credit card reward program in singapore – the consumers ...831326/fulltext01.pdf · school of...

TRANSCRIPT

School of Management Blekinge Institute of Technology

CREDIT CARD REWARD PROGRAM IN SINGAPORE: THE CONSUMERS’ CHOICE

By: Ng Hui Chen Ivy

Supervisor: Anders Hederstierna

Thesis for the Master’s degree in Business Administration

Spring 2009

Credit Card Reward Program in Singapore – The Consumers’ Choice

ii

ABSTRACT

The credit card market in Singapore is a concentrated one with local players and their

foreign counterparts all vying for a share of the local market. Card issuers are constantly

looking for new alternatives to attract new customers and entice existing ones to use their

cards. At the same time, consumers are demanding more value from their cards. It is no

longer sufficient for card issuers to compete on the basis of rates and charges alone. Reward

program has emerged to be one of the solutions to create further customer value.

Reward program has become so widespread that it is no longer considered a “bonus” to

credit card holders. Instead, it has evolved to become a “requirement” in their choice of

credit cards.

As the expectation of reward program rises, card issuers have to take a step further by not

only providing attractive rewards, but, customizing them to suit the different needs of their

customers. Issuers need to adopt a market-oriented strategy to understand customers’

needs and preferences and capture them into the type of rewards to provide.

The objective of this study is to explore the types of reward programs preferred by different

demographic groups in the Singapore context. Reward programs are classified into the

categories of “immediate rewards” versus “delayed rewards” as well as “monetary rewards”

versus “non-monetary rewards”. A questionnaire was designed as a means to collect the

primary data required. 179 respondents were involved.

The findings of the study revealed that Singapore females are more attracted by reward

programs as compared to Singapore males. In general, males prefer an immediate reward

rather than a delayed one. There is no strong correlation between age group and preference

for point accumulation program. Nor is there any strong correlation between income level

and preference for point accumulation program. Air miles accumulation is the least

preferred form of reward program among cardholders and cardholders in general are more

attracted to monetary rewards than non-monetary ones.

These results will be of interest for card issuers to further customise their reward programs

to suit the needs of their customers.

Credit Card Reward Program in Singapore – The Consumers’ Choice

iii

ACKNOWLEDGEMENTS

The completion of this thesis will not be possible without the support and contributions

by a large number of individuals.

Firstly, I would like to express my sincere gratitude to my supervisor, Anders

Hederstierna, for his invaluable support and guidance throughout the course of this

thesis. Without his advices and suggestions, the completion of this thesis will not be

possible.

My deepest appreciation goes to my family and friends for their constant

encouragements and assistance in helping to disseminate the questionnaire to a larger

group of respondents.

Also, I am grateful to all the respondents who had taken time off from their busy

schedules to complete the questionnaire.

Lastly, I would like give special thanks to my husband, Kenneth, for his unwavering

support and understanding throughout the course of this thesis.

Ivy Ng June 2009

Credit Card Reward Program in Singapore – The Consumers’ Choice

iv

TABLE OF CONTENTS

CHAPTER ONE: INTRODUCTION ..................................................................... 2

1.1 A BRIEF HISTORY ............................................................................................................... 2

1.2 THE RISE OF REWARD PROGRAM .......................................................................................... 3

1.3 MOTIVATION FOR RESEARCH TOPIC ...................................................................................... 3

1.4 OBJECTIVE OF STUDY ......................................................................................................... 4

1.5 OUTLINE OF ENTIRE THESIS ................................................................................................. 5

CHAPTER TWO: UNDERSTANDING SINGAPORE .............................................. 8

2.1 OVERVIEW OF SINGAPORE BANKING INDUSTRY ....................................................................... 8

2.2 OVERVIEW OF CREDIT CARD MARKET IN SINGAPORE................................................................. 9

2.3 SINGAPOREANS, THE MULTIPLE CARDHOLDERS ...................................................................... 11

2.4 CREDIT CARD REWARD PROGRAMS IN SINGAPORE ................................................................ 11

CHAPTER THREE: LITERATURE REVIEW ......................................................... 14

3.1 INTRODUCTION .............................................................................................................. 14

3.2 REWARD PROGRAM – THE DECIDING FACTOR ....................................................................... 14

3.3 DEFINITION OF REWARD PROGRAM .................................................................................... 16

3.4 OBJECTIVE OF REWARD PROGRAM...................................................................................... 16

3.5 CLASSIFICATION OF REWARDS AND REWARD PROGRAMS ......................................................... 17

3.6 CHOICE OF CREDIT CARD REWARD PROGRAM ........................................................................ 20

3.7 CONCEPTUAL MODEL ....................................................................................................... 21

3.7.1 Modified conceptual model ............................................................................................................ 21

3.7.2 Rationale for choice of conceptual model ....................................................................................... 23

3.7.3 Instant benefits – a type of reward program .................................................................................. 24

CHAPTER FOUR: RESEARCH METHODOLOGY ................................................ 27

4.1 INTRODUCTION .............................................................................................................. 27

4.2 RESEARCH DESIGN .......................................................................................................... 27

4.3 DATA COLLECTION .......................................................................................................... 28

4.4 DATA SOURCE ................................................................................................................ 29

4.5 SURVEY ........................................................................................................................ 30

4.6 QUESTIONNAIRE DESIGN .................................................................................................. 31

4.6.1 Organization of Questionnaire........................................................................................................ 31

4.6.2 Types of Measurement ................................................................................................................... 33

4.6.3 Multiple Indicators .......................................................................................................................... 33

4.6.4 Guidelines on Questionnaire Construction ...................................................................................... 35

4.6.5 Pre-test Conducted ......................................................................................................................... 35

4.7 SAMPLING ..................................................................................................................... 36

4.8 COLLATION OF RESPONSES ............................................................................................... 36

4.9 LIMITATION OF RESEARCH METHODOLOGY ........................................................................... 37

Credit Card Reward Program in Singapore – The Consumers’ Choice

v

CHAPTER FIVE: RESEARCH FINDINGS AND ANALYSIS .................................... 39

5.1 INTRODUCTION .............................................................................................................. 39

5.2 DEMOGRAPHIC PROFILES .................................................................................................. 39

5.2.1 Gender ............................................................................................................................................ 39

5.2.2 Age Group ....................................................................................................................................... 40

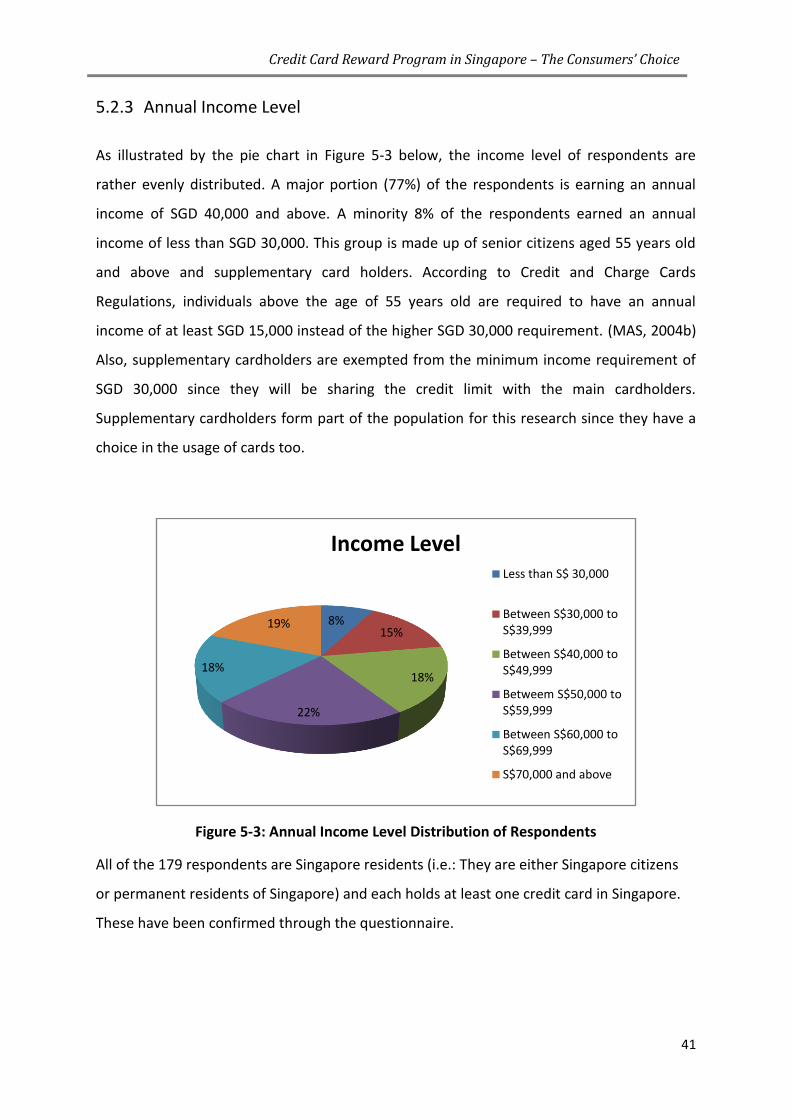

5.2.3 Annual Income Level ....................................................................................................................... 41

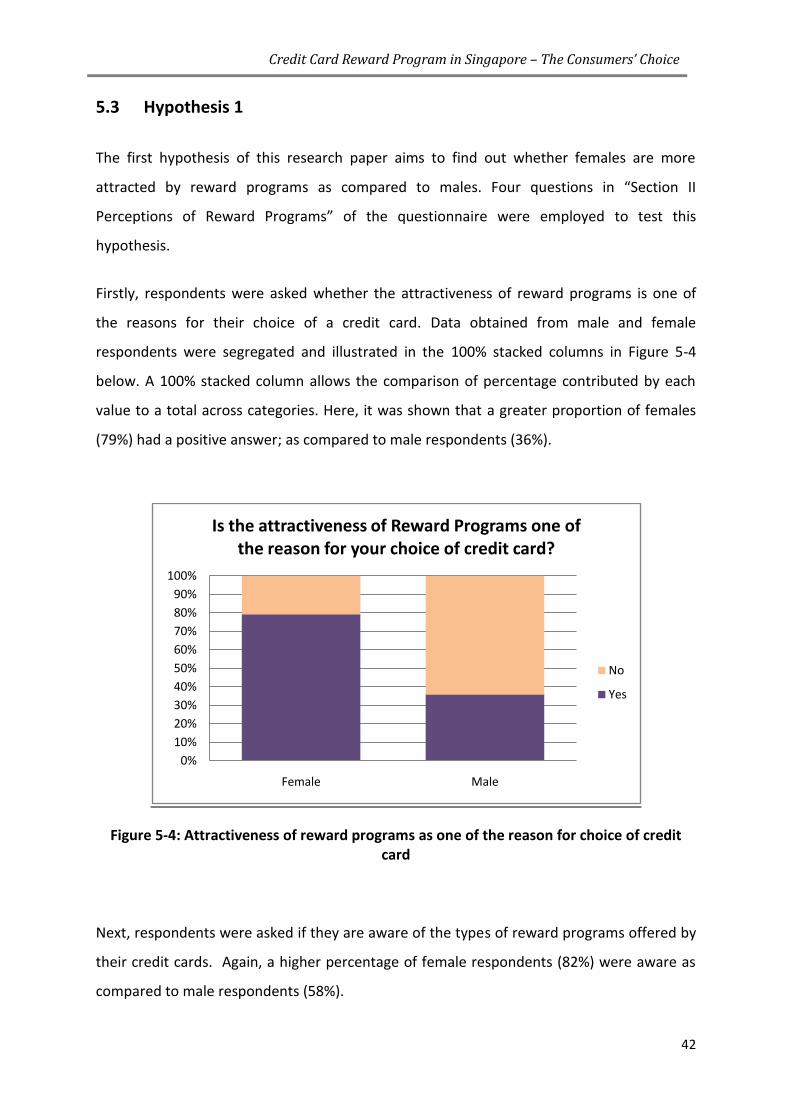

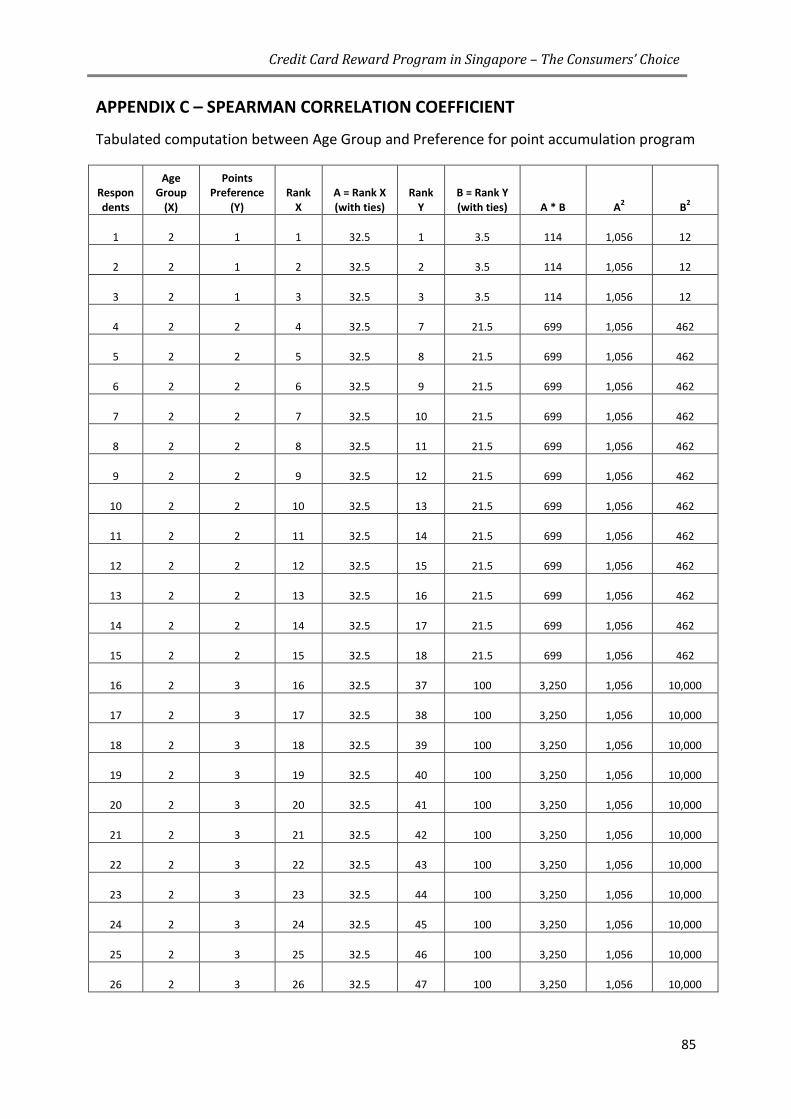

5.3 HYPOTHESIS 1 ................................................................................................................ 42

5.4 HYPOTHESIS 2 ................................................................................................................ 45

5.5 HYPOTHESIS 3 ................................................................................................................ 49

5.6 HYPOTHESIS 4 ................................................................................................................ 51

5.7 HYPOTHESIS 5 ................................................................................................................ 51

5.8 HYPOTHESIS 6 ................................................................................................................ 53

CHAPTER SIX: CONCLUSION ......................................................................... 57

6.1 SUMMARY AND FINDINGS ................................................................................................ 57

6.2 RECOMMENDATIONS ....................................................................................................... 58

6.3 AREAS FOR FURTHER RESEARCH ......................................................................................... 58

REFERENCES ................................................................................................. 61

APPENDICES ................................................................................................. 66

APPENDIX A – QUESTIONNAIRE ............................................................................................ 66

APPENDIX B – RESULTS OBTAINED FROM QUESTIONNAIRE ................................................ 71

APPENDIX C – SPEARMAN CORRELATION COEFFICIENT ....................................................... 85

Credit Card Reward Program in Singapore – The Consumers’ Choice

vi

LIST OF FIGURES

FIGURE 1-1: OUTLINE OF ENTIRE THESIS .............................................................................................. 6

FIGURE 2-1: NUMBER OF CREDIT AND CHARGE CARDS ISSUED IN SINGAPORE ............................................ 10

FIGURE 4-1: DIFFERENCES BETWEEN QUALITATIVE AND QUANTITATIVE APPROACH ..................................... 28

FIGURE 4-2 ORGANIZATION OF QUESTIONNAIRE ................................................................................. 31

FIGURE 5-1: GENDER DISTRIBUTION OF RESPONDENTS ......................................................................... 39

FIGURE 5-2: AGE GROUP OF RESPONDENTS ....................................................................................... 40

FIGURE 5-3: ANNUAL INCOME LEVEL DISTRIBUTION OF RESPONDENTS .................................................... 41

FIGURE 5-4: ATTRACTIVENESS OF REWARD PROGRAMS AS ONE OF THE REASON FOR CHOICE OF CREDIT CARD .. 42

FIGURE 5-5: AWARENESS OF TYPES OF REWARD PROGRAMS OFFERED BY CREDIT CARDS .............................. 43

FIGURE 5-6: UTILISATION OF REWARD PROGRAMS............................................................................... 43

FIGURE 5-7: TYPE OF REWARD PROGRAMS INFLUENCE CHOICE OF CARD TO USE DURING PURCHASE ............... 44

FIGURE 5-8: ORDER OF PREFERENCES FOR MALE RESPONDENTS ............................................................ 45

FIGURE 5-9: MALES RESPONDENTS WHO PREFER CASH REBATE DUE TO ITS HASSLE FREE NATURE .................. 46

FIGURE 5-10: MALE RESPONDENTS WHO DISLIKE CASH REBATE AS THEY CAN NEVER FIGURE HOW IT WORKS ... 47

FIGURE 5-11: MALE RESPONDENTS WHO SIGN UP FOR A CARD DUE TO ATTRACTIVE RETAIL DISCOUNTS .......... 48

FIGURE 5-12: MALE RESPONDENTS WHO HAVE REDEEMED THE POINTS WITHIN THE LAST 6 MONTHS............. 48

FIGURE 5-13: MALE RESPONDENTS WHO HAVE NOT BEEN REDEEMING DESPITE SUFFICIENT POINTS ............... 49

FIGURE 5-14: RANKING OF AIR MILES ACCUMULATION PROGRAM ........................................................... 52

FIGURE 5-15: RANKING ORDER OF 4 TYPES OF REWARD PROGRAMS ........................................................ 52

FIGURE 5-16: PREFERENCE BETWEEN CASH VOUCHERS AND PRODUCT REDEMPTIONS ................................. 53

FIGURE 5-17: APPEAL BETWEEN MONETARY AND NON-MONETARY REWARDS ........................................... 54

FIGURE 5-18: PREFERENCE OF MONETARY REWARDS TO NON-MONETARY ONES DUE TO ITS FLEXIBILITY ......... 55

Credit Card Reward Program in Singapore – The Consumers’ Choice

vii

LIST OF TABLES

TABLE 3-1: CLASSIFICATION OF REWARDS AND REWARD PROGRAMS ....................................................... 20

TABLE 3-2 PREFERENCE OF REWARDS BY US CONSUMERS..................................................................... 21

TABLE 3-3: MODIFIED FRAMEWORK FROM DOWLING & UNCLES (1997) AND BENAVENT & MEYER-WAARDEN

(2001). ............................................................................................................................... 22

Credit Card Reward Program in Singapore – The Consumers’ Choice

1

CHAPTER ONE

INTRODUCTION

Credit Card Reward Program in Singapore – The Consumers’ Choice

2

CHAPTER ONE: INTRODUCTION

1.1 A brief history

Consumer reward program began as early as 1896 in the United States. A company, founded

by Thomas Sperry and Shelly Hutchinson (S&H), came up with the idea of selling “stamps” to

merchants. (Simon, 2006) Merchants bought these stamps from S&H Company who in turn

gave them to their shoppers. These stamps, also known as “S&H Green Stamps” acted as

rewards for customers. The more the customers purchased, the more stamps they were

awarded. With sufficient accumulation of stamps, customers were allowed to redeem for

merchandise from a catalogue or from the local Green Stamps store. Each item listed in the

catalogue or in the Green Stamps store was assigned a value in terms of the number of

stamps required. This almost resembles today’s point accumulation program, only with the

advancement from the use of stamps to electronic points. S&H Green Stamps continued its

popularity in the next few decades.

By the 1960s, such trading stamps became so popular that major supermarket chains such

as Tesco joined the bandwagon too. (Tesco PLC, 2009)

By the 1980s, airlines started to adopt reward program that awarded customers with air

miles points. American Airlines, the first mover in the airline industry, introduced the

AAdvantage Programme in 1981. (O’Malley, 1998)

A few years later, the credit card industry followed this trend. 1986 marked the birth of the

credit card reward program. (Discover Financial Services, 2009) The “Discover Card”

introduced a cash back reward program. Cash rebates were granted to customers at the end

of each year based on the amount spent using the card.

Reward program has now emerged to be an important marketing tool used by retailers in

different industries.

Credit Card Reward Program in Singapore – The Consumers’ Choice

3

1.2 The rise of reward program

Before the introduction of reward program, credit card issuers compete among themselves

on the basis of rates and charges. Annual membership fee and interest charged for late

payments were lowered in order to gain a larger share of the market.

However, as competition increases and the market become more concentrated, card issuers

are looking for new alternatives to attract new customers and entice existing ones to use

their cards. Reward program become the solution. Card issuers started to develop the best

reward program to attract consumers.

Reward program has become so widespread that it is no longer considered a “bonus” to

cardholders. Instead, it has evolved to become a “requirement” in their choice of credit

cards.

As the expectation of reward program rises, card issuers have to take a step further by not

only providing attractive rewards, but, customizing the reward programs to suit the

different needs of their customers. Issuers need to adopt a market-oriented strategy to

understand customers’ needs and preferences and capture them into the type of rewards to

provide.

1.3 Motivation for research topic

Singapore’s banking industry has become a concentrated one since the implementation of

the 5 years liberalisation programme. The three local players, namely Development Bank of

Singapore, Overseas Chinese Banking Corporation and United Overseas Bank; together with

their foreign counterparts (including Citibank, Standard Chartered Bank, Hong Kong

Shanghai Banking Corporation etc) were all vying for a share of the local market.

In order to ensure sustainability and remain competitive in the long run, it is essential for

the players to understand what the customer wants. It is only through value creation and

Credit Card Reward Program in Singapore – The Consumers’ Choice

4

satisfaction of their needs that banks can retain customers, attract new ones and build

customer loyalty.

It is usual for a Singaporean to be a multiple card holder. However, they might not be

spending equally on all cards. Most of the Singaporeans will tend to accumulate their

spending on one “preferred” card while the rest of the cards are held for various purposes.

Accumulating spending on a single card not only allows an easy and convenient bill payment

process, it also allows cardholders to be able to maximise their reward points to achieve

higher value redemptions.

Credit cards are a major source of revenue for banks in the consumer credit sector. With

such intense competition, in order for a credit card to be “top of the wallet”, card issuers

have to understand the main deciding factor that influences the consumers’ choice of a

“preferred” card.

Previous researches have been conducted in this area and most of which conclude that the

reward program is an important consideration.

In this research paper, I will go a step further to complement prior research by exploring the

preferences of different demographic groups in the types of reward programs.

This will enable banks to adopt the right marketing strategy to attract customers, entice

them to spend on their cards and consequently, obtain a larger market share and revenue

income.

1.4 Objective of study

The objective of this research paper is to investigate the cardholder’s preference towards

the types of reward programs in the Singapore credit card market.

Specifically, the following hypotheses will be tested and analysed.

Hypothesis 1: Females are more attracted by reward programs as compared to males.

Credit Card Reward Program in Singapore – The Consumers’ Choice

5

Hypothesis 2: Males prefer an immediate reward program to a delayed reward program.

Hypothesis 3: There is a strong correlation between preference for point accumulation

program and age group.

Hypothesis 4: There is a strong correlation between preference for point accumulation

program and income level.

Hypothesis 5: Out of the 4 types of reward programs namely cash rebates, instant benefits,

point accumulation and air miles accumulation; air miles accumulation is the least preferred

among cardholders.

Hypothesis 6: Cardholders are more attracted to monetary rewards than non-monetary

rewards regardless of demographic groups.

1.5 Outline of entire thesis

This research paper is organized into six chapters.

The first chapter provides a background of the reward program, which includes a brief

history as well as how reward program rose to its important status today. It also outlines

the main motivation behind this research paper and the objectives it aims to achieve.

The second chapter introduces the readers to an overview of the Singapore banking

industry and in particular, the credit card market. It also provides an understanding of the

multiple cardholder behaviour in Singapore. The various types of credit card reward

programs available in Singapore will be discussed as well.

The third chapter examines the various previous researches that had been performed in this

area. A conceptual framework will be developed for the current research with insights from

the literature review. Rationale for the choice of conceptual framework will be explained

here.

Credit Card Reward Program in Singapore – The Consumers’ Choice

6

The fourth chapter elaborates on the type of research design adopted as well as the

research methods used. Data collection consisting of both primary and secondary data will

be explained. The type of sampling method and questionnaire design will also be discussed

here. A limitation of the research methodology adopted will be analysed.

Chapter five brings us to evaluate and analyse the research findings obtained.

Chapter six concludes the report with major findings. Recommendations from the current

research, as well as areas for further research will be highlighted here.

Figure 1-1 below illustrates the flow of the thesis.

Figure 1-1: Outline of entire thesis

1 • INTRODUCTION

2 • UNDERSTANDING SINGAPORE

3 • LITERATURE REVIEW

4 • RESEARCH METHODOLOGY

5 • RESEARCH FINDINGS AND ANALYSIS

6 • CONCLUSION

Credit Card Reward Program in Singapore – The Consumers’ Choice

7

CHAPTER TWO

UNDERSTANDING

SINGAPORE

Credit Card Reward Program in Singapore – The Consumers’ Choice

8

CHAPTER TWO: UNDERSTANDING SINGAPORE

2.1 Overview of Singapore banking industry

Singapore, the smallest nation in South-East Asia, has a land area of 710.2km2. (Singapore

Department of Statistics, 2008) Despite being small, it is renowned as a leading Asia

Financial Hub since the last decade with its politically stable environment, strong economic

fundamentals, a well developed physical and financial infrastructure as well as a strategic

geographical and time zone location. (Hew, 2002)

Since the Asia Economic Crisis that took place in 1997, the Singapore government saw a

need for further consolidation of the local banks in order to stay competitive. From a speech

by Mr Lim Hng Kiang, Deputy Chairman of Monetary Authority of Singapore (MAS), the crisis

is a clear signal that the financial services sector is a global industry. (MAS, 2002) Small

banks are no longer able to compete with the larger international banks. As Singapore’s

Prime Minister Mr Lee Hisen Loong puts it in a ministerial statement on July 2001, “the

industry is characterized by large economies of scale”. Only large banks will have sufficient

resources to compete in this globalised environment.

In May 1999, MAS announced a five year programme to liberalise access by foreign banks

into the domestic banking industry. (MAS Annual Report 2000/2001) The main objective is

to enhance the competitiveness of the banking industry, and to encourage domestic banks

to develop and strengthen their capabilities in the face of fiercer and more aggressive

competition from the bigger foreign players.

The first phase commenced in 1999, over a period of 3 years. It involved granting new

banking privileges and new licences for foreign banks.

A new category of licence known as the “Qualifying Full Bank” was introduced, number of

“Restricted Bank” licences was increased and “Qualifying Offshore Bank” privileges were

granted to approved offshore banks. (MAS, 2001)

Credit Card Reward Program in Singapore – The Consumers’ Choice

9

The first phase of the five year programme was phased in progressively, allowing time for

the local banks to upgrade themselves and at the same time ensure financial stability of the

Singapore financial system. (MAS, 2001)

The industry adjusted well to the new environment and a series of consolidation took place

from 1998 to 2001. The seven local banking groups consolidated to become today’s three

local players, namely Development Bank of Singapore, Overseas Chinese Banking

Corporation and United Overseas Bank. (MAS, 2004a)

Phase two started in June 2001, which included expanding existing privileges of Qualifying

Full Banks. More Qualifying Full Banks status was granted too. The Restricted Bank licence

ceased and was replaced by the “Wholesale Bank” licence to reflect the more privileges and

wider range of banking activities that it could undertake. All Qualifying Offshore Banks and

Offshore Banks were being upgraded to Wholesale Bank over time. (MAS, 2001)

The liberalization further enhanced Singapore’s role as an international financial centre.

2.2 Overview of credit card market in Singapore

MAS act as the central bank of Singapore. It is responsible for the financial supervision as

well as the financial development of Singapore which includes the conduct of monetary

policy, the issuance of currency as well as establishment of various statutes such as the

Banking Act to govern the banking industry. (MAS Annual Report 2007/2008)

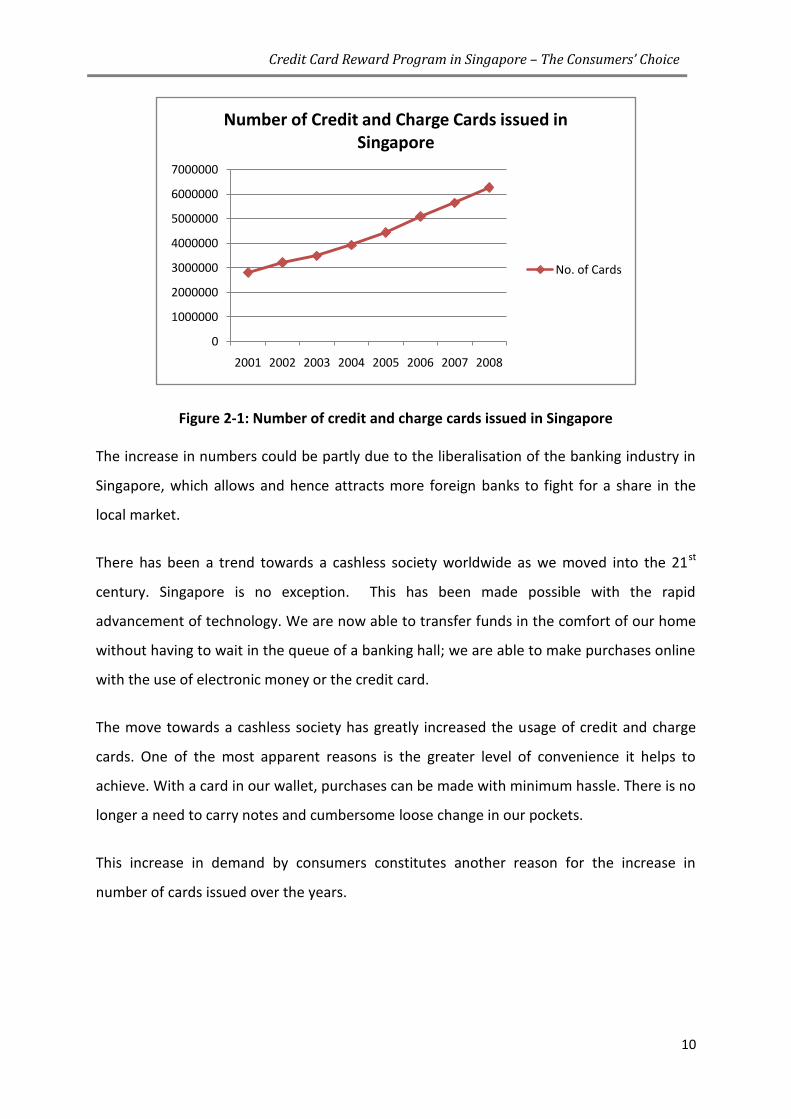

According to MAS Credit and Charge Card Statistic (MAS, 2009), over the past 8 years, the

total number of cards issued in Singapore, which includes both the main cards as well as the

supplementary cards, has been increasing. As of 2001, the total number of cards issued was

2,813,989. By the end of 2008, this figure has risen to 6,277,915. (MAS, 2009) The number

of cards issued has increased by more than 120% within the last 8 years!

Credit Card Reward Program in Singapore – The Consumers’ Choice

10

Figure 2-1: Number of credit and charge cards issued in Singapore

The increase in numbers could be partly due to the liberalisation of the banking industry in

Singapore, which allows and hence attracts more foreign banks to fight for a share in the

local market.

There has been a trend towards a cashless society worldwide as we moved into the 21st

century. Singapore is no exception. This has been made possible with the rapid

advancement of technology. We are now able to transfer funds in the comfort of our home

without having to wait in the queue of a banking hall; we are able to make purchases online

with the use of electronic money or the credit card.

The move towards a cashless society has greatly increased the usage of credit and charge

cards. One of the most apparent reasons is the greater level of convenience it helps to

achieve. With a card in our wallet, purchases can be made with minimum hassle. There is no

longer a need to carry notes and cumbersome loose change in our pockets.

This increase in demand by consumers constitutes another reason for the increase in

number of cards issued over the years.

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

2001 2002 2003 2004 2005 2006 2007 2008

Number of Credit and Charge Cards issued in Singapore

No. of Cards

Credit Card Reward Program in Singapore – The Consumers’ Choice

11

2.3 Singaporeans, the multiple cardholders

According to the Singapore Department of Statistics (2009), Singapore has a population of

4.84 million as of June 2008. Singapore residents, comprising of both Singapore citizens and

permanent residents, make up 3.64 million of the total population. Out of the 3.64 million

of Singapore residents, 2.71 millions are within the age group of 20 and above.

It was mentioned in Section 2.2 that the total number of credit and charge card issued as at

the end of 2008 was approximately 6.3 million. Comparing this statistic with Singapore

residents aged 20 and above, it can be estimated that an average cardholder in Singapore

holds more than one credit card. This is further supported by a previous research performed

by Gan et al. (2008). According to their sample size of 636 cardholders in Singapore, the

mean number of credit cards held by each cardholder is 2.27.

Major card issuers in Singapore include the three local banks; Development Bank of

Singapore, United Overseas Bank, Overseas Chinese Banking Corporation and international

players such as Citibank, Standard Chartered Bank, Hong Kong Shanghai Banking

Corporation, as well as Maybank, Bank of China and The Royal Bank of Scotland.

Each of these banks offers more than one credit card to suit the different needs and

preferences of its customers. With the wide variety of cards to choose from, it is of no

surprise that an average Singaporean has more than one plastic in their wallet.

However, the intent to hold the cards differs. Some people increase their arsenal of plastic

in order to take full advantage of any retail privileges that he or she may chance upon.

Others may hold it to increase their unsecured credit limit. Whatever the reason, card

issuers are constantly faced with a never-ending challenge to make their card the top choice

in consumers’ limited wallet space.

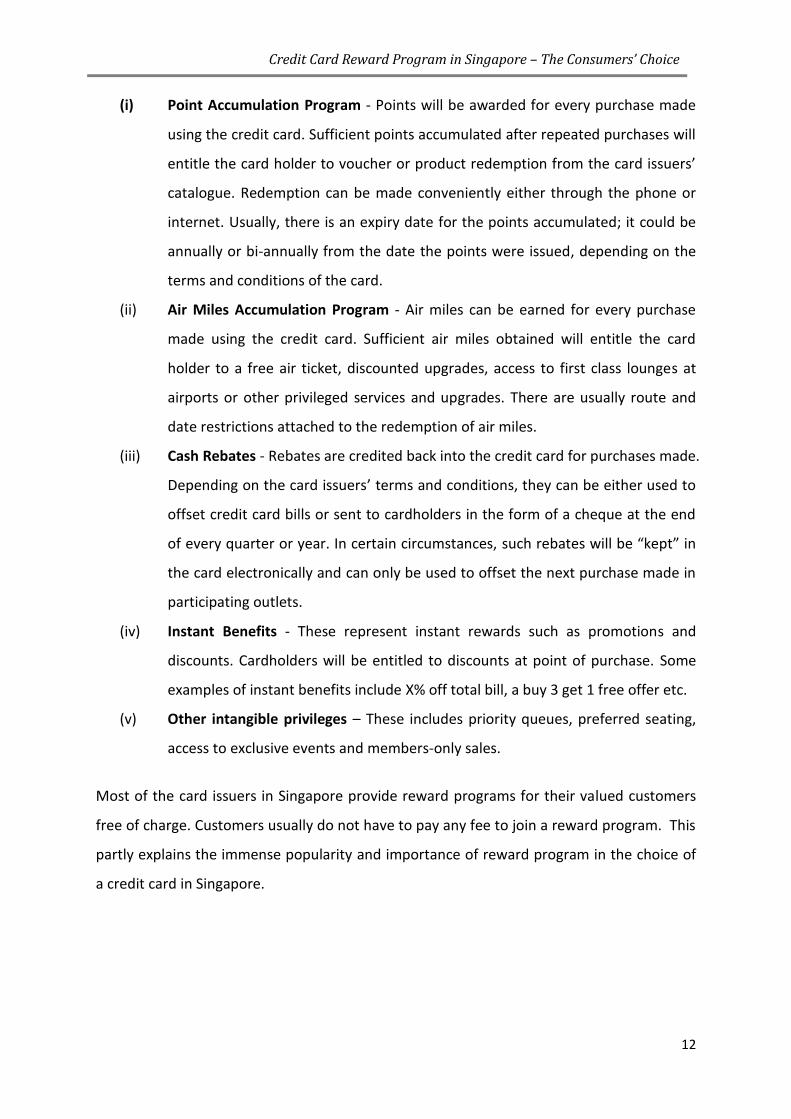

2.4 Credit Card Reward Programs in Singapore

The more common credit card reward programs offered by the various card issuers in

Singapore consist of the following:

Credit Card Reward Program in Singapore – The Consumers’ Choice

12

(i) Point Accumulation Program - Points will be awarded for every purchase made

using the credit card. Sufficient points accumulated after repeated purchases will

entitle the card holder to voucher or product redemption from the card issuers’

catalogue. Redemption can be made conveniently either through the phone or

internet. Usually, there is an expiry date for the points accumulated; it could be

annually or bi-annually from the date the points were issued, depending on the

terms and conditions of the card.

(ii) Air Miles Accumulation Program - Air miles can be earned for every purchase

made using the credit card. Sufficient air miles obtained will entitle the card

holder to a free air ticket, discounted upgrades, access to first class lounges at

airports or other privileged services and upgrades. There are usually route and

date restrictions attached to the redemption of air miles.

(iii) Cash Rebates - Rebates are credited back into the credit card for purchases made.

Depending on the card issuers’ terms and conditions, they can be either used to

offset credit card bills or sent to cardholders in the form of a cheque at the end

of every quarter or year. In certain circumstances, such rebates will be “kept” in

the card electronically and can only be used to offset the next purchase made in

participating outlets.

(iv) Instant Benefits - These represent instant rewards such as promotions and

discounts. Cardholders will be entitled to discounts at point of purchase. Some

examples of instant benefits include X% off total bill, a buy 3 get 1 free offer etc.

(v) Other intangible privileges – These includes priority queues, preferred seating,

access to exclusive events and members-only sales.

Most of the card issuers in Singapore provide reward programs for their valued customers

free of charge. Customers usually do not have to pay any fee to join a reward program. This

partly explains the immense popularity and importance of reward program in the choice of

a credit card in Singapore.

Credit Card Reward Program in Singapore – The Consumers’ Choice

13

CHAPTER THREE

LITERATURE REVIEW

Credit Card Reward Program in Singapore – The Consumers’ Choice

14

CHAPTER THREE: LITERATURE REVIEW

3.1 Introduction

There have been various studies conducted in the area of credit cards selection criteria in

Singapore and worldwide. The topic on reward program, as a loyalty marketing tool, has

also been widely discussed in different industry contexts. However, little has been published

specifically in the area of credit card reward program. This research aims to close this gap by

analysing the types of reward programs preferred by the different demographic groups in

Singapore.

In this chapter, I will begin with a review of the importance of reward program in the choice

of a credit card. This will be followed by how different researchers define reward program

and its main objectives. The different classification of reward programs will be examined

and evaluated. A conceptual model will be developed based on insights obtained from the

literature review. Lastly, rationale for the choice of a conceptual model will be explained.

3.2 Reward program – The deciding factor

The importance of reward program cannot be undermined. With a superior reward program,

card issuers are more able to position itself as “top of the wallet”. Reward program is one of

the factors influencing the choice of a credit card; it is also a deciding factor among multiple

cardholders in the choice of their “preferred” card. This is supported by various studies.

Gan et al. (2008) cited a report by Visa International (2004) that the main reason for a

Singaporean to hold multiple credit cards is to benefit from the different discounts,

promotions and privileges offered by the different cards. It was also mentioned by the

authors that studies (Carow & Staten, 1999; Schlossberg 1998; Stavins, 1996) from United

States found that rebates and rewards were the major reasons for consumers to use their

credit cards.

Credit Card Reward Program in Singapore – The Consumers’ Choice

15

Devlin et al.(2007) examined the reasons why multiple cardholders have a “main” card that

is frequently used, and “subsidiary” cards to which they use less often or perhaps only

during emergency. The most frequently stated reason from the research among Singapore

cardholders was “to take advantage of the various discounts and promotions the card issuer

had made available, which are considered to be more superior to those offered by other

issuers.” The second most frequently listed reason was “a better reward program offered by

the card issuer.”

In a study conducted by Gan and Maysami (2006), “promotional factor” is considered the

fourth most important criteria in the choice of a credit card in Singapore. Within the

variables under the promotional factor, “loyalty and reward programs” ranked the highest,

and this was followed by “special discounts in selected outlets”.

Wee (2006) cited that according to the telecast of the Big Picture by Channel New Asia, the

services provided by the card issuers as well as the attractiveness of the reward program are

the key factors that entice consumers to sign up for a credit card and utilise it. In addition,

research performed by Wee (2006) revealed that discounts tied up with retail merchants

and attractive reward programs are reasons frequently cited by Singapore women that

attracted them to sign up for a Lady’s or Women’s card, enticed them to spend on it and

retained the card.

A consumer loyalty survey was conducted by First Data Competitive Intelligence with over

1,000 US consumers in July 2008. It was found that a majority of these consumers were

members of credit card reward program. And most of them indicated that reward program

membership influenced their choice of card to use.

According to a consumer credit card program study conduct by TNS Global (a market

research firm) between August to November 2008, reward program was a significant

consideration in many of the US customers’ decisions involving credit cards. These included

their acquisition and usage considerations. A reward card is often the “primary” card and

the card that constitute the “top of the wallet” status.

Credit Card Reward Program in Singapore – The Consumers’ Choice

16

Similar surveys were conducted in Singapore in 2007 by Gow et al. (2008) published in The

Business Times, a Singapore Local Newspaper. Discounts and promotions were deemed to

be the second most important factor in the choice of a credit card.

3.3 Definition of reward program

Reward Program is also commonly known as Loyalty Program or Frequency Program.

Various definitions have been provided by researchers. According to Sharp and Sharp (1997),

“loyalty programs are structured marketing efforts that reward, and therefore, encourage,

loyal buying behaviour”.

It is a promotional tactic used by firms to enhance customer loyalty through the provision of

incentives to customers who made repeated purchases. (Kim et. al, 2001)

Johnson (1998) had similar views. He defined a loyalty program as “any marketing program

that is designed to increase the lifetime value of current customers through a long-term

interactive relationship.”

Kivetz and Simonson (2002) described a frequency program as a “form of marketing tool to

retain customers and increasing their level of usage of product and services.”

3.4 Objective of reward program

Reward programs are introduced for various objectives.

According to Dowling and Uncles (1997), there are three main objectives of a reward

program.

Firstly, it can be seen as a defensive marketing strategy to sustain current sales level and

prevent customer from switching to competitors that might led to erosion of market share.

Reward program can be used to increase the switching cost of customers since points and

Credit Card Reward Program in Singapore – The Consumers’ Choice

17

rewards accumulated will be forgone when a customer choose to switch to a competitor. In

short, a reward program seeks to “lock in” existing customers.

Secondly, it can also be seen as an offensive marketing strategy to increase the share of the

pie in the market. By developing customer loyalty, firms that adopt reward programs are

able to increase their profitability via increased and repeated purchases made by existing

customers.

Lastly, it can also be seen as a tactic that leads to cross selling to existing customers.

O’Malley (1998) also established several objectives of a reward program.

According to O’Malley, reward program is often used as a tool to generate information

regarding customers’ buying behaviour, preferences and lifestyles. Such information is

useful in helping retailers to segment their target markets and customise offers to better

serve their valued customers.

Although the main stated reason for reward program is to reward loyal customers, the

underlying motive could be to manipulate the buying behaviour of customers. Discounts

and promotions (such as buy 3 get 1 free while stock last or a 20% discount off total bill for a

specified period) can be seen as a tacit to increase the current purchases made by

customers. Lastly, O’Malley also stated that reward program is used as a defensive strategy

to combat competitors move.

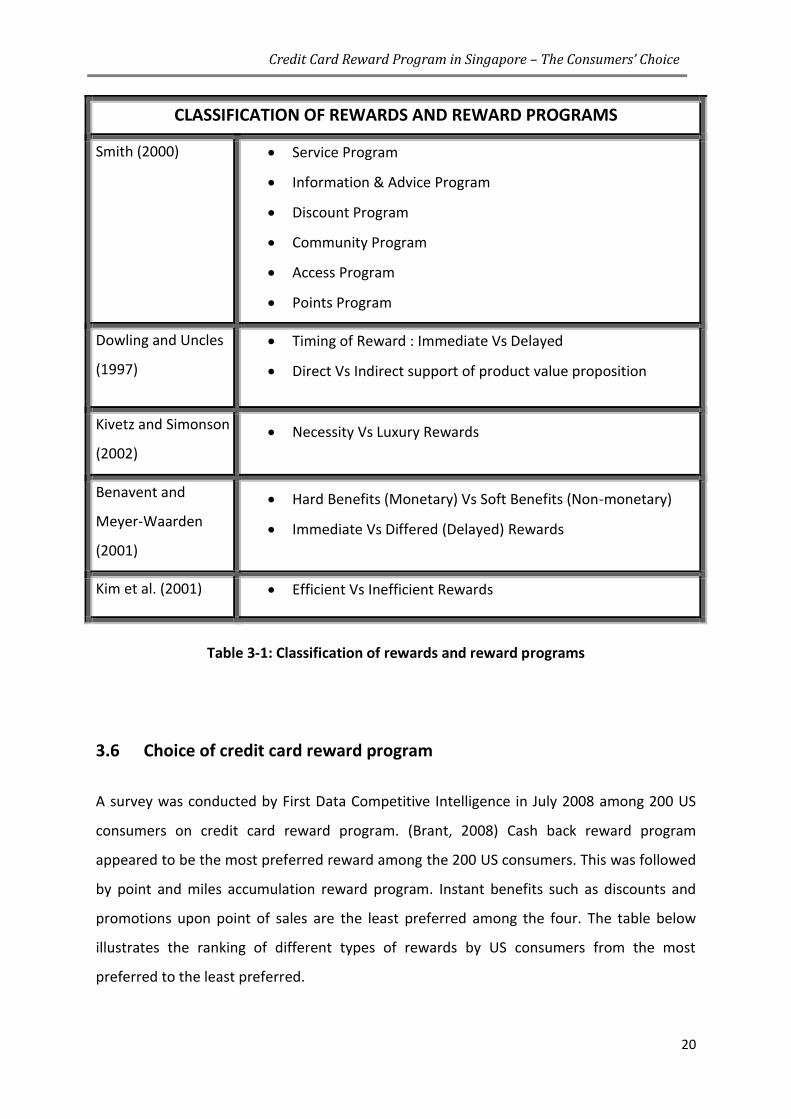

3.5 Classification of rewards and reward programs

Gillies et al. (2005) cited Smith (2000) who distinguishes six different types of loyalty

program.

(i) Service Program – One that provides VIP services to its value customers. Such as

offering priority queues and access to first class lounges at airports.

(ii) Information and Advice Program – One that uses information and advice to

enhance a product experience.

Credit Card Reward Program in Singapore – The Consumers’ Choice

18

(iii) Discount Program – One that offers members-only discounts.

(iv) Community Program – One that gets customers to interact among themselves.

(v) Access Program – One that provides customers with access to exclusive events.

(vi) Points Program – One that grants points to customer upon purchases made

which can be accumulated for future redemption.

Dowling and Uncles (1997) advocate that the attractiveness of a reward program not only

depends on the value of the rewards, it also depends on the timing of the reward. Rewards

can either be immediate or delayed. An immediate reward occurs at the point of purchase,

whereas a delayed one occurs after reaching a certain number of purchases or accumulation

of points. According to the authors, an immediate reward is often preferred.

This is further supported by Jang and Mattila (2005) who cited previous work by Bootzin et

al. (1991) who suggested that delayed redemption reduces the motivational power of

loyalty rewards.

Dowling and Uncles (1997) also classify rewards according to whether they directly support

the product’s value proposition. The authors consider rewards that directly support the

product’s value proposition to be more able to develop customer loyalty towards the

product or brand and not simply towards the reward program.

Kivetz and Simonson (2002) conducted a research to find out the effect of program

requirement on customer preference between necessity and luxury rewards. It was found

that customers preferred luxury rewards to a necessity one the higher the program

requirement.

Benavent and Meyer-Waarden (2001) differentiate rewards on the basis of whether they

are soft or hard benefits. Hard benefits refer to purely financial and tangible rewards. Soft

benefits are intangible rewards such as private sales, priority queue and other privileged

services. The authors define hard benefits as monetary rewards while soft benefits were

referred to as non-monetary ones.

Jang and Mattila (2005) had similar classification. They conducted two focus group

interviews with graduate students in hospitality management as well as constructed a

Credit Card Reward Program in Singapore – The Consumers’ Choice

19

questionnaire with 145 respondents to test the preference between monetary and non-

monetary rewards in the restaurant industry context. It was revealed that monetary reward

is the preferred choice due to its convenience and flexibility. The authors also tested the

respondents’ preference between immediate and delayed rewards as well as between

necessity and luxury rewards. Results from the study indicated that consumers preferred

immediate rewards to delayed ones. Also, a vast majority of the respondents preferred

necessary rewards to luxury rewards. It was noted that their preference for luxury rewards

increased with a higher level of effort requirement.

Kim et al. (2001) refer to two different types of rewards, efficient and inefficient rewards. A

reward is considered inefficient if it results in higher unit reward cost for the offering firm.

An example will be a cash reward. On the other hand, a free product of the firm, such as an

air ticket for an airline company will be considered an efficient reward.

Table 3-1 summarises the key classifications of rewards and reward programs provided by

the various researchers.

Credit Card Reward Program in Singapore – The Consumers’ Choice

20

CLASSIFICATION OF REWARDS AND REWARD PROGRAMS

Smith (2000) Service Program

Information & Advice Program

Discount Program

Community Program

Access Program

Points Program

Dowling and Uncles

(1997)

Timing of Reward : Immediate Vs Delayed

Direct Vs Indirect support of product value proposition

Kivetz and Simonson

(2002)

Necessity Vs Luxury Rewards

Benavent and

Meyer-Waarden

(2001)

Hard Benefits (Monetary) Vs Soft Benefits (Non-monetary)

Immediate Vs Differed (Delayed) Rewards

Kim et al. (2001) Efficient Vs Inefficient Rewards

Table 3-1: Classification of rewards and reward programs

3.6 Choice of credit card reward program

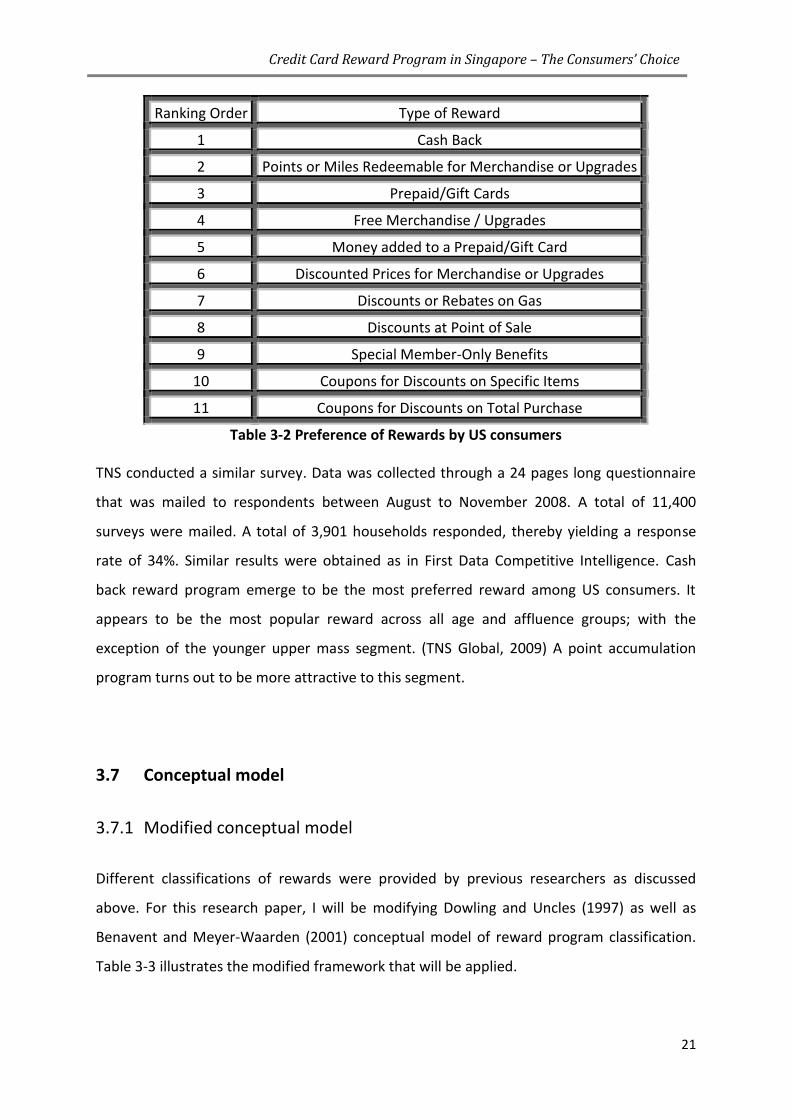

A survey was conducted by First Data Competitive Intelligence in July 2008 among 200 US

consumers on credit card reward program. (Brant, 2008) Cash back reward program

appeared to be the most preferred reward among the 200 US consumers. This was followed

by point and miles accumulation reward program. Instant benefits such as discounts and

promotions upon point of sales are the least preferred among the four. The table below

illustrates the ranking of different types of rewards by US consumers from the most

preferred to the least preferred.

Credit Card Reward Program in Singapore – The Consumers’ Choice

21

Ranking Order Type of Reward

1 Cash Back

2 Points or Miles Redeemable for Merchandise or Upgrades

3 Prepaid/Gift Cards

4 Free Merchandise / Upgrades

5 Money added to a Prepaid/Gift Card

6 Discounted Prices for Merchandise or Upgrades

7 Discounts or Rebates on Gas

8 Discounts at Point of Sale

9 Special Member-Only Benefits

10 Coupons for Discounts on Specific Items

11 Coupons for Discounts on Total Purchase

Table 3-2 Preference of Rewards by US consumers

TNS conducted a similar survey. Data was collected through a 24 pages long questionnaire

that was mailed to respondents between August to November 2008. A total of 11,400

surveys were mailed. A total of 3,901 households responded, thereby yielding a response

rate of 34%. Similar results were obtained as in First Data Competitive Intelligence. Cash

back reward program emerge to be the most preferred reward among US consumers. It

appears to be the most popular reward across all age and affluence groups; with the

exception of the younger upper mass segment. (TNS Global, 2009) A point accumulation

program turns out to be more attractive to this segment.

3.7 Conceptual model

3.7.1 Modified conceptual model

Different classifications of rewards were provided by previous researchers as discussed

above. For this research paper, I will be modifying Dowling and Uncles (1997) as well as

Benavent and Meyer-Waarden (2001) conceptual model of reward program classification.

Table 3-3 illustrates the modified framework that will be applied.

Credit Card Reward Program in Singapore – The Consumers’ Choice

22

Type of Rewards Immediate Reward Delayed Reward

Monetary Reward Instant Benefits : Discounts and

Promotions

Cash Rebates

Point Accumulation : Redemption

of Cash Vouchers

Non-monetary

Reward

Priority Queues, Privileged Services,

Exclusive member-only sales

events, preferred Seating.

Point Accumulation : Redemption

of Products / Merchandise

Air Miles Accumulation: Access to

First Class Lounges at airports, free

upgrades.

Table 3-3: Modified framework from Dowling & Uncles (1997) and Benavent & Meyer-

Waarden (2001).

The various credit card reward programs offered by card issuers in Singapore have been

further broken down into the classification of “Immediate Vs Delayed Rewards” and

“Monetary Vs Non-Monetary Rewards” in Table 3-3 above.

For this research paper, monetary rewards will be defined as rewards that can be expressed

in financial value reliably and accurately with certain degree of flexibility in usage. These

include cash rebates, discounts, product cash vouchers and lucky draws with monetary

prizes.

Non-monetary rewards will be defined as rewards that cannot be expressed in financial

value reliably and accurately. These include priority queue, preferred seating, privileged

services such as access to first class lounges at airports, product redemptions, and lucky

draws with merchandise such as car, an air ticket or a hotel stay as a prize.

Credit Card Reward Program in Singapore – The Consumers’ Choice

23

3.7.2 Rationale for choice of conceptual model

The main motivation behind this research paper is to help card issuers find out more about

the preference of reward programs among cardholders, hence, a customer-oriented

approach to classify reward programs will be employed. The classification adopted by Kim et

al. (2001), “efficient and inefficient rewards” as well as the “direct and indirect support of

product’s value proposition” by Dowling and Uncles (1997) are not adopted in this research

paper. These two classifications had a focus that is inclined towards the retailer’s

perspective instead of a customer’s perspective. The efficiency of a reward depends on the

reward costs incurred by the firm. The higher the reward cost incurred, the more inefficient

the reward, ceteris paribus. This is mainly a retailer’s concern, or in this specific case, the

card issuer’s concern. Whether a reward is efficient or not does not matter to the customer.

The same goes for Dowling and Uncles’ classification as direct or indirect support of

product’s value proposition. With a reward that supports the product’s value proposition,

retailers are more able to develop loyalty among customers towards the product instead of

towards the reward program. However, to a customer, as long as he or she is able to gain

some benefit from the reward, it does not matter whether it is in support of the product’s

value proposition.

Kivetz and Simonson (2002) classify rewards as either a “necessity” reward or a “luxurious”

one. The authors defined luxury item as “a non-essential item or service that leads to

luxurious living”. Necessity items were referred to as those “that cannot be done without”.

However, different people have different definition of what constitute a necessity and what

constitute a luxurious item depending on their standard of living and their income level.

Therefore, this classification will not be incorporated in the current research as well.

Lastly, some of Smith (2000) classifications of reward programs are not applicable in the

credit card context. They include the Community Program and Information and advice

Program. Consequently his framework will not been applied.

Credit Card Reward Program in Singapore – The Consumers’ Choice

24

3.7.3 Instant benefits – a type of reward program

Some researchers such as Dowling and Uncles (1997) consider “discounts and promotions”

as a type of reward program. However, there are others such as Yi and Jeon (2003) who

think otherwise. They do not regard instant discounts and promotions to be part of a

reward program as they deemed a reward program to be of a “long term perspective”. To

them, discounts and promotions only stimulate short term profitability and hence, should

not be included as a reward program.

The determination of whether instant benefits should be considered a form of reward

program depends largely on the particular context it is applied to. In this research paper,

with the emphasis on credit card industry, instant benefits will be considered as part of a

reward program.

A credit card industry is characterised by undifferentiated offerings and low switching cost.

At the point of purchase, customers can easily and conveniently switch from the use of one

card to another from the arsenal of plastics they have in their wallet. This is particularly so

for Singapore cardholders with their multiple card holding behaviour. Card issuers are often

faced with the challenge of ensuring continual usage from customers.

Furthermore, with the proliferation of reward programs in the credit card market, whether

such programs are able to create “loyalty” among customers remains a question. Customers

using a particular card may not do so out of pure genuine loyalty to the card or the card

issuer. They may just be rationalizing their buying behaviour to reap the most benefit from

the reward program. (Wright & Sparks, 1999) In such a case, repeated purchase using a

particular card may not signify loyalty.

Rather than encouraging “loyal buying behaviour”, a better way of interpreting a credit card

reward program is to encourage “repeated purchase” using the issuers’ card. As defined by

Kivetz and Simonson (2002), the aim of a loyalty reward program is to provide customers

with an incentive to stay with the company and prevent them from switching to other

competitors. Instant benefits such as discounts and promotions provided by credit card

issuers are able to achieve this goal.

Credit Card Reward Program in Singapore – The Consumers’ Choice

25

Credit card issuers usually have tie-ups with major retailers such as petrol stations,

restaurants or fashion boutiques offering card users with discounts and promotions. Take

the example of Citibank Singapore. Citibank has a tie-up with Esso Mobil which offers up to

a total of 18.4% discount on petrol for drivers using Citibank’s Dividend card as a form of

payment. (Citibank Singapore, 2009) Such discount and promotions tie-up often increase

the usage level of the issuers’ card. Generally, customers rationalise their purchasing

behaviour to “get something out of nothing”. (Wright & Sparks, 1999) Through provision of

such instant benefits, card issuers are able to encourage repeated purchases. Furthermore,

cardholders who are loyal customers of Esso Mobil will be enticed to sign up for a Citibank

Dividend Card. Such retail loyalty will allow card issuers to lock in customers to utilise their

card.

Since such discounts and promotions are able fulfil the objective of a reward program,

consequently, they should be included as part of the program.

Credit Card Reward Program in Singapore – The Consumers’ Choice

26

CHAPTER FOUR

RESEARCH

METHODOLOGY

Credit Card Reward Program in Singapore – The Consumers’ Choice

27

CHAPTER FOUR: RESEARCH METHODOLOGY

4.1 Introduction

There are many different types of research methods. However, it is important to choose the

most appropriate one that suits the objective of the research. This chapter will address the

type of research methods undertaken and justification of why they are chosen.

4.2 Research design

To quote Ghauri and Grönhaug (2005 p.56), “research design is the overall plan for relating

the conceptual research problem to relevant and practicable empirical research.” There are

basically 3 main classes of research designs: exploratory, descriptive and causal.

The main aim of the exploratory research is to get a better understanding of the research

problem. It is often used when the research problem is unstructured and not clearly defined.

This method offers the most flexibility and is targeted towards researchers who do not have

a clearly formulated research problem and would like to get more information to help them

determine the direction of the research.

In the case of a descriptive design, the research problem is often structured and known

before any research is undertaken. The researcher has a clear understanding of what he or

she wants to measure.

Lastly, a causal design is employed when the researcher intends to search for any cause-

and-effect relationships that exist between 2 or more variables.

For this research paper, a descriptive research design will be undertaken. From the

literature review conducted in the previous chapter, it is understood that the reward

program plays an important role in determining the choice of a “preferred” credit card in

Singapore. As such, a clear research objective was formulated with the aim of determining

Credit Card Reward Program in Singapore – The Consumers’ Choice

28

the reward programs preferences of the different demographic groups. The most

appropriate design is hence the descriptive one.

4.3 Data collection

“The choice of a data collection method will depend on an overall judgement of which type

of data is needed for a particular research problem.” (Ghauri & Grönhaug, 2005 p.108)

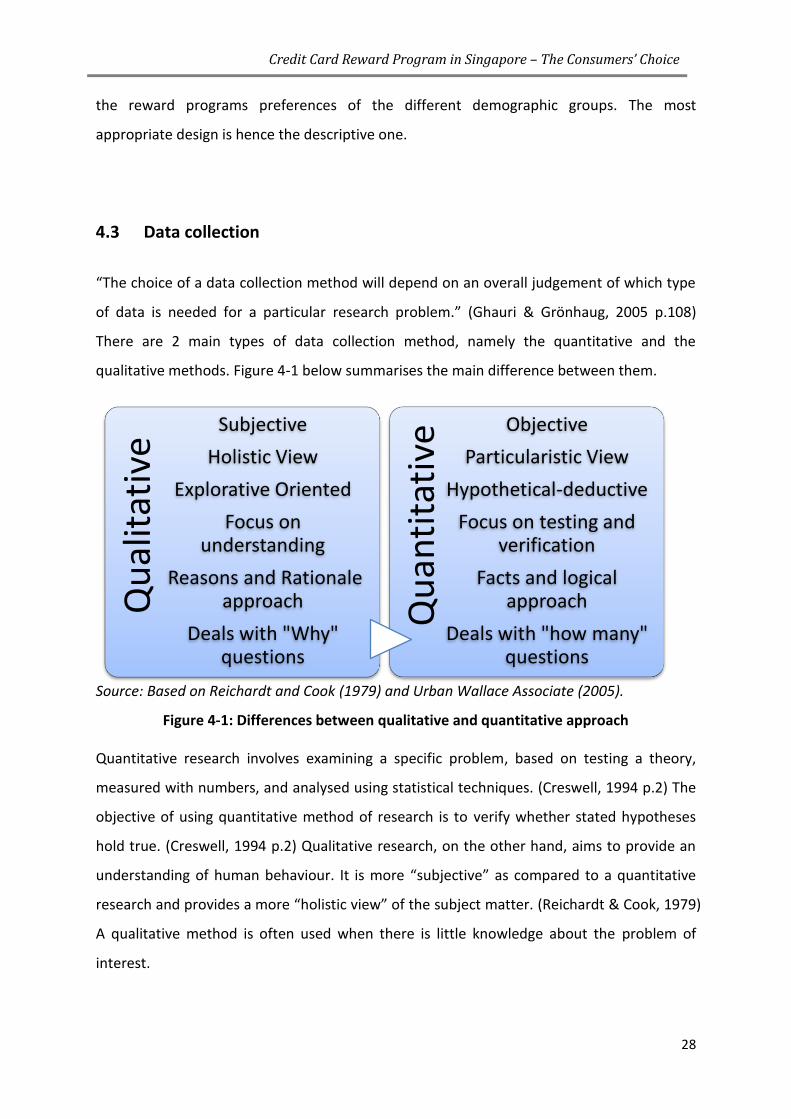

There are 2 main types of data collection method, namely the quantitative and the

qualitative methods. Figure 4-1 below summarises the main difference between them.

Source: Based on Reichardt and Cook (1979) and Urban Wallace Associate (2005).

Figure 4-1: Differences between qualitative and quantitative approach

Quantitative research involves examining a specific problem, based on testing a theory,

measured with numbers, and analysed using statistical techniques. (Creswell, 1994 p.2) The

objective of using quantitative method of research is to verify whether stated hypotheses

hold true. (Creswell, 1994 p.2) Qualitative research, on the other hand, aims to provide an

understanding of human behaviour. It is more “subjective” as compared to a quantitative

research and provides a more “holistic view” of the subject matter. (Reichardt & Cook, 1979)

A qualitative method is often used when there is little knowledge about the problem of

interest.

Qu

alit

ativ

e

Subjective

Holistic View

Explorative Oriented

Focus on understanding

Reasons and Rationale approach

Deals with "Why" questions

Qu

anti

tati

veObjective

Particularistic View

Hypothetical-deductive

Focus on testing and verification

Facts and logical approach

Deals with "how many" questions

Credit Card Reward Program in Singapore – The Consumers’ Choice

29

A quantitative approach will be used in this research paper due to the nature of the

research objective. As the purpose of this research is to “measure” the attitude and

behaviour of card holders according to their demographic groups, a quantitative approach is

more appropriate. A qualitative approach will be aimed at finding out the “reasons” or

“rationale” behind cardholders’ attitude and behaviour. In short, while the quantitative

method aims at measuring “how many”, the qualitative method aims at finding out “why”.

(Urban Wallace Associates, 2005) Six hypotheses with regards to consumer preferences of

credit card reward programs will be tested. Primary data collected will be analysed

statistically and concluded.

4.4 Data source

There are two sources of data, namely primary source and secondary source.

Secondary data source refers to data collected by people other than the researcher. Most

research studies will start off with secondary data analysis whereby a literature review on

previous related research areas will be conducted. For this research paper, a literature

review was conducted to gain further insight into the research problem and to formulate

the direction of the research paper. Secondary data is collected from various sources

including (1) Journal Articles (International Journal of Bank Marketing, International Journal

of Contemporary Hospitality Management, Journal of Services Marketing etc) (2) Internet

websites of different organizations, statutory boards and banks (Monetary Authority of

Singapore, Singapore Department of Statistics Website etc) (3) Studies and reports of

institutions (4) Textbooks (5) News articles (The Business Times) (6) Thesis and Dissertations

written by students from Blekinge Institute of Technology (BTH) and other Universities.

Secondary data may be collected for a different purpose from the current research. As such,

relevance and usability may be limited. This is one of the reasons why primary data need to

be sourced to gather information that cannot be obtained directly via secondary data or

where secondary data requires further support. There are various ways to collect primary

Credit Card Reward Program in Singapore – The Consumers’ Choice

30

data. Some of which includes experiments, observations, surveys and interviews such as a

focus group.

For this research paper, a survey will be conducted to collect the required primary data.

4.5 Survey

Surveys refer to a method of data collection that utilizes questionnaires or interview

techniques for recording the verbal behaviour of respondents. (Ghauri & Grönhaug, 2005

p.124) In this research paper, I have designed a 5 pages long, self-administered

questionnaire as a means to collect the relevant primary data required.

A self-administered questionnaire is used because of several reasons: -

Firstly, self-administered questionnaire allows a large number of respondents to be reached

quickly and easily. In order to reach a diversified group of respondents, questionnaires will

be administered via different modes. To begin with, it will be sent out via emails to my

contacts, including friends, colleagues and relatives. Social online networks such as

facebook will also be employed to reach a greater network of potential respondents. A link

is created to which respondents can visit to download a copy of the questionnaire.

Questionnaires will also be printed out and distributed to friends and colleagues for their

further distributions to their contacts. These different ways help to gather responses from

people of different background, age group and professions.

Secondly, a self-administered questionnaire comprises of standardized questions. It is

relatively free from several types of errors including interviewer bias. The tone of the

interviewer in a researcher-administered survey and the different ways of phrasing the

same question by interviewers may give rise to inaccurate responses. Furthermore,

respondents’ desire to impress the interviewers with his or her answers as well as the

unwillingness of respondents to disclose sensitive information to a stranger may hinder the

data collection process. In a self-administered questionnaire, due to the lack of face-to-face

Credit Card Reward Program in Singapore – The Consumers’ Choice

31

interactions with the interviewer, respondents are more comfortable to disclose sensitive

data.

Thirdly, responses to a questionnaire can be analysed statistically. As mentioned earlier in

Section 4.3, quantitative data collection will be used for this research paper due to the

nature of the research objective. Questionnaire will therefore be a more appropriate form

as compared to interviews such as a focus group, which is more suited for a qualitative

approach.

4.6 Questionnaire design

4.6.1 Organization of Questionnaire

The questionnaire was organized into 5 different sections as shown in Figure 4-2 below.

Figure 4-2 Organization of Questionnaire

The first section is aimed at understanding the demographics of the respondents. This

includes their gender, the age group they fall under and the annual income level they

earned.

Section 1:

Demographic Profile

Section 2: Perceptions of Reward Programs

Section 3: Types of reward

programs

Section 4: Monetary /

Non-monetary rewards

Section 5: Order of

Preference

Credit Card Reward Program in Singapore – The Consumers’ Choice

32

The second section seeks to find out the perception of reward program among respondents.

The main objective is to provide primary data for the first hypothesis of this research.

Hypothesis 1: Females are more attracted by reward programs as compared to males.

The third section seeks to test and build up respondents’ knowledge and understanding of

the 4 different types of reward programs. This section is divided into four sub-sections

representing each of the 4 types of programs. A brief definition of each type of program is

provided. Statements were posed whereby respondents have to state the extent to which

they agree with them. A good understanding of each of the 4 types of reward programs will

ensure a higher degree of accuracy in answering the last section of the questionnaire which

requires respondents to rank the reward programs in order of their preferences.

This section also serves to provide supporting indicators for the testing of hypothesis 2 and

5 as stated below.

Hypothesis 2: Males prefer an immediate reward program to a delayed reward program.

Hypothesis 5: Out of the 5 types of reward programs, air miles accumulation is the least

preferred among cardholders.

The fourth section aims to determine preferences of monetary or non-monetary rewards

among respondents. The purpose is to support the evaluation of the 6th hypothesis.

Hypothesis 6: Cardholders are more attracted to monetary rewards than non-monetary

rewards regardless of demographic groups.

The last section intents to reveal the order of preference among the 4 different types of

reward programs. The 2nd, 3rd, 4th and 5th hypothesis will be answered with these data

collected.

Hypothesis 2 and 5 has been stated above. Hypothesis 3 and 4 is as follows.

Hypothesis 3: There is a strong correlation between preference for point accumulation

program and age group.

Credit Card Reward Program in Singapore – The Consumers’ Choice

33

Hypothesis 4: There is a strong correlation between preference for point accumulation

program and income level.

4.6.2 Types of Measurement

A variety of question and response format were adopted for this questionnaire.

Closed ended questions are used throughout the questionnaire. Closed ended questions

require the respondent to pick answers from given options as opposed to an open ended

one whereby respondent has to formulate his own answers. The types of closed ended

questions used include:

(i) Nominal level of measurement. Most questions in Section 1 and 2 of the

questionnaire adopt a nominal level of measurement. Respondents are required

to choose from options that are mutually exclusive.

(ii) Ordinal level of measurement. The remaining sections of the questionnaire

employ an ordinal level of measurement which consists of a Likert Scale and a

Ranking Order.

(a) For a Likert Scale, respondents have to choose a response from the scale

ranging from (1) strongly disagree to (7) strongly agree that best describe

their attitude and behaviour.

(b) For a Ranking Order, respondents have to rank the options provided

according to their order of preference.

4.6.3 Multiple Indicators

Multiple indicators are often used to measure a construct. Through the use of multiple

indicators, researchers are more able to “cover the domain of the construct which it

purports to measure”. (Ghauri & Grönhaug, 2005 p.82)

Multiple indicators have been used in this research paper. And these are reflected in the

various questions asked in each of the section of the questionnaire. Take the example of the

Credit Card Reward Program in Singapore – The Consumers’ Choice

34

first hypothesis. The first hypothesis aims to find out if females are more attracted by

reward programs than males. Four indicators were used to measure this construct.

(i) Whether the attractiveness of the reward programs is one of the reason for the

choice of credit card

(ii) Whether respondents are aware of the types of reward programs offered by the

cards

(iii) Whether respondents have been utilising the reward programs for their cards

(iv) Whether the type of reward programs influence their choice of card to use

during a purchase.

Respondents who take the attractiveness of reward programs into consideration during the

acquisition stage and usage stage are considered to be attracted by reward programs. Those

who are aware of the types of reward programs offered by the cards and those who have

been utilising them are considered to be attracted by the rewards too.

Similarly, a series of statements were posed to respondents for each type of reward

program in Section III. This serves not only to enhance understanding and knowledge of the

respondents; it also served as a form of multiple indicators. Taking point accumulation

program as an example, six statements were posed to which respondents have to assess

their intensity of agreement. Respondents who are constantly keeping track of the amount

of points they have accumulated, who knows the procedures for redemption of points well,

who have redeemed points within the last 6 months are deemed to rank point accumulation

program as a well-liked program. Those who feel that the redemption process is too

complex and who do not spend enough to accumulate sufficient points as well as those who

have not been redeeming despite accumulating sufficient points are deemed to rank this

program lowly.

The use of multiple indicators reduces the random error that may occur in any research.

Respondents may make mistakes when responding to a questionnaire. With multiple

indicators employed to measure each construct, error on one indicator can be offset by the

other indicators. If the researcher only had one indicator, an inappropriately answered

question by respondents may deem the results to be inaccurate. (Bryman, 1989)

Credit Card Reward Program in Singapore – The Consumers’ Choice

35

4.6.4 Guidelines on Questionnaire Construction

Ghauri and Grönhaug (2005 p.129) listed some guidelines when constructing a

questionnaire and they have been taken into consideration during the design stage of this

questionnaire.

(1) As this questionnaire is aimed at targeting Singapore residents of different age group

and income level, questions were asked in a simple, concise and unambiguous

manner that considers the different respondents’ background. Clear instructions

were given for each section of the questionnaire.

(2) In order to ensure all respondents understand the terminology used throughout the

questionnaire (E.g. cash rebates, point accumulation, monetary rewards, instant

benefits etc), a brief description of each has been provided in each section and sub-

sections.

(3) Each question in the questionnaire deals with only 1 aspect of the question.

“Double- barrelled” questions were not included. This avoids confusion in answering

the questions.

(4) Different types of questions formats were adopted to make the questionnaire more

attractive and stimulate interest in the respondents.

4.6.5 Pre-test Conducted

After the questionnaire was drafted, it was sent to 6 individuals for a pre-test. These 6

individuals formed part of the target population and they were requested to complete the

questionnaire. Upon completion, a short discussion was held. Feedbacks were provided by

the 6 individuals with regards to the clarity of the questions and whether each of them

interpreted the question in the same manner. This will help to provide more validity and

reliability in the data gathered later on. Amendments were made and revised

questionnaires were sent to potential respondents.

A copy of the questionnaire is attached in Appendix A.

Credit Card Reward Program in Singapore – The Consumers’ Choice

36

4.7 Sampling

The sampling process begins with a definition of the population of concern. For this research

paper, the population will include all citizens and permanent residents of Singapore, holding

at least one credit card.

There are two broad categories of sampling procedures:

Probability Sampling

In a probability sampling, every unit in the population has a chance (greater than zero) for

being selected. There are several types of probability sampling, such as simple random

sampling, systematic sampling, stratified sampling and cluster sampling.

Non Probability Sampling

Non probability sampling refers to sampling methods whereby the probability of selection

cannot be accurately determined. As such, samples may not be “representative” of the

population concerned. (Ghauri & Grönhaug, 2005 p.146) Some examples of non probability

sampling include convenience sampling, quota sampling and judgement sampling.

In this research paper, convenience sampling is applied. This type of sampling is also known

as accidental sampling. It involves selecting samples from the part of the population that is

easily available and conveniently reachable.

4.8 Collation of Responses

The survey was conducted from May 11, 2009 till May 24, 2009. A sample size of 200 was

planned to be achieved.

Only a 100% completed questionnaire will be accepted. Some respondents had omitted the

question on income level due to sensitivity. And hence, such samples were excluded.

Credit Card Reward Program in Singapore – The Consumers’ Choice

37

A handful of the respondents misinterpreted the last question on ranking of reward

programs according to their preferences. Instead of ranking each of the 4 reward programs

as rank 1 to rank 4, they chose the same rank for more than one of the reward programs.

For instance, a respondent ranked both Cash Rebates and Instant Benefits as the first choice.

For such cases, respondents were contacted to make the necessary amendments. Those

which are not contactable will be discarded.

In total, 179 usable questionnaires were collected. This represents a response rate of

approximately 90%.

4.9 Limitation of research methodology

Sampling Method

Convenience sampling is often used when researchers are faced with the constraints of

time and resources. It, being a non probability sampling has several limitations. As

mentioned earlier, the chosen samples may not be representative of the population. Hence,

it may not be appropriate to generalize the results to the entire population.

Data collection

A self-administered questionnaire poses several limitations too. Errors due to non-response

may exist. People who choose to respond on the survey may have distinctly different

opinions and preference from people who do not respond. This may adversely biased the

data collected.

Sample Size

A sample size of 179 may not be sufficient to represent the entire population.

Data Source

Due to unavailability of data, some indirect source of secondary data was cited rather than

the original source. This will undermine the reliability of the data to a certain extent.

Credit Card Reward Program in Singapore – The Consumers’ Choice

38

CHAPTER FIVE

RESEARCH FINDINGS &

ANALYSIS

Credit Card Reward Program in Singapore – The Consumers’ Choice

39

CHAPTER FIVE: RESEARCH FINDINGS AND ANALYSIS

5.1 Introduction

In this chapter, research findings obtained from the conduct of the questionnaire will be

tabulated, discussed and analysed. Pie charts and bar charts are used to provide a clearer

illustration of the data.

As a starting point, the demographic profile of the respondents will be examined. This will

be followed by a presentation and detailed analysis of each of the 6 research hypotheses

listed in Section 1.4. The sequence of discussion will pursue the flow of the research

hypotheses.

Primary data collected are tabulated in frequency and cumulative frequency tables and will

be presented in Appendix B. Appendix B is organised according to the different sections of

the questionnaire.

5.2 Demographic profiles

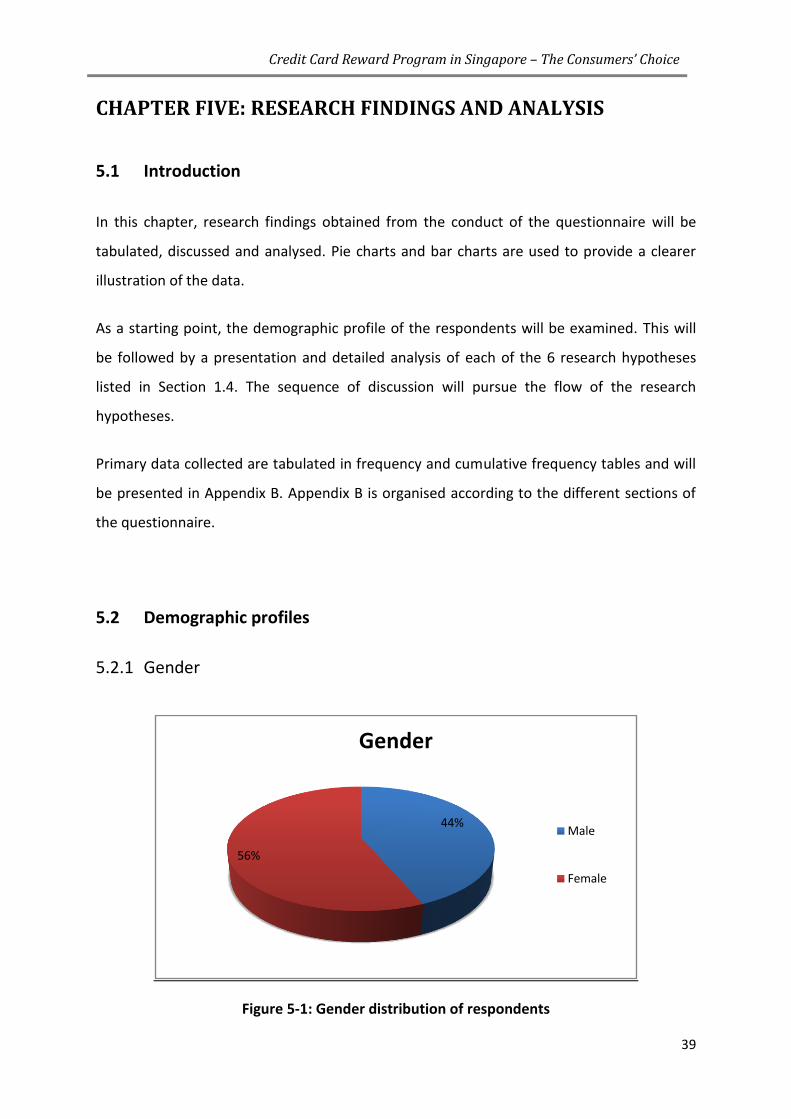

5.2.1 Gender

Figure 5-1: Gender distribution of respondents

44%

56%

Gender

Male

Female

Credit Card Reward Program in Singapore – The Consumers’ Choice

40