012

7,6

+17%

6,5

PRODUCTION OF HOME LOANS BY CRÉDIT FONCIER IN 2013 CRÉDIT FONCIER’S BORROWER

PROFILE IN 2013

Average age: 38 years old and 4 monthsSocio-professional category: worker/employee (53%) Family status: in couple (70 %)

Median purchase amount: e163kLoan term: 25 years and 5 months

Median housing loan amount: e146kDown payment: e9K

NEW PROPERTY SECTORNew housing constructions (Number of housing construction - in thousands)

Average interest rate10-year OAT (French sovereign government bonds)ECB refinancing rate

REAL ESTATE CREDIT RATES (AS OF 03/31/2014)

Source: Observatoire Crédit Logement/CSA du Financement des Marchés Résidentiels

Source: Crédit Foncier-2013

Source: Observatoire de la production des crédits immobiliers-Mai 2014

New Existing Renovation

200920082007

67

80

297

466

400

334 346

181,5

98

50,6 74 57

100

178,1

346332

183

95

42

105

225,5

421

195,5

80

44

257

68

58,4

2010 2011 2012 2013

(in %)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

3,03

2,26

0,25

Total housesHome buyers Social rental housingPrivate rental sector

Sources: Sit@del II/Crédit Foncier-2013

Source: Crédit Foncier-2013

New homes by individual customers New homes by developers Existing property

Crédit Foncier supports two categories of private operators in carrying out their operations: private investors and real estate professionals.

A KEY PLAYER IN FINANCING PRIVATE INVESTORS • Financing private investors: listed or unlisted financial companies, investment funds, OPCI* (French real estate mutual funds), REITs*…;• Financing through medium- and long-term loans, all types of corporate property assets and residential properties: nursing homes for the elderly, tourism and leisure residences…;• Leasing solutions with Locindus, in which Crédit Foncier has a 74.5% stake.

A LEADER IN FINANCING REAL ESTATE PROFESSIONALS• Financing real estate professionals at the national and regional level: real estate developers, property vendors, land and subdivision developers...;• Short-term financing, sureties and guarantees needed to structure property transactions.

SOCFIM, a wholly-owned subsidiary of Crédit Foncier, as a lender to property developers is responsible for this activity. Crédit Foncier is positioned as one of the leaders in financing real estate development in France, thanks to the expertise of SOCFIM and the territorial expertise of the regional network of Groupe BPCE (Caisses d’Epargne and Banque Populaire banks).

Crédit Foncier is also a well-known arranger and agent of financing. Crédit Foncier arranges syndication* among entities within Groupe BPCE and external clients.

ESTATE INVESTORS AND PROFESSIONAL CUSTOMERS

OUTSTANDING LOANS TO REAL ESTATE INVESTORS AND

PROFESSIONAL CUSTOMERS

€8.2 billion

MARKET SHARE IN COMMERCIAL REAL ESTATE FINANCING

10%

OF FRENCH REAL ESTATE DEVELOPERS ARE CRÉDIT FONCIER

CUSTOMERS

90%

LOAN PRODUCTION TO REAL ESTATE INVESTORS AND

PROFESSIONAL CUSTOMERS

€1.9 billion

KEY FIGURES

-12-

CRÉDIT FONCIER PROVIDES TAILOR-MADE SOLUTIONS TO

PRIVATE SECTOR

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

THE FINANCING OF REAL

Source: Crédit Foncier

-13-

DEVELOPMENT OF THE INVESTMENT IN THE COMMERCIAL REAL ESTATE MARKET (1) (in ebn)

COMMERCIAL REAL ESTATE INVESTMENT: MAINLY CONCENTRATED IN ILE-DE-FRANCE (PARIS AREA)

200420032002 2005 2006 2007 2008 2009 2010 2011 2012 2013

11 1012

18

24

29

13

911

15 14,5 15

COMMERCIAL REAL ESTATE INVESTMENT BREAKDOWN BY INVESTOR TYPE

HIGH INVESTMENT PROFITABILITY A favourable spread environment for real estate investment10-year OAT spread evolution (rate in %) and real estate rates of return in Paris Q.C.A

16%Public listed REIT* [SIIC]

/ other property companies

22%*

Non-listed REIT* [SCPI & OPCI*]

28%Funds (including sovereign)

25%Insurance / Mutual

insurance companies

9%Other investors

(1) Commercial real estate: offices, retail stores, warehouses, business premisesSource: Crédit Foncier-2013 Source: Crédit Foncier-2013

Source: Crédit Foncier-2013 Source: Crédit Foncier-2013

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20131,50

3,50

3,00

2,50

2,00

4,00

4,50

5,00

5,50

6,00(in %)

1,47

4,25

2,20

1,69

1,090,51 0,76 1,85

1,68 1,391,71

-0,51

2,05

Spread in basis points (bps) 10-year OAT TEC rate, average calculated from the monthly rates (data: source AFT, BDF)

Rate of return Paris CBD (Central business district)

Geographical commercial real estate investment breakdown

Allocation part of commitments by type of property

Ile-de-France (Paris area)

OfficesOtherregions

Retail stores

Warehouses

74%

26%

66%

24%10%

SENIOR HOUSING COMPLEXFinancing by 4 Caisses d’Epargne and Socfim of a senior housing complex comprising 133 housing units and 995 m² of usable office space in Oberhausbergen realized by Aegide group.

GENERATOR HOSTELS Real estate leasing financing of the largest youth hostel construction in France (1,000 beds) located Place du Colonel Fabien in Paris. The Generator concept offers high quality services at affordable prices.

AQUAMUNDOFinancing by 2 Caisses d’Epargne, 1 Banque Populaire bank and Socfim

of the construction of 870 cottages and 21,000 m² of common equipments for Pierre & Vacances group in Moselle Department.

SILKY WAYFinancing arranger and structurer, alongside with Caisse d’Epargne Rhône Alpes, of the offices

and laboratories construction at Villeurbanne for the worldwide embedded electronics and computerised systems platform of Alstom Transport’s.

Sud

Arc

hite

ctes

Arc

hite

ctur

e st

udio

Ory

an

d A

ssoc

iate

d

Cen

ter

Par

cs

Scap

hoid

e 3D

ILLUSTRATION OF CRÉDIT FONCIER EXPERTISE:

THE FINANCING OF REAL

THE FINANCING OF

PUBLIC ENTITIES

-14-

Crédit Foncier lends to regional authorities* and to social housing bodies.

FINANCING PUBLIC PROJECTS TOGETHER WITH CAISSES D’EPARGNE • Together with Caisses d’Epargne, Crédit Foncier helps regionals

authorities, private partners and companies in their infrastructure projects;

• Financing projects, financial engineering or tailored solutions;

• Crédit Foncier intervenes in the following sectors: Transport infrastructure (tramway, bus, bypasses, roads…); networks (public lightening, energy, heating…) ; health (hospitals …);

education (schools, middle and high schools, universities and colleges…).

FINANCING STAKEHOLDERS OF THE SOCIAL PROPERTY • Solutions optimally tailored to real social estate players: Social landlords, regional authorities*, associations …;

• Crédit Foncier proposes its servicing platform to support the interventions of Caisses d’Epargne, which is another historical actor in this sector in France.KEY FIGURES

PRODUCTION OF PUBLIC EQUIPMENT’S LOANS

OUTSTANDING OF PUBLIC EQUIPMENT’S LOANS

€2,2 bn

€25.7bn

Source: Crédit Foncier

CRÉDIT FONCIER PROVIDES FINANCING THAT

CONTRIBUTES TO LOCAL DEVELOPMENT

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

PUBLIC ENTITIES

-15-

EVOLUTIONS OF FRENCH LOCAL PUBLIC AUTHORITIES INDEBTEDNESS* (in Mde)

(*) Annual debt as of 31 December according to the regulation n°3605 of the European Commission

Sources: National accounts – Notification of 31 Mars 2014, INSEE

SOCIAL HOUSING: CRÉDIT FONCIER’S PRODUCTION STRUCTURE BREAKDOWN BY ASSETS TYPE

5%Property

arrangement 5%

Renovation works

18%Retirement

centers

5%Youth hostels

5%Student residences

55%Family housing

Source: Crédit Foncier-2013

CRÉDIT FONCIER’S LOCAL AUTHORITIES LOAN PRODUCTION BREAKDOWN BY TYPE OF CUSTOMER

20%Municipalities8%

Departments

1%Regions

36%Healthcare centers

35%Groups

of municipalities

Source: Crédit Foncier-2013

SOCIAL HOUSING: CRÉDIT FONCIER’S PRODUCTION STRUCTURE BREAKDOWN BY CLIENT TYPE

17%Local public

organisations

11%Associations

1%Others

1%Local authorities*/Healthcare centers

68%Social landlords

Source: Crédit Foncier-2013

2004 2005 2006 2007 2008 2009 2010 2011 2012

113,0 119,5 127,3 137,4 148,3 157,3 163,3 168,9 176,1

2013

182,3

STUDENT RESIDENCE IN PAU 100% financing of the construction of 204 student apartments located in the Coudères residence being part of an urban renewal project promoting diversity: student housing, family housing, child protection centers and municipal rooms.

THE DIGITAL CAMPUS OF THE EUROPEAN UNIVERSITY OF BRETAGNE Being financed by Crédit Foncier together with the Caisse d’Epargne Bretagne Pays de Loire, Breizh Connect company provides construction, operation and maintenance of the first digital campus in France that will connect students with research centers all across Bretagne.

IRCA – REGIONAL INSTITUTE OF CANCER OF ALSACE Following the request of the Caisse d’Epargne d’Alsace, a contribution of 67% of the required funding was provided for building a Regional Cancer Center resulting from an alliance of Paul

Strauss Center and university hospitals of Strasbourg.

Dou

g an

d W

olf f

or M

iche

l R

enon

’s a

rchi

tect

ure

stud

io

Gro

upe

6

Rud

y R

icci

otti

and

Ale

xand

re L

acaz

e

ILLUSTRATION OF CRÉDIT FONCIER EXPERTISE:

Real estate services are provided by Crédit Foncier Immobilier (CFI), a wholly-owned subsidiary of Crédit Foncier. Crédit Foncier Immobilier supports institutional investors, companies, developers, banking and financial institutions as well as local authorities* across different activities.

ADVISORY, VALUATION AND RESEARCH • Advice to institutional owners in their real estate activities;• Expertise of all types of property products;• Valuation of real estate assets;• Research on all residential and commercial property markets.

BROKERAGE AND PROPERTY MANAGEMENT UNDER THE AD VALOREM BANNER• Ad Valorem Investissement provides consultancy services for buying or selling block sales;• Ad Valorem Bureaux supports companies in the search for new facilities;• Brokerage of new and existing building, on behalf of large

institutional owners or developers with Ad Valorem Residential;• Lease managment with Ad Valorem Gestion.

As a part of synergies with Groupe BPCE, Crédit Foncier makes these various services available to other Group entities and their customers.

SERVICESREAL ESTATE

KEY FIGURES

TURNOVER€41m

SALES RECORDED

610MISSIONS OF EXPERTISE AND

VALUATION

41,000

REAL ESTATE EXPERT IN FRANCE 1st **

CRÉDIT FONCIER IMMOBILIER

-16-

* Considering the 2013 total turnover published on “societe.com”** Considering the 2013 turnover for the Expertise activity published on “societe.com”Source: Crédit Foncier Immobilier

CRÉDIT FONCIER IMMOBILIER PROVIDES A FULL RANGE OF SERVICES FROM ADVISORY

TO BROKERAGE

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

Crédit Foncier Immobilier, is the fourth-largest French

real estate consultant*

Market research4%

Residential 20%

Offices 1%

Property management / Leasing3%

Real estate valuation (Serexim)

19%

Expertise39%

Consulting and audit4%

Investment10%

-17-

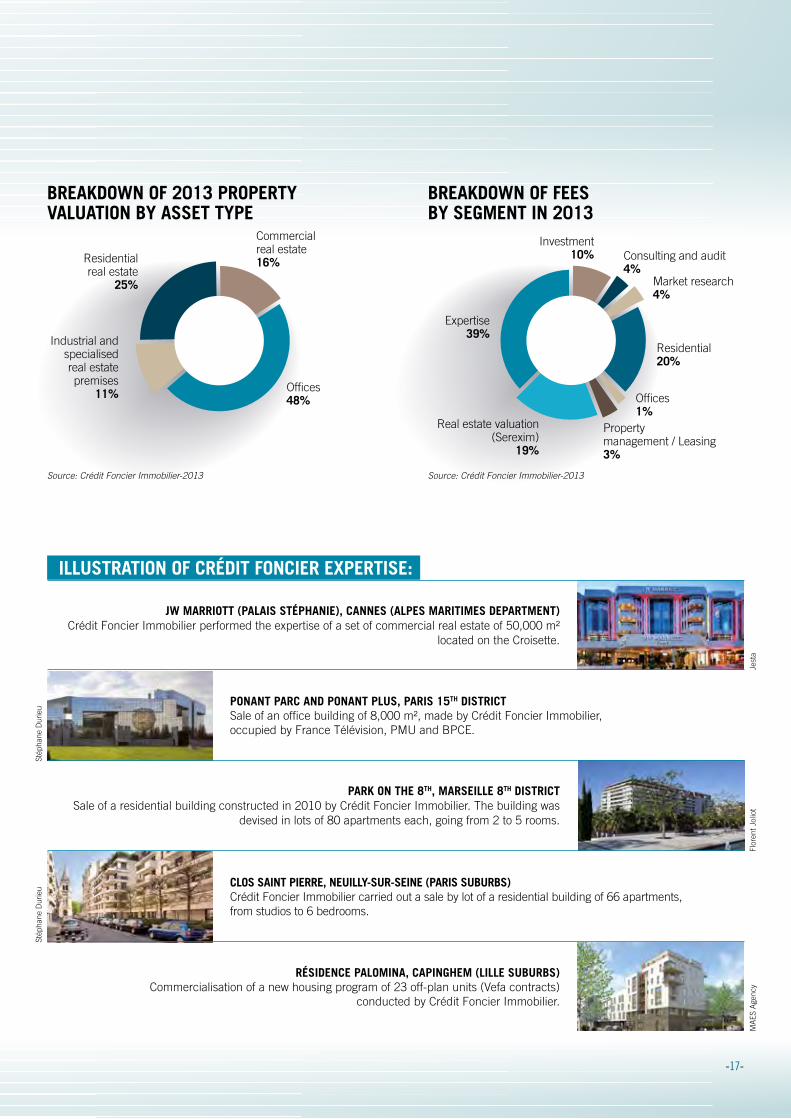

BREAKDOWN OF FEES BY SEGMENT IN 2013

BREAKDOWN OF 2013 PROPERTY VALUATION BY ASSET TYPE

Commercial real estate16%

Offices48%

Industrial and specialised real estate premises

11%

Residential real estate

25%

Source: Crédit Foncier Immobilier-2013 Source: Crédit Foncier Immobilier-2013

PONANT PARC AND PONANT PLUS, PARIS 15TH DISTRICTSale of an office building of 8,000 m², made by Crédit Foncier Immobilier, occupied by France Télévision, PMU and BPCE.

CLOS SAINT PIERRE, NEUILLY-SUR-SEINE (PARIS SUBURBS)Crédit Foncier Immobilier carried out a sale by lot of a residential building of 66 apartments, from studios to 6 bedrooms.

RÉSIDENCE PALOMINA, CAPINGHEM (LILLE SUBURBS)Commercialisation of a new housing program of 23 off-plan units (Vefa contracts)

conducted by Crédit Foncier Immobilier.

PARK ON THE 8TH, MARSEILLE 8TH DISTRICTSale of a residential building constructed in 2010 by Crédit Foncier Immobilier. The building was

devised in lots of 80 apartments each, going from 2 to 5 rooms.

JW MARRIOTT (PALAIS STÉPHANIE), CANNES (ALPES MARITIMES DEPARTMENT)Crédit Foncier Immobilier performed the expertise of a set of commercial real estate of 50,000 m²

located on the Croisette.

Stép

hane

Dur

ieu

Flor

ent J

olio

tJe

sta

MA

ES A

genc

y

Stép

hane

Dur

ieu

ILLUSTRATION OF CRÉDIT FONCIER EXPERTISE:

FINANCIAL

OPERATIONSFinancial operations business line ensures the refinancing of loans granted by Crédit Foncier and other Groupe BPCE entities.

The funding is mainly provided by Compagnie de Financement Foncier, société de credit foncier (French legal covered bonds* issuer) and a wholly-owned subsidiary of Crédit Foncier, whose primary objective is to refinance the mortgage and public sector lending activities by issuing obligations foncières (French legal covered bonds*). Its ability to innovate in terms of products and financial engineering enabled it to quickly become a prominent player on the global markets.

Compagnie de Financement Foncier stands out among other european covered bonds* issuers by a broader investor base in Asia and in the US, as well as Central banks – of which 80 hold Compagnie de Financement Foncier’s obligations foncières – and insurers.

Under Groupe BPCE’s new strategic plan “Growing Differently”, Compagnie de Financement Foncier will share with the entire group its funding capacities and its ability to raise long-dated liabilities at an advantageous cost compared with other refinancing vehicles. In addition to its traditional funding tools, Crédit Foncier is developing its activities in securitising real estate loans.

Crédit Foncier is positioned as an innovative player in setting up securitisation funds dedicated to this type of operation. Having launched, in 1991, the first public securitisation of mortgage loans in France, Crédit Foncier has a thorough and long-standing expertise in this area.

KEY FIGURES

€75 bnOUTSTANDING OF

OBLIGATIONS FONCIÈRES

AAA/Aaa/AA+RATINGS OF OBLIGATIONS FONCIÈRES

AS OF MAY 31, 2014 (S&P/MOODY’S/FITCH)

REGULATORY OVERCOLLATERALIZATION* RATIO

118.1%

REGULATORY CAPITAL

€4.4 bn

NET INCOME

€32.6m

-18-

Source: Crédit Foncier

COMPAGNIE DE FINANCEMENT FONCIER, A

WHOLLY-OWNED SUBSIDIARY OF CRÉDIT FONCIER, WHOSE PURPOSE IS TO REFINANCE

THE MORTGAGE AND PUBLIC SECTOR LENDING ACTIVITIES

GRANTED BY CRÉDIT FONCIER.

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

OPERATIONS 0

100

200

Scan

dinav

ia

German

ySp

ainFra

nce UK

Italy

Switz

erlan

d

Benelu

x

Irelan

d

USA/Can

ada

Austr

ia

Portu

gal

Austr

alia/N

ZOthe

rs

300

400

500

600

700

0

50

100

150

200

250

800 300

Issuance Outstanding

GLOBAL COVERED BONDS* MARKET IN 2012 (in ebn)

Source: European Covered Bond Council (ECBC)

Source: Crédit Foncier-2013

2% Asia3% Italy

7% Scandinavia

9% Other

36% Germany

41% France

2% UK

4% Italy

2% North America

1% Spain

2% Japan

1% Switzerland

1% Germany

2% Other87% France

8%Replacement

securities

5%Other assests

43%Mortgage loans

44%Public sector

exposures

63%Insurance

compagnies

2%Pension funds

9%Due to central banks

12%Banks

14%Asset managers

BY REGION

BREAKDOWN OF ASSETS (AS OF 12/31/2013)

BY TYPE OF ASSETS

BY INVESTOR TYPE BY REGION

BREAKDOWN OF OBLIGATIONS FONCIÈRES ISSUANCES (AS OF 12/31/2013)

Source: Crédit Foncier-2013Source: Crédit Foncier-2013

Source: Crédit Foncier-2013Source: Crédit Foncier-2013

COMPAGNIE DE FINANCEMENT FONCIER BUSINESS MODEL

Mortgage loans andrelate items

Publicexposures

Finance assets

Replacementsvalues

Derivatives (swaps*)

Assetselectionpurchase

InvestorsObligationsfoncières+privileged debt

Subordinated debt*,capital andunsecured debt*

-19-* see glossary p.23

2013 RESULTSCRÉDIT FONCIER’S

2013 2012 VARIATION

Net banking income 572 721 -149

Operating expenses -547 -581 34

Gross operating income 25 140 -115

Cost of risk -250 -131 -119

Income from holdings consolidated by the equity method 2 2 0

Income from other non-current assets 15 3 12

Income before tax -208 14 -222

Income tax 80 -5 85

Minority interests -2 -2 0

Group share of net income -130 7 -137

C/I ratio (1) 95.6% 80.6% +15.0 pts

(in €M)

(1) Cost income ratio = OPEX/NBI.

-20-

Net banking income amounted to e572m, down almost 21% compared to 2012. The main reason for this decrease is the net impact of transactions aimed at reducing balance sheet size that were initiated in late 2011 as part of the strategic plan (disposal of securities and buyback of obligations foncières) for - e146m.Additionally, it should be noted that the reassessment of the credit spread on structured issues at fair value through profit or loss represented a e59m expenditure in 2013 (compared to a e55m expenditure in 2012). Commissions, meanwhile, are up, mainly due to an increase in prepayments.

Overheads, depreciation and amortisation amortisation amounted to e547m, down 6% from 2012 due to a continued effort to control management costs. This change is being caused by both a decrease in labour costs (particularly as a result of the provisional retirement agreement instituted in 2012) and by control over costs for fees and real estate expenses.

It should also be noted that the project to share computing resources with the Caisses d’Epargne platform has become operational.

Cost of risk resulted in a net provision of e250m, up significantly from 2012 due to a - e51m allocation to collective provisions on the portfolio of international assets and a considerable amount of allocations on a few specific loans.

Income from other non-current assets amounted to e15m in 2013 and takes into account the capital gains from the Paris property “Foncier Home”.

The group share of net income consequently amounted to - e130m for 2013. The prudential ratios have therefore been met, with a tier one* ratio of 9.7% under the standard method.

CRÉDIT FONCIER FACTBOOK 2013

* see glossary p.23

-21-

ASSETS 2013 2012

Cash and amounts due from central banks 7,400 3,705

Financial assets at fair value through profit or loss 2,754 3,438

Hedging derivatives 6,289 10,317

Available-for-sale financial assets 3,172 3,693

Loans and receivables due from credit institutions 15,218 18,578

Loans and receivables due from customers 102,335 108,741

Revaluation adjustment on interest rate risk-hedged portfolio 4,127 6,310

Held-to-maturity financial assets 135 135

Current tax assets 346 321

Deferred tax assets 1,054 728

Accrued income and other assets 4,973 7,103

Investments in companies accounted for by the equity method 56 55

Investment property 34 41

Property, plant and equipment 47 115

Intangible assets 7 10

Goodwill 13 13

TOTAL 147,960 163,303

EQUITY AND LIABILITIES 2013 2012

Financial liabilities at fair value through profit or loss 4,527 5,562

Hedging derivatives 6,284 11,144

Due to credit institutions 44,070 36,656

Due to customers 268 271

Debt securities 82,242 97,545

Revaluation adjustment on interest rate risk-hedged portfolio 0 49

Current tax liabilities 2 31

Deferred tax liabilities 1 2

Accrued expenses and other liabilities 5,854 7,319Provisions 234 238

Subordinated debt* 789 803

Group share of consolidated equity 3,590 3,586

o/w net income for the period -130 7

Non-controlling (minority) interests 99 97

TOTAL 147,960 163,303

(in €M)CONSOLIDATED BALANCE SHEET

CRÉDIT FONCIER4, quai de Bercy94224 Charenton Cedex

EXTERNAL COMMUNICATION AND [email protected]

HUMAN RESOURCES DEPARTMENT [email protected]

INVESTOR [email protected]

CRÉDIT FONCIER DE FRANCE

S.A. (French public limited company) with share capital of 1,331,400,718.80 eurosHead office: 19, rue des Capucines - 75001 ParisExecutive offices and postal address: 4, quai de Bercy - 94224 Charenton Cedex Paris Trade and Companies Register No.542 029 848Insurance intermediary registered with ORIAS under n°07 023 327

INTERNATIONAL REPRESENTATIVE OFFICES

GERMANYErik LEMAIREVon-der-Tann Strasse 2, 80539 - [email protected]

SWITZERLANDSuisse Public Finance Solutions SPFS19 rue de Candolle, 1205 - GENEVASWITZERLANDPhone: [email protected]

NORTH AMERICA Stéphane GARCIES1800 McGill College Avenue, Suite 2940, H3A 3J6 - MONTRÉAL, QCCANADAPhone: +1 514 [email protected]

JAPANFrédéric CHARLOT- METZLERHibiya Kokusai Building,18 F,2-2-3 Uchisaiwaicho, Chiyoda-ku - TOKYO 100-0011JAPONPhone: +81 (0)3 [email protected]

CONTACTS

-22-

CRÉDIT FONCIER FACTBOOK 2013

-22-

GLOSSARYBullet loan: property loans when the borrower pays only the interest each month. The principal is repaid at maturity of the loan.

Covered bonds: debt securities backed by a cover pool composed of mortgages or public sector loans.

FGAS: guarantee fund for property purchase by modest income individuals, supported by the State as a welfare measure.

First-time homebuyer: a person who buys a home for the first time as his or her residence.

Junior debt: debt that ranks after senior debt. It is a debt that is lower in repayment priority than senior debt.

Local/regional authorities: municipalities, departments, regions, Public Inter-municipal Cooperation (EPCI) with own taxation and others Local Public Entreprises (EPL).

Mortgage: security recorded by a notarial act is a right granted to a creditor on a property.

OPCI: French real estate mutual funds.

Overcollateralisation: rule according to which the total amount of eligible assets of a société de crédit foncier must be higher than the total amount of their liabilities secured by a privileged claim, e.g. covered bonds.

PAS: loans for low and mid-income families instituted to encourage homeownership by modest resources’ households and distributed only by Banks having signed a specific agreement with the French State.

PTZ+: (“Interest-free loan”) regulated, subsidised and subject to certain condition home loan for first time homebuyer with low or modest income resources.

Public-private partnership: financing method by which a public authority relies on private providers to finance and manage equipment providing or contributing to public service.

Real estate investor: an investor having the aim of generating income and accumulating property assets over time.

REIT: real estate investment trust whether public listed (SIIC in France) or not (SCPI or OPCI* in France).

Senior debt: debt with special garantees and for which repayment takes priority over other creditors, such as those holding subordinated debt or junior debt.

Surety: personal warranty given by a third party (natural person, mutual guarantee company ...) who undertakes to pay to the lending institution the amounts owed if the borrower defaults.

RICS: The Royal Institution of Chartered Surveyors (RICS) is an English professional organization whose mission is to regulate and promote the real estate profession, maintain a level of excellence and professionalism of its members through continuing education, protect customers and consumers through a strict code of Conduct (the 5 principles of the RICS) and provide advice, analysis and impartial assistance.

Securitisation: is the process of taking an illiquid asset, or group of assets, and through financial engineering, transforming them into a security

Solvency: measures the capacity to repay debts over the short, medium and long term in accordance with strict and tested rules.

Subordinated debt: a debt that ranks below other debts and is repayable after other debts have been paid.

Subsidised loan: a home loan eligible for state aid at an advantageous interest rate subject to certain conditions.

Swap: a financial derivative that consists of an agreement to exchange future cash flows between two parties.

Syndicated loan: a loan that is provided by a group of banks.

Tier one: the portion of financial institution equity deemed to be the most solid (core). It consists primarily of share capital, reserves from earnings and minority interests in subsidiaries.

Unsecured debt: debt that is not secured by a mortgage or other surety.

-23--23-

Crédit Foncier4, quai de Bercy - 94224 Charenton Cedex

Tel: +33 (0)1 57 44 80 00

Head office19, rue des Capucines - 75001 PARIS

www.creditfoncier.comfoncier.fr