currency trader0609p62

DESCRIPTION

TRANSCRIPT

June 2009

Volume 6, No. 6

Strategies, analysis, and news for FX traders

PATTERN + FILTER: Screening intraday FX trades p. 20

HOW RISK AVERSION DRIVES the FX market p. 14

CAN CHINA LEAD THE GLOBE out of recession? p. 8

PROTECTIONISMand the forex market p. 10

CURRENCY VOLATILITYand Treasury returns p. 26

FOREX BROKERAGES chafe at new NFA

rule p. 36

Contributors . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Global Markets

All eyes on China . . . . . . . . . . . . . . . . . . . . .8China’s recent economic numbers have been

encouraging, but questions remain about their

validity and whether the Asian dragon can light

the world economy on fire by itself.

By Currency Trader Staff

For now, protectionist

banter recedes . . . . . . . . . . . . . . . . . . . . .10So far, we’ve avoided a global trade war

driven by protectionism. Another economic

downswing could put nations to the test,

though.

By Currency Trader Staff

On the Money

Risk aversion . . . . . . . . . . . . . . . . . . . . .14Extraordinary times call for out-of-the-box

thinking about markets.

By Barbara Rockefeller

Trading Strategies

Midpoint filter for intraday FX . . . . . . . . .20What happens when you use the previous

day’s range to determine when to take long

or short trades the next day?

By Currency Trader Staff

Advanced Strategies

Currency volatility and long-term

treasury returns . . . . . . . . . . . . . . . . . . . .26The belief that higher currency volatility leads to

steeper yield curves and negative bond returns

has been challenged by the 2008-2009 financial

upheaval.

By Howard L. Simons

CONTENTS

2 June 2009 • CURRENCY TRADER

continued on p. 4

Display Up to 10 Levels of

Market Depth

1-Click Entry Order

{o

of h{

1E

{Competitive Bid/Ask Spreads

EUR/USD 10:02:18D

Buy 10000.5Sell 1000

10Bid 875 Offer 870

Amt(M) Cpty Bid Offer Cpty Amt(M)

20.5 861 883 29.5Bid Alert: 1.27100 Net Open 0

ALL ALL

1.0 870 875 1.0

1.0 866 883 1.0

1.0 856 884 10.0

10.0 856 885 7.5

7.5 855 886 10.0

High 1.27552Low 1.25338

1.01.0 8701.26870

8751.26875 1.26895

1.26890

1.26885

1.26880

1.26875

1.26870

1.26865

1.26860

1.26855

New Order

FOREX CAPITAL MARKETS, FINANCIAL SQUARE, 32 OLD SLIP, 10TH FLOOR, NEW YORK, NY 10005 USA - 1-646-432-2970

www.fxcm.com/atforex1-646-432-2970

WARNING: Trading foreign exchange on margin carries a high level of risk and may not be suitable for all investors. Before deciding to trade foreign exchange, you should carefully consider your monetary objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your deposited funds, and therefore you should not speculate with capital that you cannot afford to lose. *Without proper risk management, currency trading has a high degree of leverage which can lead to large losses as well as gains. **Please note FXCM Micro in its discretion may or may not offset individual transactions unlike transactions in most FXCM Standard accounts.

Margin-based FX Trading* Agency Execution** Liquidity from Multiple Global Banks

4 June 2009 • CURRENCY TRADER

Have a question about something you’ve seen in Currency Trader?

Submit your editorial queries or comments to

Looking for an advertiser?Consult the list below and click on the company name for a direct link

to the ad in this month’s issue of Currency Trader.

CONTENTS

Ablesys

CMS Forex

dbFX

eSignal

E*TRADE FINANCIAL

Forex & Options Expo

FXCM

fxKnight.com

Institute of Higher Earning

InterbankFX

MoneyShow.com

NinjaTrader

RS of Houston

TraderPlanet.com

Tsunami Trading

Forex News

FIFO mandate causes headaches

for U.S. FX dealers . . . . . . . . . . . . . . . . . .36The NFA’s new rule regarding first-in-first-out

trade exits has forex dealers rushing to make

the necessary changes to their platforms.

By Chris Peters

International Markets . . . . . . . . . . . . . .38Numbers from the global forex, stock,

and interest-rate markets.

Global Economic Calendar . . . . . . . . . . . .41Important dates for currency traders.

Key concepts . . . . . . . . . . . . . . . . . . . . . . .42

Events . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42Conferences, seminars, and other events.

New products & services . . . . . . . . . . . . . .43

Important Note: Futures and options transactions are complex and carry a high degree of risk. They are intended for sophisticated investors and are not suitable for everyone. For more information, please read the Characteristics and Risks of Standardized Options and the Risk Disclosure Statement for Futures and Options available by visiting etrade.com/options and etrade.com/futures or by calling 1-800-ETRADE-1.New Accounts claim based on internal E*TRADE FINANCIAL Corp. metrics for average daily gross new E*TRADE Bank and E*TRADE Securities accounts between 3/1/08–2/28/09. Net new accounts were in excess of 150,000 over the same period.1. The new account holder will be charged 99¢ (per side, per contract, plus exchange fees) futures commissions for each futures trade executed once a qualifi ed account is opened and funded and deposited funds have cleared. After the 90 day offer period, each futures trade is $2.99 (per side, per contract, plus exchange fees). This offer is not valid for IRAs, other retirement, business, trust or E*TRADE Bank accounts. Excludes current E*TRADE Securities customers, E*TRADE FINANCIAL Corp. associates and non-U.S. residents. Offer only applies to new E*TRADE Futures Accounts opened with a $10,000 minimum deposit. Account holders must maintain minimum funding in all accounts ($10,000 minus any trading losses) for at least six months or credit may be surrendered. Limit one new E*TRADE Futures account per customer. We reserve the right to terminate this offer at any time. In addition to the $2.99 per contract per side commission, futures customers will be assessed certain fees including applicable futures exchange and NFA fees, as well as MF Global fl oor brokerage charges for execution of non-electronically traded futures and futures options contracts. These fees are not established by E*TRADE Securities and will vary by exchange.E*TRADE Securities LLC and Trading Technologies are separate and unaffi liated companies.CME Group does not offer or provide any investment advice or opinion regarding the nature, potential, value, suitability or profi tability of any product or investment strategy. The Globe Logo, CME Group and Forex E-micros® are trademarks of Chicago Mercantile Exchange Inc.Securities products and services are offered by E*TRADE Securities LLC, Member FINRA/SIPC/NFA.Futures accounts are carried by MF Global, an unaffi liated company.System response and account access times may vary due to a variety of factors, including trading volumes, market conditions, system performance and other factors.©2009 E*TRADE FINANCIAL Corp. All rights reserved.

SIZEMATTERS.Introducing Forex E-Micro Futures.1/10 the contract size, 1/10 the risk exposure.

DIRECT ACCESS to Every Secure& Regulated U.S. Market

NO FEE Futures Platformpowered by Trading TechnologiesTM

TRADE THEM AT E*TRADE

FREE EDUCATION & DedicatedCustomer Service

For 90 days, $2.99 thereafter

ETRADE.COM/FUTURES 1-800-ETRADE-1

NEW

1000 new accounts a day

1

�Howard Simons is president of

Rosewood Trading Inc. and a strategist for

Bianco Research. He writes and speaks fre-

quently on a wide range of economic and

financial market issues.

�Barbara Rockefeller (http://www.rts-forex.com) is

an international economist with a focus on foreign

exchange. She has worked as a forecaster, trader, and con-

sultant at Citibank and other financial institutions, and

currently publishes two daily reports on foreign exchange.

Rockefeller is the author of Technical Analysis for Dummies

(For Dummies, 2004), 24/7 Trading Around the Clock, Around

the World (John Wiley & Sons, 2000), The Global Trader (John

Wiley & Sons, 2001), and How to Invest Internationally, pub-

lished in Japan in 1999. A book tentatively titled How to

Trade FX is in the works. Rockefeller is on the board of

directors of a large European hedge fund.

6 June 2009 • CURRENCY TRADER

Editor-in-chief: Mark Etzkorn

Managing editor: Molly Goad

Associate editor: Chris Peters

Contributing editor:

Howard Simons

Contributing writers:

Barbara Rockefeller, Marc Chandler

Editorial assistant and

webmaster: Kesha Green

Art director: Laura Coyle

President: Phil Dorman

Publisher,

Ad sales East Coast and Midwest:

Bob Dorman

Ad sales

West Coast and Southwest only:

Allison Chee

Classified ad sales: Mark Seger

Volume 6, Issue 6. Currency Trader is published monthly by TechInfo, Inc., 161 N. Clark St., Suite 4915, Chicago, IL 60601. Copyright © 2009 TechInfo,Inc. All rights reserved. Information in this publication may not be stored orreproduced in any form without written permission from the publisher.

The information in Currency Trader magazine is intended for educational pur-poses only. It is not meant to recommend, promote or in any way imply theeffectiveness of any trading system, strategy or approach. Traders are advisedto do their own research and testing to determine the validity of a trading idea.Trading and investing carry a high level of risk. Past performance does notguarantee future results.

For all subscriber services:www.currencytradermag.com

A publication of Active Trader®

CONTRIBUTORSCONTRIBUTORS

Recent economic reports out of China have sur-prised on the upside, leading some marketwatchers to cast their gaze eastward in thesearch for the growth engine that will propel

the global economy out of its current recession. The International Monetary Fund (IMF) is projecting a

1.3-percent decline in global growth in 2009 — the first con-traction since World War II, and well below the 4- to 4.5-percent average global gross domestic product (GDP)growth rate of the past 20 years. While the U.S. remainsmired in negative growth numbers, with GDP plunging 5.7percent in Q1 2009, China might have already hit its eco-nomic low point and be climbing higher out of its econom-ic morass.

The question is, can it power the rest of the world torecovery?

Can the Dragon lead?Not alone, according to Sherman Chan, economist atMoody’s Economy.com. Despite its burgeoning clout,China does not yet outweigh the U.S. and other economiesthat are still floundering.

“Although China’s economy maintains a positive out-look, the dragon is not powerful enough to end the globalrecession,” he says. “Despite years of stellar GDP growth,China still ranks behind the U.S. — the epicenter of theglobal turmoil — in contribution to world output. The com-bined influence of the major economies in recession — theU.S. along with Europe and Japan — is far too great forChina to offset. The most China can help in this global cri-sis is to cushion the downturn in some economies throughimports.”

Mingchun Sun, chief China economist at NomuraInternational, agrees. “China is still a relatively small por-tion of the world economy,” Sun says. “China will be the

first coming out, but may not have the strength to lead theworld out.”

Stephen Webster, director of London-based TopEcon,frames it differently. “I believe it is more accurate to saythat China [will] outperform most other economies in thenext two years and make a significant contribution to glob-al recovery, alongside other key countries like India.”

As evidence, Webster cites IMF forecasts for China topost 6.5-percent GDP growth in 2009 and India to come inat 4.5 percent, vs. -2.8 percent in the U.S. and -4.2 percent inthe Eurozone. Webster notes the IMF expects China andIndia to grow at 7.5 and 5.6 percent rates, respectively, com-pared to a zero GDP reading for the U.S. and a -0.4 percentGDP rate in the Eurozone.

Although the Chinese growth engine will play a pivotalrole, it is itself part of a larger system.

“China’s rebound should also have an important positiveimpact on global confidence and on commodity prices,”Webster adds. However, he warns this process will taketime. “In part, it’s a vicious circle, with China’s revivaldepending on demand from the U.S. and Europe.”

Recent numbers: Low, but stabilizingWhen assessing China’s economic strength and theprogress of its recovery from the global economic crisis,“what you see from China is not always what you get,”says James Pressler, associate international economist at theNorthern Trust Company in Chicago.

For example, Pressler notes that China issued its first-quarter 2009 GDP data ahead of the U.S. and that Chinadoes not revise its GDP figures. “The exact figures are sub-ject to a degree of politicization, but what’s more importantis the trajectory of slowing growth,” he says.

Released in mid-April, Q1 Chinese GDP came in at 6.1percent year-over-year. That sounds stellar from anAmerican perspective, but as Pressler points out, that num-ber is “the lowest rate of growth they have posted thisdecade.” (Q2 2008 GDP was 10.1 percent, Q3 2008 was 9percent, and Q4 2008 was 6.8 percent.)

But that, Pressler adds, might be good news in the longerrun.

“At this point, we feel that growth has reached its lowpoint. We feel the second quarter GDP figure will be betterthan the first quarter,” he says.

In the wake of stronger-than-expected economic news,

GLOBAL MARKETS

8 June 2009 • CURRENCY TRADER

All eyes on ChinaThe question now isn’t whether or not the world will catch cold if China sneezes — it’s whether or not

the world will regain its appetite if China puts away its Kleenex and aspirin.

BY CURRENCY TRADER STAFF

The Chinese economy will play

a pivotal role in a global recovery,

but it is itself simply a part of

a larger system.

CURRENCY TRADER • June 2009 9

Moody’s Economy.com recently upped its 2009 China GDPforecast from 7 to 7.5 percent. Some analysts say China’shuge fiscal stimulus package has helped propel a Chineserecovery.

Of industrial production, Chan notes that it “not onlyavoided falling into negative territory, but its recoverycame earlier than expected.”

In inflation-adjusted terms, Chinese industrial produc-tion was 7.3 percent in April. The low point during therecent slowdown was a 5.4-percentreading in November 2008.

“They are used to double-digitgrowth,” Pressler says. Nonetheless,the rebound in industrial productiondata “shows that we are seeing fiscalstimulus kicking in, or at least the fig-ures suggest it is working.”

Exports reboundingPressler says a pickup in the exportsector is an important reason for opti-mism. Overall, he believes the worst ofChina’s export decline is over. After aJuly 2008 peak of $128.7 billion,monthly exports slowed to a low of$68.2 billion in February 2009.However, Pressler explains that lowreading was somewhat impacted bythe Lunar New Year that month, atime when “production slows downand there isn’t as much trading withregional participants.”

From there, the numbers haveincreased. March 2009 exports were$95.5 billion, and the April numbercame in at 91.6 billion, which “putsChina back at levels seen in the firstand second quarter of 2007,” Presslersays.

What did they do right?Many economists say the Chinese gov-ernment deserves kudos for an effec-tive stimulus package, which Presslersays totaled around $549 billion.

“China is putting some of thatmoney — all those reserves it is sittingon — into play,” says Pressler.

Webster says the fiscal stimulus wasaimed at “infrastructure, farming, andconstruction projects, with some addi-tional allocations to the social security,welfare, and health systems.”

The measures were timely andforceful, according to Sun. “The posi-tive impact on consumption will prove

larger than most people expect,” Sun says. Webster also credits China for easing credit conditions by

reducing interest rates and putting pressure on banks to bemore liberal in their lending practices.

However, while the Chinese government may haveearned a pat on the back in one sense, the argument can bemade that some of the steps they’ve taken might look betterin the short term than the long term. For example, Pressler

continued on p. 10

10 June 2009 • CURRENCY TRADER

notes “they are shoring [exports]up through subsidies and loan-forgiveness programs — shoringthem up during a time whenslower growth should weed outthe less-efficient companies.”

What are the potential repercus-sions for this special treatment ofthe Chinese export sector? “Theywill continue to have an economi-cally inefficient export sector thatwill rely on an artificially weakcurrency and government subsi-dies, rather than productionenhancements, innovations, and arise up the value-added scale,”Pressler explains.

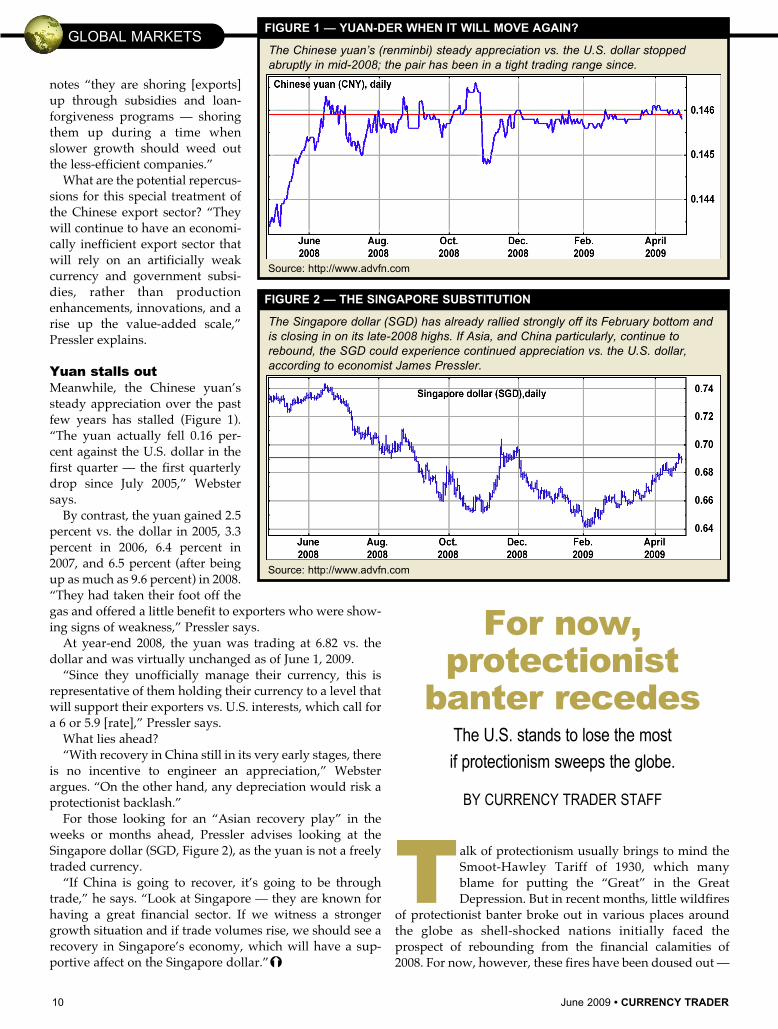

Yuan stalls outMeanwhile, the Chinese yuan’ssteady appreciation over the pastfew years has stalled (Figure 1).“The yuan actually fell 0.16 per-cent against the U.S. dollar in thefirst quarter — the first quarterlydrop since July 2005,” Webstersays.

By contrast, the yuan gained 2.5percent vs. the dollar in 2005, 3.3percent in 2006, 6.4 percent in2007, and 6.5 percent (after beingup as much as 9.6 percent) in 2008.“They had taken their foot off thegas and offered a little benefit to exporters who were show-ing signs of weakness,” Pressler says.

At year-end 2008, the yuan was trading at 6.82 vs. thedollar and was virtually unchanged as of June 1, 2009.

“Since they unofficially manage their currency, this isrepresentative of them holding their currency to a level thatwill support their exporters vs. U.S. interests, which call fora 6 or 5.9 [rate],” Pressler says.

What lies ahead? “With recovery in China still in its very early stages, there

is no incentive to engineer an appreciation,” Websterargues. “On the other hand, any depreciation would risk aprotectionist backlash.”

For those looking for an “Asian recovery play” in theweeks or months ahead, Pressler advises looking at theSingapore dollar (SGD, Figure 2), as the yuan is not a freelytraded currency.

“If China is going to recover, it’s going to be throughtrade,” he says. “Look at Singapore — they are known forhaving a great financial sector. If we witness a strongergrowth situation and if trade volumes rise, we should see arecovery in Singapore’s economy, which will have a sup-portive affect on the Singapore dollar.”�

GLOBAL MARKETS

The Singapore dollar (SGD) has already rallied strongly off its February bottom andis closing in on its late-2008 highs. If Asia, and China particularly, continue torebound, the SGD could experience continued appreciation vs. the U.S. dollar,according to economist James Pressler.

Source: http://www.advfn.com

FIGURE 2 — THE SINGAPORE SUBSTITUTION

The Chinese yuan’s (renminbi) steady appreciation vs. the U.S. dollar stoppedabruptly in mid-2008; the pair has been in a tight trading range since.

Source: http://www.advfn.com

FIGURE 1 — YUAN-DER WHEN IT WILL MOVE AGAIN?

For now, protectionist

banter recedesThe U.S. stands to lose the most

if protectionism sweeps the globe.

BY CURRENCY TRADER STAFF

Talk of protectionism usually brings to mind theSmoot-Hawley Tariff of 1930, which manyblame for putting the “Great” in the GreatDepression. But in recent months, little wildfires

of protectionist banter broke out in various places aroundthe globe as shell-shocked nations initially faced theprospect of rebounding from the financial calamities of2008. For now, however, these fires have been doused out —

thanks to some economic stabilization — but economistswarn the issue of protectionism is not likely to disappearentirely any time soon.

“Protectionist measures are clearly one of the major risksto global recovery,” says Stephen Webster, director ofLondon-based TopEcon. “It is a big temptation for countriesto resort to infringing either the rules or the spirit of freetrade to help encourage growth in their own economies.”

In one of the most notable protectionist salvos in the U.S.,in February the $900 billion stimulus bill was initially ladenwith a “Buy American” clause thatstipulated that only U.S.-made goodscould be used in projects funded bythe bill. According to Jay Bryson, glob-al economist at Wachovia, coolerheads ultimately prevailed and thefinal version was “watered down” tostate that actions had to be consistentwith current U.S. trade law.

“In the West, the U.S. seems to becoming under the most fire for protec-tionist tendencies,” Webster says. “Forexample, Canadian Industry MinisterTony Clement has criticized U.S.Congress for its injurious ‘BuyAmerican’ rules that bar Canadianfirms from bidding on U.S. stimulusprojects. Indeed, the Buy Americanprovision in the U.S. stimulus bill hasresulted in opposition not only acrossthe globe but also from withinAmerica itself, with the big fear that itwill lead to similar restrictions inother countries.

“Similarly, U.S. President BarackObama’s promise to modify tax lawsthat currently allow U.S. companies topay less tax if they outsource to, orcreate a job in, India — rather than theU.S. — has been criticized by someIndian factions as a protectionistmeasure.”

Ultimately, some argue, the issueboils down to jobs.

“The flashpoint domestically is,where are all the jobs? We keep send-ing them abroad,” says Ken Goldstein,economist at the Conference Board inNew York. “There is fancy talk aboutquotas, tariffs, protectionism, andimmigration — but what it reallycomes down to is jobs.”

This issue has not been confined tothe U.S. in recent months. In March,for example, French President NicolasSarkozy found himself embroiled inthe middle of a protectionist debate

after he encouraged automaker Renault to shift productionback into France. However, Sarkozy backed off.

“There has also been a lot of protectionism banter in Asiabetween China and its neighboring countries,” Webstersays.

CURRENCY TRADER • June 2009 11

continued on p. 12

“Protectionism results in global trade

wars nobody can afford to wage.”

12 June 2009 • CURRENCY TRADER

GLOBAL MARKETS

The protectionism domino effectOnce protectionism starts, it’s very difficult to stop — aproblem everyone seems to understand economically, butnot necessarily politically.

“We are fully cognizant if we go down that path and tryto put up a wall around us, everyone will put up a wallagainst us,” Goldstein says. “It is less than a zero-sumgame.”

Economists generally agree the Smoot-Hawley tariff is aclear example of the perils of protectionism.

“It was damaging not only to the U.S. economy but alsoto others economies,” Webster says. “It raised U.S. tariffs onsome 20,000 imported goods to record levels and manycountries retaliated with by raising their own tariffs on U.S.goods. U.S. exports and imports were reduced by morethan 50 percent. Some observers blamed the tariff for caus-ing the Great Depression. That remains a controversy tothis day, but it undoubtedly soured trading relations withother countries and caused the shrinkage of world trade.”

Bryson agrees. Smoot-Hawley is the “poster child forwhy you don’t want to be doing this. It starts a global tradewar that nobody can afford to wage.”

Bryson notes that any potential negative repercussionsfrom protectionist moves are merely theoretical at thispoint. But if governments become excessively nervousagain and enact protectionist measures later this year ornext, Bryson speculates that “some sort of trade war wouldaffect stock markets. Global growth would probably beslower and that would first affect companies that do a lot ofinternational business. My guess is it would be negative forthe dollar.”

Free tradeWebster puts forth the economic case for free trade. “Faircompetition resulting from free trade helps increase effi-ciency and depress world prices by allowing countries tospecialize in producing or supplying what they are good at,and letting other countries specialize in the areas they arebest at,” he says. “Protection arguably leads to the opposite.

“If emerging markets are allowed to do what they do bestby utilizing comparative advantage, it also helps to allevi-ate global poverty and reduces the need for global aid fromthe richer countries,” he continues. “The fight against pro-tectionism should promote the idea that everyone canbecome better off and people should not be fearful of unem-ployment and change. Trying to protect employment byraising tariffs or some other protectionist measure has a dis-torting influence, and the U.S. — perhaps more than anyother country in the world — has its industrial roots in ini-tiative and entrepreneurship. In any case, protectingdomestic industries against foreign competition is ultimate-ly counterproductive, since more often than not it leads toretaliation, higher costs, and lower levels of world trade.”

For now, though, rebounding equity markets and stabi-lizing economic statistics have put out the protectionistflames that were burning so hot earlier in the year. If thisturns out to be more of a respite than a reversal, however,the embers may regain strength.

“So far, we have not seen a lot of signs of protectionism,but if the global recession drags on, it could very well rearits ugly head again,” Bryson says. “I don’t think this issuehas gone away yet, but for now we have avoided the worstof it. We’ll see.”�

Bob DormanAd sales East Coast and [email protected]

(312) 775-5421

Allison CheeAd sales West Coast and Southwest

[email protected](415) 272-0999

Mark SegerAccount Executive

[email protected](312) 377-9435

Three good tools for targeting customers . . .

— CONTACT —

��������������������������

�������������������������

��������������������

������������������������

�������������

����������������

�������������

����������������

�������������������

���������������������������������������������������������������������� �� ������ ���������������������������������� �� ������ ��������

��������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������

�������������������������������������������������������������������������������������������������������������������������������������

���

����������������������������������������������������������������������������������

�����������������������������������

�����������������������������������������������

�������������������������������������������������������������������

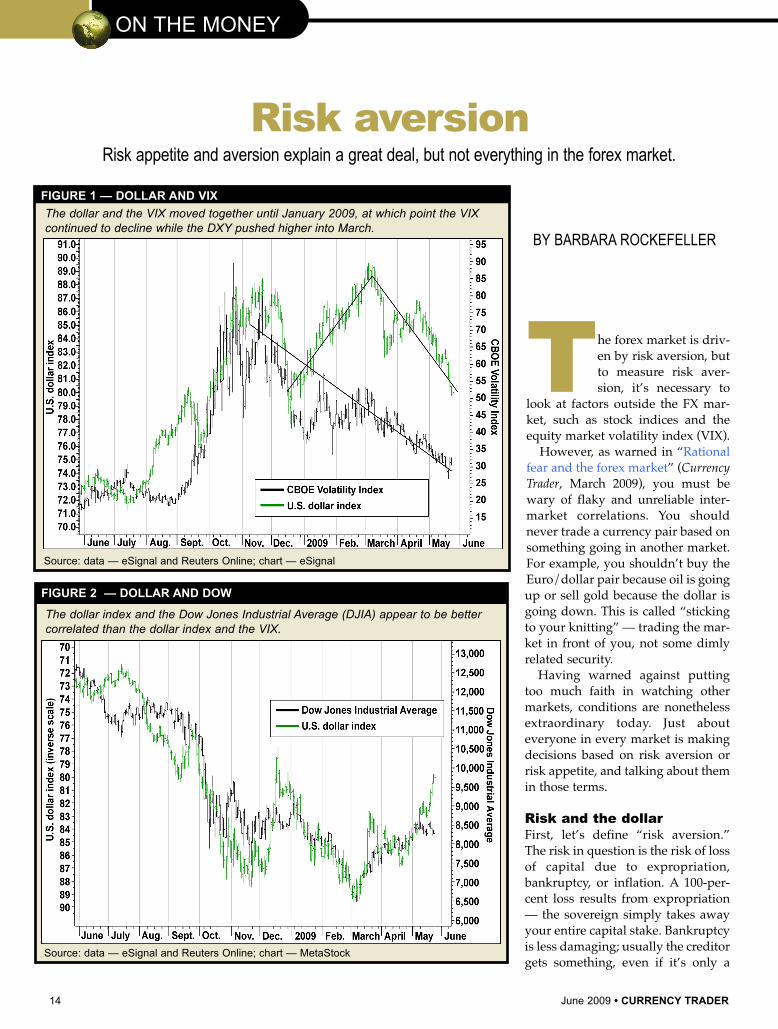

The forex market is driv-en by risk aversion, butto measure risk aver-sion, it’s necessary to

look at factors outside the FX mar-ket, such as stock indices and theequity market volatility index (VIX).

However, as warned in “Rationalfear and the forex market” (CurrencyTrader, March 2009), you must bewary of flaky and unreliable inter-market correlations. You shouldnever trade a currency pair based onsomething going in another market.For example, you shouldn’t buy theEuro/dollar pair because oil is goingup or sell gold because the dollar isgoing down. This is called “stickingto your knitting” — trading the mar-ket in front of you, not some dimlyrelated security.

Having warned against puttingtoo much faith in watching othermarkets, conditions are nonethelessextraordinary today. Just abouteveryone in every market is makingdecisions based on risk aversion orrisk appetite, and talking about themin those terms.

Risk and the dollarFirst, let’s define “risk aversion.”The risk in question is the risk of lossof capital due to expropriation,bankruptcy, or inflation. A 100-per-cent loss results from expropriation— the sovereign simply takes awayyour entire capital stake. Bankruptcyis less damaging; usually the creditorgets something, even if it’s only a

ON THE MONEY

The dollar index and the Dow Jones Industrial Average (DJIA) appear to be bettercorrelated than the dollar index and the VIX.

FIGURE 2 — DOLLAR AND DOW

Source: data — eSignal and Reuters Online; chart — MetaStock

BY BARBARA ROCKEFELLER

14 June 2009 • CURRENCY TRADER

FIGURE 1 — DOLLAR AND VIX

The dollar and the VIX moved together until January 2009, at which point the VIXcontinued to decline while the DXY pushed higher into March.

Source: data — eSignal and Reuters Online; chart — eSignal

Risk aversionRisk appetite and aversion explain a great deal, but not everything in the forex market.

few cents on the dollar. Inflation isan insidious form of expropria-tion. By creating or allowing infla-tion, the government devalues thepurchasing power of the money,sometimes to an extreme degree.

At the height of the globalfinancial-sector crisis, the dollarwas a safe haven from the poten-tial bankruptcy of banks in otherparts of the world. Investorsbelieved it was safe to place cashin U.S. bank deposits because U.S.banks were too big to fail and/orFDIC insurance would be effec-tive. Because the U.S. operatesunder the rule of law and hadundergone a banking crisis in liv-ing memory (the savings and loancrisis of the 1980s), during whichno depositor lost money, using U.S.dollar bank deposits as a safe havenwas a logical course of action.

As risk aversion had investors in itsgrip, two other things happened: thestock markets of developed countriesfell dramatically — as much as 30 to 45percent — and central banks slashedthe return on money. The truly riskaverse were pretty much stuck withbank deposits as the only sane place topark their capital.

As part of the financial rescue plan,however, the Fed printed vastamounts of new money. So far theincrease in money supply is trapped inthe banking system as “capital” andhas not leaked out to the general econ-omy. But those who fear inflation areconcerned that when the banks dotheir job of recycling this money sup-ply through lending, inflation willinevitably follow. As economist MiltonFriedman said, “Inflation is alwaysand everywhere a monetary phenome-non.” Fed Chairman Ben Bernankemight be a smart guy and have onlythe best intentions, but doubt runshigh he can put the genie back in thebottle.

As a result, the target of risk aver-sion has changed. As the financial cri-sis came to a boil in September-November 2008, the initial target was

equities; now it’s the dollar on thebasis of inflation fear. It was a remark-ably speedy transfer of risk aversionfrom one target to another.

Figure 1 shows the dramatic rise inthe CBOE Volatility Index (VIX) inautumn 2008, with a rise by the dollarindex (DXY) at the same time. The twoindicators moved in sync until January2009, at which point the VIX continuedto trail off while the dollar indexpushed higher into March and subse-quently trailed off by less. The VIX hasfallen in a rough line downward whilethe dollar index has formed an upside-down V.

The dollar index and the Dow JonesIndustrial Average (DJIA) appear tooffer a better correlation (Figure 2). Itseems, though, that when the dollarindex rose more than the Dow inMarch and May, the Dow’s failure tofollow dragged the dollar index backdown.

But does this make sense? On anoutright capital-flow basis, foreignershave gone from net divestiture of U.S.equities last year to net buyers. TheTreasury International Capital Systemreport in May showed foreigners werenet buyers of $15.1 billion of U.S. equi-ties in March, up from a mere $1 bil-lion in January (they bought $33.5 bil-lion in March 2008). Does this accountfor the rise in both the dollar and the

Dow? Well, yes, but only in part.Foreigners account for only a smallfraction of total U.S. stock-marketinvestment; domestic players such aspension funds and mutual funds areresponsible for a much bigger percent-

CURRENCY TRADER • June 2009 15

As the S&P has rallied, so has the Euro — meaning, the U.S. dollar has declined.

FIGURE 3 — S&P AND EURO

Source: data — eSignal and Reuters Online; chart — MetaStock

continued on p. 16

ON THE MONEY

age. Also, official data is released very late, so unless a mar-ket participant hears a story from a broker that foreignersare buying again, foreign participation would tend to haveonly a small effect on the Dow.

In fact, in terms of the risk-aversion paradigm, the newconventional wisdom argues the opposite: a rise in U.S.equities means a drop in risk aversion, which in turn meansthe need for dollars parked in checking accounts (as a safe-

haven) is reduced. Given this world-view, a rising stock market is, per-versely, bad for the dollar. Figure 3,which shows the S&P 500 index andthe Euro/dollar pair (EUR/USD),bears out this thesis: As the S&Prises, the Euro rises, too.

How can both things be true —that U.S. stocks go up on foreignpurchases but also go down on areduction of risk aversion? Theanswer is that the “foreigners buy-ing” story is weak and the risk-aver-sion thesis is more powerful.

Emerging markets and commoditiesThe biggest outcome from the rise inrisk aversion is the emerging bubblein emerging-market currencies andstock indices. Figure 4, which showsthe Brazilian Bovespa stock index(BVSP) and the Indian Sensex stockindex (BSESN), shows these marketsactually reversed earlier than theU.S. market. Both indices werealready rising in January, and after asetback in March, they have gainedmore off their bottoms than U.S. andEuropean indices as of June 1.

The rise in emerging-marketstocks reflects a thread in the currentthinking that emerging markets maymanage a v-shaped recovery (down,then right back up) rather than theL-shaped recovery (down, then side-ways for a long time) the West andJapan will almost certainly get. Forone thing, China implemented itsstimulus package immediately,whereas the U.S. has hardly started.Also, trade between China andBrazil has gone up, not down —unlike the trade pattern elsewhere,with exports from Germany, forexample, down 9.7 percent in thefirst quarter this year. China has alsocontinued to buy and stockpile com-

modities, including oil, copper, and gold, contributing torobust prices that are hardly justified by developed coun-tries’ fundamentals (Figure 5).

The conventional wisdom is that the minute the price ofoil goes up, the dollar goes down. This inverse relationshipis another example of market perversity, since you’d thinkdemand for dollars would go up as the price of a commod-ity denominated in dollars goes up. A rise in the price of oil

16 June 2009 • CURRENCY TRADER

The Brazilian and Indian stock markets reversed earlier than the U.S. market, andthey have gained more off their bottoms than U.S. and European indices.

FIGURE 4 — EMERGING MARKETS

China has continued to stockpile commodities, including copper and gold, contributing to robust prices unjustified by developed countries’ fundamentals.

FIGURE 5 — COMMODITIES

Source: data — eSignal and Reuters Online; chart — MetaStock

Source: data — eSignal and Reuters Online; chart — eSignal

is also commonly interpreted as asign of fresh U.S. demand for ener-gy, which means growth prospectsare looking up for the U.S.

Shouldn’t this be dollar-favor-able, too? Not in the new upside-down world of risk aversion.Traders are so convinced of theinverse relationships that a knee-jerk sell-off in dollars occurs whenthe price of oil rises; sometimesyou can see the relationship hourby hour on the charts. It’s illogical,but it is the way the market choos-es to think today.

Finally, we come to gold, whichhas been rising, if sporadically, asthe financial crisis has evolved.Figure 6 shows gold (GC) and Eurocurrency (EC) futures. Gold has anunaccountably steeper slope offthe October low. If both securitiesreflect pure risk aversion from the dol-lar, you’d think the slope would be thesame or nearly the same. Besides, theypeak and withdraw at different times.Clearly there are fundamentals andmarket sentiment factors at work,other than general risk aversion.

Economic fundamentalsThe one thing missing from all therisk-aversion talk is the fundamentalsof the economies. In December andagain in March, the FX market favoredthe first-in, first-out (FIFO) story thatsuggested the U.S. would recover fromrecession faster and more widely thanany other country: Growth counts.Over long time periods, currencies arehighly correlated with inflation-adjust-ed real growth. The so-called greenshoots of recovery some analysts claimto see poking their heads out of thedirt are more likely to grow roots in theliberal soil of the U.S. than in the strict-ly regulated economies of Europe andJapan. Besides, the U.S. is a vast coun-try. It has, literally, room for shoots toappear in many places, and whilesome of them will no doubt be weeds,the universal expectation is that theU.S. will lead the global recovery.

But growth is taking a back seattoday on the emergence of yet anotherhigh-risk situation. The Standard &

Poor’s ratings agency downgraded theUK’s sovereign rating from “stable” to“negative” in late May 2009 on thebasis that total public debt outstandingwas nearly 100 percent of GDP. The FXmarket immediately turned to thequestion of whether the U.S. would benext to be downgraded, since U.S. debtis already about $11 trillion dollars inan economy of about $13.5 trillion, andrising by the minute. That doesn’tinclude unfunded future liabilities ofabout $44 trillion for Social Securityand Medicare. However, this potentialdowngrade story had a short shelf lifewhen the Chinese quickly remarkedpublicly about their preference for thedollar as the reserve currency, for spe-cific reasons. They say the dollar is stillthe best option to meet the criteria of“safety, liquidity, and profitability,” inthat order.

An official from the StateAdministration of Foreign Exchangesaid “According to exchange-ratetrends, the Euro, sterling, and yen areall high-risk currencies, where the dol-lar has been relatively safe.” Officialssay China’s dollar holdings, almost $2trillion, are simply too big to hedge“without spooking the currency mar-kets.” Moreover, the Chinese like dol-lar liquidity — its historic role since1945. China perceives that Eurozonepolicy-making lacks “the responsive-

ness, flexibility, and aggression of theU.S.”

While the rating agencies probablylack the moxie to name the U.S. as hav-

CURRENCY TRADER • June 2009 17

The differing paths of gold and the Euro currency futures suggest there are fundamentals and market sentiment factors at work, not just risk aversion.

FIGURE 6 — GOLD AND EURO

Source: data — eSignal and Reuters Online; chart — MetaStock

continued on p. 18

18 June 2009 • CURRENCY TRADER

ing a “negative” outlook on the debtsituation, the Chinese can alwayschange their minds — or get agree-ment at some point that the IMF’s spe-cial drawing right (SDR) should be thenew reserve currency (see “Treasurybacks down from China currencymanipulation stance,” Currency Trader,May 2009). The over-indebtedness ofthe U.S. is an old risk being newlynamed as a special risk to the dollar.This violates — in spades — the over-all risk-aversion thesis that a rise inrisk aversion means a flight to the dol-lar.

Possible scenariosHow will the current chapter end? Onelikely scenario has it that a crisis willdevelop in an emerging market, simi-lar to 1997-1998, and soaring stockmarkets will again tumble like domi-nos. It seems clear that some stockmarkets are in bubble mode, so it might not take much of acrisis to get a major pullback from emerging markets, to thebenefit of the dollar.

Another idea floating around is that the U.S. should issuebonds in Euros or yen, which doesn’t reduce the totalindebtedness but might make it more attractive to some for-eign investors. Nobody is expecting realistic plans for actu-ally reducing U.S. indebtedness any time soon.

In Figure 7, the standard error channel (drawn to oneerror on either side of the linear regression from the very

beginning of the Euro) indicates that at year-end 2009, wecan expect a range of 1.6533 to 1.2761, with the linear regres-sion line itself landing at 1.4647. The red lines start with asupport line connecting Euro lows and spaced out to showresistance and a midline.

As a practical matter, now that the market is picking onthe dollar, these are probably realistic ranges, and a strongerdollar is just wishful thinking. �

For information on the author see p. 6.

The standard error channel implies the Euro will be somewhere between 1.6533to 1.2761 at year-end.

FIGURE 7 — EURO PROJECTION

Source: data — eSignal and Reuters Online; chart — MetaStock

“Forecasting follies,” Currency Trader, May 2009.The only technicals that provide tradable forecasts are patterns — but you have to be on the correct time frame and you can’t forget about the fundamentals.

“Listening to the chart,” Currency Trader, April 2009.While everyone debates the ramifications of various policy measures, what is the Euro/dollar chart saying?

“Rational fear and the forex market”Currency Trader, March 2009.Analysis of several intermarket relationships suggests the role ofrisk aversion in the forex market is no cut-and-dried issue.

“Competitive devaluations, the EMU, and the yen”Currency Trader, February 2009.Currency devaluation never works in the long run — just askJapan — but that doesn’t mean panicky governments won’t use itto try to stem the flow of blood in the near term.

“The Euro: Prosperity or perdition?”Currency Trader, January 2009.The belief the Euro sell-off has ended may be based on some

false assumptions about how the U.S. and Europe are handlingthe economic crisis.

“The six Ds of depression,” Currency Trader, December 2008.The buck has gotten a bounce from the recent financial panic,but the longer-term picture isn’t quite as bullish.

“Euro and dollar at parity?” Currency Trader, November 2008.A few short months ago the world was contemplating Euro $2.Now, the talk is all about Euro $1. What are the odds it will happen?

“Crisis of confidence,” Currency Trader, October 2008.As Wall Street and Washington prove themselves equally inept,the dollar suffers.

“The dollar-oil connection,” Currency Trader, September 2008.As oil broke, so did the Euro/dollar pair. What can we learn fromanalyzing bursting bubbles?

You can purchase and download past articles athttp://store.activetradermag.com.

ON THE MONEY

Related reading: Other Barbara Rockefeller articles

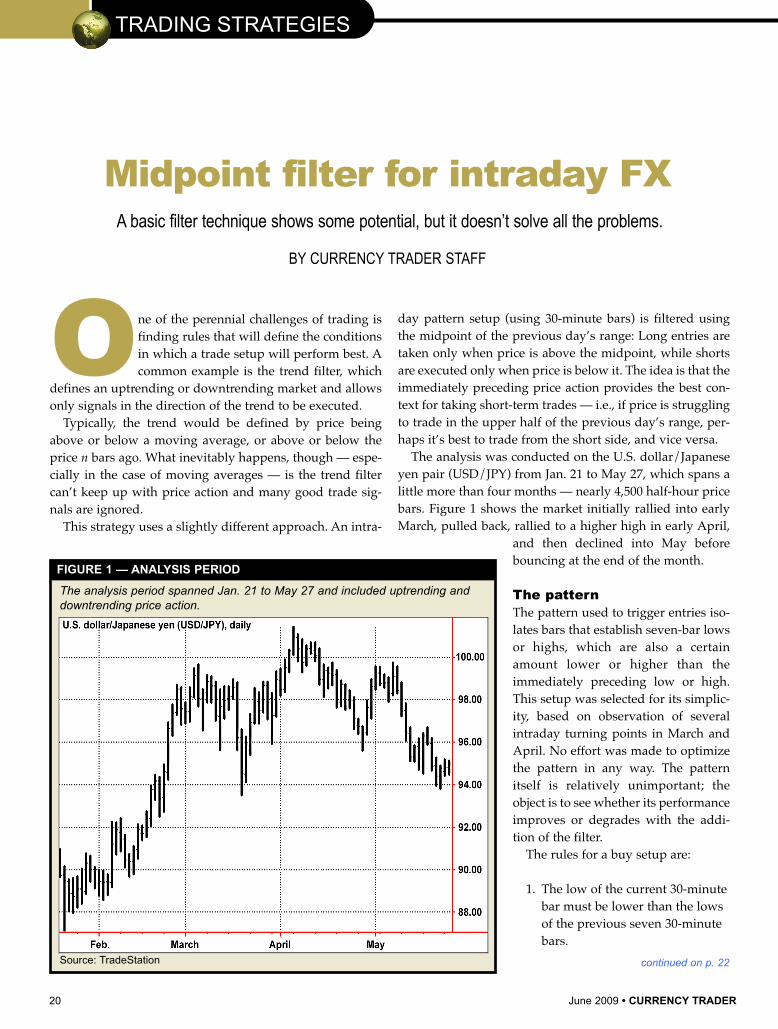

One of the perennial challenges of trading isfinding rules that will define the conditionsin which a trade setup will perform best. Acommon example is the trend filter, which

defines an uptrending or downtrending market and allowsonly signals in the direction of the trend to be executed.

Typically, the trend would be defined by price beingabove or below a moving average, or above or below theprice n bars ago. What inevitably happens, though — espe-cially in the case of moving averages — is the trend filtercan’t keep up with price action and many good trade sig-nals are ignored.

This strategy uses a slightly different approach. An intra-

day pattern setup (using 30-minute bars) is filtered usingthe midpoint of the previous day’s range: Long entries aretaken only when price is above the midpoint, while shortsare executed only when price is below it. The idea is that theimmediately preceding price action provides the best con-text for taking short-term trades — i.e., if price is strugglingto trade in the upper half of the previous day’s range, per-haps it’s best to trade from the short side, and vice versa.

The analysis was conducted on the U.S. dollar/Japaneseyen pair (USD/JPY) from Jan. 21 to May 27, which spans alittle more than four months — nearly 4,500 half-hour pricebars. Figure 1 shows the market initially rallied into earlyMarch, pulled back, rallied to a higher high in early April,

and then declined into May beforebouncing at the end of the month.

The patternThe pattern used to trigger entries iso-lates bars that establish seven-bar lowsor highs, which are also a certainamount lower or higher than theimmediately preceding low or high.This setup was selected for its simplic-ity, based on observation of severalintraday turning points in March andApril. No effort was made to optimizethe pattern in any way. The patternitself is relatively unimportant; theobject is to see whether its performanceimproves or degrades with the addi-tion of the filter.

The rules for a buy setup are:

1. The low of the current 30-minutebar must be lower than the lows of the previous seven 30-minute bars.

TRADING STRATEGIES

The analysis period spanned Jan. 21 to May 27 and included uptrending anddowntrending price action.

FIGURE 1 — ANALYSIS PERIOD

Source: TradeStation

20 June 2009 • CURRENCY TRADER

Midpoint filter for intraday FXA basic filter technique shows some potential, but it doesn’t solve all the problems.

continued on p. 22

BY CURRENCY TRADER STAFF

TRADING STRATEGIES

2. The current low must be at least 0.12 lower than the previous low.

Formulas for these rules are:

1. Low0 < Lowest(Low1…7);2. Low1-Low0 >= .12

Where the subscripts 0, 1, etc., referto the current bar, 1 bar ago, etc.

The rules are reversed for shortentries:

1. The high of the current 30-minute bar must be higher than the highs of the previous seven 30-minute bars.

2. The current high must be at least 0.12 higher than the previoushigh.

Formulas for these rules are:

1. High0 < Highest(High1…7);2. High1-High0 >= .12

Figure 2 shows several of thesesetup bars, both long and short.

Figure 3 shows the median close-to-close gains or losses for 16 barsafter long and short setups, alongwith the median one- to 16-bar movesfor all 30-minute bars in the analysisperiod. Overall, the dollar-yen pairhad a very mild upward bias duringthis period (black line). Price actionafter buy signals (blue line) wasnotably more bullish, while priceaction after short signals (red line)was erratic, but more bearish than thetypical price action.

The raw signals results are aboutwhat we hoped for (in that they

22 June 2009 • CURRENCY TRADER

Long signals outperformed the market's slight upside bias during the analysisperiod, while short signals were erratic but followed more often by selling thanbuying.

FIGURE 3 — RAW SIGNAL

Entry signals were abundant — perhaps too abundant — during the review win-dow, with more than 700 total signals occurring over the course of four months.

FIGURE 2 — PATTERN SIGNALS

Source: TradeStation

CURRENCY TRADER • June 2009 23

weren’t flat-out wrong), so we pro-ceeded to see if taking trades based onthe previous day’s midpoint mighthelp performance. Some filtering iscertainly necessary, based on the num-ber of trades that were triggered:There were 703 signals (339 long and364 short) in the review period, andgiven the typical gains are not particu-larly large, commissions would nega-tively impact profits disproportionally.

Filtering with the midpoint A midpoint filter rule was applied asfollows:

1. Take long trades only if the closing price of the current 30-minute bar is above the midpoint of the previous day’s range.

2. Take short trades only if the closing price of the current 30-minute bar is below the midpoint of the previous day’s range.

Figure 4 shows how the filtered sig-nals compared with the raw signals.The differences are not dramatic, butthey are evident. For both long andshort signals, improvement is mostnoticeable in the first five bars afterentry, after which results diverge. Thefiltered bullish pattern slightly outper-formed the raw signal for almost theentire 16-bar follow-up period, whilethe filtered short pattern was moreerratic, but still turned lower in thefinal four bars.

Figure 5 compares the winning per-centages of raw and filtered long sig-nals. The filtered signals had higherwinning percentages at 13 of the 16intervals, but the improvement was

not dramatic. The improvement wasmost apparent in the final three bars.(The relatively high winning percent-age for both sets of signals from bar 10to bar 16 — above 60 percent — mightbe surprising, but it is likely a functionof the market’s upward bias duringthis time.)

Figure 6, however, shows the filterhad no real improvement on the win-ning percentage of short trades. Thefilter increased the winning percent-age at half the bar intervals, decreasingthe other half — although theimprovement from bars 13-16 wasnoteworthy.

The most dramatic difference inapplying the filter was in the numberof trade signals, which decreased 68percent to 221 (109 long and 112 short).

Sizing things upAlthough the midpoint filterimproved the trade setup’s overall

continued on p. 24

The filtered long signals outperformed their raw counterparts, while the filteredshort signal performance was mixed. The most notable result of the filter was a68-percent reduction in trade signals.

FIGURE 4 — ALL SIGNALS

24 June 2009 • CURRENCY TRADER

TRADING STRATEGIES

profitability, increased the winningpercentage of long trades, and reducedthe number of trades dramatically, thebenefits were very modest. However,given the large number of trade exam-ples, there is an indication the basictrading approach has some promise.There are a few additional ideas to test,and ways results might be enhanced:

1. Find a better-performing setup pattern. The fact the rules were simply inverted for the long and short sides of the market leaves room for immediate improvement.

Also, the results were based on entering on the close of the signal bar and exiting on the close one to 16 bars later. These rules provided robust results but are likely to provide fertile ground for designing better-performing techniques, not to mention the use of a stop-loss.

2. Both the time frame and filter reference point (the previous day’s midpoint) were representative. In addition to researching other time frames (e.g., trading daily signals using a weekly or monthly filter), other ideas include adjusting the filter level higher or lower based on whether the previous day closed up or down, or to average or weight the midpoints of the past n days.

The challenge is to balance the bene-fits of filtering a signal with theunavoidable compromises.�

The filter had a less-positive effect on the short-trade winning percentage, withthe exception of the final bars.

FIGURE 6 — SHORT ENTRY WINNING PERCENTAGE

The filter improved the winning percentage of long trades, but not dramatically.

FIGURE 5 — LONG ENTRY WINNING PERCENTAGE

ADVANCED STRATEGIES

26 June 2009 • CURRENCY TRADER

How can we describethis sorry decadefor financial mar-kets? A good start

might be, “Everything you knowis wrong.” After all, lower interestrates are supposed to be good forequities, and yet that was dis-proven in both directions. Howabout higher commodity pricesand a weaker dollar being nega-tive for bonds? That didn’t workeither. And the benefits of globaldiversification? Um, no, that justseemed to mean you lost money ina large number of places simulta-neously.

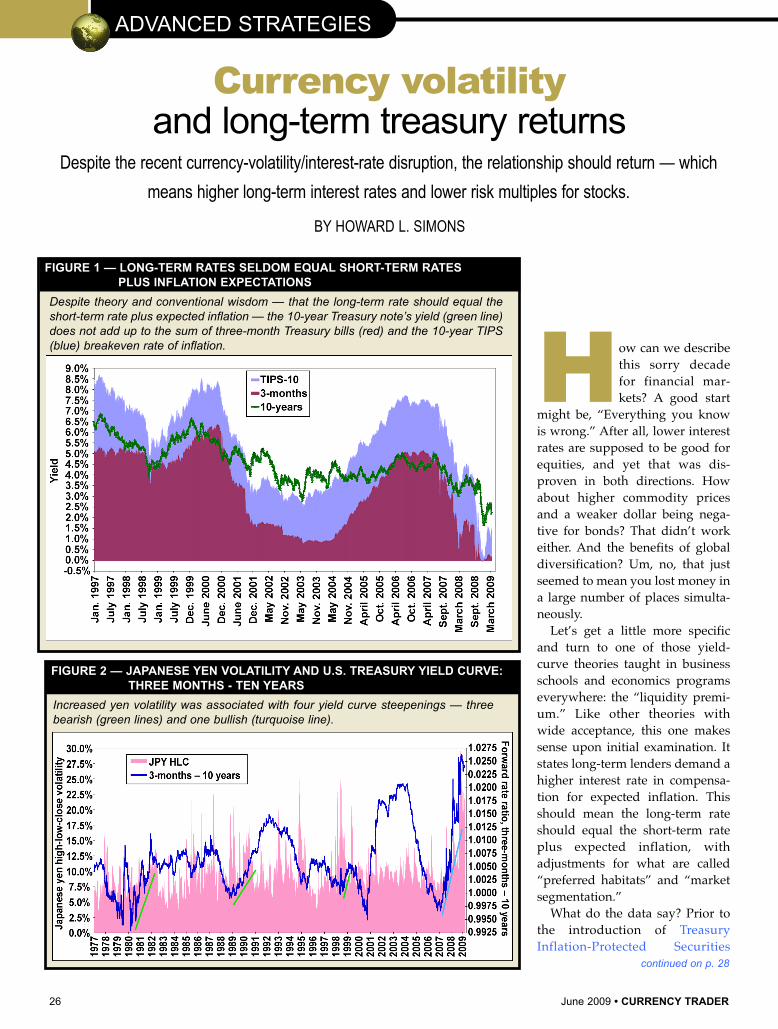

Let’s get a little more specificand turn to one of those yield-curve theories taught in businessschools and economics programseverywhere: the “liquidity premi-um.” Like other theories withwide acceptance, this one makessense upon initial examination. Itstates long-term lenders demand ahigher interest rate in compensa-tion for expected inflation. Thisshould mean the long-term rateshould equal the short-term rateplus expected inflation, withadjustments for what are called“preferred habitats” and “marketsegmentation.”

What do the data say? Prior tothe introduction of TreasuryInflation-Protected Securities

Despite theory and conventional wisdom — that the long-term rate should equal theshort-term rate plus expected inflation — the 10-year Treasury note’s yield (green line)does not add up to the sum of three-month Treasury bills (red) and the 10-year TIPS(blue) breakeven rate of inflation.

FIGURE 1 — LONG-TERM RATES SELDOM EQUAL SHORT-TERM RATES PLUS INFLATION EXPECTATIONS

continued on p. 28

Currency volatility and long-term treasury returns

Despite the recent currency-volatility/interest-rate disruption, the relationship should return — which

means higher long-term interest rates and lower risk multiples for stocks.

Increased yen volatility was associated with four yield curve steepenings — threebearish (green lines) and one bullish (turquoise line).

FIGURE 2 — JAPANESE YEN VOLATILITY AND U.S. TREASURY YIELD CURVE:THREE MONTHS - TEN YEARS

BY HOWARD L. SIMONS

(TIPS) in January 1997, there was noconcrete, market-derived measure ofinflation expectations. The TIPSbreakeven inflation rate, which is thedifference between nominal Treasuryyields and TIPS yields at a givenmaturity, is an imperfect measure (see“TIPS, treasuries and insurance,”Active Trader, May 2008).

Even with that caveat in mind, noone can look at Figure 1 and matchthe 10-year Treasury note’s yield tothe sum of three-month Treasury billsand the 10-year TIPS breakeven rateof inflation. Something other thaninflation expectations must be affect-ing the liquidity premium.

Currency volatilityThe U.S. is highly dependent on for-eign investors to fund its massivetrade and budget deficits. While nei-ther of these deficits affects the dollar

ADVANCED STRATEGIES

Japanese yen HLC volatility rises during a bullish steepening.

FIGURE 3 — JAPANESE YEN VOLATILITY AND U.S. TREASURY YIELD CURVE

as we might think (see “Whatdrives the dollar index?” CurrencyTrader, January 2006), the oppositeis not true. A foreign investor inthe U.S. is long the dollar and willneed to sell those dollars at somepoint in the future.

Two risk factors arise for theforeign investor in the U.S. Thefirst and most straightforward isthe risk of dollar depreciationover time. That risk, which hasbeen realized many times overthe entire floating exchange-rateera, can be hedged using knowntechniques and instruments.

The second risk is less straight-forward but just as real: high cur-rency volatility. Even within a long-term static trend, suchas the one between the dollar and the Japanese yen betweenlate 1999 and mid-2008, higher volatility raises the disper-sion of outcomes for the ultimate repatriation of funds —that is, higher currency volatility is a risk for investors, and

for bond investors that risk must be accounted for in lowerprices and higher yields.

If this is indeed the case, we should be able to see somemeasure of a long-term relationship between the liquidity

continued on p. 30

The Swiss National Bank has been far less interventionist than the Bank of Japan, pro-viding a cleaner picture of its effects on the FRR between three months and 10 years.

FIGURE 4 — SWISS FRANC VOLATILITY AND U.S. TREASURY YIELD CURVE:THREE MONTHS - TEN YEARS

30 June 2009 • CURRENCY TRADER

ADVANCED STRATEGIES

premium and currency volatility. Let’s examine the long-term high-low-close volatility (HLC) for the Japanese yenand the Swiss franc, going back to 1977. Japan has been animportant creditor to the U.S. for the past three decades.The Swiss franc was chosen because it has a continuous his-tory uninterrupted by the advent of the Euro. HLC volatil-ity is defined as:

where N is the number of days between 4 and 29 thatminimizes the function:

HLC volatility will be mapped against the yield curveover three different segments: three months against 10years, one year against 10 years, and two years against 10years. The Federal Reserve’s constant-maturity measuresfrom the H15 report are used for the interest-rate data at thenote horizons.

The the yield curve’s shape will be normalized by the for-ward rate ratio (FRR) between the maturity pairs. The FRRis the forward rate between two bonds divided by the yieldof the longer-dated instrument. For example, the FRRbetween two and 10 years is the rate at which we can lockin borrowing for eight years starting two years from now,divided by the 10-year rate itself. The more a FRR exceeds1.00, the steeper the yield curve is; a FRR less than 1.00denotes an inverted yield curve.

The yen and the yield curveMuch of the trade in the yen during recent years has beendriven by the yen carry trade, the borrowing of low-interestyen to lend elsewhere (see “A closer look at the carry

trade,” Currency Trader, June2007). Whenever the Bank ofJapan threatens to tighten creditor whenever the world’sinvestors flee risk, as happenedin late 2008 and early 2009, theyen strengthens and its volatilityjumps.

A policy response by theFederal Reserve often is associat-ed with this trade; it certainlywas after the onset of the creditcrunch in August 2007. This isnot, however, a rule. Yen volatili-ty spikes during the late 1980s, in1995, and during the 1998 LongTerm Capital Management crisis,occurred within the context of aflattening yield curve. Both theFederal Reserve and the Bank ofJapan were trying either to stemthe dollar’s slide, the yen’s rise,or both, during these episodes.

Let’s map the yen’s HLCvolatility against the three FRRsmentioned above. First, let’s lookat the FRR between three-monthTreasury bills and 10-yearTreasury notes (Figure 2). Threeperiods of a bearish steepening

The FRRs starting at one and two years track Swiss franc HLC volatility similarly to yenHLC volatility. The relationship during the bullish 2007-2008 steepening is especially strong.

FIGURE 5 — SWISS FRANC VOLATILITY AND U.S. TREASURY YIELD CURVE

continued on p. 32

• Gain perspectives, advice, and learn the latesttrends in our TRADING STRATEGIES ANDTECHNIQUES; STOCKS, OPTIONS, AND ETFS;and FUTURES, COMMODITIES, AND FOREXsections

• Watch on-demand video WEBCASTS from toptraders as they share their strategies and tips ontoday’s markets

• Utilize trading TOOLS to help you research andrefine your trading strategies and decisions

• Sign up for free TRADING e-letters and daily alertsand receive innovative trading tips and proventechniques straight to your inbox

…and much, much more!

Discover why

is a leading destination forthe latest content fromtrading experts.

MoneyShow.com ProvidesExpert Trading Insights YouCan Profit From:

www.MoneyShow.comPowerful and Profitable Advice Directly from Experts, 24/7

Githler Center | 1258 North Palm Avenue | Sarasota, FL 34236-3604800/970-4355 | www.InterShow.com

Priority code 013315

Active_Trader-Ad-MS_com:Layout 1 12/16/08 3:52 PM Page 1

32 June 2009 • CURRENCY TRADER

of the yield curve — that is, a steeper yield curve driven byrising long-term rates — are marked with green lines. Afourth, marked with a turquoise line, is the 2007-2008 bull-ish steepening. All are associated with increases in yen HLCvolatility.

We should not expect the effect to be as pronounced dur-ing bearish steepenings for the other two FRRs, thosebetween one- and two-year notes on the short end and 10-year notes on the long end (Figure 3): If 10-year note yieldsare rising during periods of rising inflation, rising econom-ic growth or both, the incentives to maintain yen carrytrades are high. However, we should expect yen HLCvolatility to rise during a bullish steepening, one defined bya change in American monetary policy and one where thedollar’s interest-rate advantage to the yen may be decreas-ing. That is the case for both of these FRRs.

The Swiss franc and the yield curveThe Swiss franc’s HLC volatility history has differed con-siderably from the yen’s. It reached its highs during thestrong inflation of the late 1970s and early 1980s as theworld sought refuge in the franc, so much so the Swissimposed an interest-rate penalty on foreign deposits (see“Franc-ly my dear, I don’t give a carry,” and “The Swissfranc’s commodity connection,” September and October

2008, respectively). Because the franc is a funding currencyfor carry trades, its HLC volatility rose after the onset of the2007 credit crunch as these positions were unwound.

As the Swiss National Bank has been far less interven-tionist over the years than the Bank of Japan, we should geta cleaner picture of its effects on the FRR between threemonths and 10 years, and we do (Figure 4). The same com-ments made for yen HLC volatility apply and the chart ismarked identically to Figure 2.

In Figure 5, the FRRs starting at one and two years trackfranc HLC volatility similarly to yen HLC volatility inFigure 3, and for the same reason. The relationship duringthe bullish steepening of 2007-2008 is especially strong.

Implications for long-term Treasury returnsIf rising currency volatility steepens the yield curve and ifthe best time to buy bonds is when the yield curve is flat toinverted, it should stand to reason a combination of highcurrency volatility and a steep yield curve should lead topoor returns on 10-year Treasury notes.

We can gauge this effect visually by mapping three-month-ahead returns on 10-year T-notes against the threeFRRs and each currency’s HLC volatility. In Figure 6, posi-tive returns are marked with blue bubbles and negativewith white; the size of each bubble corresponds to the mag-

Positive returns are marked with blue bubbles, negative returns with white; the size of each bubble represents the magnitude of the return.

FIGURE 6 — THREE-MONTH AHEAD PERCENTAGE RETURNS ON TEN-YEAR TREASURIES:AS FUNCTION OF JAPANESE YEN AND SWISS FRANC VOLATILITY AND FORWARD RATE RATIO

continued on p. 34

Attend and Take Home Valuable Expert Knowledgeon How to:• Recognize which option strike price and expiration month to buy or sell• Find the right currency pairs to offer you the most upside during specific

news announcements• Minimize your risk and determine profit and stop levels before every trade• Determine which currency pairs offer the best "carry trade" interest• Enhance your trade accuracy using the latest tools and software• Read the underlying psychology of the markets to determine which

currency pair to buy or sell

Platinum Sponsors Media PartnerGold Sponsors

Githler Center • 1258 North Palm Avenue • Sarasota, FL 34236-5604800/226-0323 • www.MoneyShow.com

a Production of

www.FXandOptionsExpo.comDiscover complete Expo details, learn how to attend,

and register free online. Or, call 800/970-4355.Mention priority code 014538.

Las Vegas | August 2-4, 2009Caesars Palace

Discover Dozens of Forex and Options Strategies from Profitable Traders

Attend and Gain the Ultimate Insight on Today'sMarket Trends for Forex and Options Traders

Dan Gramza Jon Najarian Guy Adami Kathy Lien Rob Booker Cornelius Luca

Confirmed Speakers Include:

and many more!

and much more!

Currency_Trader_Ad-LVFX09:Layout 1 5/21/09 12:57 PM Page 1

34 June 2009 • CURRENCY TRADER

nitude of the return. The green horizontal and vertical linesmark the values on March 23, 2009.

If the conjecture is true, we should see a preponderanceof white bubbles — negative three-month-ahead returns —in the upper right corner of each bubble cluster. Prior to theextreme dislocations in both currency and bond marketsstarting in September 2008, the upper right edges of theclusters had been largely white. This changed once the yencarry trade started to unwind; the jump in yen volatilitycombined with a flight into U.S. Treasuries pushed theupper-right corner into a zone of positive forward returnsfor the yen (top).

A different situation prevailed for the Swiss franc (bot-tom). Here the upper-right corner became largely empty,but the forward Treasury returns in the lower-left cornerturned negative. What we have here is one more instance of

a long-term relationship reversing under extreme financialstress.

The long-term verity that higher currency volatility leadsto steeper yield curves, and ultimately to negative returnson bonds, has been challenged by the 2008-2009 financialupheavals. We should expect this relationship to return,and lead to higher long-term interest rates. These higherinterest rates in turn lower risk multiples for stocks andraise the cost of capital throughout the economy.

This lesson should have been learned by policymakers inthe 1970s. If it was, it has been forgotten, and the long-termconsequences will be as negative now as they were between1971 and 1982.�

For information on the author see p. 6.

“A cross-rate to bear”Currency Trader, May 2009.The Euro/yen pair isn’t just a currency cross-rate — it’s agauge of global risk.

“And it’s one, two, three — what are we trading for?”Currency Trader, April 2009.They don’t call them frontier markets for nothing. A look atVietnam’s currency and stock market over the past fewyears.

“Sovereign credit risk and currencies”Currency Trader, March 2009.Government actions are perversely rewarding the guilty: Asa nation’s credit rating deteriorates, its borrowing costs falland its currency, at least temporarily, rises.

“Minor trends make minor friends”Currency Trader, February 2009.Do minor currencies offer trading opportunities the majorsdon’t? Find out what the numbers say.

“Let the trend be your friend: The majors”Currency Trader, January 2009.If currencies trend so much, why do trend followers usuallyhave such blah performance? This and other questions areanswered in this study of currency trends.

“The rupee and emerging markets”Currency Trader, December 2008.Analysis suggests India’s status as a global economicpower is no accident.

“Nordic currency confusion”Currency Trader, November 2008.Get a handle on the dynamics of the Northern European currencies.

“The Swiss franc’s commodity connection”Currency Trader, October 2008.How can the Swiss currency be, of all things, a commodity currency?

“Franc-ly, my dear, I don’t give a carry” Currency Trader, September 2008.Investigating the Swiss franc carry trade, and what mightchange its dynamics.

“The short, awful life of the dollar carry trade” Currency Trader, August 2008.The implications of the weak-dollar policy and the dollar’s role asa funding currency.

“Getting carried away with the kiwi” Currency Trader, July 2008.What’s driving the New Zealand dollar, and how long is it likely tolast?

“Currencies and commitments” Currency Trader, June 2008.Find out what COT data conveys about forex price action.

“Currencies and stock-index performance” Currency Trader, April 2008.Find out how stock indices relate to the performance of their currencies.

“Howard Simons: Advanced Currency Concepts, Vol. 1”A discounted collection that includes many of the articles listedhere.You can purchase and download past articles at

http://store.activetradermag.com

Related reading:Other Howard Simons articles

ADVANCED STRATEGIES

BY CHRIS PETERS

36 June 2009 • CURRENCY TRADER

On July 31 the National Futures Association (NFA),the self-regulatory body which oversees most forex

dealers in the U.S., will implement a rule disallowing NFA-registered forex traders from holding two offsetting posi-tions in the same account. This means traders using a tech-nique called “hedging,” in which an equal but oppositeposition is entered in the same currency pair to essentiallyfreeze an existing profit or loss, will instead have their ini-tial position closed out when the second order is entered.

While the efficacy of this technique is highly debatable, arepresentative from one major forex dealer says traders are

fleeing U.S. dealers in droves, transferring accounts to deal-ers in the UK and elsewhere.

But while there is outcry against the NFA dictating whattechniques a trader can and can’t use, one stipulation in therule that has so far flown under the radar could potentiallyhave much larger implications for all U.S. forex traders,especially those simultaneously running multiple strategies.The NFA has said not only must forex dealers close out off-setting positions, but orders must be closed on a first-in-first-out (FIFO) basis. FIFO is common in futures and equitymarkets, but is a completely new concept for forex dealers,

so much so that many will need to signifi-cantly alter their trading platform technolo-gy. The new rule, which was initially sched-uled to take effect on May 15, was pushedback to July at the request of the dealers whoclaimed they needed more time to re-pro-gram their platforms.

Automated troubleThe new FIFO requirements could signifi-cantly impact traders who use automatedalgorithmic trading strategies, especiallythose using multiple strategies. FIFO couldpotentially disrupt these strategies becausea specific stop or limit could no longer beattached to a specific order. If a stop-loss ishit, for example, it must be executed againstthe first opened position. So, if two differentstrategies enter trades in the same currencypair, one after the other, and the secondstrategy then signals an exit but the firstdoes not, the first strategy’s position will beclosed.

One way around this could be setting upseparate accounts for different strategies(which could also be a way for traders tocontinue using the hedging technique). Butas one forex brokerage representative said,while some dealers are promoting this as analternative, others are wary of suggesting itbecause it goes against the intent of theNFA’s rule.

The issue could also potentially bebypassed through the use of more compli-cated order types such as one-cancels-the-other (OCO). However, many forex dealers

FOREX NEWS

FIFO mandate causes headaches for U.S. FX dealersWhile the ban on forex hedging has some forex traders grumbling, first-in-first-out

could have even greater implications on trading strategies.

Managed money: Barclay Trading Group’s currency trader rankings for April 2009

Top 10 currency traders managing more than $10 million as of April 30, ranked by April 2009 return.

2009 $ UnderRank Trading April YTD mgmt.

advisor return return (millions)

1. 24FX Management Ltd 7.00% 12.06% 25.1

2. Alder Cap'l (Alder Global 20) 3.40% 12.27% 192.6

3. Hathersage (Daily Currency) 3.11% 5.17% 119.9

4. Quiddity (FX) 3.00% 5.43% 10.0

5. Stonehenge Capital Mgmt (CM1) 2.40% 5.92% 32.0

6. Geo Economic Mgmt. System Ltd 2.27% 9.51% 37.5

7. King's Crossing Cap'l (FX Model) 1.93% -2.03% 48.0

8. Harmonic Capital (Gl. Currency) 1.83% -1.28% N/A

9. arsago Premium Currencies 1.71% 6.70% 525.0

10. Metro Forex Inc (Tri Gl FX) 1.42% 5.35% 105.3

Top 10 currency traders managing less than $10 million and more than $1 million as of April 30, ranked by April 2009 return.

1. Sagacity (HedgeFX100) 3.33% 14.28% 1.3

2. Blue Fin Capital (Managed Currency) 3.16% 3.74% 1.6

3. Wealth Builder FX Group 3.00% 40.27% 5.1

4. Absolute Asset Mgmt (Trading 1) 2.48% 0.58% 3.6

5. Drury Capital (Currency) 2.12% -0.17% 3.6

6. Overlay Asset Mgmt. (Emerging Mkts) 1.76% -3.82% 1.1

7. Coral Rock Investments (Institutional) 1.17% 0.77% 4.0

8. Marek D. Chelkowski (Forex) 1.00% 2.68% 2.1

9. H3 Global Advisors (Currency) 0.83% -4.37% 4.7

10. Cambridge Strategy (Dev. Markets) 0.50% -1.10% 5.0

Source: BarclayHedge (http://www.barclayhedge.com). Based on estimates of the composite of allaccounts or the fully funded subset method. Does not reflect the performance of any single account.PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE PERFORMANCE.

CURRENCY TRADER • June 2009 37

LEGEND:

Volume: 30-day average daily volume, in thousands.

OI: 30-day open interest, in thousands.

10-day move: The percentage price move from theclose 10 days ago to today’s close.

20-day move: The percentage price move from theclose 20 days ago to today’s close.

60-day move: The percentage price move from theclose 60 days ago to today’s close.

The “% rank” fields for each time window (10-daymoves, 20-day moves, etc.) show the percentile rankof the most recent move to a certain number of theprevious moves of the same size and in the same

direction. For example, the % rank for 10-day moveshows how the most recent 10-day move compares tothe past twenty 10-day moves; for the 20-day move,the % rank field shows how the most recent 20-daymove compares to the past sixty 20-day moves; forthe 60-day move, the % rank field shows how the mostrecent 60-day move compares to the past one-hun-dred-twenty 60-day moves. A reading of 100% meansthe current reading is larger than all the past readings,while a reading of 0% means the current reading islower than the previous readings.

Volatility ratio/% rank: The ratio is the short-termvolatility (10-day standard deviation of prices) divided

by the long-term volatility (100-day standard deviationof prices). The % rank is the percentile rank of thevolatility ratio over the past 60 days.

CURRENCY FUTURES SNAPSHOT as of May 27

The information does NOT constitute trade signals. It is intended only to provide a brief synopsis of each market’sliquidity, direction, and levels of momentum and volatility. See the legend for explanations of the different fields.

Market Symbol Exchange Volume OI 10-day move/% rank 20-day move/% rank 60-day move/% rank Volatility ratio/rankEurocurrency EC CME 166.5 114.0 2.05% / 32% 5.86% / 72% 10.71% / 100% .51 / 88%British pound BP CME 79.8 86.4 5.07% / 88% 9.75% / 100% 14.31% / 100% .67 / 100%Japanese yen JY CME 77.4 80.6 1.23% / 15% 1.23% / 25% 2.68% / 7% .17 / 18%Canadian dollar CD CME 54.2 69.8 4.20% / 63% 9.33% / 100% 15.47% / 100% .62 / 83%Australian dollar AD CME 48.4 77.5 2.41% / 21% 10.83% / 93% 24.06% / 100% .29 / 28%Swiss franc SF CME 33.8 31.2 1.70% / 21% 5.15% / 91% 8.31% / 100% .52 / 90%Mexican peso MP CME 10.0 46.4 0.33% / 8% 5.41% / 57% 17.18% / 100% .21 / 22%U.S. dollar index DX ICE 5.4 24.3 -2.67% / 40% -5.01% / 86% -9.67% / 98% .53 / 83%New Zealand dollar NE CME 2.3 16.4 2.15% / 6% 10.82% / 69% 25.51% / 100% .37 / 65%E-Mini eurocurrency ZE CME 2.2 1.9 2.05% / 32% 5.86% / 72% 10.71% / 100% .51 / 88%Note: Average volume and open interest data includes both pit and side-by-side electronic contracts (where applicable). Price activity is based on pit-traded contracts.

This information is for educational purposes only.Currency Trader provides this data in good faith, butassumes no responsibility for the use of this infor-mation. Currency Trader does not recommend buy-ing or selling any market, nor does it solicit orders tobuy or sell any market. There is a high level of riskin trading, especially for traders who use leverage.The reader assumes all responsibility for his or heractions in the market.

do not currently offer these types oforders and would need to programthem from the ground up.

Also, the stated intention of the ruleis to protect inexperienced traders whomay not realize that entering a hedgeposition will incur extra costs (i.e.,extra commissions), which ultimatelybenefits the forex dealer. But becauseof FIFO, those who choose to run, forexample, a long-term and a short-termstrategy in the same pair, may need touse more sophisticated and complextrade management techniques to doso.

Platform adjustmentsForex dealers are scrambling to makethe necessary changes to their plat-forms, which is one reason they arestill (mostly) remaining quiet aboutFIFO’s implications. Because thefuture of the U.S. forex market is stilluncertain, dealers are reluctant to rockthe boat too much — at least not untilthey have adjusted their platforms forthe new rules.

For many dealers, this may meanthey will need to offer two separate

platforms: one for U.S. customers andone for non-U.S. customers. For a plat-form such as Metatrader 4, made byMetaQuotes software, a non-U.S. com-pany which has offices in Russia,Cyprus, and Singapore, it is unclearwhether it will implement any changesat all, which could cause problems forU.S. customers who use the platform.A spokesman at the company’s UKcontact number was unaware of theNFA rule and said it’s possible theymay address the issue in Metatrader 5,scheduled for release in the fall.

Some forex brokerages see the FIFOrequirement, along with the ban onoffsetting positions, as something thatwill make U.S. dealers less competitiveinternationally. One dealer suggeststhe NFA make some concessionaryrules, such as guaranteed positive slip-page on limit orders, to balance out thecomplicated new rules. Although thiscould cause dealers to take a hit onprofits, it would help them retain cus-tomers by providing an advantageover non-U.S. dealers elsewhere in theworld. The NFA did not returnrequests for comment.�

INTERNATIONAL MARKETS

Currentprice vs. 1-month 3-month 6-month 52-week 52-week Previous

Rank* Country Currency U.S. dollar gain/loss gain/loss gain/loss high low rank

1 British pound 1.59001 8.12% 10.16% 4.73% 2.0148 1.3501 10

2 Swedish krona 0.13375 8.09% 18.38% 6.25% 0.1701 0.1068 15

3 Australian dollar 0.78104 8.06% 20.03% 21.00% 0.9849 0.6005 3

4 New Zealand dollar 0.61845 8.02% 20.31% 13.68% 0.7921 0.4892 14

5 Canadian dollar 0.88965 7.65% 10.90% 9.85% 1.0176 0.7653 5

6 Brazilian real 0.49474 7.48% 17.74% 14.37% 0.6414 0.3751 4

7 Russian ruble 0.03232 6.07% 15.31% -11.62% 0.04334 0.02695 6

8 South African rand 0.12069 6.00% 19.71% 20.44% 0.1391 0.0841 1

9 Euro 1.40041 5.73% 9.30% 8.46% 1.6038 1.2329 17

10 Indian rupee 0.0212 5.37% 5.84% 5.89% 0.03974 0.01843 2

11 Swiss franc 0.92226 5.10% 7.13% 10.34% 0.9987 0.813 16

12 Taiwanese dollar 0.03072 3.36% 6.52% 2.40% 0.03312 0.02835 11