critical implementation considerations in applying the ...€¦ · critical implementation...

TRANSCRIPT

Critical implementation considerations in applying the 2014 SORP and new UK GAAP

May 2014

Accounting for further And higher educAtion

The new UK GAAP 1

BACKGROUndFRS 102 is the core of new UK GAAP, providing a concise and simplified accounting framework for entities in its scope. FRS 102 replaces all current UK accounting standards (SSAPs, FRSs and UITFs) with a single FRS. It completes the suite of new UK GAAP standards, the other two being:

• FRS 100 ‘Application of Financial Reporting Requirements’

• FRS 101 ‘Reduced Disclosure Framework’.

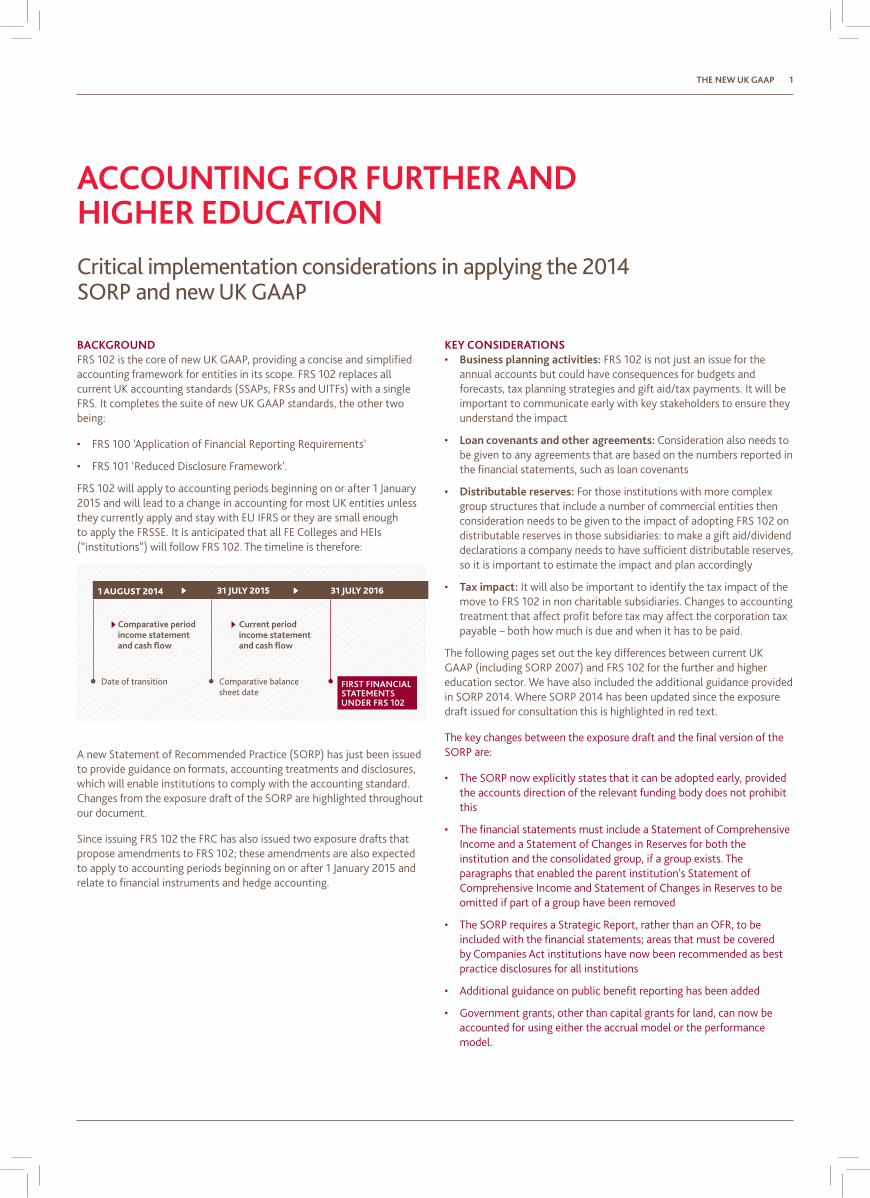

FRS 102 will apply to accounting periods beginning on or after 1 January 2015 and will lead to a change in accounting for most UK entities unless they currently apply and stay with EU IFRS or they are small enough to apply the FRSSE. It is anticipated that all FE Colleges and HEIs (“institutions”) will follow FRS 102. The timeline is therefore:

A new Statement of Recommended Practice (SORP) has just been issued to provide guidance on formats, accounting treatments and disclosures, which will enable institutions to comply with the accounting standard. Changes from the exposure draft of the SORP are highlighted throughout our document.

Since issuing FRS 102 the FRC has also issued two exposure drafts that propose amendments to FRS 102; these amendments are also expected to apply to accounting periods beginning on or after 1 January 2015 and relate to financial instruments and hedge accounting.

Key COnSideRAtiOnS• Business planning activities: FRS 102 is not just an issue for the

annual accounts but could have consequences for budgets and forecasts, tax planning strategies and gift aid/tax payments. It will be important to communicate early with key stakeholders to ensure they understand the impact

• Loan covenants and other agreements: Consideration also needs to be given to any agreements that are based on the numbers reported in the financial statements, such as loan covenants

• distributable reserves: For those institutions with more complex group structures that include a number of commercial entities then consideration needs to be given to the impact of adopting FRS 102 on distributable reserves in those subsidiaries: to make a gift aid/dividend declarations a company needs to have sufficient distributable reserves, so it is important to estimate the impact and plan accordingly

• tax impact: It will also be important to identify the tax impact of the move to FRS 102 in non charitable subsidiaries. Changes to accounting treatment that affect profit before tax may affect the corporation tax payable – both how much is due and when it has to be paid.

The following pages set out the key differences between current UK GAAP (including SORP 2007) and FRS 102 for the further and higher education sector. We have also included the additional guidance provided in SORP 2014. Where SORP 2014 has been updated since the exposure draft issued for consultation this is highlighted in red text.

The key changes between the exposure draft and the final version of the SORP are:

• The SORP now explicitly states that it can be adopted early, provided the accounts direction of the relevant funding body does not prohibit this

• The financial statements must include a Statement of Comprehensive Income and a Statement of Changes in Reserves for both the institution and the consolidated group, if a group exists. The paragraphs that enabled the parent institution’s Statement of Comprehensive Income and Statement of Changes in Reserves to be omitted if part of a group have been removed

• The SORP requires a Strategic Report, rather than an OFR, to be included with the financial statements; areas that must be covered by Companies Act institutions have now been recommended as best practice disclosures for all institutions

• Additional guidance on public benefit reporting has been added

• Government grants, other than capital grants for land, can now be accounted for using either the accrual model or the performance model.

Comparative period income statement and cash flow

Date of transition Comparative balance sheet date

Current period income statement and cash flow

FiRSt FinAnCiAL StAtementS UndeR FRS 102

ACCOUntinG FOR FURtheR And hiGheR edUCAtiOn Critical implementation considerations in applying the 2014 SORP and new UK GaaP

1 AuguSt 2014 31 JuLY 2015 31 JuLY 2016

The new UK GAAP 2

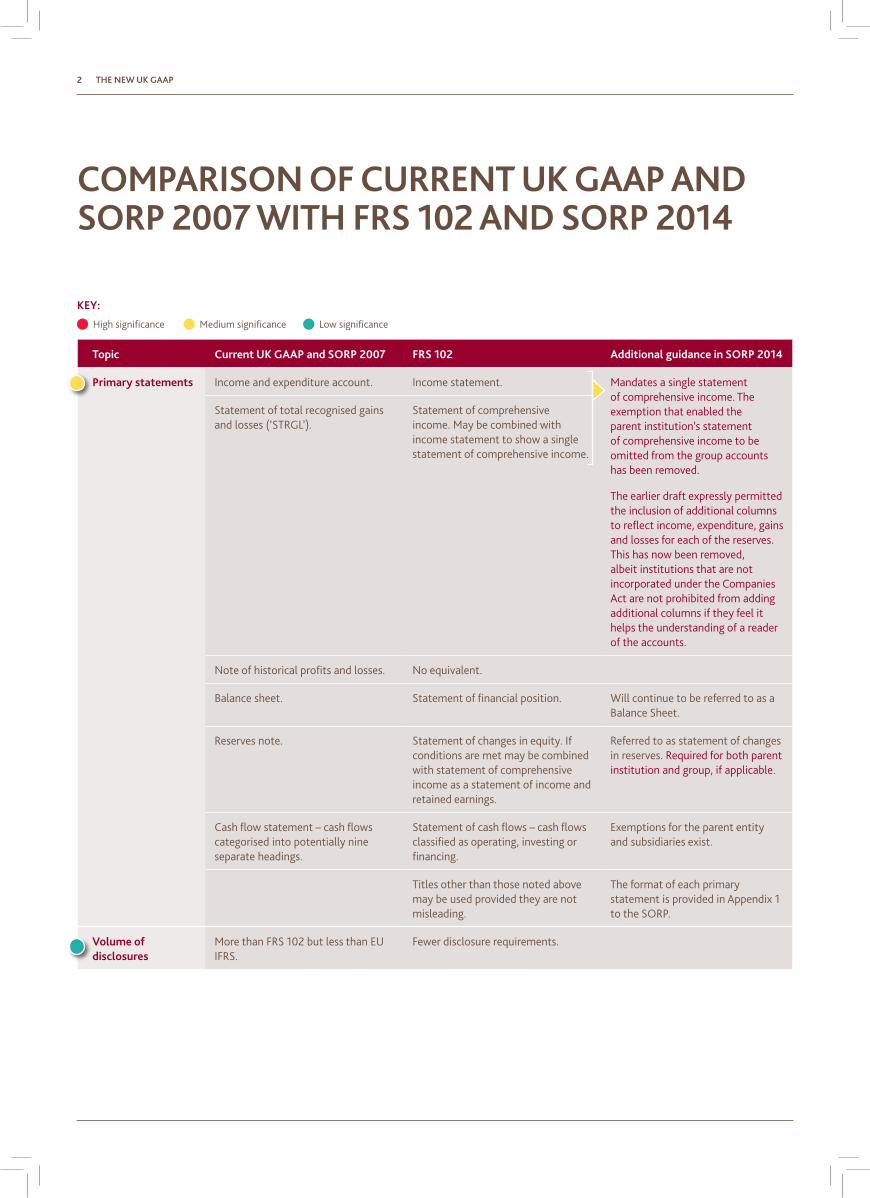

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

Primary statements Income and expenditure account. Income statement. Mandates a single statement of comprehensive income. The exemption that enabled the parent institution’s statement of comprehensive income to be omitted from the group accounts has been removed.

The earlier draft expressly permitted the inclusion of additional columns to reflect income, expenditure, gains and losses for each of the reserves. This has now been removed, albeit institutions that are not incorporated under the Companies Act are not prohibited from adding additional columns if they feel it helps the understanding of a reader of the accounts.

Statement of total recognised gains and losses (‘STRGL’).

Statement of comprehensive income. May be combined with income statement to show a single statement of comprehensive income.

Note of historical profits and losses. No equivalent.

Balance sheet. Statement of financial position. Will continue to be referred to as a Balance Sheet.

Reserves note. Statement of changes in equity. If conditions are met may be combined with statement of comprehensive income as a statement of income and retained earnings.

Referred to as statement of changes in reserves. Required for both parent institution and group, if applicable.

Cash flow statement – cash flows categorised into potentially nine separate headings.

Statement of cash flows – cash flows classified as operating, investing or financing.

Exemptions for the parent entity and subsidiaries exist.

Titles other than those noted above may be used provided they are not misleading.

The format of each primary statement is provided in Appendix 1 to the SORP.

Volume of disclosures

More than FRS 102 but less than EU IFRS.

Fewer disclosure requirements.

High significance Medium significance Low significance

Key:

The new UK GAAP 3

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

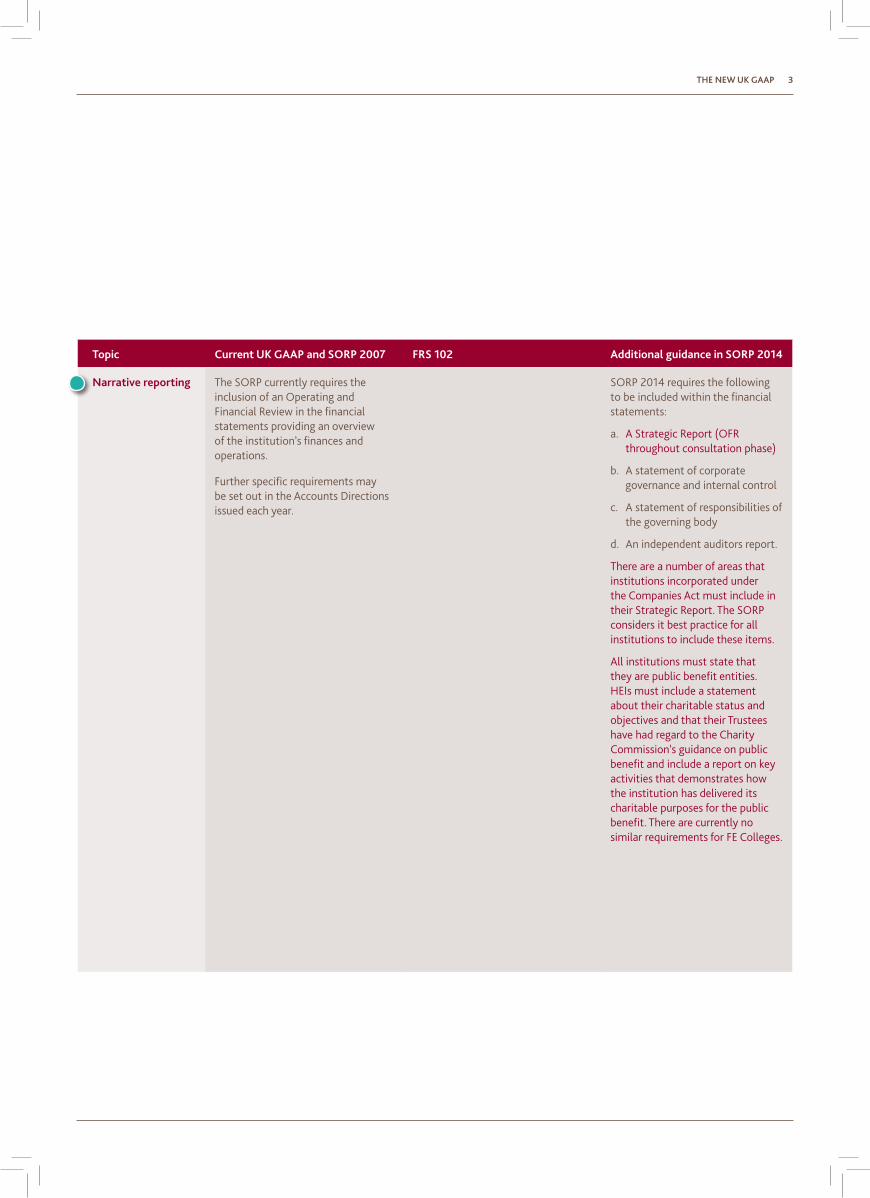

narrative reporting The SORP currently requires the inclusion of an Operating and Financial Review in the financial statements providing an overview of the institution’s finances and operations.

Further specific requirements may be set out in the Accounts Directions issued each year.

SORP 2014 requires the following to be included within the financial statements:

a. A Strategic Report (OFR throughout consultation phase)

b. A statement of corporate governance and internal control

c. A statement of responsibilities of the governing body

d. An independent auditors report.

There are a number of areas that institutions incorporated under the Companies Act must include in their Strategic Report. The SORP considers it best practice for all institutions to include these items.

All institutions must state that they are public benefit entities. HEIs must include a statement about their charitable status and objectives and that their Trustees have had regard to the Charity Commission’s guidance on public benefit and include a report on key activities that demonstrates how the institution has delivered its charitable purposes for the public benefit. There are currently no similar requirements for FE Colleges.

The new UK GAAP 4

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

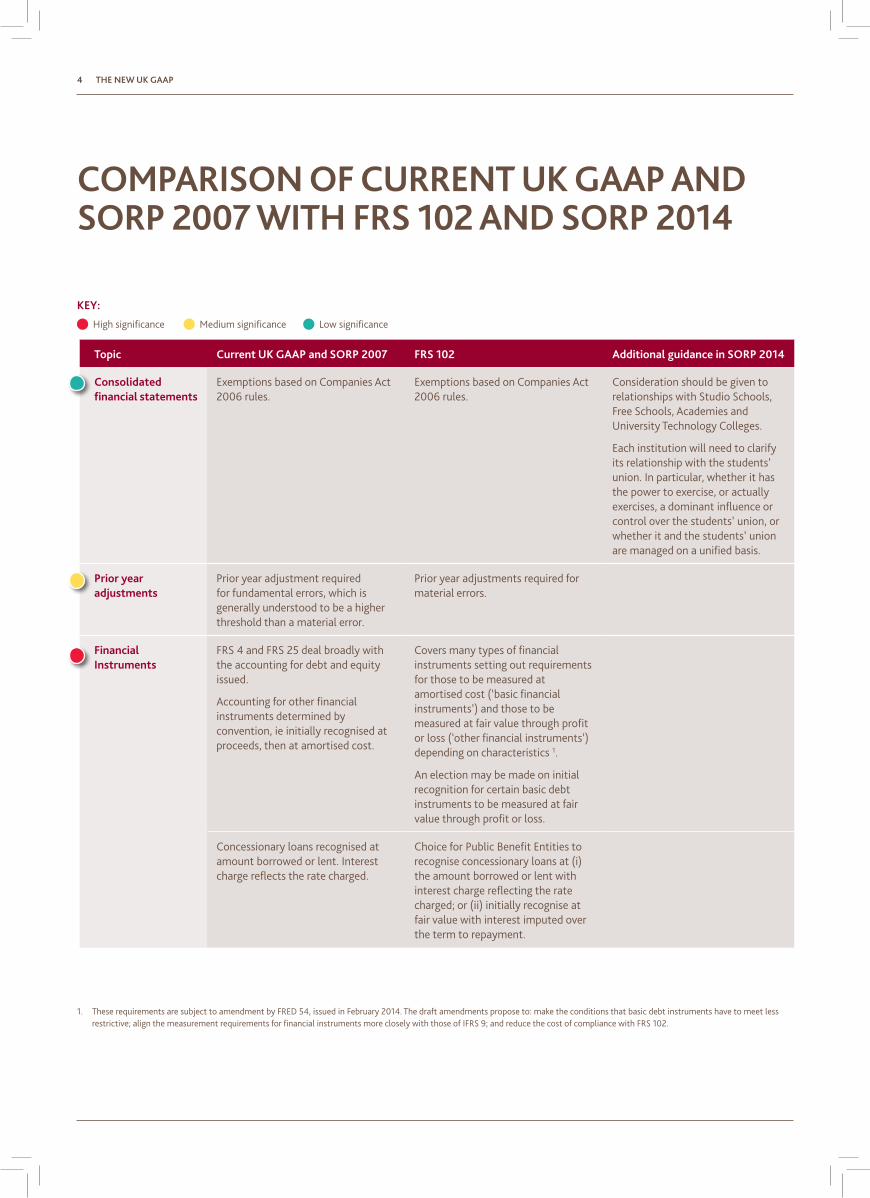

Consolidated financial statements

Exemptions based on Companies Act 2006 rules.

Exemptions based on Companies Act 2006 rules.

Consideration should be given to relationships with Studio Schools, Free Schools, Academies and University Technology Colleges.

Each institution will need to clarify its relationship with the students’ union. In particular, whether it has the power to exercise, or actually exercises, a dominant influence or control over the students’ union, or whether it and the students’ union are managed on a unified basis.

Prior year adjustments

Prior year adjustment required for fundamental errors, which is generally understood to be a higher threshold than a material error.

Prior year adjustments required for material errors.

Financial instruments

FRS 4 and FRS 25 deal broadly with the accounting for debt and equity issued.

Accounting for other financial instruments determined by convention, ie initially recognised at proceeds, then at amortised cost.

Covers many types of financial instruments setting out requirements for those to be measured at amortised cost (‘basic financial instruments’) and those to be measured at fair value through profit or loss (‘other financial instruments’) depending on characteristics 1.

An election may be made on initial recognition for certain basic debt instruments to be measured at fair value through profit or loss.

Concessionary loans recognised at amount borrowed or lent. Interest charge reflects the rate charged.

Choice for Public Benefit Entities to recognise concessionary loans at (i) the amount borrowed or lent with interest charge reflecting the rate charged; or (ii) initially recognise at fair value with interest imputed over the term to repayment.

1. These requirements are subject to amendment by FRED 54, issued in February 2014. The draft amendments propose to: make the conditions that basic debt instruments have to meet less restrictive; align the measurement requirements for financial instruments more closely with those of IFRS 9; and reduce the cost of compliance with FRS 102.

High significance Medium significance Low significance

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

Key:

The new UK GAAP 5

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

Financial instruments (continued)

No specific rules around bad debt provisions – amount determined by expectation.

Provide for bad debts only when there is objective evidence of impairment.

Limited disclosure requirements. To include accounting policies; carrying amount by category; basis of de-recognising financial assets; collateral; defaults and breaches on financial liabilities; analysis of gains and losses on financial instruments; and information about fair value.

derivatives and hedge accounting

Derivative contracts are not held at fair value on the balance sheet unless an election is made under the Companies Act and full provisions of FRS 26 applied.

Derivatives are measured at fair value through profit or loss. Gains and losses on derivatives held as hedging instruments and meeting certain conditions are permitted to be shown in other comprehensive income to the extent the hedging relationship is effective 2.

investments in Associates (group accounts)

Equity accounting. Equity accounting.

Share of all losses recognised even when this leads to an interest in net liabilities, unless the investor has irrevocably withdrawn from the relationship.

The default treatment is the opposite of current UK GAAP, ie the investor stops recognising losses when its investment reaches zero, unless it has a legal or constructive obligation to make good its share.

2. The detailed requirements around hedge accounting are subject to amendment by FRED 51. The draft amendments aim to update the requirements for hedge accounting in FRS 102 to achieve two ends: (a) to allow entities to apply hedge accounting when this reflects their economic and risk management strategies, without onerous conditions; and (b) to use concepts and language that are, as far as possible, consistent with those included in IFRS 9. The draft amendments to FRS 102 propose to allow entities to use hedge accounting where the hedging instrument, hedged item and hedging relationship meet certain broad conditions. It permits these relationships to be discontinued at any point, and prescribes the accounting treatment for their ongoing use and their discontinuation.

The new UK GAAP 6

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

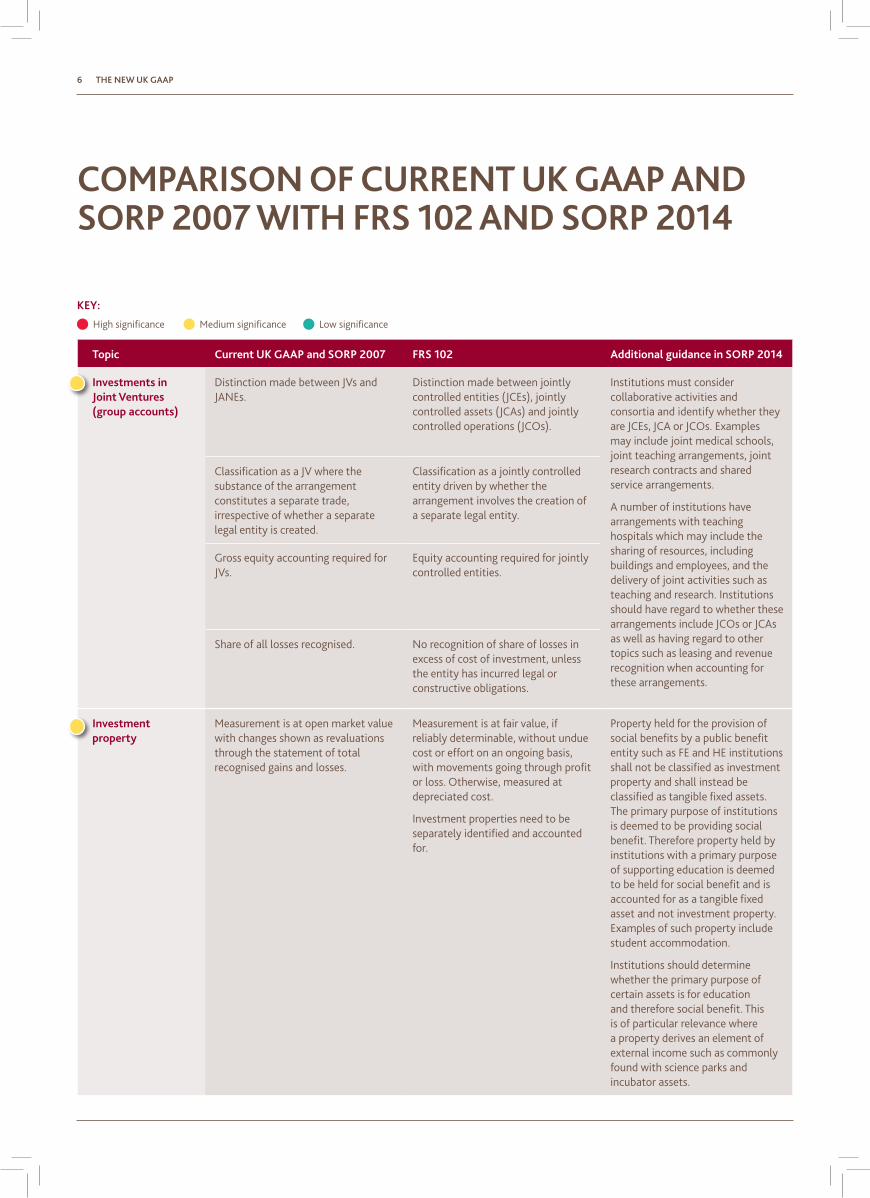

investments in Joint Ventures (group accounts)

Distinction made between JVs and JANEs.

Distinction made between jointly controlled entities (JCEs), jointly controlled assets (JCAs) and jointly controlled operations (JCOs).

Institutions must consider collaborative activities and consortia and identify whether they are JCEs, JCA or JCOs. Examples may include joint medical schools, joint teaching arrangements, joint research contracts and shared service arrangements.

A number of institutions have arrangements with teaching hospitals which may include the sharing of resources, including buildings and employees, and the delivery of joint activities such as teaching and research. Institutions should have regard to whether these arrangements include JCOs or JCAs as well as having regard to other topics such as leasing and revenue recognition when accounting for these arrangements.

Classification as a JV where the substance of the arrangement constitutes a separate trade, irrespective of whether a separate legal entity is created.

Classification as a jointly controlled entity driven by whether the arrangement involves the creation of a separate legal entity.

Gross equity accounting required for JVs.

Equity accounting required for jointly controlled entities.

Share of all losses recognised. No recognition of share of losses in excess of cost of investment, unless the entity has incurred legal or constructive obligations.

investment property

Measurement is at open market value with changes shown as revaluations through the statement of total recognised gains and losses.

Measurement is at fair value, if reliably determinable, without undue cost or effort on an ongoing basis, with movements going through profit or loss. Otherwise, measured at depreciated cost.

Investment properties need to be separately identified and accounted for.

Property held for the provision of social benefits by a public benefit entity such as FE and HE institutions shall not be classified as investment property and shall instead be classified as tangible fixed assets. The primary purpose of institutions is deemed to be providing social benefit. Therefore property held by institutions with a primary purpose of supporting education is deemed to be held for social benefit and is accounted for as a tangible fixed asset and not investment property. Examples of such property include student accommodation.

Institutions should determine whether the primary purpose of certain assets is for education and therefore social benefit. This is of particular relevance where a property derives an element of external income such as commonly found with science parks and incubator assets.

High significance Medium significance Low significance

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

Key:

The new UK GAAP 7

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

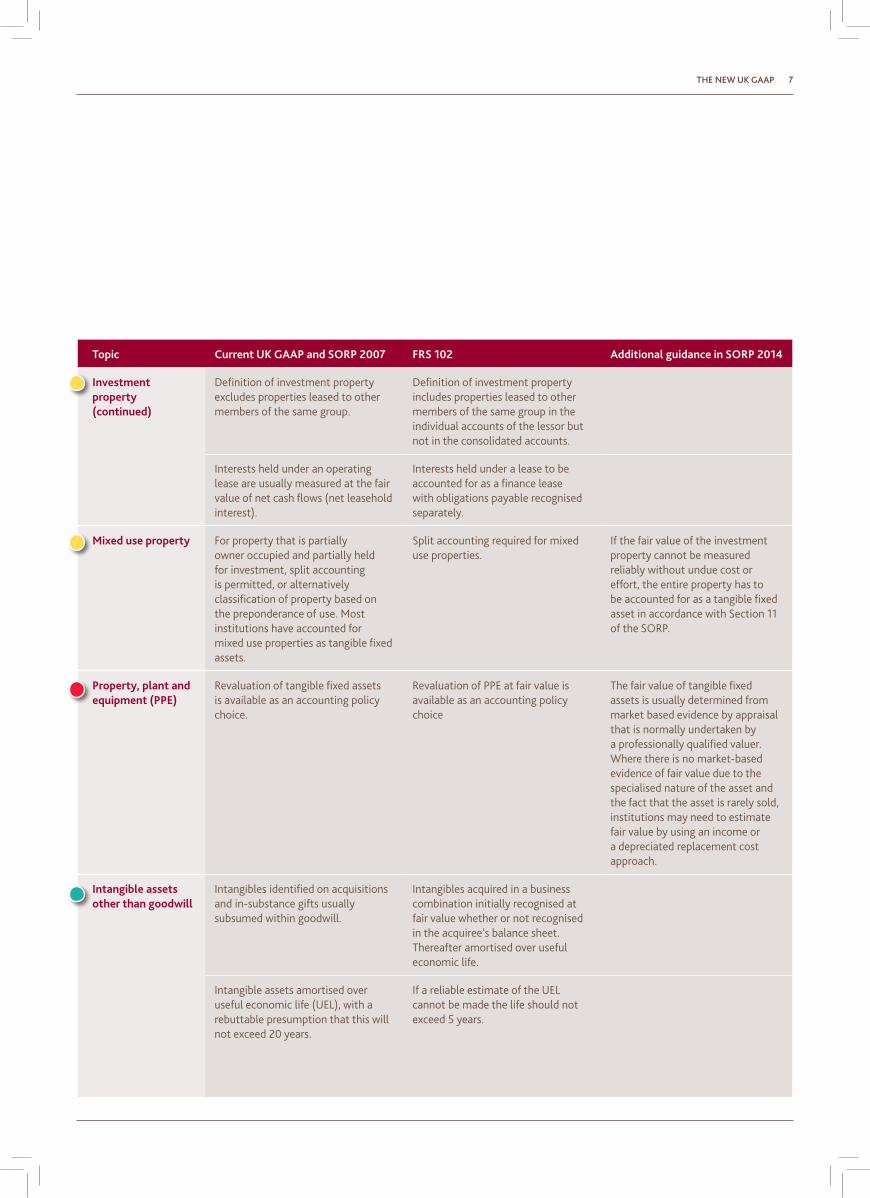

investment property (continued)

Definition of investment property excludes properties leased to other members of the same group.

Definition of investment property includes properties leased to other members of the same group in the individual accounts of the lessor but not in the consolidated accounts.

Interests held under an operating lease are usually measured at the fair value of net cash flows (net leasehold interest).

Interests held under a lease to be accounted for as a finance lease with obligations payable recognised separately.

mixed use property For property that is partially owner occupied and partially held for investment, split accounting is permitted, or alternatively classification of property based on the preponderance of use. Most institutions have accounted for mixed use properties as tangible fixed assets.

Split accounting required for mixed use properties.

If the fair value of the investment property cannot be measured reliably without undue cost or effort, the entire property has to be accounted for as a tangible fixed asset in accordance with Section 11 of the SORP.

Property, plant and equipment (PPe)

Revaluation of tangible fixed assets is available as an accounting policy choice.

Revaluation of PPE at fair value is available as an accounting policy choice

The fair value of tangible fixed assets is usually determined from market based evidence by appraisal that is normally undertaken by a professionally qualified valuer. Where there is no market-based evidence of fair value due to the specialised nature of the asset and the fact that the asset is rarely sold, institutions may need to estimate fair value by using an income or a depreciated replacement cost approach.

intangible assets other than goodwill

Intangibles identified on acquisitions and in-substance gifts usually subsumed within goodwill.

Intangibles acquired in a business combination initially recognised at fair value whether or not recognised in the acquiree’s balance sheet. Thereafter amortised over useful economic life.

Intangible assets amortised over useful economic life (UEL), with a rebuttable presumption that this will not exceed 20 years.

If a reliable estimate of the UEL cannot be made the life should not exceed 5 years.

The new UK GAAP 8

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

Business combinations and goodwill

Merger accounting permitted if certain criteria are met.

Merger accounting permitted for public benefit entity combinations that are in substance a gift or that are a merger.

Intangible assets rarely recognised separately from goodwill on a business combination.

Recognise identifiable intangibles (eg customer relationships and brands) on a business combination that can be measured reliably at fair value. Amortise over useful economic life (or no more than 5 years if UEL can’t be reliably estimated)

Adjustments may be made to the fair values of assets and liabilities acquired in a business combination in the first and second balance sheets after the acquisition (ie to the end of the first full year post acquisition).

Adjustments may only be made to amounts recognised at the acquisition date if they are identified within 12 months of the business combination, and are adjusted retrospectively. Thereafter they are only treated as adjustments to the initial accounting in order to recognise an error.

Goodwill amortised over UEL, with a rebuttable presumption that this will not exceed 20 years.

If a reliable estimate of the UEL cannot be made the life should not exceed 5 years.

Negative goodwill deferred in balance sheet and released to income statement over appropriate periods.

Negative goodwill deferred in balance sheet and released to income statement over appropriate periods.

For non-exchange transactions this is in the year of gift.

Leases Current UK GAAP has no specific requirements to split contracts that contain a lease into their separate elements.

FRS 102 requires arrangement that contain a lease to be identified, with the “lease element accounted for as an operating or finance lease as appropriate.

Lease incentives over the period to the first rent review.

Lease incentives spread over the lease term.

Disclosure required of the annual lease commitment.

Disclosure required of the total future minimum lease commitment.

Disclosure required of the aggregate rents receivable in the period.

Disclosure required of the total future minimum lease receivable.

High significance Medium significance Low significance

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

Key:

The new UK GAAP 9

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

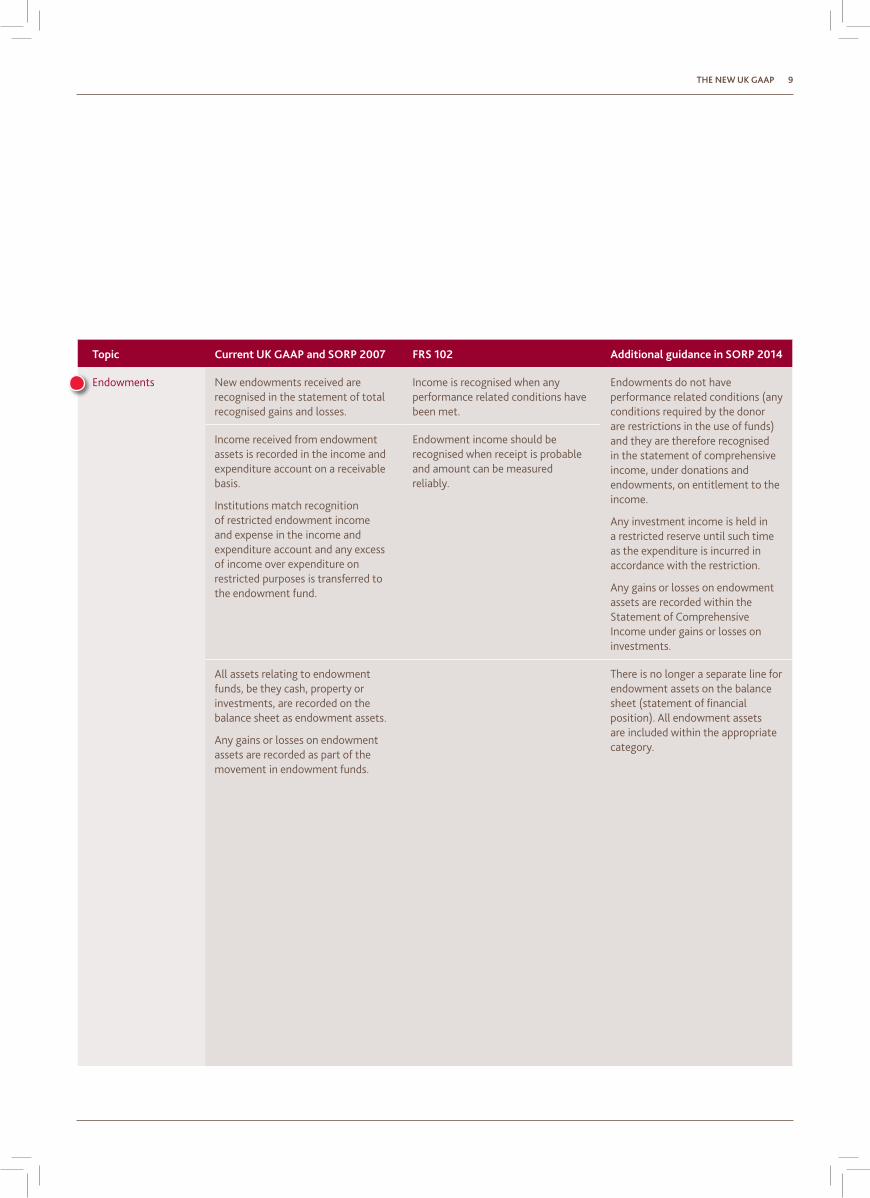

Endowments New endowments received are recognised in the statement of total recognised gains and losses.

Income is recognised when any performance related conditions have been met.

Endowments do not have performance related conditions (any conditions required by the donor are restrictions in the use of funds) and they are therefore recognised in the statement of comprehensive income, under donations and endowments, on entitlement to the income.

Any investment income is held in a restricted reserve until such time as the expenditure is incurred in accordance with the restriction.

Any gains or losses on endowment assets are recorded within the Statement of Comprehensive Income under gains or losses on investments.

Income received from endowment assets is recorded in the income and expenditure account on a receivable basis.

Institutions match recognition of restricted endowment income and expense in the income and expenditure account and any excess of income over expenditure on restricted purposes is transferred to the endowment fund.

Endowment income should be recognised when receipt is probable and amount can be measured reliably.

All assets relating to endowment funds, be they cash, property or investments, are recorded on the balance sheet as endowment assets.

Any gains or losses on endowment assets are recorded as part of the movement in endowment funds.

There is no longer a separate line for endowment assets on the balance sheet (statement of financial position). All endowment assets are included within the appropriate category.

The new UK GAAP 10

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

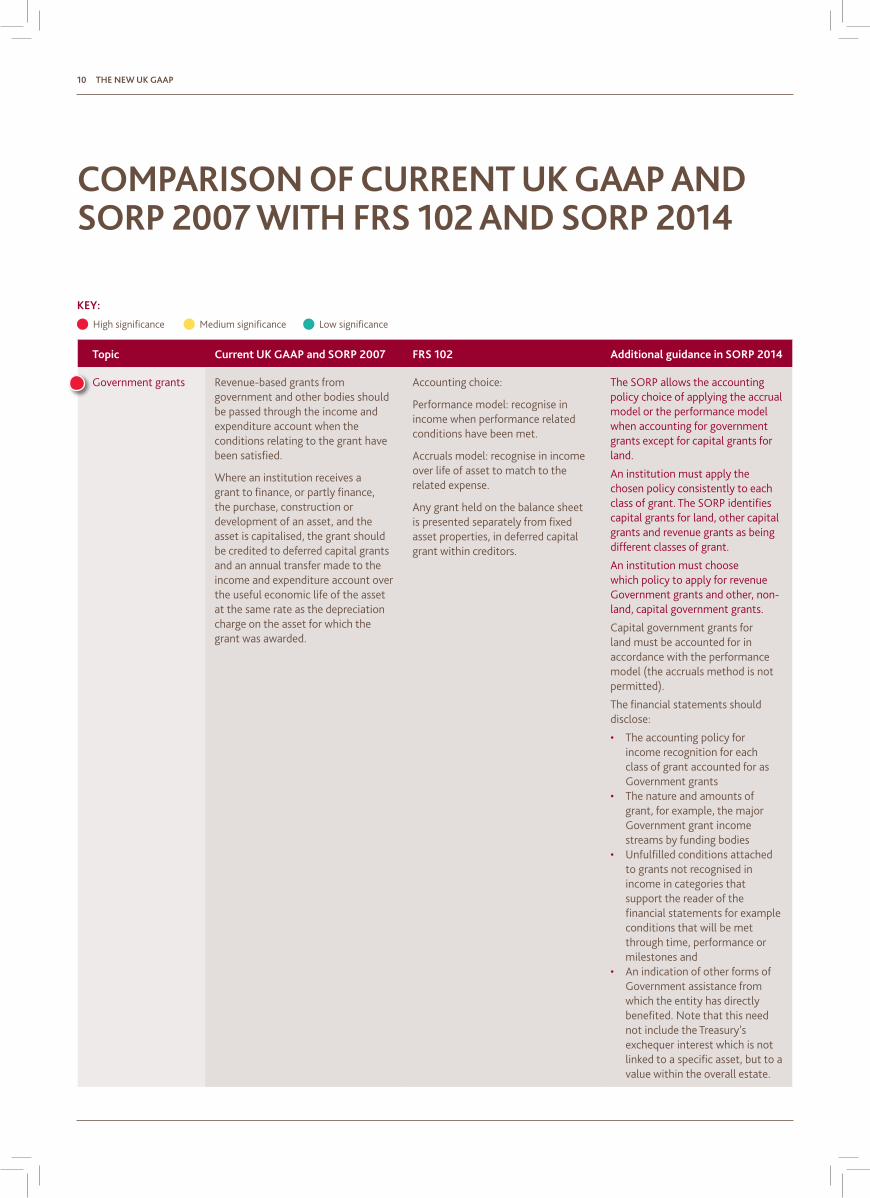

Government grants Revenue-based grants from government and other bodies should be passed through the income and expenditure account when the conditions relating to the grant have been satisfied.

Where an institution receives a grant to finance, or partly finance, the purchase, construction or development of an asset, and the asset is capitalised, the grant should be credited to deferred capital grants and an annual transfer made to the income and expenditure account over the useful economic life of the asset at the same rate as the depreciation charge on the asset for which the grant was awarded.

Accounting choice:

Performance model: recognise in income when performance related conditions have been met.

Accruals model: recognise in income over life of asset to match to the related expense.

Any grant held on the balance sheet is presented separately from fixed asset properties, in deferred capital grant within creditors.

The SORP allows the accounting policy choice of applying the accrual model or the performance model when accounting for government grants except for capital grants for land.

An institution must apply the chosen policy consistently to each class of grant. The SORP identifies capital grants for land, other capital grants and revenue grants as being different classes of grant.

An institution must choose which policy to apply for revenue Government grants and other, non-land, capital government grants.

Capital government grants for land must be accounted for in accordance with the performance model (the accruals method is not permitted).

The financial statements should disclose:

• The accounting policy for income recognition for each class of grant accounted for as Government grants

• The nature and amounts of grant, for example, the major Government grant income streams by funding bodies

• Unfulfilled conditions attached to grants not recognised in income in categories that support the reader of the financial statements for example conditions that will be met through time, performance or milestones and

• An indication of other forms of Government assistance from which the entity has directly benefited. Note that this need not include the Treasury’s exchequer interest which is not linked to a specific asset, but to a value within the overall estate.

High significance Medium significance Low significance

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

Key:

The new UK GAAP 11

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

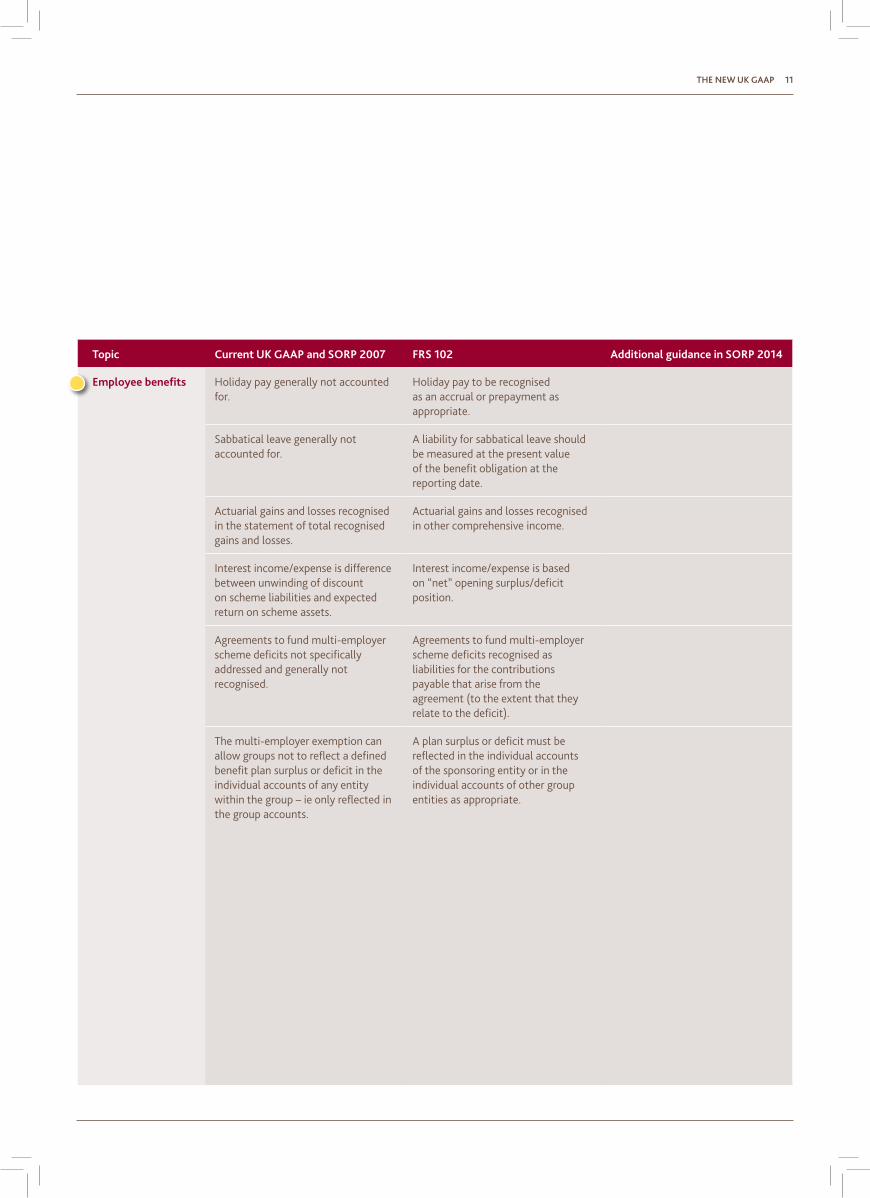

employee benefits Holiday pay generally not accounted for.

Holiday pay to be recognised as an accrual or prepayment as appropriate.

Sabbatical leave generally not accounted for.

A liability for sabbatical leave should be measured at the present value of the benefit obligation at the reporting date.

Actuarial gains and losses recognised in the statement of total recognised gains and losses.

Actuarial gains and losses recognised in other comprehensive income.

Interest income/expense is difference between unwinding of discount on scheme liabilities and expected return on scheme assets.

Interest income/expense is based on “net” opening surplus/deficit position.

Agreements to fund multi-employer scheme deficits not specifically addressed and generally not recognised.

Agreements to fund multi-employer scheme deficits recognised as liabilities for the contributions payable that arise from the agreement (to the extent that they relate to the deficit).

The multi-employer exemption can allow groups not to reflect a defined benefit plan surplus or deficit in the individual accounts of any entity within the group – ie only reflected in the group accounts.

A plan surplus or deficit must be reflected in the individual accounts of the sponsoring entity or in the individual accounts of other group entities as appropriate.

The new UK GAAP 12

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

Related party disclosures

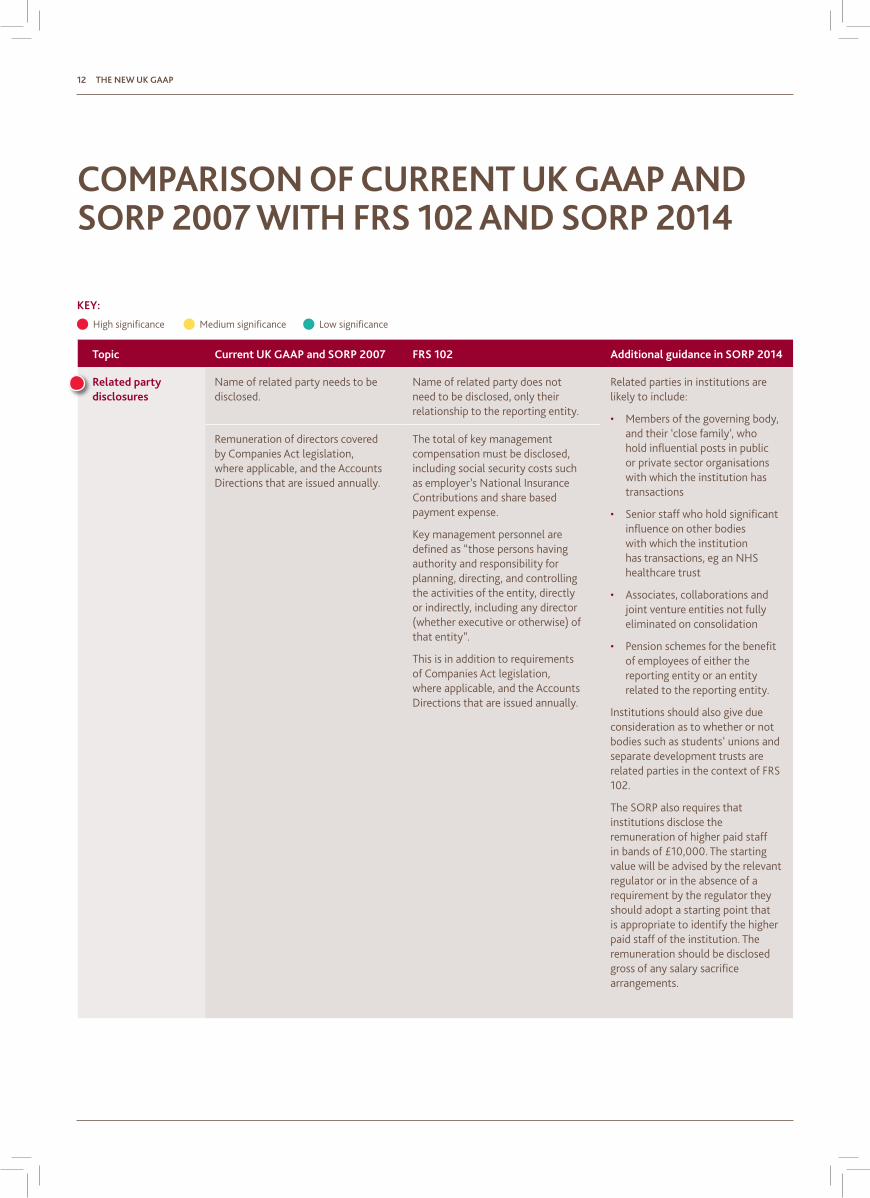

Name of related party needs to be disclosed.

Name of related party does not need to be disclosed, only their relationship to the reporting entity.

Related parties in institutions are likely to include:

• Members of the governing body, and their ‘close family’, who hold influential posts in public or private sector organisations with which the institution has transactions

• Senior staff who hold significant influence on other bodies with which the institution has transactions, eg an NHS healthcare trust

• Associates, collaborations and joint venture entities not fully eliminated on consolidation

• Pension schemes for the benefit of employees of either the reporting entity or an entity related to the reporting entity.

Institutions should also give due consideration as to whether or not bodies such as students’ unions and separate development trusts are related parties in the context of FRS 102.

The SORP also requires that institutions disclose the remuneration of higher paid staff in bands of £10,000. The starting value will be advised by the relevant regulator or in the absence of a requirement by the regulator they should adopt a starting point that is appropriate to identify the higher paid staff of the institution. The remuneration should be disclosed gross of any salary sacrifice arrangements.

Remuneration of directors covered by Companies Act legislation, where applicable, and the Accounts Directions that are issued annually.

The total of key management compensation must be disclosed, including social security costs such as employer’s National Insurance Contributions and share based payment expense.

Key management personnel are defined as “those persons having authority and responsibility for planning, directing, and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of that entity”.

This is in addition to requirements of Companies Act legislation, where applicable, and the Accounts Directions that are issued annually.

High significance Medium significance Low significance

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

Key:

The new UK GAAP 13

topic Current UK GAAP and SORP 2007 FRS 102 Additional guidance in SORP 2014

Specialised activities: Service concessions

Under current UK GAAP, there is guidance on such contracts in FRS 5: Accounting for the substance of transactions.

The key consideration under FRS 5 is whether an operator has assets (eg a property) used to provide the contracted services, or alternatively a debtor, being the right to receive payments for the contracted services (in which case the property is an asset of the grantor).

Which of the two contracting parties should be recognising the asset and related liability is driven by an assessment of who is exposed to the associated risks and rewards of that asset.

FRS 102 defines a service concession arrangement as an arrangement where a public sector body or public benefit entity (the grantor) contracts with a private sector entity (the operator) to construct (or upgrade), operate and maintain infrastructure assets for a specific period of time.

Specifically, the following conditions must be met:

a. The grantor controls or regulates what services the operator must provide, to whom, and at what price

b. Where the arrangement is for a period less than the useful economic life of the infrastructure assets, the grantor controls any significant residual interest in the property at the end of the term of the arrangement.

Where these two conditions are met, the grantor rather than the operator will recognise the asset(s) which is (are) the subject of the contract, and a liability for the payments for its obligation under the service concession arrangement, ie account for any amounts payable, including any amounts guaranteed as a finance liability.

HEIs may find themselves in this situation if, say, they enter into arrangements with other parties to refurbish, build, or take over student accommodation at some point in the future in return for payments or guaranteeing liabilities of the operator. The SORP clarifies that student accommodation is an infrastructure asset.

The SORP provides a decision tree to determine whether an arrangement will be accounted for as a service concession arrangement:

a. Is the institution acting as principal within the arrangement?

b. Does the arrangement meet the definition of a service concession arrangement?

c. Does the arrangement pass the control tests set out in FRS 102?

If all three tests are met then the arrangement will be accounted for in accordance with leasing arrangements in FRS 102 and an asset and liability will be recognised at the present value of the minimum lease payments.

Future lease payments are allocated between finance charges, lifecycle costs, service costs and repayment of the liability.

The new UK GAAP 14

topic Current UK GAAP and SORP 2007 Additional guidance in SORP 2014

transition Section 35 sets out the requirements on transition. Of particular note are:

• Any adjustments arising from restating transactions or other events or conditions that arose before the date of transition should be recognised directly in retained earnings at the date of transition.

• Exemptions available relating to:

– Business combinations: you can elect not to apply Section 19 Business Combinations and Goodwill to business combinations that were effected before the date of transition. However if any business combination is restated then all later business combinations must also be restated. This applies equally to public benefit entity combinations

– Fair value as deemed cost: you can elect to measure an item of property, plant and equipment; investment property; or intangible asset at fair value on the transition date and then use that fair value as deemed cost at that date. As this exemption can be applied to items of property, plant and equipment rather than classes of or all, it is possible to ‘cherry pick’ which items are treated in this way

– Revaluation as deemed cost: you can elect to measure an item of property, plant and equipment; investment property; or intangible asset using a previous GAAP revaluation performed at or before the transition date and then use that revalued amount as deemed cost at the date of transition. As this exemption can be applied to items of property, plant and equipment rather than classes of or all, it is possible to ‘cherry pick’ which items are treated in this way

– The corresponding credit on using fair value/previous GAAP revaluation as deemed cost should be recorded in revenue reserves with other transition adjustments

– Borrowing costs: an entity electing to adopt an accounting policy of capitalising borrowing costs as part of the cost of a qualifying assets may elect to treat the date of transition as the date on which capitalisation commences.

• Disclosure is required of:

– Each change in accounting policy

– A reconciliation of equity under current UK GAAP to equity determined under FRS 102 at the date of transition and end of latest period presented in the most recent financial statements prepared under current UK GAAP

– A reconciliation of the profit or loss determined under current UK GAAP to its profit or loss determined in accordance with FRS 102.

Assets inherited from local authorities and similar bodies: should be held at existing book value on transition or at revaluation if a transition option to revalue is applied.

COmPARiSOn OF CURRent UK GAAP And SORP 2007 With FRS 102 And SORP 2014

High significance Medium significance Low significance

Key:

nOteS

JAMeS ASton, MBe

nAtiOnAL heAd OF edUCAtiOn

m: +44 07899 052 989 e: [email protected]

This publication has been carefully prepared, but it has been written in general terms and should be seen as broad guidance only. The publication cannot be relied upon to cover specific situations and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact BDO LLP to discuss these matters in the context of your particular circumstances. BDO LLP, its partners, employees and agents do not accept or assume any liability or duty of care for any loss arising from any action taken or not taken by anyone in reliance on the information in this publication or for any decision based on it.

BDO LLP, a UK limited liability partnership registered in England and Wales under number OC305127, is a member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. A list of members’ names is open to inspection at our registered office, 55 Baker Street, London W1U 7EU. BDO LLP is authorised and regulated by the Financial Conduct Authority to conduct investment business.

BDO is the brand name of the BDO network and for each of the BDO Member Firms.

BDO Northern Ireland, a partnership formed in and under the laws of Northern Ireland, is licensed to operate within the international BDO network of independent member firms.

© May 2014 BDO LLP. All rights reserved.

www.bdo.co.uk

HB0

6164

for more information:If you would like further information about this publication please contact:

www.bdo.co.uk