current liabilities and payroll chapter 11 copyright ©2014 pearson education, inc. publishing as...

TRANSCRIPT

Current Liabilities and Payroll

Chapter 11

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 11-1

Liabilities

• Best described as:– Debts and obligations owed to others.

• Three primary characteristics:– They occur as a result of a past

transaction or event.– They create a present obligation for

future payments.– They are an unavoidable obligation.

11-2

Current Liabilities

Long-Term Liabilities

Will be paid from current assets within one year or the company’s operating

cycle, whichever is longer.

Due after one year or the company’s operating cycle,

whichever is longer.

Two Major Categories

11-3

Current Liabilities(examples) • Accounts payable• Short-term notes payable• Sales tax payable• Current portion of long-term notes payable• Accrued liabilities• Unearned revenues

4

5

Eastman Chemical Footnote Disclosure

6

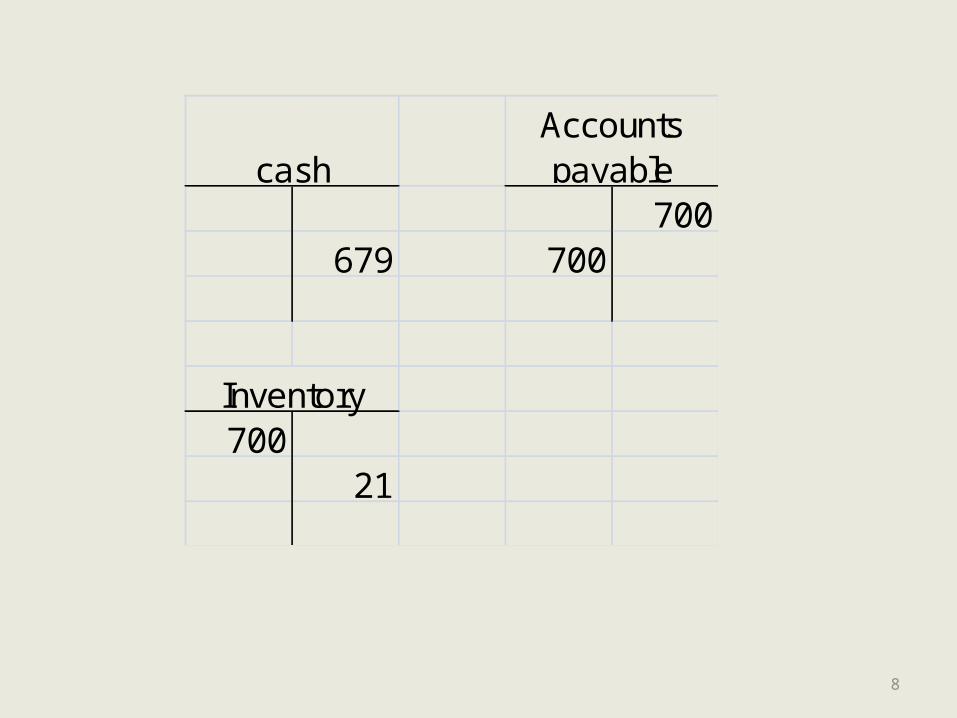

Accounts Payable(example)

• For products and services purchased on account

• Integrated accounts payable and inventory systems

• Paid later within a discount period or not• Usually due in 30 days

7

8

cashAccounts payable

700679 700

Inventory700

21

Sales Tax Payable

• Tax levied by state on retail sales• Record sales, with the taxes, as follows:

• Record and forward the sales tax to the state

9

10

cashAccounts payable Sales revenue

10,600 10,000 600

InventorySales Tax Payable

600600

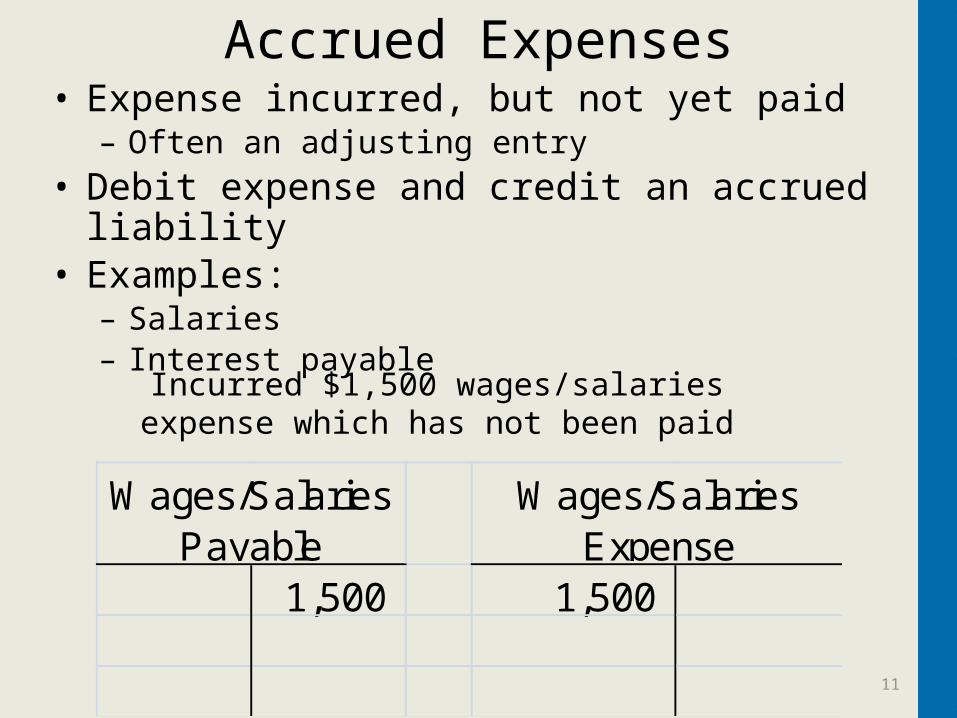

Accrued Expenses• Expense incurred, but not yet paid

– Often an adjusting entry

• Debit expense and credit an accrued liability• Examples:

– Salaries – Interest payable

11

Wages/Salaries Payable

Wages/Salaries Expense

1,500 1,500

Incurred $1,500 wages/salaries expense which has not been paid

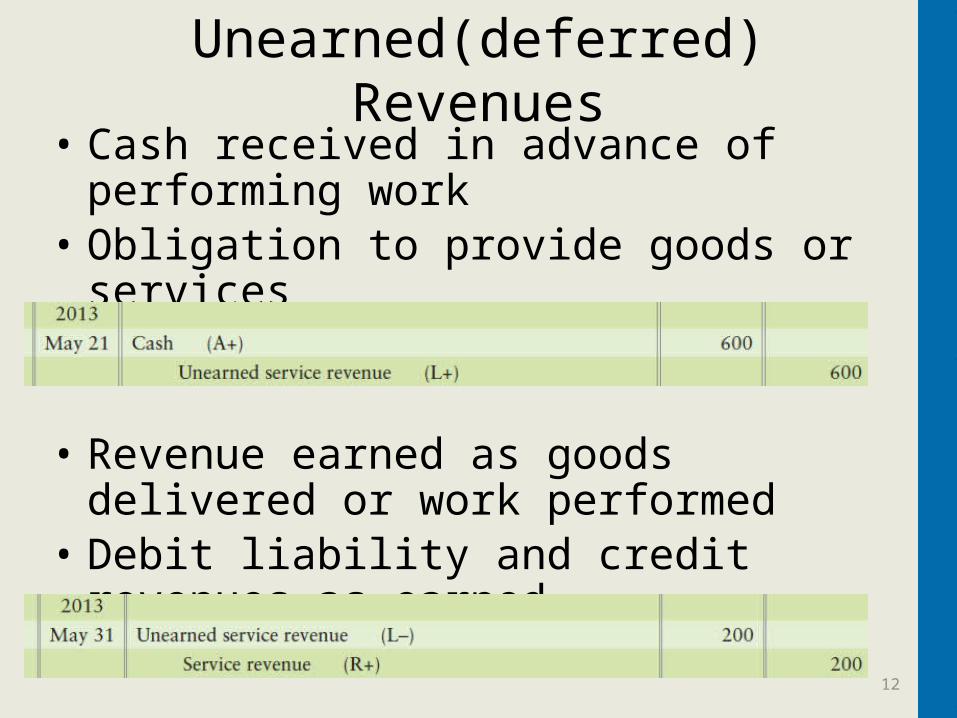

Unearned(deferred) Revenues• Cash received in advance of performing

work• Obligation to provide goods or services

• Revenue earned as goods delivered or work performed

• Debit liability and credit revenues as earned

12

13

cashUnearned revenue Sales revenue

600 600 600 600

14

Unearned(deferred) Revenues

11-15©2014 Pearson Education, Inc. Publishing as Prentice Hall

11-16©2014 Pearson Education, Inc. Publishing as Prentice Hall

Current portionLong-Term Debt

11-17©2014 Pearson Education, Inc. Publishing as Prentice Hall

Accounting for Payroll

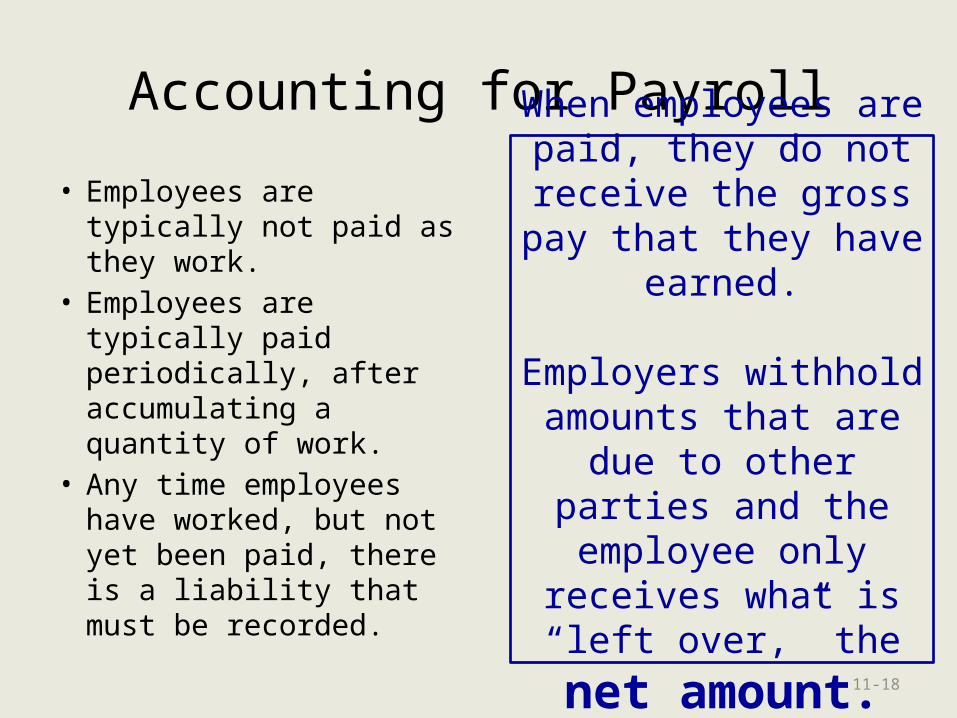

• Employees are typically not paid as they work.

• Employees are typically paid periodically, after accumulating a quantity of work.

• Any time employees have worked, but not yet been paid, there is a liability that must be recorded.

When employees are paid, they do not

receive the gross pay that they have earned.

Employers withhold amounts that are due to

other parties and the employee only receives what is “left over,” the

net amount.11-18

Accounting for Payroll

OASDI Taxes

Medicare Taxes

Federal Income

Tax

State and Local

Income Taxes

Voluntary Deductions

Gross Pay

Net Pay

11-19

FICA

Amounts withheld depend on the employee’s earnings and the tax rates. Employers owe the income tax

amounts withheld from employees’ gross pay to the appropriate government agency.

Amounts withheld depend on the employee’s earnings and the tax rates. Employers owe the income tax

amounts withheld from employees’ gross pay to the appropriate government agency.

Federal Income

Tax

State and Local Income

Taxes

Withholding for Employee Income Tax

Top rate of 39.6% on income > $400,000

For example, in some states the state income tax rate is

5%.

11-20

OASDI Taxes

Medicare Taxes

These amounts are due to the federal government following withholding.

Withholding for Employee Social Security and Medicare(FICA Taxes)

4.2%Applied to first

$110,100 of earned income

1.45%Applied to 100%

of income

11-21

6.2% as of 2013

Union Dues

Savings Accounts

Pension Contributions

Insurance Premiums

Charities

Union Dues

Savings Accounts

Pension Contributions

Insurance Premiums

Charities

Optional Withholding Deductions

• Amounts withheld depend on the employee’s request.

• Employers must forward the voluntary deductions withheld from employees’ gross pay to the designated agency.

11-22

Recording Payroll

• This table summarizes the payroll and withholdings for Smart Touch Learning for December.

• As shown in Exhibit 11-2, a Payroll Register is normally used to accumulate this data.

Gross Pay 28,580$ Withholdings OASDI $961 Medicare 414 Income Tax 5,716 Health Insurance 645 Other 60

Total Withholdings 7,796 Net (take-home) Pay 20,784$

11-23

Recording Payroll

Typically, the payroll checks will be drawn against a separate payroll checking account that is only used for

payroll.

Date Accounts and Explanation Debit Credit

Dec. 31 Salaries and Wages Expense 28,580 FICA - OASDI Taxes Payable 961 FICA - Medicare Taxes Payable 414 Employee Income Taxes Payable 5,716 Employee Health Ins. Payable 645 Other Payables 60 Salaries and Wages Payable 20,784 To record payroll for December.

11-24

A L + E

= Various Salaries/Wages

Payables Expense

Employer Payroll Taxes

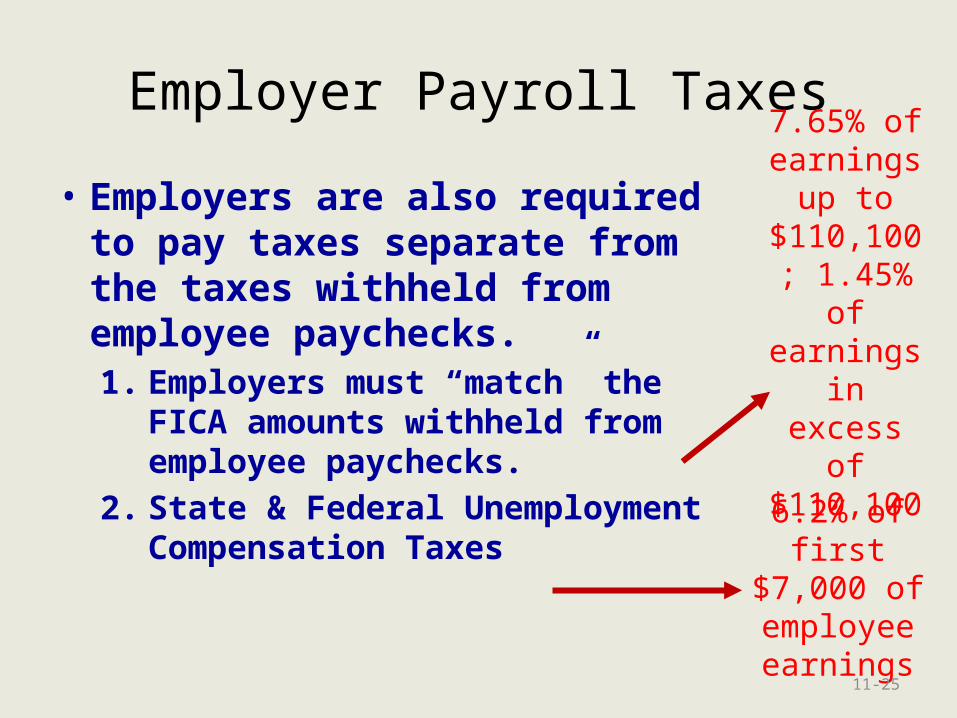

• Employers are also required to pay taxes separate from the taxes withheld from employee paychecks.1. Employers must “match” the

FICA amounts withheld from employee paychecks.

2. State & Federal Unemployment Compensation Taxes

7.65% of earnings

up to $110,100; 1.45% of

earnings in excess of $110,100

6.2% of first $7,000 of employee earnings

11-25

Unemployment Taxes

• Unemployment checks are paid out of the Unemployment Insurance Fund.

• Companies pay into the fund monthly (5.6% to the state and 0.60% to the federal government).

• The rate varies with each company’s employment history.

11-26

Recording PayrollIn December, Smart Touch Learning had wages subject

to OASDI of $22,880 (one employee went over the $110,000 limit). Wages subject to Medicare were

$28,580. FUTA and SUTA were due on $4,000 of wages paid to a new employee.

Date Accounts and Explanation Debit Credit

Dec. 31 Payroll Tax Expense 2,081 FICA--OASDI Taxes Payable 1,419 FICA--Medicare Taxes Payable 414 Federal Unempl. Taxes Payable 24 State Unempl. Taxes Payable 224 To record employer payroll taxes.

11-27

A L + E

= Various Payroll Tax

Payables Expense

$4,000 * .6%

$4,000 * 5.6%

$22,580 * 1.45%

$22,880 * 6.2%

Internal Controls for Payroll

• Efficiency Controls– Payroll is usually automated, rather than

prepared by hand.

• Disbursement Controls– Employees sign for checks or present ID’s.– Hiring and firing is separated from payroll

preparation.– Time clocks and direct deposit are also

used.

11-28

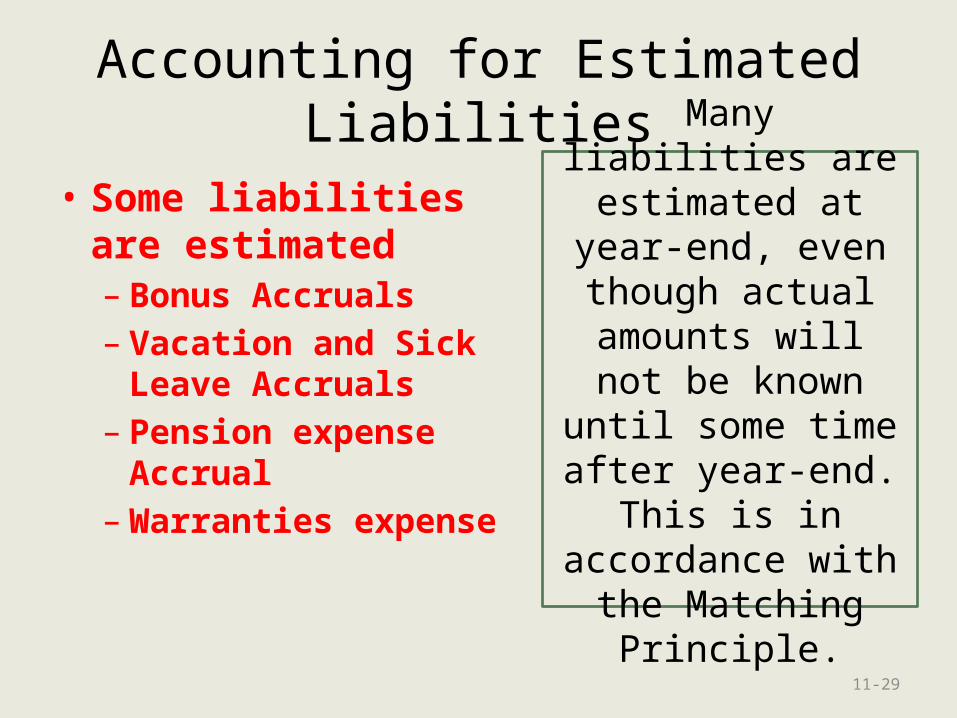

Accounting for Estimated Liabilities

• Some liabilities are estimated– Bonus Accruals– Vacation and Sick

Leave Accruals– Pension expense

Accrual– Warranties expense

Many liabilities are estimated at year-end, even though

actual amounts will not be known until

some time after year-end. This is in

accordance with the Matching Principle.

11-29

Dell Warranty Disclosure

30

11-31

Contingent Liabilities

• A contingent liability is a POTENTIAL liability that depends on a future event.

• How do we disclose a liability that might arise in the FUTURE as a result of something that has occurred in the PRESENT?

11-32

Contingent Liabilities

• The type of disclosure of a contingent liability depends on two issues:

1. How likely is the future event?

2. Can the amount of the liability be reasonably estimated?

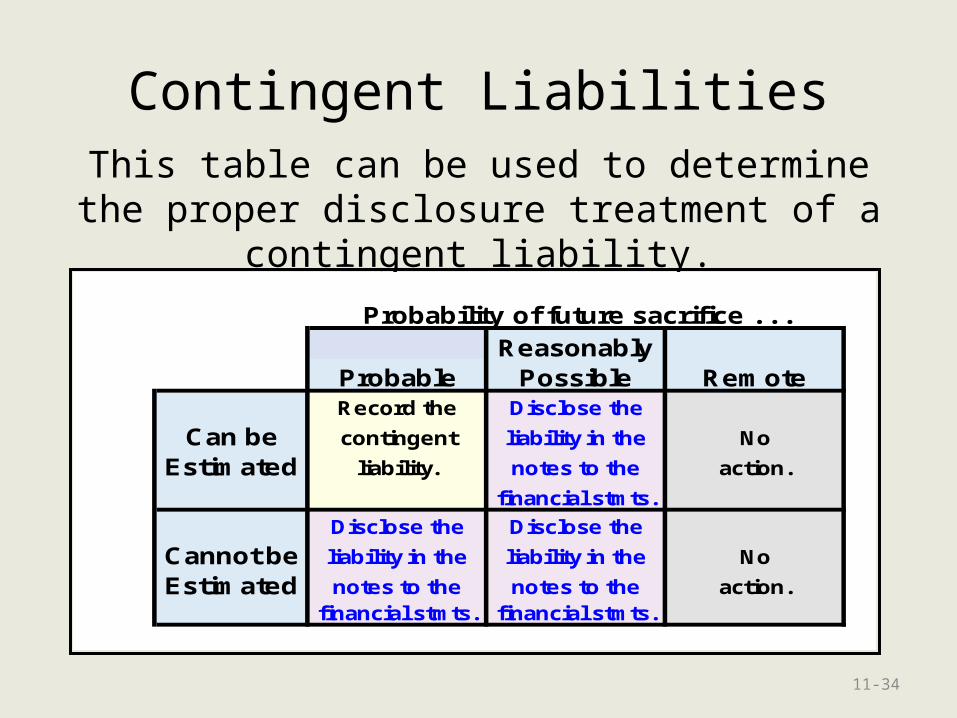

11-33

Probability of future sacrifice . . .Reasonably

Probable Possible RemoteRecord the Disclose the

Can be contingent liability in the No

Estimated liability. notes to the action.

financial stmts.

Disclose the Disclose the

Cannot be liability in the liability in the No

Estimated notes to the notes to the action.financial stmts. financial stmts.

Am

ou

nt

. . .

Contingent LiabilitiesThis table can be used to determine the proper

disclosure treatment of a contingent liability.

11-34

11-35

Times-Interest-Earned Ratio

This ratio is used to evaluate a business’s ability to pay interest

expense.

A high ratio indicates that the company is better able to pay its interest.

Times-Interest-Earned Ratio

= ( Net Income

+Income Tax

Expense +

Interest Expense

) ÷Interest Expense

11-36

Times-Interest-Earned Ratio

Times-Interest-Earned Ratio

= ( Net Income

+Income Tax

Expense +

Interest Expense

) ÷Interest Expense

Compute the Times-Interest-Earned Ratio for Green Mountain for 2011

11-37

Times-Interest-Earned Ratio

Times-Interest-Earned Ratio

= ( Net Income

+Income Tax

Expense +

Interest Expense

) ÷Interest Expense

= ( 199,501$ + $101,699 + 57,657$ ) ÷ 57,657$

= 358,857$ ÷ $57,657

= 6.22 (rounded)

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 11-38