cross country differences in venture capital financing

TRANSCRIPT

1 | Page

CROSS-COUNTRY DIFFERNECES IN VENTURE CAPITAL FINANCING

APRIL 2013

MASTER THESIS

Author: Christian Scheel Tost – 221086-1109 Study program: MSc. Applied Economics and Finance Course: Master Thesis Supervisor: Jens Frøslev Christensen Date of submission: 2013-04-19 Page count: 88 Word count: 36.404 Character count (with spaces): 226.329

Can a well-functioning venture capital industry spur innovation within local economies – an empirical comparison of the US, UK, IL and DK venture capital markets and investment approach?

2 | Page

Contents

Contents ......................................................................................................................................................................................... 2

Executive Summary ................................................................................................................................................................... 6

1. Introduction ............................................................................................................................................................................. 7

1.2 Research Objective ......................................................................................................................................................... 9

1.3 Research Method .......................................................................................................................................................... 10

1.4 Research Design ............................................................................................................................................................ 12

2. Introduction: Venture Capital Financing of Start-Ups in Business Administration Theory ........................ 13

2.1 Definition of Venture Capital ................................................................................................................................... 13

2.2 Equity Financing: Venture Capital Financing ...................................................................................................... 13

2.2.1 Crowd Funding ....................................................................................................................................... 14

2.2.2 Institutional Venture Capital ................................................................................................................ 15

2.2.3 Independent Venture Capital (IVC) .................................................................................................... 16

2.3. Stages in the Financing Life Cycle of a Start-up ................................................................................................ 17

2.3.1 Venture Characteristics in the Different Stages ................................................................................. 18

2.3.2 Structure of Independent Venture Capital Firms .............................................................................. 19

2.3.3 Role of Independent Venture Capital Firms in Start-ups ................................................................ 20

2.4 Theoretical Foundation for Explanation of the Behavior of Venture Capital Firms ............................. 21

2.4.1 Agency Theory Model: Asymmetric Information, Moral Hazard and Adverse Selection .......... 22

2.4.2 Mitigation of Agency Risk ..................................................................................................................... 23

2.5 Typical Venture Capital Investment Process: VC Investment Cycle ........................................................... 24

2.5.1 Contact Phase ......................................................................................................................................... 24

2.5.2 Screening Investment Ideas .................................................................................................................. 25

2.5.3 Due Diligence ......................................................................................................................................... 26

2.5.4 Management Phase (Value Adding Services) ..................................................................................... 30

2.5.5. Exit Phase ............................................................................................................................................... 32

3. Empirical Study on Explaining the Venture Capital Impact on Innovation and Economic Growth ...... 34

3 | Page

3.1 Empirical Study and Definition of Innovation ................................................................................................... 34

3.1.1 What is Innovation? ............................................................................................................................... 34

3.1.2 How to Measure Innovation ................................................................................................................ 35

3.2 Economic Growth With Innovation ...................................................................................................................... 37

3.2.1 Managing and Facilitating Quality Innovations ................................................................................. 38

3.3 Literature Review: Does Venture Capital Spur Innovation? ........................................................................... 41

3.2.1 Does Venture Capital Create Innovative Incentive? ......................................................................... 41

3.2.1 Does Venture Capital Spur Sustainable Innovation? ........................................................................ 42

4. National Innovation Systems: Macroeconomic Environment of the Venture Capital Industry in the US,

UK, IL and DK ......................................................................................................................................................................... 44

4.1 General Demographic, Economic Data and the Venture Capital Markets ................................................ 44

4.2 Macroeconomic Attractiveness of VC Markets .................................................................................................. 46

4.2.1 Capital Availability.................................................................................................................................. 47

4.2.2 Entrepreneurial Capital ......................................................................................................................... 48

4.2.3 Entrepreneurial Culture ......................................................................................................................... 49

4.2.4 Nation Infrastructure ............................................................................................................................. 50

4.2.5 Regulative Environment........................................................................................................................ 51

4.3 Overview of attractiveness of DK, IL, UK, and US ......................................................................................... 51

5. Research Framework Model and Hypotheses Development ................................................................................. 55

5.1 Average Size of Investment ....................................................................................................................................... 55

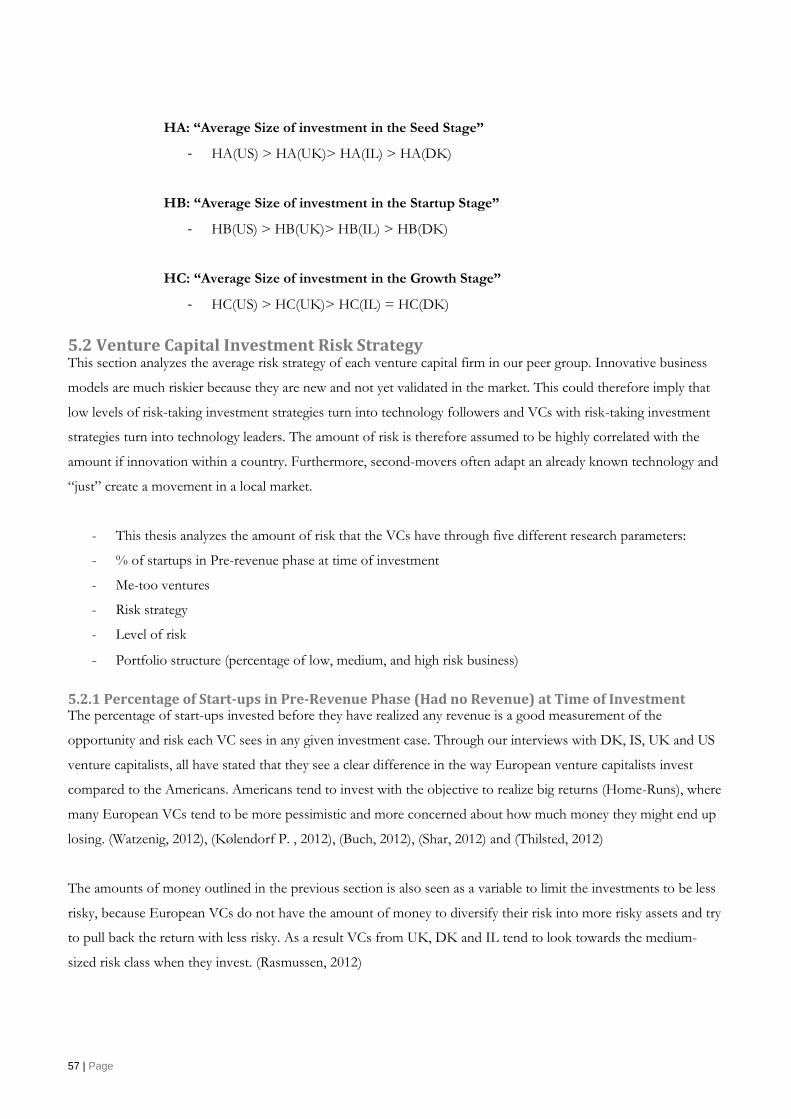

5.1.1 Hypotheses Development: HA, HB, and HC ................................................................................... 56

5.2 Venture Capital Investment Risk Strategy ............................................................................................................ 57

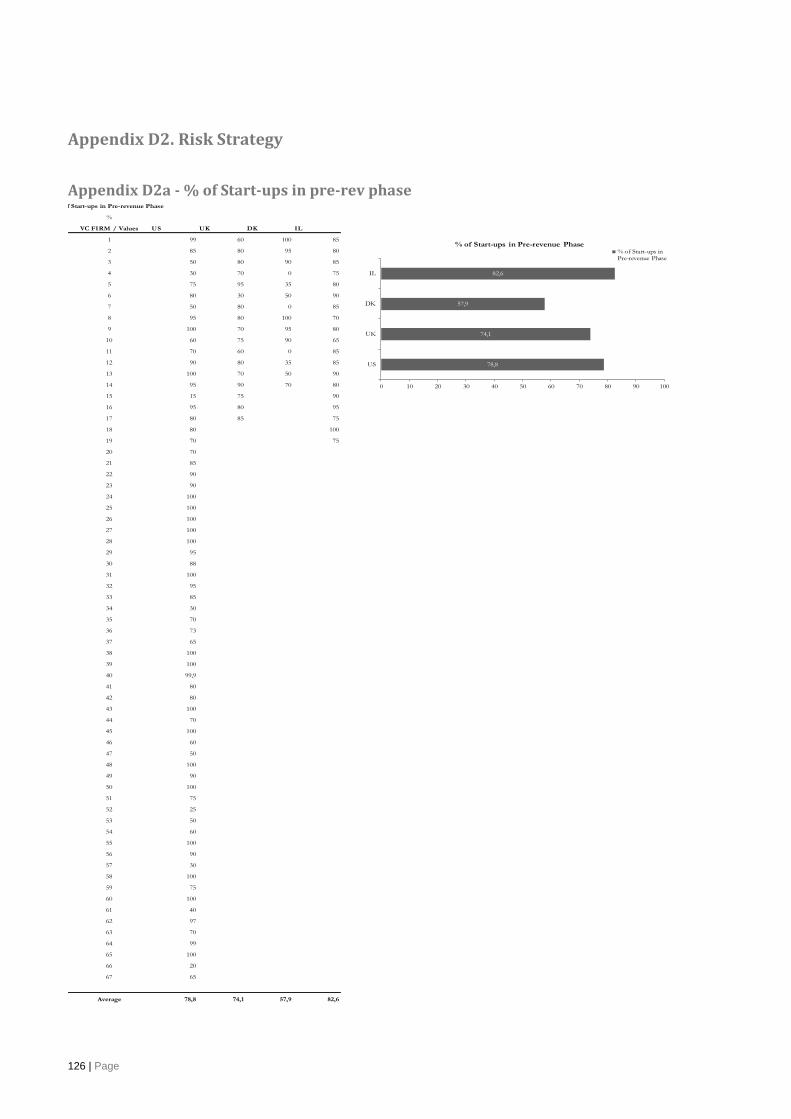

5.2.1 Percentage of Start-ups in Pre-Revenue Phase (Had no Revenue) at Time of Investment ........ 57

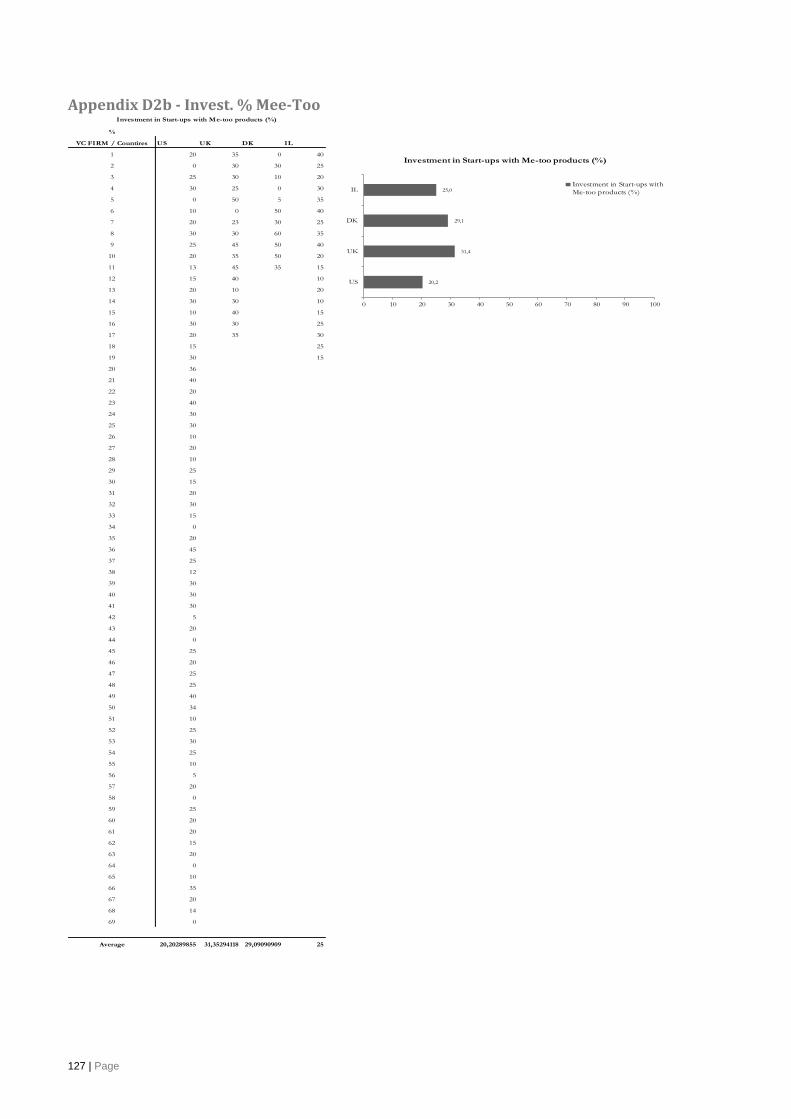

5.2.2 Me-Too Ventures, Risk Strategy and Level of Risk .......................................................................... 58

5.2.3 Portfolio Structure ................................................................................................................................. 59

5.3 Due Diligence ................................................................................................................................................................ 60

5.3.1 Management Team Due Diligence ...................................................................................................... 60

5.3.2 Market and Product/Service Due Diligence ...................................................................................... 61

4 | Page

5.4 Management Phase (Value Adding Phase) ........................................................................................................... 63

5.5 Exit Phase........................................................................................................................................................................ 65

6. Analysis and Comparison of Findings ........................................................................................................................... 67

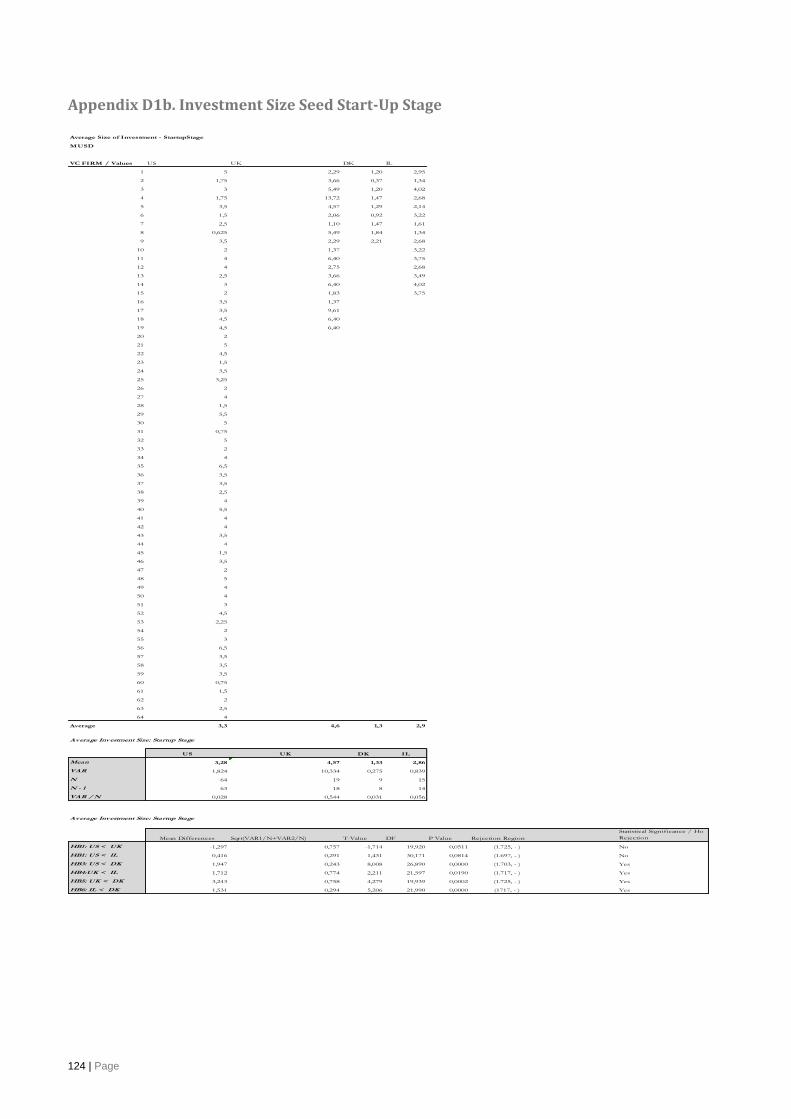

6.1 Average Size of Investment: Investment Strategy .............................................................................................. 67

6.1.1 Average Size of Investment: Seed Stage ............................................................................................. 67

6.1.2 Average Size of investment: Startup Stage ......................................................................................... 69

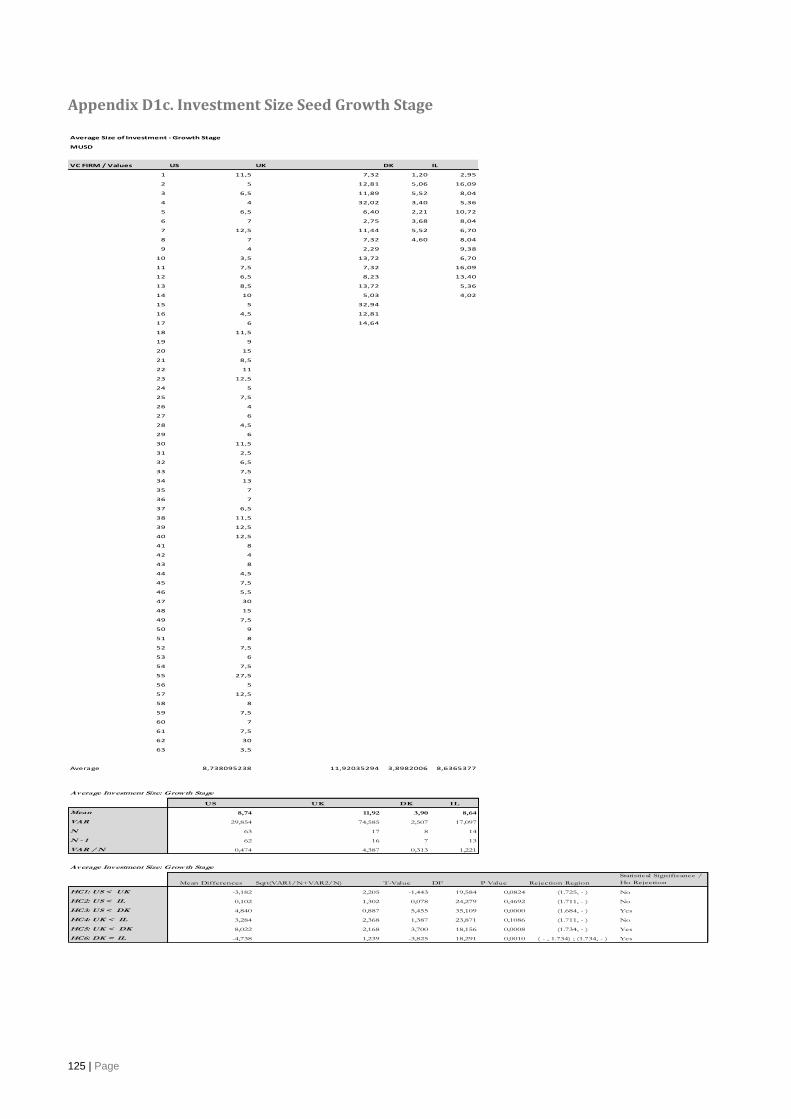

6.1.3 Average Size of Investment: Growth Stage ....................................................................................... 71

6.1.4 Conclusion on Investment Strategy ..................................................................................................... 73

6.2 Investment Risk Strategy: Risk Strategy ................................................................................................................ 73

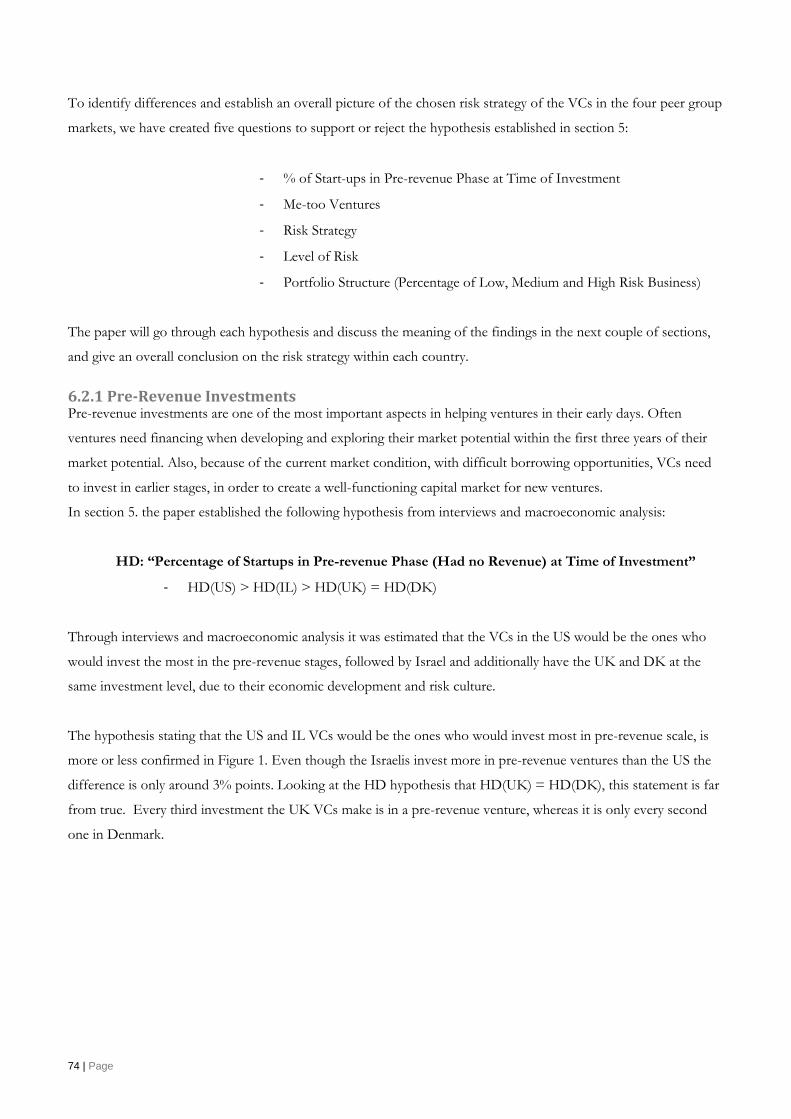

6.2.1 Pre-Revenue Investments ..................................................................................................................... 74

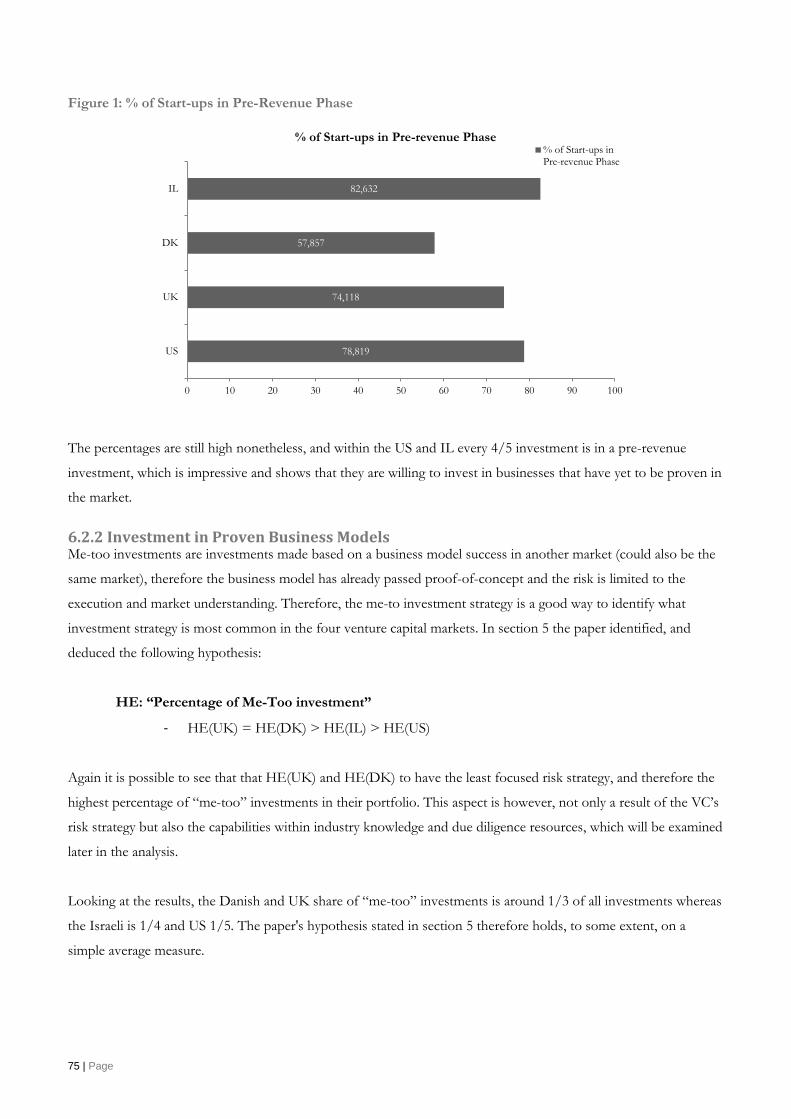

6.2.2 Investment in Proven Business Models .............................................................................................. 75

6.2.3 Investment Strategy ............................................................................................................................... 76

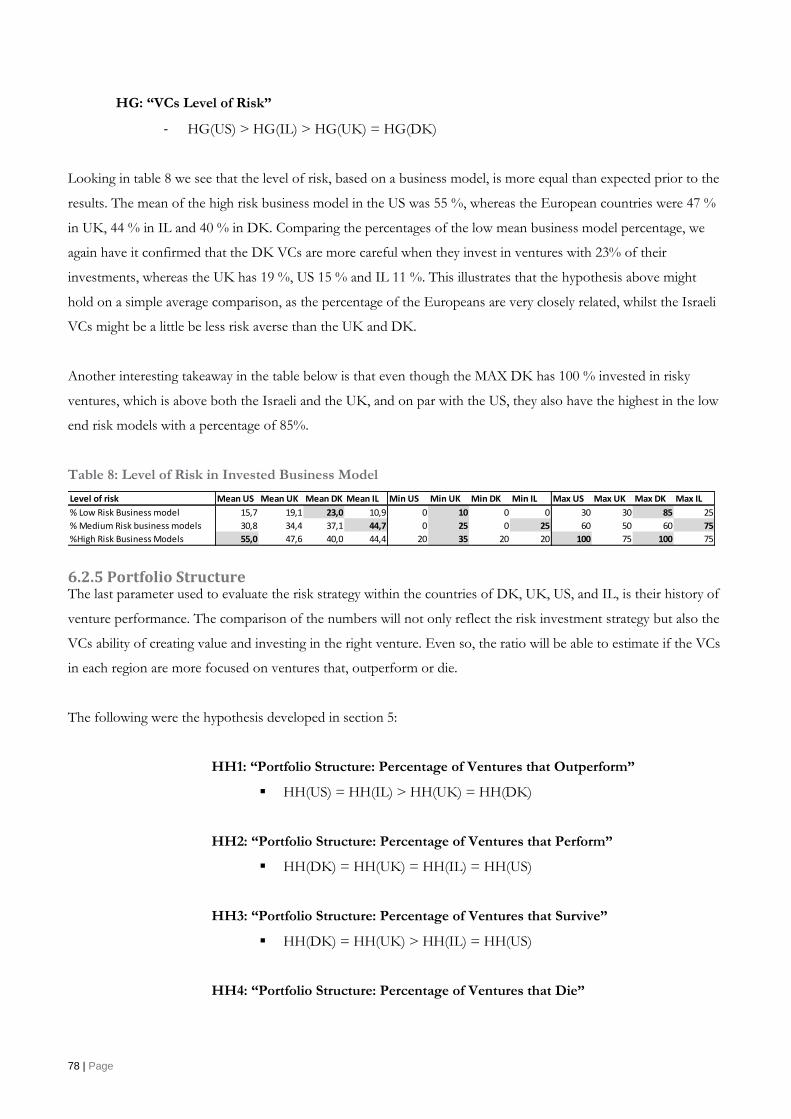

6.2.4 Level of Risk ........................................................................................................................................... 77

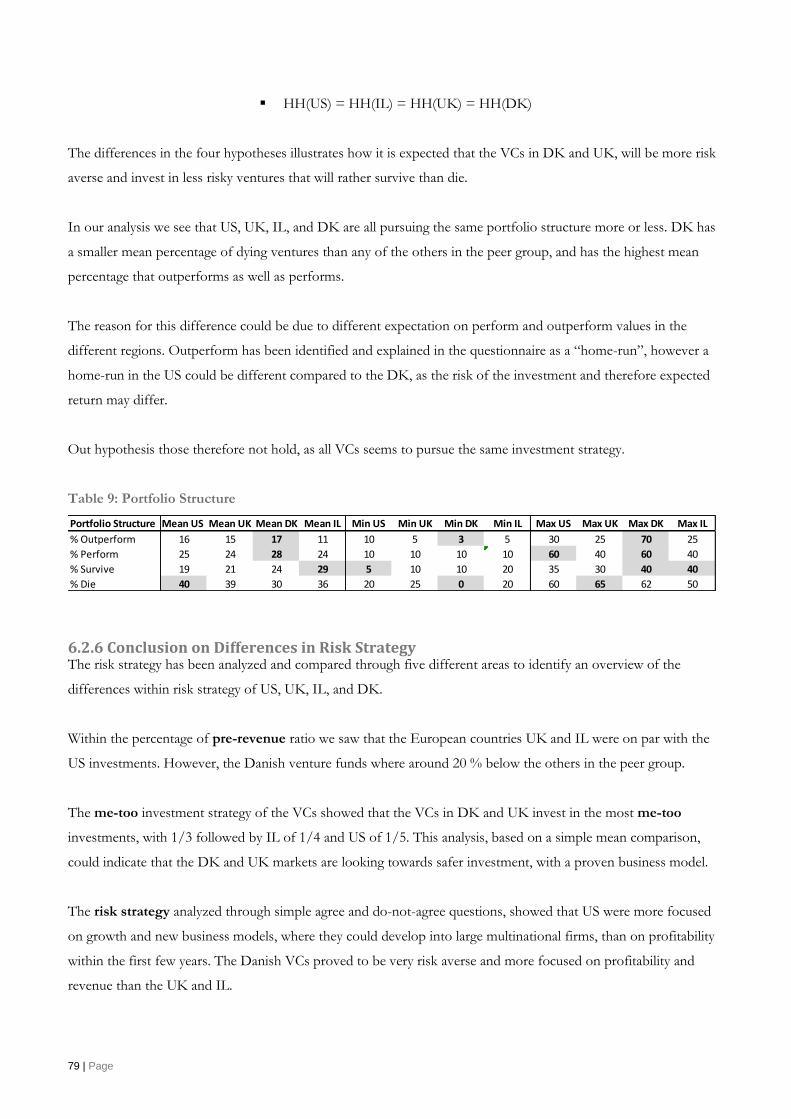

6.2.5 Portfolio Structure ................................................................................................................................. 78

6.2.6 Conclusion on Differences in Risk Strategy ....................................................................................... 79

6.3 Due Diligence: Limitation of Risk and Maturity of Market ............................................................................ 80

6.3.1 Replacement of CEO – Management Team ...................................................................................... 80

6.3.2 Differences in Market Due Diligence Approach ............................................................................... 81

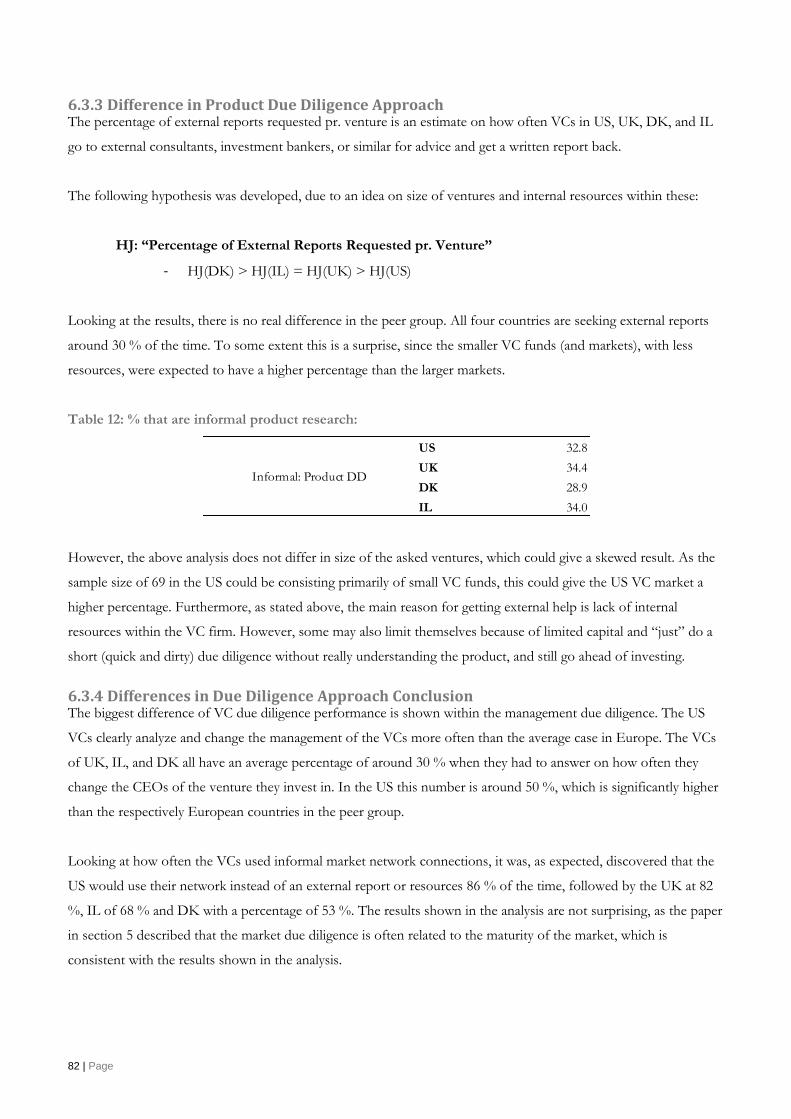

6.3.3 Difference in Product Due Diligence Approach ............................................................................... 82

6.3.4 Differences in Due Diligence Approach Conclusion ....................................................................... 82

6.4 Management Phase: Value Adding Strategy ......................................................................................................... 83

6.4.1 Employee Mix ......................................................................................................................................... 84

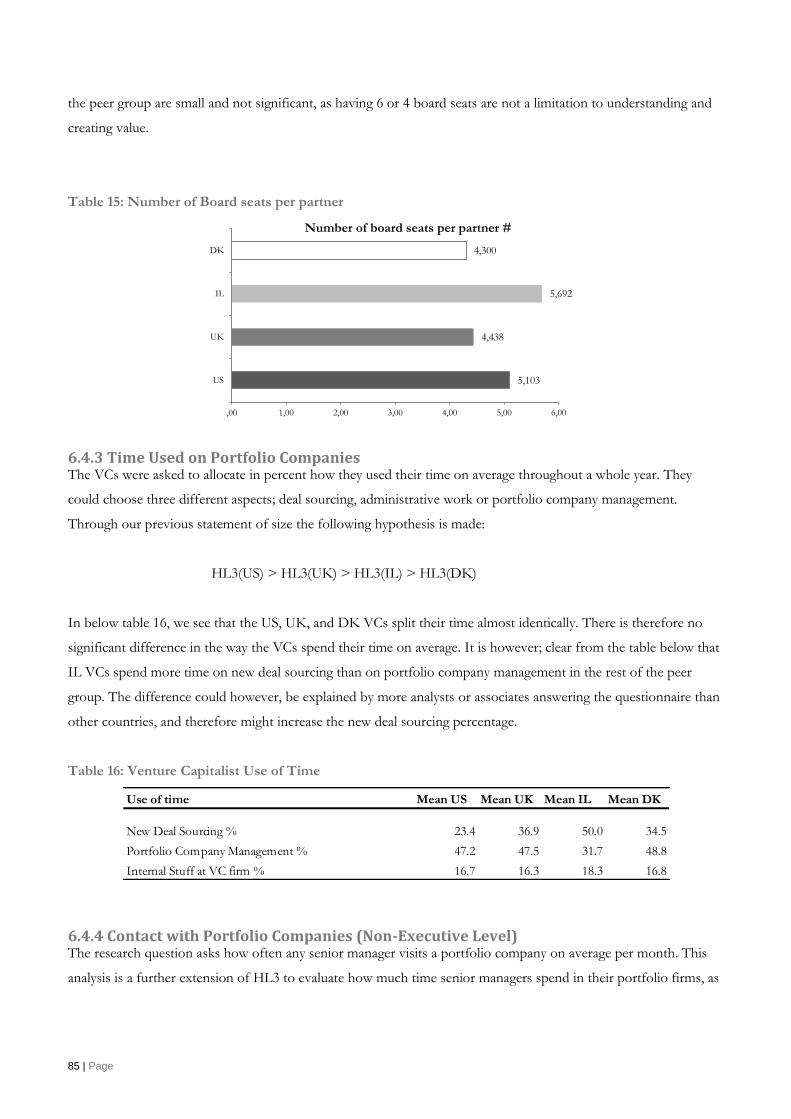

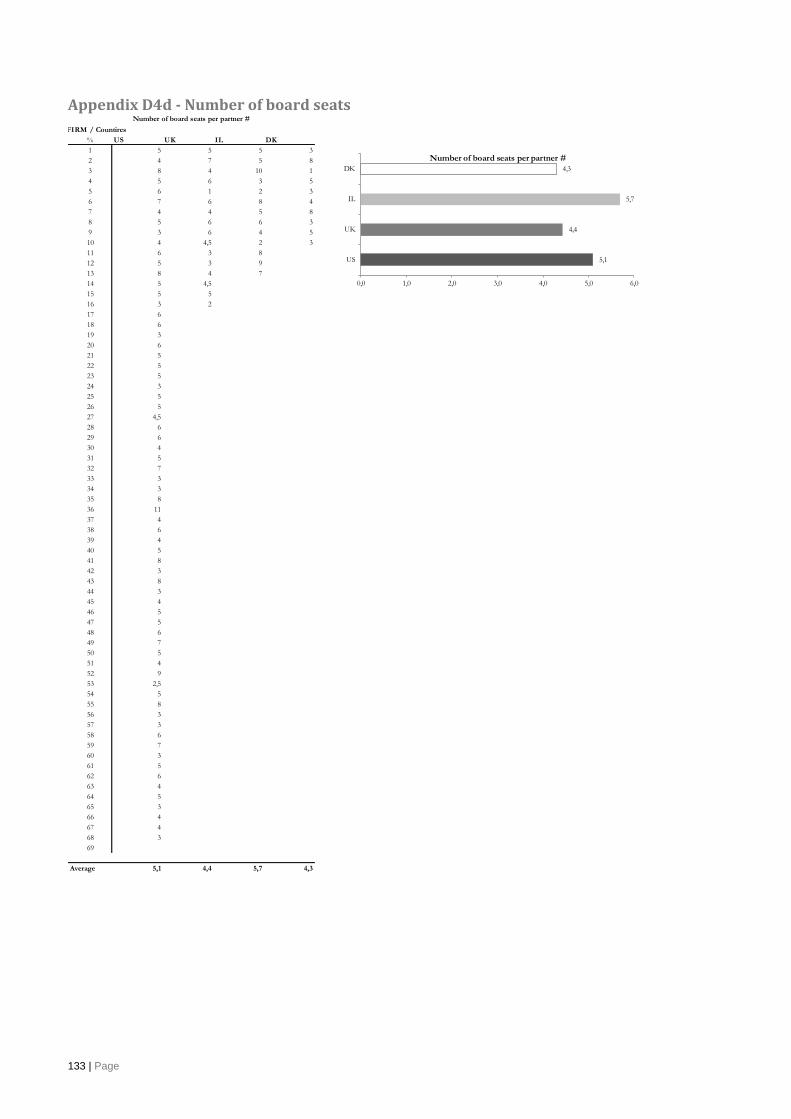

6.4.2 Number of board seats per partner ..................................................................................................... 84

6.4.3 Time Used on Portfolio Companies ................................................................................................... 85

6.4.4 Contact with Portfolio Companies (Non-Executive Level) ............................................................ 85

6.4.5 Conclusion: Differences in Value Adding Services ........................................................................... 86

6.5 Exit Phase........................................................................................................................................................................ 87

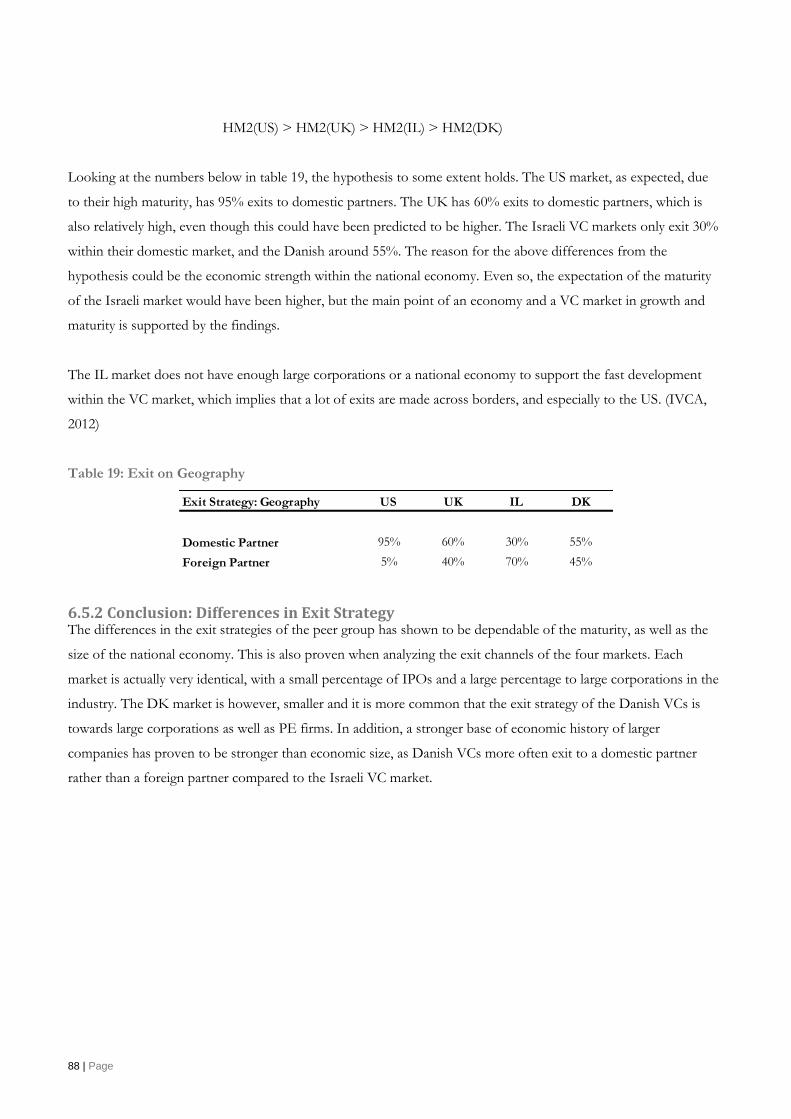

6.5.1 Exit Strategy: Channel and Geography ............................................................................................... 87

5 | Page

6.5.2 Conclusion: Differences in Exit Strategy ............................................................................................ 88

7. Discussion of the analysis and the impact on the impact on the innovation .................................................... 89

7.1. Investment Strategy, Risk Strategy, Due Diligence & Exit Phase (Spurring Innovation) .................... 89

7.2. Management Phase (Creating Sustainable Innovation) ................................................................................... 90

7.3. Concluding remarks on innovation differences ................................................................................................. 91

8. Conclusion .............................................................................................................................................................................. 92

8.1. Summary of the Results ............................................................................................................................................. 92

8.2. Concluding remarks: Implication of the differences and their impact on sustainable innovation .... 94

8.2. Limitation and critique ............................................................................................................................................... 94

8.3. Further Research .......................................................................................................................................................... 96

9. Bibliography ........................................................................................................................................................................... 97

10. Appendix ........................................................................................................................................................................... 106

6 | Page

Executive Summary The literature on venture capital and the finance of innovation is vast. Much of it focuses upon the existence and

extent of non-financial value added to new ventures, through active ownership also known from the private equity

industry.

This thesis develops a framework to identify cross-country differences within the investment strategies and value-

adding activities, and see if some of these differences could cause a better functioning venture capital industry.

Similar frameworks have often been used to investigate which activities add most value to ventures and also in

determining differences between different venture capitalists like private and public sector venture capitalists. The

framework developed in this thesis is founded in venture capital and innovation theory, which provides the insights

necessary to investigate how the venture capital approach can or cannot spur innovation, and hereby identify

perception perceptions of the value added from their venture capitalist and their network. The purpose of the

investigation is to uncover cross-country difference of how venture capitalists invest in Denmark, Israel, United

Kingdom and in the Unites States, and see if some of these differences can be traced back to whether some

countries have a better innovative eco-system than other countries.

The empirical data is mainly collected through a survey sent out to 60 venture firms, in Israel and Denmark, as well

as previous data points of 67 VCs in the United States and 15 in the United Kingdom. In addition, the hypothesis

development tested in this paper has been developed through 11 interviews of different venture capitalists,

entrepreneurs and business angels in Europe and the US.

Overall the research shows that the differences found between the four venture capital markets have limited

influence on the overall value adding services, and therefore there is no sufficient evidence that the U.S ventures are

capable of adding more value and should be copied into the European ventures' way of doing business. There are

however, significant differences in the way VCs invest in the four markets, and especially the DK market, which

seems more risk averse than the US, IL and UK venture markets and with a lower average amount of investment

throughout the lifecycle. Even though the above results are not conclusive, the research has clearly identified

differences between the four countries that could limit the innovative ideas and the development of healthy

ventures, and therefore create a less attractive ecosystem for startups.

7 | Page

1. Introduction Venture Capital refers to a specialized form of industrial finance that can be used to prove a business concept, help

set up a business or allow it to expand (Cumming D. , 2010). In the last century, venture capital has developed as an

important intermediary in financial markets, providing capital to firms that might otherwise have difficulties

locating capital towards expansion of their venture, such as biotechnology, IT, software, etc. In addition, venture

capital is often appealing for young companies with inadequate operating history that are too small to raise capital

in public markets and have yet to reach the point where they are able to obtain a bank loan or complete a debt

offering. The high risk that venture capitalists take on, by investing in smaller and less mature companies, venture

capitalists in exchange usually get significant control over company decisions, in addition to a significant portion of

the company's ownership (and consequently future value). (Privco, 2011)

The origins of the term "venture capital" are unknown, and there is no standard definition of it. It is, however,

generally agreed that the traditional venture capital era began in 1946, when General Georges Doriot, Ralph

Flanders, Karl Compton, Merrill Griswold, and others organized American Research & Development (AR&D), the

first (and, after it went public, for many years the only) public corporation specializing in investing in illiquid

securities of early stage issuers (Ante, 2008). In the 1960’s the US venture capital industry for technology firms got

consecrated when Silicon Valley laid the fundament for an inspiring environment for the information technology

industry to grow, whereas we today see London and Berlin as the new technology hubs of Europe, (Malik, 2011)

and (Johnson, 2012)

During the 1980’s and 1990’s, there was a tremendous boom in the American Venture Capital industry. The pool

of US venture funds – partnerships specializing in early stage equity or equity-linked investments in young or

growing firms – has grown from just over USD 1 billion in 1980 to about USD 29.4 billion in 2011. (NVCA, 2012)

Much of this growth seems to have bypassed Europe. European VC’s have long been overshadowed by the funds

specializing in buy-outs and other later-stage transactions: not only has the level of such activities been far lower

than elsewhere, but so have the returns. While there was a brief surge of European venture capital activity in the

late 1990s, it proved short lived and many of the new entrants collapsed early in the next decade. Many of the

policy initiatives of that era, such as the creation of the pan-European EAASDAW market for young growth

companies, and the First North market in the Nordic countries, have been written off as failures.

The European Venture Capital emerged about 20 years after the US emerged in the 1960’s in Boston,

Massachusetts investing in young technology firms. In the early 1980’s, the European Venture Capital invested

around 1/8 of the equivalent of their US counterparts. (Roure, Keeley, & van der Heyden, 1990) Furthermore, this

gap seems to be widening, especially within the information technology sector, proven with data from Jeng, Wright,

Mason, Sapienza, Friend and Manigart, that suggests that the rate of success of venture capital-backed startups in

Europe is far less than that of the U.S. (Jeng, 2000), (Wright, Robbie, Albrighton, Mason, & Harrison, 1998)

(Sapienza et al.; Burton), (Friend and Manigart) The scope and sophistication of the venture capital industry in the

US is one reason for the exceptional ability of the US to continually nurture new global and trailblazing information

8 | Page

technology gazelles, as well as other industries, such as Cleantech and Biotech. According to Jeng and Well, in

comparison to European venture capitalists, the propensity and frequency at which high growth information

technology start-ups which are developed by US venture capitalist are much higher.

Venture capitalists are today regarded as key actors in well-integrated innovation systems. (Cooke et al., 1997;

Florida and Kenney, 1988; Kenney, 2011; Powell et al., 2002; Samila and Sorenson, 2010) Persuaded by the belief

that venture capital firms are the ideal partners for financing corporate research and development, many OECD

governments have sought to promote innovation by channeling public funds to venture capital firms, securing

favorable fiscal and regulatory frameworks and directly mobilizing venture capital firms in support of small,

innovative firms. (EVCA, 2012; OECD, 1997)

To maximize the effectiveness of these policies it is important to understand exactly where in the product

development process venture capital firms (VCs) are most likely to enter (research or development) and how this

affects invention and contributes to create sustainable businesses that will grow with the economy. Theoretically

public agencies might find themselves in one of the following three scenarios:

- First, VCs might target their funding and managerial efforts both to research and development

- Second, VCs might focus only on ventures in the developed stage

- Third, VCs might focus exclusively on the commercialization of preexisting inventions, leaving both

research and development out of their boundaries

Denmark has frequently been seen as one of the biggest knowledge hubs, with a high educational level and an

entrepreneurial mindset, compared with similar Nordic and European countries (European Commision, 2012).

However, the Danish knowledge society has for many years been less superior when it comes to innovative

ventures and their success rate. Historic numbers show that the number of ventures who have succeeded has long

been overtaken by other Nordic and European counterparts, and so has the perceived number of discontinued

ventures (Zephyr, 2012). More so, there have been fewer successful tech firms in Denmark compared with other

European countries, and in many cases it has proven that “Danish” ventures in foreign countries have been more

successful. (TV2, 2012) Especially the US venture capital industry has carried out many successful startups, such as

Google, Instagram, Facebook, Etsy, Zoosk, Xirrus, etc. which and hereby helped innovative initiative to grow

within the US, and also creating economic value in the end, especially through job creation.

This research study deals specifically with the differences in the financing of start-ups within the technology

ecosystem in US, UK, Israel and Denmark. The study will map the difference between these countries and the end

discuss will focus on what could be done in the Danish Venture Capital Industry to make a better ecosystem for

innovative ideas in the future.

9 | Page

The thesis is structured as follows: The first three sections present the theoretical review on both innovation and

venture capital theory, which ends up in a theoretical discussion on the venture capital impact on innovation and

economic growth. In section four a short macroeconomic analysis is made on the four countries in the peer group,

which will be include in the hypotheses development. The fifth section gives an introduction on the research

framework and the hypotheses developments followed by a sixth section that analysis the above findings. A

discussion based on the previous section will be made based on what can be done within the Danish venture

Capital environment to enhance the spur of innovation within the tech industry. The paper will summarize with a

selection with a conclusion, limitation and further research based on the findings within this paper

1.2 Research Objective Differences in Venture Capital markets are well documented and argued for in various articles and papers, as well

as new stories on electronic platforms such as Techcrunch and Gigaom. (PWC, 2012), (Nesta, 2010) and

(Lindström, 2006) Differences on different continents, countries, regions and even cities have been enlighten the

last couple of decades (European Venture Capital, Financial Systems, Corporate Investment in innovation, and

Venture Capital), where the majority of the research projects have had the objective to show the differences from

an European and US perspective. This research acknowledges that there are differences on multiple levels within

venture capital and also internal differences within a country itself, such as, Boston to New York, London to

Birmingham and even Copenhagen to Aarhus. These differences, with some of them of notable significance, have

been neglected within this research paper and each country (UK, US, DK, IL) is seen as homogeneous clusters.

Therefore, the assumption of this empirical research study is:

There is a U.S. way of venture capital financing of startups, which is homogenous and there are

therefore no regional differences

There is a UK way of venture capital financing of startups, which is homogenous and there are

therefore no regional differences

There is a DK way of venture capital financing of startups, which is homogenous and there are

therefore no regional differences

There is a IL way of venture capital financing of startups, which is homogenous and there are

therefore no regional differences

With the above definition of the homogenous clusters per country in place, we therefore have a comparison of four

different countries. The study is both a descriptive, and a comparative analysis of each country and the goal is to

identify differences between the four countries, and hereby analyze the differences with an innovative perspective,

and identify some of the reasons why the US venture capital market has been and still is superior to the European

markets.

The differences are to be analyzed for the from the due-diligence phase until the exit phase within the venture

capital investment cycle: due diligence phase, investment stage, deal structuring and negotiation phase, management

10 | Page

phase – value adding services, and exit phase. The thesis will therefore not look into the differences in the contact

and investment criteria phase, but these phases will also be mentioned in short in the introduction to the venture

capital industry. In regard to the venture capital investment process, this empirical research aspire to answer the

following research question, propositions’ and phenomena:

What are the differences in the way US start-ups are financed with venture capital compared with the UK,

IL and DK way, and to what extent can these countries learn from the differences to help spur more

innovation within these countries?

More accurately, the thesis attempts to compare, highlight and answer the following questions:

Is the average size of investment in start-ups in the seed, start-up and growth stage in the US Post

Exchange rate adjustments larger than in UK, IL, and DK?

Is the risk strategy of the venture capital firms in the US more aggressive, and less risk averse than

in the UK, IL, and DK?

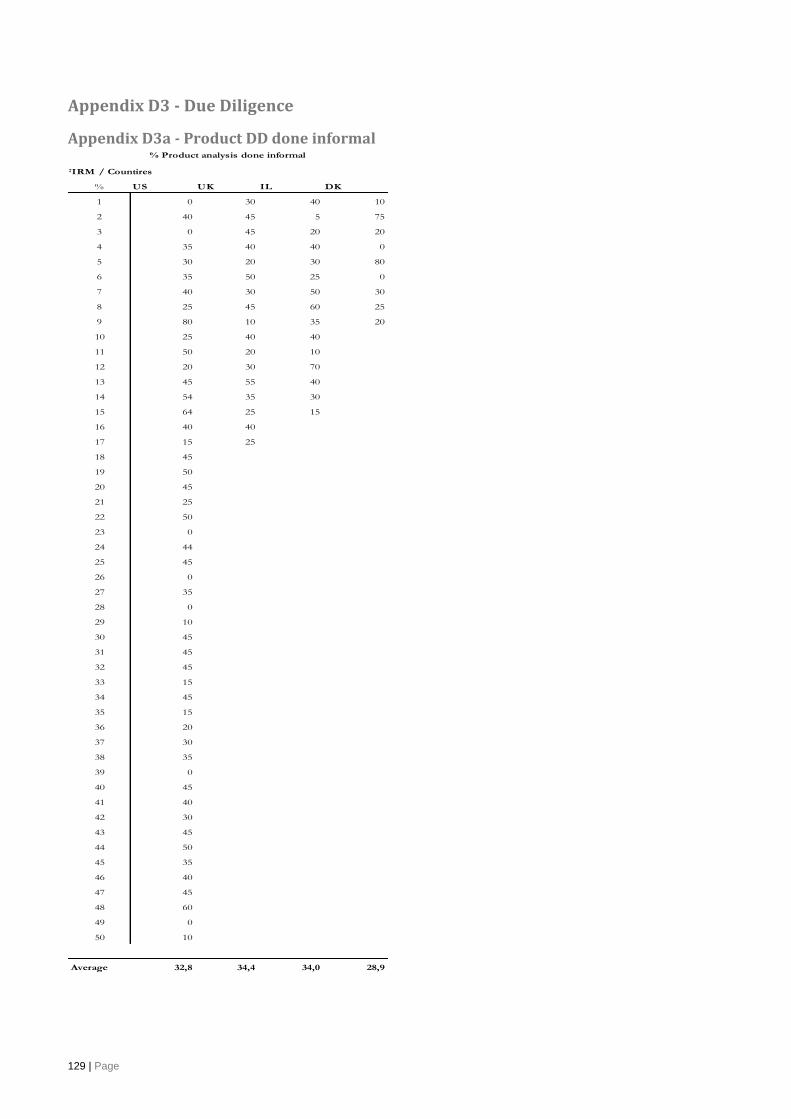

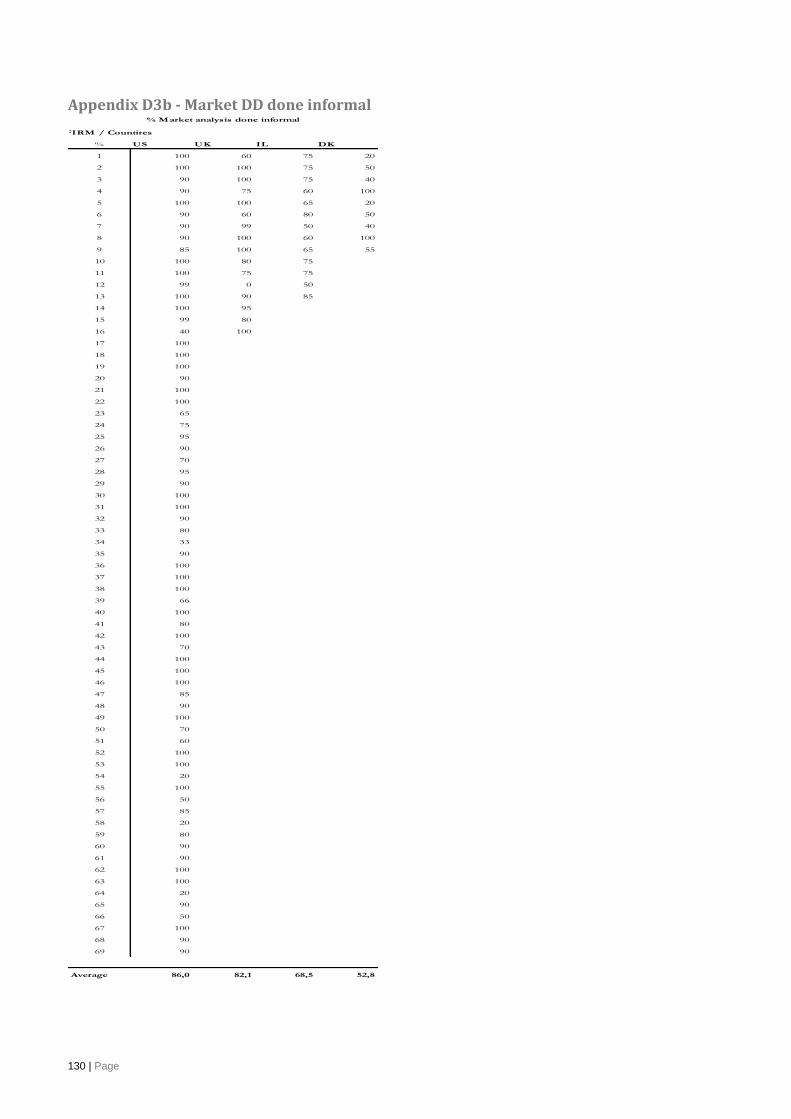

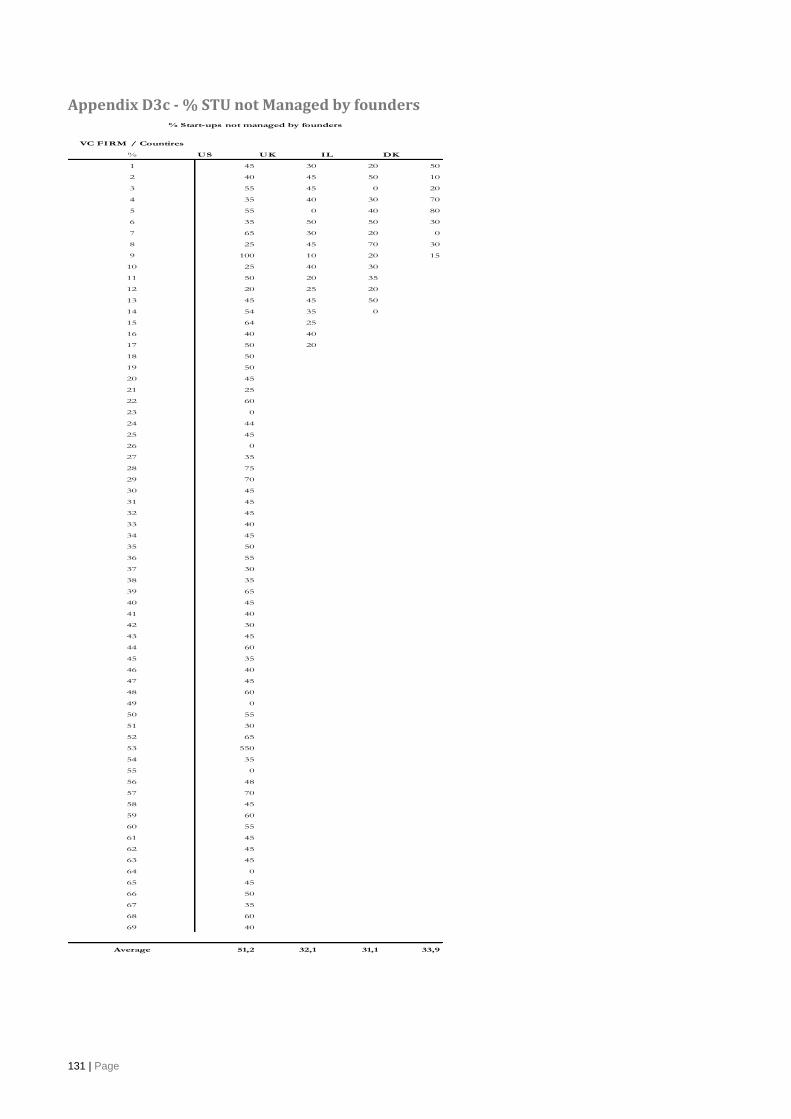

Is the percentage of due diligence (market, product, financial and team) analysis that is done

informal in the US bigger than in the UK, IL, and DK?

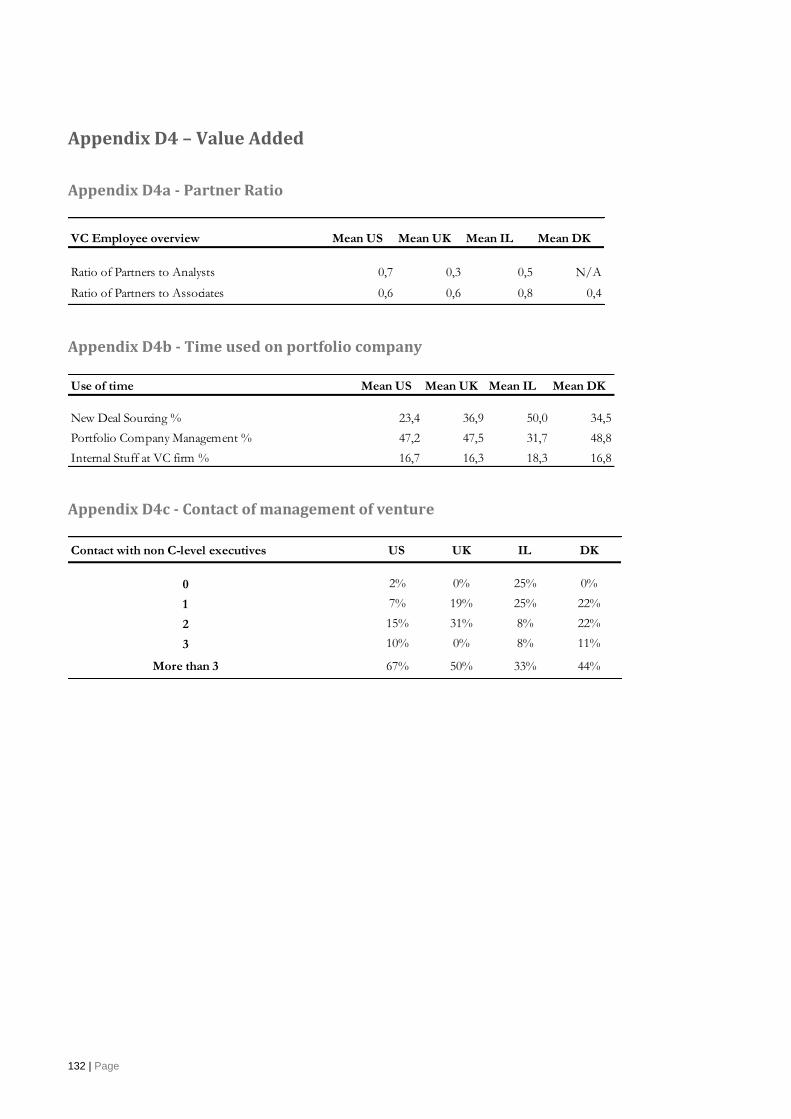

Do US venture capital firms add more value to their portfolio companies than their UK, IL and

DK counterparts?

Are the exit-channels different in the US compared with the UK, IL and DK counterparts?

This paper should be seen as an outline of the differences of the venture scenes in the United States, United

Kingdom, Israel and Denmark, with the purpose to show the main differences that spur innovation from a Venture

Capital perspective. In addition, the paper will manly take part in the microeconomic perspective, and only in short

discuss the macroeconomic take on the differences.

1.3 Research Method This thesis aims to answer the stated research question by employing three complementary research methods:

Literature review

Qualitative study

Quantitative study

First, the most relevant academic literature about venture capital, innovation and economic growth is reviewed. The

main focus is upon papers studying the differences in the venture capital financing in different countries, as well as

how venture capital spurs innovation. The purpose of the literature study is to give an overall picture of the

academic research in the domain of the research question and to obtain a theoretical framework on which the

empirical part of the thesis can be built. The literature review is also utilized to identify the best and most recent

11 | Page

methods for the quantitative part of this thesis. In addition, the empirical review of the literature within the topic of

Venture Capital to spur innovation looks to show that a better Venture Capital industry within an economy will

spur the national innovation and therefore create economic growth. The reviewed materials include articles in

scientific journals, textbooks, publications from venture capital industry associations, and other academic materials.

The empirical part of this thesis starts with an interview study based on 11 interviews with business angels,

entrepreneurs, venture fund managers, and other industry experts, from the UK, IL and DK. The objective of

these interviews where to obtain a better understanding of how venture capital companies are managed, what kind

of criteria they use in their investment decisions, and how they interact with their portfolio companies. This also

offers us an idea of what entrepreneurs and business angels see as the biggest challenges and differences between

the different countries. By interviewing experts in the field of venture capital, it is possible to ensure that all relevant

theories and hypotheses for the determinants of venture capital returns have been identified in the literature review

part of this thesis. Otherwise, there would be a risk that the academic literature on the subject has not identified all

relevant performance determinants. This might be true since, there are currently surprisingly few academic papers

concentrating purely on venture capital and its connection with innovation. The literature reviews, as well as the

qualitative study, have helped to develop the hypotheses in the thesis, which is to be analyzed from the quantitative

date study.

The most important part of this thesis is the quantitative study, which aims to analyze the differences in the

approach of the venture capital funds in different regions of the world. The findings and insights from the previous

research methods are used as inputs in the form of hypotheses development and therefore the groundwork for the

analysis. The objective of the analysis is to explain, at least partially, the observed differences between the four

different countries and their way of investing within young ventures, by finding statistically significant explanatory

variables. The research study employs secondary data collected from previous research for data on the US and UK

venture capitalist, as well new data collected from a question guide similar to the one used in the afore-mentioned

data research for the DK and IL venture capitalist. The quantitative study is done through 69 data points from the

US, 17 in the UK, 19 in the IL and 11 in DK. The collected data is in some cases analyzed statistically using

econometric methods, and some is compared by a simple average mean.

After the main differences have been identified, the study aims to give some practical suggestions on further

research in order to improve the Danish venture capital scene, given the findings in the US, UK and IL venture

capital markets.

12 | Page

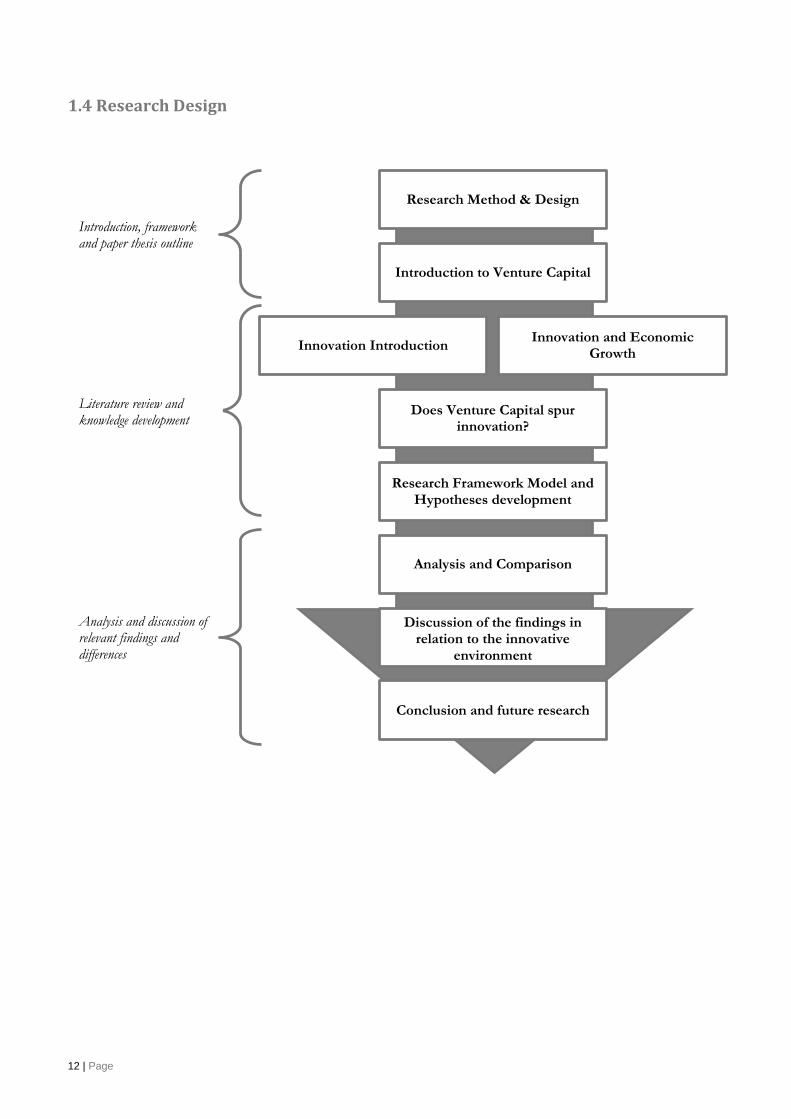

1.4 Research Design

Research Method & Design

Introduction to Venture Capital

Does Venture Capital spur innovation?

Introduction, framework and paper thesis outline

Literature review and knowledge development

Analysis and discussion of relevant findings and differences

Research Framework Model and Hypotheses development

Analysis and Comparison

Discussion of the findings in relation to the innovative

environment

Conclusion and future research

Innovation and Economic Growth

Innovation Introduction

13 | Page

2. Introduction: Venture Capital Financing of Start-Ups in Business Administration Theory

2.1 Definition of Venture Capital Though Venture Capital has been a term used extensively, “venture capital” has yet to be defined in business

literature, thus several researchers in the field have come up with their own definition: Venture capital is a segment

of the private equity industry, which focuses on investing in nascent young firms with high growth rates, and large

market potential (Haeming, 2003). Private equity includes all equity invested in corporations that are not listed on

stock exchanges, whereas venture capital is a private or institutional investment limited to relatively early-stage

companies (Arundale, 2007).

Many people have given their own definition of what venture capital is; common between them all is that they see

private capital invested in young risky assets, often very early in the business cycle of a start-up. In the next section

some basic terms within venture capital will be introduced, which are important for understanding the purpose and

the background of the main problem in this paper.

2.2 Equity Financing: Venture Capital Financing A start-up or innovation requires capital during the formation of the idea. One of the main problems many start-

ups have realized today in the process of starting a new venture/innovation is raising capital. Within the idea

generation (innovation process) start-ups need capital to finance cash flow needs long before demand and revenue

materialize. (Sherman, 2005) Typical characteristics of the financial needs of start-ups can be described as following:

Start-ups often have little history and thus possess no fundamental customer base and financial data, which

would make it difficult to create a reliable financial valuation

Start-ups are often considered by a high level of uncertainty and risk both internally and externally -

management team risk, product development risk, market risk, and exit risk

Start-ups are more likely to seize up in the market compared with established businesses are

They often do business in dynamic and perpetually evolving markets with extensive growth rates, such as

IT, BIO, Pharma, Cleantech, etc.

They often have a negative cash flow the first couple of years and are not expected to make any profits in

the forthcoming years

Business decisions are predominantly made by founders with industry knowledge but lack of management

and established business administration

The start-up is provided equity funding by early stage investors, such as venture capitalist and business

angels, who in return obtain equity share, voting and control rights

Start-ups often have a strong technology orientation

14 | Page

With no or limited operating history, missing hard-knock financial data and no collaterals, start-ups cannot raise

funds by taking loans or issuing debt securities – at least not at any favorable interest rates. Therefore, start-ups

often rely mainly on equity capital in financing entrepreneurial venture or through crowd funding.

As a result, venture capitalist and other early stage investors, make the decision whether to fund a project often

based on the perceived strength of an idea, capabilities, scalability, originality, skills and quality of the management

team. Venture capital have often been the preferred financing path for many start-ups due to the reason that start-

ups have no or limited access to debt financing.

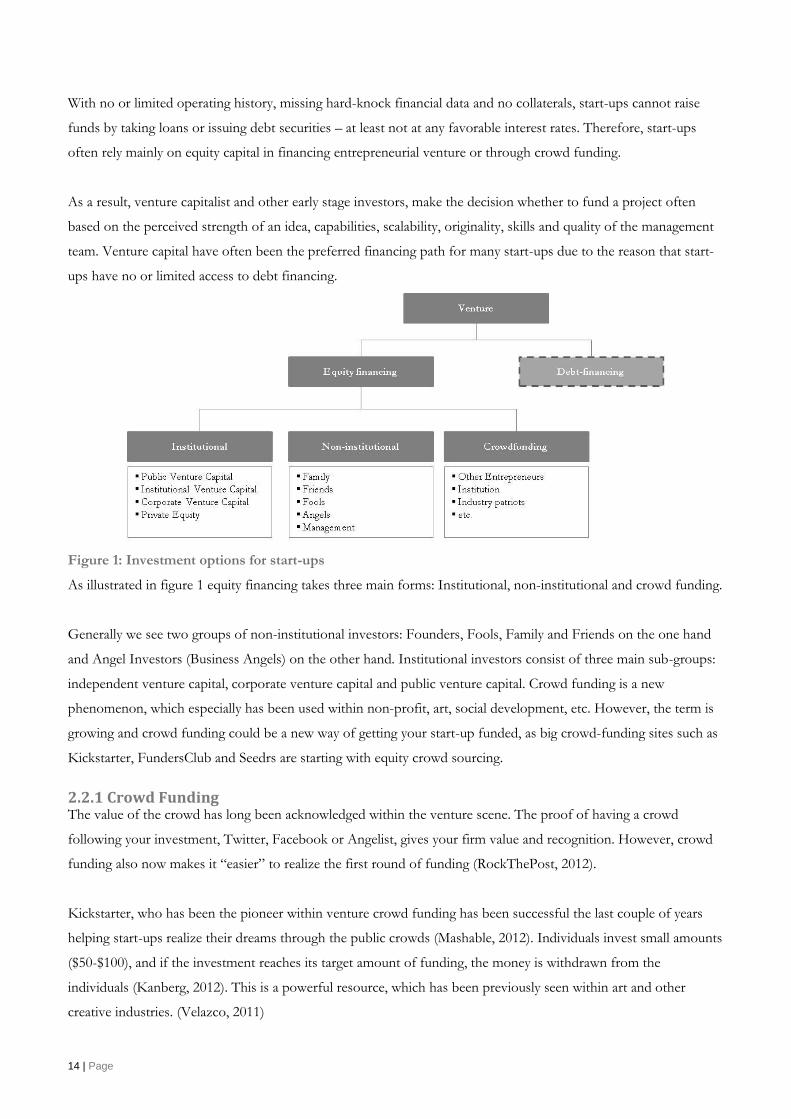

Figure 1: Investment options for start-ups

As illustrated in figure 1 equity financing takes three main forms: Institutional, non-institutional and crowd funding.

Generally we see two groups of non-institutional investors: Founders, Fools, Family and Friends on the one hand

and Angel Investors (Business Angels) on the other hand. Institutional investors consist of three main sub-groups:

independent venture capital, corporate venture capital and public venture capital. Crowd funding is a new

phenomenon, which especially has been used within non-profit, art, social development, etc. However, the term is

growing and crowd funding could be a new way of getting your start-up funded, as big crowd-funding sites such as

Kickstarter, FundersClub and Seedrs are starting with equity crowd sourcing.

2.2.1 Crowd Funding The value of the crowd has long been acknowledged within the venture scene. The proof of having a crowd

following your investment, Twitter, Facebook or Angelist, gives your firm value and recognition. However, crowd

funding also now makes it “easier” to realize the first round of funding (RockThePost, 2012).

Kickstarter, who has been the pioneer within venture crowd funding has been successful the last couple of years

helping start-ups realize their dreams through the public crowds (Mashable, 2012). Individuals invest small amounts

($50-$100), and if the investment reaches its target amount of funding, the money is withdrawn from the

individuals (Kanberg, 2012). This is a powerful resource, which has been previously seen within art and other

creative industries. (Velazco, 2011)

15 | Page

Today there are several crowd funding sites as Kickstarter, GrowVC, Fundrs, RockThe Post, Seedups, RocketHub,

FoundersClub etc. Crowd funding platforms have already revolutionized the funding of new ventures. However,

the management of all the new shareholders is a new issue raised by many experts. People who have either donated

or invested in your firm all have the right to be informed in decision making as other shareholders, which can bear

costs on the firm such as limiting the innovativeness of the ventures. Research on this field is still to be carried out,

and the results are going to be interesting. In addition, the value adding aspect of expert and knowledge of the

market will often not be part of the equity financing, within crowd funding.

Even so, crowd funding could be a new aspect of Venture Capital, and engage more start-ups and maybe even spur

innovation even more. However, this paper is not focused on crowd funding, and its importance for the future of

venture capital, even though it might have some important aspects. In addition, the aspect of comparing different

nations’ innovative process is limited as the crowd sourcing is global and therefore all start-ups are given the same

opportunity to become successful.

2.2.2 Institutional Venture Capital “Institutional Venture Capital” used as a term can be traced back to the year 1946. General Georges Doriot, Ralph

Flanders, Karl Compton, Merrill Griswold, and other angel investors with interest in investing in start-ups or other

early stage actives, established the first institutional venture capital firm “American Research & Development” in

Boston. (Bygrave & Timmons, 1986) In recent years, Haeming defines institutional venture capital as equity or

equity-linked investment in young companies, where the investor is a financial intermediary, who typically acts as an

active director or advisor in the young company. (Haeming, 2003)

National Venture Capital Association (NVCA) defines institutional venture capital as private, corporate or public

funds that focus on investments in early stage technology companies. (NVCA, 2012) Institutional venture capital

firms are financial intermediaries, who specialize in raising funds from private, corporate or public sources and

investing it in young innovative technology companies with high risk and growth potential. (Bygrave & Timmons,

1986)

Institutional investors often invest when the start-up has established some kind of “proof-of-concept”, and thereby

lower the risk of the investment significantly. As a result, institutional venture capitalists invest in start-ups after

they have been funded with non-institutional venture capital or crowd funding scenarios. In contrast to the latter,

institutional venture capitalists are very formal, highly professional and do not invest their own funds. They are

fund-managers who are employed to invest and manage custodial money, i.e. funds from third parties such as

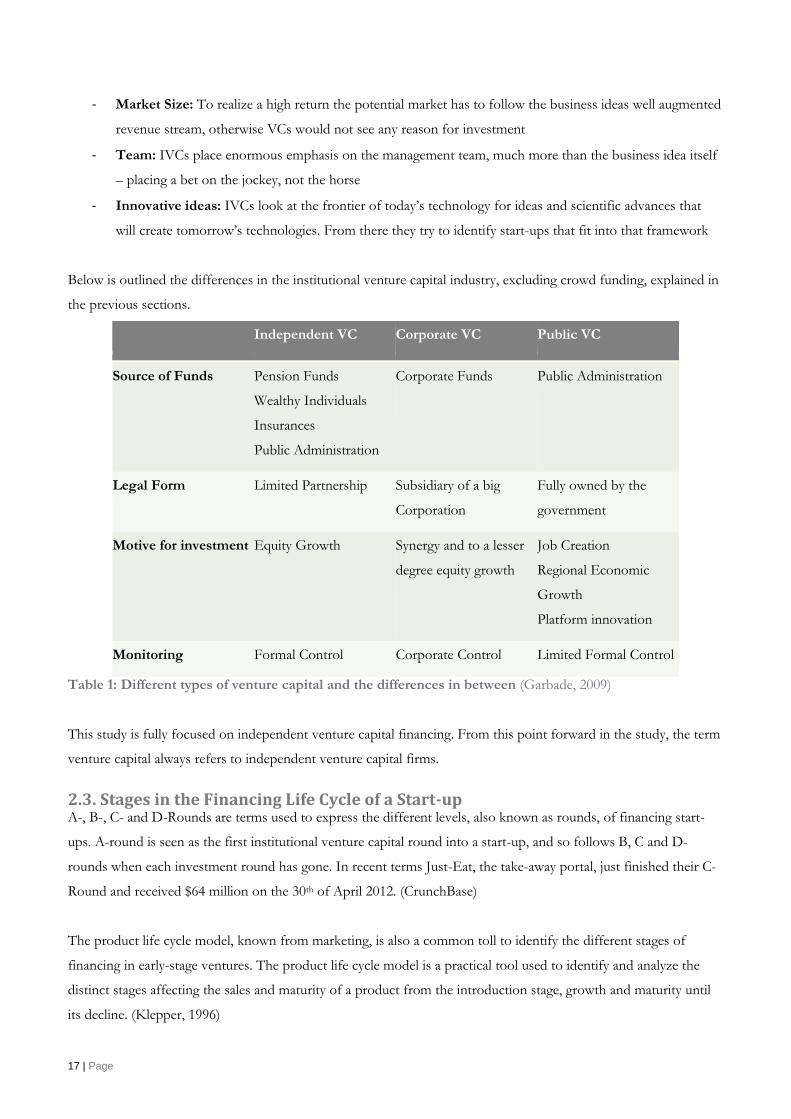

wealthy individuals, banks, insurance, university endowments, and pension funds. As depicted in fig 2.2, there are

three main types of institutional venture capital: corporate venture capital public venture capital and independent

venture capital. The source of funds, investment objectives, organizational structure, investment behavior, range of

16 | Page

non-financial value – added services and legal forms vary across all three types of institutional venture capital firms.

(Landström, 2007)

The most common way of financing start-ups around the world is still venture capital financing. Even though

crowd funding seems to be very popular, especially in the US, crowd funding is only a small amount of the total

invested capital in start-ups (CrunchBase). This thesis will therefore continue to look at independent venture

capital, which is often referred to as “traditional capital” and also seen as the majority of capital for start-ups in the

countries of DK, UK, IS and US (Lumme, Mason, & Suomi, 1998)

2.2.3 Independent Venture Capital (IVC)

2.2.3.1 Definition and Characteristics of IVC Financing IVCs are neither a subsidiary of a corporation nor do they exist to fulfill government economic policy tasks, but act

as stand-alone venture capital firms. They are normally representative of a small team of administration and

industry experts and therefore also flexible, which allows them to make quick decisions. Furthermore, IVCs are

often set up as limited partnerships in which the venture capital manager is the general partner who invests money

contributed by limited partners. Consequently, IVCs have large investment capacities and monitor start-ups

through formal control. (Nesta, 2010)

IVCs do not invest the whole amount that they raise into start-ups. Often there is a management fee of 1-3% of the

capital raised, to cover up the overhead costs of running a venture capital firm over the life of the fund. For

example, if the IVC raises 800 MDKK of a fund over 10 years, with a 2% management fee, the IVC charges 2% of

the 800 MDKK every year, which amounts to 160 MDKK (20% of 800 MDKK) over the life of the fund.

Therefore the total amount invested would only be 80% of the total amount raised. (Sbietiati, 2012) (VCIC DK,

2012)

Some cases of IVC have a management fee for the total amount raised and thereafter the management fee changes

for the percentage of the total amount invested. Often you see more deals in the end of a fund, since this will affect

the wage of the management in the IVC in active period of the fund. (Sbietiati, 2012) (VCIC DK, 2012)

In addition, if an IVC at the end of the life of a venture capital fund returns more money to limited partners than it

raised, the IVC receives a percentage of the profit. This part of the profit allocated to an IVC is called carried

interest (carry). Carried interest ranges from 20-30% of capital gain in the VC industry. (Sbietiati, 2012) (VCIC DK,

2012)

IVC have some certain criteria they look at before investing: (VCIC DK, 2012)

- High Return (Potential Revenue): IVCs are focused purely on financial gains and making big exits

17 | Page

- Market Size: To realize a high return the potential market has to follow the business ideas well augmented

revenue stream, otherwise VCs would not see any reason for investment

- Team: IVCs place enormous emphasis on the management team, much more than the business idea itself

– placing a bet on the jockey, not the horse

- Innovative ideas: IVCs look at the frontier of today’s technology for ideas and scientific advances that

will create tomorrow’s technologies. From there they try to identify start-ups that fit into that framework

Below is outlined the differences in the institutional venture capital industry, excluding crowd funding, explained in

the previous sections.

Independent VC Corporate VC Public VC

Source of Funds Pension Funds

Wealthy Individuals

Insurances

Public Administration

Corporate Funds Public Administration

Legal Form Limited Partnership Subsidiary of a big

Corporation

Fully owned by the

government

Motive for investment Equity Growth Synergy and to a lesser

degree equity growth

Job Creation

Regional Economic

Growth

Platform innovation

Monitoring Formal Control Corporate Control Limited Formal Control

Table 1: Different types of venture capital and the differences in between (Garbade, 2009)

This study is fully focused on independent venture capital financing. From this point forward in the study, the term

venture capital always refers to independent venture capital firms.

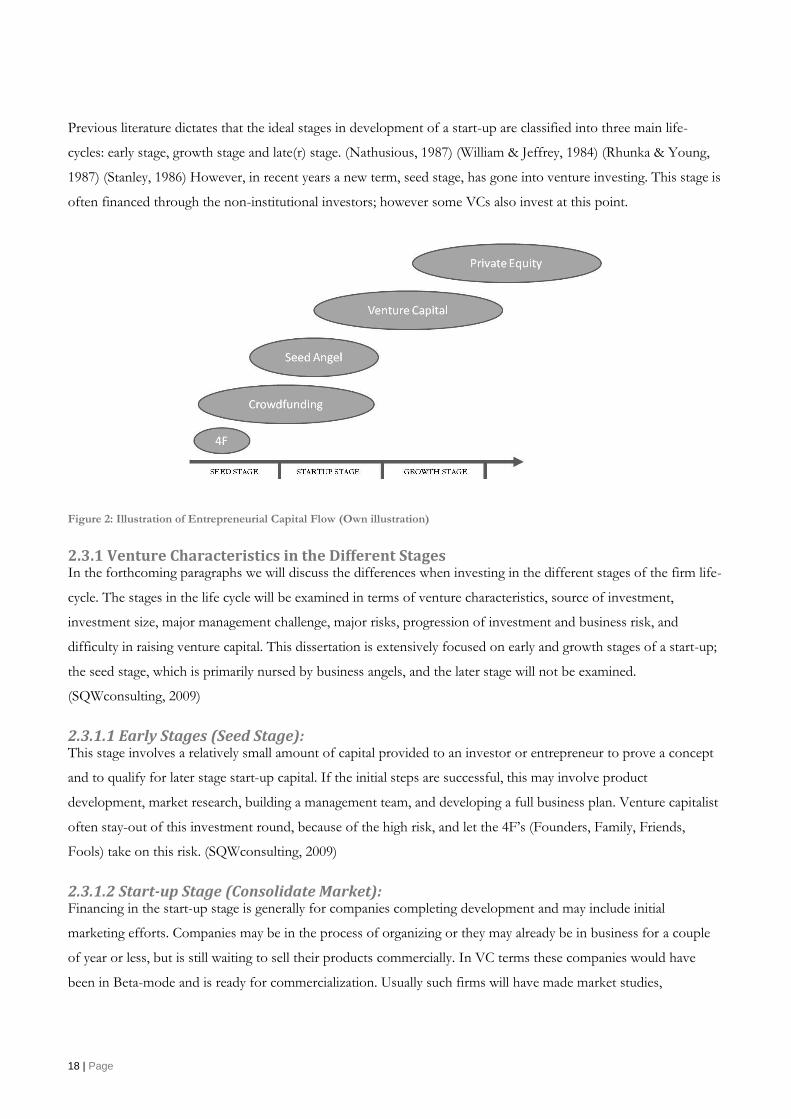

2.3. Stages in the Financing Life Cycle of a Start-up A-, B-, C- and D-Rounds are terms used to express the different levels, also known as rounds, of financing start-

ups. A-round is seen as the first institutional venture capital round into a start-up, and so follows B, C and D-

rounds when each investment round has gone. In recent terms Just-Eat, the take-away portal, just finished their C-

Round and received $64 million on the 30th of April 2012. (CrunchBase)

The product life cycle model, known from marketing, is also a common toll to identify the different stages of

financing in early-stage ventures. The product life cycle model is a practical tool used to identify and analyze the

distinct stages affecting the sales and maturity of a product from the introduction stage, growth and maturity until

its decline. (Klepper, 1996)

18 | Page

Previous literature dictates that the ideal stages in development of a start-up are classified into three main life-

cycles: early stage, growth stage and late(r) stage. (Nathusious, 1987) (William & Jeffrey, 1984) (Rhunka & Young,

1987) (Stanley, 1986) However, in recent years a new term, seed stage, has gone into venture investing. This stage is

often financed through the non-institutional investors; however some VCs also invest at this point.

Figure 2: Illustration of Entrepreneurial Capital Flow (Own illustration)

2.3.1 Venture Characteristics in the Different Stages In the forthcoming paragraphs we will discuss the differences when investing in the different stages of the firm life-

cycle. The stages in the life cycle will be examined in terms of venture characteristics, source of investment,

investment size, major management challenge, major risks, progression of investment and business risk, and

difficulty in raising venture capital. This dissertation is extensively focused on early and growth stages of a start-up;

the seed stage, which is primarily nursed by business angels, and the later stage will not be examined.

(SQWconsulting, 2009)

2.3.1.1 Early Stages (Seed Stage): This stage involves a relatively small amount of capital provided to an investor or entrepreneur to prove a concept

and to qualify for later stage start-up capital. If the initial steps are successful, this may involve product

development, market research, building a management team, and developing a full business plan. Venture capitalist

often stay-out of this investment round, because of the high risk, and let the 4F’s (Founders, Family, Friends,

Fools) take on this risk. (SQWconsulting, 2009)

2.3.1.2 Start-up Stage (Consolidate Market): Financing in the start-up stage is generally for companies completing development and may include initial

marketing efforts. Companies may be in the process of organizing or they may already be in business for a couple

of year or less, but is still waiting to sell their products commercially. In VC terms these companies would have

been in Beta-mode and is ready for commercialization. Usually such firms will have made market studies,

19 | Page

assembled the key management, and developed a business plan – and are now ready to conduct business.

(SQWconsulting, 2009)

Furthermore, financing in the later phase of the start-up stage could also increase the valuation, total size and the

share price for companies whose products are either in development or are commercially available. Due to the stage

of the venture and the outlook to commercialize the products in the near future, this round of financing, would

often be the first sign of engagement of a venture capital fund. Seed and early start-up financing tend to involve

angel investors more than institutional investors. The networking capabilities of the venture capitalists are used

more here than in the more advanced stages. (SQWconsulting, 2009)

2.3.1.3 Growth Stage (Expansion Stages) This stage is mainly focused on applying working capital to the initial expansion of a company. The company is

now producing, shipping, and have growing accounts receivables and inventories. It may or may not be showing a

profit. Some of the usage of capital may include further plant expansion, marketing, or development of an

improved product. Other institutional investor is likely to be included along with initial investors from previous

rounds. The venture capital’s role in this stage involves a switch from a supporting role to a more strategic role.

(Metrick, 2006) and (SQWconsulting, 2009)

Throughout these stages several management challenges and risks are essential to overcome, before any success can

be achieved.

2.3.2 Structure of Independent Venture Capital Firms VCs are becoming more and more specialized, both within industry focus and investment stage. Thomas Knudsen

from NorthCap Partners states that VCs typically specialize by focusing on a particular stage of the business

lifecycle. (Knudsen, 2012) Looking further into the business cycle VCs can be assessed within two main criterion:

Stage of investment

Investment horizon

Based on Figure 2 of the capital flow of investment, VCs often invest in the Start-up and Growth Stage of the

development of the firm. There are however also venture capital firms that specialize in investing and managing

start-ups in the seed. These are VCs whose funds are not very big, but who invest a lot of time and huge personal

management resources in the start-ups they invest in.

Many venture capital firms fall into the class of growth venture capital. This is normally the ideal stage, where

venture capital firms can add maximum value, namely assisting a start-up strategically and operationally to expand

in their home markets and expand into new (international) markets. Even so, there are VCs who invest in all of the

above stages, because of their internal portfolio companies and external network, to help and improve the chance

of success of the start-up.

20 | Page

Depending on the prospect of the investment, VCs tend to have a long horizon to build up a strong business case

and make the start-up profitable. Of course, the horizon depends on the time of investment (what stage), which has

been clarified above. Many VCs plan to exit within 5-7 years, as the firm should have proven to take a certain

market share in that time. One thing to keep in mind is that the start-ups that VCs invest in should be highly

growth orientated and therefore also expand rapidly into new markets.

2.3.3 Role of Independent Venture Capital Firms in Start-ups The role of VCs in start-ups is focused upon the specific added-value that VCs add in each stage of the lifecycle.

This paper discusses this by looking at how VCs support and create success for the different start-ups, and thereby

create more value and improve the rate of success in each stage. The thesis will only look at the early stage up until

the growth stage, and the later stage is therefore completely excluded in this research.

“Venture capital is more than money – venture capitalists bring valued added” – this phrase is what many sees as

the big difference, compared to bank loans and other debt orientated loans. (Kølendorf P. , 2012) Today many

recognize this term as smart-money. Whereas, dumb money is simply money where capital is the only value added.

Haeming portends that it is important to draw upfront a distinction between founders and entrepreneurs; a founder

has a lot of analytical skills but little or no idea about the market, whereas an entrepreneur is a person with

knowledge in all aspects of technology, market, finance, and people skills. (Haeming, 2003) VCs are often well

suited to fulfill these gaps of start-up founders. They have money and expertise in commercializing business

models. VCs have good access to capital, are endowed with managerial experience and often have comprehensive

knowledge of the targeted industry, and count on a well-developed network of suppliers, customers and key

personnel. Seppa and Hsu even displayed in empirical research that entrepreneurs are willing to accept lower

valuations and face higher dilution, only due to the expectation that VCs will contribute more to the future value of

their venture. (Seppa, 2002) (Hsu, 2004)

All the professional assistance that VCs deliver to start-ups can be categorized into social capital and human capital.

Human capital refers to managerial and entrepreneurial experience, whereby social capital relates to professional

contact networks that VCs provide, through their long experience within the market. This paper's research did not

uncover a specific list of what value added services VCs provide, however through interviews and readings on the

topic we have listed the following as the most important features of a VC in terms of added value:

Monitor – VCs monitor start-ups through their voting and control rights. They act as strategic generators

of sound board members for strategic initiatives

Advisor – VCs role as an advisor/consultant is probably one of the most value-adding services to new

entrepreneurs/founders. The VCs have had an enormous experience within the industry and knows what

to do in certain cases; this will often mean that the VC will succeed instead of fail. Services could be:

21 | Page

Proactively consulting in important decisions, helping executing strategies, operational issued internal

disputes, financial management, marketing, public relations, etc.

Interim Manager – In certain situations (often in the seed-stage), VCs take the role of interim managers

carrying out day-to-day operational activities. VCs helps on executing ideas and tasks, which the current

management will or could not achieve

Contact Networker – On the same page as the advisor role, the VC network is one of the most valuable.

Young entrepreneurs often lack a strong business network, due to their limited time in the “market”.

(Kølendorf P. , 2012) VCs fill this void by making strategic introduction of start-ups to the extensive

networks they have cultivated over a long period of time: customer introduction, portfolio company

introduction, strategic alliances within the VC industry, etc.

Motivator – VCs automatically take the role of mentor and motivator of the entrepreneurial teams they

invest in. They teach young founders and inspire them to work harder and goal-orientated in making the

start-up a success

Proof-of-Concept (Reputation) – Often start-ups get a “boost-of-confidence” and recognition within

the industry, when they get backed by a VC. This proves that the start-up has gotten through the “keyhole”

and that your idea has a high potential (Watzenig, 2012)

Portfolio alliances – Portfolio alliances is also seen within Private Equity. VC has many portfolio firms,

and the potential of becoming customers and partners in-between are high. Therefore, start-ups can realize

a set of new customers from which they can learn from in both the alpha and beta stages.

In the growth stage the role of the VC is more on acting as monitors, operate as directors on the board, and having

an outside-in overview of the whole development of a start-up and advising on important legal agreements and

contracts. (Broomfield, 2005) In this phase VCs help in reshaping the start-up in building a professional

organizational structure as it grows. Within this stage, changing the management team could be necessary, since the

one who founded and made the company grow, is probably not the right individual to ensure that the start-up is a

success in the next phase. VCs therefore also helps hiring people with experience within the industry and stage of

the start-up.

Start-ups that are backed by top-tier VCs can cherry pick their local alliance partners because of the name

association with coveted VC firms. In the role of a mentor in the growth phase, VCs are the entrepreneur’s

confidants with whom founders share their personal entrepreneurial problems and thoughts.

2.4 Theoretical Foundation for Explanation of the Behavior of Venture Capital Firms Start-ups and VCs tie their specific knowledge, capabilities and resources together to build a start-up that, with

these combined aspects, will have an increased chance of success. In this relationship, the VC signs contracts with

the start-up and hereafter delegates the mandate to manage the employees and the daily operation to the founders.

22 | Page

Typically in such a deal, the start-up brings the business idea, product and the people to the negotiation table,

whereas the VC often brings capital and value-adding-services, explained earlier in this section.

VCs attain a large influence in the start-up, when buying the equity of the founders and the founders are in fear of

losing control over the firm. Hence, problematic issues and conflicts can arise, when the founders of the start-up

and the VC have diverging interests and goals. The relationship between the founders of the start-up and the VC

are complex. On the one hand they have engaged in a marriage often up to a decade long, and on the other hand

the VC needs to govern the founders, and make sure that the start-up is developing as expected. The founders

could become free-riders coasting on the investment of the VC, and seek other opportunities. Agency risk is a

significant hurdle to overcome for VCs and relies on good due diligence work and people skills.

2.4.1 Agency Theory Model: Asymmetric Information, Moral Hazard and Adverse Selection An agency relationship is a relationship in which one party (principal) delegates work to another party (the agent) to

perform a job as defined in a contract. (Eisenhardt, 1989) Looking at the VC/founders conflict with an agency

theory perspective of Eisenhardt, the VCs take the role as the principal and founders takes the role as the agent.

Because the contract of the VCs and the founders is not contractually well defined, the founders of the funded

start-up could act/behave reluctantly towards the VCs. The two most important appearances of agency risk within

early venture financing are information asymmetries and goal incongruences. Cable and Shane define information

asymmetry as all the hidden (private) information that a founder or VC holds which is not necessarily readily

available to the other transaction partner. Research has in addition shown that there is a perception from founders

that the relationship with BAs (Business Angels) is better than the one they meet within VCs. (Fairchild, 2011)

Through interviews and talks with both BAs and VCs they more or less all identified three main information

asymmetry aspects: Capabilities, Intention, and Actions:

Capabilities is often an aspect which VCs try to limit through thorough research in the due diligence

session. However, it is difficult to see if the founders have the characteristics and capabilities’ to make this

venture a success

Intention is also difficult to measure. VCs will not know the founders real intention with their venture

before they have worked together in a couple of months/years. Furthermore, this information asymmetric

goes both ways. VCs will also see their knowledge and intention hidden for the founders of the firm.

Actions (moral hazard) of the founders can lead to huge successes or dramatic losses from one day to

another. VCs will have a hard time governing and controlling founders on a daily basis, Founders of the

start-up will therefore have the space and opportunity to act against the strategy which the VCs have set

for the venture.

23 | Page

Both the VCs and founders need to limit the asymmetry of information to engage in a healthy relationship and

make the best of their future work. If the goals of the VC and the founders are aligned, all actions by the founders

will lead to a concomitant maximization of the utility of the principal and agent. Both parties therefore have some

basic tools to limit this asymmetry, which will be discussed in the next section of agency risk.

2.4.2 Mitigation of Agency Risk The more the interest of the VC and the founders are aligned, the higher the likelihood of cooperation in-between

the VC and the founders on a long-term, which will without a doubt increase the chances of a successful venture.

In mitigating agency risk, the following specific mechanisms and contractual provisions, which align the interests of

both transaction partners, can be deployed. (Kaplan, 2003)

1) Screening of founders and investment opportunity is the most important factor of limiting or mitigating

agency risk within a given investment opportunity. The ability to attract and screen the right people and

business plans is a difficult task, and the ability of recognizing untruthful founders is generated through

experience rather than haven a certain checklist etc. (Rasmussen, 2012)

2) “Hand-on-the-hob” is also a great way to make sure that both parties need to perform and create value.

Witteloostuijin argues that having a substantial stake of ownership in a firm, team members may have a

greater incentive and commitment to leverage their human capital to enhance organizational performance.

(Witteloostuijin & Wijbenga, 2006) This view is often also seen within a private equity perspective, where a

lot of knowledge within the top-management has to perform to create future value within the target firm

(Splid, 2007)

3) A suitable contract requires a venture capital contract designed to align the interests of both the VC and

founders – a contract which maximizes the value of both parties. This requires that the contract should

contain both legal and financial consequences in case of severe violation. (Cable & Shane)

4) Comparable with the private equity market performance-based allocation of stock options, or other

financial incentives, to founders has historically proven to be a effectual method of increasing the efforts of

the founders (Splid, 2007)

5) Milestone Financing of a start-up in stages induces founders to fulfill and behave honestly of the given

terms, because a VC can withdraw from an investment at the next milestone if not fulfilled (Wright &

Robbie, 1998)

6) Monitoring through board positions: Through board representations, which entails voting rights,

information and approval rights, VC can gain a strong control leverage of the founders of the start-up.

7) Post-investment involvement from the VCs with the founders will make a stronger commitment, and the

possibility of the founders to feel more connected with the VC, will increase. Also, the founders might find

it more difficult to “go-their-own-ways” if the VCs are actively present and involved in strategic decisions

(Cable & Shane)

24 | Page

There are several ways in which VCs and founders can mitigate the asymmetry information. If you go on top of the

seven options, you can extract two main characteristics you should take action upon when deciding to fund a

certain start-up. Contractual design and active involvement, will limit the asymmetry information significantly,

however, it will be impossible to eliminate all asymmetry. (Lerner & Schoar, 2004)

2.5 Typical Venture Capital Investment Process: VC Investment Cycle The investment process can vary from one VC firm to another; however it typically involves five aspects. The

process starts with the sourcing and screening of ideas, followed by due diligence, negotiating the terms of the

forward work, post-investment monitoring/involvement, and generating return (exit phase). Generally, as stated

previously, the most important, and also the most common deal breaker, is the lack of faith in the current

management team and their abilities to execute the business case. The next section will briefly discuss every step of

the venture capital investment cycle.

2.5.1 Contact Phase Time is limited and is one of the most valuable resources for both VCs and Business Angels. Often cold calls, e-

mails and letters are therefore seen as “spam”, and even though many proclaim that they try to answer all inquiries,

time is limited and often the answers are given without even looking at the business plan. (Kølendorf P. , 2012)

(Buch, 2012) The only qualified deal flow routes are through strategic referrals or direct contact with a VC at an

industry event, but the strategic referral is the primarily preferred source of deal flow. Angel.co is a platform

actually based on this approach, trying to connect start-ups through network of referrals and sponsors, where

getting the right sponsor/referral could mean the difference between finding capital or not. VC’s prefer to rely on

their intimate network for new investment opportunities.

“I have invested in five different businesses now, but they all have one thing in common: I trust and know the people who have

either referred me to the cases or they are involved within the case. In my experience this is the same for many VC’s I have

encountered with my work at Just Eat” (Buch, 2012)

Even though Angel.co and crowd sourcing platforms have changed the way start-ups can promote themselves and

get social proofing, the financing part is still done through referrals either virtually or in person, and the basic

investment are therefore often linked to the personal connection. Effective networking with sponsors and referrals

of a VC is therefore paramount to receive funding. Sponsors can be angels, attorneys, accountants, consultants, or

venture capital networks. The best sponsors would however always be the ones who are within the VCs’ inner

circle; an investor or some management from previous investments who have performed. (Cardis, 2001)

Generally there are four possible deal “flow-routes” to approach a VC with the investment opportunity.

1) Strategic referral or sponsorship contact

2) Direct contact with a VC at an industry event

3) IT platforms: (Angel.co, Angellist), crowd sourcing platforms (Kickstarter, Seedrs, Fundrs), etc.

25 | Page

4) Cold contact through, mail, telephone, or letter

If it is not possible to find a suitable sponsor and investor, the next step should be to attend industry events where

the target venture capital firm would likely show up – Web 2.0, Nexxt, Barcamp, Open coffee club, Web 2.0 Expo,

Techcrunch 50, Techcrunch Europa, Comed, Idealab, Web 2.0 Summit.

VCs has three purposes to visit these industry events:

To socialize with other VCs

To socialize with entrepreneurs

To experience the latest trends within a field

The main components of a business proposal are analyzed in a short meeting and industry experts are asked of

their opinion. The VC then sends out a prompt “no” or calls to ask specific questions and requests a business plan.

This is however more common and seen as a normal procedure in the US, compared to what is seen in the EU.

(Titus, 2011) If the business plan survives the rigid initial review, the VC invites the entrepreneur for a face-to-face

presentation of the business case.

2.5.2 Screening Investment Ideas It is important to elaborate that the choice of getting VC capital is an important choice for both the VC, but also

essential for the start-up. The right chemistry between the management team and the Limited Partners (LP) and/or

General partners (GP) within the VC is essential. It is thus important to have a certain analysis from both the VC

and the start-up, when starting their initial search and screening of candidates on either funding or receiving

funding. The VCs wants to take a glimpse at the members of the future management team of their investment, and

build a strong connection with them. Presentations to VCs should be like a sales pitch – a moment of personal

selling in which you sell yourself, your team and company.

Sherman and Arundale argue that the key questions any VC needs to have answered after the presentation and the

following Q&A are: (Garbade, 2009)

Is the product or service technically sound and commercially viable?

Is the business model understandable and does it make sense?

Is the management team experienced and do they have the ability to exploit the business potential, control

the company through the growth phase and make the business happen?

Which companies are the main competitors?

How proprietary or unique are the company’s products or services?

26 | Page

How valid are the financial and strategic assumptions that support the basis for future success of the start-

up?

How big is the size of the market?

Is there an effective strategy for getting to market and building a potentially sizable and market-leading

business quickly?

Who are the early customers? How are buying decisions made? Why do they want the product?

What investment amount is needed to finance the business to the next stage?

2.5.3 Due Diligence VCs often have different approaches towards the due diligence phase, as it also depends on the internal resources

and the maturity of the overall venture capital market. However, VCs often construct a detailed review and analysis

of an investment opportunity before an investment is made. In empirical research, it is found that the most VCs

prefer an investment opportunity which offers a good management team and acceptable product and market

characteristics. (Muyzka & Birley, 1996) This is also confirmed by both T. Knudsen and J. Buch from Miinto, who

have invested in several businesses in the last couple of years.

“I know it is starting to be a cliché, but it does not make it less true. I would rather invest in a A-management team and a B-

idea or business case, than investing in a A-business case and a B-management team. Basically I think the team means

everything for a case to succeed – you have to look into the eyes of the entrepreneur and you should see fire – if I don’t I will

not invest. The management team is the one who is going to carry the business case through its tough times, and you only do

this with passion and commitment” (Buch, 2012)

As stated above the management team seems to be recognized as the simple most important fact for a VC to

invest. However, this is also highly dependent on the investment stage of the VC. Investing in the growth and later

stages requires different capabilities, of both the VCs and the investment team. The idea has probably proven that it

has potential, and now the requirements to succeed are different, which implies that the management teams’

importance might be diluted with the development of the business/start-up.

Other parameters on which the VC make their decision whether to invest or not are: perceived strength of the idea,

capabilities, skills and past record of the founders. VCs have to cover three main types of risk within their due

diligence: management risk, which influences execution risk and agency risk, and market risk; competition risk,

new entrant risk, market growth risk and market size risk and product risk; product development risk, proprietary

risk and technology obsolescence risk. Due diligence can be defined as a rigorous assessment and evaluation of the

embedded factors that affect the likelihood of failure or success of a start-up.

There are many different approach of conducting a due diligence within the industry. Some VCs basically talk with

industry experts within their network, while others buy strategy and market reports from external consultants.

27 | Page

There are three parts of a due diligence, also known from the Private Equity market; Business, Financial and Legal.

This report will not take on the Legal perspective of the due diligence, even though this perspective is often also

very interesting within start-ups. In the next couple of sections the report will go through some of the most

important areas of the due diligence phase within the VC environment. Some of the most important investment

criteria’s and how VC tends to eliminate risk within the different areas will be described. Of course the way a VC

do their due diligence differs, however, this thesis will take some of the most normal and basic characteristics of the

due diligence and enlighten these. The next section will be structured as follows:

Management Team Due Diligence

Business Model (Product Due Diligence)

Market Analysis (Market Due Diligence)

Valuation (Financial due diligence)

2.5.3.1 Management Team In a correlation analysis, Tyebjee and Bruno find a negative correlation between the independent variable

“management capabilities” and subordinate variable “risk”, which fully validates the shift in weight of the key

investment decision criteria. VCs examine the business proposal and determine what skills and characteristics are

needed by the management team to make the start-up succeed. (Tyebjee & Bruno, 1984)

They evaluate every single member of the team and in addition the chemistry in-between the members of the team,

checking for passion, focus, vision, integrity, and profound dedication needed to run a successful start-up. The

basement of each founding member falls into two categories:

a) Individual characteristics – a founder/entrepreneur has to have a good business understanding, have a

good approach towards risk and good verbal ability.

b) Experience – VCs seek a track record of the founders, both success and failures, as you learn from every

single step within the entrepreneurial environment. Founders who have successfully managed business

before, including intrapreneurs. An experienced management team knows how to react when markets

change; therefore VCs often fancy founders with extensive experience in the relevant industry. Many VCs

even find it hard to invest in entrepreneurs who haven’t experienced failure of any kind. (Gladstone &

Gladstone, 2002)