creating a global surface solutions and advanced materials ... · pdf fileit's not...

TRANSCRIPT

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Creating a global surface solutions

and advanced materials powerhouse

Bellevue Meets Management

CFO Jürg Fedier

Flims, January 15, 2016

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 2

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

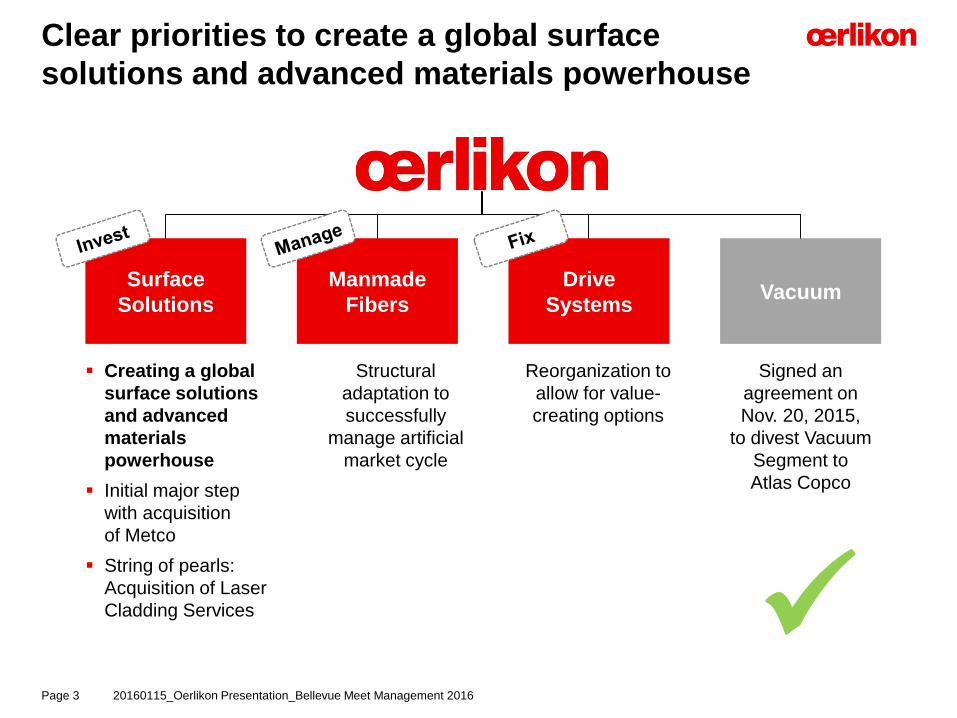

Creating a global

surface solutions

and advanced

materials

powerhouse

Initial major step

with acquisition

of Metco

String of pearls:

Acquisition of Laser

Cladding Services

Clear priorities to create a global surface

solutions and advanced materials powerhouse

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 3

Surface

Solutions

Manmade

Fibers

Drive

SystemsVacuum

Signed an

agreement on

Nov. 20, 2015,

to divest Vacuum

Segment to

Atlas Copco

Reorganization to

allow for value-

creating options

Structural

adaptation to

successfully

manage artificial

market cycle

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 4

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

The Surface Solutions Segment is a leader in

technologies to improve surface properties

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 5

Main surface functionalities

29147978Wear resistance

E.g. PVD coatings for cutting and

forming tools E.g. thermal spray coatings for

turbine blades

Thermal resistanceCorrosion / erosion

resistance

E.g. coatings for pump impellers

48711002Electrical properties

E.g. oxide coatings for fuel cells

Surface solutions

10688883Decorative

enhancement

E.g. DLC coatings for watches; ePD1

for decorative parts in cars

1 ePD = embedded PVD (thin-film coating on plastic substrate).

10688883Friction reduction

E.g. DLC coatings (Diamond-like-

coatings) for engine parts

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 6

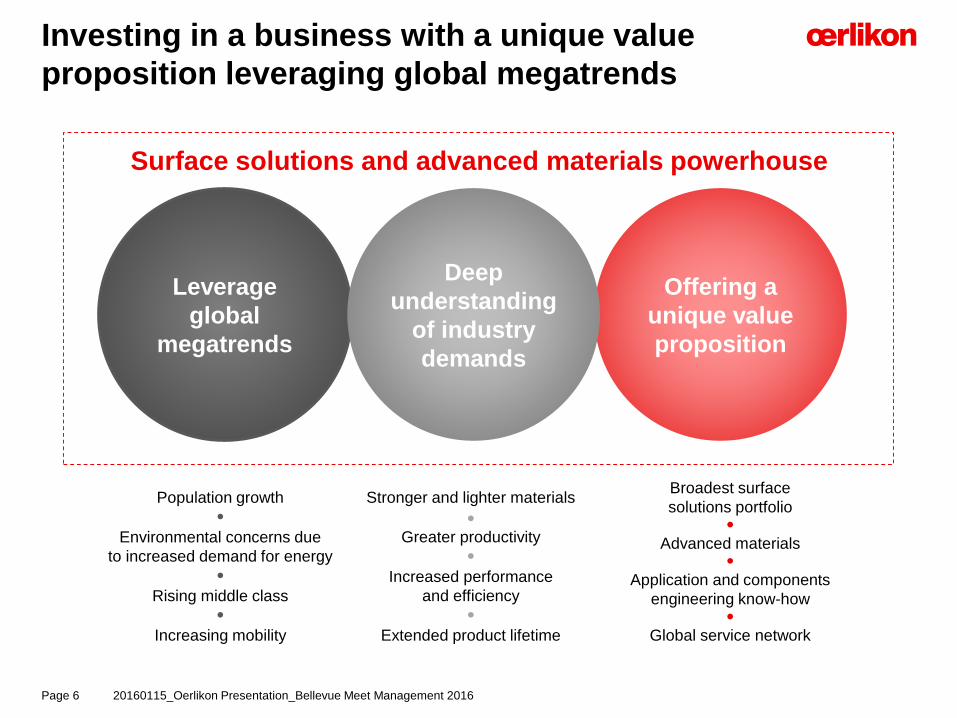

Investing in a business with a unique value

proposition leveraging global megatrends

Surface solutions and advanced materials powerhouse

Leverage

global

megatrends

Offering a

unique value

proposition

Deep

understanding

of industry

demands

Population growth

Environmental concerns due

to increased demand for energy

Rising middle class

Increasing mobility

Stronger and lighter materials

Greater productivity

Increased performance

and efficiency

Extended product lifetime

Broadest surface

solutions portfolio

Advanced materials

Application and components

engineering know-how

Global service network

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Surface Solutions Segment serving

attractive, growing end markets globally

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 7

Aviation Auto ToolingPower

generationOil & gas

General

industry

Higher fuel

efficiency

Tighter emission

regulations

Increase

resistance

requirements

Engine downsizing

Higher

productivity for

higher speed tools

Machining of ever

harder materials

Centralization of

purchasing

Higher energy

efficiency

Longer

maintenance

cycles

New-generation

technologies

More

sophisticated

extraction

methods

Oil price

Cost efficiency

Automated

production

Higher energy

efficiency

Surface Solutions Segment – underlying market growth1

Surface Solutions business outperforming underlying growth markets

2-4% 3% 2-4%

Lighter and more

efficient materials

Hotter engine

temperatures

Monolithic design

enabled by AM

4% 2% 0%

1 CAGR 2015 – 2018.

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

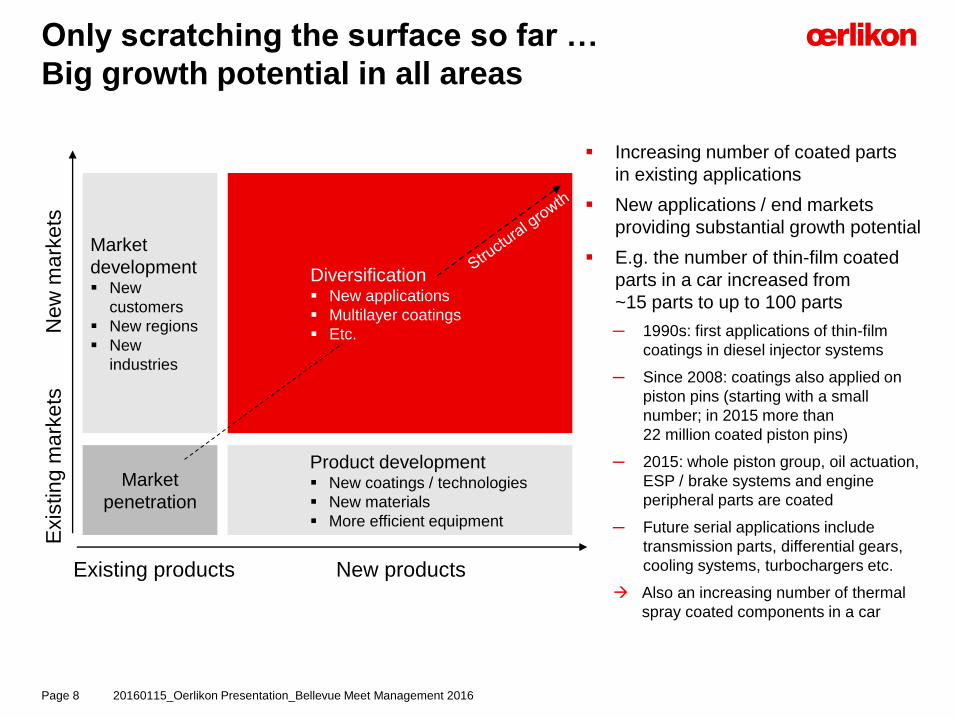

Only scratching the surface so far …

Big growth potential in all areas

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 8

Market

development New

customers

New regions

New

industries

Market

penetration

Diversification New applications

Multilayer coatings

Etc.

Product development New coatings / technologies

New materials

More efficient equipment

New products

Exis

ting m

ark

ets

Existing products

New

mark

ets

Increasing number of coated parts

in existing applications

New applications / end markets

providing substantial growth potential

E.g. the number of thin-film coated

parts in a car increased from

~15 parts to up to 100 parts

─ 1990s: first applications of thin-film

coatings in diesel injector systems

─ Since 2008: coatings also applied on

piston pins (starting with a small

number; in 2015 more than

22 million coated piston pins)

─ 2015: whole piston group, oil actuation,

ESP / brake systems and engine

peripheral parts are coated

─ Future serial applications include

transmission parts, differential gears,

cooling systems, turbochargers etc.

Also an increasing number of thermal

spray coated components in a car

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

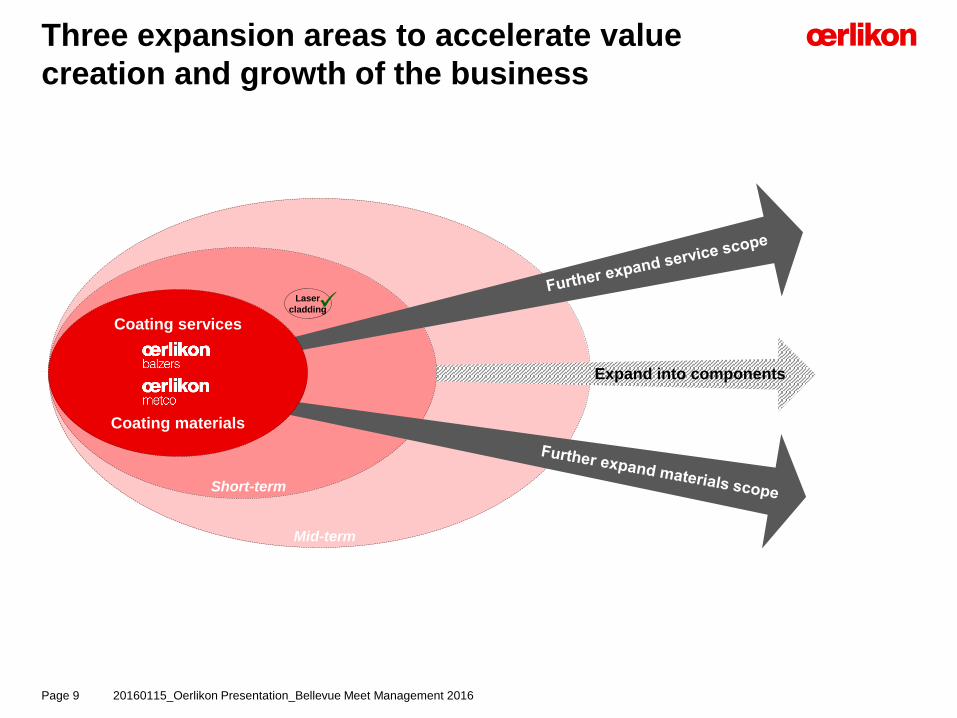

Three expansion areas to accelerate value

creation and growth of the business

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 9

Mid-term

Expand into components

Short-term

Coating services

Coating materials

Laser

cladding

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

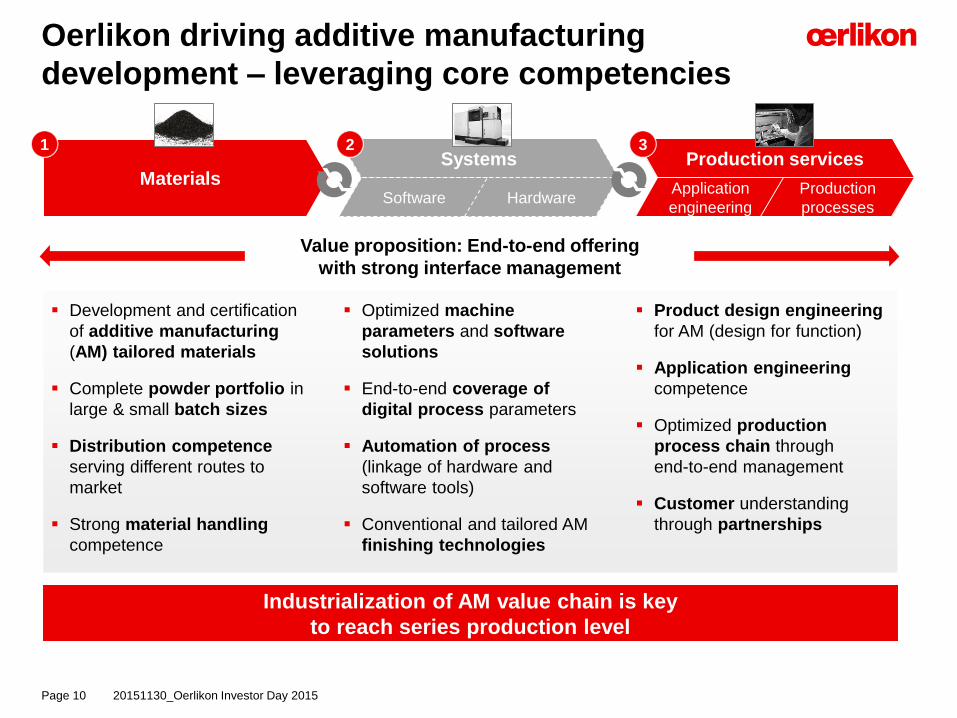

Oerlikon driving additive manufacturing

development – leveraging core competencies

Production services

Application

engineering

Production

processes

Development and certification

of additive manufacturing

(AM) tailored materials

Complete powder portfolio in

large & small batch sizes

Distribution competence

serving different routes to

market

Strong material handling

competence

Product design engineering

for AM (design for function)

Application engineering

competence

Optimized production

process chain through

end-to-end management

Customer understanding

through partnerships

Optimized machine

parameters and software

solutions

End-to-end coverage of

digital process parameters

Automation of process

(linkage of hardware and

software tools)

Conventional and tailored AM

finishing technologies

Materials

1 3

Value proposition: End-to-end offering

with strong interface management

Industrialization of AM value chain is key

to reach series production level

Systems

Software Hardware

2

20151130_Oerlikon Investor Day 2015Page 10

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Total addressable market by technology (as of 2015)

Disciplined expansion of business increases

addressable market by ~20% to ~CHF 11bn

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 11

Source: Oerlikon estimates

Additive manufacturing (AM)

Physical vapor deposition (PVD)

Brazing & welding

Nitriding (plasma & gas)

Thermal spray service

Others (components)

~CHF 9 bn ~CHF 11 bn+ additional

technologies

Total addressable market based

on current technology portfolio

Total addressable market

incl. additional technologies

By adding additional technologies such as brazing, welding and additive manufacturing, the

Surface Solutions Segment’s total addressable market increases by ~20% from

~CHF 9 billion to ~CHF 11 billion

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 12

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Oerlikon in the middle of the polyester value

chain

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 13

Refinery

Aromatics

plant

Steam

cracker

PTA plant

Polyester

yarn

Polyester

chips PET-packaging

Apparel

Home textiles

Technical textiles

Polyester chainEnergy and upstream petrochemicals

Oerlikon focus

End markets

PX

PTA

MEG

Crude

oil Naphtha

Ethylene

PX = paraxylene; PTA = purified terephthalic acid; MEG = monoethylene glycol; PET = polyethylene terephthalate.

Textile

processing

MEG plant

Polymer processing

(polycondensation)

Spinning

plant

Polyester melt

Polyester

melt

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

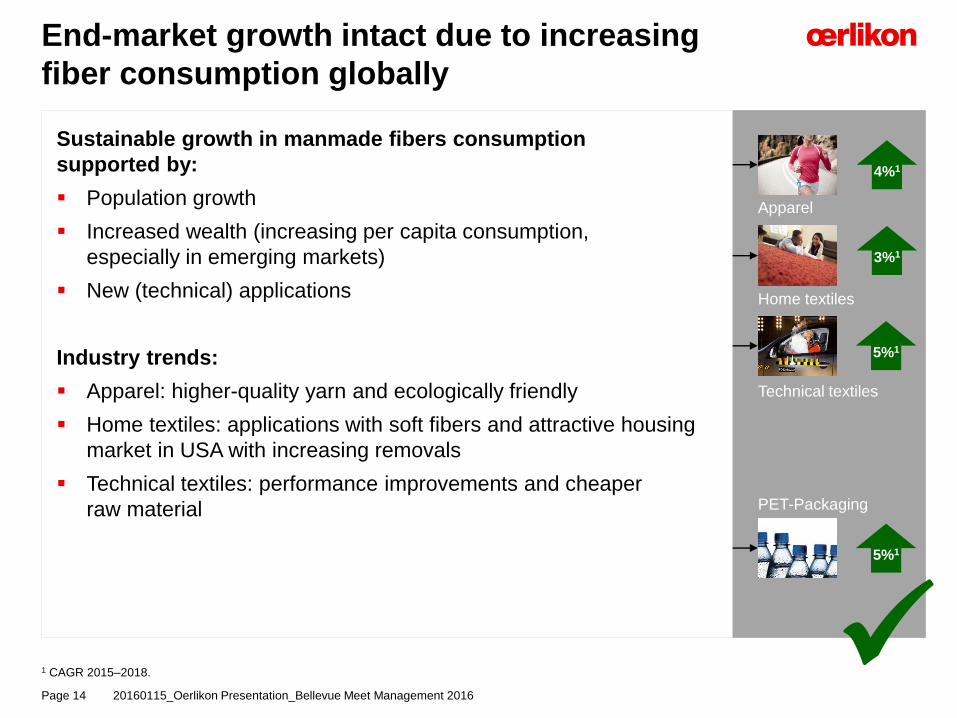

End-market growth intact due to increasing

fiber consumption globally

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 14

1 CAGR 2015–2018.

Refinery

Aromatics

plant

Steam

cracker

PTA plant

Polyester

yarn

Polyester

chips PET-PackagingMEG plant

Polymer processing

Spinning

plant Apparel

Home textiles

Technical textiles

Sustainable growth in manmade fibers consumption

supported by:

Population growth

Increased wealth (increasing per capita consumption,

especially in emerging markets)

New (technical) applications

Industry trends:

Apparel: higher-quality yarn and ecologically friendly

Home textiles: applications with soft fibers and attractive housing

market in USA with increasing removals

Technical textiles: performance improvements and cheaper

raw material

4%1

5%1

5%1

3%1

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

46

29

14

2020E2019E2018E2017E2016E201520102000

Revised growth environment in China in the

short term due to significant overcapacity

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 15

Boom of Chinese textile industry

driven by 12th five-year plan

China with ambition to become

number one in textile industry

Subsidies from Chinese

government

Easy access to financing

Overcapacity of 20 to 25%

Current situation characterized by overcapacity and general

slowdown of Chinese economy

Postponements of large-scale projects and cancellation of

smaller projects from Chinese customers

New regulations for handling chemicals after Tianjin

explosion

Slowdown of Chinese economy and devaluation of RMB also

impacting the Chinese textile industry

External factors additionally impacting global textile industry:

─ General economic downturn worldwide

─ Low oil price putting pressure on Segment’s customers

2011–15:

buildup of

overcapacity

Initial capacity assumption

(CAGR 6%)New reality

(CAGR ~3%)

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Now rather cautious indications from current drafts of

13th five-year plan (2016–2020)

Annual average growth rate of capacity expected to be

around 3% (vs. >9% in 12th five-year plan)

Chinese government controlling the new production

capacity to improve utilization of existing capacity

Three overlapping phases expected in 13th five-year

plan:

Latest assessmentInitial expectations

Initially positive indications from

first drafts of 13th five-year plan

Textile industry to be at the

core of the five-year plan

Continuous substitution of

natural fibers with

manmade fibers

Focus on high-tech fibers

Energy-efficient equipment

Directional adaptation in upcoming 13th

Chinese five-year plan1

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 16

1 13th Chinese five-year plan expected to be approved in March 2016.

Rebalancing:

Increase

capacity

utilization

Optimization:

Replace old

equipment

(technology

upgrade)

Appropriate

development:

Appropriately

recover the

growth of

production

capacity

(planned net

growth

~6 m t/a)

Phase 1Phase 2

Phase 3

2015

level

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

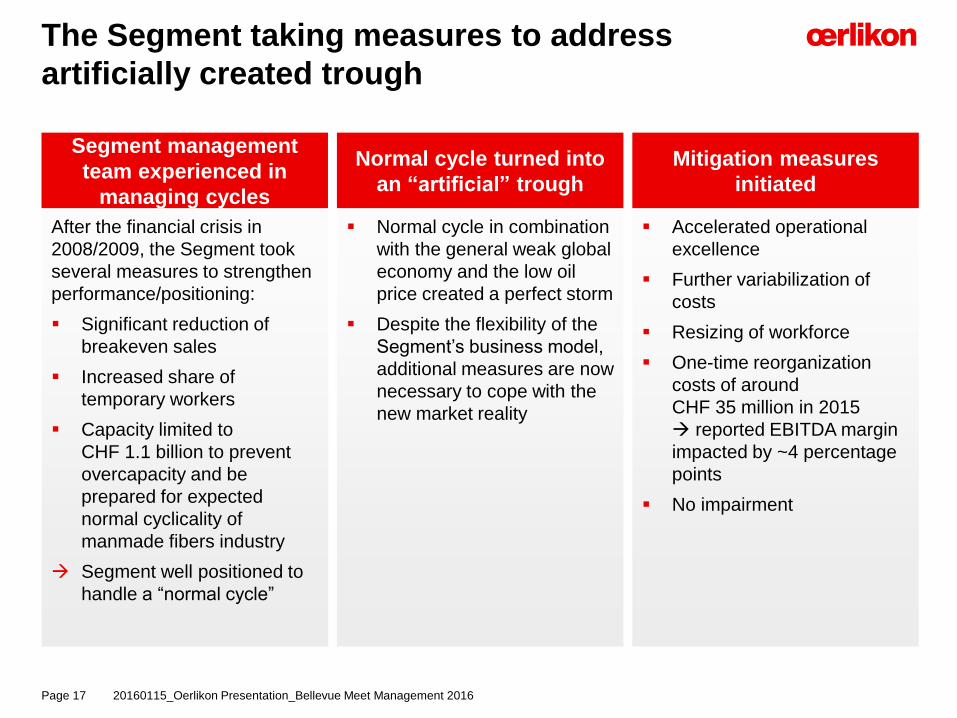

The Segment taking measures to address

artificially created trough

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 17

Accelerated operational

excellence

Further variabilization of

costs

Resizing of workforce

One-time reorganization

costs of around

CHF 35 million in 2015

reported EBITDA margin

impacted by ~4 percentage

points

No impairment

Segment management

team experienced in

managing cycles

After the financial crisis in

2008/2009, the Segment took

several measures to strengthen

performance/positioning:

Significant reduction of

breakeven sales

Increased share of

temporary workers

Capacity limited to

CHF 1.1 billion to prevent

overcapacity and be

prepared for expected

normal cyclicality of

manmade fibers industry

Segment well positioned to

handle a “normal cycle”

Normal cycle turned into

an “artificial” trough

Mitigation measures

initiated

Normal cycle in combination

with the general weak global

economy and the low oil

price created a perfect storm

Despite the flexibility of the

Segment’s business model,

additional measures are now

necessary to cope with the

new market reality

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 18

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

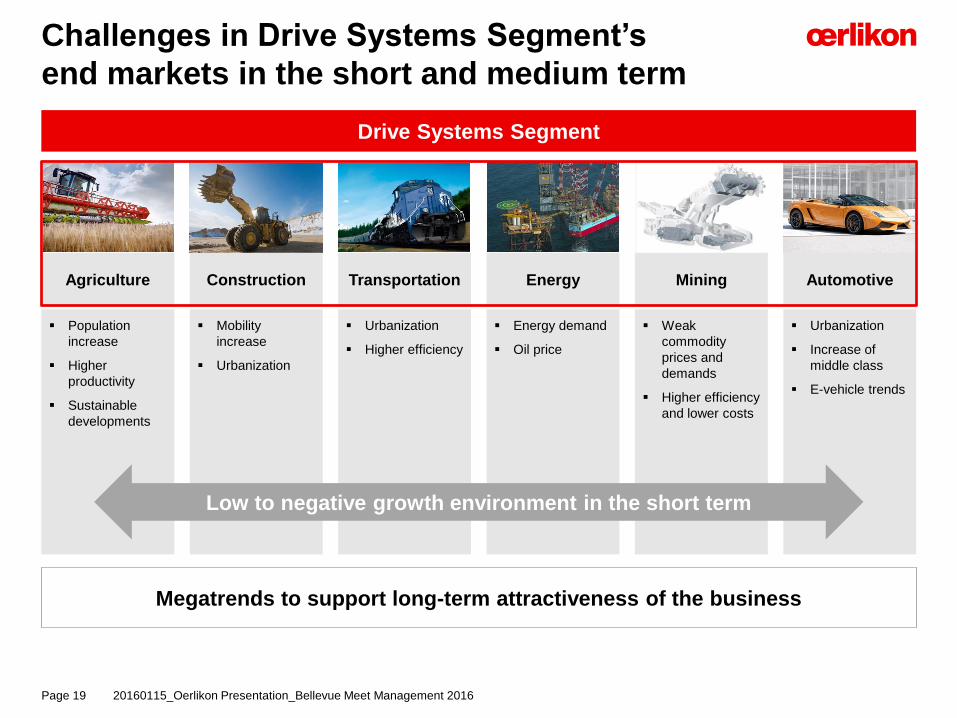

Challenges in Drive Systems Segment’s

end markets in the short and medium term

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 19

Agriculture Construction Transportation Energy Mining Automotive

Mobility

increase

Urbanization

Urbanization

Higher efficiency

Energy demand

Oil price

Weak

commodity

prices and

demands

Higher efficiency

and lower costs

Urbanization

Increase of

middle class

E-vehicle trends

Drive Systems Segment

Megatrends to support long-term attractiveness of the business

Population

increase

Higher

productivity

Sustainable

developments

Low to negative growth environment in the short term

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

New Segment strategy – focusing on key

competencies and products

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 20

Implementation of a focused factory concept with clear

lead factories for product lines

Each factory with maximum two product lines

Streamliningof productportfolio

Reduce product width: main focus on four key product

lines: gears, shifting solutions, planetary drives and

e-drives/hybrids

Reduce product depth: reduce total number of products

by around 20%

Increaserange of

applications

Focusfactoryconcept

Increase range of applications by rolling out key products

into adjacent industries with similar applications, i.e.

commercial and utility vehicles

Focus on key customers and higher-value-added projects

Improve quality of orders

Orderquality

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

About CHF 25 million

capex over the next three

years related to technology

upgrade

Reorganization provisions

in the range of CHF 55 to

65 million in 2015

Goodwill impairment of

around CHF 470 million

given the current weakness

in key end markets

impacting the medium- to

long-term outlook

Technology upgrade

Investments in cutting edge

manufacturing technology

enable the Segment to

maintain / expand its

leading position in gears

and synchronizer systems

into commercial vehicles

and to further strengthen

its competitive position in

clutch modules

Reorganization Financial impact

Reduction of cost base

─ Streamlining of

portfolio/product offering

─ Order selectivity

Resizing of global

workforce; workforce in

US already reduced by

approximately 250 FTEs

Reorganization measures initiated to adapt

to current market trends

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 21

Fix Drive Systems Segment to allow for value-creating options

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 22

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Costs and savings related to reorganization

Structural adaptation and reorganization

costs in Manmade Fibers and Drive

Systems Segment totaling

CHF 90 to 100 million in 2015

Noncash goodwill impairment in Drive

Systems Segment of around

CHF 470 million

Expected annual savings of

CHF 50 to 60 million starting 2016

Addressing cost base by reorganization and

continued operational excellence

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 23

Entire program centrally led by Group

Business Services

Productivity improvement with a focus on

supply chain management

Expected annual gross savings of

~CHF 40 million to compensate for

market-driven factors and cost inflation

Cost savings related to operational excellence program

Operational

Excellence

Recurring annual gross savings of up to CHF 100 million starting 2016

WCP = World Class Procurement; HSE = Health, Safety and Environment; WCM = World Class Manufacturing

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

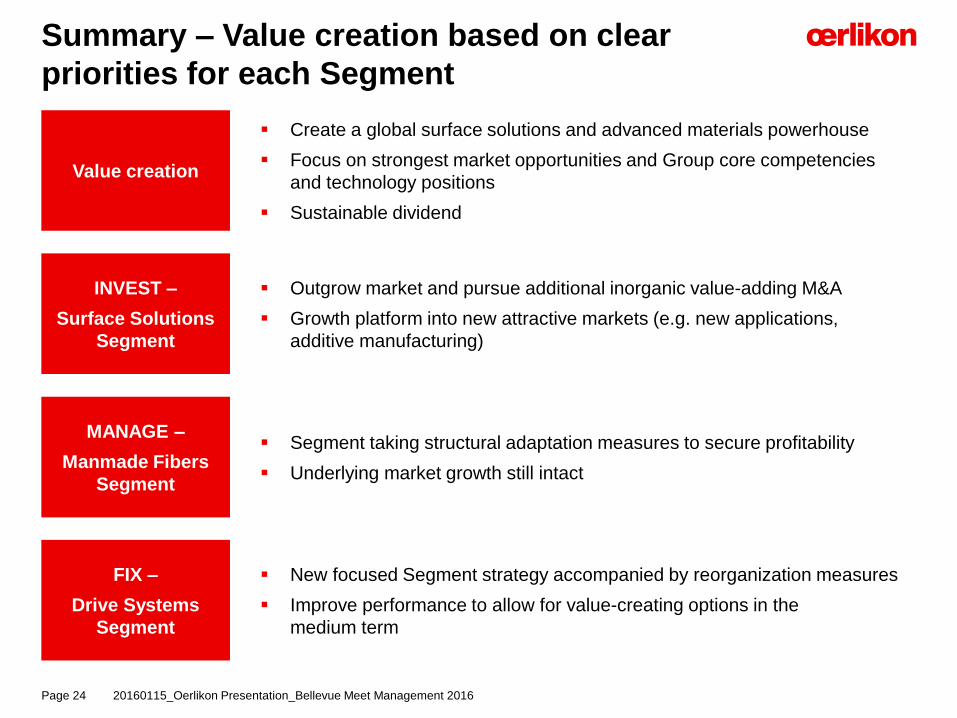

Summary – Value creation based on clear

priorities for each Segment

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 24

Value creation

INVEST –

Surface Solutions

Segment

Create a global surface solutions and advanced materials powerhouse

Focus on strongest market opportunities and Group core competencies

and technology positions

Sustainable dividend

Outgrow market and pursue additional inorganic value-adding M&A

Growth platform into new attractive markets (e.g. new applications,

additive manufacturing)

MANAGE –

Manmade Fibers

Segment

Segment taking structural adaptation measures to secure profitability

Underlying market growth still intact

FIX –

Drive Systems

Segment

New focused Segment strategy accompanied by reorganization measures

Improve performance to allow for value-creating options in the

medium term

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Agenda

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 25

1 Oerlikon priorities

– INVEST: Surface Solutions Segment

– MANAGE: Manmade Fibers Segment

– FIX: Drive Systems Segment

– Group & Summary

2 Appendix

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Oerlikon – a global industrial player

Oerlikon

Group

Sales: CHF 3 215m

EBITDA: CHF 525m

>15 500 employees

> 200 locations

36 countries

CHF 121m in R&D

Vacuum

Segment2

CHF 390m

CHF 41m

Drive

Systems

Segment

CHF 779m

CHF 82m

Manmade

Fibers

Segment

CHF 1 073m

CHF 217m

Surface

Solutions

Segment1

CHF 973m

CHF 183m

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 26

1 Metco consolidated for seven months; 2 Signed an agreement on Nov. 20, 2015, to divest Vacuum Segment to Atlas Copco

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

We want to acquire businesses that…

generate profitable growth above the

industry average

are innovation driven

extend / strengthen our technology

portfolio and/or market access

(customer access, geographic footprint)

offer a special value proposition to

customers

reduce earnings cyclicality

Acquisition criteriaCapital allocation priorities

Clearly defined capital allocation priorities

and acquisition criteria

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 27

Sustainable annual dividend

Pri

ori

tie

s

1. Invest in organic growth, R&D

and capital expenditure

2. Invest in “String of pearls”

(bolt-on M&A)

3. M&A in existing or adjacent

technologies/markets

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

A balanced portfolio with high share of

service business

Vacuum (discontinued operations)

Drive Systems

Manmade Fibers

Surface Solutions

Rest of World

Europe

Asia / Pacific

North America

Sales Q3 2015: CHF 722 million Sales Q3 2015 : CHF 722 million

41%

12%

22%

25%

39%37%

20%

4%

Segment split Regional split

Goods, Equipment

& Components

Service & Spare Parts

Sales Q3 2015 : CHF 722 million

67%

33%

Sales split

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 28

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

In CHF million In CHF million In CHF million; in % of sales

Adverse global developments in key end markets and regions as well as negative currency effects

Currency development impacts Group top-line in the amount of ~ minus 5 %

Q3 impact on profitability from Metco transaction: CHF 2.2m integration cost & CHF 7.4m amortization

Accelerated market weaknesses and

unfavorable FX impacted top-line

761722

851

-10.6%

Q3 2015Q3 20141 Q3 2015 at

constant FX

1 Q3 2014 restated for the divestment of the Advanced Technologies Segment

15.9% 16.3%

726691

825

-12.0%

Q3 2015 at

constant FX

Q3 2015Q3 20141

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 29

Order intake Sales EBITDA (margin)

122118135

-9.6%

Q3 2015Q3 20141 Q3 2015 at

constant FX

16.0%

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

In CHF million In CHF million

Order intake Sales

In CHF million; in % of sales

EBITDA (margin)

FX impact on Orders, Sales and EBITDA

Q3 2015

726691

Trans-

lation

effects

Q3 2015

FX

impact

adj.

+42

Trans-

action

effects

-7

Q3 2015

reported

5.1%

122118

Q3 2015

FX

impact

adj.

Q3 2015

reported

+6-2

3.4%

Trans-

lation

effects

Trans-

action

effects

16.016.3

Margin in %

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 30

761722

-6

Q3 2015

reported

Trans-

lation

effects

+45

Trans-

action

effects

5.4%

Q3 2015

FX

impact

adj.

Impact mainly related to translation as a result of reporting currency CHF

Appreciation of currencies (INR, USD, CNY) against CHF – EUR with devaluation against CHF

Limited impact on EBITDA margin

Impact on Segments varies in line with their global (currency) positioning

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

in CHF million Q3 2015 Q3 2014 Δ

Order intake 299 317 -5.7 %

Sales (to 3rd parties) 296 312 -5.1 %

EBITDA 63 46 +37.0 %

EBITDA margin1 21.3 % 14.6 % +6.7 pp

EBIT 38 18 >100 %

EBIT margin1 12.8 % 5.7 % +7.1 pp

Surface Solutions Segment – Strong

profitability despite lower top-line

RoW

5%

Asia /

Pacific

27%

North America

20%

Europe48%

Automotive

22%

Tooling37%22%

General

Industry

Aviation

Power Generation

12%

7%

1 as % of sales

Strong profitability achieved early cost

saving measures

Integration well on track further moving

toward normal operations

Continuous deployment of new products,

competence and applications

Europe shows positive development,

weakening in Asia; US behind expectation

MRO market flat; Automotive growth

slowed down, in particular China/Europe

Oil & Gas industry down (no prediction for

recovery short term)

Power Generation strong

Operational

performance

Market

development

Key figures

Sales

Q3 2015

Sales

Q3 2015

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 31

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Financial impact of Metco transaction –

Reality check confirms initial assumptions

2015E 2016E 2017E

>CHF 30 million >CHF 30 million >CHF 30 million

Integration costs

>CHF 10 million <CHF 10 million

~CHF 5 million >CHF 10 million

Top-line synergies

Cash

ite

ms

No

n-c

ash

ite

ms

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 32

Amortization of acquired identified intangibles assets

Cost synergies (cumulative)Reality check as of Sept. 30, 2015

Inte

gra

tio

n c

os

tsA

mo

rtiz

ati

on

Guidance

FY 2015:

>CHF 10m

9M 2015:

CHF 8.5m

Guidance FY 2015: >CHF 30m

9M 2015:

CHF 22.0m

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Illustrations of the advantages of surface

solutions

Page 33 20160115_Oerlikon Presentation_Bellevue Meet Management 2016

Surface

Solutions

Reliability

Safe, lifelong sealing for

subsea valves

Cost saving

Twenty-fold

increase in mine

dewatering pumps

and tar sand

screen life

Productivity

Coatings enable a

10% p.a. increase

in productivity

Energy efficiency

1 million liters of fuel saved

per hour, globally

Increased lifetime

Over 25 000 hours of

operation between services

Environmentally

friendly

Enabling up to 5% fuel

savings through reduction

of friction for heavy-duty

diesel engines1

Aerospace

Power generation

AutomotiveTools

Mining

Oil & Gas

1 Source: DEER 2007, Diesel Engine-Efficiency and Emissions Research Conference, Detroit.

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

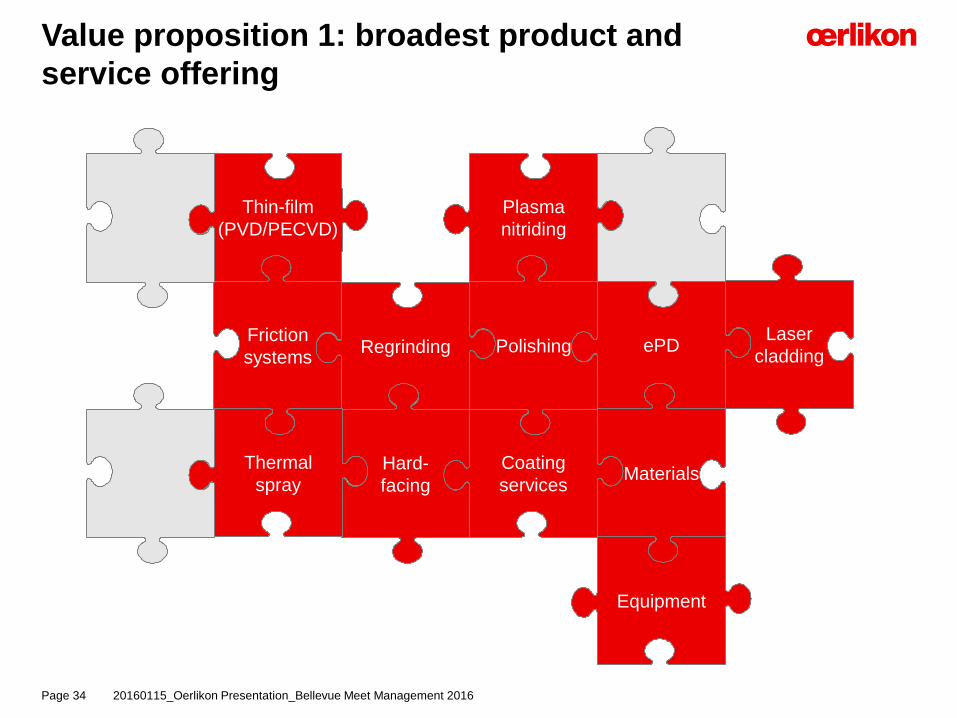

Value proposition 1: broadest product and

service offering

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 34

Friction

systemsRegrinding

Thin-film

(PVD/PECVD)

Polishing ePD

Plasma

nitriding

Coating

servicesMaterials

Hard-

facing

Laser

cladding

Thermal

spray

Equipment

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Customer example: customer in the automotive industry facing a problem with cylinder bores

Friction reduction by matching of inner bore thermal spray and PVD piston ring coating

Oerlikon delivers solutions for most challenging surface requirements through distinct technology and engineering know-how

Value proposition 2: strong application

engineering competence

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 35

Performance requirement Application engineering Coating solution

Customer facing a

problem in product

development

Oerlikon application

engineering know-how

Materials

Processes

Systems

Coatings part of

product design

Standard coating

service process

Coating integral part of next-generation product

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Value proposition 3: largest coating service

center network worldwide

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 36

24–48 hrs from pickup at customer site to reshipment

Incoming

inspection

Cleaning Pre-

treatment

Loading Coating Outgoing

inspection

Post-

treatment

Packaging /

shipping

Pickup /

delivery

Over 140 service and production

centers in 36 countries worldwide

Example of PVD coating service:

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Value proposition 4: broad and versatile

portfolio of materials and equipment

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 37

AgglomeratedAgglomerated

& sinteredAgglomerated

& HOSPAgglomerated

& densified

Sintered &crushed

Fused &crushed

Wateratomized

Gasatomized

Mechanicallyclad

Chemicallyclad

Drawn, swagedor rolled

Filled & drawn,swaged or rolled

Material feeder

Spray gun

Thermal spray materials Thermal spray equipment

Constantly developing new materials

with new properties, based on customer /

application requirements

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Reconditioning = regrinding and recoating

ReconditioningConventional coat vs. BALINIT coat

Coatings on cutting tools significantly

increase productivity and tool life

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 38

BALINIT Pertura coat from Oerlikon Balzers

…increases drilling speed by factor of

2.5 from 80 m/min to 210 m/min and

therefore increases productivity by 85%

…extends tool life time by ~67%

(1 000 holes instead of 600 holes)

+ + + + + +

4 new tools

100%total costs

1 new tool

reconditioned 3×

50%cost savings

A used tool can be reconditioned up to

three times (some tools up to eight times)

and has the same performance as a virgin

tool but at 50% of the costs

37

20

0

10

20

30

40

BALINIT®

PERTURA

+85%

Conventional

coat

Holes/minute

1,000

750

250

0

500

BALINIT®

PERTURA

Conventional

coat

+67%

600

1,000

Tool life time (# of drilled holes)

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Significant savings in production costsCoated vs. uncoated forming tools

When forming stainless steel, untreated

tools quickly approach their limits. The

series production of heat shields, for

instance, will stop at about 2 000

produced parts due to cracks in the

tool surface

With thin-film coatings, the life of the

forming tool can be extended by a

factor of ten

Coatings on forming tools reduce

production costs by more than 80%

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 39

20,000

Tool costs

(EUR)

2,000

Tool life

(number of

formed heat

shields)

11,080

10,000

+900%

+11%

Uncoated forming tool

Coated forming tool

5,245,00

0,750,55

Tool costs

per produced

part (EUR)

Total

production

costs per

part (EUR)1

-89% -86%

1 Production costs of € 0.20; extra cost per part for uncoated tools of € 0.04.

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

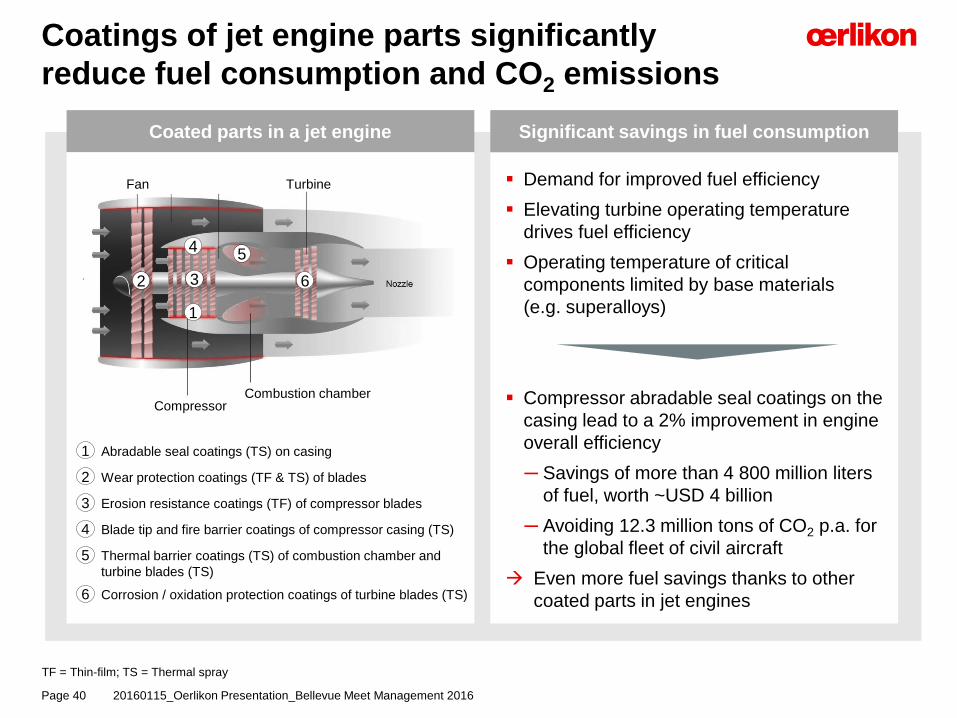

Demand for improved fuel efficiency

Elevating turbine operating temperature

drives fuel efficiency

Operating temperature of critical

components limited by base materials

(e.g. superalloys)

Compressor abradable seal coatings on the

casing lead to a 2% improvement in engine

overall efficiency

─ Savings of more than 4 800 million liters

of fuel, worth ~USD 4 billion

─ Avoiding 12.3 million tons of CO2 p.a. for

the global fleet of civil aircraft

Even more fuel savings thanks to other

coated parts in jet engines

Significant savings in fuel consumptionCoated parts in a jet engine

Coatings of jet engine parts significantly

reduce fuel consumption and CO2 emissions

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 40

Turbine

Combustion chamberCompressor

Fan

5

63

4

2

1

1 Abradable seal coatings (TS) on casing

2 Wear protection coatings (TF & TS) of blades

3 Erosion resistance coatings (TF) of compressor blades

4 Blade tip and fire barrier coatings of compressor casing (TS)

5 Thermal barrier coatings (TS) of combustion chamber and

turbine blades (TS)

6 Corrosion / oxidation protection coatings of turbine blades (TS)

TF = Thin-film; TS = Thermal spray

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Coatings allow the use of high-performing cast-

iron brake disks instead of full ceramic disks

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 41

Demand for corrosion protection, higher

performance (less fading), higher comfort

(less noise), no dust on rims

Rising demand to reduce emissions

caused by brake dust, enhanced corrosion

protection for hybrid cars

Shiny brake disks as design element

Coatings on conventional cast-iron brake

disks:

─ Add ~CHF 40 extra costs on a ~CHF 160

noncoated conventional disk

─ 3× longer lifetime compared to conventional disks

─ Brake dust emission reduced by 50%

─ 90% less costs compared to a ceramic disk

Interesting for special vehicles (RVs,

construction, military) or other applications

(wind turbines, elevators)

Less costly alternative to ceramic disks Coated brake disks in a car

1 Cast-iron brake disk heat treated and coated with TS

2 Metal matrix composite (MMC) or carbide coatings (TS)

as wear-resistant coating on brake disk

3 Heat-treatment layer for superior corrosion protection

proprietary to Oerlikon Metco

4 Coating cross section – patent pending on coating system,

patent granted for coating composition

2

3

4

Brake disk

1

TS = Thermal spray; RV = Recreational vehicles

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Success story Metco integration –

combining leading surface technologies

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 42

Status quo

Technology:

Joint development by Balzers application

and Metco process engineers

Low-temperature plasma nitriding

process for austenitic stainless steel

Market rollout:

02.2015 Process development

07.2015 Customer sampling in Germany,

Italy, France and UK

01.2016 Production

Oerlikon’s solution

Customer perspective:

Food industry has special surface

requirements: easy to clean, no abrasion

Efficient processes needed for abrasion

protection of stainless steel parts

Market is looking for an improvement on

existing solution

Oerlikon perspective:

Balzers worked on stainless steel surface

treatments, yet so far had no competitive

solution for the food industry

Metco has know-how in nitriding

Development of solution only possible

due to combined R&D forces

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Ac

qu

isit

ion

his

tory

Inve

stm

en

t fo

cu

s

Surface Solutions Segment accounting for majority of capital expenditure within Oerlikon

Capex/depreciation ratio > 1 (excluding amortization of acquired intangible assets)

─ Expansion of capacity in existing coating centers

─ Technology upgrade (combining technologies from Balzers and Metco)

─ Develop new coatings, materials and applications

─ Two to four new coating centers each year

Surface Solutions Segment accounting for the majority of R&D expenditures within

Oerlikon Group

Business constantly expanding since 2011,

major step forward with Metco acquisition

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 43

Hartec

(ePD)

Rox

(regrinding)

Metco

(thermal spray

& materials)

2011 2012 2013 2014 2015 …

All recent acquisitions within Oerlikon Group related to the Surface Solutions Segment

Laser Cladding Services

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Acquisition of Laser Cladding Services to

service upstream energy and offshore markets

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 44

Company background

Industry leader in

protective coatings

Houston, USA

Founded 2001

Protective coating design,

manufacturing and

restoration of new and

used parts mainly in the

energy and oil & gas

sectors

Service offering:

─ Laser cladding

─ Thermal spray

─ Laser hardening

─ Precision grinding

Laser cladding technology

Technology:

Laser cladding is a process to apply

metal coatings using a laser as heat

source. The laser melts the base material

and an additive powder to create a

protective coating. Unlike welding, laser

cladding provides a strong metallurgical

bond with minimal dilution of the base

material, exceptional thickness control

and a small heat-affected zone.

Typical applications:

Impellers

Pump shafts

Bearing sleeves

Axle housings

Nozzles

Expanding laser cladding activities

and complementary to thermal

spray offering of Oerlikon Metco

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Technology leader in

equipment for surface

solutions

Strong brand recognition as global

player in high-end surface solutions

Access to global OEMs in

aero, oil & gas, automotive

and general industry

Strong presence and know-how in thermal

spray materials (metals and alloys, wires,

carbides, ceramics, abradables)

Global service network

with over 140 locations

worldwide

Complete offering of surface solutions in

materials, equipment, services

(PVD1 and thermal spray)

Oerlikon can leverage core competencies in

additive manufacturing

20151130_Oerlikon Investor Day 2015Page 45

1 PVD = Physical vapor deposition.

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

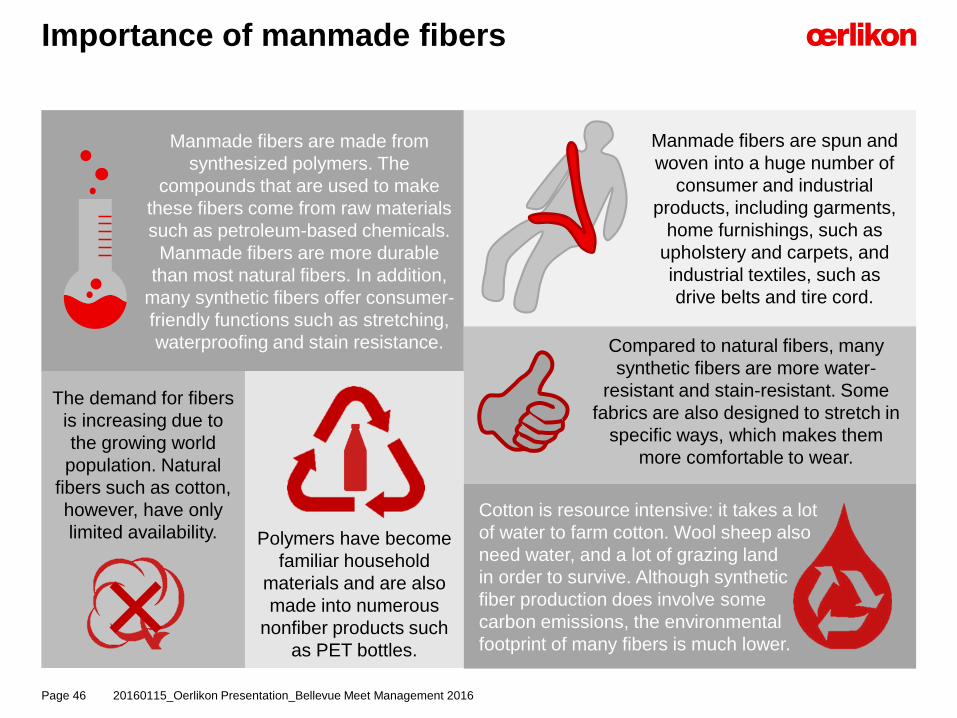

Manmade fibers are made from

synthesized polymers. The

compounds that are used to make

these fibers come from raw materials

such as petroleum-based chemicals.

Manmade fibers are more durable

than most natural fibers. In addition,

many synthetic fibers offer consumer-

friendly functions such as stretching,

waterproofing and stain resistance.

Importance of manmade fibers

20160115_Oerlikon Presentation_Bellevue Meet Management 2016

The demand for fibers

is increasing due to

the growing world

population. Natural

fibers such as cotton,

however, have only

limited availability. Polymers have become

familiar household

materials and are also

made into numerous

nonfiber products such

as PET bottles.

Manmade fibers are spun and

woven into a huge number of

consumer and industrial

products, including garments,

home furnishings, such as

upholstery and carpets, and

industrial textiles, such as

drive belts and tire cord.

Compared to natural fibers, many

synthetic fibers are more water-

resistant and stain-resistant. Some

fabrics are also designed to stretch in

specific ways, which makes them

more comfortable to wear.

Cotton is resource intensive: it takes a lot

of water to farm cotton. Wool sheep also

need water, and a lot of grazing land

in order to survive. Although synthetic

fiber production does involve some

carbon emissions, the environmental

footprint of many fibers is much lower.×Page 46

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Customer example – spinning plant

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 47

3 × 200 t/d polycondensation

504 WINGS POY

144 WINGS FDY

648 spinning positions

Polycondensation

Polymer melt

Winder

Daily output: 365 000 bobbins (15 kg each) 1 train with 275 wagons (total length of 4 km)

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

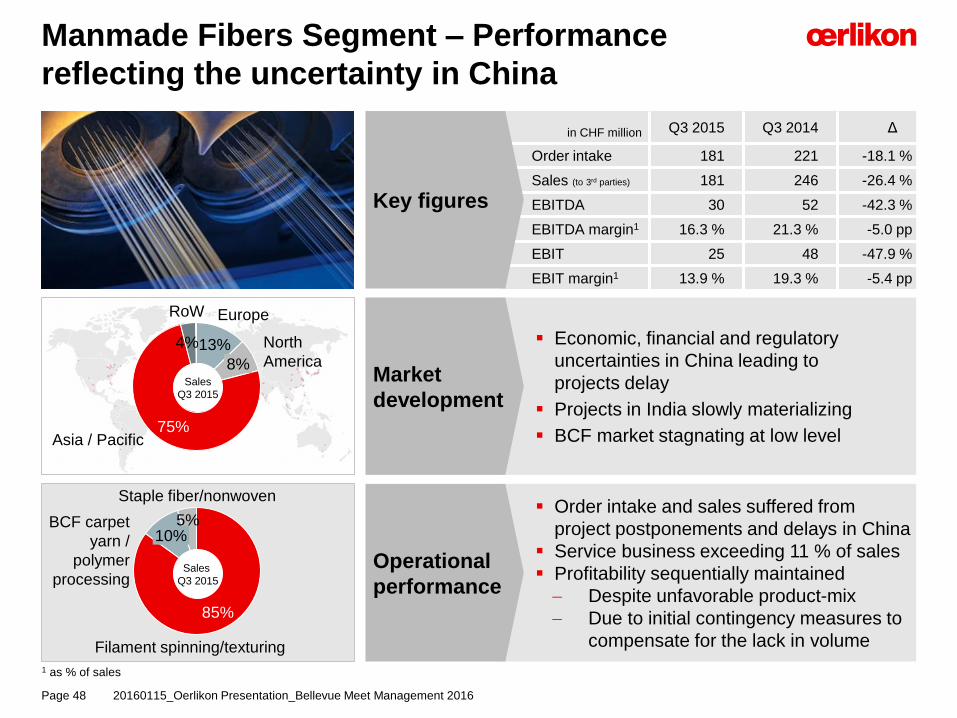

in CHF million Q3 2015 Q3 2014 Δ

Order intake 181 221 -18.1 %

Sales (to 3rd parties) 181 246 -26.4 %

EBITDA 30 52 -42.3 %

EBITDA margin1 16.3 % 21.3 % -5.0 pp

EBIT 25 48 -47.9 %

EBIT margin1 13.9 % 19.3 % -5.4 pp

Manmade Fibers Segment – Performance

reflecting the uncertainty in China

Order intake and sales suffered from

project postponements and delays in China

Service business exceeding 11 % of sales

Profitability sequentially maintained

Despite unfavorable product-mix

Due to initial contingency measures to

compensate for the lack in volume

Operational

performance

Economic, financial and regulatory

uncertainties in China leading to

projects delay

Projects in India slowly materializing

BCF market stagnating at low level

Market

development

North

America8%

Asia / Pacific

EuropeRoW

75%

13%

Staple fiber/nonwoven

85%

10%

Filament spinning/texturing

Key figures

1 as % of sales

4%

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 48

Sales

Q3 2015

Sales

Q3 2015

BCF carpet

yarn /

polymer

processing

5%

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

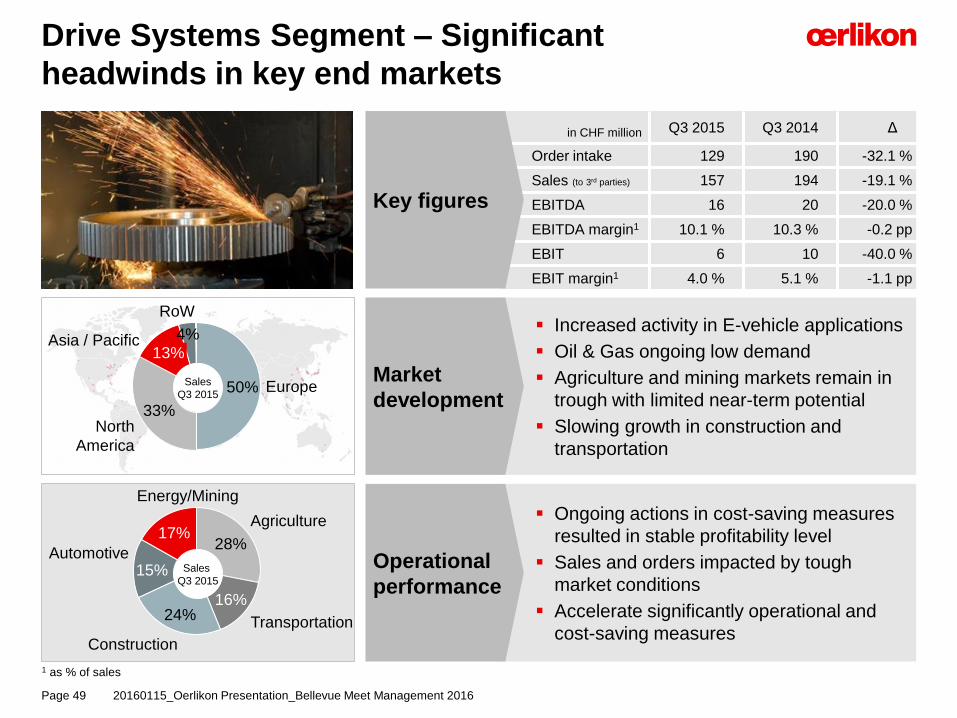

in CHF million Q3 2015 Q3 2014 Δ

Order intake 129 190 -32.1 %

Sales (to 3rd parties) 157 194 -19.1 %

EBITDA 16 20 -20.0 %

EBITDA margin1 10.1 % 10.3 % -0.2 pp

EBIT 6 10 -40.0 %

EBIT margin1 4.0 % 5.1 % -1.1 pp

Drive Systems Segment – Significant

headwinds in key end markets

RoW

Asia / Pacific13%

North

America

33%

Europe50%

Energy/Mining

17%

Automotive15%

Construction

24% Transportation

16%

Agriculture

28%

1 as % of sales

Ongoing actions in cost-saving measures

resulted in stable profitability level

Sales and orders impacted by tough

market conditions

Accelerate significantly operational and

cost-saving measures

Operational

performance

Increased activity in E-vehicle applications

Oil & Gas ongoing low demand

Agriculture and mining markets remain in

trough with limited near-term potential

Slowing growth in construction and

transportation

Market

development

Key figures

4%

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 49

Sales

Q3 2015

Sales

Q3 2015

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Core competencies

Under the brand

Oerlikon Fairfield, the

Segment is a leading

manufacturer of

engineered drive

products for OEMs

It is successfully

applying them in off-

highway equipment

as planetary drives

Increasing range of applications –

planetary drives for spray tractors

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 50

Increase range of applications

In the field of spray tractors, OEMs are constantly evolving

these machines to make them more productive

Oerlikon Fairfield developed a new planetary drive with a

hydraulic or electric motor for self-propelled spray tractors

and compact construction vehicles

The new series offers a patented internal service brake

that improves safety and performance by eliminating the

potential for chemical corrosion present with external

braking mechanisms

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Increasing range of applications –

bevel gear set for commercial vehicles

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 51

Core competencies

Under the brand Oerlikon Graziano,

the Segment is a leading

manufacturer of bevel gear sets

Bevel gear sets are one of the

most demanding gear

configurations

Oerlikon Graziano is successfully

applying them in agriculture and

automotive applications as

differentials and power transfer

units

Increase range of applications

Oerlikon Graziano successfully expanded the

core technology into new markets and

applications, such as differentials for commercial

vehicles, all-terrain vehicles (ATV) and electric

cars

Oerlikon Graziano is also introducing

electronically controlled limited slip differentials

to the performance car market

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

2015 top-line targets aligned to new market

realities while profitability target confirmed

Order intake

EBITDA

Sales

2015E2014

At prior-year level

3 215

2015 Group Guidance

Oerlikon expects, compared to

2014 reported figures (continuing

operations) and based on constant

exchange rates:

Order intake to grow by low single-

digit

Sales to be at prior-year level

EBITDA1 margin to be at prior-

year level

Based on January exchange

rates, a translation effect of

11-12 % is estimated

1 Including full absorption of all related one-time integration and accounting effects from Metco transaction

525

2014 2015E

At constant

exchange rates

2015E

3 028

2014

Low single-digit growth

At constant

exchange rates

Margin around

prior-year level 16.3%

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 52

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

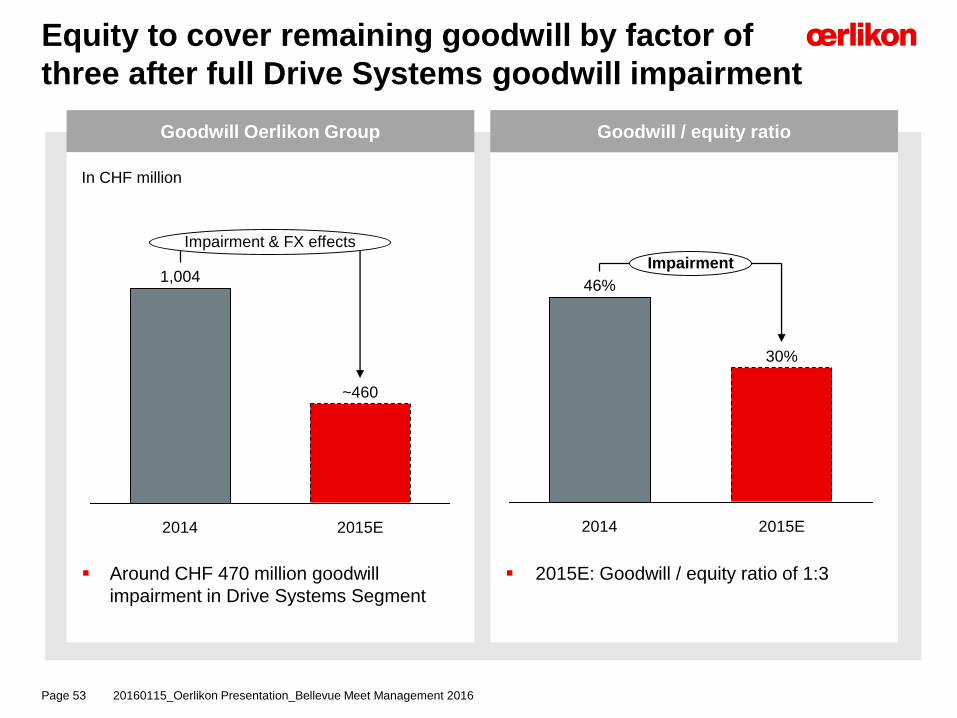

2015E: Goodwill / equity ratio of 1:3

Goodwill / equity ratioGoodwill Oerlikon Group

In CHF million

Around CHF 470 million goodwill

impairment in Drive Systems Segment

Equity to cover remaining goodwill by factor of

three after full Drive Systems goodwill impairment

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 53

2014

1,004

2015E

Impairment & FX effects

~460

2014

Impairment

2015E

46%

30%

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Sales 3rd 2015 (e) COGS 2015 (e)

Balanced FX profile across the Group –

Limited Swiss franc exposure

4%11%

20%

11%

54%

RMB OtherEUR USDCHF

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 54

No major currency mismatch – natural hedge in place

Limited transaction risk

Translation effects from reporting currency CHF

25%

13%

48%

12%

2%

≈

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

R&D and CapEx on Segment level1

CapEx / Depr. & Amort. H1 2015

CapEx H1 2015

Depreciation & Amortization H1 2015

R&D expenses H1 2015

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 55

Vacuum

(7 %)

19%

9%Drive Systems

(2 %)

Manmade Fibers (3 %)

55%

17%

Surface

Solutions (6 %)

9%

Drive Systems22%

Manmade Fibers

61%

Vacuum

8%

Surface

Solutions

CHF

65m

CHF

91m

Drive Systems

58% Surface

Solutions13%

Vacuum

8%

21%

Manmade Fibers

CHF

71m

0.75

VacuumManmade

Fibers

Surface

Solutions

1.01

Drive

Systems

1.13

0.86

Group (0.95)

1 H1 2015 continuing operations; 2 Amortization adjusted for amortization of acquired intangible (CHF 14.6 million)

(% of Segment sales)

2

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Asset allocation and employees

on Segment level

Employees (FTE) by Region H1 2015

Net operating Assets H1 2015

Employees (FTE) by Segment H1 2015

Operating assets H1 2015

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 56

Vacuum

7%

Drive Systems 30%

Manmade Fibers

16%

Surface

Solutions47%

Vacuum

7%

Drive Systems 34%

Manmade Fibers

7%

Surface

Solutions52%

CHF

3 439m

Corporate

1%

Vacuum

11%

Drive Systems 33%

Manmade Fibers

16%

Surface

Solutions39%

CHF

2 561m

RoW

2%

33%Asia / Pacific

North America

13%

Europe52%15 62915 629

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

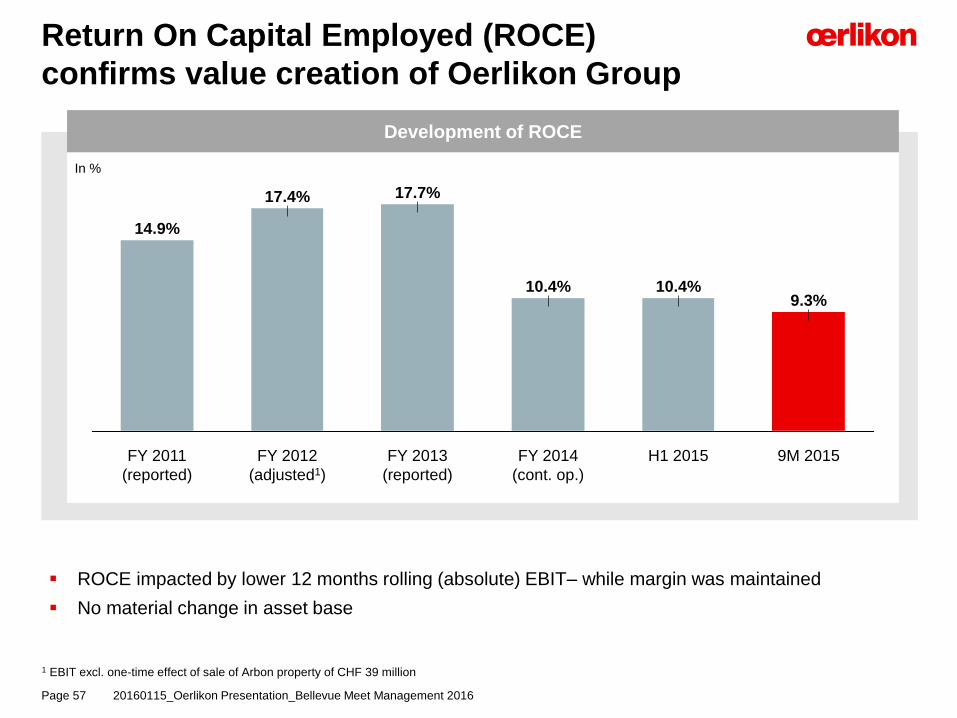

In %

Development of ROCE

Return On Capital Employed (ROCE)

confirms value creation of Oerlikon Group

FY 2012

(adjusted1)

17.7%

FY 2011

(reported)

14.9%

FY 2013

(reported)

H1 2015

10.4%

FY 2014

(cont. op.)

10.4%

17.4%

9.3%

9M 2015

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 57

ROCE impacted by lower 12 months rolling (absolute) EBIT– while margin was maintained

No material change in asset base

1 EBIT excl. one-time effect of sale of Arbon property of CHF 39 million

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

as of December 31, 2015, indexed; 100 percent = closing price per December 30, 2014

Oerlikon share price development

as of December 31, 2015

Oerlikon shareholder structure1

Oerlikon shares

57.0%Free float

(incl. 0.1 %

treasury shares)

43.0%

Renova Group

1 Based on 339 758 576 shares outstanding and latest notification by Renova (as of December 15, 2015 of 146 222 889 shares)

Listed on Swiss Exchange (SIX) since 1973

Securities symbol: OERL

Securities number 81 682

ISIN: CH0000816824

No. of shares outstanding: 339 758 576 shares

(as of Sept. 30, 2015)

Re-entry to Swiss SMIM on April 17, 2012

Addition to STOXX Europe 600 as of June 18, 2012

Oerlikon shares

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 58

60,0

80,0

100,0

120,0

140,0Oerlikon SMI SMIM STOXX Europe 600 STOXX Europe 600 Industrial

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Coverage –

9 Buy/Accumulate & 5 Hold/Neutral

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 59

Broker Analyst Recommendation Date of last

update

Target

price

AlphaValue Pierre-Yves Gauthier Buy 10.12.2015 12.00

Baader Helvea Reto Amstalden Buy 02.12.2015 12.50

Bank am Bellevue Alessandro Foletti Hold 04.12.2015 9.80

Berenberg Bank Sebastian Künne Hold 07.12.2015 9.20

Credit Suisse Patrick Laager Outperform 04.12.2015 11.00

Jefferies Graham Phillips Buy 28.10.2015 12.00

Kepler Cheuvreux Hans-Joachim Heimbürger Hold 01.12.2015 9.00

Mainfirst Michael Inauen Outperform 01.12.2015 11.50

Mirabaud Securities LLP Thomas Baumann Buy 01.12.2015 12.25

RBC Capital Markets Wasi Rizvi Outperform 01.12.2015 11.50

Société Générale Christophe Quarante Hold 10.12.2015 10.00

UBS André Rudolf von Rohr Buy 18.12.2015 10.50

Vontobel Michael Foeth Buy 03.12.2015 12.00

Zürcher Kantonalbank Armin Rechberger Marketweight 02.12.2015 -

Consensus 9 positive

5 neutral

11.02

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

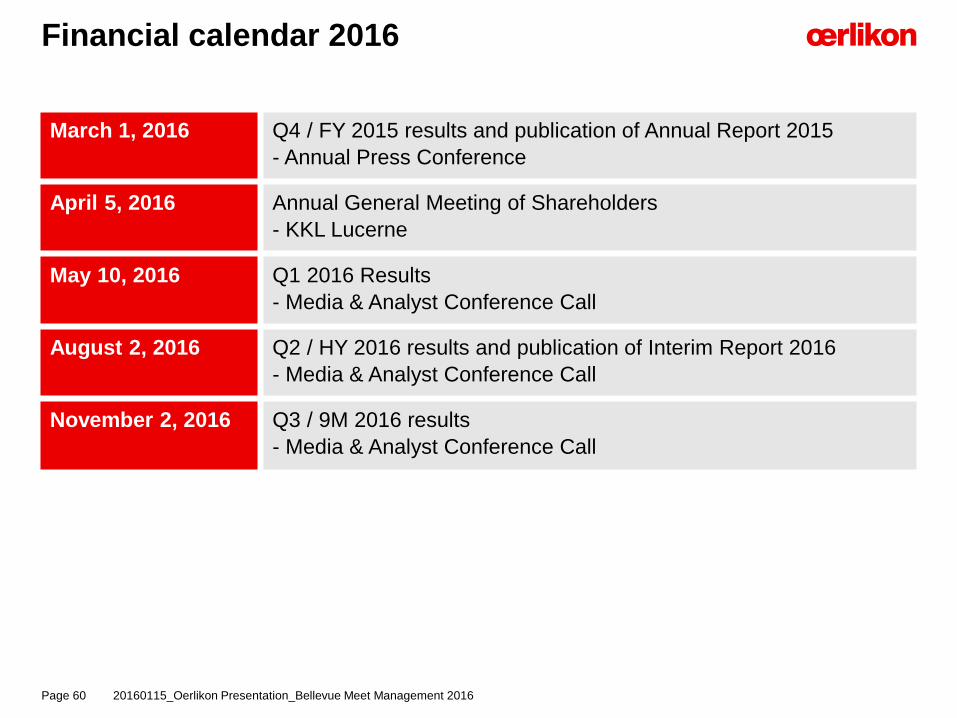

Financial calendar 2016

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 60

March 1, 2016 Q4 / FY 2015 results and publication of Annual Report 2015

- Annual Press Conference

April 5, 2016 Annual General Meeting of Shareholders

- KKL Lucerne

May 10, 2016 Q1 2016 Results

- Media & Analyst Conference Call

August 2, 2016 Q2 / HY 2016 results and publication of Interim Report 2016

- Media & Analyst Conference Call

November 2, 2016 Q3 / 9M 2016 results

- Media & Analyst Conference Call

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

Investor Relations contact

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 61

OC Oerlikon Management AG, Pfäffikon

Churerstrasse 120

CH – 8808 Pfäffikon SZ

Switzerland

Andreas Schwarzwälder

Head of Investor Relations

Phone: +41-58-360-9622

Mobile: +41-79-810-8211

E-mail: [email protected]

It's not allowed to change the master It's not allowed to change the master

8,6

4,7

8,0

9,1

6,6

8,3

0,9

0,5

Version September 2012

OC Oerlikon Corporation AG, Pfäffikon, (together with its affiliates hereinafter referred to as “Oerlikon”) hasmade great efforts to include accurate and up-to-date information in this document. However, Oerlikonmakes no representation or warranties, expressed or implied, as to the truth, accuracy or completeness ofthe information provided in this document, Neither Oerlikon nor any of its directors, officers, employees oradvisors, nor any other person connected or otherwise associated with Oerlikon, shall have any liabilitywhatsoever for loss howsoever arising, directly or indirectly, from any use of this document.

The contents of this document, including all statements made therein, is based on estimates, assumptionsand other information currently available to the management of Oerlikon. This document contains certainstatements related to the future business and financial performance or future events involving Oerlikonthat may constitute forward-looking statements. The forward-looking statements contained herein could besubstantially impacted by risks, influences and other factors, many of which are not foreseeable at presentand/or are beyond Oerlikon’s control, so that the actual results, including Oerlikon’s financial results andoperational results, may vary materially from and differ than those, expressly or implicitly, provided in theforward-looking statements, be they anticipated, expected or projected. Oerlikon does not give anyassurance, representation or warranty, expressed or implied, that such forward-looking statements will berealized. Oerlikon is under no obligation to, and explicitly disclaims any obligation to, update or otherwisereview its forward-looking statements, whether as a result of new information, future events or otherwise.

This document, including any and all information contained therein, is not intended as, and may not beconstrued as, an offer or solicitation by Oerlikon for the purchase or disposal of, trading or any transactionin any Oerlikon securities. Investors must not rely on this information for investment decisions and aresolely responsible for forming their own investment decisions.

Disclaimer

20160115_Oerlikon Presentation_Bellevue Meet Management 2016Page 62