credit reports & scores original author: peggy olive richland county uw-extension with...

TRANSCRIPT

Credit Reports & Scores

Original author: Peggy Olive Richland County UW-ExtensionWith Adaptations by Bridget Mouchon from WHPE power-point and

other Extension resources.

All Credit is Not Equal

Good Credit

vs.

Bad Credit

Credit ties upfuture income

for today’s expenses.

Managing Your Credit

• Every time you pay a bill (or don’t) it contributes to your credit history– Paying ‘slow’ or not at all is seen as a

warning to other lenders– Signs of ‘Risky behavior’– May result in

• Higher interest rates and fees• More rejections of loans• Smaller loan amounts

Credit Risk (to you & to lenders)

28/36 Rule • A good credit risk when mortgage

payments are below 28% of gross monthly income, and total debt payments are below 36%.

Types of Credit• Revolving Credit Account

• Credit cards – MasterCard, Discover, Visa, JC Penney, etc.

• Charge Account• Utilities, dentist, Diners Club, etc.

• Installment Loans• Car loan, mortgage, student loan,

payday loan, etc.

Secured vs. Unsecured

Dischargeable vs.

Non-dischargeable

Types of Credit

Credit Cardsvs.

Debit Cards

Credit CardsPros:• Credit history• Emergencies• Perks• Disputes• $50 liability

Cons:• Interest

rates• Late fees• Annual fee?• Cash

advance fees

Debit CardsPros:• No interest• Quick cash• Online

purchases

Cons:• Fees

•Overlimit•Point of sale•Who’s ATM?

• Blocking• $500 liability?

• Pay Day Loans• Rent to Own• Car Title Loans• Pawn Shops

400-800%

40-700%• Rapid Tax Refund Anticipation Loans

Subprime Types of Credit

Pay Day Loans

• The average loan is rolled over 4 times.

Making Minimum Payments on a Credit Card

Balance: $1000Annual Interest: 18%Minimum Payment: 3% or $30

Know How Much Today’s Credit Will Cost You

Tomorrow

$1000.00Payment #1 -- 30.00

970.00Interest + 14.55

New Balance = 984.55Payment #2 -- 29.54

New Balance = 955.01Interest +

14.33New Balance = 969.34

Late Fee + $35 =

$1004.34Overlimit Fee + $35 =

$1039.34

• It will take 69 payments to pay off the $1000 original balance.

• The finance charge will be $472.51 not including any late fees or over-limit charges.

• The original $1000 now costs $1472.51

Pop Quiz

What is a credit report?

A credit report tells…

•How you’ve paid your debts•How much debt you have•Whether you’ve made

payments on time

What’s in your credit report?

Credit reports contain…

•Identifying information•Credit history•Inquiries•Public record information

Credit reports DON’T contain…

Credit reports DON’T contain…

• Checking or savings account balances

• Income• Medical history• Purchases made with cash or

checks• Business account information• Race, gender, religion, national

origin• Driving record

Who cares about your

credit report?• Creditors / Lenders• Insurance Companies• Landlords• Employers• Utility Companies• Government Agencies• YOU!

Credit Reporting Agencies

•Equifax•Experian•TransUnion

Getting your FREE Credit Report

Consumers are entitled to receive one free credit file disclosure every 12 months from each of

the nationwide consumer credit reporting companies.

FREE Credit Report• www.annualcreditreport.com

• 1-877-322-8228

• Annual Credit Report Request ServicePO Box 105281Atlanta GA 30348-5281

Credit Report Sections

1. Personal Information2. Public Records3. Potentially negative items4. Accounts in good standing5. Optional Consumer

Statement

Credit Report Sections

6. Special Messages7. Hard Inquiries8. Soft Inquiries9. Directions to Correct Errors

Disputing Wrong Information on Credit

Reports• You can dispute mistakes or outdated

items for free. Ask the credit-reporting agency for a dispute form or submit your dispute in writing, along with any supporting documentation. Do not send them original documents.

• If the reinvestigation does not resolve your dispute, have the credit bureau include your version of the dispute in your file and in future reports.

• Fico Score most widely used• Vantage Score – 3 Bureaus• Many other “score” brands

Credit Scores

Credit Scores Cont…

• A credit score is referred to as a FICO score.– Based on models developed by Fair Isaac Corporation.

• The models begin with information on your report, using it to calculate your score.

• Scores range from 300-850.– The majority are between 600 and 800.– They vary from one credit bureau to another.

• Visit www.myfico.com/ScoreEstimator.html to get an estimate of your score.

What does my score mean?

• What is a good score?– The national average is 678.– This is often the minimum for receiving credit.

• A good credit score doesn’t just mean that you’ll get a loan, it also means you’ll pay less for it.

• A low FICO score may result in a credit card rate twice that of a high FICO score.

FICO Score

Source: Fair Isaac Corporation

Factors That Determine Your Score

Your Payment History

– Lenders want to know how you have handled credit payments in the past.

Amount You Owe and Your Available Credit– Shows the amount

you owe on your mortgage, car loan, and all other outstanding debt, along with your total available credit.

Factors That Determine Your Score

Length of Credit History

– The longer the credit accounts have been opened, and the longer you have had accounts with the same creditor, the higher your credit score.

Types of Credit Used– The wider the

variety of credit, the higher the score.

– Using different types of credit indicates you know how to handle your money.

Factors That Determine Your Score

New Credit – New applications for credit will

lower your score. – Those moving towards

bankruptcy take all available credit to stay afloat.

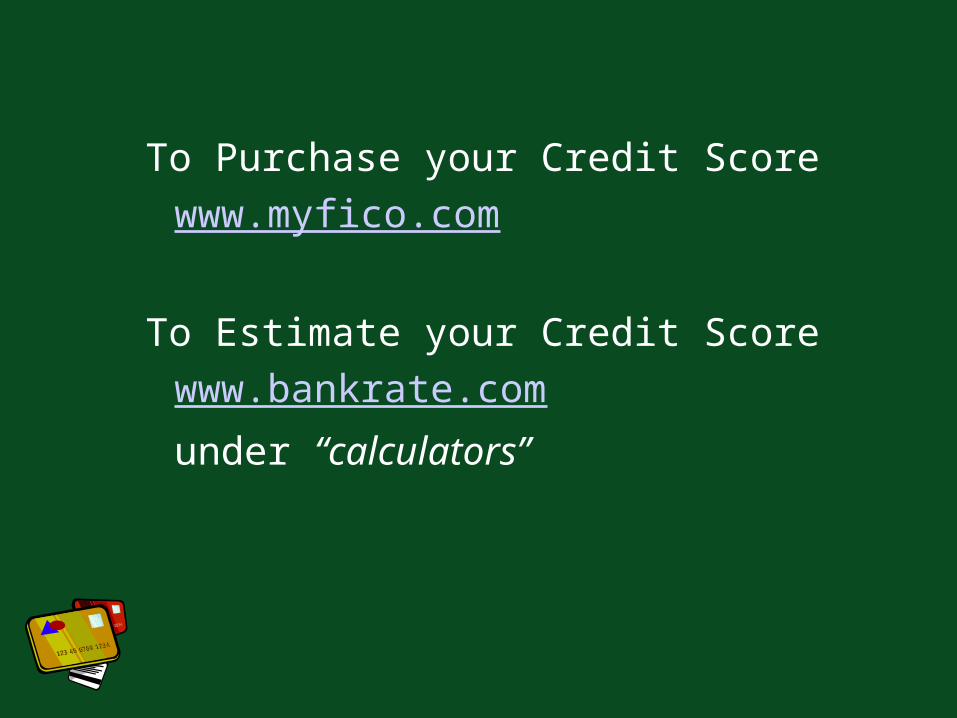

To Purchase your Credit Scorewww.myfico.com

To Estimate your Credit Scorewww.bankrate.com

under “calculators”

Catching up on credit payments:

$ Don’t take on any new debt

$ Use “PowerPay” strategy

“Power Pay” Concept• Pay your credit payments as usual.• When first loan is paid off . . .

. . . apply that payment to the next loan.

• When loan two is paid off . . .. . . add that payment to the next loan.

• Continue this process until all loans are paid off.

Utah State University Extensionwww.powerpay.org

Power Pay StrategyDiscove

rMasterCar

dDoctor

April $22 $35 $35

May $22 $35 $35

June $57 $35 $0

July $57 $35 ---

August $57 $35 ---

September $0 $92 ---

October --- $57 $35

…and so on --- $92 $0

When you can’t pay bills . . .

• Act now!• Financial Counseling