cushman & wakefield the economy cre and investment ideas -

TRANSCRIPT

Kevin J. Thorpe, Chief Economist

March 2016

The U.S. Economy, CRE Outlook and 2016 Investment Ideas

The U.S. Economy & CRE Outlook

© Copyright 2016 Cushman & Wakefield. All rights reserved.

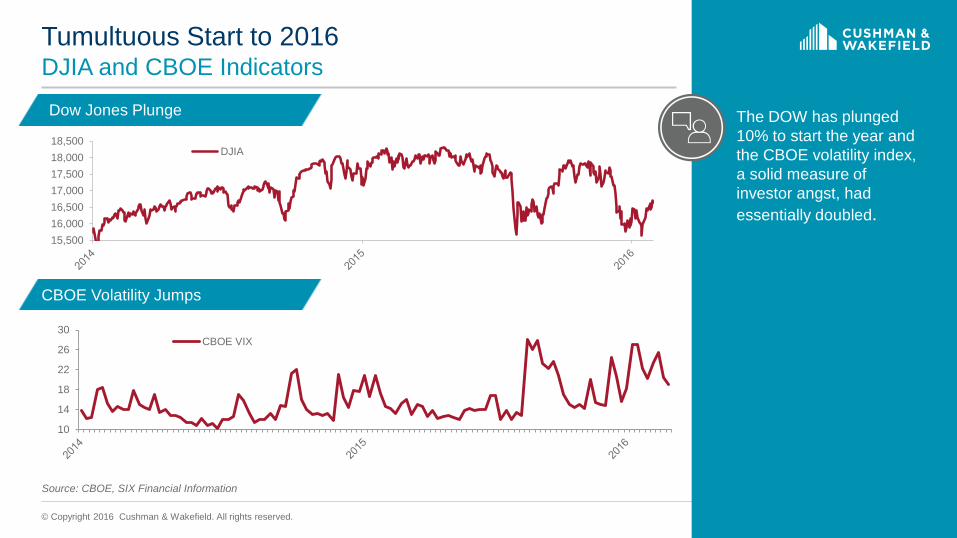

Tumultuous Start to 2016 DJIA and CBOE Indicators

The DOW has plunged 10% to start the year and the CBOE volatility index, a solid measure of investor angst, had essentially doubled.

10

14

18

22

26

30CBOE VIX

15,50016,00016,50017,00017,50018,00018,500

DJIA

Source: CBOE, SIX Financial Information

Dow Jones Plunge

CBOE Volatility Jumps

© Copyright 2016 Cushman & Wakefield. All rights reserved.

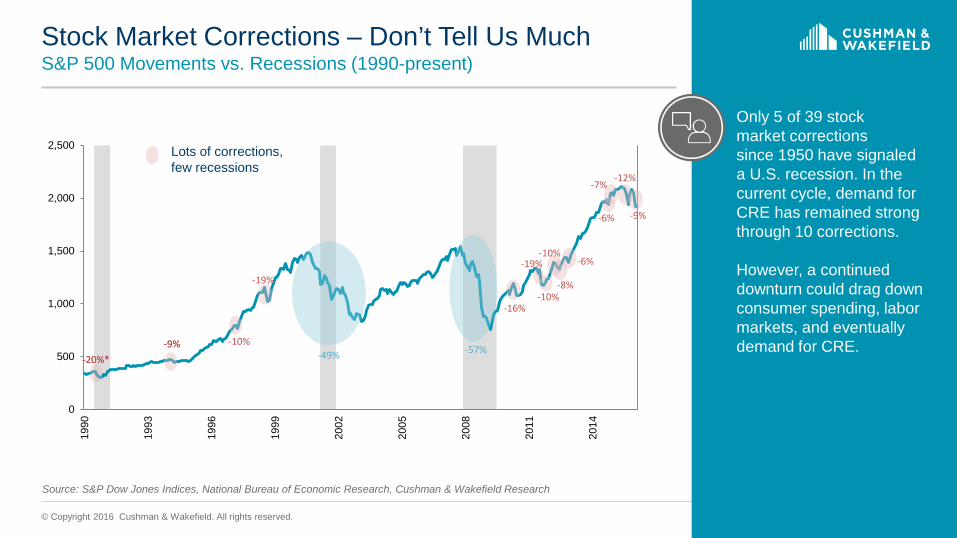

Stock Market Corrections – Don’t Tell Us Much S&P 500 Movements vs. Recessions (1990-present)

0

500

1,000

1,500

2,000

2,500

1990

1993

1996

1999

2002

2005

2008

2011

2014

-20%* -9%

-20%* -9% -10%

-19%

-49% -57%

-16%

-19%

-10%

-10%

-8%

-6%

-6%

-7% -12%

-9%

Source: S&P Dow Jones Indices, National Bureau of Economic Research, Cushman & Wakefield Research

Lots of corrections, few recessions

Only 5 of 39 stock market corrections since 1950 have signaled a U.S. recession. In the current cycle, demand for CRE has remained strong through 10 corrections. However, a continued downturn could drag down consumer spending, labor markets, and eventually demand for CRE.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Tumultuous Start to 2016

Source: Commercial Mortgage Alert

CMBS Spreads Widen

CMBS Issuance Slows

80

100

120

140

16010-Year AAA Swap

02468

101214

D J 2015 F M A M J J A S O N D J 2016 F

CMBS Issuance, $bil.

As Wall Street anxiety seeps into CRE, should investors monetize core assets? Shift real estate portfolios away from risky assets and refocus on core? Or just wait to see if it blows over?

© Copyright 2016 Cushman & Wakefield. All rights reserved.

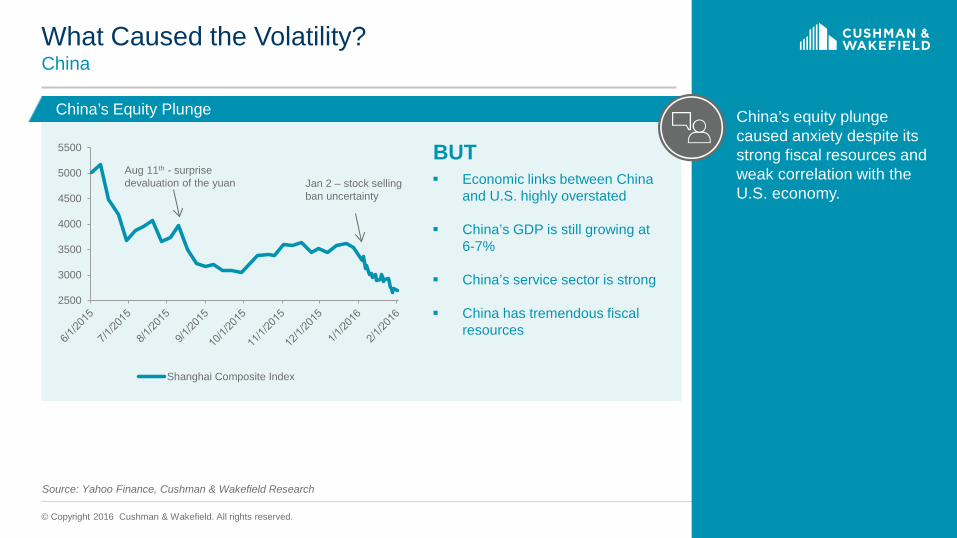

What Caused the Volatility? China

Source: Yahoo Finance, Cushman & Wakefield Research

2500

3000

3500

4000

4500

5000

5500

Shanghai Composite Index

Aug 11th - surprise devaluation of the yuan Economic links between China

and U.S. highly overstated

China’s GDP is still growing at 6-7%

China’s service sector is strong

China has tremendous fiscal resources

BUT

China’s Equity Plunge

Jan 2 – stock selling ban uncertainty

China’s equity plunge caused anxiety despite its strong fiscal resources and weak correlation with the U.S. economy.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

What Caused the Volatility? The U.S. Dollar

Source: Federal Reserve, Cushman & Wakefield Research

It’s a function of a strengthening economy

Puts downward pressure on oil and commodity prices

A stronger U.S. dollar has never caused a recession

Makes foreign goods cheaper for U.S. consumers

BUT

Strengthening U.S. Dollar

90

95

100

105

110

115

120

125

130

U.S. Dollar Broad Index

A strengthening U.S. dollar has never caused a recession but puts downward pressure on commodity prices and hurts U.S. manufacturing.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

What Caused the Volatility? Oil

Source: Moody’s Analytics, Cushman & Wakefield Research

Cheap gas is a tax break for consumers

Lowers business costs

Low oil is consistent with strong periods of U.S. GDP growth

Most CRE markets will benefit via multiplier effect

BUT

Plunge in Oil

35

45

55

65

75

85

95

105

115

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

BaselineStronger Growth ScenarioLow Oil Price Scenario

Brent Crude

The plunge in oil prices is causing discomfort, yet is favorable for lower costs for consumers and businesses.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Deflation is Still a Threat Consumer Price Index, % Change

Source: Oxford Economics, Cushman & Wakefield Research

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

2013 2014 2015

Germany Asia SpainDenmark Italy EurozoneSweden

Why should U.S. investors be concerned about deflation outside of the U.S.? If prices fall, that will in turn shrink business profits, which leads to job losses, which leads to further price cuts, then even more job losses.

Prices Fall

Profits Shrink

Job Loss

Prices Fall Further

Profits Shrink

Job Loss

Deflation by Country Potential Downward Spiral

© Copyright 2016 Cushman & Wakefield. All rights reserved.

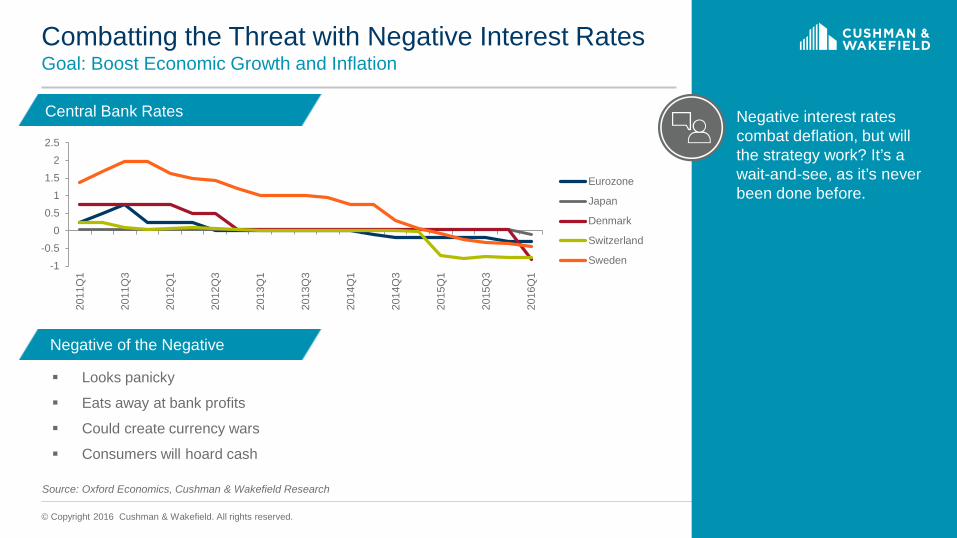

Combatting the Threat with Negative Interest Rates Goal: Boost Economic Growth and Inflation

Source: Oxford Economics, Cushman & Wakefield Research

Central Bank Rates

Negative of the Negative

-1-0.5

00.5

11.5

22.5

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

2014

Q3

2015

Q1

2015

Q3

2016

Q1

Eurozone

Japan

Denmark

Switzerland

Sweden

Looks panicky

Eats away at bank profits

Could create currency wars

Consumers will hoard cash

Negative interest rates combat deflation, but will the strategy work? It’s a wait-and-see, as it’s never been done before.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Driving Even More Foreign Capital to the U.S.

Source: Federal Reserve, Cushman & Wakefield Research

M2 Money Supply

U.S. 10-Year Treasury Yield

11000

11500

12000

12500

Jan

2014

Feb

2014

Mar

201

4

Apr 2

014

May

201

4

Jun

2014

Jul 2

014

Aug

2014

Sep

2014

Oct

201

4

Nov

201

4

Dec

201

4

Jan

2015

Feb

2015

Mar

201

5

Apr 2

015

May

201

5

Jun

2015

Jul 2

015

Aug

2015

Sep

2015

Oct

201

5

Nov

201

5

Dec

201

5

Jan

2016

M2 Money Supply, $bil.

1.7

1.9

2.1

2.3

10/2

3/15

11/6

/15

11/2

0/15

12/4

/15

12/1

8/15

1/1/

16

1/15

/16

1/29

/16

2/12

/16

2/26

/16

10-Yr Treasury Yield Adopts Negative Rate Policy

Europe

Japan

It is clear that the negative interest rate policy is driving even more capital to the United States.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Global Private Capital Fundraising for CRE

Source: Preqin, Cushman & Wakefield Research Forecast

706

600

$0

$100

$200

$300

$400

$500

$600

$700

$80019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

F

Aggregate Capital Raised, $Bill.

Recent strong fundraising for CRE is due, in part, to volatility in other asset classes such as oil, commodities, and stocks causing capital to be rechanneled to real estate.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

U.S. Job Growth Is Booming Strongest Job Growth Years Since 1990

Source: U.S. Bureau of Labor Statistics

0

0.5

1

1.5

2

2.5

3

3.5

4

1994 1998 1997 1999 1995 2014 2000 1989 2015 1996

Job Growth, Mill.

1st

6th 9th

Full potential of job growth has not been felt because productivity is weaker than normal; underemployment is still elevated; labor force participation has been weak; wage growth has been weak. From a CRE perspective, no single factor is more important than job creation – and that remains very healthy.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

127

129

131

133

135

137

139

141

143

145

Nov

200

0

Jul 2

002

Mar

200

4

Nov

200

5

Jul 2

007

Mar

200

9

Nov

201

0

Jul 2

012

Mar

201

4

Nov

201

5

Total Nonfarm, mils

U.S. Employment Growth

Source: U.S. Bureau of Labor Statistics

Monthly Change (000’s): Job losses peak to trough: 8,716,000

Job gains in recovery: 13,251,000 Total Nonfarm

Office -Using

Dec 2014 292 77

Jan 2015 221 31

Feb 2015 265 52

Mar 2015 84 36

Apr 2015 251 86

May 2015 273 91

Jun 2015 228 99

Jul 2015 277 71

Aug 2015 150 45

Sep 2015 149 56

Oct 2015 295 107

Nov 2015 280 48

Dec 2015 271 78

Jan 2016 172 35

Feb 2016 242 41

Job growth surged in February and job openings remain at record levels indicating businesses still want to hire aggressively.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Investors are Drawn to the Jobs Major Markets: Top 25 Job-Producing Cities in 2015

Source: BLS, Oxford Economics, RCA, Cushman & Wakefield Research

Job losses peak to trough: 8,716,000

Job gains in recovery: 13,251,000

Rank in Job Growth

Rank in Sale Volume Market Job Growth 000's

1 240 New Delhi 204.4 2 1 New York 144.7 3 3 Los Angeles 139.4 4 2 London 122.6 5 11 Dallas 113.2 6 324 Tianjin 106.2 7 47 Beijing 106.1 8 45 Singapore 82 9 13 Atlanta 84.4 10 5 San Francisco 71.4 11 10 Miami 67.8 12 4 Hong Kong 65.1 13 23 Melbourne 60.5 14 15 Seattle 62.6 15 6 DC Metro 60.6 16 19 Houston 57.6 17 8 Chicago 55.4 18 28 Madrid 53.8 19 14 San Jose 53.4 20 20 Phoenix 51.3 21 9 Boston 51.3 22 17 Sydney 48.4 23 N/A Riverside 48.2 24 30 Orlando 44.2 25 21 San Diego 40.6

These 16 U.S. cities accounted for $286 billion in transactions last year, representing 1/3 of global sales activity.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

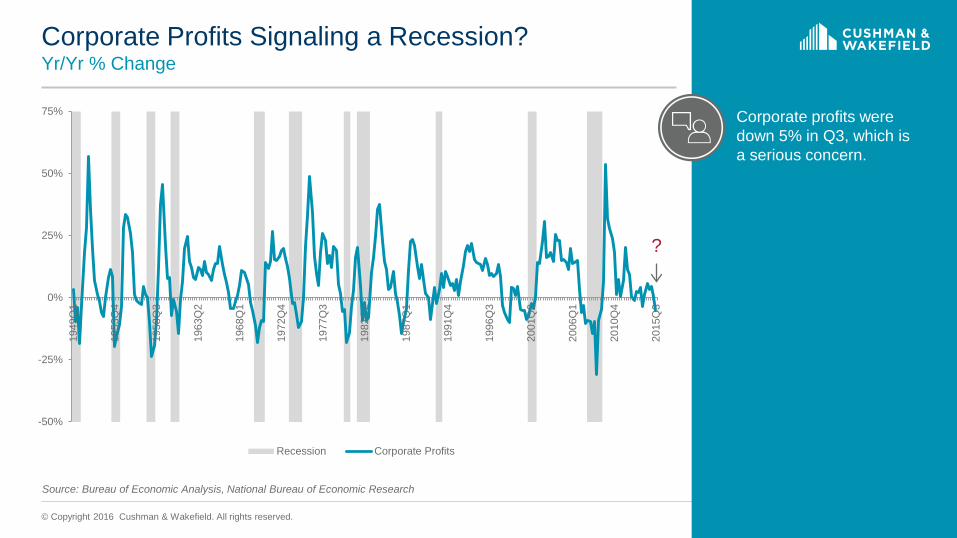

Corporate Profits Signaling a Recession? Yr/Yr % Change

Source: Bureau of Economic Analysis, National Bureau of Economic Research

Job gains in recovery: 13,251,000

33% of Global Sales Activity

Occurs in these U.S. Cities

-50%

-25%

0%

25%

50%

75%

1949

Q1

1953

Q4

1958

Q3

1963

Q2

1968

Q1

1972

Q4

1977

Q3

1982

Q2

1987

Q1

1991

Q4

1996

Q3

2001

Q2

2006

Q1

2010

Q4

2015

Q3

Recession Corporate Profits

Corporate profits were down 5% in Q3, which is a serious concern.

?

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Probably Not Corporate Profits by Sector (Yr/Yr % Change, Q3 2015 vs Q3 2014)

Source: Bureau of Economic Analysis, National Bureau of Economic Research

Job gains in recovery: 13,251,000

33% of Global Sales Activity

Occurs in these U.S. Cities

-43.0%

-15.0%

-12.8%

-3.2%

-1.1%

2.0%

2.5%

9.5%

12.6%

14.5%

16.3%

17.4%

17.8%

18.5%

19.1%

19.9%

23.9%

34.8%

42.5%

86.7%

-60% -40% -20% 0% 20% 40% 60% 80% 100%

Utilities

Machinery

Petroleum & Coal

Other Nonfinancial

Wholesale Trade

Other Durable Goods

Financial

Fabricated Metal

Non-Durable

Retail

Manufacturing

Electrical Equip & Components

Other Non-Durable Goods

Food & Beverage

Information

Durable Goods

Chemical Products

Transport & Warehousing

Computer & Electronics

Motor Vehicles & Parts

Only 3.5% of total domestic profits

6.6% of total domestic

16% of total domestic profits

Outside of energy, most businesses and sectors in the U.S. economy are growing. It is projected that corporate profits in non-energy sectors grew by 3% in Q4 2015.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

U.S. Macro Forecast Updated February 26, 2016

Source: Various, Cushman & Wakefield Research Forecasts

Job gains in recovery: 13,251,000

33% of Global Sales Activity

Occurs in these U.S. Cities

>> Click here for full analysis from our latest U.S. Macro Report

2015 2016 Annual Q2 Q3 Q4 Q1 Q2 Q3 Q4 2015 2016 2017

U.S. Economy Real GDP, % 3.9 2.0 1.0 1.1 2.9 3.0 3.2 2.5 2.4 2.8 Nonfarm Employment, 000 610 623 720 726 763 636 520 2,890 2,645 2,329 Office-using Employment, 000 219 192 210 198 195 136 184 827 713 666 Unemployment Rate, % 5.4 5.2 5.0 4.9 4.8 4.7 4.8 5.3 4.8 4.9 Retail Sales & Food Services, % 6.8 4.5 0.8 6.1 5.7 4.7 3.6 2.1 4.8 4.4 CPI Inflation, % 3.0 1.6 0.8 0.8 1.4 2.2 2.1 0.2 1.6 2.1 CCI 96 98 96 99 104 102 103 98 102 104 Fed Funds Rate, % 0.1 0.1 0.2 0.3 0.5 0.8 0.8 0.1 0.6 1.6 10-year Gov't Bond, % 2.0 2.2 2.2 2.0 2.1 2.5 2.7 2.3 2.4 2.9 ISM Manufacturing Index 52.6 51.3 49.7 47.6 48.1 50.0 51.0 51.6 49.2 54.3 West Texas Intermediate, $/bbl 58 47 42 36 38 42 49 49 41 57 Office Sector Net Absorption, msf 22.7 20.8 21.3 20.7 23.2 21.7 20.9 81.8 86.5 77.4 Vacancy 14.4% 14.2% 13.9% 13.7% 13.5% 13.1% 13.1% 14.2% 13.4% 13.0% Asking Rents $27.45 $27.91 $28.28 $28.46 $28.60 $29.00 $29.26 $27.72 $28.83 $30.13 Industrial Sector Net Absorption, msf 61.7 55.9 62.8 52.1 61.8 59.3 47.1 234.7 220.3 154.0 Vacancy 7.7% 7.5% 7.2% 7.0% 6.9% 7.0% 7.0% 7.5% 7.0% 7.1% Asking Rents $5.35 $5.37 $5.45 $5.50 $5.59 $5.64 $5.74 $5.36 $5.62 $5.99 Retail Sector* Net Absorption, msf 9.5 13.9 11.2 10.4 12.1 14.8 9.0 40.0 46.3 37.5 Vacancy 7.8% 7.6% 7.5% 7.3% 7.2% 7.0% 6.9% 7.7% 7.1% 7.3% Asking Rents $23.14 $23.10 $23.24 $23.40 $23.34 $23.75 $23.85 $22.92 $23.59 $24.06

Top CRE Investment Ideas

Buy Government Towns

#9

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Buy Government Towns Worst of Fiscal Drag is Over

With history as a guide, when tax revenues are coming in, the government finds a way to spend them.

Source: Congressional Budget Office, OMB

Federal Deficit Has Stabilized Deficit spending as % of GDP

Federal Spending Will Grow

-10%-8%-6%-4%-2%0%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

CBO - Forecast OMB - Forecast Moody's - Forecast

-4%

1%

6%

11%

16%

21%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

e

2016

e

2017

e

2018

e

2019

e

2020

e

Federal Outlays YOY Growth

Average

© Copyright 2016 Cushman & Wakefield. All rights reserved.

2014 2015 Trend

DC Metro 19.3 60.6

NoVa 1.0 25.3

Baltimore 12.4 28.0

Buy Government Towns

Source: Consolidated Report on Federal Funds, BLS, Cushman & Wakefield Research

Highest Fed Spend Major Markets

0% 10% 20% 30% 40%

U.S.

Baltimore

Northern VA

DC Metro

Fed Spending as % GDP

Job Growth Momentum, 000’s

Cap Rate Spread vs. Peers

DC 5.8%

New York 4.4%

Spread 140 bps

Baltimore 7.0%

Oakland 6.3%

Spread 70 bps

When federal spending increased last year, job growth in the DC, Northern Virginia and Baltimore markets began to soar.

Buy Sunbelt Markets

#8

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Buy Sunbelt Markets Job Growth Booms in Sunbelt

Top 30 Job-Producing Markets Top 25 Office Absorption Markets 2015

Rank City 2015 (000s) 1 New York 144.8 2 Los Angeles 139.4 3 Dallas 113.2 4 Atlanta 84.4 5 San Francisco 71.4 6 Miami 67.8 7 Seattle 62.6 8 DC Metro 60.6 9 Houston 57.5 10 Chicago 55.4 11 San Jose 53.9 12 Phoenix 51.4 13 Boston 51.3 14 Riverside 48.2 15 Orlando 44.2 16 Detroit 44.0 17 San Diego 40.7 18 Denver 38.3 19 Charlotte 37.1 20 Portland, OR 34.7 21 Minneapolis 34.5 22 Tampa 33.7 23 Philadelphia 33.5 24 San Antonio 33.1 25 Austin 30.0 26 Indianapolis 28.6 27 Baltimore 28.0 28 Nashville 26.2 29 Las Vegas 25.5 30 Salt Lake City 23.4

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Seat

tleAu

stin

Nas

hville

San

Jose

Ral

eigh

/Dur

ham

New

Hav

en, C

TO

rland

oC

olor

ado

Spr

ings

East

Bay

Phoe

nix

San

Mat

eo, C

AFo

rt M

yers

, FL

Tam

paSa

lt La

ke C

itySa

n Fr

anci

sco

Cin

cinn

ati

Jack

sonv

illeM

iam

iD

alla

sC

olum

bus

Atla

nta

Los

Ang

eles

Mem

phis

Den

ver

St. P

eter

sbur

g, F

L

Net Absorption as % of Inv.

The sunbelt region has dominated in nearly every relevant economic growth metric for the past 30 years.

Source: BLS; Cushman & Wakefield Research

Sell Core to Aggressive Foreign Capital

#7

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Sell Core to Aggressive Foreign Capital

Source AFIRE, Cushman & Wakefield Research

Job gains in recovery: 13,251,000

% of Foreign Capital in 2015

10%

12%

17%

18%

22%

23%

28%

31%

39%

53%

0% 10% 20% 30% 40% 50% 60%

Chicago

Los Angeles

DC VA burbs

Atlanta

Houston

Seattle

Boston

San Francisco

Manhattan

DC

Foreign investors are attracted to trophy office space in gateway cities and have been paying a premium for it.

AFIRE’s Top U.S. Targets

1. New York

2. Los Angeles

3. San Francisco

4. Washington, DC

5. Boston and Seattle

Buy Secondary Tech Markets

#6

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Waves of Innovation

Source:The Kondratiev Cycles

33% of Global Sales Activity

Occurs in these U.S. Cities

The Kondratiev Cycles | Long-term Technology & Growth Cycles

1785 1845 2020 1990 1950 1900

Inno

vatio

n

Iron Water power

Mechanization Textiles

Commerce

Steam power Railroad

Steel Cotton

Electricity Chemicals

Combustion engine

Petrochemicals Electronics

Aviation Space

Digital networks Biotechnology

Software IT 1st

2nd 3rd

4th

5th

6th

Hydraulic fracking 3D printing Mobile tech

Social media Data mining

Cloud computing Bioscience

Green chemistry

The tech boom is not just a hot trend; although the trajectory will bend at times, the current wave of innovation will drive economic growth for many years.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Tech Hubs and Office Rent Growth Percent of Jobs in Technology Industries & Change in Rent Since 2010

Source: Cushman & Wakefield Research

U.S. 6.5%

Seattle 10.7%

Portland 11.9%

San Francisco 110.8%

San Jose 36.2%

Denver/Boulder 19.0%

Austin 30.6%

Washington, DC 6.1%

New York 53.0%

Boston 18.2%

9.9% 8.2%

9.6%

8.8%

12%

26.5%

10.6%

8.7%

7.6%

4.7% Technology sectors share of workforce

Change in rent since 2010

Core tech markets are hot and engines remain strong, but are bumping up against labor shortages and housing affordability issues.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Buy Secondary Tech Markets

Salt Lake City, UT High tech employment has risen by 25% since 2010. Housing very affordable.

Oakland, CA 12 miles from tech hub SF/San Jose; office vacancy of 12% vs. 5.7% in SF. Rents 64% cheaper.

Los Angeles - Downtown West LA vacancy is 11.6%; rest of LA 15-20% vacant, $20 rent delta suggests demand will spread.

Northern VA Proximity to DC, highly educated, elevated office vacancy of 20% due to gov’t spending cuts; lots of trained gov’t contractors looking for work.

Atlanta, GA Midtown drawing tech firms from suburban locations. 66% of residents are Gen Y or Gen Z. 90% success rate for tech firms.

Chicago, IL Tech-related hiring exploding downtown/River North. Huge talent pool and concentration of service sectors. Expanding footprint while finance/law are downsizing. Known for tech incubators.

Minneapolis, MN Hottest in periphery of Minneapolis core — central locations, but not typical class A office space. Warehouse District (the main tech center) and near-downtown locations are drawing demand.

Phoenix, AZ Low cost of living, doing business (rents, home prices). Some major firms already are shifting back-end office here due to cost advantage. South Scottsdale and Tempe North markets attracting tenants despite high rents due to “Live/Work/Play” atmosphere.

Raleigh-Durham, NC Downtown Durham is being revitalized as old tobacco warehouses are turning mixed-use. Despite highest rents, continues to draw demand from tech tenants. Similar story for Raleigh’s Downtown.

Midtown Manhattan Tech firms (TAMI), not Wall Street, are gobbling up space in Midtown South where vacancy is now 6.6%. Tech will roll into Downtown/Financial District where vacancy 2x higher & rents $15 cheaper.

Buy Europe

#5

© Copyright 2016 Cushman & Wakefield. All rights reserved.

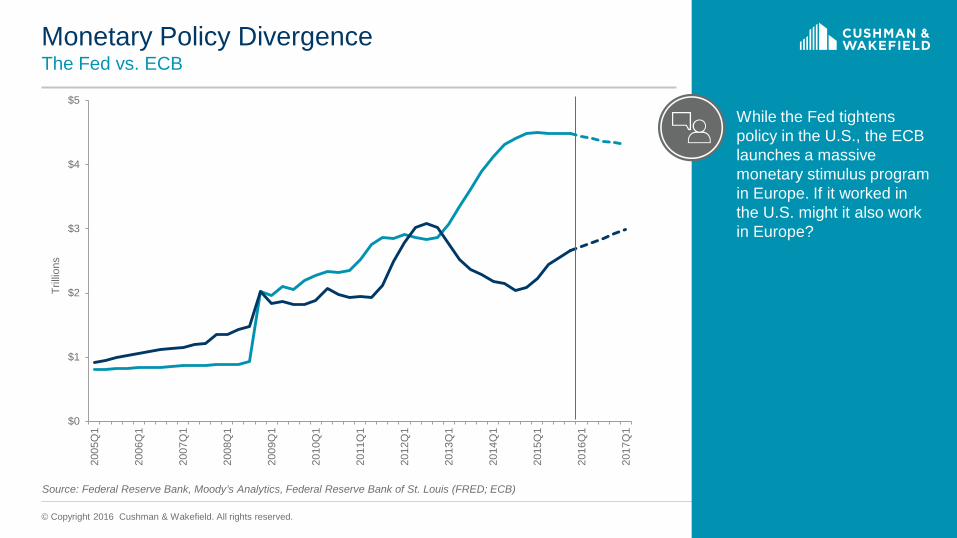

Monetary Policy Divergence The Fed vs. ECB

Source: Federal Reserve Bank, Moody’s Analytics, Federal Reserve Bank of St. Louis (FRED; ECB)

$0

$1

$2

$3

$4

$520

05Q

1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

Q1

Trill

ions

While the Fed tightens policy in the U.S., the ECB launches a massive monetary stimulus program in Europe. If it worked in the U.S. might it also work in Europe?

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Office Rent Growth: Who’s Hot, Who’s Not Prime Rents: % Change Q3 2015/Q3 2014

Source: Cushman & Wakefield Research

-10%

-5%

0%

5%

10%

15%

20%

HOT

NOT

Leasing fundamentals in Dublin and London are hot, but as quantitative easing trickles into the broader economy, expect to see significant run-up in values throughout Europe.

Buy Industrial Infill

#4

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Follow the Supply Chain

Source: Cushman & Wakefield Research

The “sweet spots” are areas between population centers, railroads and the interstate highways which have a geographical advantage to get products to large population centers.

KEY Sweet Spots Intermodal, Inland Ports, and Inland Population Centers

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Follow the Supply Chain

Source: Cushman & Wakefield Research

70% of all U.S. industrial absorption occurred in these markets in 2015.

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Buy Infill Warehouse 2015 Change in Rents by Type (Yr/Yr, % Change)

4.3% 3.6%

8.8%

0%

2%

4%

6%

8%

10%

All Industrial Distribution/E-commerce Infill Warehouse

Source: CoStar, Cushman & Wakefield Research

Infill warehouse rent increases in 2015 were double those of other industrial categories.

Buy Class A Neighborhood Shopping Centers

#3

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Buy Class A Neighborhood Shopping Centers

Source: Real Capital Analytics, Cushman & Wakefield Research

Retail Cap Rates By Product Type More Upside in Secondary Markets

Boston Chicago LA Miami New York Philadelphia San

Francisco DC

Regional Mall

(All Classes) 6.1% 7.3% 6.3% 6.0% 6.0% 6.4% 6.1% 6.3%

Regional Mall

(Class A) 4.7% 5.1% 4.3% 4.6% 4.0% 4.6% 4.0% 4.4%

Shopping Centers

(Class A) 6.9% 7.5% 6.6% 7.0% 6.0% 7.0% 5.9% 6.7%

Urban Retail (All Classes) 5.4% 6.5% 5.6% 5.6% 5.2% 5.8% 5.1% 5.3%

Urban Retail (Class A) 4.4% 5.1% 4.9% 4.5% 4.0% 4.5% 4.0% 4.6%

Market Cap Rate (2015)

Nashville 7.5%

Minneapolis 7.4%

Charlotte 7.4%

Atlanta 6.9%

Dallas 6.8%

Baltimore 6.4%

Philadelphia 6.3%

There is room for cap rate compression in class A neighborhood shopping centers.

Build/Buy Multifamily in Non-Gateways

#2

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Multifamily Markets with Lower Vacancy than U.S. Average As of Q4 2015

67% of the U.S. has vacancy

below 5%

The apartment sector is booming across the country. You don’t have to play in the major metros to do well in multifamily.

Source: REIS

Rank Vacancy < 3%

1 New Haven 2 Central New Jersey 3 Sacramento 4 Rochester 5 Syracuse 6 Detroit 7 Oakland-East Bay 8 Buffalo 9 San Bernardino/Riverside

10 San Diego 11 Tacoma

Vacancy < 5% 33 Omaha 34 San Francisco 35 Suburban Maryland 36 Wichita 37 Knoxville 38 Miami 39 St. Louis 40 Fort Worth 41 Northern New Jersey 42 Salt Lake City 43 Tampa-St. Petersburg 44 Richmond 45 U.S. Average = 4.4% 46 Fort Lauderdale 47 Charlotte 48 Greenville 49 Kansas City 50 Suburban Virginia 51 Phoenix 52 Tucson 53 Las Vegas

Vacancy < 4% 12 Orange County 13 Providence 14 Ventura County 15 New York 16 Cincinnati 17 Westchester 18 Cleveland 19 Long Island 20 Los Angeles 21 Philadelphia 22 Hartford 23 Albuquerque 24 Baltimore 25 Dayton 26 Chicago 27 Colorado Springs 28 Milwaukee 29 Pittsburgh 30 Lexington 31 Minneapolis 32 San Jose

Don’t Bet Against the Cycle Quite Yet

#1

© Copyright 2016 Cushman & Wakefield. All rights reserved.

Don’t Bet Against the Cycle

This may be the longest expansion in the history of United States.

Probability Expansion Continues A Few Points to Keep in Mind:

84%

78%

80%

82%

84%

86%

88%

90%

92%

94% Leading indicators still okay

U.S. financial system is sound

Tailwinds still exist: M2 money

supply surge, low interest rates and low oil

Central banks are still stimulating

Source: Moody’s

Kevin J. Thorpe, Chief Economist

March 2016

The U.S. Economy, CRE Outlook and 2016 Investment Ideas