credit risk securitization and bank soundness - … · credit risk securitization and bank...

TRANSCRIPT

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 1/29André Uhde

Credit Risk Securitization and Bank SoundnessEvidence from the Micro-Level for Europe

Tobias C. MichalakAndré Uhde

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 2/29André Uhde

Motivation I

Remarkable growth of the market for credit risk securitization worldwide and particular in Europe since 1997.

Micro-level: diversification of concentrated credit risk exposures, alternative source of funding. Macro-level: reduction of the overall concentration of credit risk in the entire financial system.

General reassessment of risks inherent in structured finance instruments across the whole financial community due to the subprime crisis from mid-2007.

IMF values mark to market losses on structured finance instruments at approx. 1,405 bn USD (IMF, 2010).

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 3/29André Uhde

Motivation II

As a response the Basel Committee has recommended important proposals for enhancing the Basel II-framework in the area of securitization (BCBS, 2009).

Pillar 1: Higher risk weights to securitization exposures (higher minimum regulatory capital requirements),

Pillar 2: Additional stress-testing and addressing securitization business in the supervisory review process (SRP),

Pillar 3: Strengthening disclosure requirements with regard to securitization exposures and special purpose vehicles (SPV).

Consultation process proposed to end in July 2010.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 4/29André Uhde

Motivation III

Against this background this paperempirically investigates the impact of credit risk securitizations on bank soundness,using a unique sample of 749 cash and synthetic transactions,issued by 60 stock-listed bank holdings from the EU-13 plus Switzerland,over the period from 1997-2007.

We complement previous empirical studies for several aspects:First study for European banking markets,Accounting-based z-score and further market-based distance-to-default measures included as proxies for bank soundness,IV estimations to control for probable reverse causation,Evaluation of different “effect channels”,Large variety of sensitivity analyses.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 5/29André Uhde

Theoretical background (micro-level)

The impact of credit risk securitization on the originating bank’s financial soundness is ambiguous and depends on various aspects:

In relation to senior tranches being transferred, the sum of credit default risks in the first-loss position typically retained by the bank as a quality signal towards external investors (Jiangli et al., 2007; DeMarzo, 2005),

The risk-level of new assets being funded with liquid capital from true sale securitization transactions (Krahnen and Wilde, 2008),

The degree of diversification of the bank’s overall asset portfolio after having taken in these new assets (Cebenoyan and Strahan, 2004),

The opportunity to realize regulatory capital arbitrage by means of securitization due to missing former Basel I-regulations on this business field.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 6/29André Uhde

Empirical evidence I (Event studies)

Lockwood et al. (JBF, 1996)296 securitization announcements and issue dates (121 from banks) from 39 originators in the U.S. between 1985 an 1992,positive impact of credit risk securitization on the bank’s systematic risk,stronger impact for pre-event financially weaker banks.

Franke and Krahnen (WP, 2006)73 securitization announcements of 27 banks in Europe between 1999 and 2002,positive impact of credit risk securitization on systematic risk.

Hänsel und Krahnen (WP,2007)159 securitization announcements from 49 listed banks in Europe and U.S. between 1999 and 2003,positive impact of credit risk securitization on systematic risk,stronger impact for pre-event financially weaker banks in Europe.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 7/29André Uhde

Empirical evidence II (Event studies)

Uhde and Michalak (forthcoming JBF, 2010)592 announcement and issue dates of cash and synthetic securitizations from 54 European banks between 1997 and 2007,positive impact of credit risk securitization on systematic risk,increase in systematic risk is more relevant for larger banks that repeatedly engage in securitizationsecuritization is more important for small and medium financial institutions,banks have a higher incentive to retain the larger part of credit risk as a quality signal at the onset stages of securitization business in Europe,the overall risk shifting effect due to securitization is more distinct when the pre-event systematic risk is low.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 8/29André Uhde

Empirical evidence III (Panel data analyses)

Dionne and Harchaoui (WP, 2003)Panel data on Canadian commercial banks between 1988 and 1998,Negative impact of credit risk securitization on bank regulatory capital,Negative impact on bank asset quality.

Uzun and Webb (JRF, 2007)Panel data on 112 banks in the U.S. between 2001 and 2005,Negative relationship between securitization and bank capitalization, Positive effect of mortgage loan securitizations on bank profitability.

Jiangli and Pritsker (WP, 2008)Panel data on U.S. BHC between 2001 and 2007,Negative impact of mortgage loan securitizations on bank soundness and capital environment, positive effect on bank profitability.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 9/29André Uhde

Empirical analysis: Data I (z-score)

Consolidated balance sheet data from 60 stock listed bank holdings in Western Europe for 1997-2007 provided by Fitch’s Bankscope database.

Bank soundness measured as the bank’s distance to insolvency (modified, accounting-based Altman z-score, popular in relevant empirical banking studies).

with µi,t as the ROAA of bank i at time t (bank’s profitability), ki,t as the equity capital to total assets (bank’s capital

environment), σi,t as the standard deviation of the ROAA (bank’s return volatility,

3 years rolling window).

z-score increases with µ and k and decreases with σ.higher (lower) z-score implies lower (higher) probability of insolvency.z-score substituted by further market-based distance-to-default measures.

i ,t i ,ti ,t

i ,t

zμ κσ+

≡

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 10/29André Uhde

Empirical analysis: Data II (securitization)Data obtained from offering circulars and presale reports provided by Moody’s, Standard and Poor’s and FitchRatings.Securitization is included as the one-period lag of the log of the cumulated volume of credit risk securitization by bank i at time t

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 11/29André Uhde

Empirical analysis: Data III (securitization)

Development of the volume of credit risk transfer through securitization during the sample period (in million €)

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 12/29André Uhde

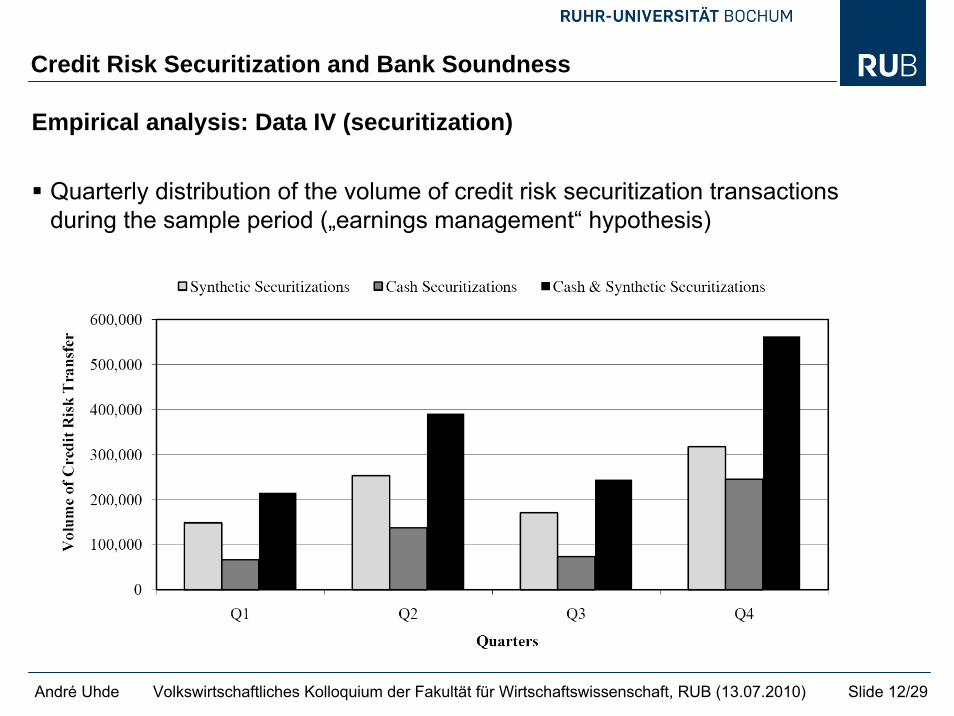

Empirical analysis: Data IV (securitization)

Quarterly distribution of the volume of credit risk securitization transactions during the sample period („earnings management“ hypothesis)

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 13/29André Uhde

Empirical analysis: Data V (securitization)

Frequent securitizers of cash transactions (n=529) and synthetic transactions (n=220)

Cash TA: 67.0% of the total volume by 10 most frequent issuers

Synthetic TA: 78.4% of the total volume by 10 most frequent issuers

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 14/29André Uhde

Empirical analysis: Data VI (control variables)

Macroeconomic measures (WDI Database)- Real GDP growth- Annual change in inflation ratest-1

- Annual real short term interest rates

Bank-specific measures (BankScope)- Business (ratio of non-interest to interest income)- Tier1 (Tier1 capital to risk weighted assets)- MBR (market-to-book ratio, market value of equity capital to its book value)- Delta net loanst-2

- Moral hazard index (proxy for risk-taking behavior under deposit insurance)

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 15/29André Uhde

Empirical analysis: Model specification I

Linear regression on panel data

where…yit represents the z-score ratio of bank i at time t,cit is the cumulated volume of credit risk securitization of bank i at

time t,xit is the vector of control variables,eit is the error term,αit is the constant term with αit = α + vi(α = bank-specific time-invariant component, vi = remaining disturbance).

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 16/29André Uhde

Empirical analysis: Model specification II

Time dummies to control for time-specific effects (regulatory changes, financial shocks etc.)

Clustered-robust SE at the bank-levelto address for heterogeneous securitization frequencies,to correct for a possible downward bias in the estimated standard errors (Moulton, 1990) that might stem from different aggregation levels of our bank-specific and macro-variables,H0 of homoscedasticity of the generalized Lagrange multiplier test based on White (1980) is rejected at ρ<0.000.

Random effects modelsuitable since the interest of inference relates to a population mean, i.e. stock-listed banks in our sample are viewed as sampled from an overallpopulation (whole banking sector),H0 of the Arellano test (1993) that the individual specific effect is uncorrelated with the independent variables cannot be rejected at ρ<0.853.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 17/29André Uhde

Empirical results – Baseline findings I

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 18/29André Uhde

Empirical results – Baseline findings II

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 19/29André Uhde

Empirical results – Robustness checks IBaseline findings may be biased due to reverse causality problems.

Banks typically use securitization to overcome regulatory frictions (capital requirements). Thus, banks exhibiting high risk exposures are more likely to employ securitization.

If this is true, causality running from securitization to bank soundness (risk) is not clear.

We instrument securitization using legislation and R&D expenses.

Legislation: proxies for the de jure development of a country’s legal and regulatory framework concerning securitization in banking.

Index variable based on cross-country information from a report provided by the European Financial Lawyers Group (2007). The index ranges from 0 to 10 with higher values indicating a more pronounced legal and regulatory environment.

R&D: proxies for the de facto usage of securitization by banks.

Data is retrieved from the WDI database provided by the World Bank. We assume that R&D may be an appropriate proxy for the cross-disciplinary research field of “financial engineering”.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 20/29André Uhde

Empirical results – Robustness checks II

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 21/29André Uhde

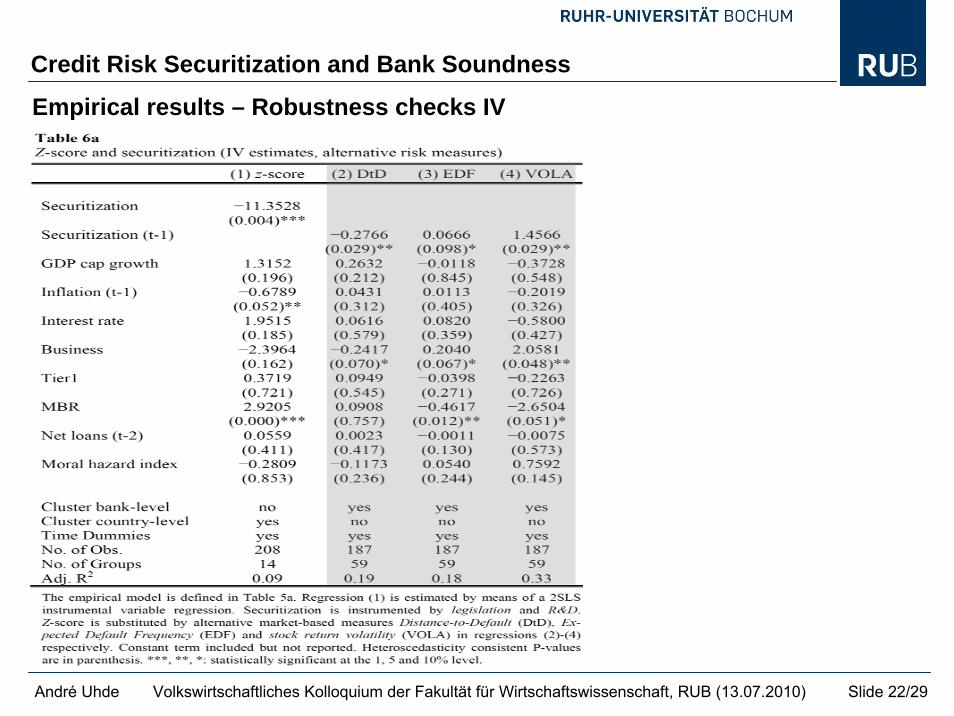

Empirical results – Robustness checks IIIWe substitute the accounting-based z-score ratio by three market-based measures of distance-to-default since our sample solely comprises stock-listed BHC.

Employing the Merton framework (1973, 1979) we include ratios that measure the default point (distress barrier): market value of assets falls below the market value of debt

Distance-to-Default (DtD)

Expected Default Frequency (EDF)

Volatility of the securitizing bank’s stock returns (VOLA)

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 22/29André Uhde

Empirical results – Robustness checks IV

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 23/29André Uhde

Preliminary conclusionBaseline results are in line with the “securitization-fragility” view from previous theoretical and empirical studies: negative impact of credit risk securitization on European banks’ financial soundness.

Explanation for empirical findings?

Two “effect-channels”:

1. Banks in our sample may predominantly employ securitization as a source of regulatory capital arbitrage / quality signaling by retaining the major part of credit risk in the first-loss position (direct effect).

2. Banks in our sample may use liquid capital from selling true sale securitization transactions as an additional funding source to take in more risky assets when restructuring their overall asset portfolios (indirecteffect).

Both effects result in a more risky overall asset portfolio ex post.

Indirect evidence for these effect-channels by regressing on single z-score components.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 24/29André Uhde

Empirical results – Effect-channels

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 25/29André Uhde

Sensitivity analyses

Banking and capital market structures- Entry restrictions (PCA, Barth et al., 2008)- Lerner-index (own calc.)- Stock market capitalization (Beck et. al., 2000)- Stock market turnover ratio (Beck et. al., 2000)

Regulatory and supervisory measures (Barth et al., 2008)- Capital regulatory index (PCA)- Private monitoring index (PCA)- Official supervisory power (PCA)

Institutional environment- Shareholder rights index (own calc. following La Porta, 1998)- Rule of law (WGI)

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 26/29André Uhde

Empirical results – Sensitivity analyses I

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 27/29André Uhde

Empirical results – Sensitivity analyses II

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 28/29André Uhde

ConclusionEmpirical results of a negative impact of credit risk securitization on bank soundness are in line with the “securitization-fragility” from theoretical models and confirm previous empirical studies by Uzun and Webb (2007) for the Canadian banking sector as well as Dionne and Harchaoui (2003) for the U.S. banking market.

Our analysis provides empirical evidence for two effect-channels, i.e.

(1) European banks retain the major part of credit default risk in the first-loss position (direct effect)

(2) Banks follow a more risky reinvestment strategy ex post (indirect effect).

Against this background proposals by the Basel Committee are a step in the right direction.

Improving minimum capital requirements concerning securitization activities is mandatory.

Strengthening disclosure requirements concerning the (off-balance sheet) first-loss position is essential.

Credit Risk Securitization and Bank Soundness

Volkswirtschaftliches Kolloquium der Fakultät für Wirtschaftswissenschaft, RUB (13.07.2010) Slide 29/29André Uhde

Thanks for your attention!

Dr. André UhdeUniversity of Bochum, Germany

Department of EconomicsEmail: [email protected]