credit union invocation - ballincollig credit union...

TRANSCRIPT

ord make me an instrument of Thy peace,

Where there is hatred, let me sow love,

Where there is injury, pardon;

Where there is doubt, faith;

Where there is despair, hope;

Where there is darkness, light;

And where there is sadness, joy.

Divine Master, grant that I may

not so much seek to be consoled as to console;

to be understood as to understand;

to be loved as to love;

for it is in giving that we receive;

it is in pardoning that we are pardoned;

and it is in dying that we are born to eternal life.

L

O

Credit UnionInvocation

Notice of

Annual General Meeting

Notice is hereby given that the

ANNUAL GENERAL MEETING of

Ballincollig Credit Union Ltd. will

take place in The Oriel House Hotel

on Monday 17th December 2012

at 8.00pm sharp.

Pat MooreSecretary

1

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Agenda for Annual General Meeting

Credit Union Invocation

The acceptance by the Board of Directors of the authorised representatives of members thatare not natural persons.

Ascertainment that a quorum is present.

Adoption of Standing Orders.

Reading and approval (or correction) of the minutes of the 2011 AGM.

Report of the Board of Directors.

Report of the Treasurer, consideration of accounts and approval of Treasurer’s honorarium.

Report of the Auditor.

Report of the Credit Committee;

Declaration of dividend and rebate of interest.

Adoption of Motions and Rule Amendments.

Report of Credit Control Committee.

Report of Marketing, Education, Promotion, & Sponsorship Committee (MEPS)

Report of Membership Committee.

Report of Finance/Investment Committee.

Report of the Supervisory Committee.

Report of the Nominating Committee.

Appointment of Tellers.

Election to fill vacancies on the Board of Directors (5), Supervisory Committee (1), and the Auditor.

Approval of International Development Foundation Fund contribution.

Any other business.

Announcement of election results.

Adjournment or close of meeting.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

2

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Board of Directors1. Catherine Greene2. John P. Curtin3. Pat Moore4. Irene Byrne5. Mary O’Mahony6. Breda Callanan7. Karen Bohane8. Finbarr Bradley9. Denis O’Sullivan10. Paddy McCarthy11. Paul Healy

Secretary : Pat Moore

Company Number : 347CU

Registered OfficeCredit Union House,Harrington Street,Ballincollig,Co. Cork.

AuditorsMoore Stephens NathansChartered Accountants &Registered Auditors,83, South Mall,Cork.

Business AddressCredit Union House,Harrington Street,Ballincollig,Co. Cork.

BankersAllied Irish Banks,Main Street, Ballincollig,Co. Cork.

SolicitorsO’Donnell, Breen-Walsh, O’DonoghueTrinity House, 8 George’s Quay, Cork.

Credit Committee1. Bob O’Hea 3. Catherine Greene2. Irene Byrne 4. Breda Callanan

Credit Control Committee1. Mary O’Mahony 3. Paddy McCarthy2. Sheila Maguire

Marketing, Education, Promotion & Sponsorship1. Mary O’Mahony 3. Linda Walsh O’Neill2. Catherine Greene

Membership Committee1. Marie Kierse 3. Ann Marie Cosgrove2. Donal O’Regan 4. Ann Quinn

Finance/Investment Committee1. John P. Curtin 5. Sarah Kidney2. Denis O’Sullivan 6. Martin Desmond3. Catherine Greene 7. Colin Irwin4. Dermot Long

Supervisory Committee1. Michael Sealy 3. John O’Brien 2. Nicola O’Connell

Management & Staff

C o m p a n y I n f o r m a t i o n

Mary BrowneNiamh BuckleyPhil CallanMary ColemanAnn-Marie CosgroveHelen Deasy Peg HayesColin IrwinSarah KidneyMaria KierseDermot Long

Margaret McGeoughAlison MurphyEdel MurphyOwen O’DohertyBridget O’DonoghueKaren O’SheaAnn QuinnNicola QuinnElizabeth WalshLinda Walsh O’NeillSinead Leavey

(Chairperson)(Treasurer)(Secretary)(Vice-Chairperson)

Unit 12,Ballincollig Shopping Centre,Ballincollig,Co. Cork.

3

4

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Standing Orders

VotingEach member shall be entitled to one voteirrespective of his/her shareholding, inaccordance with Standard Rule 139.

Election ProcedureNominations may be accepted from the floorin accordance with Standard Rule 137.Election to the Board of Directors, to theSupervisory Committee, and the position ofAuditor shall be by a majority vote and bysecret ballot. A ballot paper for the election of the Boardand the Supervisory Committee, whereapplicable, will be distributed to eachmember at the A.G.M.

MotionsAll motions from the floor of the A.G.M.must be proposed and seconded bymembers present at the A.G.M. and movedby the proposer. If the proposer is absentwhen the motion is called, the motion shallbe deemed to have failed. A proposer of a motion may speak for suchperiod as shall be at the discretion of theChairman of the meeting and shall have theright of reply before the motion is put to themeeting for a vote.In exercising his/her right of reply, aproposer may not introduce new material. The seconder of the motion shall have suchtime as shall be allowed by the Chairman tosecond the motion. Members are entitled to speak on any suchmotion and must do so through the Chair.All speakers to any motion shall have suchtime as shall be at the discretion of theChairman. The Chairman shall have the absolute rightto decide at any time when a motion hasbeen sufficiently discussed and may put themotion to the meeting giving the proposerthe right of reply before doing so.

MiscellaneousThe Chairman of the Board of Directorsshall be the Chairman of any generalmeeting, except where he/she is notavailable, then it shall be the Vice-Chairman,except where he/she is not available, inwhich case the Board shall decide amongst

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

themselves who shall act as Chairman of anygeneral meeting. The Chairman may at his/her discretion,extend the privilege of the floor to anyperson who is not a member.Matters not covered by the Agenda may beintroduced under “Other Business” at thediscretion of the Chairman. The Chairman’s decision on any matterrelating to these Standing Orders orinterpretation of the same shall be final. In accordance with Standard Rule 132 (1) nomember shall have more than one vote oneach question at any general meeting of thecredit union or any adjournment thereofirrespective of his/her shareholding, or thenumber of accounts in his/her name in thecredit union provided, however, that exceptin voting at elections, the presiding membershall have a second or casting vote in theevent of equality of voting. Voting by proxyshall be allowed only when a member otherthan a natural person votes through arepresentative, who is a member of thegroup, duly authorised in writing for thatpurpose and accepted as such by the Boardof Directors. Refer to Standard Rule 138 alsore election procedure.Any matter to be decided upon by vote at theA.G.M. shall, unless otherwise expresslyprovided for by the law or the rules, bedecided upon by simple majority.

Suspension of Standing OrdersAny one of these Orders or all of theseStanding Orders may be suspended on amotion to this effect receiving a two-thirdsmajority of those present and entitled tovote.

Alteration of Standing OrdersStanding Orders may be amended or alteredat a general meeting and only if a motion tothis effect has received a two-thirds majorityof those present and voting.

AdjournmentsAdjournments of the AGM shall take placeonly in accordance with Standard Rule 132.

12.

13.

14.

15.

16.

17.

18.

19.

5

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

C h a i r p e r s o n ’ s R e p o r t

Dear Members,

On behalf of the Board of Directors of your Credit Union I welcome you to this our 40th AnnualGeneral Meeting where we will present our annual report for 2011. This has been anotherdifficult year but I am delighted to report a surplus of €733,018 an increase of 319% on last yearsresults. Our loan book has continued to decline and at the end of the 2012 stood at €20,303,174- as against €22,971,742 at end of 2011. Member’s shares now stand at €45,018,549 at end of 2012(€47,553,032 -2011).

On the arrears side our provision for bad and doubtful debts has risen by €189,666 to €2,958,359.This is an ongoing source of concern for your Board and in the past year we have allocatedadditional resources to our credit control section. However in these difficult times ofunemployment and financial difficulty we are striving to treat members, who do encounterdifficulties in their personal circumstances, fairly and with sympathy. Again we would urge allmembers who may have difficulties in meeting their obligations to call to us at an early stage andwe will do our best t o help you.

The Board has put a lot of preparation in anticipation of the Credit Union Bill and the changesand compliance requirements associated with this. BCU has invested in a Risc Managementsystem which is now operational on the system and were fortunate to have the expertise in houseto manage the development and implementation of this system. In addition BCU has prepareda new Strategic Plan 2012-2015 with the help of PINTA Consultants and the delivery of thetargets and objectives contained in this plan will allow BCU to become stronger, more secureand assist with expansion in the future. The success of the Plan will involve a lot of hard workfor Board, Volunteers and Staff.

BCU is also committed to reducing the interest rates as part of this Strategic Plan and the Boardhave agreed a reduction of 1% from 1st January 2013.

During the year our WEB access has continued to attract new users and I would encouragemembers who have not already done so to sign up for access to our site. www.bcu.ie

We have continued our involvement with the schools in our common bond who have alwayssupported the Credit Union saving scheme by encouraging the pupils to participate. We thank

6

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

C h a i r p e r s o n ’ s R e p o r t ( C o n t )

the Principals and Teachers for supporting BCU in bringing “The Credit Union” to the youth ofthe Parishes and surrounding areas. It is heartening to see that our membership continues toincrease and we will continue to market BCU as an attractive and friendly financial communityintuition.

I would like to thank the 3219 members who borrowed over €8.5 million from BCU during thepast year. Your Credit Union is a financial co-operative which thrives when members use thefacilities and services which in turn provides an income allowing the organisation to continueand improve our service delivery to you our members. I would ask all members who use theservices of BCU to continue doing so and encourage family members and friends to utilise theservices that BCU has to offer in order to generate more income which will contribute toachieving the target of reduced interest rate in the life time of the Strategic Plan which will be ofbenefit to all members as BCU has the funds to lend and are open for business. BCU iscommitted to the economic sustainability of Ballincollig and will continue to work with theBusiness Association to achieve this end.

As we approach the festive season it is timely to reflect on our members who have passed awayduring the year and we extend our deepest sympathies to their families.

I would like on your behalf to pay a special tribute to my fellow Directors, members of theSupervisory committee and Volunteers on the various committees. They have all served BCUwith diligence and dedication. We always welcome new volunteers and if you have the timeperhaps you would offer your experience and expertise to BCU. I would also like to thank theStaff for their professionalism, courtesy and support at all times.

Finally and most importantly I thank you our members for your co-operation and support. Ourguarantee to you is that we will continue to give, now and in the future, our total priority inserving your needs in an efficient and effective way.

Catherine GreeneChairperson

7

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M o t i o n s & R u l e A m e n d m e n t s

Resolution No. 1

That this Annual General Meeting agrees to amendRule 1 of the Standard Rules for Credit Unions(Republic of Ireland) by the deletion of “andFinancial Services Authority” where it appears inthe definition of “Bank” so as to read as follows:

“Bank” means the Central Bank of Ireland via theoffice of the Registrar of Credit Unions;

Resolution No. 2

That this Annual General Meeting agrees to amendRule 1 of the Standard Rules for Credit Unions(Republic of Ireland) by the insertion of thefollowing definition of “civil partner”:

“civil partner” has the meaning assigned to it bythe Civil Partnership and Certain Rights andObligations of Cohabitants Act, 2010;

Resolution No. 3

That this Annual General Meeting agrees to amendRule 44 (9) of the Standard Rules for Credit Unions(Republic of Ireland) by the insertion of “civilpartner,” after spouse where appearing in line 2 soas to read as follows:

(9) The credit union shall not accept from an officer of the credit union a guarantee for a loan to another member unless that other member is the officer's spouse, civil partner, child or parent.

Resolution No. 4

That this Annual General Meeting agrees to amendRule 136 (2) of the Standard Rules for CreditUnions (Republic of Ireland) by the insertion of “aminimum of ” so to read as follows:

(2) The nominating committee shall consist of a minimum of three members, at least one of whom shall be a director.

Resolution No. 5

That this Annual General Meeting agrees to amendRule 152 (2) (b) of the Standard Rules for CreditUnions (Republic of Ireland) by the insertion of“civil partner,” after spouse where appearing in line 1so as to read as follows:

(2) None of the following persons shall be qualified for election as auditor of the credit union:

(b) a parent, spouse, civil partner, brother, sister or child of an officer or voluntary assistant of the credit union;

These motions & rule amendments are carriedforward from the 2011 AGM.

AMENDMENTS TO STANDARD RULESARISING FROM LEAGUE AGM 2012

Rule 22

That this Annual General Meeting agrees to amendRule 22 of the Standard Rules for Credit Unions(Republic of Ireland) by the deletion of “when thecredit union has been unable to contact the memberfor a period of three years” with “when there has beenno member initiated transaction on the account for aperiod of three years” and substitute the word“ordinary” for “registered” where appearing in line 3so as to read as follows:

Rule 22. Dormant accounts

The credit union may deal with shares and depositaccounts as hereinafter provided when there hasbeen no member initiated transaction on theaccount for a period of three years and when noreply has been received within thirty days from themember to a notice sent, by ordinary post, tohim/her at his/her last known address, of intent bythe credit union to close the account(s). Such shareand deposit accounts shall then be transferred to thereserve account. Dividends and interest shallcontinue to be payable on such accounts.

8

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Minutes of A.G.M. of Ballincollig Credit Union Limited held on Friday December 16th 2011 in the G.A.A. Pavilion, Ballincollig.

Board of Directors present: Catherine Greene. Irene Byrnes, John P. Curtin, Paddy McCarthy, BredaCallanan, Finbarr Bradley, Paul Healy, Mary O’Mahony, Karen BohaneSupervisory: Pat Moore: Michael Sealy; Bob O’HeaStaff: Dermot Long: Sarah Kidney; Colin Irwin: Elizabeth Walsh: Niamh BuckleyAuditor: Ned Murphy: Nathan Moore StephensIn attendance: Anthony Dennehy, ILCU: Fionnula Walsh-Breen

The Chairperson Catherine Greene opened the meeting with the Credit Union Invocation.A quorum was ascertained and followed by the adoption of Standing Orders.Proposed by P Moore and Seconded by J Curtin. Agreed by the meeting:

The Secretary Mary O’Mahony read the minutes of the 2010 AGM.Matters Arising: Dave O’Herlihy proposed that the minutes be corrected to include the Boards agreement tohold an EGM in March 2011 to discuss the interest increase and the options to be outlined in relation toShopping Centre/Harrington St. This agreement was clarified by the Supervisory Committee: The meetingwas never held and Dave O’Herlihy asked for that to be reflected in the minutes. This was seconded by DonalO’Callaghan and agreed.Proposed by Dave O’Herlihy and Seconded by Derry Canty. Agreed by meeting:

Chairperson’s report:

Catherine began her report by outlining the Director’s responsibilities. The Directors are required to selectsuitable accounting policies and apply them consistently, also make judgements and estimates reasonable andprudent. They must prepare financial statements on the going concern basis, safeguard the assets of the creditunion and hence take reasonable steps for the prevention and detection of fraud and other irregularities inaccordance with the Credit Union Act of 1977. Catherine continued her address to the meeting and gave avery comprehensive report in which she • Referenced the performance of BCU in the current economic climate • Mentioned changes to working practice as per the Regulator Instructions• Decisions in relation to • Current status of the internet banking programme• Introduction of the saving stamp machine. • Proposed installation of an ATM machine. • Announced that the Mass for deceased members would be held in January. • Catherine thanked her fellow Directors, the Staff and Management for their support during the year.

Proposed By Pat Moore. Seconded by John Curtin.

M i n u t e s o f 2 0 1 1 A G M

9

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Treasurer’s report:

John Curtin presented the report as per the copy circulated by post to the Membership and expresseddisappointment with the report showing a deficit. This was mainly due to the provision for bad debts, newregulatory requirements, loss in investments and bad debt write off. He also expressed concern in relation tothe decline in the loan book which has reduced considerably and the management costs where he was hopingto make savings. He mentioned that with prudent management he would be hoping for a better report in2012. He responded to various questions on cost of staff uniforms, cost of consultants, security of bonds, baddebt write off and provision and running costs. Due to the increased interest rate in 2011 and the proposalnot to pay a dividend Dave O’Herlihy proposed a vote of no confidence in the Board. This led to a heateddebate with input from Anthony Dennehy, Director ILCU who read the rules in relation to Director’sresponsibilities and outlined some of the scenarios that could happen if the motion was passed. A number ofother speakers advised the membership present as to the legal aspect and the validity of the motion. Daveagreed to defer his motion and bring it up under any other business.

Finance and Investment Report:

This report was read by the Treasurer John Curtin who gave a very detailed assessment of our InvestmentPortfolio which diversified across a mix of products, institutions and maturities which weighted in favour ofshort term deposits He told the meeting the aim is to maximise the return while remaining compliant withthe C.U. Act of 1997, the Trustee [Authorised Investment] Order 1998 and Regulatory requirements.Treasurers Report was agreed on the proposal of John O’Brien and seconded by Brian O’Neill.

Supervisory Committee Report:

Pat Moore, Chairperson of the Supervisory Committee presented the Supervisors report as per the circulatedreport and added that the Committee were disappointed at the decision to increase the interest rate on loanswhile not tackling the increased expenditure and in particular the management and staff costs which werein excess of the guidelines.

Concern was voiced in relation to the recent survey undertaken which was inaccurate with the cost torefurbish Harrington Street and was circulated without the approval of the Board and the responses receivedwere flawed as a result. Concern was also expressed in relation to the proposed non-payment of a dividendand he stated that the incoming Board have to address all of those issues for 2012.Agreed on the proposal of Derry Canty and seconded by Tony Lynch.

M i n u t e s o f 2 0 1 1 A G M ( C o n t )

10

Auditors Report:

Ned Murphy in presenting the Auditors report on behalf of Moore, Nathan Stephens stated that In theiropinion the financial statements give a true and fair view in accordance with generally accepted accountingpractice in Ireland of the state of the affairs of the credit union as at 30th September 2011 and of its incomeand expenditure and cash flows for the year then ended, and have been properly prepared in accordance withthe provisions of the Credit Union Act, 1997. They have obtained all the information and explanations whichwe consider necessary for the purposes of our audit. In their opinion proper books of account have been keptby the credit union, financial statements are in agreement with the books of account. In their opinion theinformation given in the Directors’ Report is consistent with the financial statements. Circulated reportproposed by Ted Murphy, seconded by Brian O’Neill and agreed.

NUMEROUS RAFFLES TOOK PLACE DURING THE COURSE OF THE MEETING.

Credit Committee Report:

Paul Healy delivered the Credit Committee report as per the circulated report and also stated that Ballincolligwas strong and secure and that the reserves were higher that the requirement set out by the Regulator. Proposed by Nicola O’Connell, seconded by Gary O’Brien and adopted:

Credit Control Report:

Paddy McCarthy presented this report as circulated and in response to questions from the floor listed theprocedures taken as part of the bad debt collection process and the procedure to deal with arrears. Proposed by Marian Dineen, Seconded by Phil Cullen and agreed

Marketing Education & Promotion Committee:

Mary O’Mahony delivered the report on the Marketing, Education and Promotion Committee stating thatthe ethos of the credit union was still to hand and that the activities of the community had to be supported.It was the intention of the Committee to focus on reducing the expenditure while maintaining the highestlevels of the goals, mainly increasing the membership, promoting the credit union’s ethics, growing the loanbook and sponsoring many local organizations and groups. After a short discussion in which the cost ofMarketing and promotion was debated the report was adopted on the Proposal of Marian Dineen and seconded by Phil Cullen:

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M i n u t e s o f 2 0 1 1 A G M ( C o n t )

11

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M i n u t e s o f 2 0 1 1 A G M ( C o n t )

Membership Committee Report:

Mary O’Mahony presented the Membership report stating that 315 new members joined last year and addedthat she would like to see this continue to rise over the coming years. Total membership is at 15,500approximately at the end of the year. Life savings, insurance is automatically available to members to joinbefore the age of 70 years. Savings carry life insurance up to €7,700. Debt benefit insurance of €1,300 is takenout by BCU on each member who joins before their 70th birthday. All of these insurances are currentlyprovided at no direct cost to our members. Total paid out under all insurances in the last year was€222,496.61: Beneficiaries can receive up to €23,000 without having to take out probate in the event of thedeath of a member. During the year 36 of the membership died. The Board, supervisors and staff would liketo extend their sincere condolences to the families and wish to remind you that the annual mass for thedeceased members will be celebrated early in the New Year in the churches within the common bond

Proposed By Marion Dineen and seconded by Phil Cullen: Agreed by the meeting.

Report of the Nomination Committee:

Nominations & Election: Mary O’Mahony stated that there were four positions and not five as advertised.Nicola O’Connell, Phil Cullen, Gerry Byrne and Pat O’Connell were appointed as tellers: There were fivenominations, Irene Byrne, Eddie Fitzgerald, Mary O’Mahony, Pat Moore and Paddy McCarthyGary O’Brien was also nominated from the floor for the Board by Ted Murphy seconded by Derry Cantywhich brought the number of candidates to six.John O’Brien was nominated for the Supervisors by Pat Moore Seconded by Dermot Long. Nicola O’Connellwas proposed by Gary O’Brien, seconded by Aoife Greene stepped down as teller and was replaced by RenaO’Connor. Michael Sealy, John O’Brien and Nicola OConnell were the candidates for the Supervisoryvacancies.

The Board proposed Nathan & Co. for the position of Auditors.

Voting Papers were distributed and on completion were collected by the tellers for counting.

The following results were declared following the Members vote which was overseen by Michael SealyMember of the Supervisory Committee and Ned Murphy external auditor.Auditors for 2012: Moore, Nathan, Stephens elected:Board: Irene Byrne 3 years: Pat Moore 3 years: Paddy McCarthy 2 years and Mary O’Mahony 1 year.Supervisory Committee: Michael Sealy 3 years: John O’Brien 2 years: Nicola O’Connell 1 year

12

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M i n u t e s o f 2 0 1 1 A G M ( C o n t )

Honorarium: An honorarium of €10,000.00 gross to be paid to the Treasurer, John Curtin for the excellentwork that he undertakes was agreed on the proposal of Gary O’Brien and seconded by Brian O’Neill.

ANY OTHER BUSINESS

Dave O’Herlihy asked for his original motion in relation to the vote of no confidence be discussed. A numberof people spoke passionately about the situation with the costs of running two outlets and the fact that theinterest rate was increased in 2010 and there was no dividend or interest rebate for 2011. Members spoke oftheir concern of the high management costs of running the two branches so close to each other. Onemember highlighted the issue of the availability of Harrington Street and stated the Town Centre hadadvantage i.e. parking, longer opening hours, and days - Harrington Street because of shorter opening timewas a disadvantage - and members did not have a choice only to go to New Town Centre when HarringtonSt. was closed. The result of a recent survey did not show a true reflection, like with like. Another issue wasthe cost of renting the premises which was seen as dead money. The question of selling the lease or if theBoard could seek to purchase another premises in the Town Centre was discussed. John Curtin replied toNicola O’Connell about the high Consultancy Fees. He stated that Ballincollig Credit Union did not have theexpertise available and said that it was necessary to pay for such expertise. Dave O’Herlihy withdrew hismotion of no confidence stating that he was aware that the Board Members acted in the best interests andwere doing so on a voluntary basis.Dave O’Herlihy then proposed the following motion which was submitted for publication to the generalmembership.“I propose that in the light of the current economic climate that Ballincollig Credit Union retain theregistered office at Ballincollig Credit Union situated at Harrington Street as the sole trading outlet for BCUand that the shopping centre outlet be closed and negotiations entered into with the landlord or landlord’sagents to determine the balance of the lease or sorry to terminate the balance of the lease for BallincolligShopping Centre” This was seconded by a number of people including Irene Healy, Gerry Byrnes, Derry Canty, Pat Moore andBob O’Hea. Fionnula Breen -Walsh advised the AGM in her capacity as Credit Union Solicitor that this couldbe constituted as illegal and was in breach of the lease agreement. However when questioned further shestated that she had not read the lease in question but assumed that it was a standard lease. A discussionensued as to the possibility of selling Harrington Street as it would no longer be used for the business of theCredit Union and under the Act it would have to be disposed of. A long debate took place with variousspeakers supporting the move back to Harrington Street. The following amendment was put to the floor butfailed to secure a seconder “That in the event that this motion is carried and negotiations are entered into,that there is a condition in the motion that if we fail to negotiate our way out of the lease that we do what isfinancially most sensible for the credit union, which is to continue on with one premises in the town centreand close for business in Harrington Street, and utilise the building for the good of the community groupsthat are around”.

13

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M i n u t e s o f 2 0 1 1 A G M ( C o n t )

Tony Lynch asked Ms Breen-Walsh to word the motion in a way that the membership would not beapproving an illegal act but Ms Breen-Walsh said that this would not be possible. Tony Lynch then amendedthe motion to read “I propose that we move across to Harrington Street and re-open the branch on a five daybasis. We enter into negotiations with the landlord of the shopping centre with the view to exiting the lease.And when that is completed all the staff will go to Harrington Street. If Harrington Street requiresrefurbishment then let us get three or four invoices to find out what the cost is”. Pat Moore in seconding theamendment suggested that the amended motion from Tony Lynch should be considered as Ms Breen-Walshstated that the original motion was illegal.

Brian O’Neill then made an amendment to the Motion asking for the successful negotiations to get out of thelease be undertaken prior to the move. “The amendment was that nobody moves from the Shopping Centreto Harrington Street. They stay there until the lease is extinguished or they stay there permanently if it’s notextinguished”. This amendment was seconded by Dermot Long and when put to a vote was defeated by 35-11. Tony Lynch’s amendment was put to the floor and was passed by a vast majority of the Members on ashow of hands.

Catherine thanked everyone for attending and for their patience as it was a very long and acrimoniousmeeting and wished all a Happy Christmas Meeting ended 1.30 am approx.

Catherine GreeneChairperson

Pat MooreSecretary

14

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

15

Directors’ Repor t

STATEMENT OF DIRECTORS’ RESPONSIBILITIESFor the Year Ended 30th September 2012

The Credit Union Act 1997 (as amended) requires the Directors to prepare financial statements for eachfinancial year which give a true and fair view of the state of affairs of the Credit Union and of the Income &Expenditure of the Credit Union for that period. In preparing those financial statements, the Directors arerequired to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Credit Union will continue in business.

The Directors are responsible for keeping proper accounting records which disclose with reasonable accuracyat any time the financial position of the Credit Union and which enables them to ensure that the financialstatements are prepared in accordance with Accounting Standards generally accepted in Ireland and complywith the Credit Union Act 1997 (as amended). They are responsible for safeguarding the assets of the CreditUnion and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

On Behalf of the Board:

Catherine Greene Pat Moore John P. Curtin 27th November 2012 Chairperson Secretary Treasurer

STATEMENT OF SUPERVISORY COMMITTEE’S RESPONSIBILITIESFor the Year Ended 30th September 2012

The Credit Union Act 1997 (as amended) requires the appointment of a Supervisory Committee which willoversee directors in the performance of their functions, examine books and documents of the Credit Union andverify a sample of member balances.

On Behalf of the Supervisory Committee

Michael Sealy 27th November 2012Chairperson

S u p e r v i s o r y R e s p o n s i b i l i t i e s

Tr e a s u r e r ’ s R e p o r t

16

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Introduction

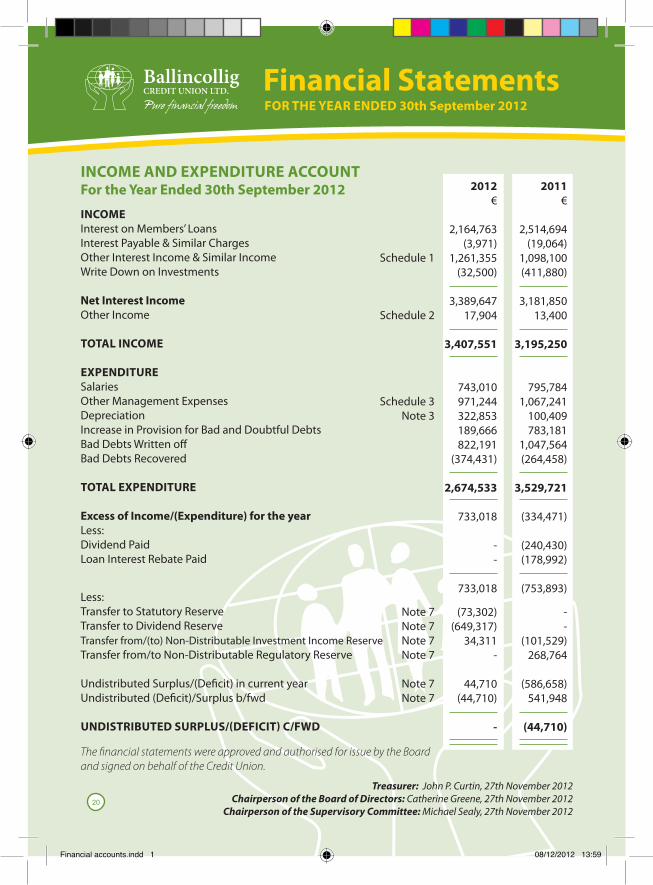

I am happy to submit my report for y/e 2012. This year we have returned to Surplus. €733,018 againsta loss of €334,471 last year.

The main factors in this result were:• Reduction in Bad Debts written off and provided for. Our policy, for the last number of years ofprudent representation of our Loan book has resulted in reduced write-offs.• Our Investment losses have been greatly reduced due to a policy of investment in short-termdeposits. This will be affected in 2013 as deposit interest rates are dropping. Some are now offering lessthan 1% • Reduced Salaries and Operating costs of approx €100,000

Loan Book/LendingDuring the year we granted €8,570,741. This is a reduction of €1,125,734 on last year. This lending isthe life blood of our Credit Union. Ideally we need more members to borrow. I would like to thankthose members who borrowed from B.C.U.and ask you to encourage your friends and family to do thesame.

The balance on the Loan Book has reduced to €20,303,174. This was €22,971,742 last year.Despite this reduction we have managed to maintain our overall income.

This was mainly due to :• Incease in Investment Income €1,261,355 against €1,098,100 last year• Reduction in write down on Investments €32,500 against €411,880The Credit Committee and, indeed, all staff should be congratulated for their work.

The Credit Committee will give you more details of the year’s lending in the Credit Committe report.

Credit Control/Delinquency:The level of arrears continue to climb. This is partly due to the economic climate and stricterregulatory controls of dealiong with members arrears. However previous prudent management of ourLoan Book has reduced the current level of write offs and provisions, This year we wrote off andprovided for an extra €1,011,857 against last year €1,830,745. This shows a reduction of €818,888. The external audit of our Loan Book indicates that these loan write offs may have bottomed out andwe hope to see a further reduction going forward.

17

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

InvestmentsAs with previous years, we are being guided by our professional advisors, Global Reach Securities. Thecommittee and I continued the policy of mainly short term deposit investment.We achieved an averagereturn of 3.68%, in the year to September on our investments, compared to 3.32% in 2011. This isgreater than we had forecast but we cannot expect this rate of return to continue as reduced returns arebeing strongly forecast for the next year. The Regulators liquidity requirements( funds available in lessthan 3 months) demand that we hold at least 20% of our unattached shares in short term deposits;. Iam happy to report that we have liquidity of 25%, well in excess of regulatory requirement. We are alsorequired to hold no more than 25% in any one institution. This proved challenging during the year asAIB, EBS & Anglo (an old investment) are now the one institution. I would like to thank the Financecommittee for the time and effort put into managing our funds.

FutureLike all Credit Unions we have been requested, by the Financial Regulator, to prepare a five yearStrategic Plan. To assist in this we have obtained the services of a specialist firm who have carried outthis process for many Credit Unions. We expect to review all aspects of our operations, new serviceswe can provide to members and areas we can reduce our costs. The process has started and Staff andboard members have been interviewed to get their input. Members have also been asked for theirinput. We expect this plan to be available to us before Christmas and we hope to commence it’simplementation in the new year. The progress on our Harrington Street move will be reported on byour Chairperson.

SummaryBallincollig Credit Union Limited remains in a safe, strong and secure financial position. Theutilisation of reserves to absorb the deficit last year ensured that Ballincollig Credit Union Limited hasa strong and viable future, and shows the value of having built up strong reserves. Our focus is toprotect our members savings and despite Bad Debt and Investment write offs we have achieved this.Our Balance Sheet is strong and we are exceeding the Regulators requirements. We are aware that whilethe economic climate remains difficult, we will have to remain prudent in the management of ourbusiness and the protection of our members funds.. However, we are confident that with the supportof our members and the determination of Directors and staff we will be well positioned to moveforward and continue to be the first choice provider of financial services in our community. I hope tobe able to propose to the members at AGM that we pay a prudent Dividend and Interest Rebate.

I would like to take this opportunity to thank my fellow directors, our supervisors,staff and thevoluntary members of all the committees for their continued support, professionalism words ofwisdom and courtesy at all time.

John Curtin27 th November 2012

Tr e a s u r e r ’ s R e p o r t ( C o n t )

18

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

I n d e p e n d e n t A u d i t o r ’ s R e p o r t

To the Members of Ballincollig Credit Union Ltd.

We have audited the financial statements of Ballincollig Credit Union Limited for the year ended 30September 2012 comprising of the Income and Expenditure Account, Balance Sheet, Cash FlowStatement and related notes.

These financial statements have been prepared under the accounting policies set out herein and theaccounting standards issued by the Accounting Standards Board and promulgated by CharteredAccountants Ireland (Generally Accepted Accounting Practices in Ireland).

Respective responsibilities of the directors and auditorsAs described in the Statement of Directors’ Responsibilities the Credit Union directors are responsiblefor the preparation of the financial statements in accordance with applicable law and GenerallyAccepted Accounting Practice in Ireland including the accounting standards issued by the AccountingStandards Board and published by Chartered Accountants Ireland.

Our responsibility is to audit the financial statements in accordance with relevant legal and regulatoryrequirements and International Standards on Auditing (UK and Ireland).

This report is made solely to the Credit Union’s members, as a body, in accordance with Section 120of the Credit Union Act, 1997 (as amended). Our audit work has been undertaken so that we mightstate to the Credit Union’s members those matters we are required to state to them in an auditor’sreport and for no other purpose. To the fullest extent permitted by law we do not accept or assumeresponsibility to anyone other than the Credit Union and the Credit Union’s members as a body, forour audit work, for this report, or for the opinions we have formed.

We report to you our opinion as to whether the financial statements give a true and fair view inaccordance with Generally Accepted Accounting Practice, and are properly prepared in accordancewith the Credit Union Act, 1997 (as amended). We also report to you whether in our opinion: properbooks of accounts have been kept by the Credit Union and whether the information given in thedirectors’ report is consistent with the financial statements. In addition, we state whether we haveobtained all the information and explanations necessary for the purposes of our audit and whether theCredit Union’s balance sheet and its income and expenditure are in agreement with the books ofaccount.

We read the other information contained in the Annual Report and consider if it is consistent with theaudited financial statements. The other information comprises only the Directors’ Report. We considerthe implications for our report if we become aware of any apparent mis-statement or materialinconsistencies with the financial statements. Our responsibilities do not extend to any otherinformation.

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

19

I n d e p e n d e n t A u d i t o r ’ s R e p o r t ( c o n t )

Basis of audit opinionWe conducted our audit in accordance with International Standards on Auditing (UK and Ireland)issued by the Auditing Practices Board. An audit includes examination, on a test basis, of evidencerelevant to the amounts and disclosures in the financial statements. It also includes an assessment ofthe significant estimates and judgements made by the directors in the preparation of the financialstatements, and of whether the accounting policies are appropriate to the Credit Union’scircumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which weconsidered necessary in order to provide us with sufficient evidence to give reasonable assurance thatthe financial statements are free from material misstatement, whether caused by fraud or otherirregularity or error. In forming our opinion we also evaluated the overall adequacy of thepresentation of information in the financial statements.

OpinionIn our opinion the financial statements give a true and fair view, in accordance with GenerallyAccepted Accounting Practice in Ireland, of the state of the affairs of the Credit Union as at 30September 2012 and of its income and expenditure and cashflows for the year then ended and havebeen properly prepared in accordance with the provisions of the Credit Union Act, 1997 (asamended).

We have obtained all the information and explanations we consider necessary for the purposes of ouraudit. In our opinion, proper books of account have been kept by the Credit Union. The financial statements are in agreement with the books of account.

In our opinion, the information given in the Directors’ Report is consistent with the financialstatements.

Moore Stephens Nathans, 27th November 2012Chartered Accountants &Registered Auditors,83, South Mall,Cork.

John A. Callaghan

Financial StatementsFOR THE YEAR ENDED 30th September 2012

INCOMEInterest on Members’ LoansInterest Payable & Similar ChargesOther Interest Income & Similar IncomeWrite Down on Investments

Net Interest IncomeOther Income

TOTAL INCOME

EXPENDITURESalariesOther Management ExpensesDepreciationInc rease in Provision for Bad and Doubtful DebtsBad Debts Written offBad Debts Recovered

TOTAL EXPENDITURE

Excess of Income/(Expenditure) for the yearLess:Dividend PaidLoan Interest Rebate Paid

Less:Transfer to Statutory ReserveTransfer to Dividend ReserveTransfer from/(to) Non-Distributable Investment Income ReserveTransfer from/to Non-Distributable Regulatory Reserve

Undistributed Surplus/(Deficit) in current yearUndistributed (Deficit)/Surplus b/fwd

UNDISTRIBUTED SURPLUS/(DEFICIT) C/FWD

The financial statements were approved and authorised for issue by the Board and signed on behalf of the Credit Union.

INCOME AND EXPENDITURE ACCOUNTFor the Year Ended 30th September 2012

Treasurer: John P. Curtin, 27th November 2012Chairperson of the Board of Directors: Catherine Greene, 27th November 2012

Chairperson of the Supervisory Committee: Michael Sealy, 27th November 2012

Schedule 1

Schedule 2

Schedule 3Note 3

Note 7Note 7Note 7Note 7

Note 7Note 7

2012€

2,164,763(3,971)

1,261,355(32,500)

3,389,647 17,904

3,407,551

743,010971,244322,853189,666822,191

(374,431)

2,674,533

733,018

--

733,018

(73,302)(649,317)

34,311-

44,710(44,710)

-

2011€

2,514,694(19,064)

1,098,100(411,880)

3,181,85013,400

3,195,250

795,7841,067,241

100,409783,181

1,047,564(264,458)

3,529,721

(334,471)

(240,430)(178,992)

(753,893)

--

(101,529)268,764

(586,658)541,948

(44,710)

20

Financial accounts.indd 1 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

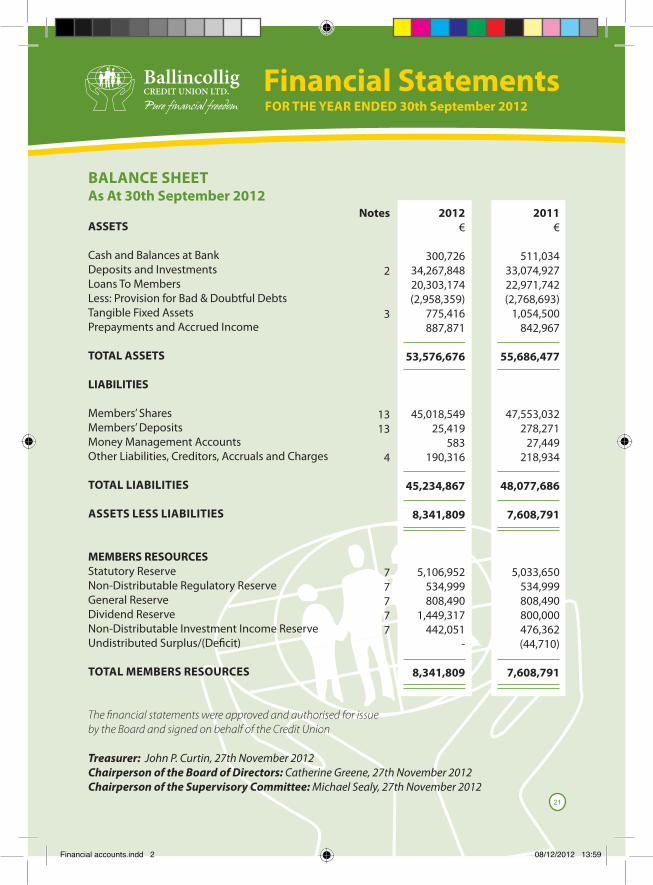

BALANCE SHEETAs At 30th September 2012

ASSETS

Cash and Balances at BankDeposits and Investments Loans To MembersLess: Provision for Bad & Doubtful DebtsTangible Fixed Assets Prepayments and Accrued Income

TOTAL ASSETS

LIABILITIES

Members’ SharesMembers’ DepositsMoney Management AccountsOther Liabilities, Creditors, Accruals and Charges

TOTAL LIABILITIES

ASSETS LESS LIABILITIES

MEMBERS RESOURCESStatutory ReserveNon-Distributable Regulatory ReserveGeneral ReserveDividend ReserveNon-Distributable Investment Income ReserveUndistributed Surplus/(Deficit)

TOTAL MEMBERS RESOURCES

The financial statements were approved and authorised for issue by the Board and signed on behalf of the Credit Union

2012€

300,72634,267,84820,303,174(2,958,359)

775,416887,871

53,576,676

45,018,54925,419

583190,316

45,234,867

8,341,809

5,106,952534,999808,490

1,449,317442,051

-

8,341,809

2011€

511,03433,074,92722,971,742(2,768,693)

1,054,500842,967

55,686,477

47,553,032278,271

27,449218,934

48,077,686

7,608,791

5,033,650534,999808,490800,000476,362(44,710)

7,608,791

2

3

1313

4

77777

Treasurer: John P. Curtin, 27th November 2012Chairperson of the Board of Directors: Catherine Greene, 27th November 2012Chairperson of the Supervisory Committee: Michael Sealy, 27th November 2012

Notes

21

Financial accounts.indd 2 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

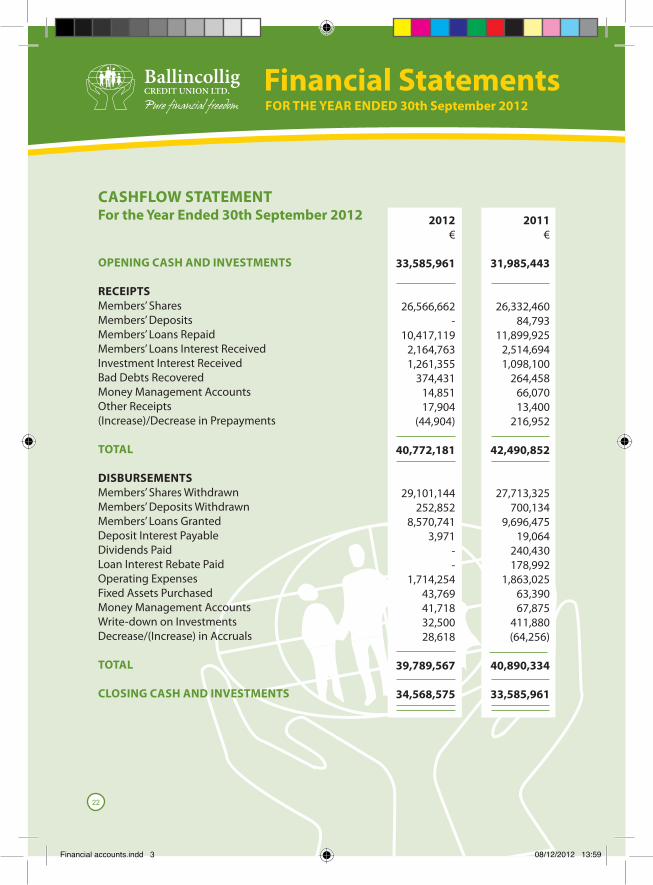

CASHFLOW STATEMENTFor the Year Ended 30th September 2012

OPENING CASH AND INVESTMENTS

RECEIPTSMembers’ SharesMembers’ DepositsMembers’ Loans RepaidMembers’ Loans Interest ReceivedInvestment Interest ReceivedBad Debts RecoveredMoney Management AccountsOther Receipts(Increase)/Decrease in Prepayments

TOTAL

DISBURSEMENTSMembers’ Shares WithdrawnMembers’ Deposits WithdrawnMembers’ Loans GrantedDeposit Interest PayableDividends PaidLoan Interest Rebate PaidOperating ExpensesFixed Assets PurchasedMoney Management AccountsWrite-down on InvestmentsDecrease/(Increase) in Accruals

TOTAL

CLOSING CASH AND INVESTMENTS

2012€

33,585,961

26,566,662-

10,417,1192,164,7631,261,355

374,43114,85117,904

(44,904)

40,772,181

29,101,144252,852

8,570,7413,971

--

1,714,25443,76941,71832,50028,618

39,789,567

34,568,575

2011€

31,985,443

26,332,46084,793

11,899,9252,514,6941,098,100

264,45866,07013,400

216,952

42,490,852

27,713,325700,134

9,696,47519,064

240,430178,992

1,863,02563,39067,875

411,880(64,256)

40,890,334

33,585,961

22

Financial accounts.indd 3 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

NOTES TO THE FINANCIAL STATEMENTSFor the Year Ended 30th September 2012

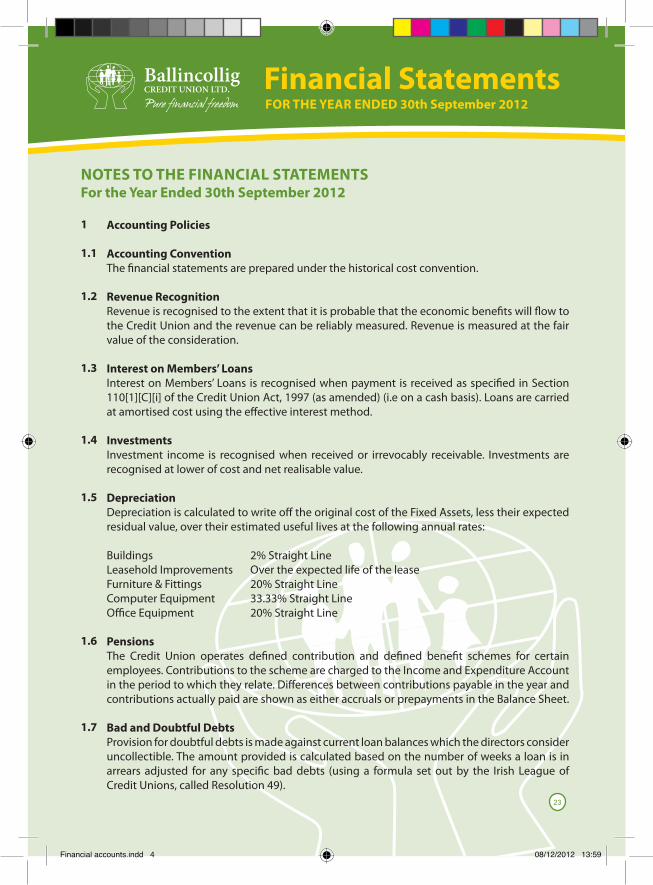

Accounting Policies

Accounting ConventionThe financial statements are prepared under the historical cost convention.

Revenue RecognitionRevenue is recognised to the extent that it is probable that the economic benefits will flow to the Credit Union and the revenue can be reliably measured. Revenue is measured at the fair value of the consideration.

Interest on Members’ LoansInterest on Members’ Loans is recognised when payment is received as specified in Section 110[1][C][i] of the Credit Union Act, 1997 (as amended) (i.e on a cash basis). Loans are carried at amortised cost using the effective interest method.

InvestmentsInvestment income is recognised when received or irrevocably receivable. Investments are recognised at lower of cost and net realisable value.

DepreciationDepreciation is calculated to write off the original cost of the Fixed Assets, less their expected residual value, over their estimated useful lives at the following annual rates:

Buildings 2% Straight LineLeasehold Improvements Over the expected life of the leaseFurniture & Fittings 20% Straight LineComputer Equipment 33.33% Straight LineOffice Equipment 20% Straight Line

PensionsThe Credit Union operates defined contribution and defined benefit schemes for certain employees. Contributions to the scheme are charged to the Income and Expenditure Account in the period to which they relate. Differences between contributions payable in the year and contributions actually paid are shown as either accruals or prepayments in the Balance Sheet.

Bad and Doubtful DebtsProvision for doubtful debts is made against current loan balances which the directors consider uncollectible. The amount provided is calculated based on the number of weeks a loan is in arrears adjusted for any specific bad debts (using a formula set out by the Irish League of Credit Unions, called Resolution 49).

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

23

Financial accounts.indd 4 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

Deposits and Investments

DepositsAllied Irish BankCIM- EBS Building SocietyEBS Building SocietyKBCBNP ParibasBank of IrelandCentral Bank ReserveIrish Life & PermanentNorthern RockBank of IrelandAnglo Irish BankUlster Bank

BondsBarclays TARNBNP ParibasGoodbody Eurostock BondGovernment BondEBS BondBOI BondAIB BondPTSB Bond

2 2012€

3,414,0531,000,0002,556,8987,286,464

100,000-

389,7427,248,173

-3,685,317

-3,525,731

29,206,378

1,000,000-

600,000494,000497,470500,000

1,000,000970,000

5,061,470

34,267,848

2011€

890,2641,000,0002,450,8517,030,000

-5,943,269

913,5445,218,814

10,363-

1,375,5963,000,000

27,832,701

1,000,0001,138,500

600,000502,055497,470503,706

1,000,495-

5,242,226

33,074,927

NOTES TO THE FINANCIAL STATEMENTSFor the Year Ended 30th September 2012

24

Financial accounts.indd 5 08/12/2012 13:59

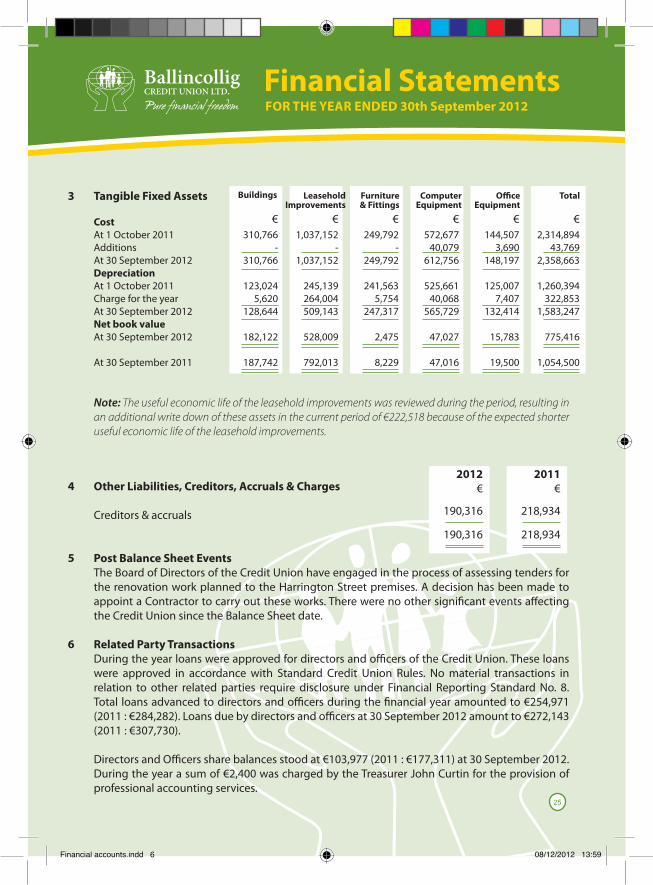

Financial StatementsFOR THE YEAR ENDED 30th September 2012

CostAt 1 October 2011AdditionsAt 30 September 2012DepreciationAt 1 October 2011Charge for the yearAt 30 September 2012Net book valueAt 30 September 2012

At 30 September 2011

3

4

5

6

Tangible Fixed Assets Buildings LeaseholdImprovements

Furniture& Fittings

ComputerEquipment

OfficeEquipment

Total

€310,766

-310,766

123,0245,620

128,644

182,122

187,742

€1,037,152

-1,037,152

245,139264,004509,143

528,009

792,013

€249,792

-249,792

241,5635,754

247,317

2,475

8,229

€572,677

40,079612,756

525,66140,068

565,729

47,027

47,016

€144,507

3,690148,197

125,007

7,407132,414

15,783

19,500

€2,314,894

43,7692,358,663

1,260,394322,853

1,583,247

775,416

1,054,500

Note: The useful economic life of the leasehold improvements was reviewed during the period, resulting in an additional write down of these assets in the current period of €222,518 because of the expected shorter useful economic life of the leasehold improvements.

Other Liabilities, Creditors, Accruals & Charges

Creditors & accruals

Post Balance Sheet EventsThe Board of Directors of the Credit Union have engaged in the process of assessing tenders for the renovation work planned to the Harrington Street premises. A decision has been made to appoint a Contractor to carry out these works. There were no other significant events affecting the Credit Union since the Balance Sheet date. Related Party TransactionsDuring the year loans were approved for directors and officers of the Credit Union. These loans were approved in accordance with Standard Credit Union Rules. No material transactions in relation to other related parties require disclosure under Financial Reporting Standard No. 8. Total loans advanced to directors and officers during the financial year amounted to €254,971 (2011 : €284,282). Loans due by directors and officers at 30 September 2012 amount to €272,143 (2011 : €307,730).

Directors and Officers share balances stood at €103,977 (2011 : €177,311) at 30 September 2012. During the year a sum of €2,400 was charged by the Treasurer John Curtin for the provision of professional accounting services.

2012€

190,316

190,316

2011€

218,934

218,934

25

Financial accounts.indd 6 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

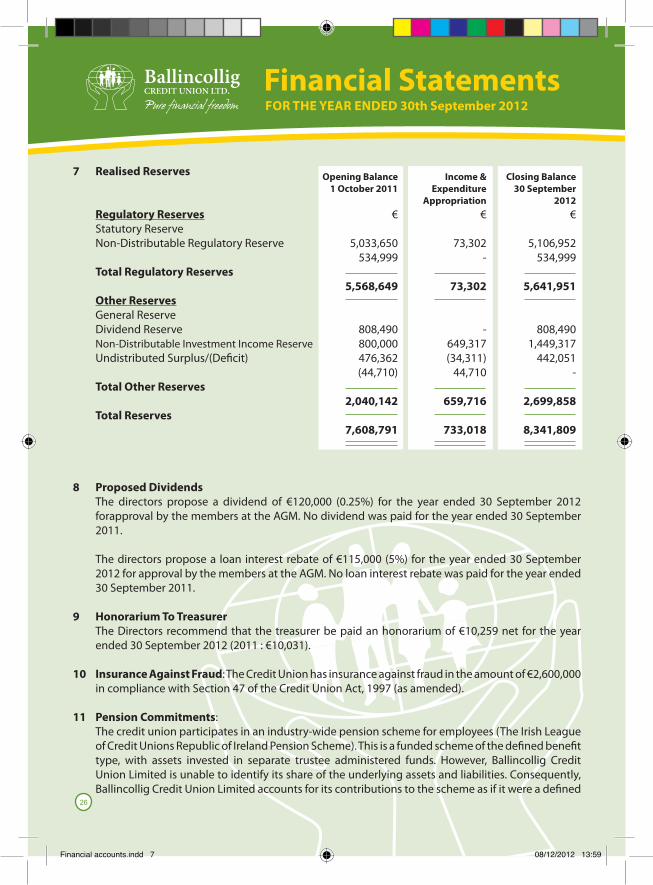

Realised Reserves

Regulatory ReservesStatutory ReserveNon-Distributable Regulatory Reserve

Total Regulatory Reserves

Other ReservesGeneral ReserveDividend ReserveNon-Distributable Investment Income ReserveUndistributed Surplus/(Deficit)

Total Other Reserves

Total Reserves

Proposed DividendsThe directors propose a dividend of €120,000 (0.25%) for the year ended 30 September 2012 forapproval by the members at the AGM. No dividend was paid for the year ended 30 September 2011.

The directors propose a loan interest rebate of €115,000 (5%) for the year ended 30 September 2012 for approval by the members at the AGM. No loan interest rebate was paid for the year ended 30 September 2011.

Honorarium To TreasurerThe Directors recommend that the treasurer be paid an honorarium of €10,259 net for the year ended 30 September 2012 (2011 : €10,031).

Insurance Against Fraud: The Credit Union has insurance against fraud in the amount of €2,600,000 in compliance with Section 47 of the Credit Union Act, 1997 (as amended).

Pension Commitments: The credit union participates in an industry-wide pension scheme for employees (The Irish League of Credit Unions Republic of Ireland Pension Scheme). This is a funded scheme of the defined benefit type, with assets invested in separate trustee administered funds. However, Ballincollig Credit Union Limited is unable to identify its share of the underlying assets and liabilities. Consequently, Ballincollig Credit Union Limited accounts for its contributions to the scheme as if it were a defined

7

8

9

10

11

Opening Balance1 October 2011

€

5,033,650534,999

5,568,649

808,490 800,000476,362(44,710)

2,040,142

7,608,791

Income & Expenditure

Appropriation€

73,302-

73,302

-649,317(34,311)

44,710

659,716

733,018

Closing Balance30 September

2012€

5,106,952534,999

5,641,951

808,4901,449,317

442,051-

2,699,858

8,341,809

26

Financial accounts.indd 7 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

contribution scheme. Contributions payable to the scheme are recognised in the income and expenditure account.

An actuarial review of the fund is normally carried out every three years by the Scheme’s independent, professionally qualified, actuary. The actuarial review looks at the past & future liabilities of the scheme.

The last completed triennial actuarial review was carried out with an effective date of 1st March 2011 using the Projected Unit Credit method. The principal actuarial assumption used in the valuation was the investment return would be 1.75% higher than the annual salary increases. The market value of the scheme’s assets at 1st March 2011 was €107.3m. The actuarial valuation disclosed a past service deficit of €28.7m on the long term funding basis at 1st March 2011. This actuarial review recommended a long term funding rate of 22.5%. The cost of risk benefits is paid in addition to this rate.

It should be noted that the above rate is based on the long term funding objectives.As a separate requirement under section 56(1) of the Pensions Act 1990, the scheme actuary must carry out a separate valuation every 3 years and produce a funding certificate for submission to The Pensions Board within 9 months of the effective date of the valuation. The purpose of the certificate is to certify whether or not the assets of the scheme at the effective date are sufficient to meet the liabilities of the scheme based on the assumption that the scheme was wound up at that date.

An actuarial funding certificate, certifying the Scheme did not meet the statutory minimum funding standard was submitted to the Pensions Board with an effective date of 1st March 2009.

Consequently, the Trustees submitted a new funding proposal, to address the shortfall in funding, to the Pensions Board. The submitted funding proposal is designed to ensure that the scheme could reasonably be expected to satisfy the funding standard as at 1st March 2019 and provides for a retirement contribution rate of 27.7%. The cost of risk benefits is payable in addition giving a total contribution rate of 30% of Pensionable Salary. This funding proposal was approved by the Pensions Board.

For the scheme year ended 29th February 2012 the actuary advised that having been directed by the Trustees and Employer, in light of the current economic outlook, that it was appropriate to revise the assumption for salary increases over the remaining term of the funding proposal from 5% pa to 3% pa he was reasonably satisfied that the scheme will satisfy the funding standard as specified in Section 44 of the Pensions Act, 1990, at the date of 1 March 2019 specified by the Pensions Board under Section 49(2) (a) of the Act for the purpose of the existing funding proposal.

The scheme’s Solvency Position in accordance with the aggregate cover for total Funding Standard liabilities as at 29th February 2012 was 90.5%.

27

Financial accounts.indd 8 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

Rates of Interest charged on Members’ LoansDuring the year ended 30th September 2012, the credit union’s rate of interest charged on members’ loans was 0.96% per month (11.6% APR).

Member’ Shares

Regular share accountFixed Term Deposit

Approval of financial statementsThe financial statements were approved by the Board of Directors and authorised for issue on 27th November 2012

12

13

14

2012€

45,018,54925,419

45,043,968

2011€

47,553,032278,271

47,831,303

28

Financial accounts.indd 9 08/12/2012 13:59

Financial StatementsFOR THE YEAR ENDED 30th September 2012

SCHEDULES TO THE FINANCIAL STATEMENTSFor the Year Ended 30th September 2012

Schedule 1 - Other Interest Income & Similar IncomeInvestment Income (before gains/losses on Investments)

Total Per Income and Expenditure Account

Analysed as follows:Received/Receivable within one year of Balance Sheet dateReceivable after one year of Balance Sheet date

Schedule 2 - Other IncomeFEXCOPPILe Cheile Commission

Total Per Income and Expenditure Account

Schedule 3 - Other Management ExpensesPension CostsTreasurers HonorariumSupervisory Committee ExpensesGeneral InsuranceRent & RatesECCU InsuranceLeague, Chapter, Registrar Filing Fees & SPS CostsDeath Benefit InsuranceLight and HeatComputer MaintenanceRepairs & MaintenanceComputer LicencesCleaningSecurityTraining General ExpensesStationery & Office ExpensesAdvertising & MarketingTelephone & PostageAGM and Convention ExpsCredit Union AllianceTravel & SubsistenceLegal and Professional FeesConsultancy FeesAudit FeesBank Interest and ChargesHarrington Street ProjectSponsorship and donations

Total Per Income and Expenditure Account

2012€

1,261,355

1,261,355

1,142,873118,482

1,261,355

9,9015,3042,699

17,904

100,97910,25910,47127,219

169,125204,303

37,94252,98416,30717,459

9,27931,711

9,1915,368

13,03018,074

7,90128,34617,48723,834

-5,384

24,31970,92222,10217,02213,137

7,089

971,244

2011€

1,098,100

1,098,100

996,571 101,529

1,098,100

8,3625,038

-

13,400

102,28110,03110,17620,847

168,551229,228

60,88150,14314,84021,700

9,92724,868

9,9708,182

30,4718,279

12,27853,43621,47726,367

6,7943,111

37,74926,97221,78031,71832,00013,184

1,067,241 29

Financial accounts.indd 10 08/12/2012 13:59

30

31

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

The Loan Book of a Credit Union is it’s income. It ensures that the savings of members areavailable to lend to other members. This is the essential Financial co-operation that is theethos of the credit union movement.

In the last financial year October 2011 to September 2012, we in Ballincollig Credit Unionhave lent out over €9 million of you, the member’s money, to other members. The loans werevaried both in their amounts and in their requirements e.g. home improvements, carseducation weddings, holidays.

As we all know these are very difficult financial times we live in. This has been particularlyevident in our Loan Book, which shows a decline of approximately €2 million since last year.This is due to a variety of reasons, the uncertain financial market, the fear of borrowing, thefear of getting in over our heads, and not knowing when our individual circumstances willchange and our worry, that we will be unable to keep up our repayments.

The Board of Ballincollig Credit Union, acknowledges and understands all of our membersworries. With these in mind we hope to put a number of measures in place to help alleviatethem. In conjunction with our Strategic Plan we intend to lower our interest rate over thenext three years. This we hope will encourage more borrowing. We need you the member toconsider us when you need a loan, we will always take a fair and reasonable approach to yourapplication. We wil listen to you, the member, at all times.

We hope in the coming year, that our Credit Union, will grow from strength to strength. Todo this we need your help and input. Help us to help you. Begin a regular saving habit nomatter how small, and when you borrow, maintain your repayments and if you get intofinancial trouble, come in and talk to us. We hope that 2013 will be a good year for all ourmembers.

The Credit Committee would like to thank their fellow directors, supervisors, staff andmanagement for all their help and support over the last year.

Bob O’HeaIrene Byrne

Catherine GreeneBreda Callanan

C r e d i t C o m m i t t e e R e p o r t

32

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Credi t Control Committee Repor t

The Credit Control Committee meets regularly to review loan repayments and report to theBoard. The task of the Credit Control Committee is to ensure that members repay theirloans as per their credit agreement. We strive to deliver a quality, open, honest andconfidential service to our members who encounter genuine difficulties with repayments.

We encourage members to make contact with the Credit Union before their accounts havearrears or the earliest time thereafter. We do recognise that where genuine cases need helpall the expertise available to the Credit Union will be made available to our members.

We remind members that the funds which BCU lend are the member’s savings and whilewe again acknowledge the difficulties that some members encounter in meeting theirobligations nevertheless the Credit Control Committee must give out the message that “Ifyou borrow from BCU you will have to pay the loan back”.

We have experienced from our interaction with members that the majority of members doengage and continue to prioritise payment to the credit union thereby maintaining a goodrelationship between the member and BCU.

We are grateful that this is the case, as getting loans in society is proving more and moredifficult and Ballincollig CU wishes to remain as the “Lender of Choice” for all membersand to continue to be a caring provider of financial services within our community.

Finally the Committee would like to thank the Board, Supervisors, Management and Stafffor their combined efforts over the past year.

Mary O’MahonySheila MaguirePaddy Mc Carthy

33

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

M a r k e t i n g , E d u c a t i o n , P r o m o t i o n & S p o n s o r s h i p R e p o r t

BCU celebrated its 40th Birthday this year of providing our widerange of services to members. Our aim for 2013 will be tocontinue to promote Ballincollig Credit Union as a majorfinancial co-operative in our area and support our memberswithin the community.

We continue to be in a strong position to lend to our members.We now offer a discounted car and home insurance deal on ourwebsite www.bcu.ie and we were amazed at the number ofmembers who have availed of this.

Another new service which has proven hugely popular is the credit union savings stamps. These cost€2 each and can be a great way for members to take control of bills and upcoming occasions.

Our Services:• Savings and Loans facilities• Loan Protection Insurance• Death Benefit Insurance• Competitive Loan interest rate• Foreign Exchange• Budget Accounts• Money Advice and Budgeting Service• Household Bill

Check out our website for all the latest news and updates or find us on facebook which allows us toconverse freely with our members and non members highlighting upcoming events, promotions andnews.

Thank you for continuing to choose Ballincollig Credit Union as your first choice for saving andlending and we look forward to meeting your needs in the coming and future years.

Finally on behalf of the MEPS committee, I would like to thank the Board, supervisors and staff fortheir continued work and support during the year.continued work and support throughout the year.

Mary O Mahony Catherine Greene

Linda O’Neill

34

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

Membership Committee Repor t

The Membership Committee are pleased to report that we again had an increase inmembership over the past year, and we thank you, our members for your continued support.In the past year we had an increase of 315 new members on last year and our totalmembership stood at 15,844 at year end.

We would like to take this opportunity to ask our members to ask their family young andold if they are members of BCU and if not we would appreciate it if you could encouragethem to join or come and ask us about joining. When a member joins BCU they have anoption to complete a form of nomination. This will allow the beneficiary, in the event of thedeath of the person making the nomination, to receive up to €23,000 without having to takeout probate. We urge all members to take advantage of this benefit by nominating abeneficiary; also to review this nomination regularly.

We feel it important to point out the benefits of membership of our credit union:• Life saving insurance is automatically available to members who join before age 70

years - your savings can carry life insurance of up to €7,700 and the amount to be paid out in the event of accidental death is doubled.

• Loan protection insurance is also available to our members; this cover will pay off your loan (subject to certain limits and conditions) should you die during the term of the loan. This insurance also gives cover for total disability, within set criteria.

• Death Benefit insurance of €1,300 is taken out by BCU on each member who joins before their 70th birthday

• All of the insurances above are currently provided at no direct cost to members. In all, the amount paid out under insurances in the past year was €150,308

During the year 41 of our members died. The Board, Supervisors and staff would like toextend their sincere condolences to the families and wish to remind you that the AnnualMass for deceased members will be celebrated early in the New Year in the churches withinour common bond.

Ann Marie CosgroveMarie KierseAnn QuinnDonal O’Regan

35

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

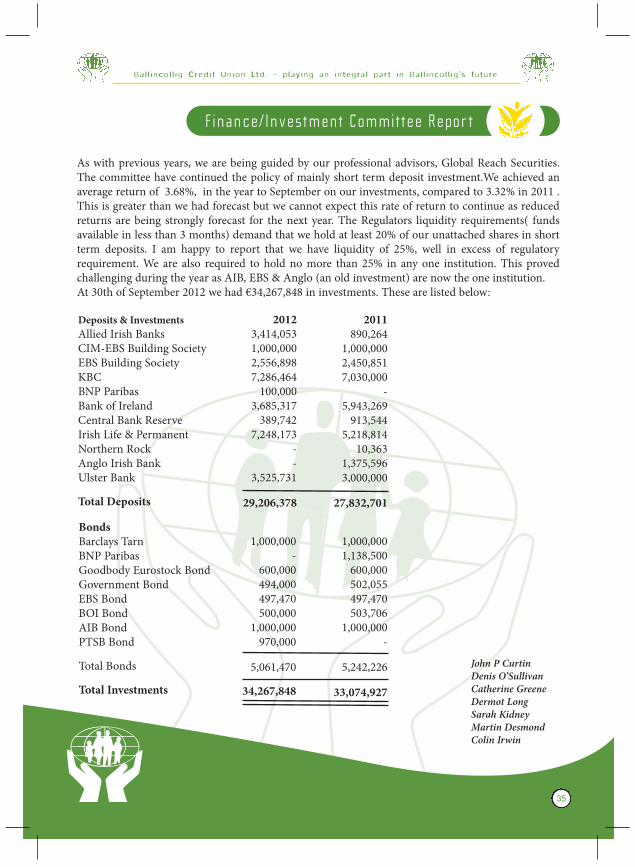

F inance/Investment Committee Repor t

As with previous years, we are being guided by our professional advisors, Global Reach Securities.The committee have continued the policy of mainly short term deposit investment.We achieved anaverage return of 3.68%, in the year to September on our investments, compared to 3.32% in 2011 .This is greater than we had forecast but we cannot expect this rate of return to continue as reducedreturns are being strongly forecast for the next year. The Regulators liquidity requirements( fundsavailable in less than 3 months) demand that we hold at least 20% of our unattached shares in shortterm deposits. I am happy to report that we have liquidity of 25%, well in excess of regulatoryrequirement. We are also required to hold no more than 25% in any one institution. This provedchallenging during the year as AIB, EBS & Anglo (an old investment) are now the one institution.At 30th of September 2012 we had €34,267,848 in investments. These are listed below:

Deposits & InvestmentsAllied Irish BanksCIM-EBS Building SocietyEBS Building SocietyKBCBNP ParibasBank of IrelandCentral Bank ReserveIrish Life & PermanentNorthern RockAnglo Irish BankUlster Bank

Total Deposits

20123,414,0531,000,0002,556,8987,286,464

100,0003,685,317

389,7427,248,173

--

3,525,731

29,206,378

BondsBarclays TarnBNP ParibasGoodbody Eurostock BondGovernment BondEBS BondBOI BondAIB BondPTSB Bond

Total Bonds

Total Investments

1,000,000-

600,000494,000497,470500,000

1,000,000970,000

5,061,470

34,267,848

John P CurtinDenis O’SullivanCatherine GreeneDermot LongSarah KidneyMartin DesmondColin Irwin

2011890,264

1,000,0002,450,8517,030,000

-5,943,269

913,5445,218,814

10,3631,375,5963,000,000

27,832,701

1,000,0001,138,500

600,000502,055497,470503,706

1,000,000-

5,242,226

33,074,927

36

Ba l l i n co l l i g C r ed i t Un i o n L t d . ~ p l a y i n g a n i n t e g r a l p a r t i n B a l l i n co l l i g ’ s f u t u r e

S u p e r v i s o r y C o m m i t t e e R e p o r t

The Credit Union Act 1997 (as amended) requires the appointment of a Supervisory Committeewhich will oversee Directors in the performance of their functions, examine books and documents ofthe Credit Union and verify a sample of members’ balances. At last year’s A.G.M. you the members,elected the Supervisory Committee to oversee, evaluate and check the operation of your CreditUnion, in accordance with the Credit Union Act 1997 (as amended) and the Standard Rules for CreditUnions.

During the past year the Supervisory Committee in accordance with Rule 2, performed a detailedexamination of the following areas:1. A random selection of accounts for verification of balances was carried out over the year

and we would like to thank members for their co-operation in completing and returning the statements. We are still getting a response rate of about 35% from the 1400 letters sent out over the year and we would urge everyone receiving these to complete and return them in the prepaid envelope enclosed.

2. Examination of books, papers, records and accounts of the credit Union.3. An inspection of Bank reconciliations, loan applications and loan securities was carried out

by Foley and O’Shea on behalf of the Committee on two occasions during the year.4. During the year we carried out counts of Tellers’ Cash, which were satisfactory.

Members of the Supervisory Committee attended monthly and additional meetings of the Board. Alldecisions made by the Board were in the best interests of the members. During the year the Boarddecided to evaluate the operation of the Credit Union and produce a Strategic Plan for the period2012-2015. Pinta Consultants were appointed to carry out this project and this month the Board,Supervisors, Management and Staff have been fully briefed on the results and very comprehensiverecommendations.

We are pleased to note the substantial progress on the project to refurbish the offices in HarringtonStreet and look forward to moving back there next summer. In the midst of the continuing financialdifficulties affecting us all, your Credit Union has managed to make good its hope expressed by theChairperson’s Statement at last year’s AGM, that we will return to surplus in 2012. Much credit forthis is due to the Board, Management and Staff but of course without the Members and your supportit would not have been possible.

Next year looks like being a very busy one, as in addition to the improvements proposed in theStrategic Plan, we are due to get a new Credit Union Act and the promise of the imposition of a raftof new controls designed for our own good including the renaming and new duties of the SupervisoryCommittee.

Michael Sealy, ChairmanNicola O’Connell, SecretaryJohn O’Brien, Member

Who have YOU nominated to receive

YOUR pot of gold?We recommend that all single account holders

over the age of 16 complete a nomination form.

Completing the nomination form will ensure that on your death,your shares and insurance (to a maximum of €23,000)will be speedily disbursed to your named beneficiaries.

A nomination may be cancelled or changed at any timeand will automatically be cancelled by marriage.

Tel: 021-4872305 • www.bcu.ie

inside_backcover.indd 1 08/12/2012 15:03