critical areas of reporting on caro, 2003 baroda branch of wirc of icai (dr.) ca. alok shah

TRANSCRIPT

CRITICAL AREAS OF REPORTING ON CARO, 2003

BARODA BRANCH OF WIRC OF ICAI

(Dr.) CA. ALOK SHAH

AUDIT REPORT

INTRODUCTION227(1A), (2), (3), and (4) applicable to all

companies while the Order exempts certain classes of companies from its application.

227(1A) does not require comments on matters specified in the sub-section unless there are any adverse comments.

CARO, however, requires a statement on each of the matters specified therein even if there are no comments.

CARO – Non-applicability

Not applicable to Private Ltd. Co. if: Paid-up capital and reserves are not more

than Rs. 50 lakhs; Does not have loan outstanding of Rs. 25

lakhs or more from any bank or financial institution

Does not have turnover exceeding Rs. 5 crores.

Limits to be considered at any point during the year

Above conditions for non-applicability are cumulative

Thus, even if ONE condition is satisfied, CARO is applicable

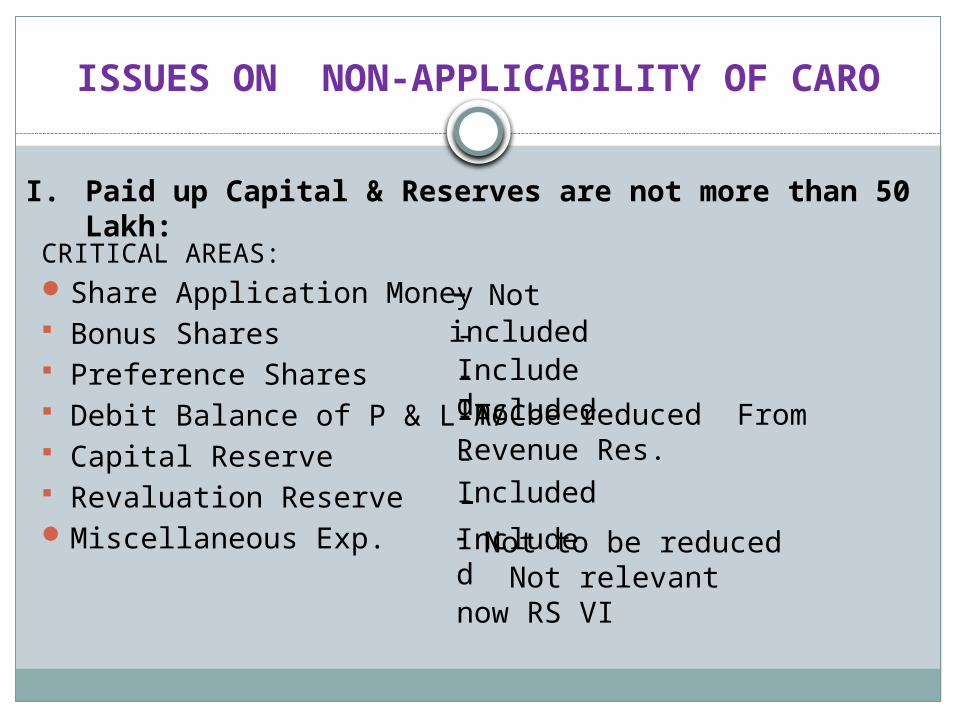

ISSUES ON NON-APPLICABILITY OF CARO

I. Paid up Capital & Reserves are not more than 50 Lakh:

CRITICAL AREAS:Share Application Money Bonus Shares Preference Shares Debit Balance of P & L A/C Capital Reserve Revaluation ReserveMiscellaneous Exp.

- Not included - Included - Included-To be reduced From Revenue Res.

- Included- Not to be reduced Not relevant now RS VI

- Included

Continued…

II. Outstanding loan from any Bank or Financial Institution not exceeding Rs. 25 LakhsISSUES:

Term Loan and Demand Loan Working Capital Loan Non-fund based Loan Outstanding on any day Private Bank or Foreign Bank NBFCs

-Include

-Include -Include-Include

-Not a financial institution

-Include

ISSUES: Sales Tax or Excise collectedTrade DiscountSales ReturnRent, Dividend, etc.Principal Business of Company is letting out

Continued…

III. Turnover does not exceed Rs. 5 Crores

- No

- No

- Reduce- No

-Yes

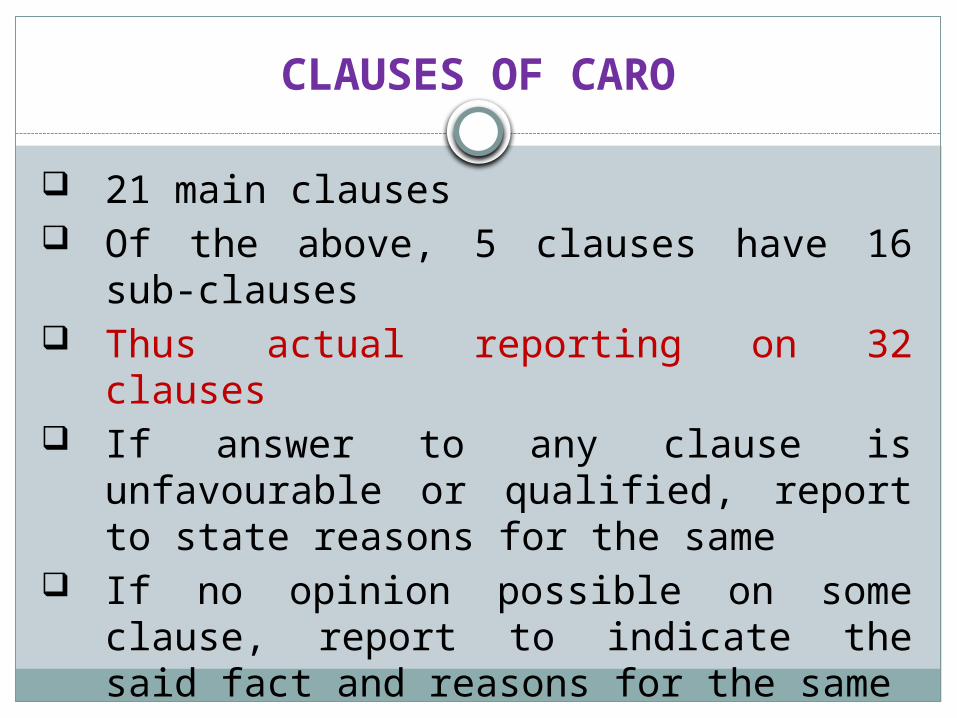

CLAUSES OF CARO

21 main clauses Of the above, 5 clauses have 16 sub-

clauses Thus actual reporting on 32 clauses If answer to any clause is unfavourable

or qualified, report to state reasons for the same

If no opinion possible on some clause, report to indicate the said fact and reasons for the same

Unfavourable/qualified opinion in bold/italics

Clause I : Fixed Assets

a. Proper Recordsb. Electronic Recordsc. Management Representation Letterd. Physical Verification of Fixed Assets and

Certificatione. Disposal of substantial part of fixed assets -

going concernf. Sufficient and Appropriate audit evidenceg. Going Concern not resolvedh. Properly dealing with Material Discrepanciesi. Reasonable intervals for Verification

Issues……

If FA register not updated for additions for the year under audit- Qualify

In case qualification given regarding non-maintenance or non-updation of FA register, to also give disclaimer as ‘in absence of FA register, we are unable to comment whether the same tallies with physical verification carried out by management’

Issues ……

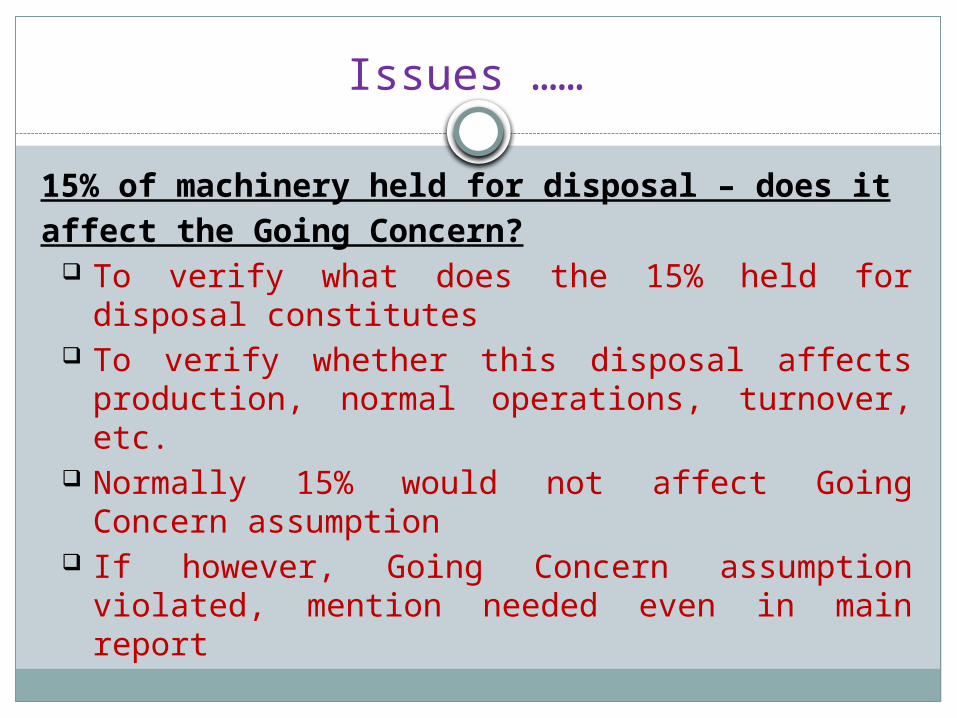

15% of machinery held for disposal – does itaffect the Going Concern?

To verify what does the 15% held for disposal constitutes

To verify whether this disposal affects production, normal operations, turnover, etc.

Normally 15% would not affect Going Concern assumption

If however, Going Concern assumption violated, mention needed even in main report

Clause II :Inventories

a. Items Covered under the term – ‘Inventory’- AS 2

b. Practical difficulties to maintain records of WIP

c. Material Discrepanciesd. Whether physical verification to be done

by auditors? If not, how does auditor certify that physical verification has been conducted?

e. Reasonable intervals?f. Reasonableness or adequacies of the

procedure of physical verification and report the inadequacies?

Clause III :LOANS

Applicability of clause to only those transactions where loans granted or taken during the year or even those granted in the past and appear on the balance sheet

Determine section 301 parties- MRL and number of parties and amount involved Whether reporting under AS 18 covers the above? What if they now qualify or cease to be covered during the year?

Rate of interest and other terms are prima facie prejudicial?

Clause III :LOANS contd….

What if no stipulations as to rate of interest and repayment or other terms?

Loans repayable on demand and interest free loan

Regular repayment of principal and interest or not

Reasonable steps for recovery of overdue loans of Rs. 1 Lacs and more

What if there are no stipulations as to rate of interest and repayment or other terms?

Issues……

Where no stipulation has been made for the repayment or payment of the interest or both, to state the fact that no comments are made because the terms of repayment and/or interest have not been specified.

To ask the management for steps taken (in writing)

No adverse comment required on the mere absence of legal steps if otherwise reasonable steps are taken

Clause IV :Internal Control System

Determination of adequacy of an internal control system?

Whether reporting on internal control systems is to be restricted only in specified areas, such as purchase of inventory and fixed assets and sale of goods and services?

Major weaknessesContinuing failure to correct major

weaknessesIf there is no internal audit, can it be said

that there is no internal control?

Clause V :Section 301 Reasonability of Transactions

Completion of entries in register u/s 301 of the said Act as to transactions for goods, material and services

Transactions > Rs. 5 Lacs are reasonable having regard to the ‘prevailing market prices’ at the relevant time

What if the supplier is a monopolist or the product is custom made?

Intangible goods

Issues …….

To determine reasonableness, to consider all the factors surrounding the transactions of purchase / sale like: Delivery period Schedule of implementation Quantity, Quality of the product/service Credit terms Previous record of supplier/buyer/client, etc.

Co-relation with disclosures under: AS 18 and sec 40A(2)(b) Domestic Transfer Pricing ?? (from AY 2013-14)

Clause VI :Deposits

To report on deposits accepted in violation of Sec. 58, 58AA and other relevant provisions and rules.

For Pvt. Ltd companies sec. 3(1)(iii) PROHIBITS invitation or acceptance of deposits from persons other than its members, directors or their relatives.

As per Rule 2(b)(iv) of Companies (Acceptance of Deposit) Rules, deposit does NOT INCLUDE amounts received by a company from any other company;

As per Rule 2(b)(ix), deposit does NOT INCLUDE amounts received from a director or relative of director or a member by a private company (declaration to be obtained that funds are not borrowed funds).

Issues…….

If a Pvt. ltd co accepts ICDs whether violation

of section 58A? As per section 3(1)(iii) Pvt. Ltd cos prohibited

from accepting deposits other than members, directors and relatives

Whether Rules can override the Act? Dept view in some cases: violation of sec. 58A Reporting necessary under CARO (and

possibly even under main report as violation of Companies Act)

Clause VII :Internal Audit

Mandatory for listed companies Applicable to non-listed companies if

the paid-up capital and reserves of the company exceed Rs. 50 lakhs; or

average annual turnover exceeding Rs. 5 crores for a period of three consecutive financial years immediately preceding the financial year concerned.

Issues……

Co has appointed independent CA firm as internal

auditor. Report submitted once covering 12 months.

Is this adequate? To examine the engagement letter To examine the scope and coverage by the IA and

the reports Whether standards on IA followed? Prima-facie the query indicates that the report

should mention that “IA needs to be strengthened”

Clause VIII :Cost Records

Proper Cost Records as prescribedOrder of the Central Government for

cost auditMRL that order is not applicableCost Audit Report if applicableIssue:What if Cost Audit is not completed before

the Statutory Auditor issues Audit Report?

Clause IX :Statutory Dues

Identification of undisputed amount Whether payment of Bonus/Gratuity to employees

and Electricity Bills constitutes statutory dues or notWhether non compliance, say, non payment of

professional tax, Advance Tax, TDS, VAT, Service Tax by the company would constitute disputed dues.

What if the demand is set aside, but the department goes in for appeal? What if the demand is confirmed, and the time to appeal by the company, has elapsed?

Forum where dispute is pending and amount involved.

Issues…..

A matter is considered as “disputed” if there is a positive evidence or action on the part of the company to show that it has not accepted the demand for payment e.g., appeal filed.

Mere representation to the concerned department does not constitute dispute.

For disputed statutory dues, information to be given for different periods for which, appeals may have been filed separately.

Clause X :Accumulated Losses

Cash losses? What if cash losses are only for one of the years?

Whether manufacturing company and service companies or trading companies are distinguished for reporting?

Whether qualifications by previous auditor to be considered to determine the net worth? What if the qualification is not quantifiable?

Computation of Losses and Net worth

Clause XI : Default in repayment of dues

What constitutes defaults …dispute with lender

Period and amount of defaultWhat if renewal is not done? Can it be

said that it is due?

Clause XII : Loans granted against securities

What are adequate documents and records?

Can the company give loans against securities unless authorized by the MoA.

Are the securities adequate? Market quotes

Fall in Market price..Temporary/Permanent

Whether the deficiencies to be reported, should relate only to documentation or even the systems?

Clause XIII : Chit funds or Nidhi

Chit Fund law applicabilityAdequate procedures..How to

determine the same?Proper repayment schedule

Clause XIV : Dealing or Trading of securities

Proper records of transactions and contractsReport of Timely entriesReport of shares and securities in the name of persons other

than company u/s 49 of the Act.

Clause XV : Guarantees for others

Proper RecordTerms and conditions are not

prejudicial to the interest of the company

Contingent LiabilityGuarantee against Loans from Private

Issues…..

Guarantee given for housing loan taken by

MD. Is the guarantee prejudicial? Whether section 295 violation (except in

Pvt. Ltd Co)? Whether terms of appointment of MD

mention that Co. will provide such guarantee?

Prima-facie seems to be prejudicial, but other facts also to be considered before deciding to qualify.

Clause XVI : Use of Term Loans

Whether term loans obtained from entities/persons other than banks/financial institutions are also covered or not

Purpose and actual utilization of term loansWhether reporting is to be made on the term loans

obtained during the year or outstanding as at the end of the year irrespective of the year in which they are obtained or not

Whether debentures are covered What procedures to be adopted in case of term loans

from banks, raised against title deeds, long term FDRs, NSCs etc., where the bank is not concerned with the purpose for which it is being obtained?

Clause XVII :Application of funds-Short term

Whether funds raised on short term basis used for long term investments

Core working capital If working capital loans are raised

against fixed deposits, are they reportable?

If current assets are used for paying long term debts, are they reportable?

Issues……

Meaning of short term / long term to be aligned with the disclosures in RS VI

In situations where Operating Cycle is more than 12 months –

Whether reporting under this clause would still be with 12 month perspective?

Clause XVIII : Preferential allotment

Preferential allotment of shares to parties and companies covered in the register maintained u/s 301

Where a private limited company having four shareholders (being relatives )holding 25% each of the share capital of the company, are allotted shares in equal proportions at a value of, say, Rs.10 while the book value of shares is, Rs. 50, would it be reportable under this clause?

Price prejudicial to the interest of the companyWill issue of ESOPs by private companies be

considered as preferential allotment? Would this clause apply to convertible bonds?

Clause XIX : Debentures

Whether reporting is required to be done in respect of debentures issued during the year or outstanding as on the year end irrespective of the year in which they were issued?

If the debentures have been issued towards the end of the year and the securities are created subsequently, what are the reporting responsibilities of the auditor under this clause?

Clause XX : End use of public issue

How to report in a case where the company has invested surplus funds, not immediately required, in short-term loans or investments?

Does this clause apply to monies raised by public issues during the year or even earlier years?

Clause XXI : Frauds

What are the reporting responsibilities in case where frauds have been committed by the directors of the company but are not reported by the company and come to the knowledge of the auditors from private sources?

Whether the total amount of frauds and the each major can be clubbed and disclosed? Whether individual amount involved in each fraud is to be separately listed out with the corresponding nature of fraud?

What are the various kinds of frauds reported?

Issues……

Fraud in consumption of gold for manufacture of ornamentsGN states “Although fraud is a broad legal

concept, auditor is concerned with fraudulent acts causing material misstatement in fin. stts.”

The above does not involve misrepresentation of fin. stts.

No reporting in CARO

Issues……

Co represents in MRL that no fraud hasoccurred. Information is however

receivedthat the purchase manager acceptscommissions for approving tenders

GN states “Although fraud is a broad legal concept, auditor is concerned with fraudulent acts causing material misstatement in fin. stts.”

Does not involve misrepresentation of fin. stts.

No reporting in CARO