current macro management and long-term growth scenarios of chinese economy

DESCRIPTION

Current macro management and Long-term growth scenarios of Chinese economy. FAN Gang National Economic Research Institute & Peking University 06-2009. I. Global Crisis and China: Policies and Scenarios. I-1, The reasons for the slowdown. Global crisis; Domestic adjustment by itself: - PowerPoint PPT PresentationTRANSCRIPT

Current macro management and Long-term growth scenarios of

Chinese economy

FAN Gang

National Economic Research Institute &

Peking University

06-2009

I. Global Crisis and China:

Policies and Scenarios

I-1, The reasons for the slowdown

• Global crisis;

• Domestic adjustment by itself:

– It is better to have a strong macroeconomic policy during the booming time, instead of doing little to let things bubble up!

– Having had that, China does not have big bubble-burst to deal with and possible to recover quicker;

I-2, The good rooms for policy maneuver

• Gov’t debt / GDP = 22%

• Banking sector in good shape;

• 2 trillion foreign reserve.

-- China has been paid off for its financial prudence and patience.

I-3, Stimulus policies

Fiscal stimulus package and 8% growth

• The net fiscal stimulus is counted for almost 3% of GDP

• 8% may not be difficult if the stimulus big enough, but market may feel still cold and unemployment still high – over capacities.

• It is “sustainable” for one or two more years .

Monetary policy?

• Quantitative management.

• Interest – rate management is constrained by the exchange-rate relationships.

Other policies!

• Investment approval and local autonomy;

• Industrial policies;

• Financial policies, such as lending policies to SMEs and mortgage/real estate.

• Land policies.

• ……

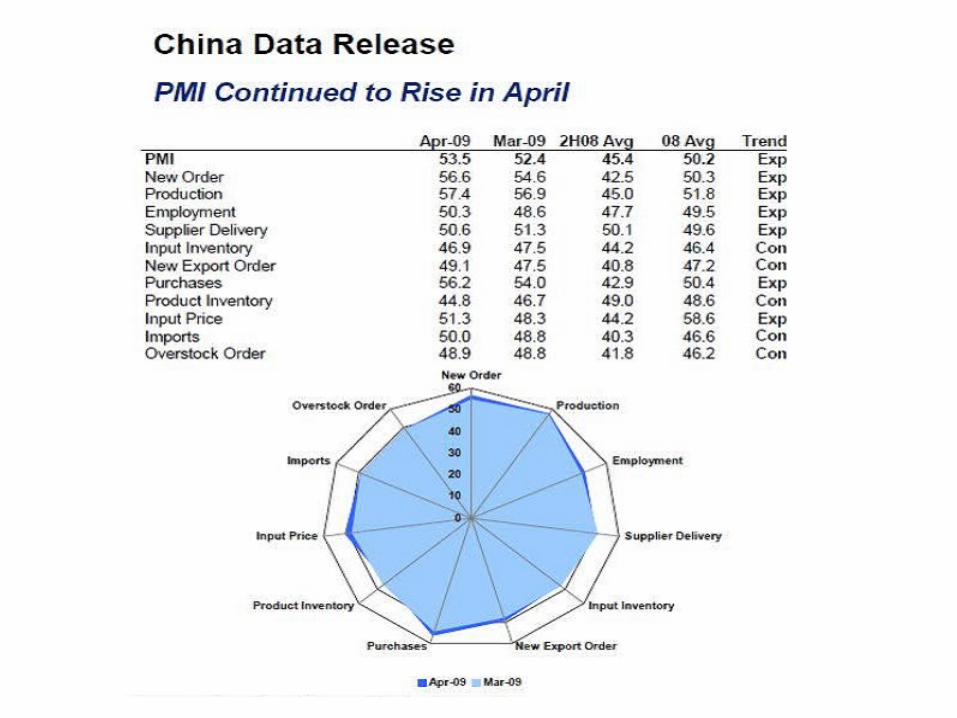

I-4. Signs of bottom-up

Figure : Import and Export Growth (%, y/y) and Monthly Trade Balance ($b)

-50

-40

-30

-20

-10

0

10

20

30

40

5006

.01

06.0

3

06.0

5

06.0

7

06.0

9

06.1

1

07.0

1

07.0

3

07.0

5

07.0

7

07.0

9

07.1

1

08.0

1

08.0

3

08.0

5

08.0

7

08.0

9

08.1

1

09.0

1

09.0

3

%

0

5

10

15

20

25

30

35

40

45

50Bil $

Trade Bal ance (Bi l $) I mport Growth Export Growth

Source: Chinese State Statistical Bureau

Figure : Change in Industrial Output and Fixed Asset Investment (y/y, %)

0

5

10

15

20

25

30

35

06.0

1

06.0

3

06.0

5

06.0

7

06.0

9

06.1

1

07.0

1

07.0

3

07.0

5

07.0

7

07.0

9

07.1

1

08.0

1

08.0

3

08.0

5

08.0

7

08.0

9

08.1

1

09.0

1

09.0

3

I ndustri al Output

Fi xed Asset I nvestment

Source: Chinese State Statistical Bureau

Figure: Change in Retail Sales of Social Consumption Goods (M/M, %)

4

9

14

19

24

29

06.0

1

06.0

3

06.0

5

06.0

7

06.0

9

06.1

1

07.0

1

07.0

3

07.0

5

07.0

7

07.0

9

07.1

1

08.0

1

08.0

3

08.0

5

08.0

7

08.0

9

08.1

1

09.0

1

09.0

3

Nomi nal seri es Real seri es

Source: Chinese State Statistical Bureau

Figure 7: Change in CPI and Ex-Factory Price Index of Industrial Products (m/m, %)

- 7- 6- 5- 4- 3- 2- 10123456789

1011

06.0

1

06.0

3

06.0

5

06.0

7

06.0

9

06.1

1

07.0

1

07.0

3

07.0

5

07.0

7

07.0

9

07.1

1

08.0

1

08.0

3

08.0

5

08.0

7

08.0

9

08.1

1

09.0

1

09.0

3

Consumer Pri ce I ndex Ex- factory Pri ce I ndex of I ndustri al Products

Source: Chinese State Statistical Bureau

1.5 Risks of monetary expansion

• The credit expansion is already over the target (RMB5 trillion);

• M2 growth rate is historically rarely high at 25.5% ;

• World commodity prices are increasing.

Naturally, people start to worry about:

• Inflation, or asset bubbles;

• Bank NPL;

Policy makers are watch too!

• Deflation is still deepen (CPI -1.5% in April, from 1.2% in March, yoy);

• Not much credit has “sneaked” into the asset market so far;

• Policy may “switch” the direction, if needed.

II. Structural Problems:

High savings and low consumption

• As observed by everyone, China’s recovery or growth is still relying on either export or investment. Consumption is still a week spot.

• And this is particularly a problem in long run given the possibility that US consumption-saving relationship may be changed (a bit) by the restructuring of financial market after the crisis.

• So, for the medium and long run, the key question remain: how China can increase its domestic consumption?

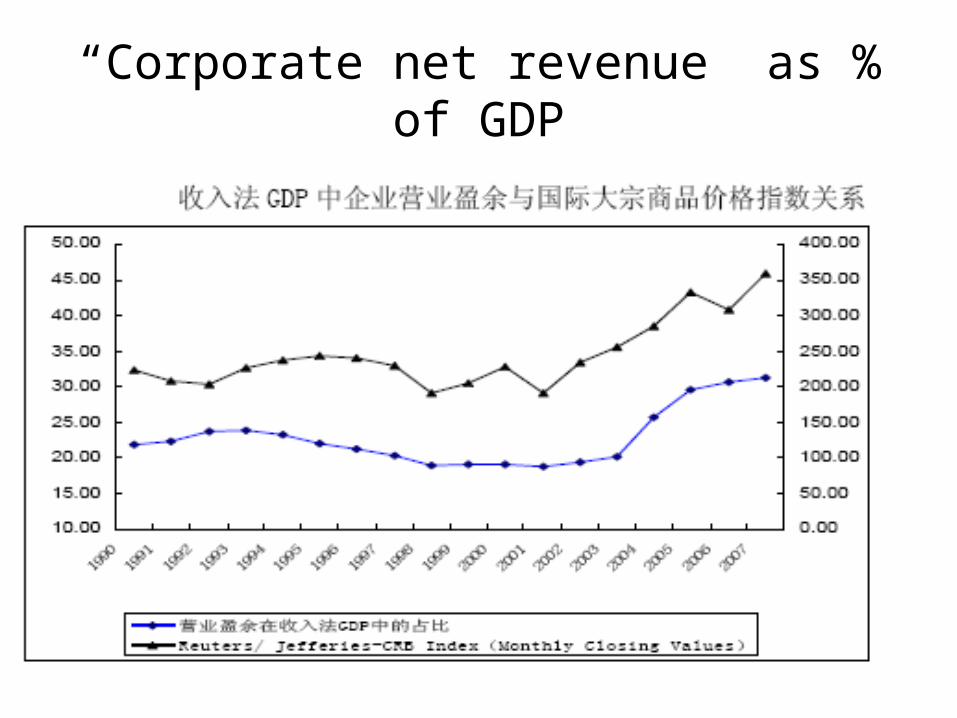

Household sector savings rate

Various sectors as % of total savings

0

10

20

30

40

50

60

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Househol d Government Corporate

Households’ disposable income / other incomes

Wage as % of GDP

“Corporate net revenue” as % of GDP

How to increase Households’ Income

• Increasing gov’t expenditures on social security/health care?

• Minimum wage increase?

• Fiscal / taxation reforms – transfers between different sectors;

• Redistribution of wealth?

III. Factors Behind

3-decades Growth and Beyond

Table, China’s Growth: Input-driven vs. Productivity Increase

(Percentage points of GDP growth rate)

1953-78 1979-88 1989-98 1999-05

Annual GDP growth 6.15 10.06 9.59 9.11

Of it: Input growth 5.83 6.70 5.16 5.36

Of it: Capital 2.59 2.58 2.70 3.59

Human captal 2.39 4.26 2.19 1.56

Productivity (TFP) 0.31 3.35 4.42 3.74

Table, Explanations to China’s Productivity Increase

1978-88 1989-98 1999-05

Total Factor Productivity

(as explained) 2.86 4.37 3.53

Market-oriented reforms 0.68 0.92 0.32

Spill-over effect of FDI 0.16 1.15 -0.35

Spill-over effect of Trade 0.46 0.19 1.33

R&D growth -0.18 0.16 0.47

Spill-over effect of Human capital 1.02 0.84 0.79

Improvement of infrastructures 0.10 0.49 1.35

Urbanization 0.78 0.74 1.35

Reduction of government costs -0.14 -0.12 -1.73

Economic Structure -0.15 0.28 0.21

Most Factors of Growth are still working

and will work for the next 10-20 years

• High savings;

• Low labor cost;

• Reform effects;

• Globalization effects;

• Education and Technology progress.

• Urbanization.