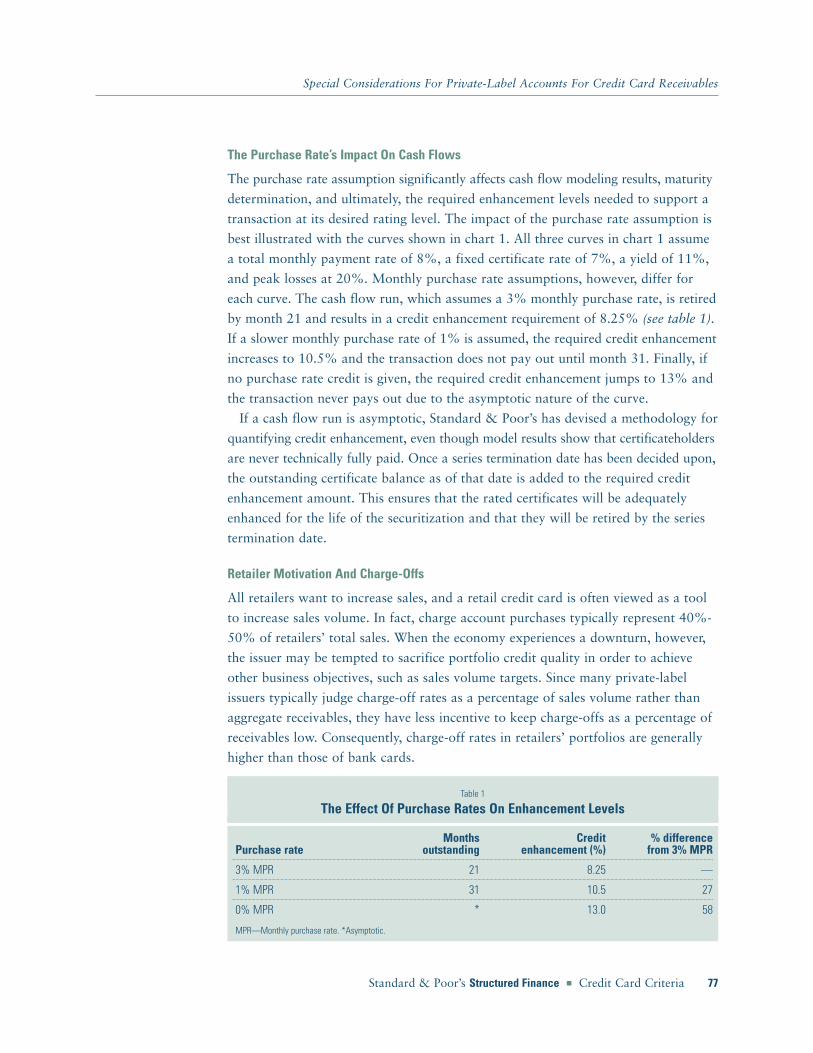

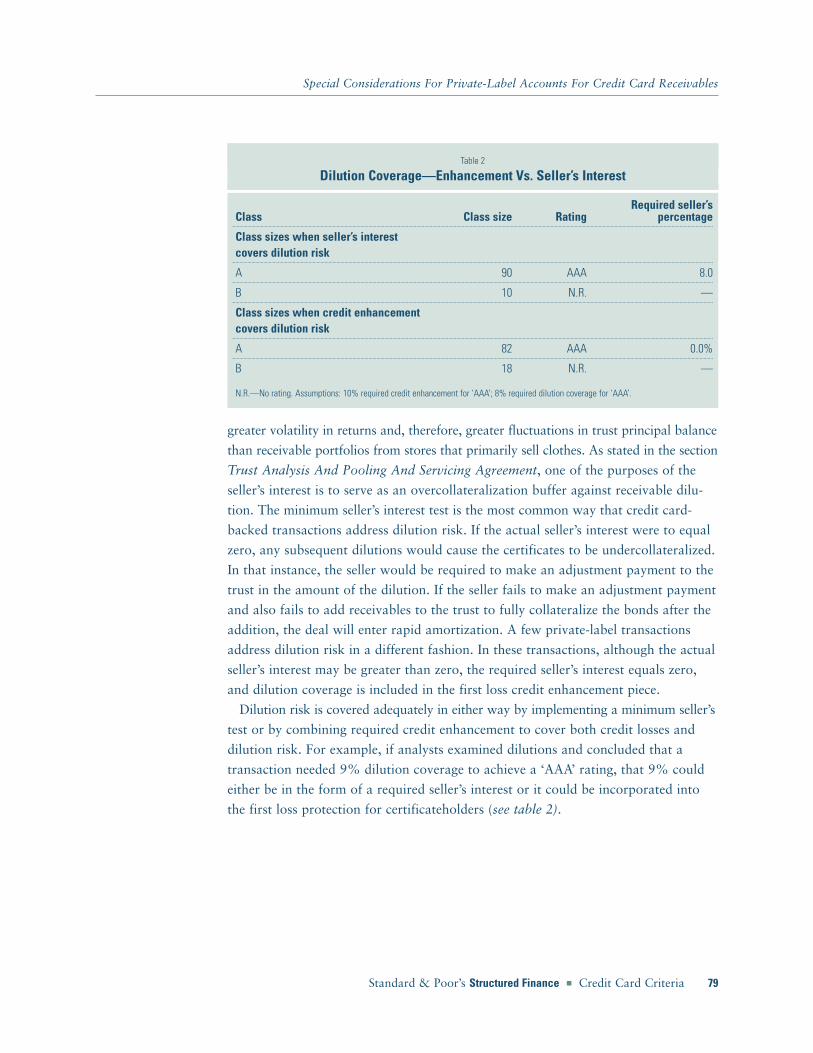

credit card criteria

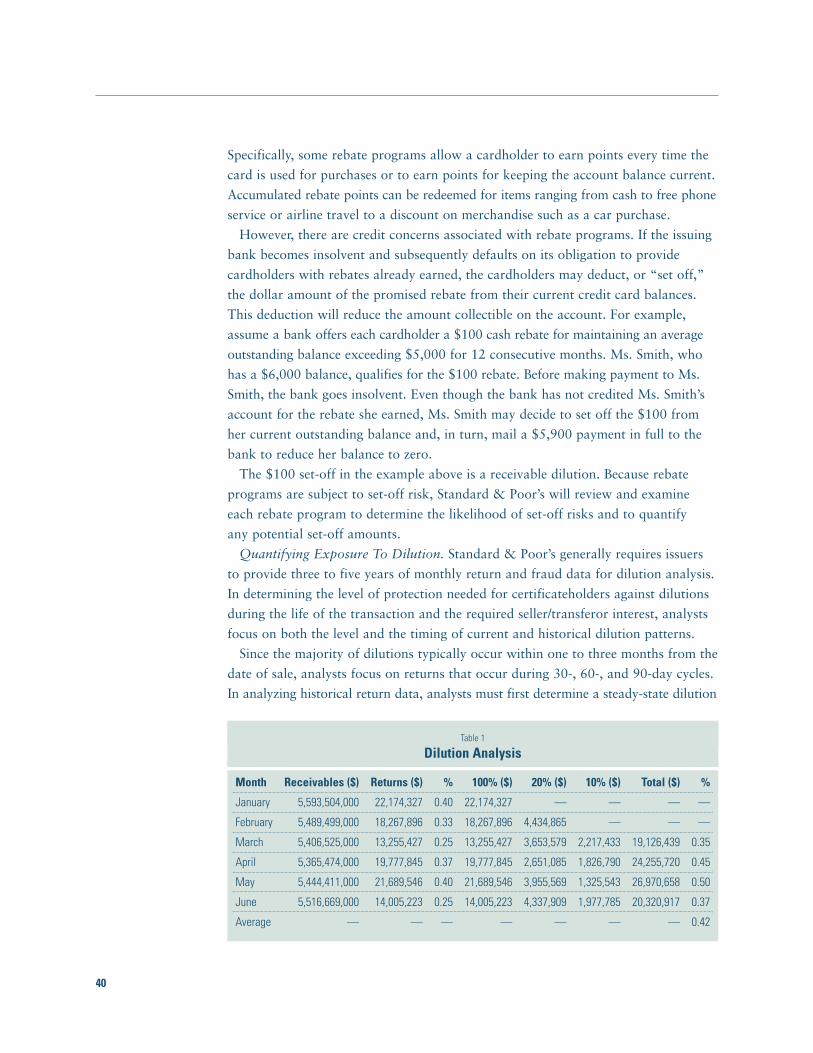

DESCRIPTION

TRANSCRIPT

Credit CardCriteria

Structured Finance

STANDARD & POOR’S RATINGS SERVICESPresident Leo C. O’Neill

Executive Vice PresidentsHendrik J. Kranenburg, Robert E. Maitner

Executive Managing DirectorsEdward Z. Emmer, Corporate RatingsClifford M. Griep, Financial Institutions RatingsVladimir Stadnyk, Public Finance RatingsRoy N. Taub, Insurance RatingsVickie A. Tillman, Structured Finance Ratings

Sanford B. Bragg, Managing Director, Managed Funds RatingsJoanne W. Rose, Senior Managing Director, General Counsel

RATINGS INFORMATION SERVICESManaging DirectorJay S. Kilberg

Vice PresidentsAndrew Cursio, Product ManagementRobert Frump, Production & Electronic DistributionPaul Stanwick, Editorial

David A. Collins, Director, Asia-PacificGuy Hewitt, Director, EuropeSusanne Barkan, Product ManagerSara Burris, Director, Design, Production, & ManufacturingJean-Claude Bouis, Editor, Franchise ProductsDonald Shoultz, Editor, Policy & Operations

EditorialJennifer O’Brien, Managing EditorNed Geeslin, Audrey Kennan, Suzanne Lorge, Donald Marleau (Tokyo),Cynthia Michelsen, Miriam Stickler, Lisa Tibbitts (Editorial Managers),Arlene Cullen (Melbourne) (Copy Editor)

Design & ProductionSandy Fong, Renee L. Mofrad, Beth Russo (Senior Managers),Elizabeth McCormack, Steve McLure (Senior Designers),Rosalia Bonanni, Theresa Moreno, Heidi Weinberg (Designers),Maura Gibbons (Junior Designer),John J. Hughes, Alicia E. Jones, Barry Ritz, Leonid Vilgorin (Managers),Dianne Henriques, Stephen Williams (Production Coordinators),Christopher Givler, Stan Kulp, Michelle McFarquhar (Senior Production Assistants)

Subscription InformationHong Kong, (852) 2533-3535London, (44) 171-826-3510Melbourne, (61) 3-9631-2000New York, (1) 212-208-8830Tokyo, (81) 3-3593-8700

Subscriber ServicesNew York (1) 212-208-1146

Web Sitewww.standardandpoors.com/ratings

Published by Standard & Poor’s, a Division of The McGraw-Hill Companies, Inc. Executive offices: 1221 Avenue of the Americas, New York, N.Y. 10020. Editorial offices: 25 Broadway, NewYork, N.Y. 10004. Copyright 1999 by The McGraw-Hill Companies, Inc. All rights reserved. Officers of The McGraw-Hill Companies, Inc.: Joseph L. Dionne, Chairman; Harold W. McGraw,III, President and Chief Executive Officer; Kenneth M. Vittor, Senior Vice President and General Counsel; Frank Penglase, Senior Vice President, Treasury Operations. Information has beenobtained by Standard & Poor’s from sources believed to be reliable. However, because of the possibility of human or mechanical error by our sources, Standard & Poor’s, or others,Standard & Poor’s does not guarantee the accuracy, adequacy, or completeness of any information and is not responsible for any errors or omissions or for the results obtained from theuse of such information.

1Standard & Poor’s Structured Finance � Credit Card Criteria

ContentsCollateral Analysis And The Rating ProcessFor Credit Card Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Review Of The Originator’s Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Legal, Collateral, And Structural Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Rating Committees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Rating Surveillance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Collateral Analysis. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Modeling Assumptions For Interchange . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

‘BBB’ Ratings Criteria For Credit Card CIAs . . . . . . . . . . . 19

Collateral Invested Amount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Market Evolution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Structural Credit Enhancement And Excess Spread . . . . . . . . . . . . . . . . . . . . 20

‘BBB’ Ratings Reflect Seller-Specific Considerations. . . . . . . . . . . . . . . . . . . . 23

Three ‘BBB’ Stress Test Scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Charge-offs/Loss-Spike Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Portfolio Yield . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Certificate Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Interest Rate Assumptions And Spikes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Payment Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

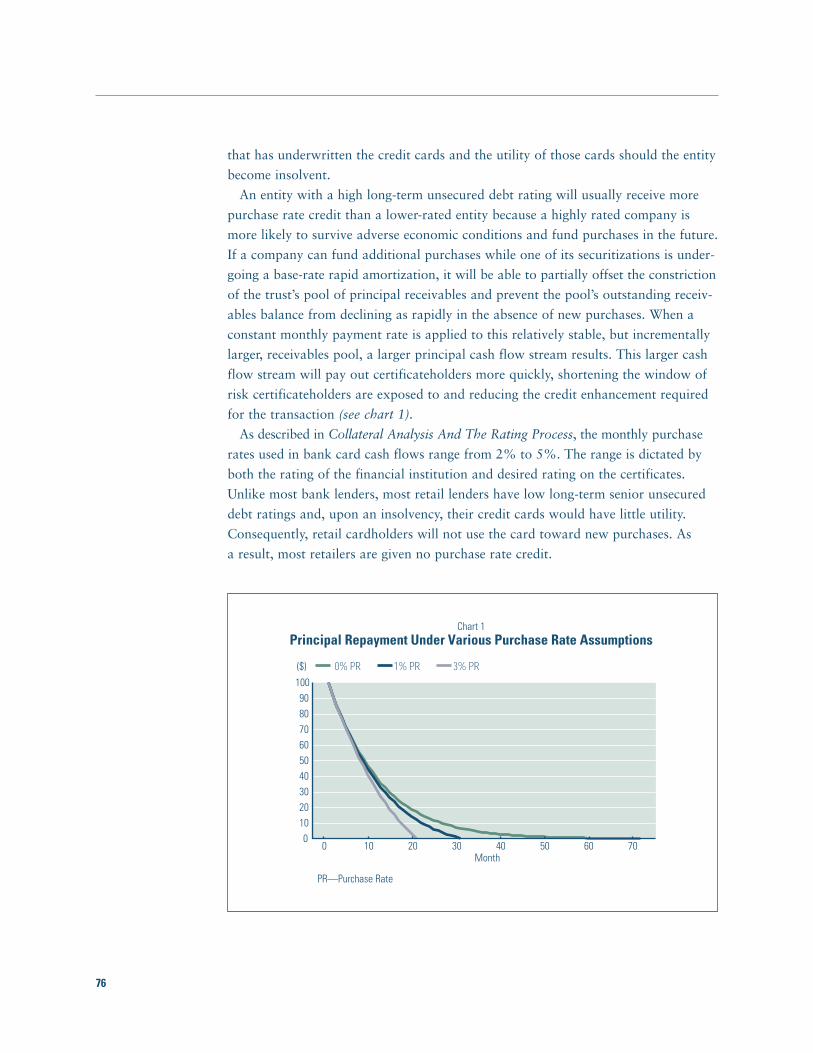

Purchase Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

CIA Owner Trust Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Legal Issues Related To Rating CIAs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Trust Analysis And Pooling And ServicingAgreement For Credit Card Receivables . . . . . . . . . . . . . . . . 35

Structural Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

The Trust . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Types Of Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2

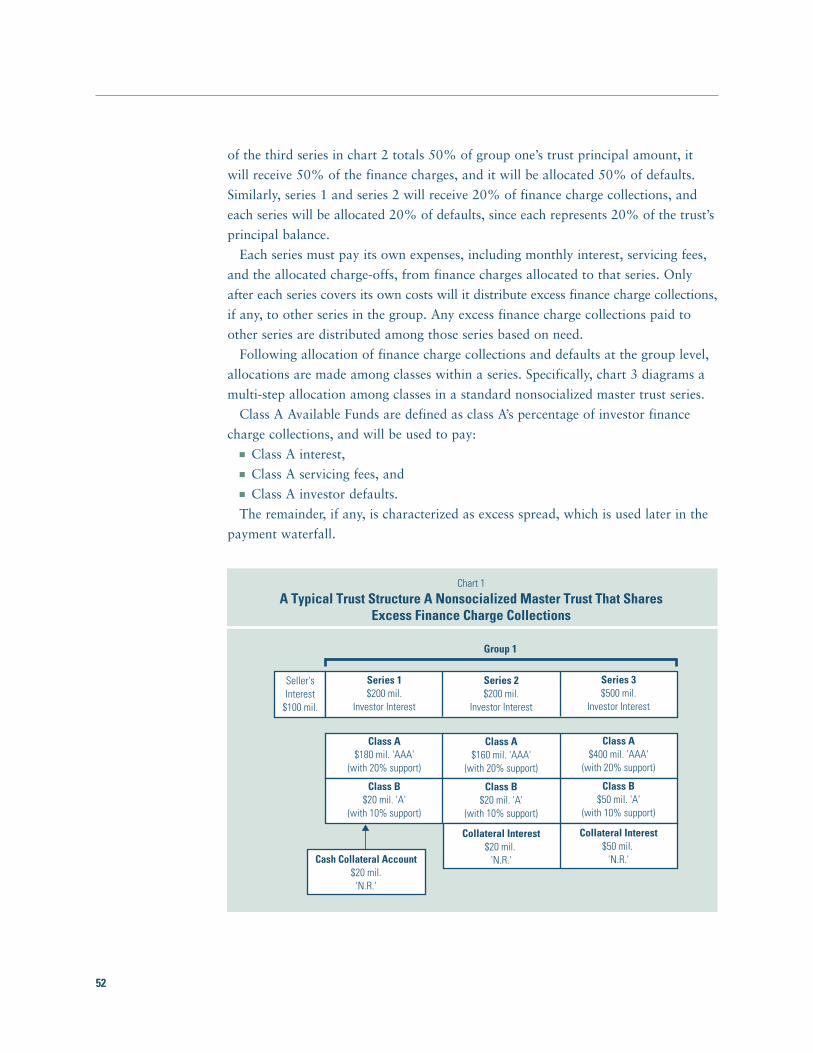

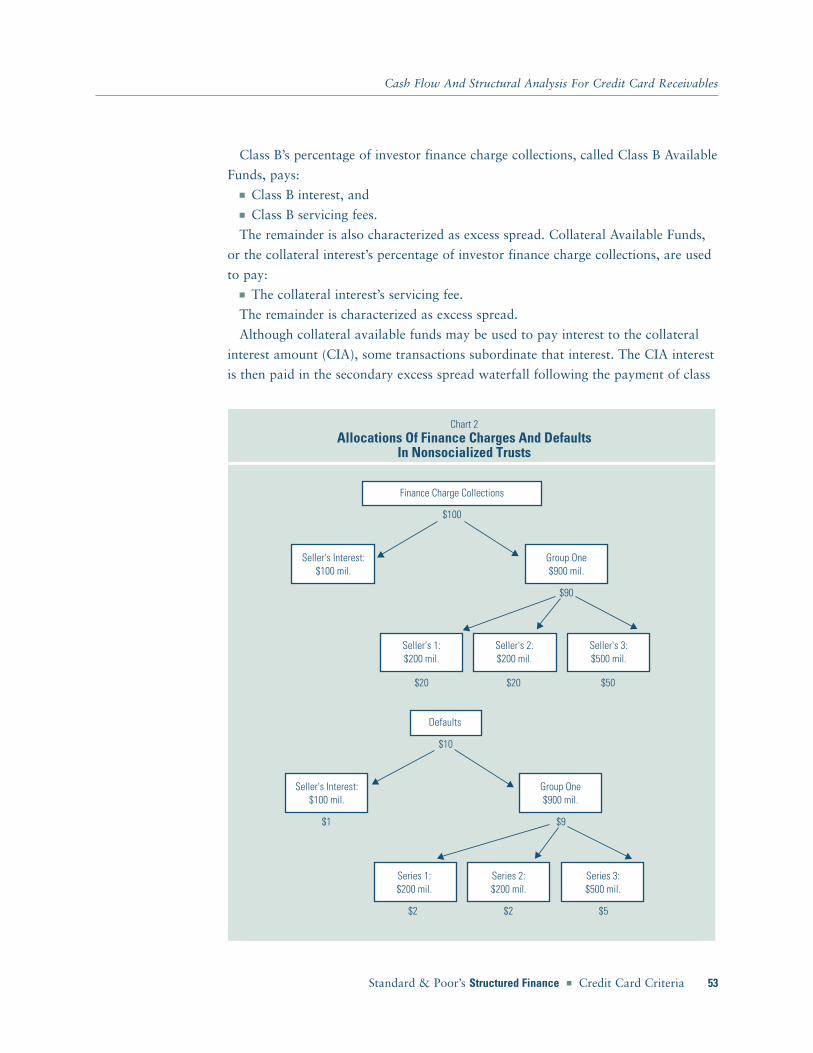

Cash Flow and Structural Analysis ForCredit Card Receivables. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Cash Flow Allocations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Subordination Of Interest Paid To The Collateral Interest Holder . . . . . . . . . 57

Principal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Series Termination And The Credit Rating . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Legal Considerations For Credit Card Receivables. . . . . . 65

General Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Bankruptcy-Remote Entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Transfers, Ownership, And Security Interest . . . . . . . . . . . . . . . . . . . . . . . . . 68

Credit Enhancement. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Selected Specific Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

Pass-Through Certificates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Master Trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Special Considerations For Private-Label AccountsFor Credit Card Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Collateral Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Special Considerations For UnsecuredConsumer Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Market Conditions Encourage Unsecured Lending . . . . . . . . . . . . . . . . . . . . 81

A Hybrid Product . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

Three Categories Of Unsecured Consumer Lending . . . . . . . . . . . . . . . . . . . . 83

Unsecured Consumer Lending Versus Credit Card Lending . . . . . . . . . . . . . . 84

Characteristics Of Unsecured Consumer Loans . . . . . . . . . . . . . . . . . . . . . . . 84

Analyzing Unsecured Consumer Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

3Standard & Poor’s Structured Finance � Credit Card Criteria

Collateral Analysis AndThe Rating Process ForCredit Card Receivables

This section describes the stages of the Standard & Poor’s rating process and

focuses on the analysis of the credit card collateral being securitized. The

collateral analysis includes examination of the originator’s operations and

strategy and the analysis of the historical performance of the credit card portfolio.

The section then discusses the stresses applied to each performance variable and

the effect of each variable on the required credit enhancement for the transaction.

Review Of The Originator’s OperationsOne of the most important aspects of any credit risk assessment is the review of the

originator’s operations. In this review, emphasis is placed on the originator’s marketing,

underwriting, and servicing operations. A rating is based on the representations of

the parties to the transaction, but the scope of the review does not include an audit.

A traditional Standard & Poor’s rating addresses the likelihood of full and timely

payment of interest and principal to certificateholders. Therefore, it addresses the

likelihood of the first dollar of default.

Legal, Collateral, And Structural AnalysisStandard & Poor’s analysis focuses primarily on the legal, collateral, and structural

characteristics of the transaction. The legal criteria for structured finance ratings,

which were developed for MBS, have evolved to cover other asset types in the ABS

market. The fundamental tenet of the criteria is to isolate the assets from the credit

risk of the seller.

The collateral analysis involves an in-depth review of historical asset performance.

Standard & Poor’s collects and analyzes years of data on the performance variables

4

that affect transaction credit risk and examines a broad array of issues related to the

originator’s operations.

The structural review involves an examination of the disclosure and contractually

binding documents for the transaction. These criteria cover many aspects of the

structure, from the method of conveyance of receivables to the trust to the method

of series termination.

Rating CommitteesA team of analysts is assigned to each transaction. After the team of analysts has

performed its review of the issuer’s operations and analyzed the collateral, a committee

of analysts is assembled to determine whether the transaction has sufficient enhance-

ment for the desired rating. The team leader is responsible for ensuring that all perti-

nent information is presented to the rating committee. The committee presentation

includes information gathered in the review process and information on the legal

and structural characteristics of the transaction.

The prospectus for publicly rated transactions is prepared by the issuer’s counsel

before a transaction is priced. However, Standard & Poor’s relies on the binding

agreements to determine whether the structure will provide timely payments. The

most important of these agreements is the pooling and servicing agreement and its

supplement. The supplement is usually drafted by the time a transaction is priced.

Analysts ordinarily present the structure of a transaction to a rating committee after

a transaction is priced, but in any event, as soon as practicable after the team receives

a draft of the supplement. Once the rating committee process is completed, a rating

letter is issued.

Rating SurveillanceAfter a rating is disseminated, it will be maintained by the asset-backed surveillance

group, which works in conjunction with the Structured Finance Ratings Asset-Backed

Group. The purpose of surveillance is to ensure that the rating continues to reflect

the performance and structure of the transaction. The surveillance team is responsible

for monitoring issue performance and identifying those issues that should be considered

for either an upgrade or a downgrade. The goal of the surveillance group is to identify

emerging risks in rated transactions. To that end, the asset-backed services surveillance

group monitors and evaluates monthly changes in performance. Data is collected

and analyzed from the individual master trusts and their component series on a

monthly basis.

To be able to analyze trust performance effectively, the asset-backed surveillance

area requires that servicers send pertinent information no later than the monthly

Collateral Analysis And The Rating Process For Credit Card Receivables

5Standard & Poor’s Structured Finance � Credit Card Criteria

distribution date. The information required includes absolute numbers on the total

trust portfolio. This data enables the surveillance group to measure any collateral

erosion and determine trust income and expenses, as well as calculate relevant trust

Collateral Analysis And The Rating Process For Credit Card Receivables

Eligible principal outstandings: Principal eligiblecredit card receivables in trust pool net of financecharges, and other fees ineligibles, and so on, asof the end of reporting period, which is used asthe analytical basis to determine minimumcollateral required.

Total gross principal outstandings: Net eligibleprincipal outstandings plus other receivables suchas finance charges, and fee interchange, andother fees.

Prefunding account balance: Amount of cash ondeposit in prefunding account available to purchasenew receivables.

Gross losses: Losses on principal receivables.Erosion of collateral recognized during the report-ing period resulting from delinquency criteria,bankruptcies, and so on, as specified in thetrust documents.

Recoveries: Income on receivables that werecharged off during any period, if applicable tothe trust structure.

Net losses: Gross losses minus recoveries.

Delinquencies: Past due amounts not yet chargedoff and segmented by month correlated with thevarious aging criteria prior to charge off.

Total income and its components: Incomeflowing into the trust (excluding recoveries),specifically including cardholder interest paymentsand fees, interchange, discounted receivablesdiscounts, and other miscellaneous income.

Principal collections: Cardholder aggregatedprincipal payments collected from cardholdersduring reporting period to repay debt due.

Purchases: New receivables generated duringthe reporting period resulting from cardholderpurchases and cash advances.

Credit support balance and changes: Periodend balance of each credit support class oraccount used to meet trust covenants and anyuses or repayments during the period.

Outstanding invested amount: Balance of eachrated and unrated investor certificate (includingcollateral interest amount).

Surveillance Variables

Seller’s interest: Principal eligible receivablesminus total invested amount divided by principalreceivables.

Yield: Total trust income divided by total out-standing receivables; annualized.

Gross and net loss rate: Losses on principalreceivables divided by principal outstandings;annualized. Net loss rate includes recoveries.

Certificate rate: Certificate interest paid toinvestors divided by outstanding invested amount;annualized.

Servicing fee rate: Servicing fees paid fromtrust divided by outstanding invested amount.

Base rate: The addition of the certificate andservicing fee rates.

Total payment rate: Total monthly collections(obligor principal and finance charge payments)divided by the previous month’s total outstandings.

Principal payment rate: Principal monthly col-lections divided by the previous month’s eligibleprincipal outstandings.

Delinquency rates: Past due amounts dividedby principal outstandings, segmented by month;annualized.

Purchase rate: Monthly purchases divided bythe previous month’s eligible principal outstandings.

Surveillance Ratios

6

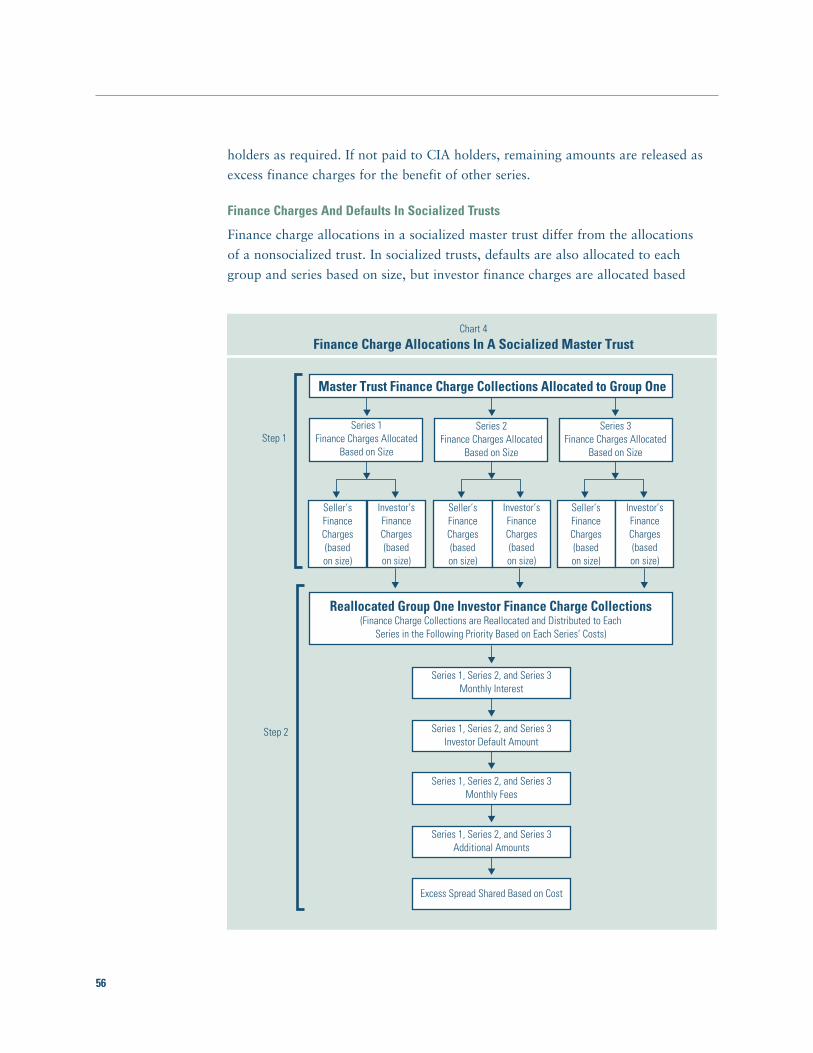

and series ratios (see boxes for surveillance variables and ratios requirements).

Monthly statistics are published by Standard & Poor’s in its Credit Card Quality

Indexes so that industry participants can use the information as a way to track credit

card performance trends.

Performance information is disclosed in a report that is prepared monthly by the

servicer of the transaction. Before a transaction’s closing date, the data that will be

itemized in the servicing report is reviewed to ensure that all necessary information

is included.

The surveillance team also tracks the credit quality of all entities that support a

rated security, such as credit or liquidity enhancers. Analysts review performance

data monthly and contact the issuer if performance deviates beyond a reasonable

band. If a committee vote results in a rating change, the issuer and trustee will be

notified. For public ratings, a press release is normally disseminated.

Collateral Analysis

Review Of The Originator’s Operations

An on-site review of an originator’s operations and management is one aspect of the

rating process. The purpose of the review is to develop an issuer-specific profile in the

areas of marketing, underwriting, servicing, and collections, and to assess other risk

factors such as geographic concentrations and economic conditions. The review pro-

vides analysts an opportunity to discuss with senior management competitive pres-

sures, franchise value, strategic objectives, underwriting, account management poli-

cies, and servicing and collections procedures. The diversity of marketing and under-

writing practices among issuers may result in significant differences in performance.

The review also enables analysts to evaluate the corporation’s organizational and

technological infrastructure, and the quality of its resources, which are critical to

effective servicing and collection of trust receivables.

Marketing

In the securitization process, the issuer retains the risk of maintaining its cardholder

borrowing base. The scope and quality of an issuer’s marketing strategy are important

determinants in an issuer’s ability to generate enough new receivables to support a

securitization program and to effectively manage the performance of the receivables.

Issuers market their credit card products through various distribution channels,

including branch networks, “take-ones” at public locations, advertisements in maga-

zines, toll-free telephone numbers, and direct mail solicitations. Traditionally, most

direct mail offers were “preapproved,” offering lines of credit “up to” specified

amounts. However, due to changes in the Fair Credit Reporting Act (FCRA), issuers

Collateral Analysis And The Rating Process For Credit Card Receivables

7Standard & Poor’s Structured Finance � Credit Card Criteria

now extend “prequalified” solicitations or “invitations to apply.” The net result is

a benefit to issuers, which now have greater leverage to decline responders who no

longer qualify.

Issuers employ a broad range of marketing strategies. For example, many issuers

focus on offering accounts to cardholders who are likely to revolve their balances

because, if credit risk is kept in check, a portfolio of revolving cards is highly profitable

compared with a portfolio of convenience users. There are many ways to attract

revolvers. Many lenders use segmentation techniques that help identify cardholders

who will be attracted to a specific offer and run small sample offers to test response

rates, profitability, and performance. If successful, they roll out a full-scale direct

mail program that targets cardholders with profiles that are similar to those of the

test sample. Others may focus on price leadership and offer low “teaser” rates to

entice cardholders to transfer balances. Responders with pristine credit profiles may

receive permanently low rates. Each of these marketing strategies affects performance

differently. In their review, analysts assess an issuer’s ability to identify, compete for,

price, and maintain high-quality accounts.

Underwriting

Standard & Poor’s assesses the quality with which a particular underwriting methodol-

ogy is developed, implemented, and practiced. Once a potential cardholder or group

of cardholders has been identified, the issuer must determine which type of credit

offer to extend. Issuers that extend similar credit offers (for example, APR and credit

line amounts) to populations with vastly different credit and behavior profiles are

called “mass marketers.” Until recently, mass-marketed offers were the predominant

credit offer in the marketplace. Mass-market issuers maintain the spread between

revenues and losses by subsidizing bad credits with good credits in their portfolio.

In response to increased competition, some issuers turned to a more “targeted”

approach, which involves segmenting their cardholder base and offering a range of

products tailored to the risks and needs of particular groups of customers. For example,

low-rate balance transfer offers are targeted to low-risk customers who revolve balances.

A targeted approach involves additional analysis of credit bureau or third-party sta-

tistical service data, or an issuer’s proprietary data warehouse. Statistical techniques

are used to develop sophisticated credit scoring models to predict and assess the

credit risk of potential cardholders, and to match an offer’s pricing to the risk profile

of the potential cardholder.

Credit scoring is a statistically based tool used to rank applicants by risk level

given the information found on applications or credit bureau reports. Points for a

variety of characteristics are added, producing a score that positions the applicant

along a scale and quantifies the odds that the account will be paid as agreed.

Collateral Analysis And The Rating Process For Credit Card Receivables

8

Issuers use credit scores in assessing a borrower’s risk of default. Cutoff points

for acceptance can change depending on the degree of risk an issuer wants to accept.

Despite their ability to provide relative rankings, credit scores do not correlate per-

formance with specific scores. The probability of a negative performance at a certain

score level will change with adverse selection in a pool of applications as well as

over time.

A targeted approach using scoring is expensive to develop and requires frequent

testing to maintain. However, for those issuers that rely primarily on credit card

accounts for corporate growth and earnings, the investment is essential to maintaining

market share and profitability. Issuers that use proprietary statistical models to offer

customized products are better able to maintain a consistent spread between revenue

and losses for each cardholder or group of similar cardholders. Their primary marketing

channel is direct mail, with limited amounts of preapproved underwriting.

Servicing And Collections

Once a new account is booked, the issuer’s ability to manage that account will

determine its tenure and profitability. Timely and accurate monthly statements and

friendly and efficient customer service generate goodwill and may increase card

usage. With the increase in competition in the industry and the availability of other

credit offers, cardholders demand better service. If an issuer cannot demonstrate an

ability to address and meet valid customer needs, it will eventually lose market share

and be left with a portfolio of cardholders with few other credit options available.

At the same time, it is important to assess an issuer’s ability to keep operating costs

in check. Over time, innovative technological techniques, such as image processing

and artificial intelligence, enable an issuer to reduce expenses, providing additional

flexibility in pricing and marketing strategies.

Adverse selection from attrition will increase the risk profile of the issuer’s portfolio

and may generate losses for certificateholders in securitized pools. Standard & Poor’s

analyzes attrition rates and the issuer’s ability and strategy to retain cardholders.

For example, some issuers have developed statistical models that help predict which

cardholders are likely to be attracted to other offers and pay down in the coming

months. Issuers can then offer these cardholders additional features such as upgrades

to gold cards, lower finance charge rates, elimination of annual fees, and cash back

features that do not impair the profitability of the account.

Effective collection efforts maximize profits to the issuer. The interests of certificate-

holders may be compromised if the issuer cannot demonstrate a prompt and effective

means to collect delinquent balances. Analysts evaluate the quality of collections

staff, collections strategy, and the timeliness of implementation when assessing loss

levels on a portfolio. For example, many servicers leverage senior collection employees

by having them focus on more seriously delinquent accounts. Many also use predictive

Collateral Analysis And The Rating Process For Credit Card Receivables

9Standard & Poor’s Structured Finance � Credit Card Criteria

dialing systems that queue delinquent accounts based on a statistical behavioral

score that identifies the riskiest cardholders. The systems also use other ranking criteria,

such as size of outstanding balances, and they incorporate legal criteria regarding

when collections staff are allowed to call delinquent cardholders. The dialer systems

calculate the optimal time of day to reach a cardholder. These systems have a positive

impact on the efficiency of collections.

Finally, an issuer’s ability to manage fraud losses is examined in a review. Most

issuers combat fraud with neural network systems that detect such activity in the

authorization process. For example, systems are typically programmed to detect

authorizations at gasoline stations for as little as one dollar. Criminals frequently use

gas pumps to test their ability to use a stolen card. Other fraud prevention measures

include mailing deactivated cards that can only be activated by the cardholder with

certain security information or mixing mass mailings of credit cards with mail that

does not contain cards. Also, issuers often stay in contact with the law enforcement

community to discuss the latest card-theft techniques used by organized crime.

Geographic Concentrations And Other Risks

Portfolios can contain additional risk factors that Standard & Poor’s evaluates during

a review. For example, the portfolio could be geographically concentrated, subjecting

it to regional economic or industrial downturns that would be diluted in a more

diversified pool. The portfolio could be heavily biased toward a particular type of

cardholder whose performance may skew the portfolio. Cardholders with similar

interests or affiliations, known as affinity groups, behave differently than consumers

who carry cards that offer rewards, such as airline miles or cash rebates.

Economic and industry trends may also affect the performance of an issuer’s port-

folio. For example, the local employment pool may be stressed due to new corporate

entrants in the region, which may reduce servicing quality or increase wage costs.

Stronger competition in an increasingly saturated market may cause an issuer to be

more lax in its underwriting standards to increase revenue. Changes in consumer

behavior, such as a greater willingness to build up excess credit or declare bankruptcy,

may cause credit quality to deteriorate.

Analysis Of Historical Collateral Performance

Before analyzing stressed cash flow scenarios, analysts examine the historical perfor-

mance of the issuer’s portfolio. Typically, the issuer’s entire portfolio is reviewed, as

master trust structures allow for account additions after a rated series closes, which

may affect the trust’s performance.

In most cases, Standard & Poor’s looks for three to five years of data from first-time

securitizers, since a track record is extremely important. Standard & Poor’s asks for

a range of portfolio data and data is usually provided in a variety of ways. However,

Collateral Analysis And The Rating Process For Credit Card Receivables

10

vintage data is considered an important segmentation and is most often requested

since it allows analysts to examine how originations from different years or campaigns

have performed. Analysts can then examine the trends in performance and match

them to changes in underwriting or servicing strategies. Vintage data can also be

used to gauge the issuer’s loss curve, and determine the ultimate level of charge-offs

by removing the effects of growth. Analysts can then infer how the issuer’s current

strategy may unfold in terms of performance.

Cash Flow Stress Tests And Their Relationship With Payout Triggers

After assessing the seller and servicer’s operations and analyzing the performance of

the issuer’s receivables, the analytical team runs cash flow scenarios that stress five

key performance variables: payment rate, purchase rate, losses, portfolio yield, and

certificate rate. Implicit in the cash flow runs is the assumption that a base rate payout

event will cause the transaction to amortize. A base rate amortization will occur

when the three-month average portfolio yield, net of losses, is insufficient to cover

the certificate interest and servicing fees averaged for the same period. At that point,

all principal payments collected from cardholders are passed through to investors.

The guidelines that follow encompass many of the parameters used to model a

typical transaction, but these are not all-inclusive. A variety of cash flow runs are

presented to a rating committee for deliberation. Also, as the market for credit card-

backed certificates is dominated by ‘AAA’ and ‘A’ rated paper, the discussion focuses

on the stress levels for those rating categories. A separate discussion of Standard &

Poor’s ‘BBB’ cash flow modeling will be discussed in a later section.

Payment Rate

The payment rate is one of the most important variables in the model because a higher

payment rate ensures that investors are paid out quickly in adverse scenarios. In a

base rate amortization, reductions in enhancement can accumulate rapidly, exposing

investors to potential default losses. Enhancement reductions, or write-downs of the

certificate, will occur when the portfolio yield is unable to cover charge-offs plus the

certificate rate and servicing fee. That is, draws on credit enhancement occur when

the excess spread is negative. Therefore, transactions that pay principal at faster

rates (i.e., those with higher payment rates) are exposed to losses over a shorter period

of time and, therefore, need less enhancement.

For a transaction with a standard base rate trigger and a typical mix of fixed- and

floating-rate assets, analysts usually assume that a transaction will enter rapid amor-

tization with a 5% annualized negative spread rate. In the first month of the rapid

amortization stress period, increases in charge-offs are the main reason excess spread

is negative. In subsequent months, charge-offs and floating-rate certificate rates, if

applicable, are assumed to rise to their ultimate levels, which raise the total negative

Collateral Analysis And The Rating Process For Credit Card Receivables

11Standard & Poor’s Structured Finance � Credit Card Criteria

spread in the trust. The payment rate assumption in an ‘AAA’ stress scenario is usually

45%-55% of the issuer’s steady-state portfolio payment rate. The discount percentage

applied to the steady-state payment rate depends on the level of payment rates, pay-

ment rate trends, servicing practices, and payment-rate volatility. The ‘A’ scenario

typically is 10% faster than the ‘AAA’ assumption (that is, 50%-60% of the

steady-state assumption).

Purchase Rate

The pooling and servicing agreement governing credit card receivables-backed trans-

actions calls for the continued transfer to the trust of all receivables arising in the

designated accounts. Therefore, purchases keep the amount of principal receivables

in the trust from declining. Higher purchase rates increase the pace of the repayment

of principal to investors. For example, assume that the monthly principal payment

rate equals 10% of the outstanding principal amount in the trust. If the purchase

rate was less than 10%, the amount of principal receivables in the trust would decline

each month, leaving a lower amount of principal collections to retire old receivables.

A steady payment rate on a declining trust balance would result in fewer dollars of

principal payments in subsequent months. However, if the purchase rate equaled the

10% payment rate, the principal receivables in the trust would remain at their initial

level, and the portfolio would not decline. Thus, monthly principal collections would

also be maintained. If the purchase rate exceeded the 10% payment rate, principal

collections would be greater than payments received and the portfolio would continue

to grow.

The purchase rates used in the model vary based on the seller’s business and per-

formance characteristics, the seller’s credit rating, and the certificate rating that the

issuer is trying to achieve. But the chief risk associated with a purchase rate assumption

is the risk of seller bankruptcy or insolvency. Therefore, higher-rated lenders are usually

given more purchase-rate credit because they are more likely to survive adverse business

conditions and fund purchases in the future. Also, bank card issuers that are part of

the VISA or MasterCard associations have franchise value that would make it more

likely for other originators to bid for their accounts if they were to disengage from

the business.

Insolvency is the chief risk because if the originator becomes insolvent, the trust

may not have ownership of, or a first perfected security interest in, receivables origi-

nated after insolvency. In the event of an insolvency, the documents generally require

the servicer to allocate collections to the trust as if the trust owned all the receivables.

Further, if the servicer is legally prevented from doing so, the documents call for the

allocation of all collections from each account to be used first to pay off the oldest

balances (as in first in, first out accounting). Since the trust has an interest in the

Collateral Analysis And The Rating Process For Credit Card Receivables

12

oldest balances, this allocation method is more advantageous than a pro rata

distribution.

The purchase rates modeled for bank cards range from 2% to 5%. In contrast,

most retail lenders are given no purchase rate credit because retailers are typically

unrated and because of low franchise value, whereby retailer cards are assumed to

have little utility in a U.S. Bankruptcy Code Chapter 7 liquidation.

Charge-offs

The risk of volatility in the charge-off rate, portfolio yield, and certificate rate is par-

tially captured by the base rate trigger. Therefore, there is only slight variation from

transaction to transaction in the stress scenario’s negative spread at the start of the

modeled rapid amortization period. As previously mentioned, rapid amortization

cash flow modeling for a ‘AAA’ case begins with excess cash flow starting at a negative

5% annualized rate. That negative rate usually results in a charge-off level that is

1.5 to two times the steady-state assumption at the start of a rapid amortization

before reaching an ultimate ‘AAA’ stress loss case within 12 months. However,

cumulative negative spread will be affected by the ultimate charge-off level and the

rate of deterioration of each performance variable, which is determined through

portfolio-specific analysis.

In a ‘AAA’ scenario, the ultimate charge-off level is typically increased by three to

five times the issuer’s steady-state charge-off level. The steady-state level is determined

by examining historical portfolio statistics and by incorporating an assessment of

underwriting and servicing quality. For ‘A’, ultimate charge-offs are assumed to

reach two to three times the steady-state level.

Portfolio Yield

Portfolio yield generally consists of three types of payments: finance charges, fees,

and interchange. Periodic finance charges are the interest cost associated with an

unpaid balance at the end of a grace period. Fees include annual membership fees,

late payment fees, and overlimit fees. Interchange is the fee paid to originators by

VISA or MasterCard for absorbing risk and funding receivables during grace periods.

Although some issuers do not include all of these sources in portfolio yield, others

include these and more. For example, recoveries from previously charged-off

accounts can be included, as can the proceeds from “receivable discounting.” A dis-

counted receivable arises when a portion (usually 1%-5%) of principal receivables is

designated as finance charge receivables. Collections of discounted principal receivables

are then treated as finance charges. Several bank card master trusts incorporated

discounting before a bulletin from the Office of the Comptroller of the Currency stated

that discounting could not be considered recourse.

Collateral Analysis And The Rating Process For Credit Card Receivables

13Standard & Poor’s Structured Finance � Credit Card Criteria

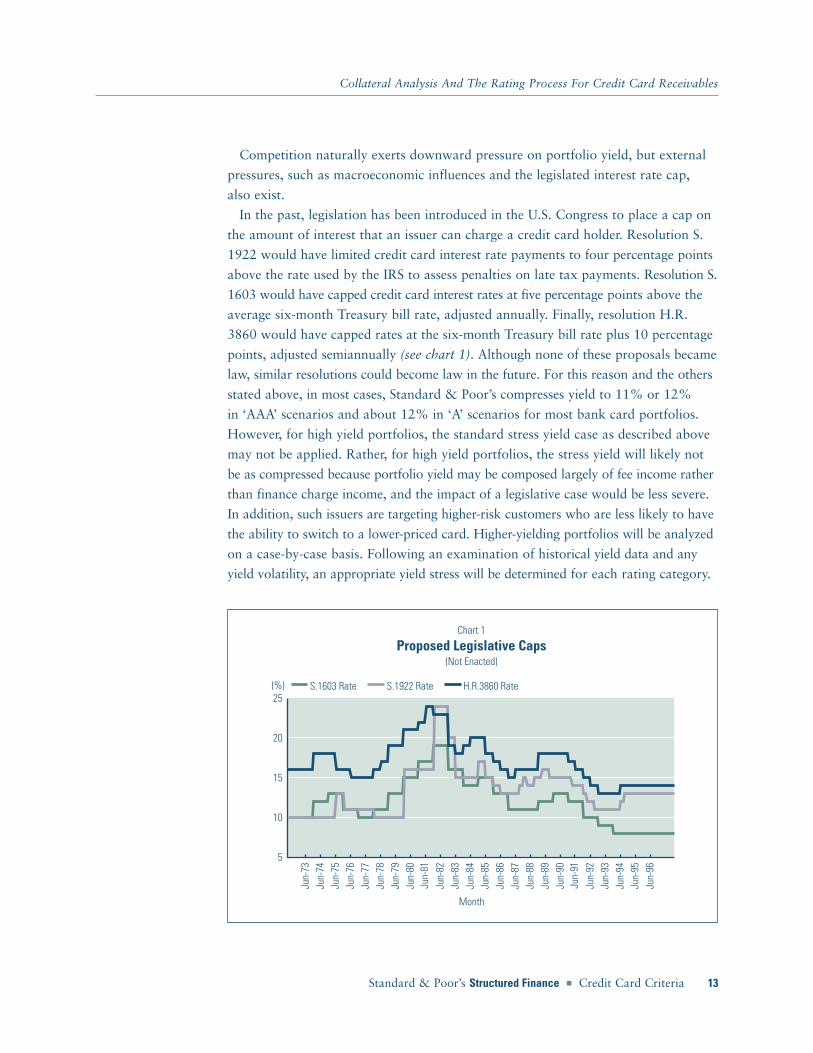

Competition naturally exerts downward pressure on portfolio yield, but external

pressures, such as macroeconomic influences and the legislated interest rate cap,

also exist.

In the past, legislation has been introduced in the U.S. Congress to place a cap on

the amount of interest that an issuer can charge a credit card holder. Resolution S.

1922 would have limited credit card interest rate payments to four percentage points

above the rate used by the IRS to assess penalties on late tax payments. Resolution S.

1603 would have capped credit card interest rates at five percentage points above the

average six-month Treasury bill rate, adjusted annually. Finally, resolution H.R.

3860 would have capped rates at the six-month Treasury bill rate plus 10 percentage

points, adjusted semiannually (see chart 1). Although none of these proposals became

law, similar resolutions could become law in the future. For this reason and the others

stated above, in most cases, Standard & Poor’s compresses yield to 11% or 12%

in ‘AAA’ scenarios and about 12% in ‘A’ scenarios for most bank card portfolios.

However, for high yield portfolios, the standard stress yield case as described above

may not be applied. Rather, for high yield portfolios, the stress yield will likely not

be as compressed because portfolio yield may be composed largely of fee income rather

than finance charge income, and the impact of a legislative case would be less severe.

In addition, such issuers are targeting higher-risk customers who are less likely to have

the ability to switch to a lower-priced card. Higher-yielding portfolios will be analyzed

on a case-by-case basis. Following an examination of historical yield data and any

yield volatility, an appropriate yield stress will be determined for each rating category.

Collateral Analysis And The Rating Process For Credit Card Receivables

Jun-

73Ju

n-74

Jun-

75Ju

n-76

Jun-

77Ju

n-78

Jun-

79Ju

n-80

Jun-

81Ju

n-82

Jun-

83Ju

n-84

Jun-

85Ju

n-86

Jun-

87Ju

n-88

Jun-

89Ju

n-90

Jun-

91Ju

n-92

Jun-

93Ju

n-94

Jun-

95Ju

n-96

Month

5

10

15

20

25S.1603 Rate S.1922 Rate H.R.3860 Rate(%)

Chart 1

Proposed Legislative Caps(Not Enacted)

14

Certificate Rate

The modeled certificate rate for ‘AAA’ ratings equals the actual rate for fixed-rate

transactions, but rises in floating-rate transactions to the capped rate when interest

rate caps are provided, or to a level that exceeds the yield on the portfolio in uncapped

deals. That ultimate uncapped level usually peaks at a rate of 15% under the ‘AAA’

stress case and 14% under the ‘A’ stress case. The rate of increase to these ultimate

levels can vary, however. In determining the ultimate level of increase on floating-rate

transactions, analysts will take into consideration other factors, including the issuer’s

ability to manage and reprice its portfolio and the rating on the certificates. Additionally,

analysts recognize that the relationship between portfolio yield and the variable cost

of funds is an important factor in determining the level of excess spread for floating-

rate certificates.

Principal Allocation Assumptions

The method used to allocate principal between the seller and the investor certificates

during amortization is yet another cash flow aspect to consider. The transactions are

usually structured to pay investor certificates based on a fixed/floating ratio allocation.

The fixed/floating allocation freezes the numerator for the series payment ratio at an

amount equal to the series investor interest at the end of the revolving period, but

the denominator floats to equal the current principal receivables in the trust. The

principal allocation percentage (PAP) for investor certificates in amortization will

equal the lesser of 100% and the following percentage: Investor interest at the end

of the revolving period divided by the greater of: (1) principal in the trust plus cash

in the excess funding account, and (2) the sum of the numerators for all series’ PAP.

Standard & Poor’s assumes that the seller’s interest would quickly reach zero in

amortization due to dilution and fixes both the numerator and denominator in the

cash flow assumption so that the ratio is equivalent to 100%. This results in a slower

payout of rated classes than if the seller’s interest were assumed to be positive under

a fixed/floating allocation. As mentioned above, series with slower principal payments

require more enhancement to cover losses.

Also, during amortization, the cash flow allocation sections of the documents provide

that certificateholders receive the benefit of principal collections from other principal-

sharing series in their revolving period. However, analysts assume that such amounts

will not be available, as many factors could cause a disruption in such cash flow. One

example of such a disruption is a seller insolvency that would cause a trustwide rapid

amortization event in which all series would amortize at the same time.

Collateral Analysis And The Rating Process For Credit Card Receivables

15Standard & Poor’s Structured Finance � Credit Card Criteria

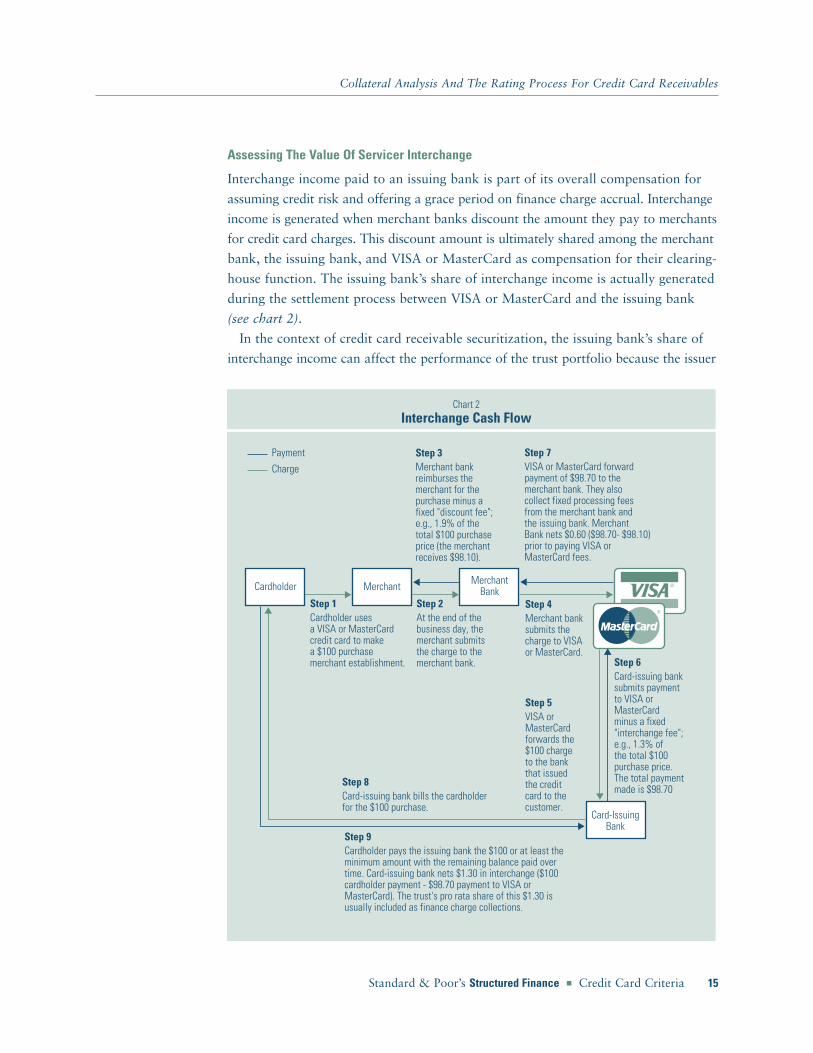

Assessing The Value Of Servicer Interchange

Interchange income paid to an issuing bank is part of its overall compensation for

assuming credit risk and offering a grace period on finance charge accrual. Interchange

income is generated when merchant banks discount the amount they pay to merchants

for credit card charges. This discount amount is ultimately shared among the merchant

bank, the issuing bank, and VISA or MasterCard as compensation for their clearing-

house function. The issuing bank’s share of interchange income is actually generated

during the settlement process between VISA or MasterCard and the issuing bank

(see chart 2).

In the context of credit card receivable securitization, the issuing bank’s share of

interchange income can affect the performance of the trust portfolio because the issuer

Collateral Analysis And The Rating Process For Credit Card Receivables

Chart 2Interchange Cash Flow

MerchantBank

Payment

Charge

®

®

Card-IssuingBank

Step 3Merchant bankreimburses themerchant for thepurchase minus afixed "discount fee";e.g., 1.9% of thetotal $100 purchaseprice (the merchantreceives $98.10).

Step 7VISA or MasterCard forwardpayment of $98.70 to themerchant bank. They alsocollect fixed processing feesfrom the merchant bank andthe issuing bank. MerchantBank nets $0.60 ($98.70- $98.10)prior to paying VISA orMasterCard fees.

Step 1Cardholder usesa VISA or MasterCardcredit card to makea $100 purchasemerchant establishment.

Step 2At the end of thebusiness day, themerchant submitsthe charge to themerchant bank.

Step 4Merchant banksubmits thecharge to VISAor MasterCard.

Step 6Card-issuing banksubmits paymentto VISA orMasterCardminus a fixed"interchange fee";e.g., 1.3% ofthe total $100purchase price. The total paymentmade is $98.70

Step 5 VISA or MasterCardforwards the $100 chargeto the bankthat issuedthe creditcard to the customer.

Step 8Card-issuing bank bills the cardholderfor the $100 purchase.

Step 9Cardholder pays the issuing bank the $100 or at least theminimum amount with the remaining balance paid overtime. Card-issuing bank nets $1.30 in interchange ($100cardholder payment - $98.70 payment to VISA orMasterCard). The trust's pro rata share of this $1.30 isusually included as finance charge collections.

Cardholder Merchant

16

typically promises to remit a pro rata share of interchange directly to the trust. At

the trust level, such supplemental cash flow is then recharacterized and applied as

additional finance charge collections to pay for transaction expenses such as certificate

interest, servicing fees and trustee fees, and defaulted amounts. If structured this

way, interchange income can provide extra loss coverage by creating a greater level

of excess spread. However, because of legal considerations, Standard & Poor’s will

not assign any credit to interchange unless certain conditions are met.

Legal Analysis Of Interchange Income

Standard & Poor’s historically has felt that the benefit of receiving interchange income 10

could evaporate upon a seller insolvency. This view was predicated on legal analysis

that suggested that perfecting interchange fees would be problematic because of the

following issues:� The property rights of the issuing bank in interchange fees are not clearly defined

in the membership agreements with VISA and MasterCard, and� Interchange fees are subject to setoff by VISA and MasterCard.

As VISA and MasterCard are not parties to the transaction, they provide no

representations, warranties, or covenants related to interchange fees. Additionally,

interchange rates are revised annually by VISA and MasterCard.

Servicing Fee Requirements And Interchange Dependency

As a means of reducing required credit enhancement levels, some servicers have offered

to have a portion of their servicing fee paid from interchange, if it is available. This

arrangement can reduce the required level of credit enhancement by contractually

limiting a portion of the required servicing fee to the actual level of monthly interchange

income allocated to the trust. For example, the servicer may require a 2% annual

servicing fee but contractually agree to accept 1% of the servicing fee from interchange

income to the extent it is available. If interchange did not exist, the servicer would

only be paid a 1% servicing fee from trust cash flows. The implication of this structural

provision is a 1% reduction in the servicing fee expense assumption for cash flow

modeling purposes, but this is only possible if the conditions below are met.

Modeling Assumptions For InterchangeStandard & Poor’s normally assumes no benefit is derived from interchange due to

perfection issues associated with these fees. Because of the legal analysis discussed

previously and the fact that interchange income is generated during the settlement

process between VISA and MasterCard and the issuing bank, analysts assume that

interchange income will not exist in a worst-case early amortization scenario. This is

Collateral Analysis And The Rating Process For Credit Card Receivables

17Standard & Poor’s Structured Finance � Credit Card Criteria

one of the assumptions used to support the reduction in portfolio yield for cash flow

modeling purposes.

However, if certain conditions are met, credit will be applied in the analysis for

servicer interchange. Analysts will run stressed cash flow scenarios with full credit

to servicer interchange only if the transaction meets the following criteria:� For investment-grade certificate ratings, the trust must have a servicer and a

trustee (as successor servicer) willing to be paid a portion of its servicing fee

from servicer interchange. Both must have high long-term senior unsecured debt

ratings, and both must accept a reduced servicing fee if interchange is not avail-

able in the future.

The rationale is that one of the highly rated entities should be available to service

the portfolio at the lower servicing fee.� The trustee must have credit card-servicing capabilities.

The trustee is obligated to service or find a replacement servicer if the current servicer

is no longer able to service the trust. Standard & Poor’s assumes that the trustee will

not be able to find a replacement servicer that will service the trust at the contracted

fee and will be required to assume that role itself. For this reason, the trustee must

have experience with servicing a credit card portfolio.

If these provisions are incorporated into the structure of the transaction, analysts

assign value to interchange income. Otherwise, interchange is viewed as an unperfected

source of income that would disappear upon the seller’s insolvency. However, if

interchange credit is given, the certificate ratings will be dependent on the servicer

and trustee’s ratings and may be affected by a downgrade of either party’s ratings.

Collateral Analysis And The Rating Process For Credit Card Receivables

19Standard & Poor’s Structured Finance � Credit Card Criteria

‘BBB’ Ratings Criteria ForCredit Card CollateralInvested Amounts

This section describes the criteria underlying Standard & Poor’s ‘BBB’ ratings.

It begins with a brief description of the collateral invested amount (CIA)

and the evolution of the CIA market. Then the section summarizes the

stresses applied to key performance variables under three separate cash flow scenarios:

the combined-stress case, the loss-spike test, and the interest rate-spike test before

concluding with a discussion of the legal aspects unique to rating CIA pieces.

Collateral Invested AmountA popular form of credit enhancement to the more senior classes, class A and class

B, is a subordinated interest known as the collateral invested amount (CIA). The

most subordinated interest is referred to by a number of different names, including

the enhancement invested amount, the C class, and the collateral interest. For purposes

of this section, it will be called the collateral invested amount or CIA. All references

are to securities issued by a master trust and backed by bank credit card receivables.

As the market has matured, issuers have placed a greater interest in expanding the

universe of buyers for the CIA to diversify funding sources. This is especially important

because many traditional CIA buyers reached their lending limits for selected names.

In addition, many investors that traditionally purchase more senior classes of credit

card-backed securities have taken an interest in purchasing the most subordinated

class to increase yield in exchange for incremental risk. These factors, along with

heightened investor concerns over consumer credit quality, have helped drive the

demand for Standard & Poor’s ratings on CIA interests.

20

Market EvolutionThe earlier credit card deals incorporated letters of credit (LOCs) from highly rated

institutions to protect investors against the risk of default. To avoid a rating depen-

dency on the credit quality of the LOC provider, the market moved to cash collateral

accounts funded by the same institutions that formerly provided the LOCs. Since

CIAs were introduced in the early 1990s they have become the most common form

of credit enhancement.

When CIA structures were first introduced, issuers had their CIAs rated mainly for

tax purposes, rather than to allay investors’ credit concerns. Issuers understood that

an investment-grade debt rating was viewed favorably by tax lawyers opining whether

the IRS would deem the CIA as debt for tax purposes. The former LOC and cash

collateral account providers were, and have continued to be, the primary investors

in the CIA market, having built their expertise for evaluating the credit risks well

before the enhancement was a ratable subordinated debt interest.

As the traditional investor market for CIAs has become saturated, issuers have

become more interested in having their CIAs rated by Standard & Poor’s to gain

greater acceptance from potential new investors and to reduce their reliance on existing

sources of finance. Additionally, traditional buyers began to express interest in having

CIAs rated to increase their ability to syndicate their positions, which would free up

capacity to invest in future transactions and create a more liquid market. Across the

board, investors have become more sensitive to credit risks and price volatility due

to credit spreads.

Structural Credit Enhancement And Excess SpreadAll credit card structures incorporate a series of amortization events that, if triggered,

cause principal collections allocated to investors to be passed through immediately

and before the scheduled payment date. Among other things, amortization events

include insolvency of the originator of the receivables, breaches of representations

or warranties, a servicer default, failure to add receivables as required, and asset

performance-related events. Additionally, a transaction will generally amortize early

if the three-month average excess spread falls below zero annualized. Excess spread

is generally defined as finance charge collections minus certificate interest, servicing

fees, and charge-offs allocated to the series. Early amortization is a powerful form

of structural credit enhancement for all certificateholders, including the CIA holders,

who are generally in the first loss position.

In a typical credit card structure, credit enhancement for the A and B classes is

fully funded at closing. For example, the class A certificate relies on the credit

enhancement provided by the subordination of class B and the CIA and/or a cash

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

21Standard & Poor’s Structured Finance � Credit Card Criteria

collateral account, if any. In contrast, the enhancement for the CIA is dynamic and

typically in the form of a reserve account. The reserve account is funded from excess

spread plus an initial deposit, if necessary. The amount of excess spread deposited

into a reserve account is dictated by the terms of the CIA loan agreement. Generally,

if excess spread falls below specified levels, excess finance charge collections are

trapped in a reserve account for the CIA’s benefit. A typical loan agreement will

require a targeted reserve fund balance based on the current level of excess spread.

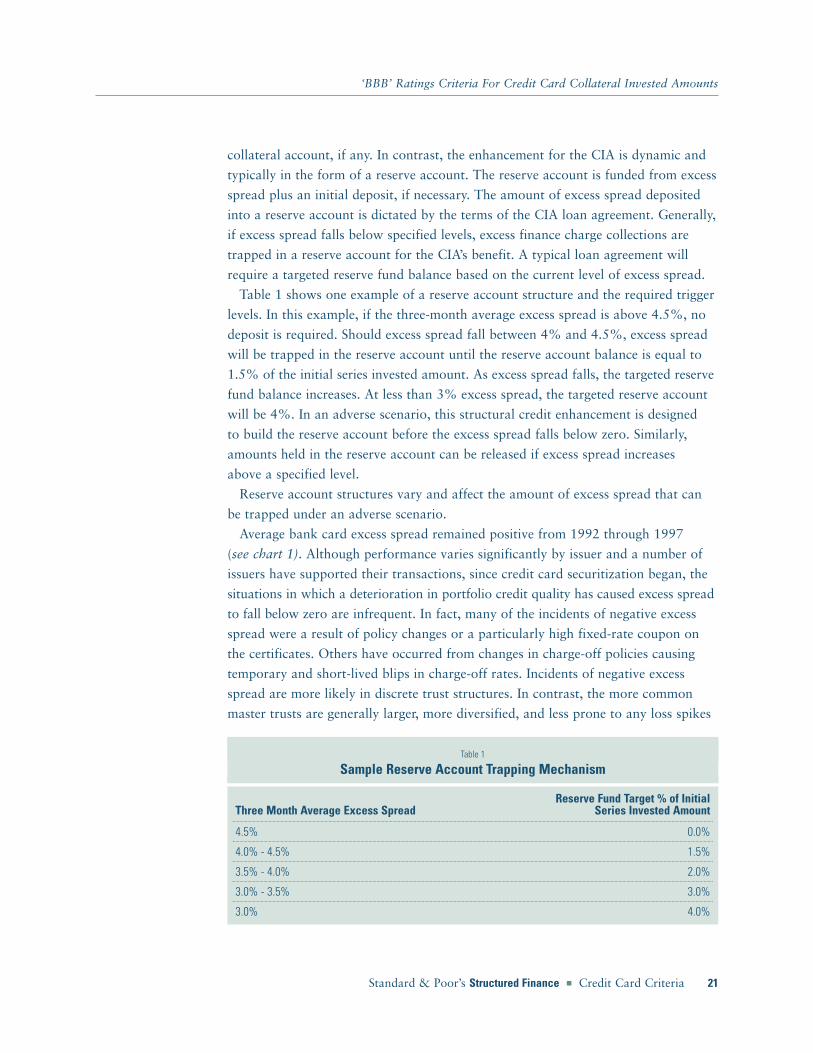

Table 1 shows one example of a reserve account structure and the required trigger

levels. In this example, if the three-month average excess spread is above 4.5%, no

deposit is required. Should excess spread fall between 4% and 4.5%, excess spread

will be trapped in the reserve account until the reserve account balance is equal to

1.5% of the initial series invested amount. As excess spread falls, the targeted reserve

fund balance increases. At less than 3% excess spread, the targeted reserve account

will be 4%. In an adverse scenario, this structural credit enhancement is designed

to build the reserve account before the excess spread falls below zero. Similarly,

amounts held in the reserve account can be released if excess spread increases

above a specified level.

Reserve account structures vary and affect the amount of excess spread that can

be trapped under an adverse scenario.

Average bank card excess spread remained positive from 1992 through 1997

(see chart 1). Although performance varies significantly by issuer and a number of

issuers have supported their transactions, since credit card securitization began, the

situations in which a deterioration in portfolio credit quality has caused excess spread

to fall below zero are infrequent. In fact, many of the incidents of negative excess

spread were a result of policy changes or a particularly high fixed-rate coupon on

the certificates. Others have occurred from changes in charge-off policies causing

temporary and short-lived blips in charge-off rates. Incidents of negative excess

spread are more likely in discrete trust structures. In contrast, the more common

master trusts are generally larger, more diversified, and less prone to any loss spikes

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

Table 1

Sample Reserve Account Trapping Mechanism

Reserve Fund Target % of Initial Three Month Average Excess Spread Series Invested Amount

4.5% 0.0%

4.0% - 4.5% 1.5%

3.5% - 4.0% 2.0%

3.0% - 3.5% 3.0%

3.0% 4.0%

22

associated with account seasoning. Additionally, several issuers have increased

excess spread by managing the composition of the securitized portfolio to reduce

loss rates or discounted receivables to boost yield.

Cash flow models are used to measure the effect of a deterioration in excess spread

on a transaction and how this deterioration affects the amount of cash that can be

trapped in a spread account to cover defaults. The cash flow model formulas reflect

the payment allocation provisions in the pooling and servicing agreements, as well

as the CIA loan agreement. For cash flow modeling purposes, excess spread is assumed

to be the lower of either the current level or the first trigger level (4.5% in the example

above) when simulating a stress test. Excess spread is not a cash flow model input;

rather, it is a model output.

Once an excess spread trigger level is breached, the reserve account builds from

monthly excess spread, if any, up to the targeted balance. If finance charge collections

are insufficient to cover certificate interest, servicing fees, and receivable charge-offs,

excess spread is negative and amounts in the reserve account will be reduced. To

achieve an investment-grade rating on a CIA, a sufficient amount of excess spread

must be available to fund a reserve account to avoid a default under various ‘BBB’

stress tests.

0

5

10

15

20

Jan-98Jan-97Jan-96Jan-95Jan-94Jan-93Jan-92

Chart 1Bank Card Trusts Excess Spread

(%)

Bank Card Loss Rate

Bank Card Wtd Base Rate

Bank Card Spread

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

23Standard & Poor’s Structured Finance � Credit Card Criteria

‘BBB’ Ratings Reflect Seller-Specific ConsiderationsWhen moving down the ratings spectrum, greater reliance can be placed on the card

issuer’s ability to originate and effectively manage its credit card business. In addition,

compared with the ‘AAA’ and ‘A’ stress cases discussed in the section Collateral

Analysis And The Rating Process, when evaluating CIA pieces, less-conservative

portfolio-stress scenarios are assumed for cash flow modeling purposes.

The ratings on the more senior classes are typically above the unsecured debt rating

of the bank that originates and services the credit card receivables that have been

transferred to the issuer. The senior class can be rated above the unsecured rating of

the bank because the senior class ratings are based primarily on the creditworthiness

of isolated pools of assets, without regard to the creditworthiness of the bank. The

probability and potential impact of the bank’s insolvency are factored into the rating

assigned to the senior certificates. Therefore, in assigning a rating to the more senior

classes, the transaction’s structure must provide the means by which the assets’ cash

flow would be available to pay debt service in a timely manner notwithstanding the

insolvency, receivership, or bankruptcy of the issuer.

In contrast, the CIA ratings are often at or below the rating of the originator/servicer.

Therefore, greater reliance can be placed on the bank’s ability to effectively service

the portfolio during the life of the transaction and to originate and transfer receivables

to the issuer. When the bank’s rating is at least as high as that of the credit card-backed

security, the bank’s credit card business can be viewed as an ongoing concern for

purposes of the CIA analysis, and performance is modeled accordingly.

In rating the CIA, the analysis incorporates many of the same factors Standard &

Poor’s considers when assigning an unsecured rating to the bank. These include

quantitative factors such as loss rates, bankruptcy data, payment rates, the mix of

variable- and fixed-rate accounts, and repricing information. More qualitative factors

are also included, such as marketing, pricing and account-retention strategies,

underwriting and account-management policies, the use of technology, the strategic

importance of the securitization program as a source of funding, and management

expertise. Additionally, Standard & Poor’s assesses macroeconomic conditions, con-

sumer behavior, geographic concentrations, competitive pressures, and franchise

value. All of these factors are critical in determining the appropriate ‘BBB’ enhancement

level for CIA classes. The links between secured and unsecured ratings at the invest-

ment-grade rating level imply the possibility that a ‘BBB’ structured rating may be

downgraded in conjunction with the downgrade of an issuer’s unsecured rating to

below investment grade.

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

24

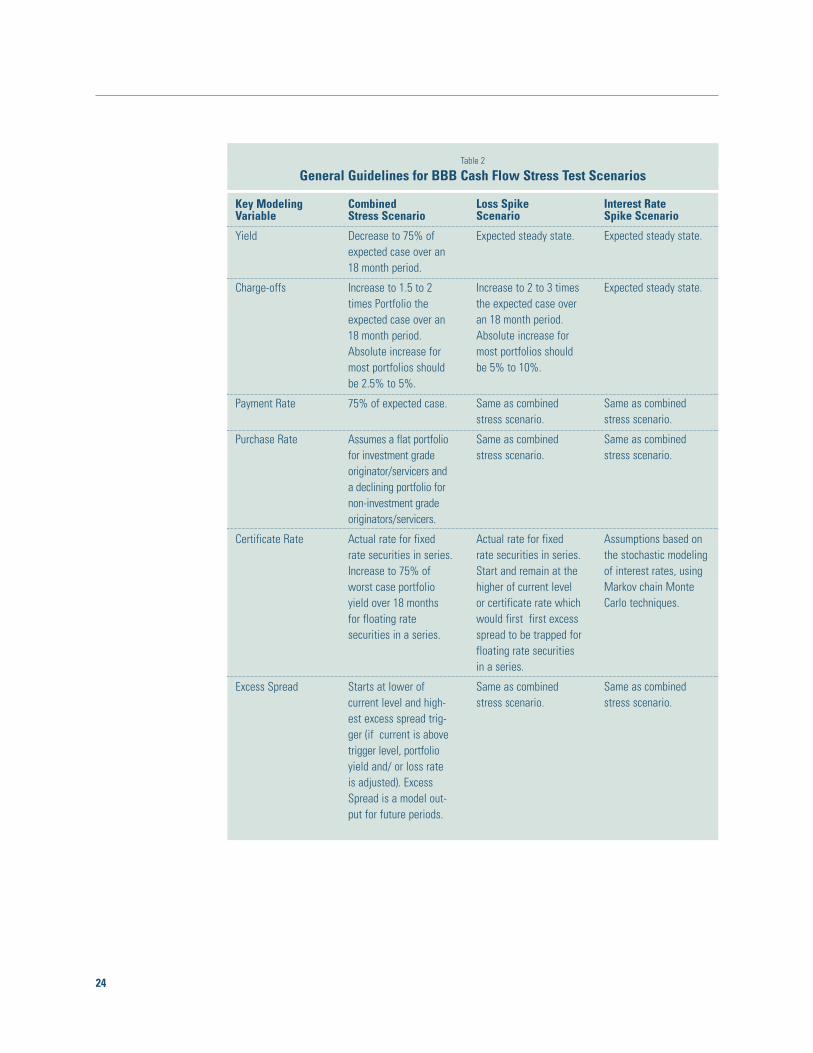

Table 2

General Guidelines for BBB Cash Flow Stress Test Scenarios

Key ModelingVariable

Yield

Charge-offs

Payment Rate

Purchase Rate

Certificate Rate

Excess Spread

CombinedStress Scenario

Decrease to 75% ofexpected case over an18 month period.

Increase to 1.5 to 2times Portfolio theexpected case over an18 month period.Absolute increase formost portfolios shouldbe 2.5% to 5%.

75% of expected case.

Assumes a flat portfoliofor investment gradeoriginator/servicers anda declining portfolio fornon-investment gradeoriginators/servicers.

Actual rate for fixedrate securities in series.Increase to 75% ofworst case portfolioyield over 18 months for floating rate securities in a series.

Starts at lower of current level and high-est excess spread trig-ger (if current is abovetrigger level, portfolioyield and/ or loss rate is adjusted). ExcessSpread is a model out-put for future periods.

Loss Spike Scenario

Expected steady state.

Increase to 2 to 3 timesthe expected case overan 18 month period.Absolute increase formost portfolios shouldbe 5% to 10%.

Same as combinedstress scenario.

Same as combinedstress scenario.

Actual rate for fixedrate securities in series.Start and remain at thehigher of current levelor certificate rate whichwould first first excessspread to be trapped forfloating rate securitiesin a series.

Same as combinedstress scenario.

Interest RateSpike Scenario

Expected steady state.

Expected steady state.

Same as combinedstress scenario.

Same as combinedstress scenario.

Assumptions based onthe stochastic modelingof interest rates, usingMarkov chain MonteCarlo techniques.

Same as combinedstress scenario.

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

25Standard & Poor’s Structured Finance � Credit Card Criteria

Three ‘BBB’ Stress Test ScenariosWhen analyzing a CIA, Standard & Poor’s will evaluate the impact of a deterioration

in pool performance or an increase in the deal’s certificate rate, or both, using three

separate cash flow scenarios. The three ‘BBB’ scenarios include a combined-stress, a

loss-spike, and an interest rate-spike scenario. Under the combined-stress scenario,

all key variables are stressed simultaneously. This combined worse case approach is

similar to the ‘AAA’ and ‘A’ stress cases, in which various performance variables are

stressed at the same time. For the loss-spike stress test, the certificate rate and portfolio

yield are held constant at the steady state and the loss rate is stressed more severely.

The interest rate-spike scenario incorporates a sharp increase in the coupon for

floating-rate securities in a series and holds loss rates and portfolio yield constant

at their expected steady states. The portfolio purchase rate and payment rate

assumptions are the same for all three scenarios. There is no strict formula for

specific stress levels applied to each modeling variable. Instead, the level of stress

is portfolio specific and is based on an analysis of the pool characteristics and an

evaluation of the originator/servicer.

Charge-offs/Loss-Spike AnalysisIn a ‘AAA’ scenario, the peak annualized loss percentage is typically three to five

times the expected steady state for the portfolio. This peak is reached in 12 months.

In contrast, in a ‘BBB’ combined-stress scenario, loss rates are increased to 1.5 to

two times the expected steady state. The peak is reached in 18 months and the absolute

level of increase typically does not exceed 500 basis points for the combined-stress

scenario. For a ‘BBB’ rating, a transaction should also be able to survive an increase

in losses of two to three times the expected steady state under a loss-spike scenario.

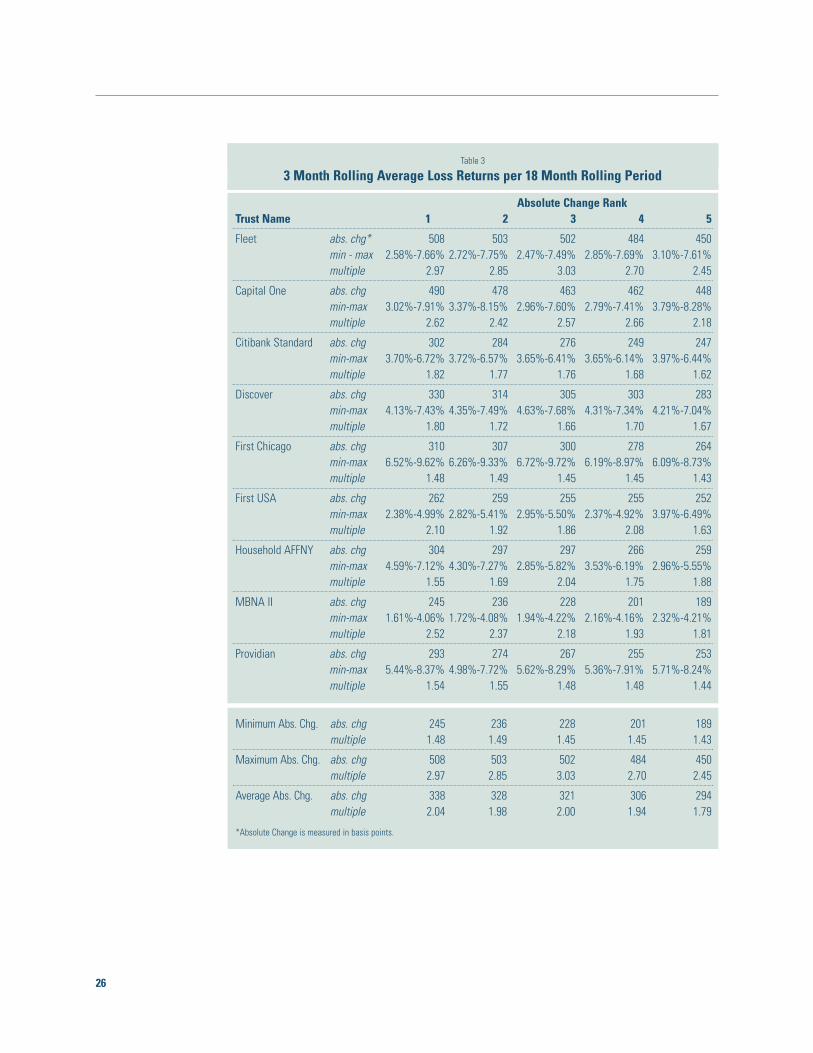

Standard & Poor’s uses ‘BBB’ loss guidelines that examine the historic performance

of securitized portfolios. Table 3 shows in basis points the absolute level of increase

for nine frequent issuers. This compares monthly loss data for each master trust for

18 months beginning in 1992 or since the trust’s inception if it was created after 1992.

The table shows the maximum increase in the three-month average charge-off rate

over the 18-month period.

In examining issuer-specific portfolio loss volatility, Standard & Poor’s evaluates

pool performance in a variety of ways. For example, one-month and three-month

average loss rate changes over rolling 12-, 18-, and 24-month periods were analyzed

for all bank card issuers. Table 3 shows each trust’s monthly loss rate percentages

compared on an 18-month rolling basis. Assume a master trust had an annualized

loss rate of 5% in January 1994 and an annualized loss rate of 7.5% in June 1995;

the absolute level of increase would be 250 basis points for that 18-month period

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

26

Table 3

3 Month Rolling Average Loss Returns per 18 Month Rolling Period

Absolute Change RankTrust Name 1 2 3 4 5

Fleet abs. chg* 508 503 502 484 450min - max 2.58%-7.66% 2.72%-7.75% 2.47%-7.49% 2.85%-7.69% 3.10%-7.61%multiple 2.97 2.85 3.03 2.70 2.45

Capital One abs. chg 490 478 463 462 448min-max 3.02%-7.91% 3.37%-8.15% 2.96%-7.60% 2.79%-7.41% 3.79%-8.28%multiple 2.62 2.42 2.57 2.66 2.18

Citibank Standard abs. chg 302 284 276 249 247min-max 3.70%-6.72% 3.72%-6.57% 3.65%-6.41% 3.65%-6.14% 3.97%-6.44%multiple 1.82 1.77 1.76 1.68 1.62

Discover abs. chg 330 314 305 303 283min-max 4.13%-7.43% 4.35%-7.49% 4.63%-7.68% 4.31%-7.34% 4.21%-7.04%multiple 1.80 1.72 1.66 1.70 1.67

First Chicago abs. chg 310 307 300 278 264min-max 6.52%-9.62% 6.26%-9.33% 6.72%-9.72% 6.19%-8.97% 6.09%-8.73%multiple 1.48 1.49 1.45 1.45 1.43

First USA abs. chg 262 259 255 255 252min-max 2.38%-4.99% 2.82%-5.41% 2.95%-5.50% 2.37%-4.92% 3.97%-6.49%multiple 2.10 1.92 1.86 2.08 1.63

Household AFFNY abs. chg 304 297 297 266 259min-max 4.59%-7.12% 4.30%-7.27% 2.85%-5.82% 3.53%-6.19% 2.96%-5.55%multiple 1.55 1.69 2.04 1.75 1.88

MBNA II abs. chg 245 236 228 201 189min-max 1.61%-4.06% 1.72%-4.08% 1.94%-4.22% 2.16%-4.16% 2.32%-4.21%multiple 2.52 2.37 2.18 1.93 1.81

Providian abs. chg 293 274 267 255 253min-max 5.44%-8.37% 4.98%-7.72% 5.62%-8.29% 5.36%-7.91% 5.71%-8.24%multiple 1.54 1.55 1.48 1.48 1.44

Minimum Abs. Chg. abs. chg 245 236 228 201 189multiple 1.48 1.49 1.45 1.45 1.43

Maximum Abs. Chg. abs. chg 508 503 502 484 450multiple 2.97 2.85 3.03 2.70 2.45

Average Abs. Chg. abs. chg 338 328 321 306 294multiple 2.04 1.98 2.00 1.94 1.79

*Absolute Change is measured in basis points.

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

27Standard & Poor’s Structured Finance � Credit Card Criteria

(a 50% increase or a 1.5x multiple). The issuer’s loss performance for other 18-month

periods, such as from February 1994 through July 1995, would be compared, and

so on. For each issuer in table 3, this 18-month rolling test was applied and the

top-five most volatile loss periods for each issuer are displayed.

In addition to the monthly loss rate history, Standard & Poor’s bases its expected

case steady-state loss rate on delinquency roll rate, vintage loss performance, and

lagged loss rate analysis. These analytical techniques help mitigate any distortions

due to recent account growth and provide insights into expected future performance.

In many cases, the expected steady-state loss rates are well above the historical average.

As a result, stressed loss rates are at considerably higher multiples compared with

historic averages.

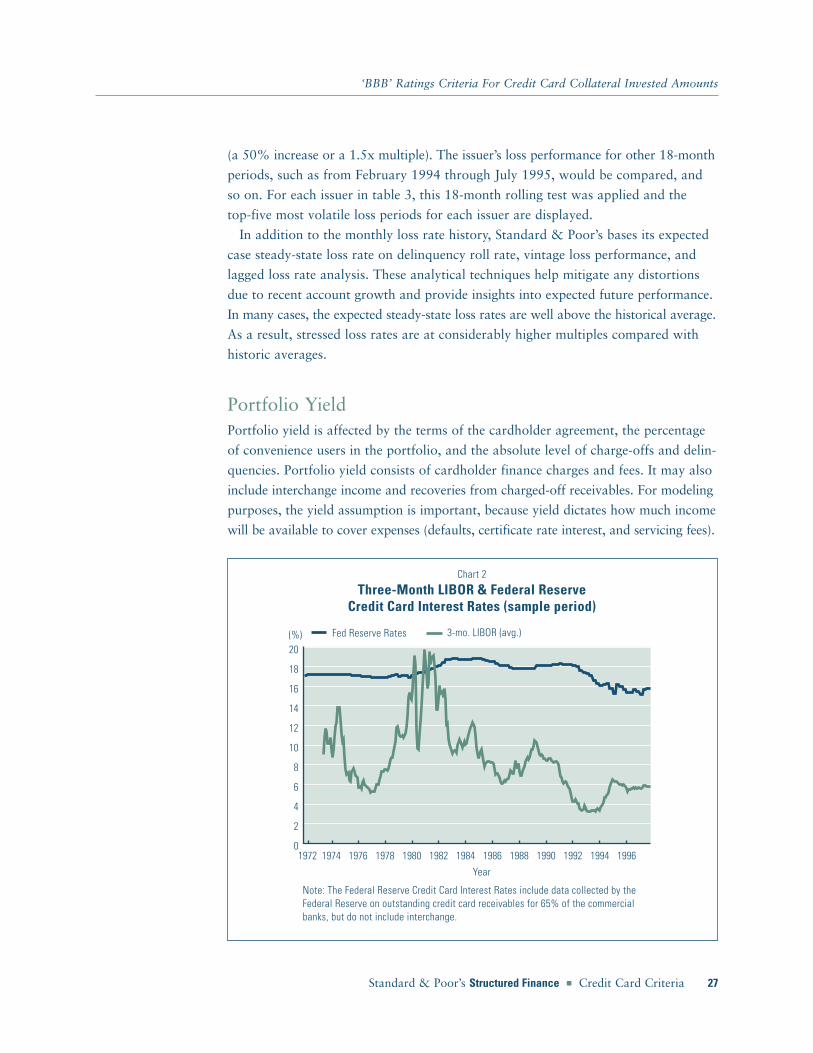

Portfolio YieldPortfolio yield is affected by the terms of the cardholder agreement, the percentage

of convenience users in the portfolio, and the absolute level of charge-offs and delin-

quencies. Portfolio yield consists of cardholder finance charges and fees. It may also

include interchange income and recoveries from charged-off receivables. For modeling

purposes, the yield assumption is important, because yield dictates how much income

will be available to cover expenses (defaults, certificate rate interest, and servicing fees).

1996199419921990198819861984198219801978197619741972

Chart 2

Three-Month LIBOR & Federal ReserveCredit Card Interest Rates (sample period)

Year

0

2

4

6

8

10

12

14

16

18

20(%) Fed Reserve Rates 3-mo. LIBOR (avg.)

Note: The Federal Reserve Credit Card Interest Rates include data collected by the Federal Reserve on outstanding credit card receivables for 65% of the commercial banks, but do not include interchange.

28

In the past, legislative proposals have been introduced to cap the amount of interest

a card issuer could charge. However, movement toward competitive floating-rate

products has mitigated the risk of a legislative cap. Nonetheless, due to the remote

possibility of a regulatory cap, as well as market competition that naturally exerts

downward pressure on portfolio yield, the yield on a portfolio is assumed to decline

in a stress scenario. In a ‘AAA’ scenario, the decline in yield is simultaneous with an

increase in losses. Although not always the case, yield in a ‘AAA’ case is typically

lowered to 11% or 12% and little credit is given to an issuer’s ability to reprice its

portfolio in this environment. However, at the ‘BBB’ level, analysts assume that if

the portfolio is well managed and nationally diverse, there would be less pressure on

price in a rising loss environment. The entire credit card industry would likely suffer

and price competition would abate, allowing issuers to raise APRs to offset higher

losses. For this reason, in a ‘BBB’ combined-stress scenario, yield is reduced to 75%

of its expected steady state over an 18-month period.

Chart 2 illustrates the industry-average credit card interest rates for a sample period.

Although the gap between credit card interest rates and three-month LIBOR has

remained quite healthy, there is a wide variance among issuers in their pricing, product

mix, and account solicitation strategies. As a result, portfolio yield differences among

issuers are significant. Analysts factor issuer-specific portfolio management strategies

into the assumptions used for cash flow modeling purposes.

Certificate RateFor fixed-rate transactions, the modeled input for the certificate rate is the actual

rate payable to certificateholders. For floating-rate transactions, however, the certificate

rate is assumed to increase over time. In floating-rate deals in which interest rate

caps are provided, interest rates are increased to the level of the cap.

The relationship between portfolio yield and the variable cost of funds is an

important factor in determining the level of excess spread for series with floating-rate

certificates. Since banks can reprice credit card accounts and the vast majority of

cards issued in recent years have had floating rates, the differential between portfolio

yield and certificate rate is assumed to be positive in a ‘BBB’ combined-stress scenario.

Standard & Poor’s arrived at its positive 3% to 5% net margin relationship by

comparing the relationship between the three-month London Interbank (LIBOR)

rate and the Federal Reserve credit card interest rates for one extended period

(see chart 2). Over this 15-year period, the greatest positive differential between the

credit card rate and LIBOR was 14.36% in September 1992, and the average difference

was 10.82%. Over this period, the gap between credit card yield and LIBOR never

dropped below 5%, with 6.52% in July 1984 as the lowest point.

‘BBB’ Ratings Criteria For Credit Card Collateral Invested Amounts

29Standard & Poor’s Structured Finance � Credit Card Criteria

In examining the three-month LIBOR rate and the Federal Reserve credit card

interest rate between June 1973 and August 1982, there are instances when the net

interest margin dipped below 5%. For much of the period of September 1979

through July 1982, the net interest margin was less than 5%, averaging just under

2.25%. During that time, there were nine months in which the indexes inverted.

Standard & Poor’s assumes that the likelihood of an inversion during a period of

rapidly rising loss rates and a declining portfolio yield (the ‘BBB’ combined-stress

scenario) is remote. The early 1980s was an unusual period when interest rates sky-

rocketed in reaction to the oil crisis. It is unlikely that the low level of net interest

margin observed then will be repeated. In addition, the credit card market and the

way it funds itself have evolved. LIBOR was not a widely traded index in the early

1980s and, consequently, was less liquid and more volatile. Furthermore, during that

time period, most bank card issuers did not borrow at the LIBOR rate. Instead,

since most issuers were full-service consumer banks, they relied primarily on consumer

deposits to fund their credit card businesses.

The cost of borrowing based on the federal rate for deposits was arguably lower

than LIBOR during the early 1980s. Since lenders did not borrow based on LIBOR,

they did not need to adjust yield and reprice portfolios to compensate for a rising

LIBOR-rate environment. At that time, virtually all credit card issuers offered the

same price to consumers: 19.8%. If the events of the early 1980s were repeated, it

would be reasonable to assume that originators would reprice their portfolios and

avoid a negative relationship between yield and certificate rate.

Although Standard & Poor’s thinks that it is unlikely that LIBOR and credit card

rates will invert in the future, it does not ignore that possibility when analyzing