credit card's possession and usage among staff in

TRANSCRIPT

CREDIT CARD'S POSSESSION AND USAGE AMONG

STAFF IN UNIVERSITI UTARA MALAYSIA

(CODE S/O 11576)

SHAFIE MOHAMED ZABRI

FIKRIYAH ABDULLAH

JUHAIDA ABU BAKAR

UNIVERSITI UTARA MALAYSIA

2006

i

DISCLAIMER

We are responsible for the accuracy of all opinion, technical comment, factual report, data,

figures, illustration and photographs in the article. We bear full responsibility for the

checking whether the material submitted is subject to copyright or ownership right. UUM

does not accept any liability for the accuracy of such comment, report and other technical

and factual information and the copyright rights claim.

Head:

-------------------------------------------

SHAFIE BIN MOHAMED ZABRI

Researcher:

-------------------------------------------

FIKRIYAH BT ABDULLAH

Researcher:

-------------------------------------------

JUHAIDA BT ABU BAKAR

ii

ACKNOWLEDGEMENT

First and foremost, we would like to extend our sincere gratitude to the Jabatan

Penyelidikan dan Inovasi, Universiti Utara Malaysia and Faculty of Finance and Banking

for giving us an opportunity to make a research under Faculty Grant. Last but most, we

wish to express our sincere appreciation to our colleagues for their encouragement, and

also to our parents and family for their unconditional support, love and patient.

iii

ABSTRACT

The smooth and efficient operation of the payment system is a critical factor in a country’s

economic growth process. Payment methods consist of cash, cheques, debit cards, credit

cards, charge cards, electronic purse and credit transfer. This study focus on a credit card as

the use of credit cards as a medium of exchange for commercial, business and social

purchases is ubiquitous. Credit card market in Malaysia also shows an increasing trend in

term of its volume of usage and number of card possessed. Credit card is a card whose

holder has been granted a revolving credit line. In this study, our respondents come from

staffs in Universiti Utara Malaysia. A survey method has been adopted in finding

information on the respondents via questionnaires. A three-section questionnaire was

developed to find the demographic and socioeconomic characteristics of the respondents,

the possession of credit card and the usage of credit card among them. All the information

from 117 respondents then analyzed using the descriptive method to reflect respondent’s

demographic and socioeconomic data together with their possession and usage of credit

card.

iv

TABLE OF CONTENTS

Page

Disclaimer i

Acknowledgement ii

Abstract iii

Table of Contents iv

List of Tables vi

CHAPTER ONE: INTRODUCTION

1.1 Credit Card Revolution 3

1.2 The Malaysian Credit Card Market 9

1.3 Background: Universiti Utara Malaysia 15

1.4 Research Objective 15

1.5 Significance of the Study 18

CHAPTER TWO: LITERATURE REVIEW

2.1 Demographic and Socioeconomic Characteristics 20

2.2 Possession and Usage of Credit Card 27

CHAPTER THREE: METHODOLOGY, DATA AND VARIABLES

3.1 The Nature of Study 33

3.2 Sampling Method

3.2.1 Sample Size 34

3.3 Data Collection Technique

3.3.1 Primary Source 35

3.3.2 Secondary Source 36

3.4 Development of Questionnaire

v

3.4.1 Layout 37

3.5 Data Analysis 39

CHAPTER FOUR: FINDINGS AND ANALYSIS

4.1 The Demographic and Socioeconomic Characteristics 40

4.2 Possession of Credit Card 47

4.3 Usage of Credit Card 54

CHAPTER FIVE: CONCLUSION

5.0 Conclusion 63

REFERENCES 65

APPENDIX

vi

LIST OF TABLES

Table Title Page

1 Malaysia Banking System: Credit Card Statistics 12

4.1.1 Respondent Profiles by Gender 41

4.1.2 Respondent Profiles by Race 41

4.1.3 Respondent Profiles by Age 42

4.1.4 Respondent Profiles by Marital Status 43

4.1.5 Respondent Profiles by Number of Dependency 44

4.1.6 Respondent Profiles by Years Working in UUM 44

4.1.7 Respondent Profiles by Monthly Income 45

4.1.8 Respondent Profiles by Job Category 46

4.1.9 Respondent Profiles by Level of Education 47

4.2.1 Number of Respondents that Possessed Credit Cards 48

4.2.2 Number of Credit Cards Owned by Respondents 48

4.2.3 Number of Credit Cards Used Regularly 49

4.2.4 Types of Credit Cards Owned 50

4.2.5 Preference of Credit Cards 50

4.2.6 Selection Criteria of a Credit Card 51

4.2.7 Purpose of Possessing Credit Card 52

4.2.8 Sources of Information on Credit Card 53

4.2.9 Preference of Co-branded Credit Card 54

4.2.10 Consideration Factors of Co-branded Credit Card 54

4.3.1 Frequency of Monthly Credit Card’s Usage 55

4.3.2 Types of Credit Card’s Usage 56

4.3.3 Type of Online Purchase by Credit Card 57

4.3.4 Concern over Interest Charged on Credit Card 58

4.3.5 Factors Motivating Credit Card’s Usage 58

4.3.6 Plan on Credit Card’s Usage 59

4.3.7 Credit Card’s Monthly Spending Amount 60

4.3.8 Credit Limit Offered to Respondents 60

1

CHAPTER 1

INTRODUCTION

Credit is a method of selling goods or services without the buyer having cash in hand.

A credit card is an automatic of offering credit to a consumer. Today, every credit card

carries an identifying number that speeds shopping transactions. The use of credit cards

as a medium of exchange for commercial, business and social purchases is ubiquitous.

Their appeal is widespread and they naturally compete with various payment systems

including cash, personal cheques, debit cards, electronic purse and credit transfers. In

developed countries such as the United States and Europe, credit card and plastic

money are viewed as an indication of cashless society. Cashless society allows high-

tech infrastructure to be carried out in developed country through the usage of plastic

money (Ingene and Levy, 1982).

Nowadays, credit card has become one of fast developed-products offered by banking

institutions in Malaysia. Currently, there are 18 credit card issuers in Malaysia such as

Citibank Berhad, HSBC (M) Berhad, Standard Chartered Bank Berhad, Malayan

Banking Berhad, Public Bank, and Bank Islam Malaysia Berhad. Customers can choose

wider range of either conventional or Syariah-based credit cards. Despite the increasing

trend, the use of cash and cheques continue to remain high in Malaysia (Bank Negara

Malaysia, 2003).

2

Moreover, research done by Datamonitor1, revealed that the Asia-Pacific credit card

market covers a relatively small proportion of its large population. Most of the

transactions are done in cash, and great deals of retailers, excluding those in large cities,

do not accept cards as payment. However, transaction habits are slowly changing as the

knowledge about cards becomes more widespread. The current leading credit card

companies in the Asia-Pacific include Citigroup, HSBC and Standard Chartered. In

Malaysia alone, HSBC Bank Malaysia as at April 2006 has about 950,000 cards in

circulation. Standard Chartered, one of the top three credit card issuers in Malaysia, has

448,000 cardholders. In response to the competitiveness of global market environment,

credit card institutions shifted their target on non-traditional consumers, such as lower

income populations and college students (Braunsberger et al., 1997).

Credit cards serve two distinct functions for consumers: a mean of payment and a

source of credit (Ausubel, 1991; Chakravorti, 1997 & 2000; Chakravorti and Emmons,

2001; Slocum and Matthews, 1970; Stavins, 2000). Based on their main use of credit

cards and the benefits sought, credit cards users can be segmented into two groups:

convenience users and revolvers (Lee and Hogarth, 1999). Convenience users tend to

employ credit cards as an easy mode of payment and to typically pay their balance in

full upon receiving the account statement. Revolvers, on the other hand, use the card

principally as a mode of financing and elect to pay interest charges on the unpaid

balance (Lee and Kwon, 2002).

1 Business Information Company Specializing in Industry Analysis.

3

Credit card is a card whose holder is granted a revolving credit line. It is also referred

as a card issued by a financial institution that allows the cardholder to use credit to

purchase goods and services up to a predetermined limit. It enables the holder to make

purchases and or cash advances up to a pre-arranged limit. The credit granted can be

settled in full by the end of a specified period or in part, with the balance taken as

extended credit. Interest may be charged on the transaction amounts from the date of

each transaction or only on the extended credit where the credit granted has not been

settled in full. Interest rates are traditionally higher than those charged on consumer

loans.

Credit cards have been another major area that banks have focused on in recent years in

line with the larger goal of promoting retail or consumer banking. The industry has seen

phenomenal growth in the number of cards in circulation as well as the amount spent

via credit card transactions. Despite the recent developments in and impediments to

credit cards usage in developed countries, one still observes the spread of credit card

ownership and usage in advanced developing countries of Asia, Africa, the Middle East

and Latin America (Kaynak et al., 1995).

1.1 Credit Card Revolution

The first credit cards were issued in the United States by Western Union in

1914. This was followed by Diners Club, which introduced a travel and

entertainment credit card in 1950 and subsequently, in 1958, Bank of America

4

issued its Bank Americard and American Express, its American Express Card.

During the 1960s and 1970s Visa and Master Card have also expanded their

operations on a global scale (Kaynak et al., 1995). In order to avoid

competition, Master Card systems and Visa established themselves as the

bank’s credit card industry in the United States (Garcia, 1980).

Credit cards were not always made of plastic. There have been credit tokens

made from metal coins, metal plate, celluloid, metal, fiber, paper and now

mostly plastic cards. Since 1960, usage of bank credit cards in the United States

had undergone phenomenal growth. Credit cards had replaced cash and cheque

in many kinds of transactions. In the retail industry, the use of “non-store” credit

cards, such as Visa, Mastercard and American Express, had also grown rapidly.

In 1978, non-store cards were used in almost three percent of all transactions in

the United State’s departmental stores with over $1 million in sales. By the end

of 1980, non-store cards had increased to eight per cent of the transactions. On

the other hand, in specialty stores with over $ 1 million sales, credit cards

accounted for ten per cent of the dollar sales volume in 1978. In 1980, credit

cards sales had increased dramatically to seventeen per cent of the dollar sales

volume (Worthington, 1990).

5

Diners Club

In 1950, a New York businessman, Frank McNamara, put forward the idea of a

plastic card, which could be used to pay for meals in all major restaurants in the

city. The inspiration for this came when he was unable to pay for a meal in New

York restaurant as he had no cash and his dining companions only had a cheque

books based on out of state banks, which the restaurant refused to accept. The

plastic card concept was that in return guaranteeing the payment, the company

organizing the scheme would receive 5 percent to 10 percent of the cost of

every meal charged to the account and that the cardholders would pay off the

outstanding balance in full at the end of every month. After some initial

difficulties in selling the concept to the restaurateurs (nine of the first ten

restaurants approached turned down the idea), eventually 27 establishments

agreed to accept what was then branded as the “Diners Club” card.

The first year of operation saw 200 members, the second year 42,000 and with

$5 annual membership fee, by the time that Diners Club became a public

company in 1955, it had some 200,000 members, $20 million in charges and

$500,000 in profits. Travel related activities such as hotels and airline were

quickly recruited as acceptance outlets, alongside restaurants and so the concept

of the T&E (travel and entertainment) card was created. The formula of the

annual fee, the merchant service charge, full payment at the end of the account

period and no pre-set upper spending limit, defines the T&E card to this day.

The principle customer was the business-person who needed records of charged

6

made for reimbursable purposes and who expected to receive repayment for

accrued expenses within a 20 to 40 day period. The success of the Diners Club

attracted competitors to the T&E market, none of whom were particularly

successful, with the exception of American Express.

American Express

American Express has long pedigree of serving the US traveler and had offices

and agents in cities around the world, alongside a well developed business of

travelers’ cheques. To this existing portfolio of products was added in 1958, a

T&E card. This card, coloured green, has become the icon most associated with

American Express and, by 1987; over 10 million such cards were in issue. To

segment its market further, American Express introduced the Gold Card (1966)

and the Platinum Card (1984) and a revolving credit card, branded Optima, in

the spring of 1987. The Optima Card was seen as a direct response to the

success of the bank owned credit cards, which had become attractive to

consumers because of the revolving credit facility that they offered, as opposed

to the T&E charge cards, which required full settlement of the amount owed, at

the end of each account period.

Bank Americard

The first bank sponsored credit plan was introduced by Flatbush National Bank

of Brooklyn, New York, in 1946, under the brand of Charge-it. It was a paper-

based system, where local merchants accepted scrip from customers in lieu of

7

cash, deposited the scrip in their accounts with the bank and the customers were

billed for the total scrip outstanding at the end of the month. The first bank card

was introduced by the Franklin National Bank of New York in 1951, but until

1958 and the introduction of an associated revolving credit line, bank cards

merely replicated T&E cards, but without the annual membership fee. One of

the banks that issued cards was the Bank of America, based in California,

which, in 1958, launched Bank Americard, a revolving credit card which by

1961 had grown to one million cards. In 1966, Bank of America introduced a

nationwide clearing system for bank credit card sales slips and this development

rapidly changed the nature of the bank credit card industry.

Previously, bankcards were local or regional in nature and were founded and

run by individual banks. This limited the usefulness of each card, due to the

restricted geographical reach of each particular card and also had the

disadvantage of high start-up costs, because of the challenge of persuading

merchants to accept a bank’s card, while knowing that the penetration of that

card was limited to the bank’s geographical coverage. The Bank of America’s

clearing system enabled other banks to join forces and thus achieved wider

acceptability of their credit cards.

Bank of America branded this service Bank Americard and licensed it to other

banks across the United States, so that they could use that brand, its design and

participate in the clearinghouse system. By 1970, 3,031 banks had affiliated to

8

the scheme and its success had produced the rival Interbank Card Association

and its Master Charge brand. The design of the card was based on the colours,

blue, white and gold, and blue and gold were the colours adopted by Barclays in

1966, when they took the first overseas license of Bank Americard and launched

Barclaycard in the UK.

Visa

Following Bank Americard’s extension of its licensing programme outside of

the USA, the International Bank Americard Cooperation (IBANCO) was

formed in 1974, to unite the financial institutions around the world who wanted

to use and promote the credit card product. The card was a success, but many of

the banks, with strong brand names in their own territory, did not want to issue a

card associated with the Bank of America. Hence, in 1977, Bank Americard

became the Visa card and IBANCO became Visa International. Visa

International is now an organization of over 22,000 financial institution

members and it creates and operates regulations and by-laws; provides a world-

wide electronic clearing system which authorizes transactions and transmits

clearing and settlement data and offers a global network of cash dispensers.

MasterCard

With the creation of the Bank Americard system and its expansion via licensing

agreements, several other large banks in the United States decided that they

would respond to this initiative by forming, in 1966, the Interbank Card

9

Association, which, in 1980, became MasterCard International. Initially, both

Visa and MasterCard required their member banks to offer only one or other of

the two cards. However, by the late 1970s, the concept of “duality” had been

established in the United States and many financial service providers are now

members of both of the international cards associations and hence issue both

MasterCard and Visa cards.

In 1970, the Interbank Card Association acquired the rights to the Master

Charge name and the design of red and yellow interlocking circles have

remained as the logo of the subsequently renamed MasterCard brand. By 1983,

the change from MasterCharge to MasterCard was completed and the two rival

international bank card associations were established as member-owned mutuals

where, under the concept of duality, ironically, card issuers could be and often

were, members of both associations.

1.2 The Malaysian Credit Card Market

The Malaysian card market has recently expanded dramatically in credit card

usage. The credit cards circulation in Malaysia could be grouped into two

categories, which are conventional and Islamic-based credit cards. The players

constitute of domestic and foreign banks and conventional credit cards have

monopolized the market since 1980s. However the market is diversified in 1992

10

with the introduction of Islamic-based credit cards by Ambank Berhad and

followed by Bank Islam Malaysia Berhad.

Credit card has become a practical and natural way of purchasing goods and

services. For instance, it is a common phenomenon to purchase groceries and

gasoline from an automated petrol station even though there was no attendant

where cardholders could charge their credit cards (Ramayah et al, 2002).

There are several top major credit cards namely Visa, Master Card, Diner’s

Club and the recent addition to the Malaysian market, American Express

(Amex) which is issued by local and foreign financial institutions. What does

the credit card represent? Convenience, assurance, revolving credits, lifestyle,

status symbol, Internet shopping, global currency, e-commerce, m-commerce

and the reasons are non-exhaustive. To acquire credit cards in Malaysia, the

applicant has to convince the card issuer that he or she has a stable income and

the ability to meet the payments made with the card. In fact, credit card is not

offered to college or university students as practiced in develop countries.

Although market leaders and followers have already been established, the

situation in the market is still very fragile and a huge potential for further

penetration exists despite the fact that the issuance of new credit card in

Malaysia increases by an average of 12 percent each year. As at 2001, Master

Card captures the largest market share (includes charge card) with 67%. The

11

rest of the cards in Malaysian wallets are Visa with 49% market share, followed

by charge cards like Amex (9%) and Diner (3%). In terms of usage, MasterCard

contributes 53% while Visa shares 34% (Bank Negara Malaysia, 2004)

Malaysia is an ideal market for credit cards in the region due to its large and

growing educated population. A research done by Visa International Ltd,

indicates that out of the 7.5 million Malaysian with bank accounts, a million of

them are eligible for credit cards as compared to other Southeast Asian

countries and Malaysia remains an attractive market for Visa International to

expand their business. Moreover, approximately 5,500,000 Malaysian earn

more than RM1,500 per month and qualify to hold credit cards. Such a vast

market is still untapped. Malaysian customers have a wide variety of card to

choose and yet the market is still low in term of penetration rate, which is only

23% as compared to Singapore (90%), Korea (90%), Japan (85%), Hong Kong

(80%), and Taiwan (70%) though the figure shown an increment year by year

(Bank Negara Malaysia, 2004).

This also clearly signifies more room for growth in the Malaysian credit card

industry, which has yet to be fully tapped by credit card issuers in the country.

This is in line with a survey adopted from The World Competitiveness

Yearbook 2000 that discovered that each American own an average of 1.745

cards, which ranked first in the number of credit cards issued in the world.

12

Malaysia ranked 29th

out of 45 countries surveyed with an average of 0.1029

cards. In other words, out of 10 people only one person owns a credit card.

Although, Malaysia ranked 29th

out of 45 countries in 2000, it seems that the

credit card issuance is tremendously growing. According to Bank Negara

Malaysia, as at June 2005, numbers of cards in circulation are 7.13 million

where 5.8 million were principal holders with the number of cards transaction

amounting to RM14.9 million. Total purchases made by the local cardholders

were RM16, 211.60 million up until June 2005 compared to RM14, 303.90

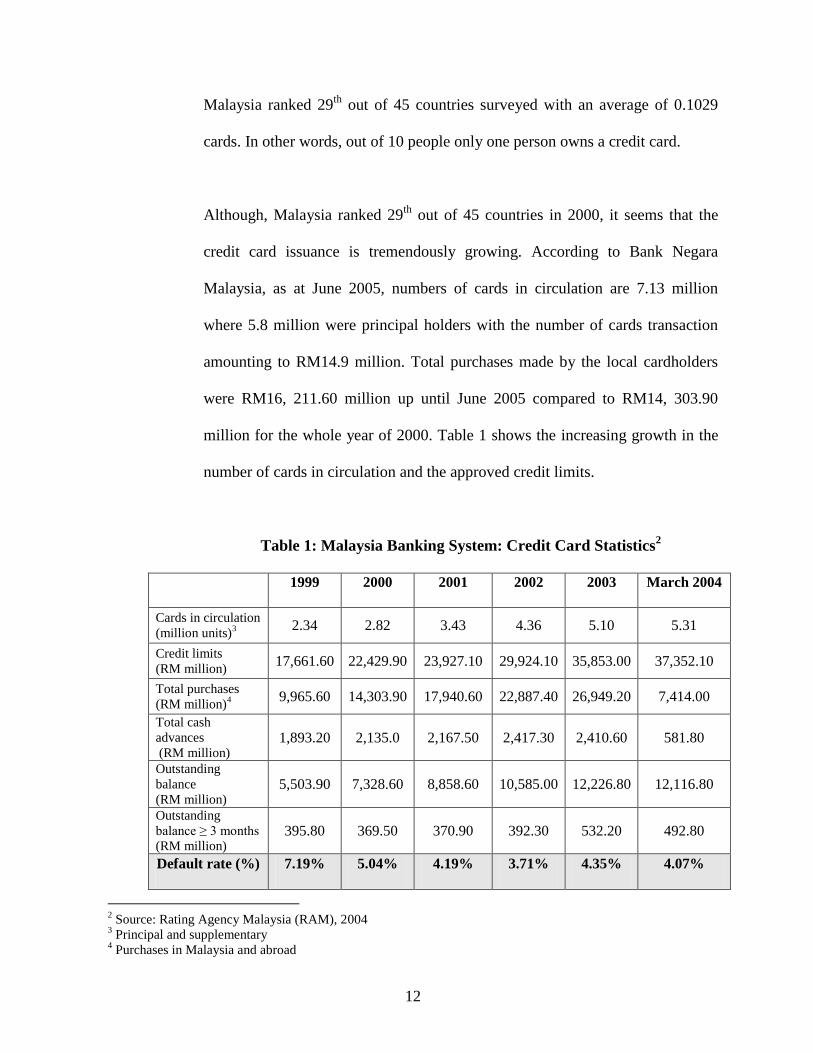

million for the whole year of 2000. Table 1 shows the increasing growth in the

number of cards in circulation and the approved credit limits.

Table 1: Malaysia Banking System: Credit Card Statistics2

1999 2000 2001 2002 2003 March 2004

Cards in circulation

(million units)3

2.34 2.82 3.43 4.36 5.10 5.31

Credit limits

(RM million) 17,661.60 22,429.90 23,927.10 29,924.10 35,853.00 37,352.10

Total purchases

(RM million)4

9,965.60 14,303.90 17,940.60 22,887.40 26,949.20 7,414.00

Total cash

advances

(RM million) 1,893.20 2,135.0 2,167.50 2,417.30 2,410.60 581.80

Outstanding

balance

(RM million) 5,503.90 7,328.60 8,858.60 10,585.00 12,226.80 12,116.80

Outstanding

balance ≥ 3 months

(RM million) 395.80 369.50 370.90 392.30 532.20 492.80

Default rate (%) 7.19% 5.04% 4.19% 3.71% 4.35% 4.07%

2 Source: Rating Agency Malaysia (RAM), 2004

3 Principal and supplementary

4 Purchases in Malaysia and abroad

13

The increasing number of credit cardholders may be due to the action taken by

Bank Negara Malaysia in reducing the minimum annual income eligibility

criteria from RM24,000 to RM18,000 effective on 28th

July 1999. Considering

the fact that the credit card industry in Malaysia is still in its infancy, the

potential for growth is evident. By 2008, the number of credit cards in

circulation is expected to be 2.6 times over that of 2003. Consistently,

transactional volume and values are expected to grow by about the same

proportion to that of cards in circulation. In order to make sure that the credit

card industry in Malaysia continues flourishing, banking institutions are urged

to accord priority to the Europay Master Card Visa (EMV) chip migration to

effectively address fraud cases involving counterfeiting of cards.

As part of the new guidelines to stimulate credit growth in late 1998 and to

ensure that charges are imposed on credit cardholders were reasonable, credit

card issuers were not allowed to charge cardholders more than 1.5% per month

or 18% per annum in finance charges. Moreover Bank Negara Malaysia also

decided that late payment charges should not be more than 1% of the amount in

default and the banking institutions would only be allowed to charge a

minimum penalty of RM5 (Lee and Toh, 1995). In addition, card-issuing

institutions require at least 5% of the outstanding balance to be paid by the due

date. The remaining balance is allowed to be rolled-over into the following

month for payment they are allowed 20 interest-free days to make payment.

14

At the same time, the general consensus from banks interviewed indicates that

Malaysian credit cardholders were well aware on the standard finance charges

and late payment imposed by credit card issuers. HSBC Bank Malaysia Berhad,

Malayan Banking Berhad, Citibank Berhad and RHB Bank Berhad all claim to

have “manageable” default rates compared to the industry's non-performing

loans rate of over 4%. Malaysia's largest credit card issuer, Citibank Berhad

whereby in every four credit cards issued, one will be a Citibank credit card, has

gone an extra mile by investing heavily in its credit card business, offering both

existing and potential credit card users innovative products, quality customer

service, convenient delivery channels as well as trained and competent sales

personnel.

Meanwhile, Malayan Banking Berhad, the leading local bank said that apart

from better products and services, the convenience aspect also plays an equally

important role when choosing a credit card. They are giving those with

Maybank accounts or credit cards the option to make online payment via

Maybank2u.com. Besides that, for those revolving account holders with other

banks where they pay 1.5% per month, Malayan Banking Berhad will offer

them credit save at 0% for three months if they transfer their remaining balance

to Malayan Banking Berhad

Malayan Banking Berhad believes all these conveniences will help customers

choose their bank as the preferred credit card issuer. As the requirement among

15

potential credit card users is fast changing, banks are intensifying their efforts to

come out with bigger promotions and better products and services to outdo their

rivals.

1.3 Background: Universiti Utara Malaysia

Universiti Utara Malaysia (UUM), one of the Public Institute of Higher

Learnings in Malaysia, was formally incorporated on 16th

February 1984. From

its humble beginnings in Tanah Merah, Jitra in 1990, UUM moved to Sintok, 48

kilometres north of Alor Setar, Kedah. As at June 2006, there are about 20,000

students with 13 faculties offering different types of degree. In order to cater

large number of students’ intake, the management has increased the number of

staff every year. Basically there are two categories of staff in UUM namely

academic and non-academic. An academic staff is referred to professor,

associate professor, senior lecturer, lecturer, tutor and language teacher while

non-academic is referred to management, professional and administrative staff.

Currently, the numbers of staff attached with UUM are 2351, which comprised

of 49% academic staff and 51% non-academic staff.

1.4 Research Objective

Nowadays, credit card customers are becoming savvier, well versed and

educated, as well as demanding, when choosing credit cards to cater for their

16

financial needs. One banker said, “As Malaysia heads towards a cashless

society, credit cards are obviously being transformed into one of the most

fundamental financial service products, especially in urban centres and also,

becoming as basic as a savings account to a customer.”

Aware of the attractiveness, more players continue to enter the domestic credit

card market resulting the growth of the market has slowed down and

competition has intensified in recent years. In view of the intensifying

competition, existing issuers in Malaysia have to fine-tune their marketing

efforts should they wish to maintain their previous growth records. In this

respect, issuers first need to explore new niches and continue converting non-

cardholders into cardholders (Ricky Yee-Kwong Chan, 1997).

In addition, research into the regional market segments of China (Cui and Liu,

2000) suggests that consumers from various regions are significantly different

from one another in terms of purchasing power, attitudes, lifestyles, media used

and consumption patterns. An overview of cardholders attitude can be revealed

either they are “active” or “inactive” similar to the classification of “light

users” or “heavy users” for tangible consumer products (Cook and Mindak,

1984; Kotler and Armstrong, 1996). Hence, credit card users can be categorized

according to their differences in cardholder usage rates. In another research

conducted by Chan (1997) claimed that an “active cardholder” refers to those

17

whose card usage rate was at least ten times per month, whereas “inactive

cardholder” referred to card usage rate of less than ten times per month.

Most importantly, Worthington (2005) has reported in China that in general

cardholders from the private sector use their credit cards far more frequently

than cardholders who work for government organization. Although most banks

in Malaysia, such as Citibank Berhad, HSBC Bank Malaysia Berhad, Standard

Chartered Bank Berhad and some other local financial institutions like Malayan

Banking Berhad and MBF Cards (M) Sdn. Bhd. had significant customer bases,

they were still competing among themselves to attract active cardholders. Thus,

understanding the needs, motivations and priorities of the consumers and

analyzing how they select suppliers and products are the first crucial steps

towards the improvement of consumer satisfaction.

Keeping the importance of marketing research and evaluation of customer’s

needs in mind, this paper aims to achieve the following objectives:

1. To find information on the demographic and socioeconomic characteristics

of credit cardholders in UUM.

2. To study on the possession and usage of credit card among staff in UUM.

18

Besides, the objective of the research also was to provide a greater depth of

understanding about the nuances of credit card ownership and usage in UUM, in

addition to knowledge about the culture of payment among Malaysian.

1.5 Significance of The Study

There are various types of payment systems available in Malaysia including

credit card. Therefore, there is a need to explore the relevant issue on the

behavior of consumers in using this type of payment system. There is a lot of

study can be done especially in exploring consumer’s behaviors towards

ownership of credit card and the way they use it. This research is expected to

contribute to literature on credit card possession and usage in Malaysia.

Information on whom currently holds credit cards, the extent of their use and

how credit card users differ in terms of demographics, socio-economics and

attitudinal orientations provide greater insights into the credit card market in

developing country markets (Kaynak and Harcar, 2001). Reliable and useful

information can be shared and used among academicians and also bankers in

furthering their study especially on consumer behaviors. The findings of this

study will have some implications to the bankers in developing their marketing

strategies in line with the customer preferences. Successful marketing strategies

are based on customer segmentation (Lucas, 1992). Once the market is

segmented, the issuer can run an analysis of the cardholder’s behavior to

determine what will encourage usage.

19

CHAPTER 2

LITERATURE REVIEW

The research literature on credit cards is varied and extensive. Several studies have

focused on a broad array of economic factors including interest charges and

consumption (Garcia, 1980 and Slom, 1991), and effects on the money supply, banking

and retailing (Hirshman, 1982 and Mandell and Murphy, 1979). Other studies have

examined credit card use (Canner and Cyrnak, 1986; Hirshman, 1982 and Lindsay et

al., 1989) from a behavioural perspective as well as credit card possession (Hawes,

1988; Kinsey, 1981; Delener and Katzenstein, 1994).

The popularity of credit cards as a payment medium has been attributed to convenience

of not carrying cash and checks, the limited liability of lost or stolen cards and

additional enhancements (Chakravorti 1997 & 2000; Chakravoti and Emmons, 2001;

Whitesell, 1992). It was found that, credit cards are predominantly used for some types

of purchases, such as telephone and Internet transactions.

Despite this shortcoming, ease of use and convenience has made credit cards very

attractive to customers in developed countries, however, relative to other consumer loan

instruments, the interest rates charged on credit cards have historically been very high

and have changed very little over time. This high growth potential makes the credit card

markets very attractive for many institutions and therefore this crowded market is very

competitive compared to other forms of payment

20

Hence, these factors have captured the attention of several researchers from a variety of

disciplines such as economics, insurance, law, marketing and psychology since the

early 1970s to study credit cards, and therefore sizable body of literature has been

created on credit card ownership and usage (Kara et al., 1996). In addition, external

factors like economic, demographic and socio-economic factors are assumed to have

some impact on the credit card use while attitudes towards credit card use are assumed

to be input variables to credit card use.

Apparently, many studies have attempted to identify markets through the analysis of

demographic, socio economic, attitudinal, and or personality characteristics (Martell

and Fitts, 1981). Behavioral work has been descriptive or correlational and has

attempted to answer the question of “Who is the credit card user and what are their

demographic and socio-economic profiles?’ (Slocum and Mathews, 1970; Plummer

1971). Along with the development of user profiles, they also concentrated on the

analysis of broader economic issues pertaining to credit card demand and supply

(Hawes et al., 1978; Adcock et al., 1977; Martell and Fitts, 1981; Goldstucker and

Hirschman,1977; Kaynak and Yucelt, 1984; Hirschman, 1979; Kinsey, 1981).

2.1 Demographic and Socioeconomic Characteristics

Accelerating competition in the banking market has driven organizations

constantly to seek to produce unique services for distinct market segments. For

instance, most US banks offer a special bundled account designed to serve the

21

needs of young men and women just starting out. Several banks have also

designed checking accounts and certificate of deposit for young people up to the

age of 21 (Mason and Ezell, 1993). Segmentation has traditionally divided

customers by either user characteristics (i.e. demographics) or by user

behaviour. While demographic information can help to classify and perhaps

define the likelihood of purchasing, or data may be needed to help us

understanding actual buying behaviour (Paden et al., 1996).

That’s why demographic and socioeconomic analysis seems to be very

important in order to cater market segmentation. A number of behavioural

studies analyzed credit card possession (Glodstucker and Hirschman, 1977;

Hawes, 1988; Kinsey, 1981) and credit card use (Canner and Cyrnak, 1986;

Feinberg, 1986; Hirschman, 1982; Lindley et al.,1989; White, 1975).

Furthermore an empirical research study conducted in urban Turkey indicates

that there are certain relationships between socio-economic and demographic

characteristics of Turkish consumers and their cardholding and usage

behaviours (Kaynak et al., 1995)

Many studies have found age, sex and marital status to be significant

determinants of credit card selection and usage (Slocum and Mathews, 1970;

Kinsey, 1981). Likewise, occupation, education and income are accepted

generally as potentially significant correlates usage (Kara et al., 1996). Income

22

has been repeatedly found to have a positive effect on credit card usage, for both

bankcards and store cards (Heck, 1984).

Past credit literature also showed that there is a close relationship between credit

card usage and the level of economic development in a country. Historical

evidence also demonstrated that the rising income and the increased in the

purchasing power of the household are among the most significant factors

during the 1980s and 1990s that resulted in increasing demand for credit card

facilities (Kara et al., 1994). This is supported by Kaynak etal., (1995) indicates

that the widespread credit card usage in Middle Eastern country only began in

1989 when the country experienced a substantial degree of economic growth

and increased standards of living of people under economic liberalization

programs of the early 1980s. Past studies also indicate that the primary

determinants of credit card use are the income and education of the household

head as well as the family life cycle stage.

In other study, Canner and Cyrnak (1985 & 1986) examine more specifically

bank card holding and use patterns. They found a decline in the proportion of

families with two bankcard accounts between the years 1978 and 1983. They

also noted that the ‘heavy holder” segment is likely to hold a wide variety of

cards; that higher income and more financially sophisticated families are likely

to be credit cards holders; that Yuppies are very much into credit cards; and that

23

nearly half of all card holders use their cards primarily for “convenience”

purposes.

This is inline with Mandell (1972), which indicate that the primary determinants

of credit card use are the income and education of the household head as well as

the family life cycle stage. Families with higher incomes are more likely to use

credit cards than are lower income families. As family income is highly

correlated with the education of the family head, families with better-educated

heads are more likely than others to use credit cards and it is concluded that a

higher level of education is positively associated with a consumer’s

predisposition of credit usage. Furthermore, Lee and Kwon (2002) have found

that respondents with some college education were most likely to possess a

store card, followed by college graduates, high school graduates and

respondents with a graduate education.

This is supported by Kaynak et al., (1995) research done in Turkey found that

income and education was positively related to card usage while gender had a

negative influence on card usage. Another study by Choi and De Vaney (1995)

in the United States revealed the same, where education was positively related

to card usage, whilst gender was negatively related to card usage. However

other research by Lindley et al., (1989) discovered a positive relationship

between female respondents and the use of credit for the purchase of household

goods and clothing. Armstrong and Craven (1993) investigated the average

24

number of credit cards by gender and found that females tended to have a higher

average number of cards than males. According to MasterCard International,

recently conducted a consumer study indicated women in the Asia Pacific are

becoming increasingly important spenders due to numbers of women getting

tertiary education and entering the workforce.

Furthermore, in South-East Asia, there are 69 working women for every 100

working men. The ratio of women graduates to men in Malaysia is at 78:100.As

a result, the number of women traveling for both business and pleasure is on the

rise and there is now a new type of customer- the traveler shopper. Of this

group, the biggest spenders are aged from 59 to 79 years, with high disposable

funds as they draw pensions and often, that of their (deceased) spouses.

Other determinants of credit card use are related to the age of the family head

and the family lifecycle stage. Generally, those household heads who are in

middle and upper age ranges and who have major expenditures with a large

discretionary income level are more likely to use credit cards compared to the

other groups. Furthermore, in an earlier study by Barker and Sekerkaya (1992),

it was discovered that credit usage in Turkey appears to have attracted the

better-educated, middle aged and married members of the upper middle class.

On the other hand, several researchers have reported a negative impact of age

on credit card usage (Adcock et al., 1977; Awh and Waters, 1974). In addition,

Danes and Hira (1990) argued that the negative age impact might also reflect a

25

cohort effect. Older families may find credit cards less acceptable for financing

use compared to younger families who have grown up using credit cards. On the

other hand, Delener and Ktazenstein (1994) and Heck (1987) found that age was

positively related to store card usage. This is supported by other researcher

(Arora, 1987; Kinsey, 1981; Mandell, 1971) found that ease of payment was

significant by age with the 29 to 39 year olds considering it more important than

the others and nevertheless, middle age group seems to be the heaviest users and

to be very affected by the credit card revolution.

Marital status was found to be significant in determining consumer’s use of

bankcards and store cards (Delener and Katzenstein, 1994). Married

respondents had more bankcards and department store credit cards than singles

and separated or divorced respondents. A consistent result was found,

examining Asian and Hispanic consumers, in that the longer these respondents

were married, the more department store credit cards they possessed. Ingram

and Pugh (1981) examined consumer ownership and usage of bank credit cards

and found that young married couples, retired heads of households, sole

survivors, and single member households tend to own fewer bank credit cards.

Results also revealed that the level of household income and education are

positively associated with bank credit card ownership.

Previous researchers have also reported a significant relationship between

ethnicity and consumer’s credit behaviour and found that ethnic has a

26

significant effect on the probability of using bankcards instead of checks. White

(1975) explained that nonwhites might find it more difficult to obtain sufficient

credit, and is therefore more likely to use store cards as a means of financing

and they tend to use credit card as a means of installment credit and thus tended

to have more credit card debt. Belinger and Valencia (1982) indicated that

Hispanics were less likely to be credit card holders than Anglo-Americans.

Furthermore, Lindley et al., (1989) indicated that Anglos were more likely to

use credit cards as payment methods in all types of consumer purchases than

were Hispanics.

More recently, Metwally (2002) study the dual banking system in Qatar and the

impact of demographic factors on consumer’s selection of a particular bank,

concluding that the market position of any bank within such a system in a

developing country is likely to change with the process of development that

results in significant changes in age structure, level of education, job mobility

and standards of living.

Moreover, Avery et al. (1986) have found those credit cards were treated

merely as one of several forms of payment methods. Findings from these papers

further supported the strong positive correlation between income, education,

wealth, urbanicity, and “middle-age” and credit card use. Their summary

position was that ‘different means of payment have different uses that vary over

socioeconomic classes”. Finally, the possession and usage may vary across

27

individuals, for instance purchasing habits may differ among males and females

and individuals’ race may also affect. After all, we would expect more educated

persons to possess credit card than those who have been poorly educated. In

short the demographic characteristics of one individual may reveal information

about the credit card possession and their usage.

2.2 Possession and Usage of Credit Card

In recent years, credit card use and ownership have expanded around the globe

substantially, bringing a “buy now, pay later” philosophy to the forefront. This

pronounced attitude has increased purchases of all types as a result of the

growth of the credit usage, encouraging consumption that would not otherwise

take place. Apparently the relationship between spending desirability with

income earned experiencing dramatic changes in the past few years (Surtherland

and Canwell, 1994). Those with more disposable income discovered to indulge

with leisure and social activities. To some people it led them to incur debt credit

card, which allow them to spend beyond their means. It is becoming a trend that

consumers today live beyond their financial capacity, and not realizing that their

expenditures consistently exceed their income (Mapother, 1999).

Apparently, past studies have indicated that the ways the credit cards are being

used vary between those who use credit cards as a convenience and those who

use them as a regular source of revolving consumer credit (Peter and Olsen,

28

1994). In effect, every credit card transaction implies an interest free loan for at

least thirty days. Therefore, convenience use of credit cards can be positively

related to the higher age, income and relative financial liquidity of the

household head. In contrast, a liberal attitude toward borrowing can be

positively related to use of revolving credit (Canner and Cyrnak, 1986).

In addition, cross tabulation of the holders by professional also revealed that the

higher incomer earners were interested in transaction convenience rather than

installment buying (Barker and Sekerkaya, 1992; Plummer, 1971; Walker and

Sauter, 1974). It has been further pointed out that convenience use can be

positively related to household age, income and relative financial liquidity.

Moreover, it is approved that convenience users generally charge greater dollar

amounts per month than revolvers, and the amount charged per month for both

types of credit users rises with family income (Canner, 1988).

Danes and Hira (1990) investigated the relationship between knowledge, beliefs

and practices in the use of credit cards. They collected data during 1982 and

found that the respondents who believed that credit cards should be used for

installment reasons were inclined to use more credit cards and to accumulate

finance charges more often. Respondents who were older and those with low

incomes believed that credit cards should be used for convenience reasons. In

addition, credit cards are predominantly used for some types of purchases, such

as telephone and Internet transaction.

29

Besides the convenience factor, Kaynak et al. (1995) found that previous credit

card literature also showed that there is a close relationship between credit card

usage and the level of economic development in a country. As the economies of

the region move further toward privatization and as free market conditions

prevail, consumer incomes will increase, and a strong middle class will emerge,

hence the increase of credit usage (Lucas, 1991). Whereas, the work of Chan

(1997) highlighted that there is positive association between usage rate and

income. This is due to the fact that most of the card issuers normally grant a

higher credit limit among the higher income group. At the same time the

wealthier cardholders many times prefer to use credit card in their purchasing

transactions.

Many studies have concluded that the dramatic growth in credit card use since

the 1980s due to the change in attitude toward credit (Canner and Cyrnak, 1980;

Godwin, 1998; Norton 1993) such a change in attitude implies that consumers

are more willing to use credit to finance current consumption. In Greek the

majority of credit cards spending is concentrated on three types of purchases

namely clothing, special items and nightclubs. Clothing is the most frequent

type of purchase. It was found that credit card spending for purchase of clothing

is estimated to be 16 billion drachmas spent per year (Meidan and Davos, 1994).

Special items such as jewellery and furs are the second most frequent type of

purchase, with 7 billion drachmas spent per year followed by spending in

nightclubs and restaurants with 5 billion drachmas per year.

30

While in Turkey, it is reported that 71.6 percent were using bank credit cards to

purchase clothing, shoe, furniture and electrical appliance. It also found that

married respondents used bank credit cards more often than single (Delener and

Katzenstein). However in China, the credit cardholders more often used their

cards in restaurants, hotels or entertainment venues, rather than in shops as

discovered in Turkey (Worthington, 2003) due to several reasons as such not all

goods can be purchased by credit card.

Regarding types of credit cards they are use, in a cross-national study conducted

by Kaynak and Yucelt (1984), it was discovered that there were similar patterns

in ownership and use between Canadian and US credit cardholders. While US

users tended to rely more on bank credit cards than did Canadians, MasterCard,

Visa and Discover were found to be the most popular credit cards used in both

countries. The cards were used for purchasing goods and services and for

identification purposes, but most respondents did not use the cards to their

maximum potential (Kaynak and Yucelt, 1984). A contrast situation exists in

Japan where domestic credit card acceptance marques are more familiar than the

international marques of MasterCard or Visa, because the majority of credit

cards on issue are for domestic use only (Worthington, 1998).

In terms of using frequency, retail credit card users differ from bankcard users

in many ways. Consumers who have store credit card indicate that they send

about twice as much, and rate the store higher on customer service than

31

customers who do not have the card (Credit World, 1988). In addition, the

shopping frequency of consumers using store credit cards is significantly higher

than those shoppers without store credit cards, reflecting the tendency of store

credit holders to maintain loyalty to that store.

Further study by Kaynak et al. (1995), which examined the frequency of credit

card usage, found that majority of the Turkish credit cardholders used their

cards less than once a week. Females, higher educated people and the higher

income groups use their credit cards more often than do their counterparts.

However, age and job do not play a statistically significant role and the heaviest

users of credit card in Turkey are come from middle age (Arora, 1987; Kinsey,

1981). This is consistent with Chebat et al. (1988) reported that in Canada,

income and education are positively related to frequency of credit card usage.

According to Warwick and Mansfield (2000), study on college students

revealed that two-thirds of the students responding possessed at least one credit

card. Of those students who owned cards, 22.8 percent owned only one, 20

percent owned two credit cards, and almost 4 percent had over 5 credit cards.

Hayhoe et al., (2000) found that effective credit attitude influenced credit card

purchasing behaviour among college students. Students with higher effective

credit attitudes were more likely to purchase goods, such as clothes, electronic

items, entertainment, travel, gasoline and auto repair and food away from home,

with credit cards.

32

Although there is quite a lot of literature on credit cards usage internationally,

very limited published research is available in Malaysia. Most of the studies

have been conducted in the United States and other developed countries.

33

CHAPTER 3

METHODOLOGY, DATA AND VARIABLES

To accomplish the foregoing research objectives, the survey approach was adopted,

which contained multiple-choice questionnaire, requiring the respondent to give fixed

responses to the statements or questions asked. Shomaker and Mccombs (1989)

indicated that surveys have proven to be an effective way to assess people’s vote

intentions, to explain their votes, to predict use of products, and to assess changes in

opinions.

3.1 The Nature of Study

This study is a descriptive one in nature. According to Sekaran (1992),

descriptive study is undertaken in order to ascertain and to be able to describe

the characteristics of variables in situations and also undertaken to describe the

relevant aspects of the phenomena of interest to the researcher whether from an

individual, organizational, industry or other perspective. Descriptive analysis

will be used to discuss the possession and usage of credit card among staffs in

Universiti Utara Malaysia.

34

3.2 Sampling Method

3.2.1 Sample Size

A sample is a subset of the population. It comprises some members selected

from the population. By studying the sample, it would be able to draw

conclusions that would be generalized to the population of interest. In this

study, the sample consists of staff in UUM, who currently own a credit card in

their name. A number of 235 staffs from various faculty, department, centre and

unit (see Appendix 1) were selected as a sampling frame. Sample was randomly

selected from the list of faculty, department, centre and unit members available

on UUM website.

This study uses non-probability sampling design such as, convenience sampling

method in order to choose sample of the population (Kerlinger, 1973) and

confidence in determining sample size proposed by Krejcic and Morgan (1970).

Respondents who took part in the survey were not selected by any criteria. They

were selected randomly based on the elements of convenience and accessibility.

3.3 Data Collection Technique

In this study, data is obtained from both primary and secondary sources. Early

studies have been done through secondary sources to gather all the related

35

information to support the literature review and process of building the

questionnaire.

3.3.1 Primary Source

This study depends heavily on data from the primary sources via mail surveys.

The data are gathered from the relevant respondents by sending the

questionnaire via internal mail. The questionnaires are mailed to 235 staffs

along with self-addressed, return envelopes including cover letter explaining the

purpose of the study. The sample comprises of 117 academic staff and 118 non-

academic staff. The technique employed also has its own unique advantages.

For instances, in situations where an appropriate sampling frame is available,

mail surveys always render a more representative sample than mall intercepts

(Churchill, 1992).

After three weeks waiting period, the questionnaires are retrieved from the

respondents. Of a total of 120 questionnaires returned, only 3 could not be used

due to incompleteness and inconsistencies. Final analysis is based on 117,

which was considered as complete, acceptable and usable, yielding 49.79

percent response rate. This response rate is quite high which is acceptable by

social science standards. This contradicts with the findings by Steeh (1981) that

stated low response rate generally associated with mail surveys. In addition,

emphasis is placed on confidentiality by guaranteeing anonymity of

36

respondents’ names. The main content of the questionnaire was related to

customers’ demographic, socioeconomic, possession and usage of credit card.

3.3.2 Secondary Source

Secondary sources are used to support and strengthen the study outcome. Data

from secondary sources will help the researcher to have in-depth knowledge

about the research topic. Secondary data are obtained through an extensive

library research, particularly from journals and articles and published reports of

the other researchers. Information are also gathered from reports such as the

Bank Negara Malaysia Annual Report, magazines and newspapers, pamphlets

published by banks and Internet (bank websites) as well as on-line journals from

Emerald Intelligence and Ebsco-Host.

3.4 Development of Questionnaire

A questionnaire was first developed and pre-tested using a sample of 50 credit

cardholders, which were staff members of Faculty of Finance and Banking,

UUM. After making the necessary modifications, the final questionnaire was

generated. The research instrument consists of a self-administered closed end

structured question, which is divided into three parts. The first part is used to

gather the demographic and socioeconomic information of the sample. The

second and third parts of the questionnaire are concerned with the information

37

related to the possession of credit card and usage of credit card among UUM

staffs respectively.

3.4.1 Layout

The questionnaire is logically structured to make completion

straightforward. The format is designed to promote quick and simple

responses by just ticking appropriate answer. Three separate sections of

the questionnaire, which are used in the data analysis, are reported

herein.

The first section of the questionnaire is designed to collect relevant

demographic and socioeconomic information from each respondent.

Such information included gender, race, age, marital status, number of

dependency, years working in UUM, monthly income and job category.

The respondent demographic and socioeconomic characteristics chosen

for this study are slight revisions of those criteria found to be statistically

significant in an earlier study. Gender is included because women seem

to be having greater impact on financial services decisions as they

achieved greater social liberalization (Anderson et al., 1976). Responses

to this first section of the questionnaire are designed to permit analysis

of the first research objective included in the study.

38

According to the research done by Maysami and Williams (2002) they

found that 56.1% cardholders in Singapore were male and the rest are

female. With regard to level of education, 45.9% of the respondents

have degree and married. The majority of the cardholders work in

offices (professional, manager and executive) with 47.8% cardholder’s

personal annual income were between S$30,000-S$39,999.

Other study has found that likely credit cardholders came from higher

income and more financially astute families. However, the major reason

for use was convenience and this factor was positively correlated with

financial liquidity, income and age Canner and Cyrnak (1985, 1986). In

addition, the study carried out by Martell and Fitts (1981) and Kaynak et

al. (1995) also showed that bank credit cardholders normally had higher

income, were better educated, owned multiple bank accounts and

employed a stable pattern of banking.

The second section includes questions pertaining to the number of credit

card owned, usage frequency of credit card, types of credit card and

factors that motivate the respondent to select a credit card. Past credit

card literatures indicated that there is a high correlation between

increased income level and rate and frequency of credit card usage

(Garcia, 1980). Further, questions such as what factors that motivate the

39

respondent to own a credit card and how did they find out information

about their credit card also incorporate in this section.

The final section is designed to generate data concerning the credit

card’s usage. In order to answer the research objective, questions such as

usage frequency, rationale for using credit card, their involvement in

online purchase, reasons for using credit card, knowledge about the

interest charged, terms and condition applied on credit card are asked. In

addition, question such as the amount spent every month via using credit

card and choice of payment are also included.

Respondents are assured of complete confidentiality in answering all the

questions. The questionnaire is written in English. A copy of the survey

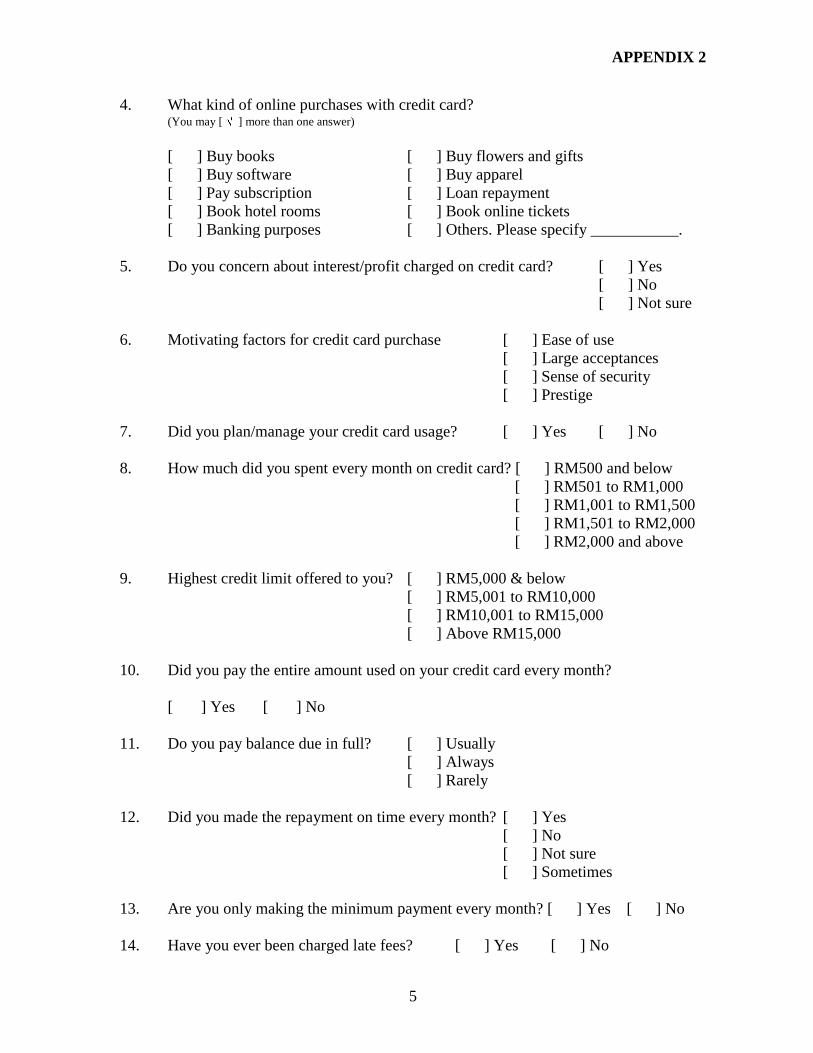

instrument is attached in Appendix 2.

3.5 Data Analysis

The responses to the credit card’s possession and usage among staff in UUM are

analyzed using Statistical Package for the Social Sciences (SPSS). An

exploratory study is conducted using descriptive frequencies and percentages to

describe the data obtained.

40

CHAPTER 4

FINDINGS AND ANALYSIS

4.1 The Demographic and Socioeconomic Characteristics

The analysis is based on usable responses received from 117 respondents. The

first section describes the analysis of frequency of demographic and

socioeconomic characteristics of the respondents. The results are shown in the

form of tables and figures, which are easier to understand and to analyze.

4.1.1 Gender

With respect to gender, the 117 sample respondents are evenly

distributed between two major gender categories. The sample contains

52.1% males and the rest were females (47.9%). With regards to

quantity, 61 respondents are males while 56 respondents are females.

Hence, the potential results of this analysis will show whether there are

any significance differences between male and female respondent’s

credit card possession and usage.

41

Table 4.1.1: Respondent Profiles by Gender

4.1.2 Race

Obviously, our respondents participated in this study come from two

major races that is Malay and Indian. It is clear from Table 4.1.2 that

majority of the respondents are Malays with a total of 114 respondents

or 97.4%, followed by Indians with a total of 3 respondents (2.6%)

respectively. The main reason is, majority of the staff are Malay and

only a small group, which represents Chinese, Indian and others.

Table 4.1.2: Respondent Profiles by Race

Characteristics Percentage

Malay

Indian

97.4

2.6

Total 100.0

Characteristics Percentage

Male

Female

52.1

47.9

Total 100.0

42

4.1.3 Age

There are six different categories of respondent’s age, comprising of age

of 26 to 30 years old, 31 to 35 years old, 36 to 40 years, 41 to 45 years

old, and above 45 years old. It is obvious that respondents of age

between 26 to 40 years old dominate the sample distribution amongst the

five major age categories, as displayed in Table 4.1.3.

Table 4.1.3: Respondent Profile by Age

Characteristics Percentage

26-30 years

31-35 years

36-40 years

41-45 years

Above 45 years

35.9

35.0

17.9

0.9

10.3

Total 100

Most of the respondents are from the age of 26 to 30 years and 31 to 35

years with a total of 42 (35.9%) and 41 (35%) respectively. This means

that the respondents’ age is evenly distributed between the two major

age categories mentioned. About 21 or 17.9% represent respondents of

age 36 to 40 years. The other 1 respondent (0.9%) and 12 respondents

(10.3%) belong to age group between 41 to 45 years old and above 45

years old respectively.

43

4.1.4 Marital Status

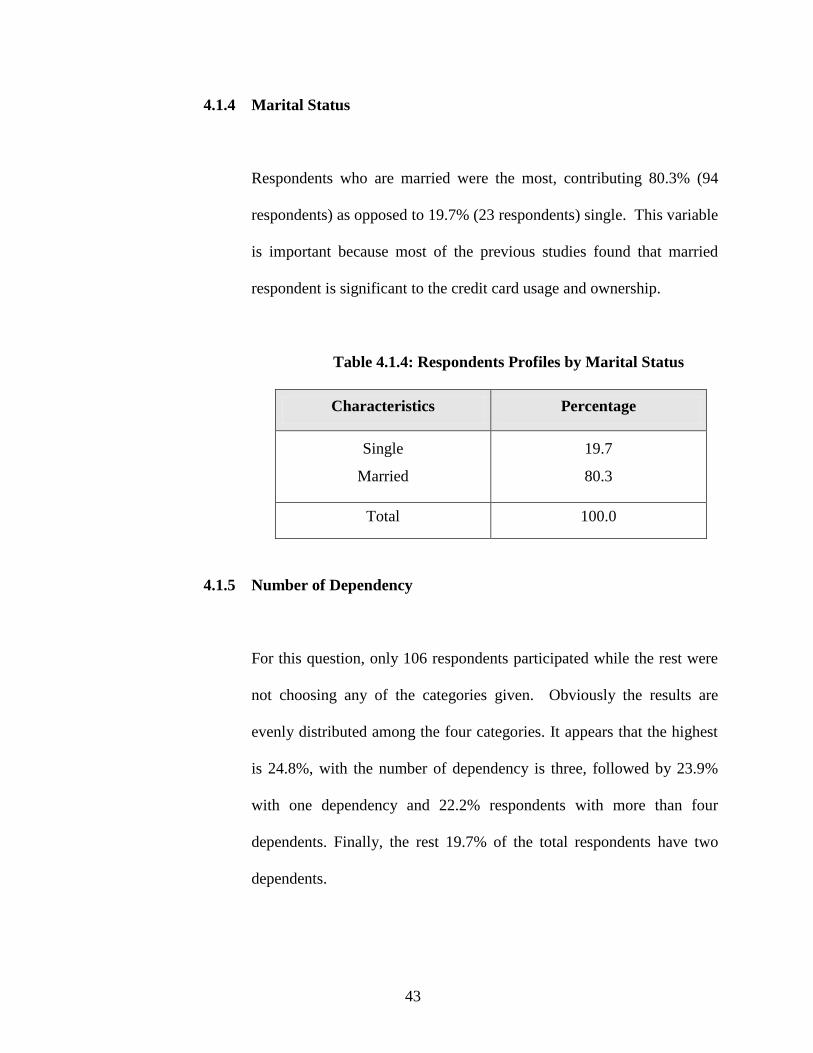

Respondents who are married were the most, contributing 80.3% (94

respondents) as opposed to 19.7% (23 respondents) single. This variable

is important because most of the previous studies found that married

respondent is significant to the credit card usage and ownership.

Table 4.1.4: Respondents Profiles by Marital Status

Characteristics Percentage

Single

Married

19.7

80.3

Total 100.0

4.1.5 Number of Dependency

For this question, only 106 respondents participated while the rest were

not choosing any of the categories given. Obviously the results are

evenly distributed among the four categories. It appears that the highest

is 24.8%, with the number of dependency is three, followed by 23.9%

with one dependency and 22.2% respondents with more than four

dependents. Finally, the rest 19.7% of the total respondents have two

dependents.

44

Table 4.1.5: Respondents Profiles by Number of Dependency

Characteristics Percentage

One

Two

Three

Four and Above

23.9

19.7

24.8

22.2

Total 100.0

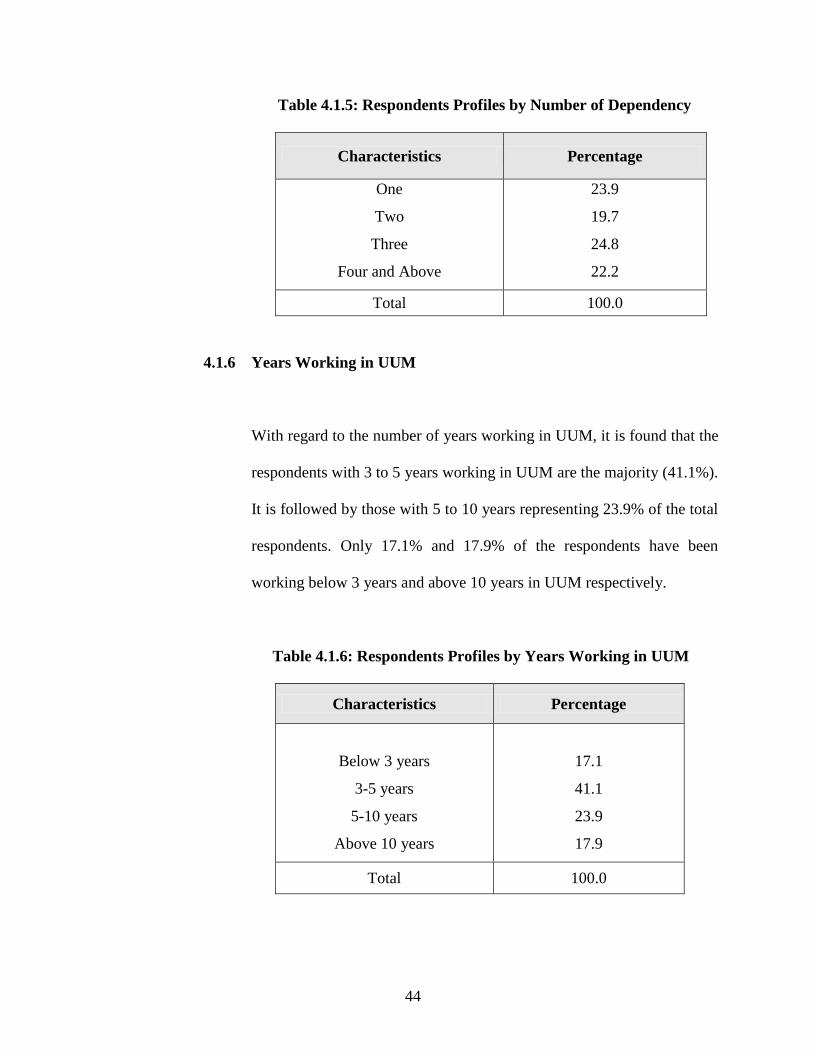

4.1.6 Years Working in UUM

With regard to the number of years working in UUM, it is found that the

respondents with 3 to 5 years working in UUM are the majority (41.1%).

It is followed by those with 5 to 10 years representing 23.9% of the total

respondents. Only 17.1% and 17.9% of the respondents have been

working below 3 years and above 10 years in UUM respectively.

Table 4.1.6: Respondents Profiles by Years Working in UUM

Characteristics Percentage

Below 3 years

3-5 years

5-10 years

Above 10 years

17.1

41.1

23.9

17.9

Total 100.0

45

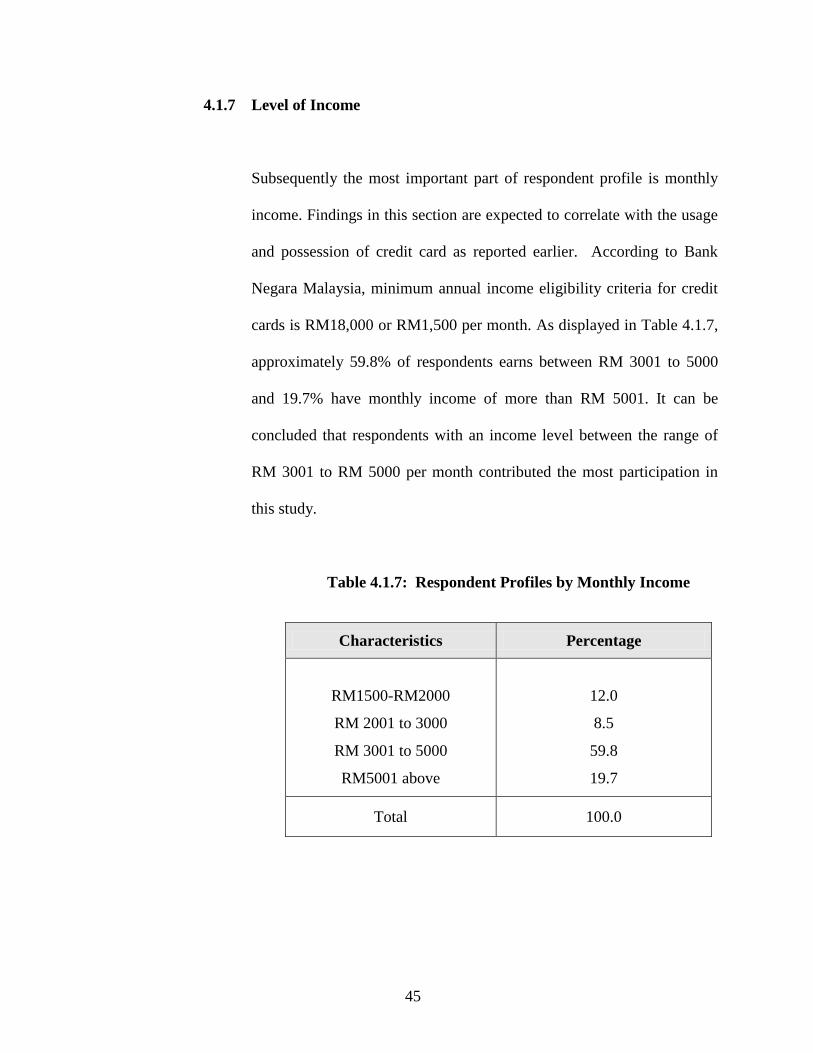

4.1.7 Level of Income

Subsequently the most important part of respondent profile is monthly

income. Findings in this section are expected to correlate with the usage

and possession of credit card as reported earlier. According to Bank

Negara Malaysia, minimum annual income eligibility criteria for credit

cards is RM18,000 or RM1,500 per month. As displayed in Table 4.1.7,

approximately 59.8% of respondents earns between RM 3001 to 5000

and 19.7% have monthly income of more than RM 5001. It can be

concluded that respondents with an income level between the range of

RM 3001 to RM 5000 per month contributed the most participation in

this study.

Table 4.1.7: Respondent Profiles by Monthly Income

Characteristics Percentage

RM1500-RM2000

RM 2001 to 3000

RM 3001 to 5000

RM5001 above

12.0

8.5

59.8

19.7

Total 100.0

46

4.1.8 Job Category

Interestingly, as shown in Table 4.1.8, the majority of the respondents

comprise of academician including tutor and language teacher, which

represents approximately 88.9% or 104 of the total number of

respondents working in UUM. Jobs such as accountant, registrar,

assistant registrar, executive officer, secretary and clerk are classified

under management staff. Management staff only represents 11.1% of the

respondents or 13 in terms of number.

Table 4.1.8: Respondent Profiles by Job Category

4.1.8 Level of Education

Based on Table 4.1.9, majority of respondents are found to hold Masters

Degree, which represent 73.5% of the total sample or 147 respondents

while 18.8% or 22 respondents with PhD. Further were a total of 9.4%

or 11 respondents holding a diploma. The rest 1.7% or 2 respondents

Characteristics Percentage

Academician

Management

88.9

11.1

Total 100.0

47

hold bachelor degree. As expected, many respondents possess a higher

level of education since majority of the respondents are academic staffs.

This type of respondents is expected to have more exposure to the

financial and banking matters in order to fulfill their financial needs.

Table 4.1.9: Respondent Profiles by Level of Education

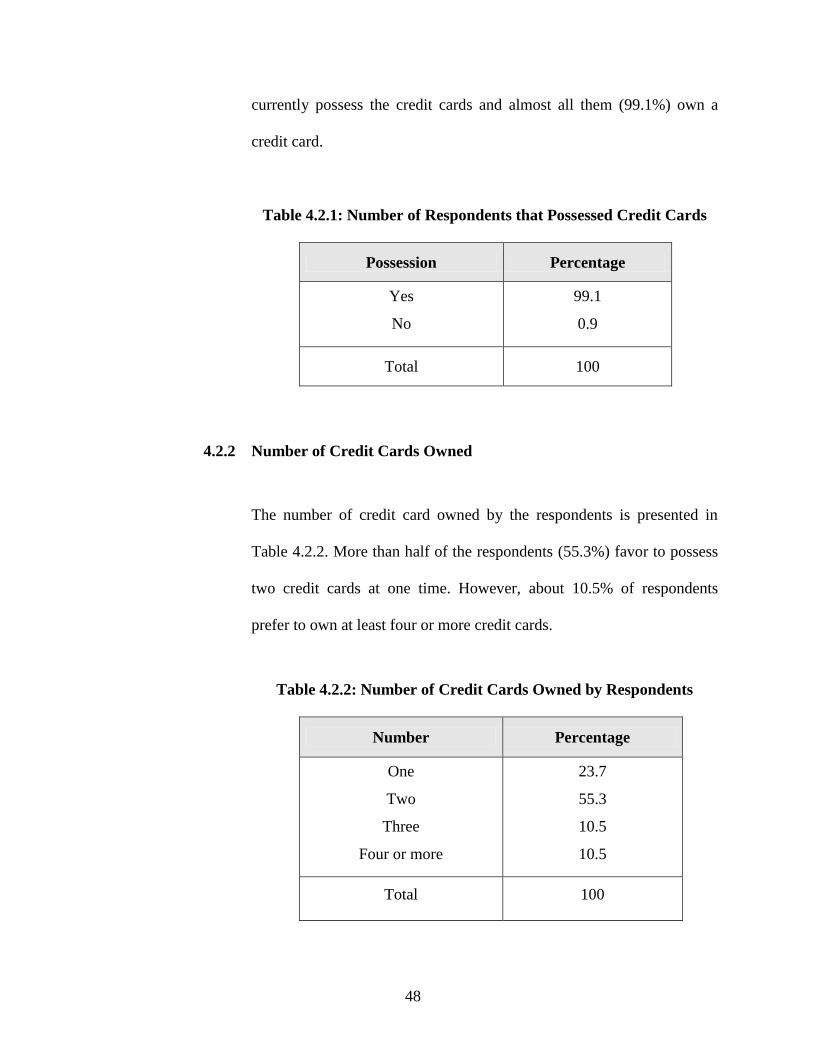

4.2 Possession of Credit Card

Section B of the questionnaire is designed to study the possession or ownership

of credit card among staffs in UUM.

4.2.1 Credit Card Possession

Nowadays, people prefer to own a credit card because credit card is a

convenient payment mode as it can be readily used for making purchases

at merchant outlets. Table 4.2.1 shows the number of respondents that

Characteristics Percentage

Diploma

Bachelor Degree

Masters Degree

PhD

9.4%

1.7%

70.1%

18.8%

Total 100.0

48

currently possess the credit cards and almost all them (99.1%) own a

credit card.

Table 4.2.1: Number of Respondents that Possessed Credit Cards

Possession Percentage

Yes

No

99.1

0.9

Total 100

4.2.2 Number of Credit Cards Owned

The number of credit card owned by the respondents is presented in

Table 4.2.2. More than half of the respondents (55.3%) favor to possess

two credit cards at one time. However, about 10.5% of respondents

prefer to own at least four or more credit cards.

Table 4.2.2: Number of Credit Cards Owned by Respondents

Number Percentage

One

Two

Three

Four or more

23.7

55.3

10.5

10.5

Total 100

49

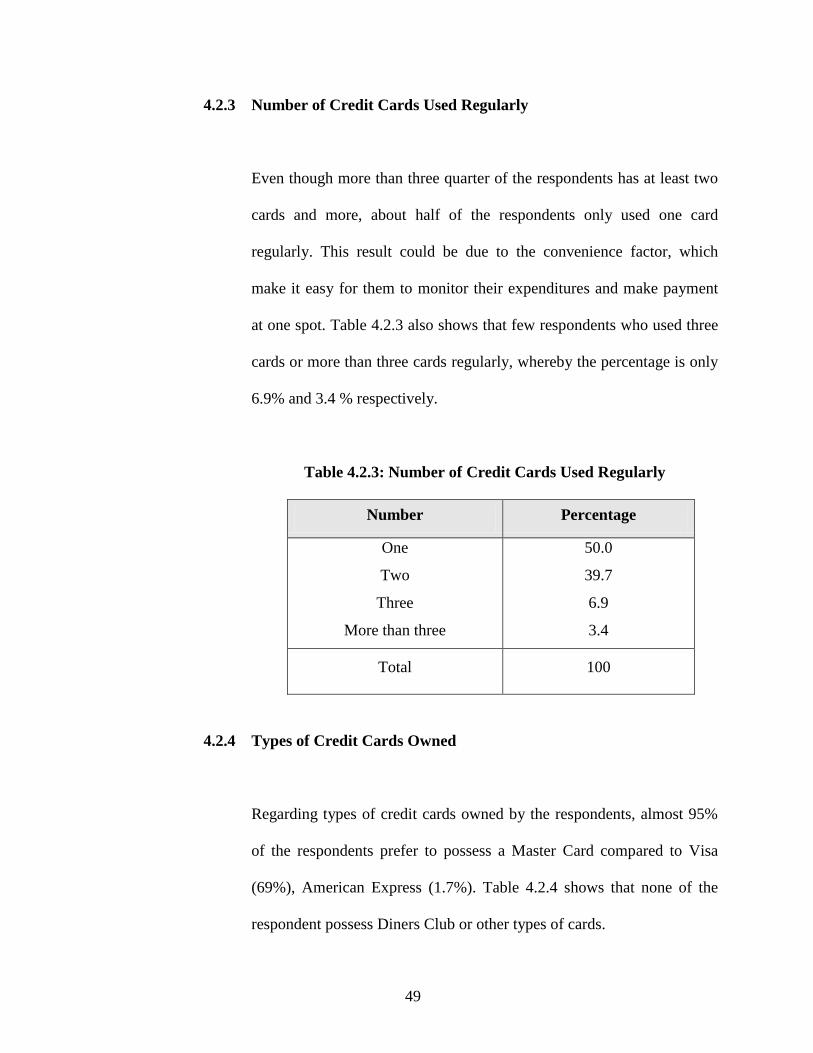

4.2.3 Number of Credit Cards Used Regularly

Even though more than three quarter of the respondents has at least two

cards and more, about half of the respondents only used one card

regularly. This result could be due to the convenience factor, which

make it easy for them to monitor their expenditures and make payment

at one spot. Table 4.2.3 also shows that few respondents who used three

cards or more than three cards regularly, whereby the percentage is only

6.9% and 3.4 % respectively.

Table 4.2.3: Number of Credit Cards Used Regularly

Number Percentage

One

Two

Three

More than three

50.0

39.7

6.9

3.4

Total 100

4.2.4 Types of Credit Cards Owned

Regarding types of credit cards owned by the respondents, almost 95%

of the respondents prefer to possess a Master Card compared to Visa

(69%), American Express (1.7%). Table 4.2.4 shows that none of the

respondent possess Diners Club or other types of cards.

50

Table 4.2.4: Types of Credit Cards Owned

Types Percentage

Visa

MasterCard

American Express

Diners Club

Others

69.0

94.8

1.7

0.0

0.0

4.2.5 Preference of Credit Cards

The credit line provided by the Islamic credit card has attractive and

competitive features as those of conventional credit card issuers.

Therefore, more financial institutions are now offering the facility as an

alternative to conventional credit card. Based on Table 4.2.5, 69.4% of

the respondents prefer to have both Islamic and conventional credit

cards rather than sticking to one type only, either Islamic credit card or

conventional credit card.

Table 4.2.5: Preference of Credit Cards

Types Percentage

Conventional

Islamic

Both

6.3

24.3

69.4

51

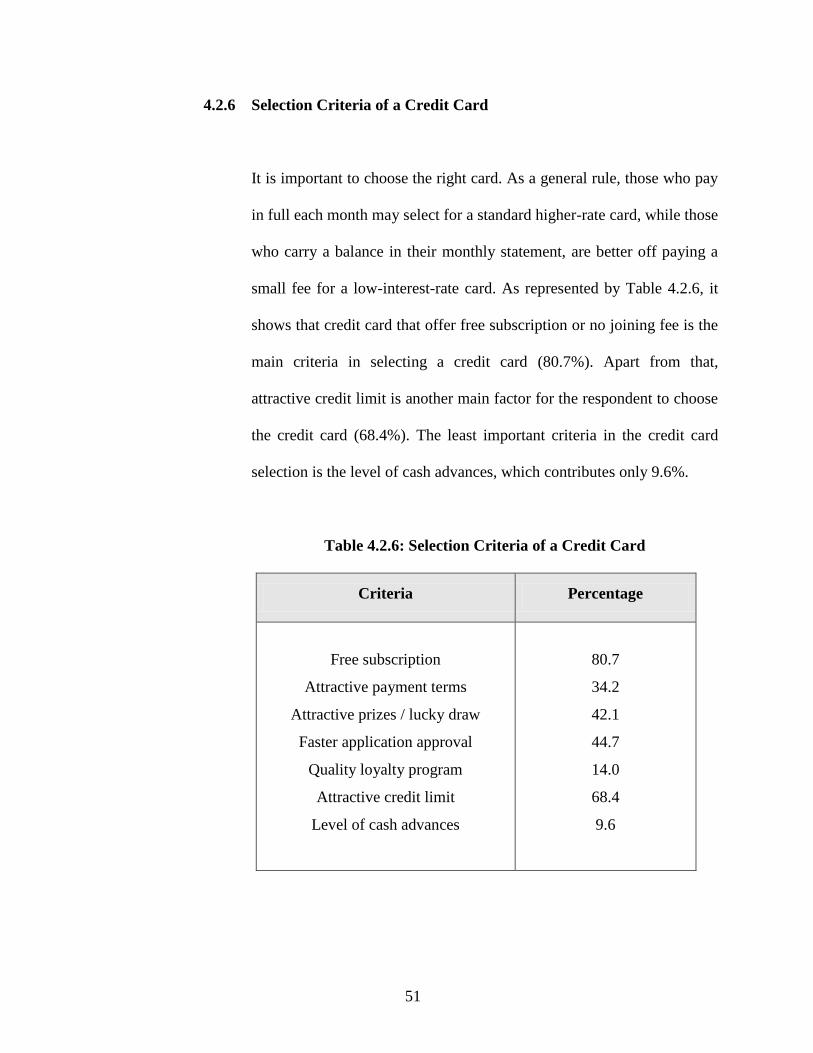

4.2.6 Selection Criteria of a Credit Card

It is important to choose the right card. As a general rule, those who pay

in full each month may select for a standard higher-rate card, while those

who carry a balance in their monthly statement, are better off paying a

small fee for a low-interest-rate card. As represented by Table 4.2.6, it

shows that credit card that offer free subscription or no joining fee is the

main criteria in selecting a credit card (80.7%). Apart from that,

attractive credit limit is another main factor for the respondent to choose

the credit card (68.4%). The least important criteria in the credit card

selection is the level of cash advances, which contributes only 9.6%.

Table 4.2.6: Selection Criteria of a Credit Card

Criteria Percentage

Free subscription

Attractive payment terms

Attractive prizes / lucky draw

Faster application approval

Quality loyalty program

Attractive credit limit

Level of cash advances

80.7

34.2

42.1

44.7

14.0

68.4

9.6

52

4.2.7 Purpose of Possessing Credit Card

There are a few reasons for possessing a credit card. As showed in Table

4.2.7, 86.2% of the respondents indicate that the main reason of owning

the credit card is for their own convenience whereby it enables the

respondents to make purchases of goods and services at any time instead

of using cash. Only 16.4% of the respondents feel that, by possessing a

credit card, it represents or indicates the prestige that they have. This

condition may be applicable for those who owned platinum cards since

the qualification to possess platinum card is very high.

Table 4.2.7: Purpose of Possessing Credit Card

Purpose Percentage

Convenience

Indication of prestige

Sense of security variables

Economic variables

Global acceptance

86.2

16.4

19.8

44.8

38.8

4.2.8 Sources of Information on Credit Card

The information about credit card mostly comes from friends and

relatives (61.2%) rather than marketing strategy (54.3%) conducted by

53

banks. This shows that friends and relatives are more reliable because

these people can really share their valuable experience with the

respondents especially on the advantages and disadvantages of

possessing a credit card. As indicates in Table 4.2.8, internet networking

seems to be the least effective source of information on credit card

whereby the percentage is only 10.3%.

Table 4.2.8: Sources of Information on Credit Card

Sources Percentage

Television

Magazine

Internet

Friends and relatives

Sales representative

Bank’s marketing strategy

18.1

45.7

10.3

61.2

44.0

54.3

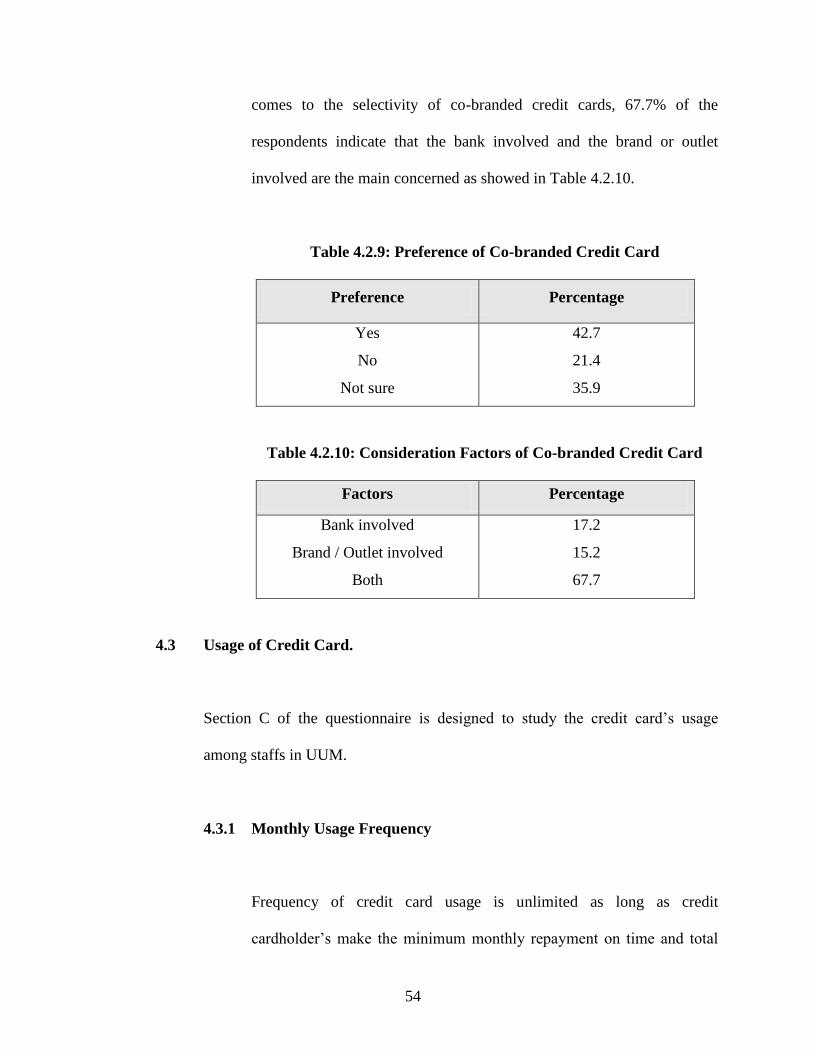

4.2.9 Co-branded Credit Card

A co-branded credit card is a card, which issued jointly by a credit card

issuer and a merchant under a well-known brand name. The merchant

normally offers additional benefits to the cardholders, such as discount

on certain products and reward points for the purchases made. As

presented in Table 4.2.9, 42.7% prefer co-branded credit card. When it

54

comes to the selectivity of co-branded credit cards, 67.7% of the

respondents indicate that the bank involved and the brand or outlet

involved are the main concerned as showed in Table 4.2.10.

Table 4.2.9: Preference of Co-branded Credit Card

Preference Percentage

Yes

No

Not sure

42.7

21.4

35.9

Table 4.2.10: Consideration Factors of Co-branded Credit Card

Factors Percentage

Bank involved

Brand / Outlet involved

Both

17.2

15.2

67.7

4.3 Usage of Credit Card.

Section C of the questionnaire is designed to study the credit card’s usage

among staffs in UUM.

4.3.1 Monthly Usage Frequency

Frequency of credit card usage is unlimited as long as credit