creative destruction of business

TRANSCRIPT

January’17@_mrogers

TheCreativeDestructionofBusinessThedeathofGoliath

Thedistributednatureof… everything

WeareintheinstallationphaseofanewtechnologicalrevolutionAsaresult…

‘Industry4.0’/‘TheSecondMachineAge’– callitwhatyouwill;thenatureofwork,thefirm,theeconomyisbeingreinvented.

2Source: Carlota Perez

PerezTechnologicalSurgeCycle

GestationB

BigBangB

CollapseRecovery BigBangC

Time

1.Irruption

2.Frenzy

TurningPoint

3.Synergy

4.Maturity

1. CreativeDestruction

2. NewParadigmvs.OldParadigm

3. FinancialCapitalLeads

4. BubbleCreation

1. CreativeConstruction

2. WidespreadApplicationofNewParadigm

3. ProductionCapitalLeads

Installation Deployment

20– 30years 20– 30yearsMaturityA

GestationPeriodC

2007wasnotourturningpoint.Wearestillintheinstallation

phase

0

10

20

30

40

50

60

70

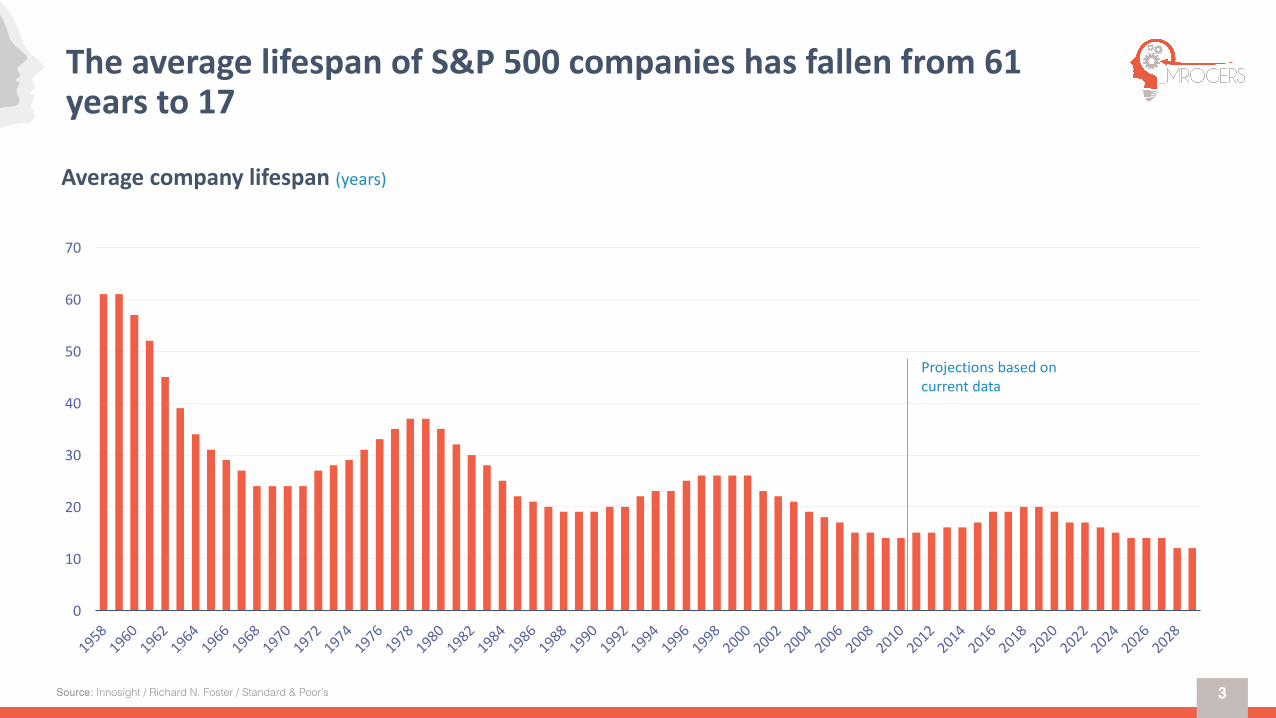

Averagecompanylifespan(years)

Projectionsbasedoncurrentdata

TheaveragelifespanofS&P500companieshasfallenfrom61yearsto17

3Source: Innosight / Richard N. Foster / Standard & Poor’s

Newtechnologycanbeadoptedfasterthaneveracrosstheglobe

4Source:singulairty.com

YearsuntilusedbyonequarterofAmericanpopulation

1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

10

0

20

30

40

50 Electricity1873

46

Telephone1876

35

Radio1897

31

Television1926

26

PC1975

16MobilePhone1983

13

TheWeb1983

7iPod2001

4

Facebook2004

3

iPhone2007

2.5

Arangeofinterconnectedforcesareloweringthedrawbridge,allowingnewentrantstocrossthemoatthatonceprotectedlargeempires

Thepriceofbeingbig

Innovationisnolongertopdown

Computingismorepowerfulandcheaperthanever

Tomorrowcomessooner

TherenaissanceofITinfrastructure

Theriseofcloudcomputing

MachineLearning– itworks

Everythingisconnected

Thecultofentrepreneurism

OpenSource

Theabundanceofcapital

Riseofthefreelanceeconomy

Thenatureofwork

Blockchain /Web3.0

5

Technology

EconomicsCulture

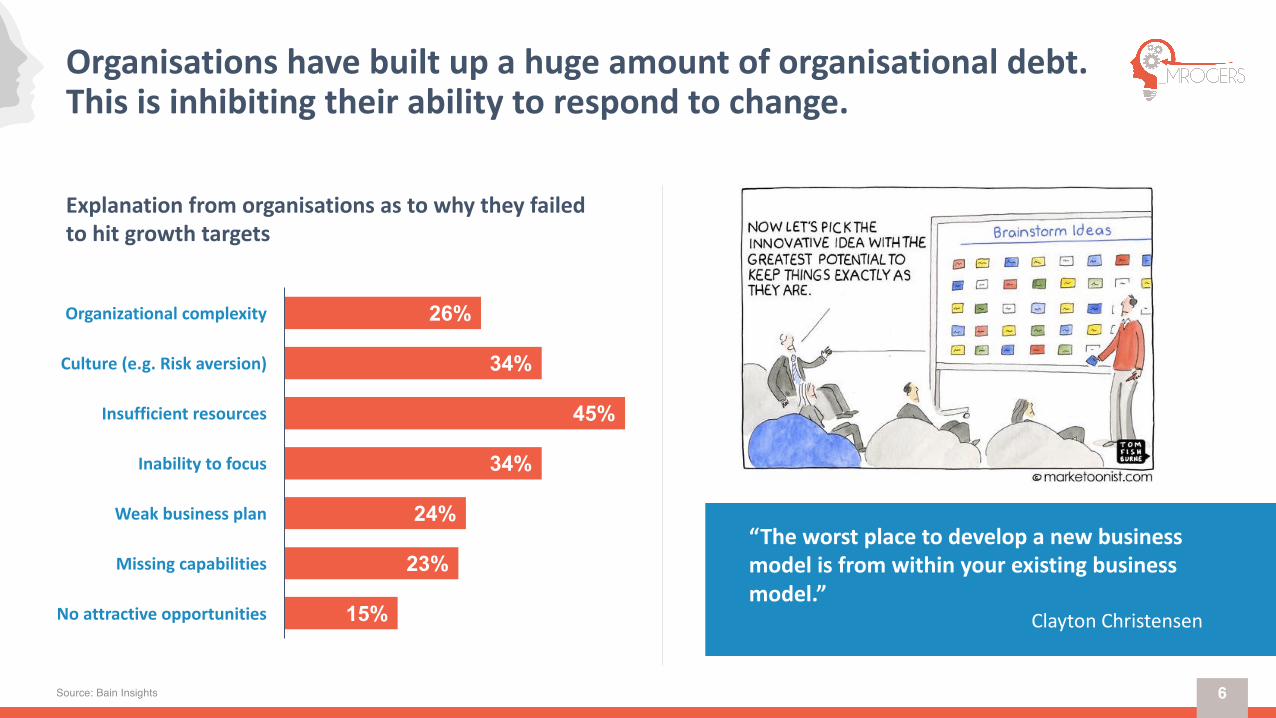

Organisations havebuiltupahugeamountoforganisational debt.Thisisinhibitingtheirabilitytorespondtochange.

6

15%

23%

24%

34%

45%

34%

26%

No attractive opportunities

Missing capabilities

Weak business plan

Inability to focus

Insufficient resources

Culture (e.g. Risk aversion)

Organizational complexity

Source: Bain Insights

“Theworstplacetodevelopanewbusinessmodelisfromwithinyourexistingbusinessmodel.”

ClaytonChristensen

Explanationfromorganisations astowhytheyfailedtohitgrowthtargets

Redesigningthefirm- fromhumanpyramidtodistributednetwork

7

GitHubhasroughly600employeesdistributedthroughouttheglobe,with20%ofitsworkforceoutsidetheUS.Thenumberofworkerswhotelecommunicateacrossindustriesdoubledbetween2005and2014,upto3.6millionworkers.

Redesigningthefirm- fromvaluechainstoecosystems

8

Services

FirmInfrastructure

HumanResourceManagement

Technology

Procurement

InboundLogistics Operations Outbound

LogisticsMarketing&

Sales

PrimaryActivities

Supp

ort

Activ

ities

ECOMMERCEECOSYSTEM

Merchandi-sing

Marketing

Multi-Channel

IntegrationPerformance

CustomerService

EmergingMarkets

Infrastruc-ture

Financial

Infrastructure

Merchandising

Marketing

CustomerService

Multi-Channel

Integrations

Financial

Performance

EmergingMarkets

Platform

Database

Fulfilment Hosting

CMSPresen-tationLayer

Graphics

Personali-zation

Catalogmanagem

ent

Imaging&Modeling

RichMedia

Reviews

AfiliateMarke-ting

CSE

PPCSearchMarke-ting

Retarge-ting

SEO

SocialMedia

CallCenters

Satisfaction

ContactManage-ment

LiveChat

Returns

StoreLocator

LocalSearch

Promotions

In-StoreCouponsShopping

Cart

AlternatePayments

Authenti-cation

Security

OrderManage-ment

PayProcessing

Usability

ContentDelivery

Testing

Analytics

SidePerforman-

ce

DataMining

Widgets

MobileCommerce

SmartKiosk

SocialCommerce

In2001,Nokiadescribedmanufacturingasacorecompetency.75%ofNokiaphonesweremadein8Nokiafactories.In2016,theiPhonehas189supplierswith789locations,noneownedbyApple.

Thenotionofcompetitionchangesdramatically.Nolongeraboutcreatingmoatsbutbuildingbridges.

Nosiloissafe.Theenterprisewillbedelivered‘asaservice’

9Source: CB Insights

Theessenceofacompanyisitsproductandbrand

Customer

Marketing&Sales

Product&Brand

Analytics CustomerService

IT Ops

Finance DataManagement Engineering

HR

10

Traditionalmanagementdepartmentscanbedeliveredbyarangeofcompanies,requiringasmallerdedicatedteam.Allowingforgreaterfocus.

Source: CB Insights

ForcesallowingDavidstotakeonGoliaths

Deflationarypressureoflaunchingastart-upisunrivalled

$5,000,000

$500,000$50,000 $5,000

Thecostoflaunchingofstart-up

2000 2005 2009 2011

12Source: UpFront Ventures

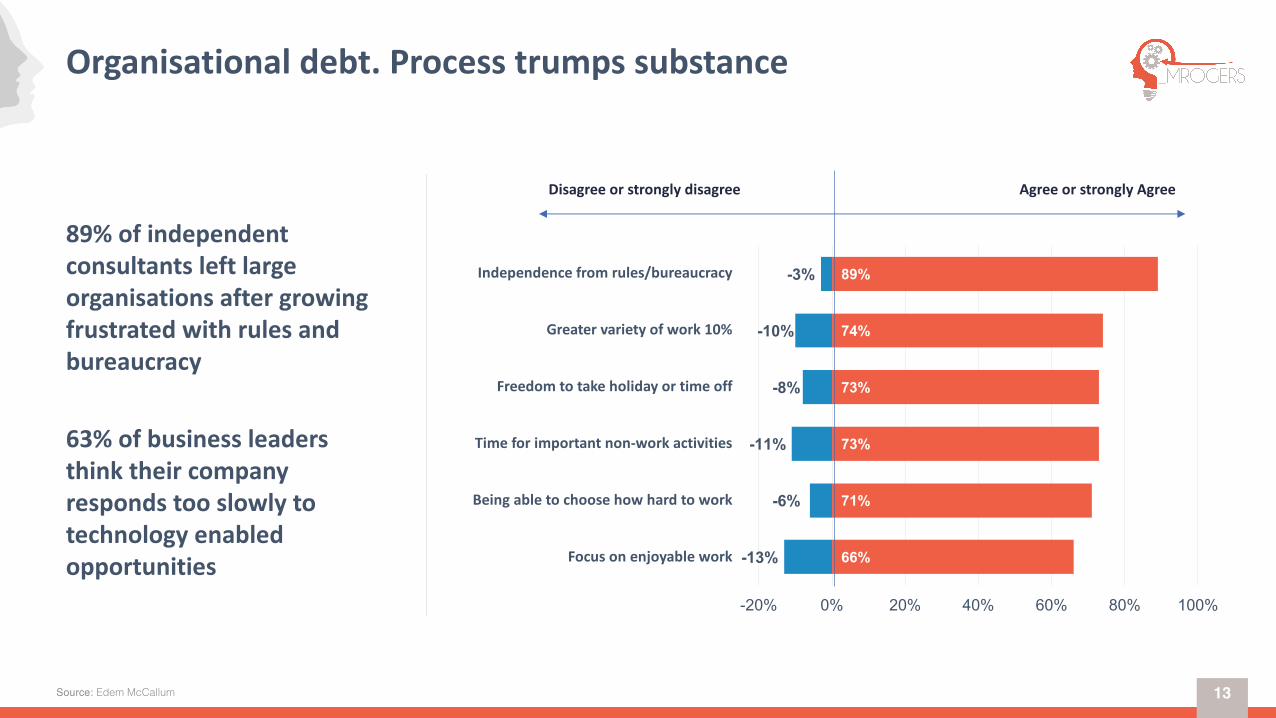

Organisationaldebt.Processtrumpssubstance

13

89%ofindependentconsultantsleftlargeorganisationsaftergrowingfrustratedwithrulesandbureaucracy

63%ofbusinessleadersthinktheircompanyrespondstooslowlytotechnologyenabledopportunities

Source: Edem McCallum

-13%

-6%

-11%

-8%

-10%

-3%

66%

71%

73%

73%

74%

89%

-20% 0% 20% 40% 60% 80% 100%

Disagreeorstronglydisagree AgreeorstronglyAgree

Focusonenjoyablework

Beingabletochoosehowhardtowork

Timeforimportantnon-workactivities

Freedomtotakeholidayortimeoff

Greatervarietyofwork10%

Independencefromrules/bureaucracy

Computingischeap.Softwareiseatingtheworld.Theworldisprogrammable

14

“Sixdecadesintothecomputerrevolution,fourdecadessincetheinventionofthemicroprocessor,andtwodecadesintotheriseofthemodernInternet,allofthetechnologyrequiredtotransformindustriesthroughsoftwarefinallyworksandcanbewidelydeliveredatglobalscale.”

-- Andreesen

Jan’80 Jan’84 Jan’88 Jan’92 Jan’96 Jan’00 Jan’04 Jan’08 Jan’12 Jan’14

60.000

50.000

40.000

30.000

20.000

10.000

0

ReleaseofIBMPC

ReleaseoffirstMacintosh

IBMannounceThinkPadtablets

1billioninstalledPCsWorldwid

Source: Bloomberg

Jan’80 Dec’83 Nov’87 Oct’91 Sep’95 Aug’99 Jul’03 Jun’07 May’11 Dec’14

1.000

0

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

ThePriceof PCsPersonalcomputersarenow99.9%cheapertodaythanin1980

Personalcomputers&peripheralequipmentpriceindex Computerssoftwarepriceindex

ThePriceofSoftwareComputerssoftwarearenow0.7%ofitspricein1980

RiseofOpenSource

15Source: Black Duck Software

78%ofcompaniesrunonopensource.Lessthan3%don’tuseOSSinanyway

67%ofcompaniesactivelyencouragedeveloperstoengageinandcontributetoopensourceprojects

90%ofcompaniesthatuseOpenSourceSoftwaresayitimprovesefficiency,

interoperabilityandabilitytoinnovate

Riseofcloudcomputing

8 12 16 21 26 32 37 42 46 50 53 55

2538

61

83

106

126142

153161 166 170 173

0

20

40

60

80

100

120

140

160

180

200

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Publiccloudspendingforecasts($bn)

SaaSandPaaS PubliccloudIaaShardwareandinfrastructuresoftware

16Source: Statista 2016

• Gartner,January2016:Theworldwidepubliccloudservicesmarketisprojectedtogrow16.5%in2016to$204bn.Thehighestgrowthcomingfrominfrastructureservices(infrastructureasaservice).Projectedtogrow38.4%.

• MorganStanleypredictscloudproductswillbe30%ofMicrosoft’srevenueby2018.

• In2015AWS(AmazonWebServices)generated$7.88bninrevenue,up69%fromthepreviousyear.

Robotsareuseful

17

1000

15000

30000

45000

0

10000

20000

30000

40000

50000

2013 2014 2015 2016

Source: Amazon

Amazon’sRobotBoomThenumberofrobotsdeployedinAmazonfacilitieshasrisensharply

The20thcenturyworked.Theindustrialrevolutionworked.Nowexcesscapital– inAugust’16thevalueofnegative-yieldingbondshit$13.4tn.In2016theS&Pdistributedmorethan$1tnbacktoshareholders(20xmoremoneycomingoutofbigcompaniesthangoingintostart-ups)

18

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1820

1824

1828

1832

1836

1840

1844

1848

1852

1856

1860

1864

1868

1872

1876

1880

1884

1888

1892

1896

1900

1904

1908

1912

1916

1920

1924

1928

1932

1936

1940

1944

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

WorldGDPperperson

Source: U.S. Bureau of Economic Analysis

CorporateVCs– thenewR&D

1.7 2.1 2.3 2.2 1.72.7 2.6 2.7

3.85.1

3.54.5 4.9

7.4

11.3

5.5

8

4.7

160190 191

219 212227

253268

283303

340 334 324350

377

313335

298

0

50

100

150

200

250

300

350

400

0

2

4

6

8

10

12

QuarterlyGlobalCVCFinancingTrend

Investment($B) Deals

8598 95

112 104 111124 125

147 140157 164 171 166

191177

188176

0

50

100

150

200

250

ActiveCorporateVCs

UniqueCVCInvestors

19

Globally,53newCVCunitsmadetheirfirstinvestmentin2016Corporatesarenowlookingtostart-upstointroduceinnovationintotheorganisation

Source: CB Insights

Whatisdigitaltransformation?

20

Competitivelinesredrawn

21

Disruptionrequiresanecosystemofparticipantstocometogether.Thisisevidentacrossindustries,particularlyinfinancialservicesandautomotive.

Thenotionofcompetitionchangesdramatically.Nolongeraboutcreatingmoatsbutbuildingbridges.

Source: CB Insights & Bloomberg

Start-upswithsuperiorproprietarytechnologyare‘unbundling’everyindustry,focusingonaniche.Atthesametimeaseverycompanybecomesa‘techcompany’platformsareleadingtogreatersectorconvergence

Uber

TataOwnerofJaguarLand

Rover

Toyota

Volvo FiatChrysler

Microsoft Google

Ford

SAIPS Chariot

CivilMaps

NirenbergNeuro-science

VelodyneLidar

Lyft

Didi UberChina

CruiseAuto-mation

Sidecar

GM

Apple

VW

BMW

NokiaHERE

Daimier

Baidu

Mobileye

Intel

DriveNow

Scoop

Car2Go

Ride-Scout

MyTaxy

Hailo

Black-lane

AthionCarLeaseInterna-tional

Matter-net

Gett DFKI

Renault-Nissan

Sylpheo

Investment Partnership FailedTalks PersonnelMove

Themergingworldoftechnologyandcars

Themovefrompipelinetoplatforminvolvesthreekeyshifts:1. Fromresourcecontroltoresourceorchestration2. Frominternaloptimizationtoexternalinteraction3. Fromafocusoncustomervaluetoafocusonecosystemvalue

- PlatformLabs

Nature ofbusinessScaleisnolongerdependentonprocesseswithinthebusiness,it'sdrivenbynetworkprocesses.Scale,byscalingtheseinteractions.Valuechaintoecosystemisnolongerlinearbutnetworked.

22Source: Ocean Tomo, LLC

17%32%

68% 80% 84%83%

68%

32% 20% 16%

0%

25%

50%

75%

100%

1975 1985 1995 2005 2015

ComponentsofS&P500MarketValue

IntangibleAssets TangibleAssets

Land Capital

Labour

Data Talent

IP

Thevalueoftalent

23

239000177000

53000 47000 9199

Numberofemployeesat$200bmarketcap

GE Verizon Google Apple Facebook

Valueperemployeeat£200bmarketcapValueperemployeewhen

FacebookacquiredInstagramfor$1b

$77m$837k $1.1m $3.71m $4.29m $21.7m

Source: Bloomberg

Howtonavigatedigitaltransformation?

24

OperatingModels.Theartofexecution.Apoorlyexecutedstrategyisworthless.

Culture.TheinvisibleadvantageNocompanyhasaculture.Everycompanyisaculture– Peter Thiel

Data.Thefuelofbusiness83%ofcompaniesagreethatdataistheirmoststrategicasset.Yetcompaniesestimatetheyareanalysing12%oftheirdata.

OperatingModels.FromCathedraltoBazaar

Organisatons becomeecosystemsnotvaluechains.Platformsandecosystemswillnotreachasteadystate,butconstantlymorph.“Changeistheonlyconstantinlife.“ - Heraclitus

In2001,Nokiadescribedmanufacturingasacorecompetency.75%ofNokiaphonesweremadein8Nokiafactories.In2016,TheiPhonehas189supplierswith789locations,noneownedbyApple.

Metcalfe'slaw:thevalueofanetworkasawholeisproportionaltothesquareofthenumberofparticipants.Thisworldrequiresamodular,plug-and-playinfrastructure,andonwhichthefocusisonintegrationandinteroperability.

Gartner’s2016CIOreportarticulatesthat“aplatformprovidesthebusinesswithafoundationwhereresourcescancometogether– sometimesquicklyandtemporarily,sometimesinarelativelyfixedway– tocreatevalue.

Youdon’tchangethingsbyfightingtheexistingmodel—youchangethingsbymakingtheexistingmodelobsolete.

25

‘Coopetition’andsymbioticrelationships- thechallengebecomeshowtoaligneveryone’sefforts,evenwhencompeting.

Culture.Controlwhatyoumustnotwhatyoucan

26Source: Patrick Cheesman

Astudyfrom Gensler foundthatthemostimportantfactorindeterminingwhetheracompanywasinnovativewastrust.“Innovativecompaniesexercisetrustwithemployees”.

GillianTett,inherbook‘TheSiloEffect’,looksathoworganisations mustcreateasocialstructurethatinfluencesthewaypeoplethink,organise andintegrate.Thenorms,values,symbols,measuresandprocesseswithinafirmallinhibitorsupportacultureofinnovation.

Culturemustnotonlynotresistchangebutencourageit.Employeesseehowtheproblemischangingandtheopportunitiespresented,andfeelempoweredtoactratherthanprotecttheirsiloorprofitandlossstatementswithintheorganisation.

Everyvaluestatement,process,structure,rewardsystem,metric,symbol,etc.manifestthemselvesintoacompany’sculture.Cultureisauniquecomplexsystem.Beawareofhowthedecisionsandactionsyoutakewillimpactit.

Artefacts

Behaviours

Norms

Beliefs Assumptions

Values

Hardtosee

Easytosee

Data.Thefuelofbusiness

27

80%ofCEOswereworriedabouttheirdataquality.

“Smartdatastructuresanddumbcodeworksalotbetterthantheotherwayaround.”

Datawilldriveinvestmentdecisions,frontlinedecisionmaking,andcreateasingleviewofthecustomeracrosstheorganisation.• Storage:Datawarehousetodatalakes• Insight:Datascientistsuselargedatasetsandmachinelearningtogiveamore

forwardlookingview• Decisions:Manyleadersandmanagersstillfailtodrivedecisionsbasedondata.

Companiesmustunderstandwhatdatatheyneedandhowtogovernit,introducinganenterprisewideMDM(masterdatamodel)willcreateefficientfeedbackloopsto‘learnfast’

Entrepreneursstartwithapassiontosolveaproblem,butastheyscale,theconversationchanges.Nolongeraretheyusingpassivedatatoobservetheworld,butactivedatatoevaluatetheirproductsandperformance.Then,astheyscaleandestablishthemselvesasanincumbent,theconversationturnstoefficiency,costs,etc.Firmslosewhatmadethemgreat;theylosethatconnectiontothevaluetheyare

creating.

Source: Patrick Cheesman

“Dataisthenewoil.It’svaluable,butifunrefineditcannotreallybeused.Ithastobechangedtocreateavaluableentity thatdrivesprofitableactivity;so,mustdatabebrokendownandanalysedforittohavevalue.”

-- CliveHumby

Bigisclever

28

Today’seconomyfavoursbigcompanies.The

conventionalwisdomthatsmallcompaniesaremoresuitedtoinnovationisagrosssimplification.

Ecosystemsneedtobemanagedbyacore

companythathasthescaleandskillstoprovide

technologicalleadership.

Americanfirmswith5,000ormorepeoplespend

morethantwiceasmuchperworkeronR&Dasthosewith100-500

employees.

Controllinganecosystemrequiresmorecapitalexpenditurethaninthepast

29

0

100

200

300

400

500

1990/2005 1995/2010 2000/2015

Annualrevenue($bn,realterms)

Wintel1990-2000 GAFA2005-2015

0510152025303540

Annualcapex($bn,real)

Microsoft Google Apple Facebook Amazon

GAFAhas10xthescaleFundamentalchangeinwhatitmeanstobealeadingtechcompany

ThatscalemeansmuchmoreinvestmentAnnualcapexhasincreased from$1bnto$34bnsince2000

Source: Bloomberg, a16z

Breakthroughinnovationrequiresgreaterappliedeffort

30Source: Bloomberg, a16z

SustainingMasteryOveraTechnology:

Buildingoffirmfoundations;improving,augmenting,applying

PioneeringEngineering&Science:Prospectingfornewpossibilities;exploring,evaluating,inventing

THEBRAKTHROUGH

NEWTECHNOLOGYCURVE

DeminshingReturns

EXISTINGTECHNOLOGY

CURVE

MEA

SURE

OFAD

VANCE

MEN

T

DisruptiveInnovation– ClaytonChristensenIn2004DARPAhelditsfirstgrandchallengefordriverlesscars.A150milecoursethroughCalifornia’sMojaveDesert.

Twovehiclesdidn’tmakeittothestartingarea,oneflippedoverinthestartingareaandthreehoursintotheraceonlyfourcarswerestilloperational.Thewinnercovered7.4miles.

In2010Googleannouncedithascompleted100,000ofmilesofautonomousdriving.

S-curvetheorydemonstratesprogressisgradualandthensudden.

Innovationiscompounded.Thisleadsto

exponentialgrowth.

ThedeathofGoliathThedistributednatureof…everything

Thebuildingblocksareinplacefor‘thesecondmachineage’/’industry4.0’

Areyouthemostevolveddinosaur?

CaughtintheRedQueen’sRace– runningfasterwithoutmakingprogress.

Thisisnotdoomandgloom.

Culturallywehavebecometooriskaverse.

Weplanandbuildthefuture.

Thefutureisnotrandom.Youcannotaffordtobepassive.