current developments on the global commercial … commercial vehicles... · current developments on...

TRANSCRIPT

Current Developments on theGlobal Commercial Vehicle Market

Prof. Dr. Bernd GottschalkPresidentGerman Association of the Automotive Industry (VDA)

International Press Workshop “Commercial Vehicles – A Mobile Future”9 July 2004, Frankfurt/Main

Commercial Vehicle Markets

I. Global

II. Germany

page 3

page 41

I. Global Commercial Vehicle Markets- Overview- by Region

- North America- South America- Asia- Eastern Europe- Western Europe

page 4

page 10

page 12

page 15

page 21

page 28

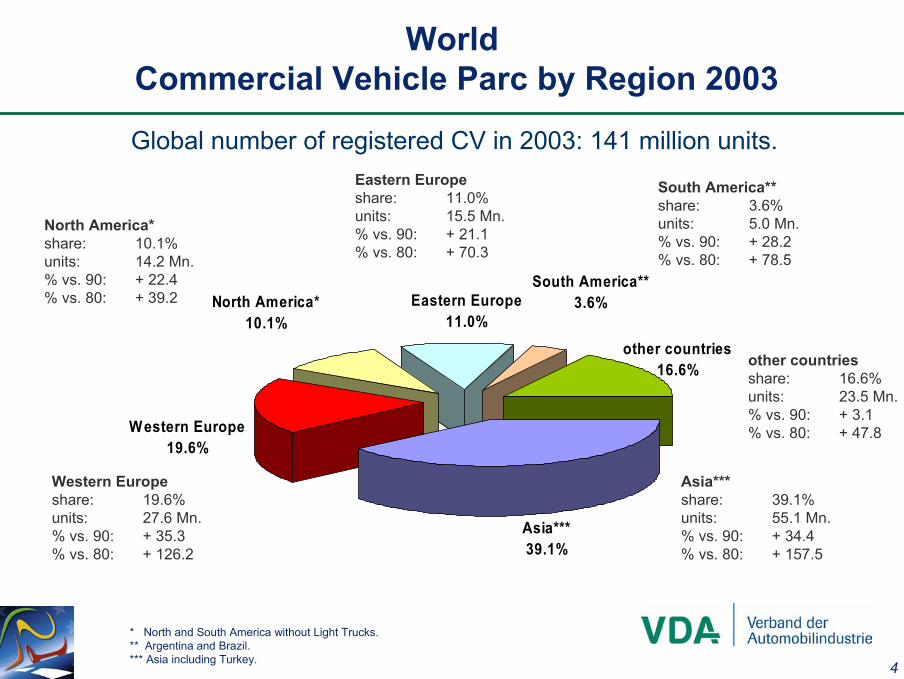

4

Asia***39.1%

Western Europe19.6%

other countries16.6%

South America**3.6%Eastern Europe

11.0%North America*

10.1%

WorldCommercial Vehicle Parc by Region 2003

Global number of registered CV in 2003: 141 million units.

North America* share: 10.1%units: 14.2 Mn.% vs. 90: + 22.4% vs. 80: + 39.2

Eastern Europeshare: 11.0%units: 15.5 Mn.% vs. 90: + 21.1% vs. 80: + 70.3

South America**share: 3.6%units: 5.0 Mn.% vs. 90: + 28.2% vs. 80: + 78.5

Asia***share: 39.1%units: 55.1 Mn.% vs. 90: + 34.4% vs. 80: + 157.5

Western Europeshare: 19.6%units: 27.6 Mn.% vs. 90: + 35.3% vs. 80: + 126.2

other countriesshare: 16.6%units: 23.5 Mn.% vs. 90: + 3.1% vs. 80: + 47.8

* North and South America without Light Trucks.** Argentina and Brazil.*** Asia including Turkey.

5

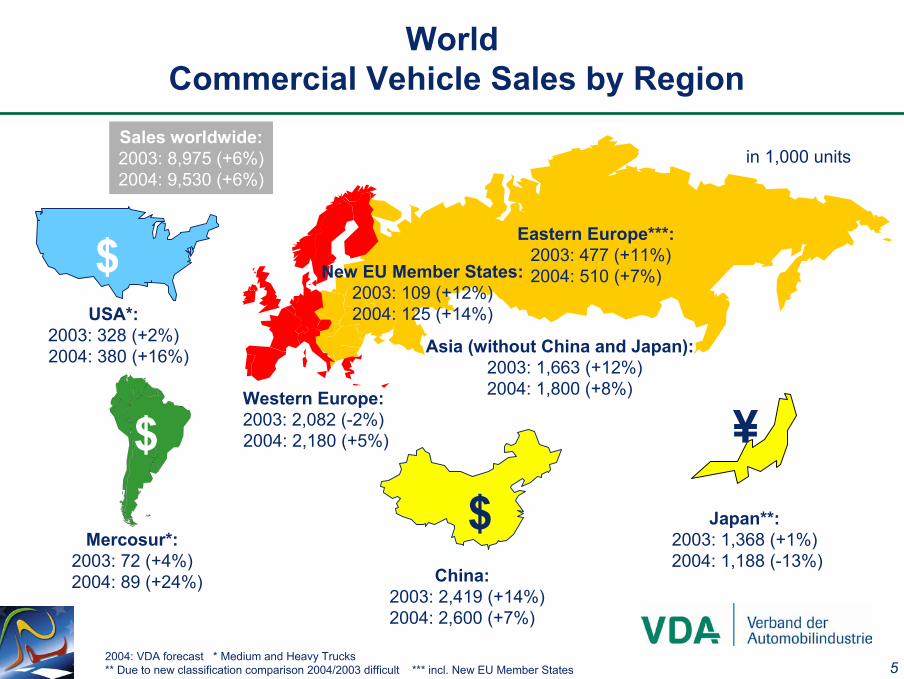

WorldCommercial Vehicle Sales by Region

Sales worldwide:2003: 8,975 (+6%)2004: 9,530 (+6%)

Sales worldwide:2003: 8,975 (+6%)2004: 9,530 (+6%)

USA*:2003: 328 (+2%)2004: 380 (+16%)

$

Japan**:2003: 1,368 (+1%)2004: 1,188 (-13%)

¥

China:2003: 2,419 (+14%)2004: 2,600 (+7%)

$Mercosur*:

2003: 72 (+4%)2004: 89 (+24%)

$Western Europe:2003: 2,082 (-2%)2004: 2,180 (+5%)

Asia (without China and Japan):2003: 1,663 (+12%)2004: 1,800 (+8%)

Eastern Europe***:2003: 477 (+11%)2004: 510 (+7%)

in 1,000 units

2004: VDA forecast * Medium and Heavy Trucks ** Due to new classification comparison 2004/2003 difficult *** incl. New EU Member States

New EU Member States:2003: 109 (+12%)2004: 125 (+14%)

6

WorldCommercial Vehicle Production by Region

Worldin Mn share in % in Mn share in % in Mn share in % in Mn share in % in Mn share in % in Mn

1980 1.6 21.1 0.3 3.9 3.9 51.3 0.2 2.6 1.6 21.1 7.6

1985 1.4 17.0 0.3 3.6 4.6 56.2 0.4 4.9 1.5 18.3 8.2

1990 1.8 22.0 0.2 2.4 3.5 42.7 0.6 7.2 2.2 26.5 8.3

1995 1.8 21.9 0.4 4.9 2.6 31.7 1.1 13.4 2.3 28.1 8.2

2000 2.3 25.9 0.4 4.5 1.8 20.0 1.5 16.9 2.9 32.7 8.9

2003 2.1 23.1 0.3 3.3 1.8 19.8 2.4 26.4 2.5 27.4 9.1

2005 2.2 21.6 0.4 3.9 1.9 18.6 3.0 29.4 2.7 26.5 10.2

2010 2.3 19.1 0.5 4.3 2.0 17.0 4.0 34.0 3.0 25.6 11.8

other countriesWestern Europe USA* Japan China

* Medium- and Heavy-Trucks.

7

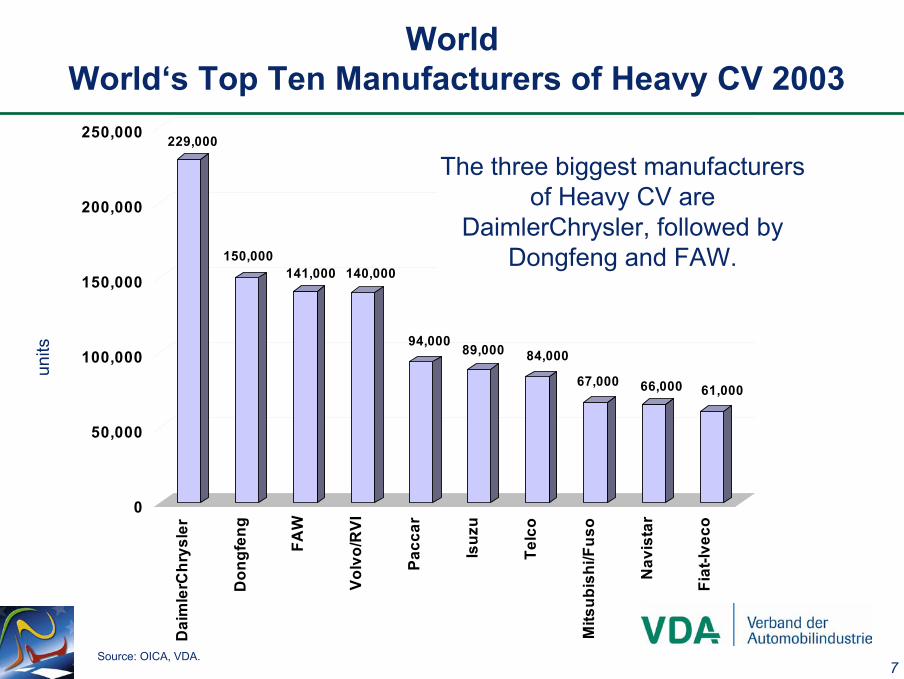

WorldWorld‘s Top Ten Manufacturers of Heavy CV 2003

229,000

150,000141,000 140,000

94,000 89,000 84,000

67,000 66,000 61,000

0

50,000

100,000

150,000

200,000

250,000

Dai

mle

rChr

ysle

r

Don

gfen

g

FAW

Volv

o/R

VI

Pacc

ar

Isuz

u

Telc

o

Mits

ubis

hi/F

uso

Nav

ista

r

Fiat

-Ivec

o

units

Source: OICA, VDA.

The three biggest manufacturers of Heavy CV are

DaimlerChrysler, followed by Dongfeng and FAW.

8

WorldWorld‘s Top Ten Manufacturers of Heavy Buses 2003

28,000

13,000 13,00011,000

7,000 7,000 7,0006,000 6,000

4,000

0

5,000

10,000

15,000

20,000

25,000

30,000

Dai

mle

rChr

ysle

r

Telc

o

Ash

ok L

eyla

nd

FAW

Volv

o

Don

gfen

g

Hyu

ndai

-Kia

Neo

man

Irisb

us

Cha

ngjia

ng B

us

units

Buses over 8 t.Source: OICA, VDA.

DaimlerChrysler held its rank as the leading

manufacturer of heavy buses in 2003.

9

Karosa(Czech Rep.)

Trends towards Globalisation amongstthe Most Important Commercial Vehicle Manufacturers

MitsubishiMotors Corp. 37.3%

Volkswagen

Scania34.0%

Toyota

Hino50.1%

Daihatsu100%

Seat100%

Sisu

Navistar Tatra

HyundaiMotor Company

Kia44.0% Asia Motors

10%

4.4%

DaimlerChrysler

FreightlinerMercedes-BenzEvoBus

Western Star

Orion Americanla France

SterlingSetra Mercedes-Benz

Dodge

PACCAR

DAFLeyland Trucks

FodenTrucks

KenworthTruck

PeterbiltMotors

Ford

Mazda33.4%

Getrag FordTransmission

Nissan Motors

44.6%

23.2%

15%

Cooperation

Astra(Italy)

Naveco(China)

IvecoMagirus

Irisbus

Uralaz(Russia)

Fiat

IvecoEurofire

Iveco InternationalTrucks Australia

Iveco FordTruck

IvecoPegaso

Iveco FiatBrazil

Ssangyong

GM-Daewoo42.1%

Mitsubishi FusoTruck and Bus

Corp.

65.0%

20.0% Daimler HyundaiTruck Corp.

50.0%

AshokLeyland

15%

Source: company data, VDA, Globalinsight

Askam Kamyon(Turkey)BMC

(Turkey)

Levend(Turkey)

Eicher(India)

FAW (Jiefang)

VWdo Brazil

General Motors

Fuji HeavyInd. (20%)

Suzuki20%

Isuzu12%

Vauxhall/Opel100%

IBC100%

Holden

AB Volvo

RenaultTrucks

MackTrucks Volvo BusVolvo Trucks

20%

Renault V.I.

22.5%

Nissan Diesel Dacia100%

Terberg(NL)

33.3%

PSA

Peugeot Citroën

Iveco

LDV (UK)

ZIL (Russia)

GAZ (Russia)

Ikarus BusHeuliez Bus50%

Haveco(China)

50%Otoyol

(Turkey)

27%

97.5%Atlas vehicles

(Marocco)

49%Dongfeng

MAN

ERFÖAF Star SteyrNEOMAN

Neoplan Bus MAN Bus

TFM Bus& Coaches

ZhengzhouYutong BusMAZ

MAN Truck &Bus China

10

-41.0-37.5

-32.6

-20.2 -19.1

-1.9

28.7

13.1

-9.4-3.0

-9.9

10.4

57.8

46.5

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

1.Q. 0

1

2.Q. 0

1

3.Q. 0

1

4.Q. 0

1

1.Q. 0

2

2.Q. 0

2

3.Q. 0

2

4.Q. 0

2

1.Q. 0

3

2.Q. 0

3

3.Q. 0

3

4.Q. 0

3

1.Q. 0

4Ja

n.-May

04

USASales of Heavy-Trucks

chan

geon

pre

viou

sye

arin

per

cen

t

Sales of Heavy-TrucksJan.-May 2004: 72,654Jan.-May 04/03: + 46.5%

Sales of Heavy-TrucksJan.-May 2004: 72,654Jan.-May 04/03: + 46.5%

Clear rebound of U.S.-Heavy-Truck sales 2004

11

107,

433

118.

204 13

1,71

2

11,432

13,223

15,486

17,408

18,015

24,863

136,

273

130,

638

172,

061

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

USA Canada Mexico NAFTA

1-5/2002 1-5/2003 1-5/2004

North AmericaProduction of Medium- and Heavy-Trucks 2004

units

1-5/2004: 131,712change vs. 1-5/03: + 32.5%change vs. 1-5/02: + 22.6%

1-5/2004: 172,061change vs. 1-5/03: + 31.7%change vs. 1-5/02: + 26.2%

1-5/2004: 15,486change vs. 1-5/03: + 17.1%change vs. 1-5/02: + 35.5%

1-5/2004: 24,863change vs. 1-5/03: + 38.0%change vs. 1-5/02: + 42.8%

The production of Medium-and Heavy-Trucks in NAFTA countries increased by 26 per cent in the last two years.

12

30.7

10.2

-13.9

-19.3 -19.5-17.2

-13.7

4.6

22.7

-0.3

15.7

25.2

21.2

30.7

-20

-10

0

10

20

30

40

1.Q. 0

1

2.Q. 0

1

3.Q. 0

1

4.Q. 0

1

1.Q. 0

2

2.Q. 0

2

3.Q. 0

2

4.Q. 0

2

1.Q. 0

3

2.Q. 0

3

3.Q. 0

3

4.Q. 0

3

1.Q. 0

4Ja

n.-May

04

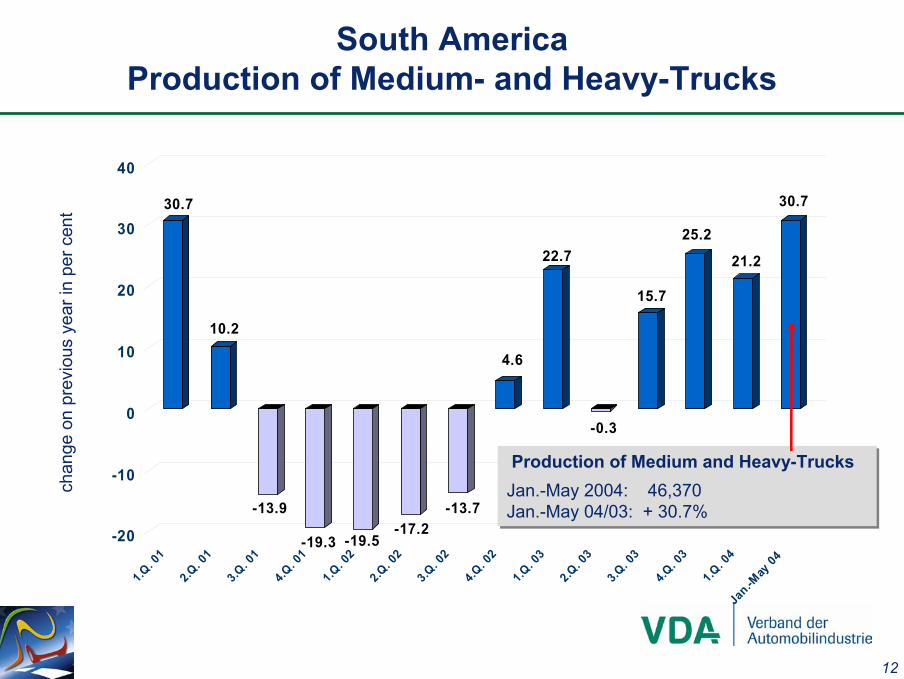

South AmericaProduction of Medium- and Heavy-Trucks

chan

geon

pre

viou

sye

arin

per

cen

t

Production of Medium and Heavy-TrucksJan.-May 2004: 46,370 Jan.-May 04/03: + 30.7%

Production of Medium and Heavy-TrucksJan.-May 2004: 46,370 Jan.-May 04/03: + 30.7%

13

After the market slumped by more than 75 per cent from 2000 to 2002 sales of medium and heavy trucks are on the rise again.

South AmericaSales of Medium- / Heavy-Trucks in Argentina

Einheiten 04 / 03 Einheiten 04 / 03Mercedes-Benz 429 382.0 1,985 451.4 32.6 24.9 Volkswagen 150 72.4 1,037 229.2 17.0 21.8 Total German Trucks 579 229.0 3,022 347.7 49.6 46.6 Ford 319 293.8 1,878 528.1 30.8 20.7 GM 0 - 0 - 0.0 0.0 Iveco 202 155.7 697 98.0 11.4 24.3 Scania 96 638.5 365 1303.8 6.0 1.8 Sonstige 25 66.7 135 42.1 2.2 6.6

Total Trucks 1,221 235.4 6,097 321.4 100.0 100.0

Medium and Heavy Trucks

May January - May % market share (Jan.-May)2004 2003

Source: Adefa.

14

South AmericaSales of Medium- / Heavy-Trucks in Brazil

Einheiten Einheiten

Mercedes-Benz 921 8.1 4,374 9.7 29.2 28.8 Volkswagen 1,044 11.4 4,901 - 2.1 32.7 36.2 Total German Trucks 1,965 9.8 9,275 3.1 61.8 65.0 Agrale 69 30.2 262 - 3.7 1.7 2.0 Fiat 117 317.9 254 71.6 1.7 1.1 Ford 900 16.0 4,183 11.3 27.9 27.1 GM 1 - 1 - 0.0 0.0 PSA 10 25.0 56 100.0 0.4 0.2 Iveco 180 36.4 968 50.8 6.5 4.6

Total Medium Trucks 3,242 16.4 14,999 8.4 100.0 100.0

Einheiten Einheiten

Mercedes-Benz 1,245 16.2 5,913 24.2 32.4 35.0 Volkswagen 1,083 27.6 4,655 27.1 25.5 26.9 Total German Trucks 2,328 21.3 10,568 25.5 57.9 61.9 Ford 513 22.4 2,418 49.8 13.2 11.9 Iveco 103 87.3 506 146.8 2.8 1.5 Scania 503 75.9 2,205 33.2 12.1 12.2 Volvo 566 48.2 2,559 50.0 14.0 12.5

Total Heavy Trucks 4,013 31.1 18,256 34.2 100.0 100.0

Medium Trucks May Januar - May

04 / 03 04 / 03

Heavy Trucks May Januar - May

04 / 03 04 / 03 2004 2003

% market share 2004 2003

% market share

Source: Anfavea.

15

22 30 27

-16

24

-30 -31

29

182

-50

0

50

100

150

200

China

Indien

Indon

esien

Japa

n

Malays

ia

Philipp

inen

Südko

rea

Taiwan

Thaila

nd

AsiaCV Sales in Individual Countries January-May 2004

chan

geon

pre

viou

sye

arin

per

cen

t

Sales of Commercial Vehicles in Asia:Striking increase in Turkey, strong rise in

India, Thailand, China and Malaysia.

China1,206,618

India115,079

Indonesia*131,257 Japan1)

470,144

Malaysia*31,667 Philippines

21,476South Korea

100,146

Taiwan64,196

Turkey118,935

* Sales up to April.1) Due to new statistical classification comparison to 2003 is not significant.

16

AsiaSales of Commercial Vehicles in China

0

50,000

100,000

150,000

200,000

250,000

300,000

1998 1999 2000 2001 2002 2003 2004

units

Trends and seasonally-adjusted monthly figures.

Total Sales of Commercial VehiclesJan.-May 2004: 1,206,619 Jan.-May 04/03: + 20.5%

Total Sales of Commercial VehiclesJan.-May 2004: 1,206,619 Jan.-May 04/03: + 20.5%

2003 total sales of Commercial Vehicles increased by

12.6 per cent to 2.4 Mn.

17

ChinaProduction of Heavy-Trucks by Manufacturer 2003

.

FAW Group Corp.: 98,288(-21%)

Dongfeng MotorGroup: 84,022

(-1%)

China National Heavy Duty: 21,136

(62%)

Beijing Auto Industry: 16,106

(589%) ChongqingHongyan: 16,082

(28%)

others: 19,513(80%)

33%

8% 6%6%

8%

39%

Source: Catarc.In brackets: change on previous year.

Production of Heavy-TrucksJan.-May 2004: 143,975 Jan.-May 04/03: + 14.1%

Production of Heavy-TrucksJan.-May 2004: 143,975 Jan.-May 04/03: + 14.1%

18

ChinaProduction of Medium-Trucks by Manufacturer 2003

.

Dongfeng Motor Group: 66,057(-16%)

Chengdu Wangpai: 8,965(49%)

ShannxiAuto: 8,226

(6%)

HubeiSanhuan:

3,737(-52%)

FAW Group: 42,289(-21%)

52%

33%

7%6%

2%

Source: Catarc.In brackets: change on previous year.

Production of Medium-TrucksJan.-May 2004: 80,836 Jan.-May 04/03: + 29.1%

Production of Medium-TrucksJan.-May 2004: 80,836 Jan.-May 04/03: + 29.1%

19

AsiaSales of Commercial Vehicles in India

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

01 02 03 04

Total Sales Medium- / Heavy-CV

units

Total sales of commercial vehicles:Jan.-May 2004: 115,079Jan.-May 04/03: + 30.0%

Total sales of commercial vehicles:Jan.-May 2004: 115,079Jan.-May 04/03: + 30.0%

From 2001 to 2003 sales of medium and heavy commercial vehicles rose by 64 per cent, while sales of all classes went up by 61 per cent.

Source: SIAM.

20

AsiaProduction of Commercial Vehicles in Turkey

units

2003 production of medium and heavy commercial vehicles rose by 55 per cent, while production of buses rose by 89 per cent.

150%

Source: OSD.

150%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

96 97 98 99 00 01 02 1-5/03 1-5/04

busesheavy cvmedium cv

150%

21

Eastern EuropeProduction and Sales of Commercial Vehicles

units

0

100,000

200,000

300,000

400,000

500,000

600,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Production SalesDespite recovery in the last two years,

production in 2003 only reached55 per cent of production in 1992 .

22

Eastern EuropeSales of Commercial Vehicles up to 6 t by country 2003

units

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

LatviaLith

uania

EstoniaBulgari

aSloveniaSlovakia

Czech R

epublicRoman

ia

Poland

Ukraine

Russia

2002: 282,158 Vehicles 2003: 304,072 Vehicles

In 2003 sales of commercial vehicles up to 6 t rose by 8 per cent to 304,100 units.

The Russian Federation accounted for 57 per cent of total sales.

23

Eastern EuropeSales of Commercial Vehicles over 6 t by country 2003

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Estonia

LatviaBulgari

aLith

uaniaSloveniaSlovakiaRoman

ia

Ukraine

Czech R

epublic

Poland

Russia

2002: 92,457 Vehicles 2003: 100,517 Vehicles

units

Clear rise of sales (+ 9 per cent) of commercialvehicles over 6 t to 100.500 units.

The Russian Federation accounted for two thirds of total sales.

24

34

30

15

3

18

10

0

5

10

15

20

25

30

35

40

Polen

Tsch

ech.

Rep.

Slowak

. Rep

.

Ungar

n

Rumän

ien

Russla

nd

Eastern EuropeSales of Commercial Vehicles, January-May 2004

chan

geon

pre

viou

sye

arin

per

cen

t

Poland14,227

Czech Republic12,265

Slovakia4,877

Hungary*9,969

Romania12,905

Russia*91,624

* Sales up to April.

Sales in Eastern Europe:Signifcant growth rates reflect highertransport needs in „bigger“ Europe.

25

13%

14%

16%

17%

5%

11%

12%12%

PolandSales of Commercial Vehicles over 6 t, Jan.-April 2004

.

Volvo: 535(453)

DAF: 406(244)

Scania: 368(270)

Iveco: 351(161)

others: 156(306)

In brackets: Sales of previous year.Source: Samar.

Renault: 446(329)

Mercedes: 496(401)

MAN: 388(214)

Sales of commercial vehicles:Jan.-April 2004: 3,146Jan.-April 04/03: + 32%

Sales of commercial vehicles:Jan.-April 2004: 3,146Jan.-April 04/03: + 32%

26

Czech RepublicSales of Medium- and Heavy-Trucks, Jan.-May 2004

474 471

388

313293

256 241

303

0

100

200

300

400

500

600

Iveco Mercedes Renault MAN DAF Scania Volvo others

units

Source: SAP.

Sales of Medium- and Heavy-TrucksJan.-May 2004: 2,739Jan.-May 04/03: – 7%

Sales of Medium- and Heavy-TrucksJan.-May 2004: 2,739Jan.-May 04/03: – 7%

27

SlovakiaSales of Medium- and Heavy-Trucks, Jan.-May 2004

233

183

166 163

125

88 87

27

0

50

100

150

200

250

Iveco Mercedes Renault Volvo Scania DAF MAN others

units

Source: ZAP.

Sales of Medium- and Heavy-TrucksJan.-May 2004: 1,072Jan.-May 04/03: + 5%

Sales of Medium- and Heavy-TrucksJan.-May 2004: 1,072Jan.-May 04/03: + 5%

28

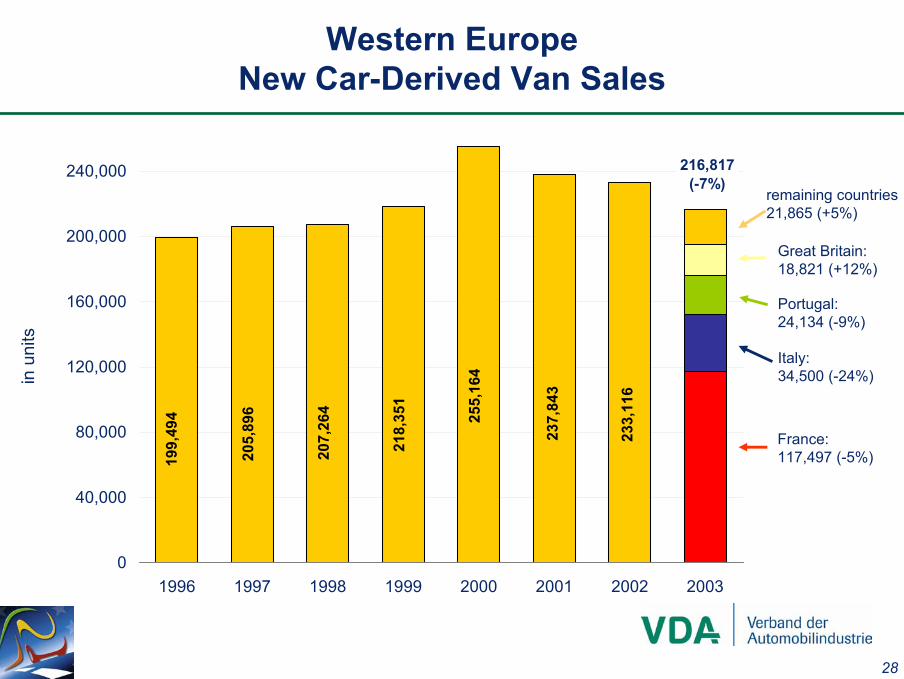

207,

264

205,

896

199,

494

218,

351

255,

164

237,

843

233,

116

0

40,000

80,000

120,000

160,000

200,000

240,000

1996 1997 1998 1999 2000 2001 2002 2003

216,817(-7%)

Western EuropeNew Car-Derived Van Sales

in u

nits

France:117,497 (-5%)

Italy:34,500 (-24%)

Portugal:24,134 (-9%)

Great Britain:18,821 (+12%)

remaining countries21,865 (+5%)

29

95

5

31

572

287

74

654

217

53

5

28

449

249

62

345

15

199

11

0 100 200 300 400 500 600 700

Large Pickups

Small Pickups

Heavy Vans

Full-size Vans

Mid-size Vans

Compact Vans

Small Vans

Micro Vans

Car-Derived Vans

1996: 1.406 mn. cv up to 6 t

2003: 1.946 mn. cv up to 6 t

Western EuropeNew Registrations of CV up to 6 t by Segment

Main market growth took place inthe segment of small vans (+89%).

in 1

,000

uni

ts

30

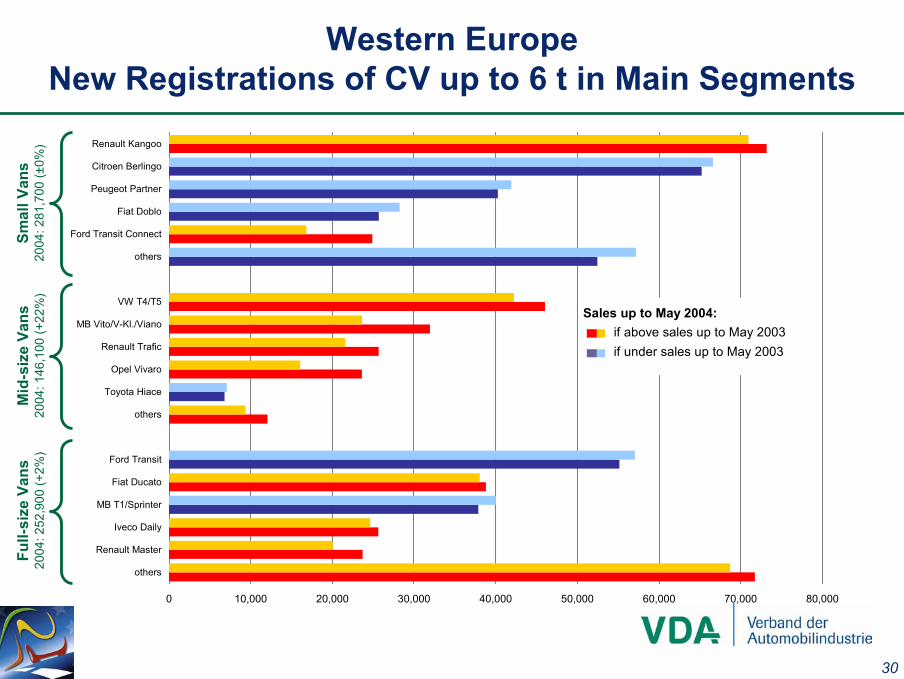

Western EuropeNew Registrations of CV up to 6 t in Main Segments

Smal

l Van

s20

04: 2

81,7

00 (±

0%)

Mid

-siz

eVa

ns20

04: 1

46,1

00 (+

22%

)Fu

ll-si

zeVa

ns20

04: 2

52,9

00 (+

2%)

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

others

Renault Master

Iveco Daily

MB T1/Sprinter

Fiat Ducato

Ford Transit

others

Toyota Hiace

Opel Vivaro

Renault Trafic

MB Vito/V-Kl./Viano

VW T4/T5

others

Ford Transit Connect

Fiat Doblo

Peugeot Partner

Citroen Berlingo

Renault Kangoo

Sales up to May 2004:if above sales up to May 2003if under sales up to May 2003

31

Western EuropeMarket share of CV up to 6 t*, up to May 2004

In this year‘s first five months the German manufacturers were ableto slightly expand their market share.

per c

ents

hare

s

* by segment (exclusive car-derived vans)

DaimlerChrysler10%

Ford11%

Toyota2%

VW Group9%

Fiat Group14%

Renault / Nissan20%

Opel7%

others5%

PSA22%

32

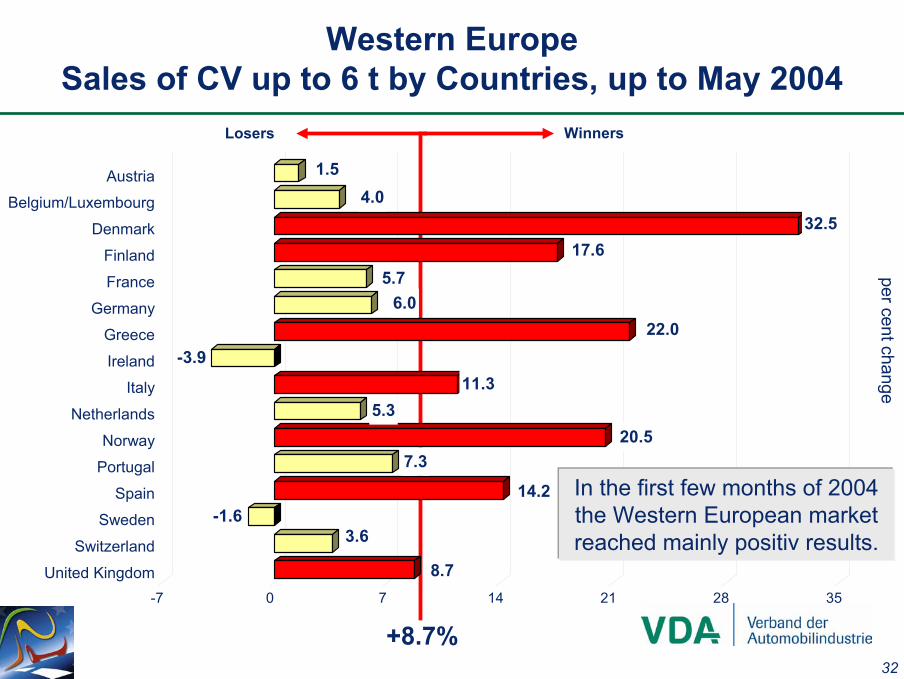

Losers Winners

+8.7%

8.7

3.6-1.6

14.2

7.320.5

5.311.3

-3.922.0

6.05.7

17.632.5

4.01.5

-7 0 7 14 21 28 35

United Kingdom

Switzerland

Sweden

Spain

Portugal

Norway

Netherlands

Italy

Ireland

Greece

Germany

France

Finland

Denmark

Belgium/Luxembourg

Austria

Western EuropeSales of CV up to 6 t by Countries, up to May 2004

per centchange

In the first few months of 2004 the Western European marketreached mainly positiv results.

33

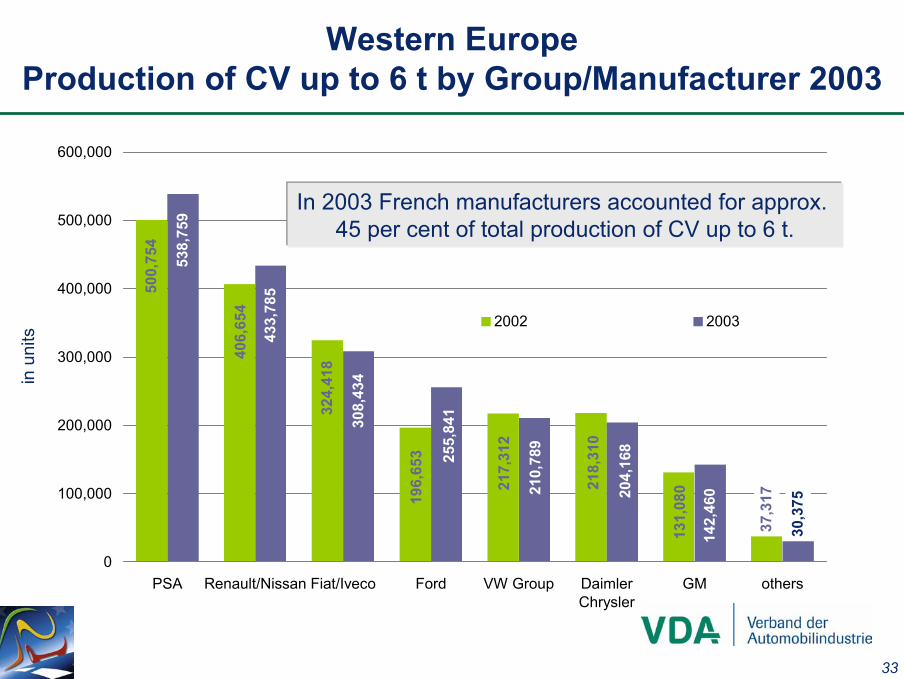

37,3

17

500,

754

406,

654

324,

418

196,

653

217,

312

218,

310

131,

080

30,3

75

538,

759

433,

785

308,

434

255,

841

210,

789

204,

168

142,

460

0

100,000

200,000

300,000

400,000

500,000

600,000

PSA Renault/Nissan Fiat/Iveco Ford VW Group DaimlerChrysler

GM others

2002 2003

Western EuropeProduction of CV up to 6 t by Group/Manufacturer 2003

in u

nits

In 2003 French manufacturers accounted for approx. 45 per cent of total production of CV up to 6 t.

34

Western EuropeCV Sales over 6 t up to 16 t, January - May 2004

units 04/03 in % units 04/03 in % 2004 2003

Belgium 132 - 35 808 - 8 2.6 2.4 Denm ark 38 6 207 7 0.7 0.6 Germ any 2,146 - 9 10,594 4 33.8 33.4 Finland 39 - 22 221 21 0.7 0.6 France 579 - 16 3,383 - 15 10.8 11.4 Greece 62 3 248 47 0.8 0.7 United Kingdom 1,377 - 3 7,146 3 22.8 22.4 Ireland 101 29 569 4 1.8 1.3 Italy 619 - 9 2,919 - 8 9.3 11.3 Luxem bourg 12 - 20 59 - 26 0.2 0.2 Netherlands 126 6 817 13 2.6 2.1 Aus tria 63 - 33 369 - 13 1.2 1.4 Portugal **) 43 - 57 493 - 7 1.6 1.6 Sweden 59 - 6 290 - 12 0.9 0.8 Spain 575 4 2,654 2 8.5 8.1 European Union 5,971 - 8 30,777 - 1 98.1 98.3 Norway 61 - 6 394 25 1.3 1.1 Switzerland 32 - 41 198 - 7 0.6 0.6

Western Europe Total 6,064 - 8 31,369 - 1 100.0 100.0

WE without Germany 3,918 - 8 20,775 - 3 66.2 66.6

m arket shareCommercial Vehicles over 6 t up to 16 t*

May January - May

* Without buses.

35

Western EuropeCV Sales over 16 t, January - May 2004

units 04/03 in % units 04/03 in % 2004 2003

Belgium 615 - 1 3,971 5 4.0 3.4 Denm ark 346 10 1,706 11 1.7 1.7 Germ any 4,535 13 23,078 19 23.2 21.6 Finland 241 8 1,347 27 1.4 1.2 France 2,987 12 17,898 4 18.0 17.2 Greece 63 11 278 0 0.3 0.3 United Kingdom 2,760 7 13,576 1 13.6 16.0 Ireland 275 7 1,529 3 1.5 1.2 Italy 1,851 - 9 8,616 - 8 8.6 10.4 Luxem bourg 76 - 13 367 - 22 0.4 0.5 Netherlands 1,087 4 6,011 6 6.0 4.9 Aus tria 648 0 3,377 16 3.4 3.3 Portugal 269 15 1,380 32 1.4 1.2 Sweden 330 - 20 1,670 - 3 1.7 2.0 Spain 2,623 8 12,609 10 12.7 12.7 European Union 18,706 6 97,413 7 97.7 97.7 Norway 256 7 1,237 15 1.2 1.2 Switzerland 147 - 38 1,017 - 15 1.1 1.1

Western Europe Total 19,109 6 99,667 7 100.1 100.0

WE without Germany 14,574 4 76,589 4 76.9 78.4

m arket shareCommercial Vehicles over 16 t*

May January - May

* Without buses.

36

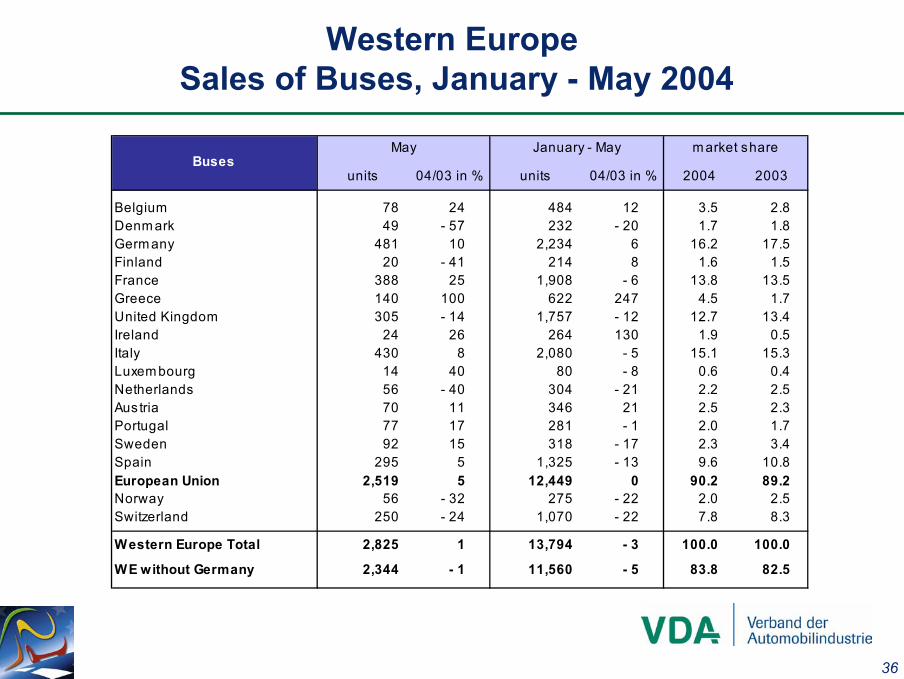

Western EuropeSales of Buses, January - May 2004

units 04/03 in % units 04/03 in % 2004 2003

Belgium 78 24 484 12 3.5 2.8 Denm ark 49 - 57 232 - 20 1.7 1.8 Germ any 481 10 2,234 6 16.2 17.5 Finland 20 - 41 214 8 1.6 1.5 France 388 25 1,908 - 6 13.8 13.5 Greece 140 100 622 247 4.5 1.7 United Kingdom 305 - 14 1,757 - 12 12.7 13.4 Ireland 24 26 264 130 1.9 0.5 Italy 430 8 2,080 - 5 15.1 15.3 Luxem bourg 14 40 80 - 8 0.6 0.4 Netherlands 56 - 40 304 - 21 2.2 2.5 Aus tria 70 11 346 21 2.5 2.3 Portugal 77 17 281 - 1 2.0 1.7 Sweden 92 15 318 - 17 2.3 3.4 Spain 295 5 1,325 - 13 9.6 10.8 European Union 2,519 5 12,449 0 90.2 89.2 Norway 56 - 32 275 - 22 2.0 2.5 Switzerland 250 - 24 1,070 - 22 7.8 8.3

Western Europe Total 2,825 1 13,794 - 3 100.0 100.0

WE without Germany 2,344 - 1 11,560 - 5 83.8 82.5

BusesMay m arket shareJanuary - May

37

Paccar13%

Volvo/RVI29%

other2%

Mercedes18%

Scania13%

Iveco-Magirus4%

MAN15%

Fiat-Gruppe*)6%

Western EuropeMarket Share of CV over 16 t, January - May 2004

* Without Iveco-Magirus.

The market share of VDA companies was 50 per cent

during the first five months of this year.

38

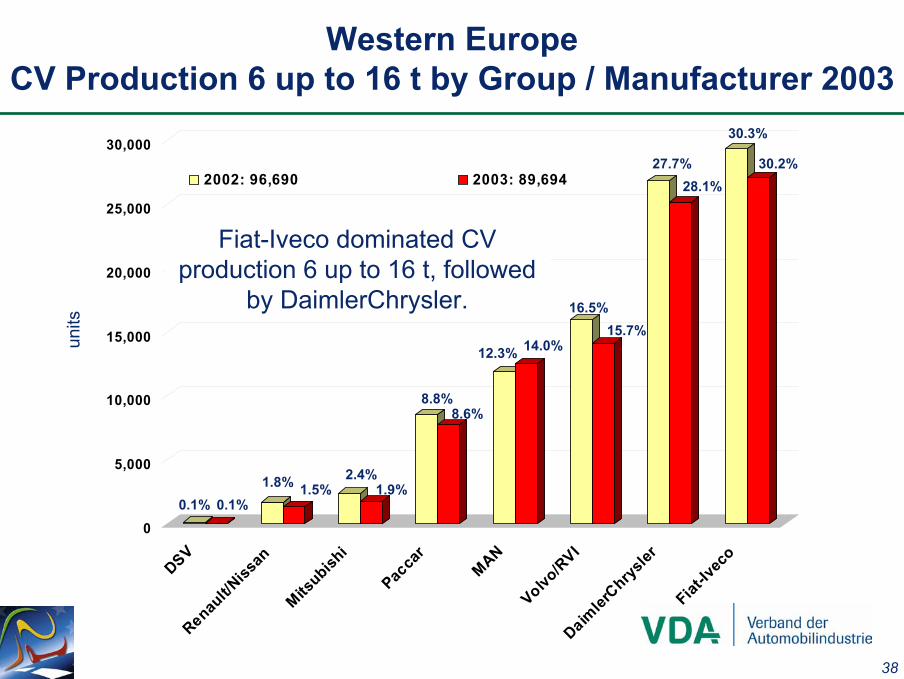

Western EuropeCV Production 6 up to 16 t by Group / Manufacturer 2003

units

0

5,000

10,000

15,000

20,000

25,000

30,000

DSVRenau

lt/Niss

an

Mitsubish

i

Pacca

r

MAN

Volvo/R

VIDaim

lerChrys

ler

Fiat-Iv

eco

2002: 96,690 2003: 89,694

0.1%1.5% 1.9%

15.7%

8.6%

14.0%

30.2%28.1%

0.1%1.8% 2.4%

16.5%

8.8%

12.3%

30.3%

27.7%

Fiat-Iveco dominated CV production 6 up to 16 t, followed

by DaimlerChrysler.

39

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

others

Pacca

r

Fiat-Iv

eco

Scania

MANDaim

lerChrysler

Volvo/R

VI2002: 273,249 2003: 288,138

0.4%

11.0% 11.1%

14.6%13.4%

20.6%

28.8%

0.3%

10.9%12.2%

15.0%13.6%

29.3%

Western EuropeCV Production over 16 t by Group / Manufacturer 2003

units

.

18.7%

Volvo/RVI was the mostimportant manufacturer of

commercial vehicles over 16 t.

40

606

352

219262

17384

20

23

35

105

131 30

14

2130

20

100

200

300

400

500

600

700

Spain

France

German

y

Italy

United

King

dom

Sweden

Belgium

Netherl

ands

Portug

al

Austria

cv over 6 t

cv up to 6 t

Western EuropeCV Production by Weight Classes in 2003

Germany accounts for 34 per cent of Western European CV production over 6 t.

in 1

,000

uni

ts

II. Germany- Domestic Market- Exports- Production- Key Figures - Freight Transport Market

page 42

page 54

page 60

page 65

page 69

42

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

98 99 00 01 02 03 04

GermanyDomestic Orders for Commercial Vehicles up to 6 t

units

up to May 2004: -8%

up to June 2004: +12%

total up to May 2004: +4%

imported makes

German makes

Trends and seasonally-adjusted monthly figures

Orders for transporters are rising slightly.

43

500

1,500

2,500

3,500

4,500

5,500

6,500

7,500

8,500

98 99 00 01 02 03 04

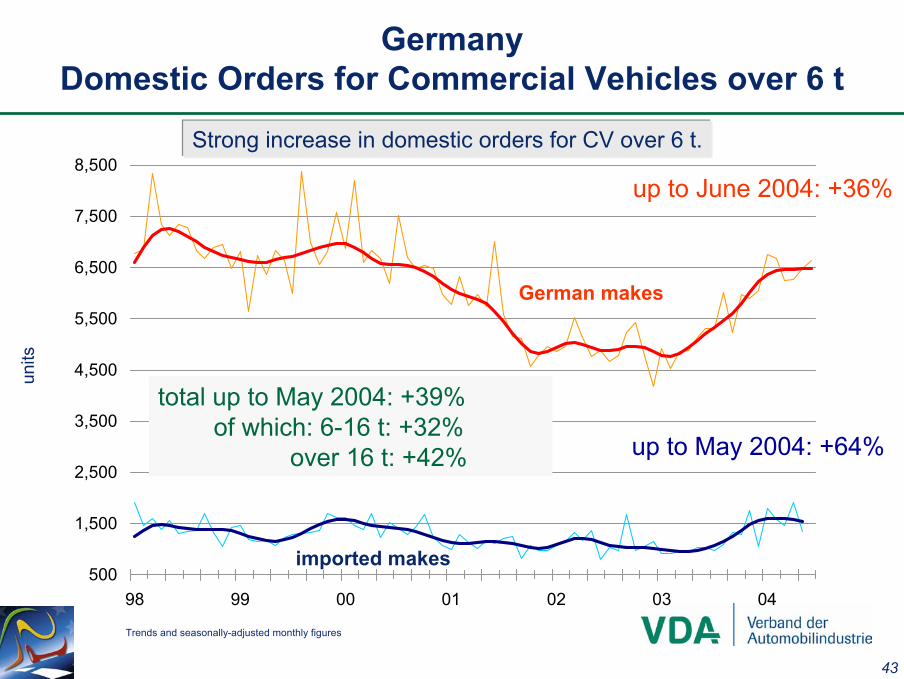

GermanyDomestic Orders for Commercial Vehicles over 6 t

units

up to May 2004: +64%

up to June 2004: +36%

total up to May 2004: +39%of which: 6-16 t: +32%

over 16 t: +42%

imported makes

German makes

Trends and seasonally-adjusted monthly figures

Strong increase in domestic orders for CV over 6 t.

44

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

98 99 00 01 02 03 04

GermanyDomestic Order Backlog of Commercial Vehicles

units

May 2004: 11,000 (-6%)

June 2004: 55,300 (+34%)< 6 t: 35,500 (+24%)> 6 t: 19,800 (+56%)

total May 2004: 67,400 (+21%)

imported makes

German makes

Trends and seasonally-adjusted monthly figures imported makes: order backlog up to 3.5 t

45

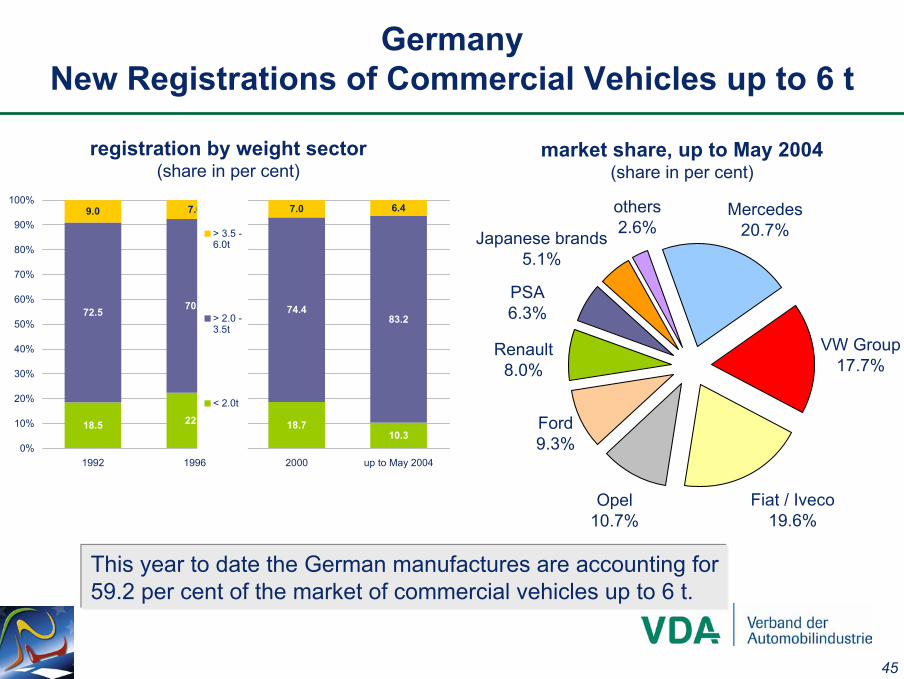

Mercedes20.7%

VW Group17.7%

Ford9.3%

Renault8.0%

Japanese brands5.1%

Fiat / Iveco19.6%

Opel10.7%

PSA6.3%

others2.6%

GermanyNew Registrations of Commercial Vehicles up to 6 t

registration by weight sector(share in per cent)

market share, up to May 2004(share in per cent)

This year to date the German manufactures are accounting for59.2 per cent of the market of commercial vehicles up to 6 t.

18.5 22.4 18.710.3

72.5 70.0 74.483.2

9.0 7.6 7.0 6.4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1996 2000 up to May 2004

> 3.5 -6.0t

> 2.0 -3.5t

< 2.0t

46

GermanyNew Registrations of CV up to 6 t in the Main Segments

units

109,

718

104,

298

60,3

73

104,

967

84,9

6293,8

11

43,9

47

42,6

35

34,9

52

0

20,000

40,000

60,000

80,000

100,000

120,000

Small Van Mid-size Van Full-size Van

1998 2000 2002 2003 05/2003 05/2004

-7%+24% -3%

03/98: -4%03/98: -19%

03/98

: +55

%

Renault KangooCitroën Berlingo

Opel Combo

VW T 5MB Vito / V-Kl. / Viano

Opel Vivaro

MB SprinterFord Transit

VW LT

47

GermanyMarket Shares of Commercial Vehicles over 6 t by Make

CV over 16 t, up to May 2004(share in per cent)

CV over 6 up to 16 t, up to May 2004(share in per cent)

The German manufacturers are dominating both the medium-and the heavy-duty CV segment.

Mercedes47.2%

MAN / ERF23.8%

Fiat / Iveco18.8%

others10.2%

Mercedes37.8%

MAN / ERF27.4%

Fiat / Iveco6.9%

Scania6.8%

Volvo / RVI11.3%

Paccar8.1%

others1.7%

48

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

98 99 00 01 02 03 04

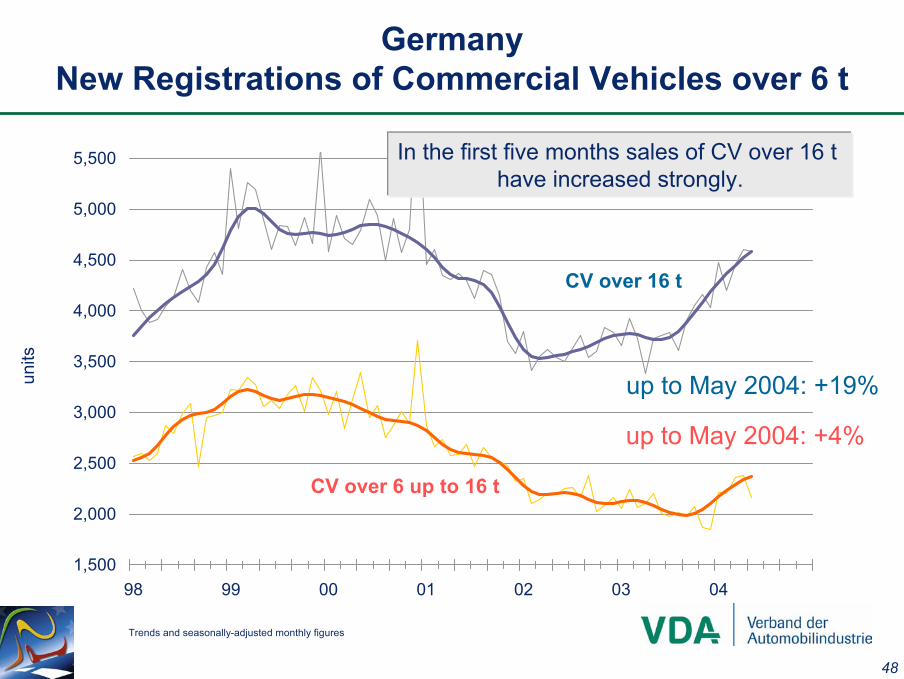

GermanyNew Registrations of Commercial Vehicles over 6 t

Trends and seasonally-adjusted monthly figures

up to May 2004: +4%

up to May 2004: +19%units

CV over 16 t

CV over 6 up to 16 t

In the first five months sales of CV over 16 t have increased strongly.

49

0

10

20

30

40

50

60

70

6-10 t 10-12 t 12-14 t 14-16 t over 16 t

1994 1998 2002 up to May 2004

GermanyNew Registrations of Commercial Vehicles over 6 t

shar

ein

per

cen

t

Apart from the weight segment of over 16 t the segmentof over 10 to 12 t also gained importance.

50

2,70

3

2,43

9

2,31

2

2,03

3

2,04

0

575 584

9,18

1 9,99

5

7,41

7

5,85

6

5,55

3

1,67

6

2,21

1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1999 2000 2001 2002 2003 up to May2003

up to May2004

tipper up to 6 t tipper over 6 t

+24%

+2%

GermanyNew Registrations of Tippers

units

After three years of decline tipper newregistrations have started to increase again in 2004.

51

20,0

39

17,6

32

11,4

68

11,4

80

15,9

03

17,0

93 19,3

44

24,9

72

28,4

57

27,8

95

25,9

67

23,7

51 25,6

30

11,1

37 13,3

55

0

5,000

10,000

15,000

20,000

25,000

30,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 up toMay2003

up toMay2004

16

20

24

28

32

36

40

+20%

GermanyNew Registrations of Semitrailer Tractors

new

regi

stra

tions

in u

nits

The demand for semitrailer tractors ison record levels right now.

shareof sem

itrailertractorsin new

registrationsof

comm

ercialvehiclesover6 t

52

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

98 99 00 01 02 03 04

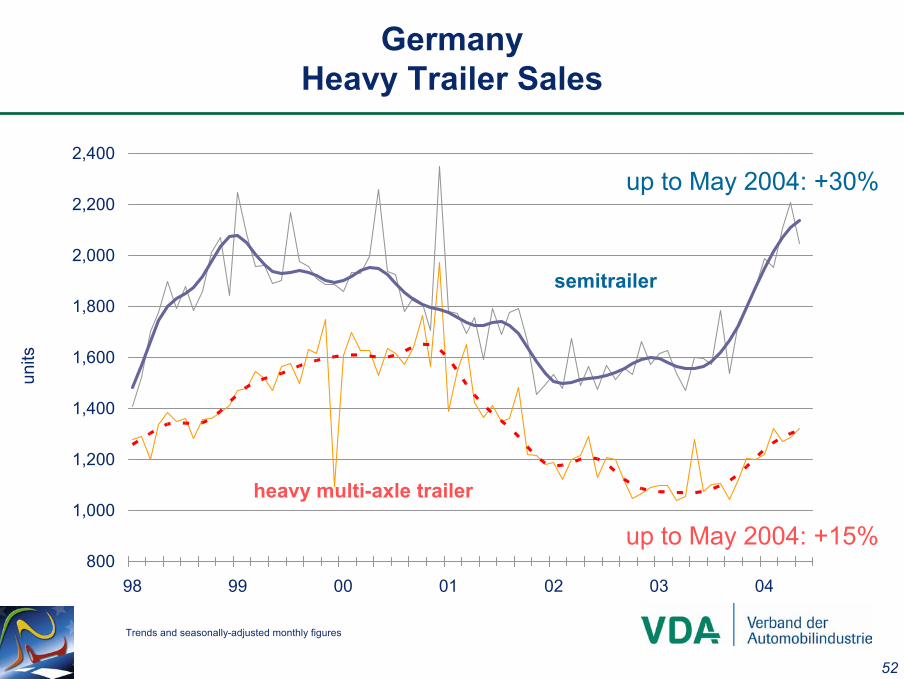

GermanyHeavy Trailer Sales

units

Trends and seasonally-adjusted monthly figures

up to May 2004: +15%

up to May 2004: +30%

semitrailer

heavy multi-axle trailer

53

800

1,200

1,600

2,000

2,400

2,800

98 99 00 01 02 03 04

GermanyNew Registrations of Motor Caravans and Caravans

units

Trends and seasonally-adjusted monthly figures

up to May 2004: +7%

up to May 2004: -4%

caravans

motor caravans

54

9,000

13,000

17,000

21,000

25,000

29,000

33,000

98 99 00 01 02 03 04

GermanyForeign Orders and Exports of CV up to 6 t

units

up to June 2004*: +26%

Trends and seasonally-adjusted monthly figures* Change figures are based on previous year figures that were corrected later due to the move of production sites** Incl. intake of orders for vehicles from foreign production (in Europe)

up to June 2004*: +5%

exports

foreign demand**

55

14,338

7,156

4,605

4,260

3,912

3,841

2,596

0 3,000 6,000 9,000 12,000 15,000

United Kingdom

France

Netherlands

Spain

Italy

Turkey

Belgium (-19%)

(+337%)

(-16%)

(+4%)

(-4%)

(+3%)

(+25%)

GermanyExports of CV up to 6 t in Selected Countries*, up to May 2004

Expo

rts in

uni

ts(C

hang

e ag

ains

tpre

viou

sye

arin

bra

cket

s)

* Exports adjusted due to move of production

Exports: 58,500 (+3%)EU-15: 44,700 (+4%)new EU-10: 3,800 (-2%)Asia: 4,700 (+163%)

56

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

98 99 00 01 02 03 04

GermanyForeign Orders and Exports of CV over 6 t

units

up to June 2004: +34%

up to June 2004: +14%

exports

foreign demand**

Trends and seasonally-adjusted monthly figures** Incl. intake of order for vehicles from foreign production (in Europe)

57

5,783

4,956

3,898

3,810

1,922

1,841

1,730

1,623

0 1,000 2,000 3,000 4,000 5,000 6,000

United Kingdom

France

Italy

Spain

Austria

Turkey

South Africa

Poland (+65%)

(+15%)

(+153%)

(+1%)

(+2%)

(-18%)

(-7%)

(+8%)

Germany Exports of CV over 6 t in Selected Countries, up to May 2004

Expo

rts in

uni

ts(C

hang

e ag

ains

tpre

viou

sye

arin

bra

cket

s) Exports: 43,700 (+11%)EU-15: 25,400 (-1%)new EU-10: 4,200 (+30%)Asia: 7,500 (+40%)Africa: 2,900 (+17%)

58

1,472

1,073

983

881

806

419

0 400 800 1,200 1,600

Turkey

Iran

Saudi Arabia

Kuwait

United Ar. Emirates

Oman

up to May 2003

up to May 2004

(+122%)

(+71%)

(+2,281%)

(-40%)

(+22%)

(+116%)

GermanyExports of CV over 16 t in Important Asian Countries

Expo

rts in

uni

ts(C

hang

e ag

ains

tpre

viou

sye

arin

bra

cket

s)

This year to date exports of CV over 16 t to Asia have increased above averageby 41 per cent.

59

9,747 11,371

19,04014,152

22,891

28,435 27,522

17,731

46,025

63,655

25,856

31,507(+22%)

89,239(-10%)

98,996

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

92 93 94 95 96 97 98 99 00 01 02 03 -04/03 -04/04

GermanyExports of Used Commercial Vehicles to Eastern Europe

Source: Statistisches Bundesamt

units

In this year‘s first five months a total of 49,700 used CV was shipped abroad (+21%), 31,500 of which were sent to Eastern Europe (+22%) and 7,000 of those (+16%) to Poland.

up to April 2004Trucks < 5t 16,826 (+21%)Trucks > 5t 9,535 (+18%)Semitrailer tractors 3,870 (+28%)Buses 1,276 (+51%)

60

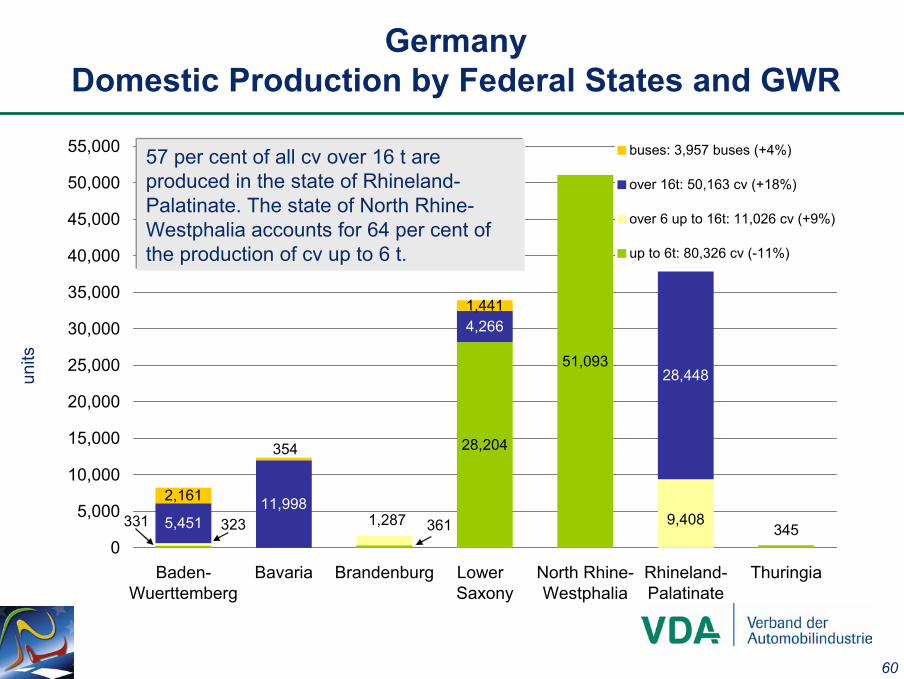

28,204

51,093

5,45111,998

4,266

28,448

2,161

1,441

323 361 345331 1,287 9,408

354

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

Baden-Wuerttemberg

Bavaria Brandenburg Lower Saxony

North Rhine-Westphalia

Rhineland-Palatinate

Thuringia

buses: 3,957 buses (+4%)

over 16t: 50,163 cv (+18%)

over 6 up to 16t: 11,026 cv (+9%)

up to 6t: 80,326 cv (-11%)

GermanyDomestic Production by Federal States and GWR

units

57 per cent of all cv over 16 t areproduced in the state of Rhineland-Palatinate. The state of North Rhine-Westphalia accounts for 64 per cent of the production of cv up to 6 t.

61

0

2,000

4,000

6,000

8,000

10,000

12,000

98 99 00 01 02 03 04

GermanyProduction of German Commercial Vehicles over 6 t

Trends and seasonally-adjusted monthly figures

units

up to May 2004: +9%

up to May 2004: +18%

CV over 16 t

CV over 6 up to 16 t

Production of CV over 6 t in full swing.

62

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

98 99 00 01 02 03 04

GermanyBus Production and Sales

Trends and seasonally-adjusted monthly figures

units

up to June 2004:+9%

up to June 2004:+24%

Exports

Production

up to June 2004:+1%New Registrations

Production and sales accelerating.

63

32,377

22,592

13,779

4,617 3,582

5,181

4912,752

16,378

2,95518,443 29,666

3,167

1,757

9,762

6,281

1,504

363106

237

0

10,000

20,000

30,000

40,000

50,000

60,000

EU-15 new EU-10 LatinAmerica

NorthAmerica

EasternAsia

WesternAsia

Africa

buses: 19,647 buses (+9%)

over 16 t: 54,231 cv (+35%)

over 6 up to 16 t: 34,723 cv (+20%)

up to 6 t: 76,947 cv (-17%)

GermanyGerman Production Abroad up to May 2004

units

The focus of German productionabroad lies for CV up to 6 t in Europe and for CV over 6 t as well as for buses in America.

64

GermanyGerman Production Abroad up to May 2004

units

332

706

3.194 388

3.306 656

4.571 463

7.561

8.196

8.864

10.176286

21.886

23.672

18.657 23.253

49.381

0 10.000 20.000 30.000 40.000 50.000

others

South Africa

Argentina

Turkey

Canada

Austria

Mexico

Belgium

Poland

Spain

Brazil

USA

DaimlerChrysler: 119,500 cv (incl. buses)

Ford: 10,200 cv

MAN: 8,900 cv (incl. buses)

VW: 46,900 cv

up to May 2004: 185,500 cv (+3 per cent)

65

372,458890,156

-45,00498,358

109,789

173,32692,955

242,224-248,061

144,531

152,890

456,854547,562

606,2331,009,744

-250,000 0 250,000 500,000 750,000 1,000,000

Africa

Asia total

Japan

China

Latin America

NAFTA

USA

new EU-10

Poland

Hungary

Czech Rep.

France

Italy

Spain

United Kingdom

GermanyForeign Trade Balance of the Commercial Vehicle Industry* in 2003: 6.4 billion €

EU-25 is main trade partner of thethe German CV industry (73 per cent)(7 per cent of which new EU countries).

in b

illion

euro

*Overall commercial vehicle exports - imports (incl. used vehicles)

66

GermanyExports of the German Commercial Vehicle Industry

in b

illion

euro

4.8

1.1

4.9

12.4

2.9

11.1

0

2

4

6

8

10

12

14

CV manufacturers Trailers and bodies CV parts industry

1993 1995 1997 1999 2001 2003

2003

/1993

: +15

8%

2003/1993: +175%

2003

/1993

: +12

9%

67

GermanyTurnover of the German Commercial Vehicle Industry

in b

illion

euro

10.013.3 15.3

19.324.0 24.56.0

5.34.8

5.9

6.5 6.9

5.04.4

7.5

9.2

11.512.1

0

5

10

15

20

25

30

35

40

45

1993 1995 1997 1999 2001 2003

CV parts industry

Trailers and bodies

CV manufacturers

21.023.0

27.6

34.4

42.043.5

total

68

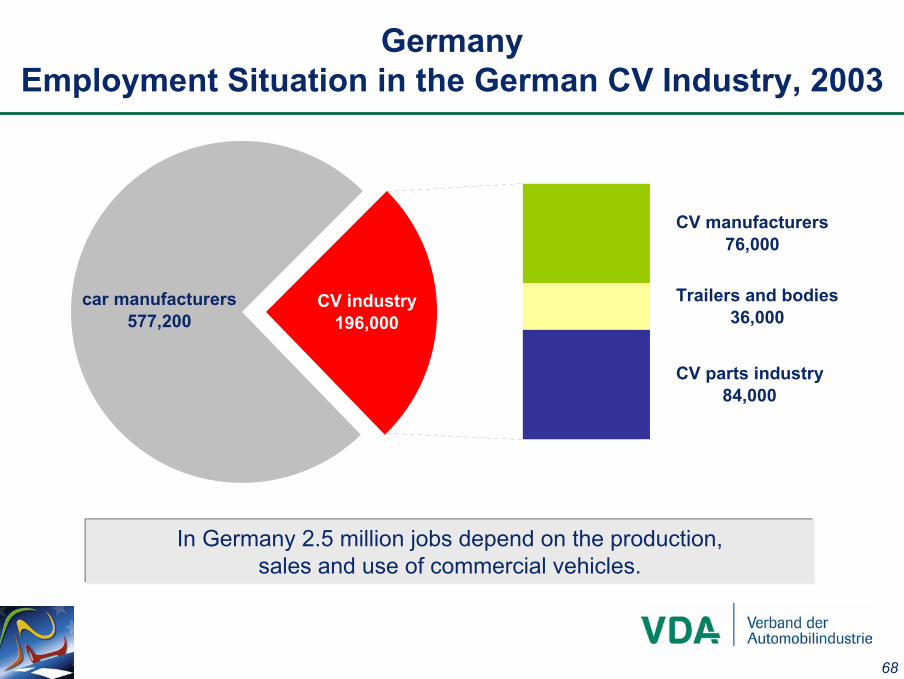

GermanyEmployment Situation in the German CV Industry, 2003

In Germany 2.5 million jobs depend on the production,sales and use of commercial vehicles.

car manufacturers 577,200

CV industry196,000

CV parts industry 84,000

Trailers and bodies36,000

CV manufacturers 76,000

69

Freight Transport in Germany up to 2015

Source: DIW, BMVBW, PROGNOS

in b

illion

tonn

eki

lom

etre

s

71.5

48.8

78.6

64.9

51.4

125.4

61.9

54.8

169.9

74.0

65.0

361.4

115.0

90.0

485.0

0

100

200

300

400

500

600

700

1970 1980 1990 2002 2015

road

inland waterways

rail

70

Freight Transportation by Modesin the New EU-Member States

in b

illion

tkm

Source: prog trans AG*Poland, Czech Rep., Hungary, Slovenia, Estonia

130.8

189.7 207.2

90.3

93.0100.2

4.7

4.0

2.9

0

50

100

150

200

250

300

350

2000 2010 2015

road rail inland waterways

71

Freight Transport in Europe by Freight Category in 2001Shares of Modes of Transport in per cent of Tonne Kilometres

Source: EU Commission

90%

21%

57%

60%

79%

74%

85%

7%

41%

22%

33%

9%

18%

14%

3%

38%

21%

7%

12%

8%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

agricultural products

coal

petroleum and petroleumproducts

ore, steel and other metalproducts

cement and buildingmaterials

chemicals and fertilisers

vehicles, machinerymanufactured articles

road rail inland waterways

72

Infrastructure Investment per Unit Outputper Kilometer in Germany

Source: DIW, own calculations

in m

illion

euro

per b

illion

pass

enge

rand

tonn

eki

lom

etre

s(in

199

5 pr

ices

)

5

10

15

20

25

30

35

40

45

50

1960 1965 1970 1975 1980 1985 1990 1995 2000 2002

road rail inland waterways

73

Reduction in Exhaust Gas Thresholds in Europe

100%

40%

36%

25%

18%

18%

100%

46%

46%

32%

22%

22%

100%

56%

49%

34%

13%

7%

100%

51%

21%

15%

3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CO HC NOx Particles

1990 1993 1996 2000 2005 2008

74

Freight Transportation in GermanyDecoupling of km driven from tkm

Source: ifo, DIW, prognos, VDA

0

100

200

300

400

500

600

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

km driven (in billion km) billion tkm

75

GermanyYearly Financial Burden of a 40 t - Truck

Source: BGL* burden in 2003 for a 40 t - truck, Euro II, with air suspension in long-distance traffic,

135,000 km/year, 34 l/100 km fuel consumption

Eur

o

21,591

17,442 16,52114,812

11,606

1,521

549399

716

511

0

5,000

10,000

15,000

20,000

25,000

Germany France Italy Netherlands Luxembourg

tax on oil

motor vehicle tax

23.112

17.99116.920

15.528

12.117

76

7.48 7.76

9.009.41

9.9110.74

13.0

16.36

4

6

8

10

12

14

16

1995 1996 1997 1998 1999 2000 2003 2005*

GermanySales Trend in Express Courier & Parcel Services

Source: BdKEP * Forecast

in b

illion

euro

Strong sales growth in Express Courier & Parcel Services- a consequence of e-commerce -

but impossible without commercial vehicles for delivery.