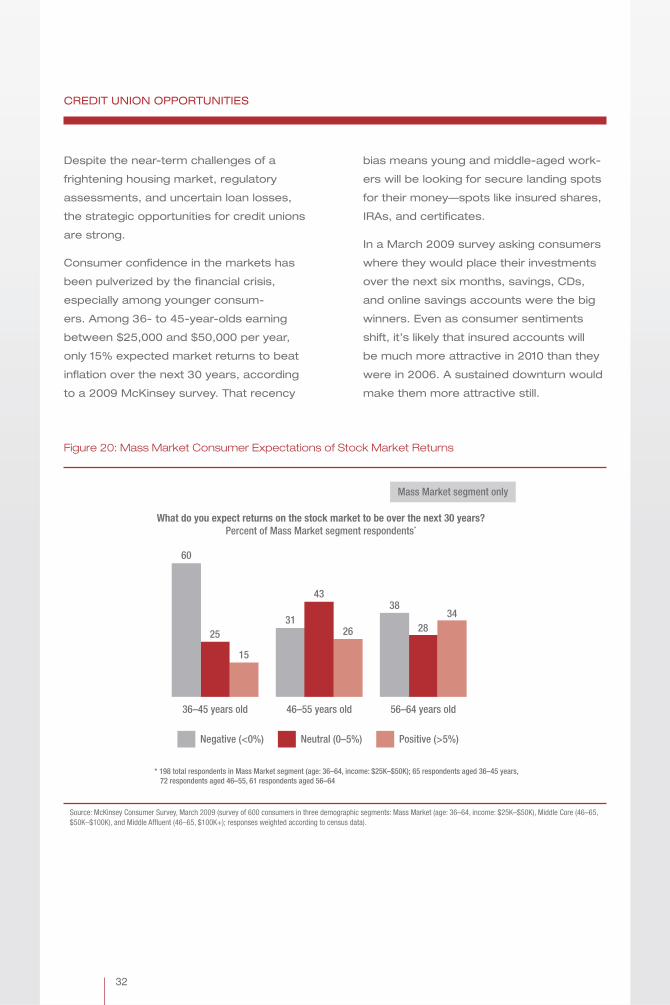

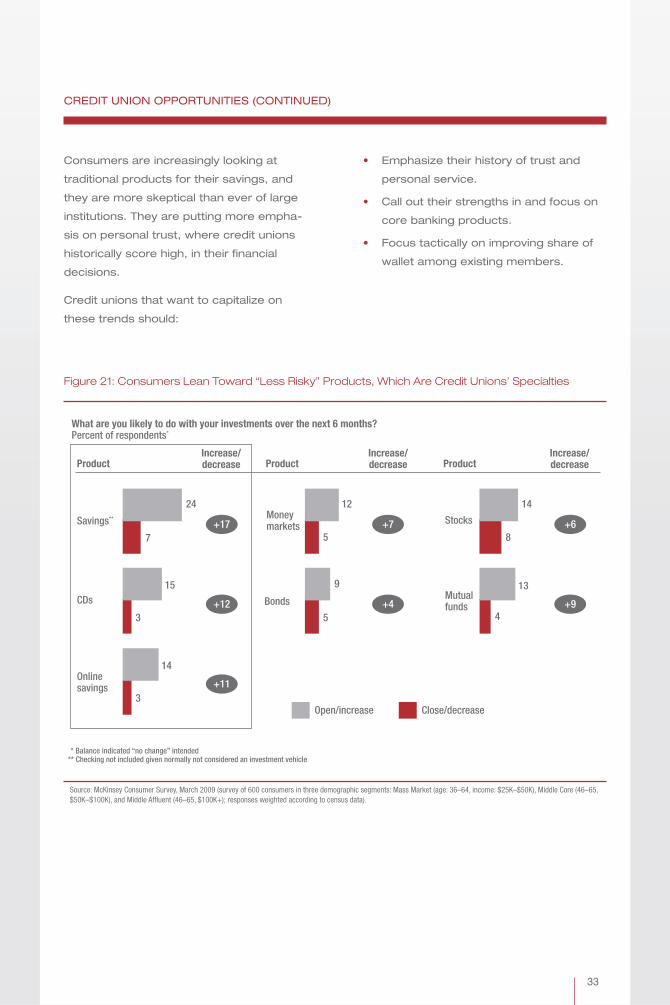

customer experience and credit union a … experience and credit union opportunities: a...

TRANSCRIPT

Cu

sto

mer E

xp

erie

nce a

nd

Cre

dit U

nio

n O

pp

ortu

nitie

s

Customer Experience

and Credit Union

Opportunities:

A Collaboration with

McKinsey & Company

Mark MeyerCEO, Filene Research Institute

Ben RogersResearch Director, Filene Research Institute

Foreword by Dorian StonePartner, McKinsey & Company

Filene Research Fellow

ideas grow here

PO Box 2998

Madison, WI 53701-2998

Phone (608) 231-8550

PUBLICATION #203 (1/10)

www.filene.org ISBN 978-1-932795-82-0

ISB

N 978-1-932795-82-0

Customer Experience

and Credit Union

Opportunities:

A Collaboration with

McKinsey & Company

Mark MeyerCEO, Filene Research Institute

Ben RogersResearch Director, Filene Research Institute

Foreword by Dorian StonePartner, McKinsey & Company

Filene Research Fellow

Copyright © 2010 by Filene Research Institute. All rights reserved.ISBN 978-1-932795-82-0Printed in U.S.A.

Deeply embedded in the credit union tradition is an ongoing search for better ways to understand and serve credit union members. Open inquiry, the free flow of ideas, and debate are essential parts of the true democratic process.

The Filene Research Institute is a 501(c)(3) not-for-profit research organization dedicated to scientific and thoughtful analysis about issues affecting the future of consumer finance. Through independent research and innovation programs the Institute examines issues vital to the future of credit unions.

Ideas grow through thoughtful and scientific analysis of top-priority consumer, public policy, and credit union competitive issues. Researchers are given considerable latitude in their exploration and studies of these high-priority issues.

The Institute is governed by an Administrative Board made up of the credit union industry’s top leaders. Research topics and priorities are set by the Research Council, a select group of credit union CEOs, and the Filene Research Fellows, a blue ribbon panel of academic experts. Innovation programs are developed in part by Filene i3, an assembly of credit union executives screened for entrepreneurial competencies.

The name of the Institute honors Edward A. Filene, the “father of the U.S. credit union movement.” Filene was an innova-tive leader who relied on insightful research and analysis when encouraging credit union development.

Since its founding in 1989, the Institute has worked with over one hundred academic institutions and published hundreds of research studies. The entire research library is available online at www.filene.org.

Progress is the constant replacing of the best there

is with something still better!

— Edward A. Filene

iii

Filene Research Institute

iv

For their help with, and participation in, this important customer experience research, the Filene Research Institute would like to thank Dorian Stone, Filene Research Fellow and Partner, McKinsey & Company, San Francisco; and Kurt MacAlpine, Senior Engagement Manager, McKinsey & Company, Toronto. We would also like to thank the participants at each of our roundtables:

Linda Armyn, Bethpage Federal Credit Union, Bethpage, New York

Barbara Bass, Credit Union League of Connecticut, MeridenMichelle Bloedorn, Member Loyalty Group, ChicagoKathy Chartier, Members Credit Union, Stamford, ConnecticutJeanne Denton, Nikkei Credit Union, Gardena, CaliforniaBrent Dixon, The Haberdashery, Brooklyn, New YorkBruce Fafard, Ledge Light Federal Credit Union, Groton,

ConnecticutRebecca Gerothanas, Summit Credit Union, Madison, WisconsinLisa Ginter, CommunityAmerica Credit Union, Lenexa, KansasLori Hall, American Airlines Federal Credit Union, Fort Worth,

TexasLucy Ito, California/Nevada Credit Union League, Rancho

Cucamonga, CaliforniaSteve Koenen, Altra Federal Credit Union, La Crosse, WisconsinRandy Kohout, CUNA Mutual Group, Madison, WisconsinKen Landis, Pasadena Service Federal Credit Union, Pasadena,

CaliforniaCaroline Lane, Co-Op Financial Services, Rancho Cucamonga,

CaliforniaJean-Albert Maisonneuve, Affinity Federal Credit Union, Basking

Ridge, New JerseyConnie Mattis, Service 1st Federal Credit Union, Danville,

Pennsylvania

Acknowledgments

v

AcknowledgmentsAngela McCathran, People’s Trust Federal Credit Union, Houston, Texas

Tara McQuillen, Discovery Federal Credit Union, Wyomissing, Pennsylvania

Robert Michaud, Mid-Hudson Valley Federal Credit Union, Kingston, New York

Heather Nally, Purdue Employees Federal Credit Union, West Lafayette, Indiana

Kerry Parker, A+ Federal Credit Union, Austin, TexasJohn Parsons, First City Credit Union, Los AngelesPete Paulson, Corporate America Family Credit Union, Elgin,

IllinoisCarey Price, Baxter Credit Union, Vernon Hills, IllinoisDaniel Ptacek, United Nations Federal Credit Union, New YorkJon Reske, UMassFive College Federal Credit Union, Hadley,

MassachusettsCathy Rios, Travis Credit Union, Vacaville, CaliforniaLynda Savoit, Orange County’s Credit Union, Santa Ana,

CaliforniaPatricia Shermot, CTCE Federal Credit Union, Reading,

PennsylvaniaTansley Stearns, Connex Credit Union, North Haven,

ConnecticutChristopher Stevenson, Credit Union Executives Society,

Madison, WisconsinJoanne Todd, Northeast Family Federal Credit Union,

Manchester, ConnecticutJennifer Ventimiglia, USA Federal Credit Union, San DiegoSuzanne Walden, Chevron Federal Credit Union, Oakland,

CaliforniaJoni Walker, Missoula Federal Credit Union, Missoula, MontanaFrank Weidner, Alliant Credit Union, ChicagoJason Werts, Unitus Community Credit Union, Portland, Oregon

vii

Foreword ix

Executive Summary and Commentary xi

About the Authors xv

Chapter 1 Stellar Customer Satisfaction: Opportunity or Achilles’ Heel? 1

Chapter 2 Defining and Improving Customer Experience 11

Chapter 3 Frontline Performance and Customer Experience 21

Chapter 4 Conclusion and Recommendations 37

Endnotes 41

Table of Contents

ix

By Dorian Stone,Partner, McKinsey & Company, and

Filene Research Fellow

Recently overheard: “I have the best insurance agent; I even got money back from my insurer last year since it’s a mutual. I’ll miss them now that I’m switching.”

This consumer’s love-lost story is a common and pervasive one across financial services. Over the past 10 years, property and casualty mutual insurers have lost 2% of market share in premiums. That per-centage could have been even bigger if the larger mutual players had not moved as aggressively as they did on price. Mutual life insurers have lost a full 40% of their market share (partly due to conversions to public companies). In that same time, credit unions have lost 3% market share of deposits even against banks smaller than $20 billion (B). In many of these cases cooperative members are voting not at their annual meetings, but instead with their wallets at the offices of for-profit competitors.

For decades credit unions have done a lot for their members and deserve their place at the top of the customer satisfaction rankings. Today, as a segment, they have the highest ratings—with small banks following closely. But top customer satisfaction ratings can be achieved in multiple ways, and different methods have profound impacts on consumer choices on deposits, loans, and investments and on the ultimate economic impact on the institution. In fact, credit union efficiency consistently fell short of even the smallest banks in the nation until the economic collapse last year.

What we’ve found at McKinsey is that banks and financial institu-tions that are winning market share compensate for “good enough” customer satisfaction relative to the top marks of credit unions by investing heavily in the convenience and functionality elements of their product and service delivery. By doing so, they have achieved a higher ROI on their customer experience performance that better reinforces their economic position relative to credit unions.

Looking across the industry, high-performing banks have long driven functional improvements into and across offers and channels. They have invested in branches, sophisticated electronic delivery, and sales staff. They have, however, lagged in most cases on the emotional elements of the customer experience. Moreover, banks make explicit decisions about whom they are targeting and what measures they deem as successful in winning those customers. These banks know they can’t please all of the people all of the time. As a result, they make better trade-offs and decisions about where to invest, who to prioritize in the use of those investments, and how to resolve com-plaints that arise.

Foreword

x

In contrast, many credit unions make explicit decisions to please every member every time, to support every community as best as possible, and to hold on to every employee as long as possible. As a result, credit unions launch offers with high degrees of built-in compromise, keep the wrong employees, and succeed in diverting resources from critical functional operations.

Today, creating a stronger emotional bond and a more personal frontline experience is a key differentiator for banks—but it is not a differentiator for the average credit union. Why? Because credit unions have forgotten to build the basic quality of service and offerings that create fundamental value in consumers’ eyes. Credit unions—and mutuals more broadly—underperform on that func-tional value across most industries.

Exacerbating the situation, most credit unions are building addi-tional goodwill through a continued emphasis on emotional ele-ments like consumer trust and personal touch in the customer interaction rather than on consistently getting the basics right. More-over, many credit unions often target customer experience excellence as a goal in and of itself rather than as a means to an end. Customer experience is a means to greater share of wallet, greater efficiency in serving that customer and, ultimately, greater institutional value.

This report shows that in transitional times like these, credit unions may survive by maintaining that historical goodwill—but they can-not win without a focus on delivering functional as well as emotional value to the consumer, and doing so in a more effective manner.

In the last 12 to 24 months, many credit unions may have been lulled into believing that the windfall of deposits they have experi-enced is a sign of longer-term shifts in consumer preference for the average credit union. However, as we shared at a number of credit union system conferences last year, our research suggests that this is a short-lived window of opportunity. Depending on the near-term stability of the banking sector, that window may close too quickly for the typical credit union to make use of it.

xi

By Ben Rogers,Research Director

Every high school has a Tom. He’s a decent student, and he’ll attend an OK college. He’s on the cross-country team but finishes most races out of the top 10. His pants are a few years past the going style. Tom is earnest and sincere, and actually pretty fun once you get to know him. His sincerity has won him the confidence of many of the girls.

But Tom has one big hang-up. When it comes to serious dating, Tom always strikes out. He can get a date to the dance, but long-term, steady relationships are where he falls short. It annoys Tom to watch his friends fall for the wrong guys time after time—the jerk with the nice car or the slacker who lives to party. Tom knows those guys aren’t right for his friends, and deep down his friends usually know it, too.

Every girl likes Tom well enough, but none of them will commit to him. “Credit unions seem to be like the guy who’s best friends with every girl in school but can’t get a date,” says Brent Dixon, a young adult advisor at the Filene Research Institute. Credit unions are like Tom.

What Is the Research About?This report, a collaboration between the Filene Research Institute and global consultancy McKinsey & Company, explores the mystery of Tom:

Why do consumers consistently give credit unions their highest • satisfaction scores and yet take their business elsewhere?And, just as importantly, what can credit unions do about it?•

To address the issue, Filene and McKinsey convened three regional roundtables in which participating credit unions were asked to review McKinsey’s customer satisfaction and customer experience research. Then they were asked to consider how credit unions can leverage their phenomenal satisfaction levels among members. In the roundtables, representatives from 31 credit unions ranging in size from $27 million (M) to $7B in assets discussed the research pro-vided by McKinsey and suggested best practices that credit unions can adopt to track and use customer satisfaction to their strategic advantage.

The primary material for this report comes from McKinsey’s in-depth research on customer experience, employee engagement, and customer satisfaction. McKinsey relies on regular, proprietary surveys of consumers to inform its advice on a broad range of industries—from grocery stores to airlines, and from hotels to Internet service

Executive Summary and Commentary

xii

providers. The 2009 customer experience survey on which most of the report is based draws on 3,900 respondents who offered their views on retail banking. The survey measures satisfaction, asks what matters most for driving satisfaction, and seeks to validate the rela-tionship between satisfaction and value creation.

Three McKinsey consultants shared their deep expertise with the credit union groups, and their names show up throughout the report as subject matter experts. They are:

Dorian Stone, partner, San Francisco.• Kurt MacAlpine, senior engagement manager, Toronto.• Joshua Kanter, associate principal, New York.•

Much of the additional material and best practices in this report come from the three credit union roundtables and will be cited less formally than in Filene’s traditional academic reports. The best prac-tices and ideas that emerged from the roundtables are credited where possible. The words “customer” and “member” are used interchange-ably throughout the report to reflect the original McKinsey research.

What Did the Research Reveal?Credit unions clearly and consistently garner high satisfaction scores, but it’s also clear that satisfaction doesn’t necessarily bring growth or market share. In fact, it may disguise underlying credit union challenges.

The report’s key findings may be uncomfortable for credit unions that embrace member satisfaction and empowerment at any cost. For those credit unions, “cost” is the key word. Credit unions as a whole are at the top of the customer satisfaction heap, which means that few additional satisfaction gains are possible. Therefore, continued investment in improving customer satisfaction will deliver little or no marginal benefit. Instead, the report suggests that credit unions should try to maintain their preferred status but redirect manage-ment efforts and resources toward improving crucial functional areas, such as remote delivery, member wait times, and problem resolution.

In addition, the report finds that:

Credit unions outperform banks handily on emotional factors, • like trustworthiness and member pride in doing their banking there. But they have fewer advantages in functional categories, like online tools and convenience.The type of customer satisfaction metric an institution uses is • less important than consistent analysis of changes in satisfaction scores.

xiii

Frontline employees, especially branch managers, are the most • important link in good or bad customer experience.

What Are the Credit Union Implications?Credit unions’ basic structure impels them to consider the needs of members before anything else. This report suggests that those needs are not always best served by better and better personal service. If they were, credit unions’ advantage in satisfaction would become an advantage in market share.

Credit unions should treat member satisfaction and improved mem-ber experience as means to an end—never as ends in themselves. The right satisfaction-driven goals will be different for every credit union, but they should include concerns about long-term viability, market share growth, wallet-share growth, and sustainable profit-ability. Member satisfaction efforts that do not consider ROI inflate expenses. With margins thin, and likely to remain so for the foresee-able future, credit unions can’t afford satisfaction at all costs.

On the same note, credit unions already score at the top in customer satisfaction, so most credit unions will find little marginal benefit in trying to improve scores even more. A more sustainable strategy for high-satisfaction credit unions is to monitor member perceptions closely while introducing high ROI initiatives like improved sales channels and streamlining delivery systems. If the members don’t

balk, credit unions stand to gain.

Finally, this report suggests that credit unions build on and trumpet what leads members to be more satisfied in the first place: high levels of trust, the

eagerness of existing members to speak well of the credit union, and good overall value.

In other words, this report is designed to help Tom get more dates. And then maybe a steady girlfriend.

The McKinsey research used as the basis of this report is avail-able to registered members of the Filene Research Institute. To view the data, please visit www.filene.org/publications/detail/mckinsey.

xv

About the Authors

Mark C. MeyerMark C. Meyer is the CEO of the Filene Research Institute. Mark joined the Institute in January 2003, starting an open-source revolu-tion in credit unions. He founded the prestigious Filene i3, a group of next-generation credit union leaders focused on identifying and launching transformative financial products, services, or business models relevant to consumers.

An internationally recognized credit union expert, Mark’s opinion and research have been cited in dozens of publications including the Wall Street Journal, and he has contributed to National Public Radio. He has lectured to hundreds of audiences across North America, Asia, and Europe. He has served as an advisor to the U.S. Depart-ment of the Treasury.

Mark has authored market-leading reports on innovation, consumer behavior, and the financial services needs of young adults. He also serves as secretary on the board of directors for Summit Credit Union, the largest credit union in Wisconsin.

Prior to his work at Filene, Mark served as an attorney at Montgom-ery, Little & McGrew in Denver, Colorado; as vice president and legal counsel at Arizona State Credit Union; and as assistant vice president at the CUNA Mutual Group.

Mark received his JD from the University of Nebraska College of Law and his BS in business administration from Northern Arizona University. He is licensed to practice law in Arizona and Colorado.

Ben RogersBen Rogers is the research director of the Filene Research Institute, where he manages and edits a large pipeline of economic, behavioral, and policy research related to the consumer finance industry. He pre-viously served as director of the Institute’s CU Tomorrow project, as editor of the CEO Report, and as chairman of the National Directors’ Convention. Ben has been cited in the Wall Street Journal, American Banker, the Credit Union Times, and the Credit Union Journal. He earned a master’s degree from Northwestern University and a BA from Brigham Young University.

Credit unions are rightly famous for putting members first and keeping them happy. For continued growth, happy may not be the right focus.

CHAPTER 1Stellar Customer Satisfaction: Opportunity or Achilles’ Heel?

2

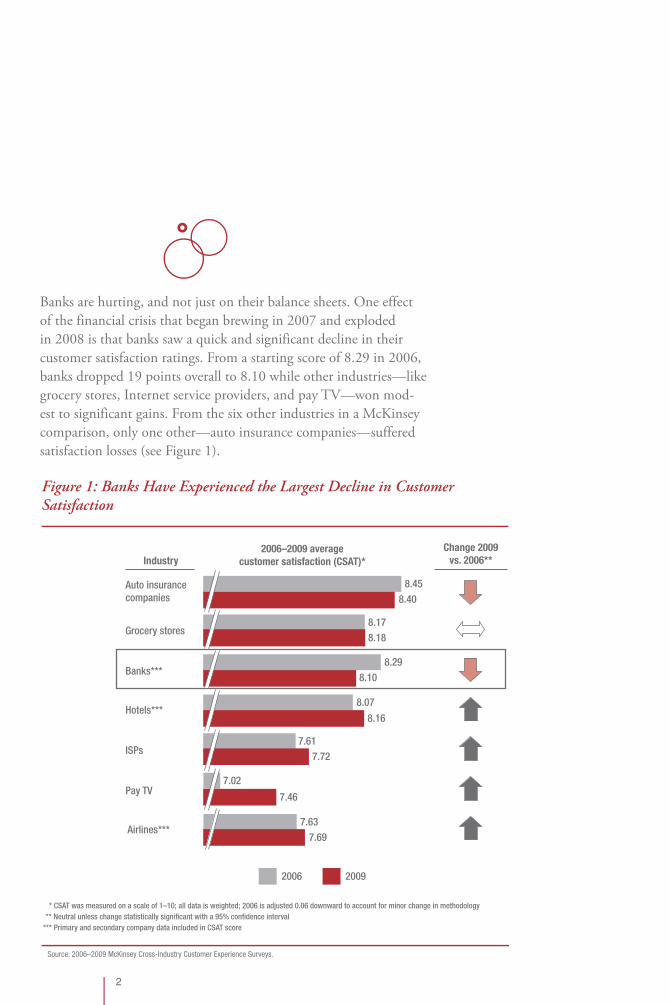

Banks are hurting, and not just on their balance sheets. One effect of the financial crisis that began brewing in 2007 and exploded in 2008 is that banks saw a quick and significant decline in their customer satisfaction ratings. From a starting score of 8.29 in 2006, banks dropped 19 points overall to 8.10 while other industries—like grocery stores, Internet service providers, and pay TV—won mod-est to significant gains. From the six other industries in a McKinsey comparison, only one other—auto insurance companies—suffered satisfaction losses (see Figure 1).

Industry2006–2009 average

customer satisfaction (CSAT)*

20092006

Auto insurancecompanies

Grocery stores

Banks***

Hotels***

ISPs

Pay TV

Airlines***

* CSAT was measured on a scale of 1–10; all data is weighted; 2006 is adjusted 0.06 downward to account for minor change in methodology** Neutral unless change statistically significant with a 95% confidence interval

*** Primary and secondary company data included in CSAT score

8.45

8.178.18

8.298.10

8.07

8.16

7.617.72

7.02

7.46

7.637.69

8.40

Change 2009vs. 2006**

Figure 1: Banks Have Experienced the Largest Decline in Customer Satisfaction

Source: 2006–2009 McKinsey Cross-Industry Customer Experience Surveys.

DEFINITIONS

This report refers often to consumers

and members, but especially customers.

These terms are used interchangeably

despite the fact that credit unions serve

members. This is because the original

McKinsey research and data use “cus-

tomer” language, which is retained here for

consistency and clarity. Where the word

“member” appears, it should be consid-

ered synonymous with “customer.”

There are several discrete terms that

hold specific connotations throughout the

report. Each is separate, but all are related.

Customer experience: total set of

elements (from promises and messag-

ing to execution) that determine the

value delivered to customers and drive

specific customer behavior that benefits

both the customer and the business

(e.g., repeat purchases, referrals).

Customer satisfaction: measures a

customer’s overall satisfaction with the

business; a commonly used metric of

quality of customer experience.

Employee engagement: extent to

which employees commit to the orga-

nization and, as a result: (1) how hard

they work to please customers and

drive sales, and (2) how long they intend

to stay with the organization.

Functional value: describes tangible

benefits like proximity of branches, good

online delivery, and overall convenience.

Emotional value: comprises intan-

gible factors like trust and feeling good

about telling others you bank there.

It’s unclear from the data whether banks suffered satisfaction declines because of tangible operational changes over the three-year period or as a result of consumer sentiment that turned against financial institutions perceived as being responsible for the recession. Regard-less of the source of their discontent, customers have clearly become disillusioned in recent years, which should present opportunities for smaller, responsible organizations like credit unions.

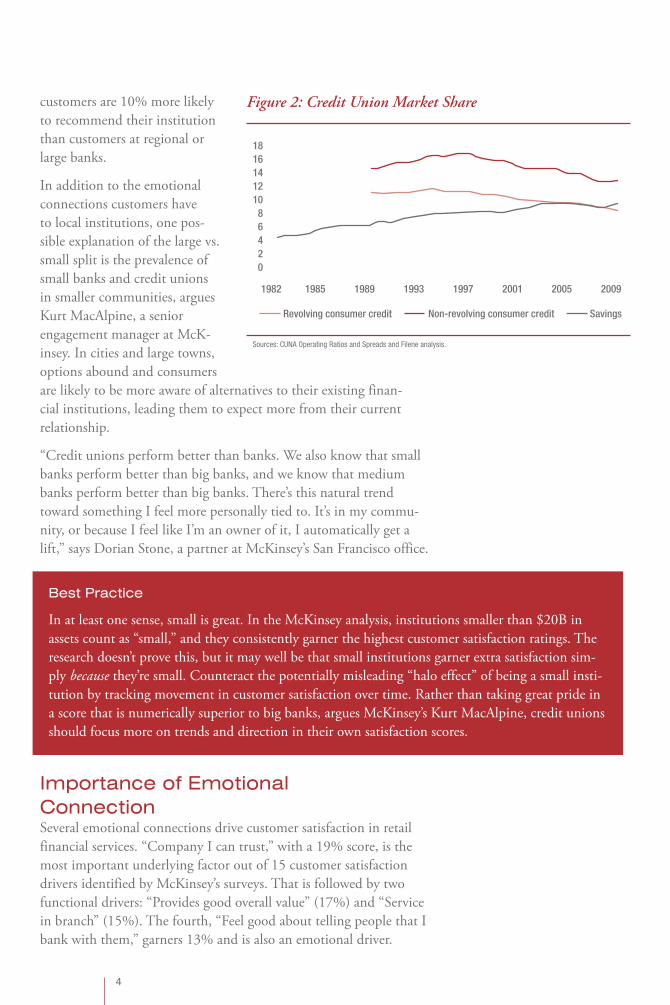

Opportunities, yes; change, no. While total satisfaction with banks declined from 2006 to 2009, credit unions’ market share of deposits saw few gains, non-revolving credit merely stabilized, and revolving credit continued to decline (see Figure 2).

Halo EffectsSize matters. Credit unions and small banks share the best scores in customers’ overall satisfaction and their willingness to recommend. Satisfaction and willingness to recommend scores go down as assets grow. Credit union and small bank customers are 10% more likely than those at regional banks to be satisfied and 14% more likely than customers at large banks. Similarly, credit union and small bank

3

4

customers are 10% more likely to recommend their institution than customers at regional or large banks.

In addition to the emotional connections customers have to local institutions, one pos-sible explanation of the large vs. small split is the prevalence of small banks and credit unions in smaller communities, argues Kurt MacAlpine, a senior engagement manager at McK-insey. In cities and large towns, options abound and consumers are likely to be more aware of alternatives to their existing finan-cial institutions, leading them to expect more from their current relationship.

“Credit unions perform better than banks. We also know that small banks perform better than big banks, and we know that medium banks perform better than big banks. There’s this natural trend toward something I feel more personally tied to. It’s in my commu-nity, or because I feel like I’m an owner of it, I automatically get a lift,” says Dorian Stone, a partner at McKinsey’s San Francisco office.

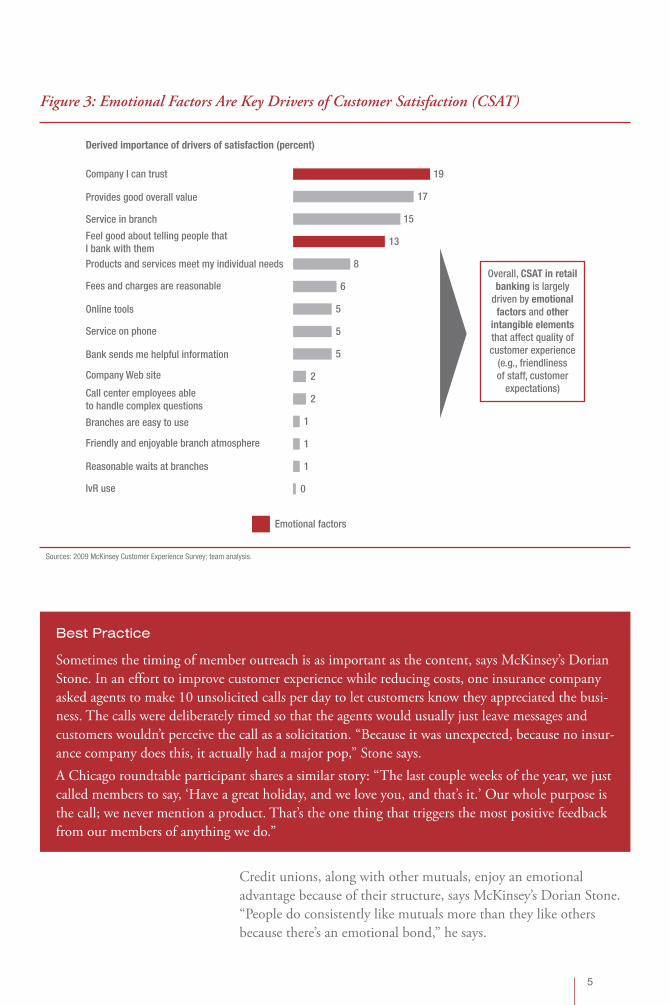

Importance of EmotionalConnectionSeveral emotional connections drive customer satisfaction in retail financial services. “Company I can trust,” with a 19% score, is the most important underlying factor out of 15 customer satisfaction drivers identified by McKinsey’s surveys. That is followed by two functional drivers: “Provides good overall value” (17%) and “Service in branch” (15%). The fourth, “Feel good about telling people that I bank with them,” garners 13% and is also an emotional driver.

Best Practice

In at least one sense, small is great. In the McKinsey analysis, institutions smaller than $20B in assets count as “small,” and they consistently garner the highest customer satisfaction ratings. The research doesn’t prove this, but it may well be that small institutions garner extra satisfaction sim-ply because they’re small. Counteract the potentially misleading “halo effect” of being a small insti-tution by tracking movement in customer satisfaction over time. Rather than taking great pride in a score that is numerically superior to big banks, argues McKinsey’s Kurt MacAlpine, credit unions should focus more on trends and direction in their own satisfaction scores.

02468

1012141618

1982 1985 1989 1993 1997 2001 2005 2009

Revolving consumer credit Non-revolving consumer credit Savings

Figure 2: Credit Union Market Share

Sources: CUNA Operating Ratios and Spreads and Filene analysis.

5

Credit unions, along with other mutuals, enjoy an emotional advantage because of their structure, says McKinsey’s Dorian Stone. “People do consistently like mutuals more than they like others because there’s an emotional bond,” he says.

Derived importance of drivers of satisfaction (percent)

Emotional factors

Company I can trust 19

Provides good overall value 17

Service in branch 15

Products and services meet my individual needs 8

Fees and charges are reasonable 6

Online tools 5

Service on phone 5

5Bank sends me helpful information

Company Web site 2

Call center employees ableto handle complex questions

2

Branches are easy to use 1

Friendly and enjoyable branch atmosphere 1

Reasonable waits at branches 1

IvR use 0

Feel good about telling people thatI bank with them

13

Overall, CSAT in retailbanking is largely

driven by emotionalfactors and other

intangible elementsthat affect quality ofcustomer experience

(e.g., friendlinessof staff, customer

expectations)

Figure 3: Emotional Factors Are Key Drivers of Customer Satisfaction (CSAT)

Sources: 2009 McKinsey Customer Experience Survey; team analysis.

Best Practice

Sometimes the timing of member outreach is as important as the content, says McKinsey’s Dorian Stone. In an effort to improve customer experience while reducing costs, one insurance company asked agents to make 10 unsolicited calls per day to let customers know they appreciated the busi-ness. The calls were deliberately timed so that the agents would usually just leave messages and customers wouldn’t perceive the call as a solicitation. “Because it was unexpected, because no insur-ance company does this, it actually had a major pop,” Stone says.A Chicago roundtable participant shares a similar story: “The last couple weeks of the year, we just called members to say, ‘Have a great holiday, and we love you, and that’s it.’ Our whole purpose is the call; we never mention a product. That’s the one thing that triggers the most positive feedback from our members of anything we do.”

6

However, Stone says, “people also feel that mutuals do not actually provide the value and the functional basics, the functional perfor-mance that’s needed, that they get from the for-profit, non-mutual companies out there in banking.” So, despite the preeminence of trust and the importance of “feeling good,” factors like overall value, products that meet individual needs, and online tools weigh into consumers’ decisions about financial institutions. This is especially true for new and potential members, who have no history of an emo-tional bond.

Further, to many consumers financial service decisions are much more about economic value (real or perceived) than they are about emotion. A credit union that resonates emotion-ally but fails to convey its fundamental value to consum-ers is in danger of losing the relationship.

Credit unions have historically felt leery about introducing sales into a culture that garners such high member satisfaction. But credit unions can actually convey fundamental value to members by ramping up sales initiatives. An institution that offers products and service that are good for con-sumers has nothing to fear from emphasizing cross-sells, Stone says. But a credit union culture that is too “nice” to assert itself stands to lose market share and lose out at a key step in the marketing funnel.

Customer Satisfaction in the FunnelThe classic marketing funnel imagines customers moving through several stages before they commit to a product purchase, whether of sneakers or a checking account. First comes awareness, then famil-iarity, then consideration and deliberation, and finally purchase. At each step the potential customer might opt out, and only a few arrive finally at the point of purchase.

“What satisfaction is particularly powerful in doing is getting [customers] to the consideration step. It gets you into the consider-ation set, but you don’t actually see it in the performance set,” Stone says. High satisfaction doesn’t necessarily make you appear more advantageous compared to competing product offerings. Having a

Best Practice

One way to capitalize on local, emotional connections is to emphasize products that are hyper-specific to your market. Jon Reske of UMassFive College FCU in Hadley, Massachusetts, volunteers the example of the credit union’s farm share loans. In western Massachusetts, members often buy farm shares that entitle them to a season of fresh produce, but some mem-bers don’t have the $900 necessary to pay the upfront cost of the share. UMassFive loans the small amount and then takes payments as payroll deductions over the course of the season. Most local loans are not profit centers, but they build goodwill and positive customer satisfaction. Other local loan ideas from UMassFive: energy loans to pay for energy costs like heating oil deliveries, fuel-efficient transportation, or Energy Star–certified appliances; and bike loans for students.

7

demonstrably better product is what gets customers to purchase.

Customer satisfaction enhanced by proactive sales will get potential cus-tomers much further along the market-ing funnel, Stone says. “While people may like us and consider us, it’s not clear that we have any advantage when we get further down the sales process to get a greater share of their deposit or wallet, [or] sell the next product. We’re

left standing just the same flat, toe to toe with everybody else.”

A key differentiator of the sales vs. service environment is that sales cultures focus on individual products and talk to customers about individual products. In order to get better, Stone continues, credit unions have to focus on the tangible or economic value—on the individual product and the individual interaction quality.

Importance of Functional ServicesIn McKinsey’s surveys, consumers indicate they are more emotion-ally connected to credit unions than they are to banks. Credit unions also score better than banks in functional categories, but the advan-tage there is less pronounced and it may be misleading, according to MacAlpine.

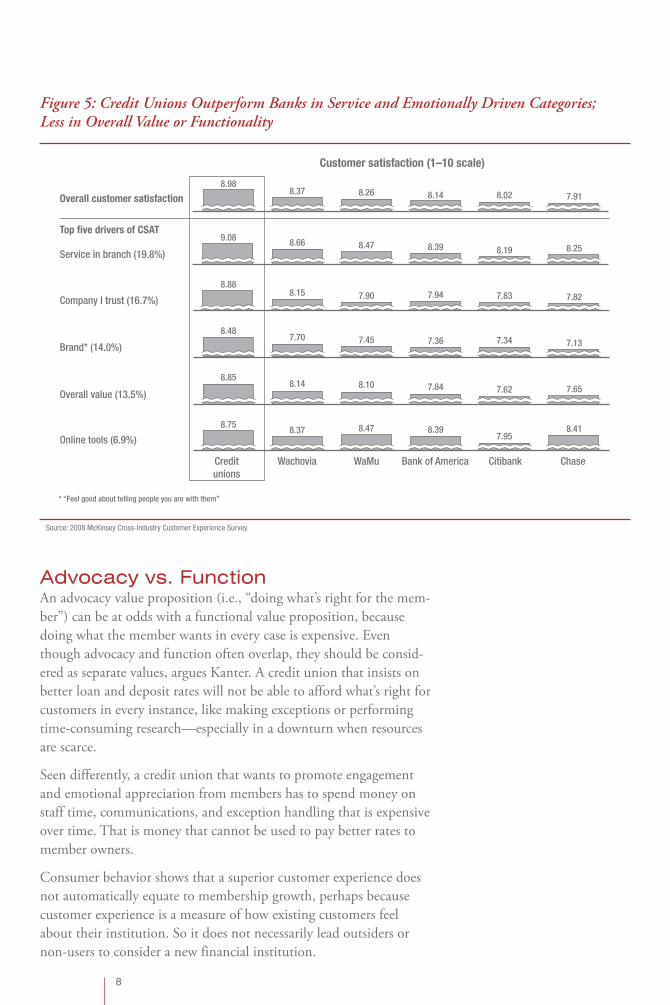

That’s because credit unions seem to enjoy an emotional “halo effect” in their members’ minds. Members often enjoy a deeper connection with their credit union, so they probably rank some credit union services more charitably than a direct comparison would justify. For example, members in aggregate rate their credit unions’ online tools more highly than customers of large banks rank their banks’ online tools (see Figure 5). But a dispassionate comparison between most credit unions’ online tools and those of Citibank or Chase would not be favorable for the credit union.

And credit unions’ traditional emotional advantage is fading, espe-cially in relation to small banks. “Small banks have figured this out. And you know what? They don’t have 150,000 employees to deal with. So they’re actually taking action now and closing these gaps, such that the differentiation that used to be so stark between a credit union and the bank is diminished,” says Joshua Kanter, an associate principal at McKinsey’s New York office.

Awareness Familiarity Consideration Purchase Loyalty

Figure 4: Marketing Funnel

Source: McKinsey Quarterly, June 2009.

8

Advocacy vs. FunctionAn advocacy value proposition (i.e., “doing what’s right for the mem-ber”) can be at odds with a functional value proposition, because doing what the member wants in every case is expensive. Even though advocacy and function often overlap, they should be consid-ered as separate values, argues Kanter. A credit union that insists on better loan and deposit rates will not be able to afford what’s right for customers in every instance, like making exceptions or performing time-consuming research—especially in a downturn when resources are scarce.

Seen differently, a credit union that wants to promote engagement and emotional appreciation from members has to spend money on staff time, communications, and exception handling that is expensive over time. That is money that cannot be used to pay better rates to member owners.

Consumer behavior shows that a superior customer experience does not automatically equate to membership growth, perhaps because customer experience is a measure of how existing customers feel about their institution. So it does not necessarily lead outsiders or non-users to consider a new financial institution.

Overall customer satisfaction

Customer satisfaction (1–10 scale)

Top five drivers of CSAT

Creditunions

Wachovia WaMu Bank of America Citibank Chase

* “Feel good about telling people you are with them”

8.988.37 8.26 8.14 8.02 7.91

Service in branch (19.8%)

9.08 8.66 8.47 8.39 8.19 8.25

Company I trust (16.7%)

8.888.15 7.90 7.94 7.83 7.82

Brand* (14.0%)

8.487.70 7.45 7.36 7.34 7.13

Overall value (13.5%)

8.858.14 8.10 7.84 7.62 7.65

Online tools (6.9%)

8.758.37 8.47 8.39

7.958.41

Figure 5: Credit Unions Outperform Banks in Service and Emotionally Driven Categories; Less in Overall Value or Functionality

Source: 2008 McKinsey Cross-Industry Customer Experience Survey.

9

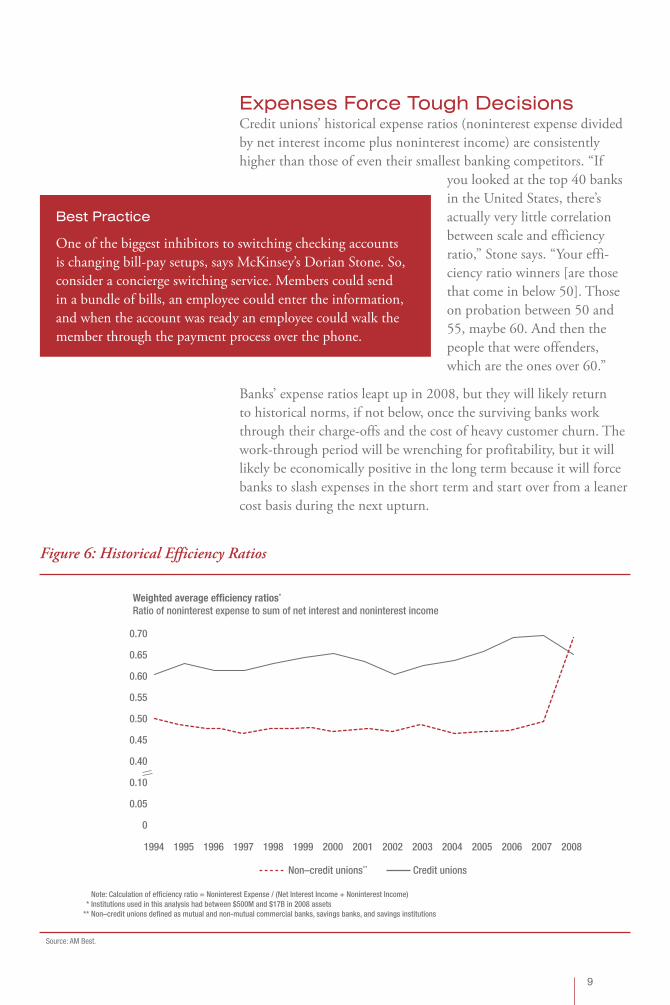

Expenses Force Tough DecisionsCredit unions’ historical expense ratios (noninterest expense divided by net interest income plus noninterest income) are consistently higher than those of even their smallest banking competitors. “If

you looked at the top 40 banks in the United States, there’s actually very little correlation between scale and efficiency ratio,” Stone says. “Your effi-ciency ratio winners [are those that come in below 50]. Those on probation between 50 and 55, maybe 60. And then the people that were offenders, which are the ones over 60.”

Banks’ expense ratios leapt up in 2008, but they will likely return to historical norms, if not below, once the surviving banks work through their charge-offs and the cost of heavy customer churn. The work-through period will be wrenching for profitability, but it will likely be economically positive in the long term because it will force banks to slash expenses in the short term and start over from a leaner cost basis during the next upturn.

0

* Institutions used in this analysis had between $500M and $17B in 2008 assets** Non–credit unions defined as mutual and non-mutual commercial banks, savings banks, and savings institutions

Note: Calculation of efficiency ratio = Noninterest Expense / (Net Interest Income + Noninterest Income)

0.05

0.10

0.40

0.45

0.50

0.55

0.60

0.65

0.70

Weighted average efficiency ratios*

Ratio of noninterest expense to sum of net interest and noninterest income

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Non–credit unions** Credit unions

Figure 6: Historical Efficiency Ratios

Source: AM Best.

Best Practice

One of the biggest inhibitors to switching checking accounts is changing bill-pay setups, says McKinsey’s Dorian Stone. So, consider a concierge switching service. Members could send in a bundle of bills, an employee could enter the information, and when the account was ready an employee could walk the member through the payment process over the phone.

10

“The for-profit [banks] are leaner and meaner, and we [credit unions] rest on our laurels, where we’re going to offer a little better rate,” says one Los Angeles–area CEO. “Our margins are thinner because our cost of funds is higher. Our loan rate’s a little lower. We’re squeezed a little tighter [than banks].”

Add to that economic analysis a philosophical analysis, MacAlpine says. He summarizes feedback from other credit union CEOs: “We’re going through one of the worst financial crises of the last 80 years, and most people I sat with around the table are saying, ‘I’m not doing layoffs; we’re not going to replace or upgrade our workforce; we’re going to toe the line.’ You wouldn’t hear that in most compa-nies.” He contrasts that with two more typical reactions from compa-nies during a downturn: Those that are marginal have to reduce their workforces to survive, and those that are in relatively good shape see this downturn as “the opportunity of a lifetime to upgrade the talent that we have.”

The pursuit of positive customer experience can be an undermining force if not weighed against the health of the organization and other strategic goals. That’s not because a focus on customer experience is bad for the members, but because it can exert cost pressure that forces management to take undue risks.

SummaryCredit unions hold valuable goodwill from their members. It seems that both their structure and their size contribute to positive emo-tional feelings, which spill over into high satisfaction scores.

Emotional factors and satisfaction get existing members to consider opening new products with credit unions, but they are less effective in closing the deal. Credit unions should beware the “halo effect,” which leads members to think and speak well of them without neces-sarily bringing more business.

Credit unions, which historically have been less operationally effi-cient than their banking peers, should use the downturn to become leaner and scrutinize the ROI of any new programs designed to further please members.

Knowing what members want is hard enough. Harder still: balancing better member satisfac-tion with operational expenses. The best orga-nizations identify profitable satisfaction drivers and ignore the rest.

CHAPTER 2Defining and Improving

Customer Experience

12

Navel gazing is satisfying, but it’s not always right. One of the big-gest mistakes companies of all stripes make is assuming they know what their customers want, McKinsey’s Joshua Kanter says. But pet projects or staff-designed initiatives won’t always resonate with customers.

“You’ve got to understand what’s really important to people, because there are the things that we believe we do particularly well and [that] we want to matter to people. It doesn’t always matter to people,” Kanter says. Furthermore, and more subtly, “there are things that people tell you are impor-tant and other things that are really important to them.”

Taking that difference seriously leads management to better analysis. At the most basic level it means polling members and soliciting feedback before and during new initiatives. That function can be served by traditional or online polling or in focus groups.

More powerful than polling, however, Kanter says, is measuring how customers respond to new customer experience initiatives. While it’s fairly easy to measure the return of a marketing campaign, measuring customer experience is more difficult, because the indicators trail the investments. Customers will respond to positive changes, but it won’t always show up in satisfaction surveys overnight.

This is one of the reasons consistent customer experience track-ing is more important than the kind of metric used, McKinsey’s Dorian Stone says. Comparing Net Promoter (NPS) methodologies to customer service methodologies yields few insights. And the cost of changing from an existing method can be high considering the implementation costs and potential confusion among staff, Stone adds. “You might as well stick with what you’ve got. If you’re using a CSAT, use a CSAT. If you’re using NPS, it’s good enough.”

Best Practice

Regardless of your chosen customer satisfaction metric, use a 1–10 scale rather than a 1–5 scale, suggests McKinsey’s Dorian Stone. Doing so allows members to offer more meaningful distinctions of whether they’re satisfied, neutral, or unsatisfied.

The real value in these customer measurements comes from track-ing improvements or declines that follow new initiatives. “The member doesn’t necessarily know what they need, so we need to be more [of an] advocate. We need to really take more of a consultative approach,” says one Los Angeles roundtable participant.

Value of Customer Satisfaction MeasurementEvery executive, whether at a credit union or a computer manufac-turer, is susceptible to the navel-gazing fallacy: assuming customers want the same thing the executive wants and acting accordingly. This thinking is particularly dangerous in gauging the value of customer experience for two reasons: First, there’s no guarantee that even an informed executive can know what customers want; and second, a customer experience that may have worked perfectly in the past may no longer be valuable. Worse, it may be valuable but for exactly the wrong kind of consumer. Different demographic and psychographic groups will value different customer experiences.

For example, high-net-worth individuals will prize a different experi-ence than young borrowers, and middle-income professionals will want a different experience than college students. So, before a credit union decides to improve its customer experience or seeks to mea-sure its results, it needs to identify its target groups, says Stone.

Large, sophisticated companies often track their customer satisfac-tion scores, but they don’t delve deeply enough into the drivers behind the satisfaction, Stone adds. For example, it’s tempting to assume that satisfaction at the credit union is improving because frontline staff have been asked to greet members by name, when in fact the improvements are more closely linked to a new Web service or streamlined underwriting.

13

Best Practice

Verify the value of new customer experience initiatives with members before you invest. Con-sider using surveys, focus groups, or—most effectively—data about how similar investments have changed member behavior in the past. Alternately, rather than offering a survey about whether they would like a shiny new drive-through, give members options about whether they would prefer the drive-through to mobile banking or better auto loan rates. “I see too many of my clients build-ing the next big mousetrap,” says McKinsey’s Joshua Kanter. “Make sure that the things you’re making your investments on are actually going to be valued before you go too far into it.”

GEN Y AND CUSTOMER EXPERIENCE

Consumers increasingly demand function-

ality from their financial institutions. That’s

in addition to any emotional bond institu-

tions can make, and in no cohort is this

more apparent than with Generation Y.

“What the younger generations now care

most about is actually less to credit union

strengths,” says McKinsey’s Dorian Stone.

They are looking for multi-channel relation-

ships, and they want to receive that in a

way that feels personal for them.

That personalization is key. Lori Hall, of

American Airlines Federal Credit Union in

Fort Worth, says that her credit union’s

research shows two clear needs from

younger members: first, the desire for

heavy up-front engagement, followed by

the desire to be left alone. “First it’s, ‘Teach

me, walk me through this, hold my hand,’

and then [it’s], ‘Leave me alone because

I’m impatient and I want to be able to do it

any time.’”

Multi-channel relationships are increasingly

important because young adults say con-

venience is most important to them when

they first choose a financial institution.1 And

convenience for the modern financial cus-

tomer includes:

Branch locations.•

ATM access.•

Extended business hours.•

Telephone access.•

Internet access.•

Mobile access.•

14

0%

5%

10%

15%

20%

25%

30%

35%

40% 37.4%

Convenience

23.8%

Products

21.7%

Service

2.8%

Inertia

2.7%

Reputation

Figure 7: Why Young Adults Choose Their Financial Institution

Source: Jinkook Lee, Attracting Young Adults: What Do We Know About Their Use of Financial Institutions and Payment Behaviors? (Madison, WI: Filene Research Institute, 2008), 7.

GEN Y AND CUSTOMER EXPERIENCE (CONTINUED)

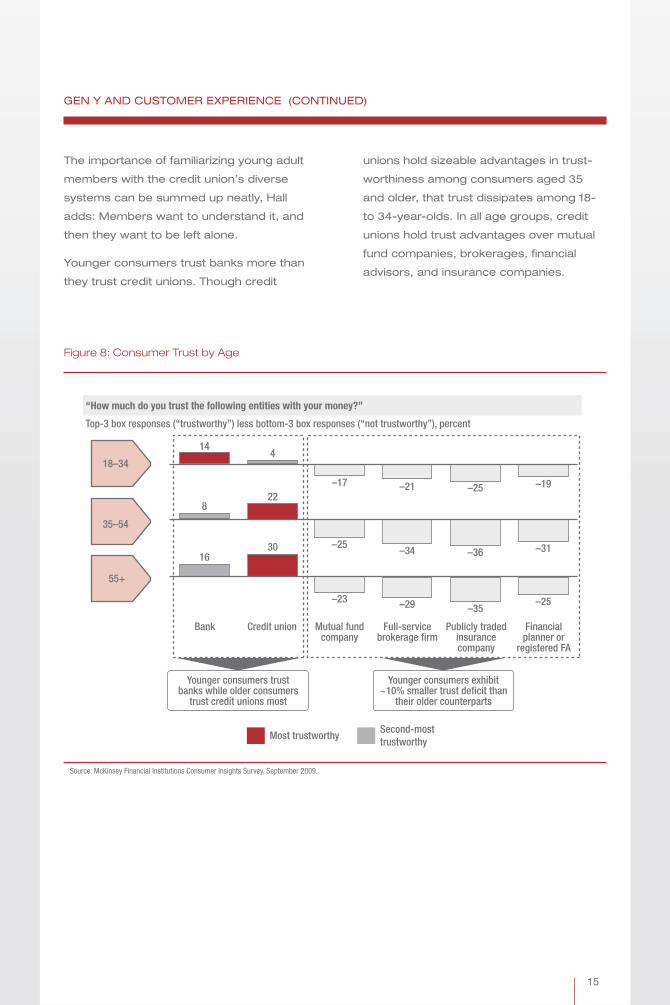

The importance of familiarizing young adult

members with the credit union’s diverse

systems can be summed up neatly, Hall

adds: Members want to understand it, and

then they want to be left alone.

Younger consumers trust banks more than

they trust credit unions. Though credit

unions hold sizeable advantages in trust-

worthiness among consumers aged 35

and older, that trust dissipates among 18-

to 34-year-olds. In all age groups, credit

unions hold trust advantages over mutual

fund companies, brokerages, financial

advisors, and insurance companies.

14

Top-3 box responses (“trustworthy”) less bottom-3 box responses (“not trustworthy”), percent

“How much do you trust the following entities with your money?”

8

16

4

22–17 –21 –25

–36

–35

–19

–31

–25

–34

–29

–25

–23

30

Bank Credit union Mutual fundcompany

Younger consumers trustbanks while older consumers

trust credit unions most

Younger consumers exhibit~10% smaller trust deficit than

their older counterparts

Full-servicebrokerage firm

Publicly tradedinsurancecompany

Financialplanner or

registered FA

18–34

35–54

55+

Most trustworthySecond-mosttrustworthy

Figure 8: Consumer Trust by Age

Source: McKinsey Financial Institutions Consumer Insights Survey, September 2009.

15

16

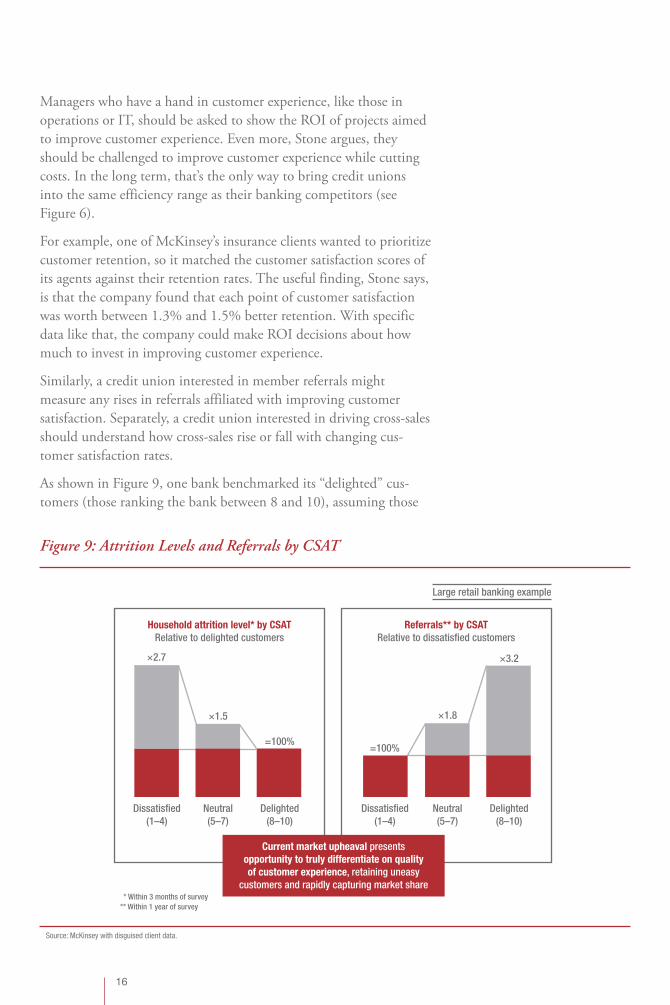

Managers who have a hand in customer experience, like those in operations or IT, should be asked to show the ROI of projects aimed to improve customer experience. Even more, Stone argues, they should be challenged to improve customer experience while cutting costs. In the long term, that’s the only way to bring credit unions into the same efficiency range as their banking competitors (see Figure 6).

For example, one of McKinsey’s insurance clients wanted to prioritize customer retention, so it matched the customer satisfaction scores of its agents against their retention rates. The useful finding, Stone says, is that the company found that each point of customer satisfaction was worth between 1.3% and 1.5% better retention. With specific data like that, the company could make ROI decisions about how much to invest in improving customer experience.

Similarly, a credit union interested in member referrals might measure any rises in referrals affiliated with improving customer satisfaction. Separately, a credit union interested in driving cross-sales should understand how cross-sales rise or fall with changing cus-tomer satisfaction rates.

As shown in Figure 9, one bank benchmarked its “delighted” cus-tomers (those ranking the bank between 8 and 10), assuming those

Dissatisfied(1–4)

×2.7

Neutral(5–7)

×1.5

Large retail banking example

* Within 3 months of survey** Within 1 year of survey

Delighted(8–10)

=100%=100%

Dissatisfied(1–4)

Neutral(5–7)

×1.8

Delighted(8–10)

×3.2

Household attrition level* by CSATRelative to delighted customers

Referrals** by CSATRelative to dissatisfied customers

Current market upheaval presentsopportunity to truly differentiate on qualityof customer experience, retaining uneasy

customers and rapidly capturing market share

Figure 9: Attrition Levels and Referrals by CSAT

Source: McKinsey with disguised client data.

17

customers were retained at the highest possible rate. From there, it was apparent that “neutral” customers (ranking between 5 and 7)

showed attrition levels 50% higher, and “dissatisfied” cus-tomers left more than two-and-a-half times more often.

Conversely, if dissatisfied cus-tomers can be expected to offer the fewest number of referrals, a similar analysis shows that this bank’s neutral customers were

nearly twice as likely to make referrals as the malcontents. Delighted customers were more than three times as likely to refer. In each case, establishing a benchmark allows management to quantify the busi-ness outcomes of improving customer satisfaction.

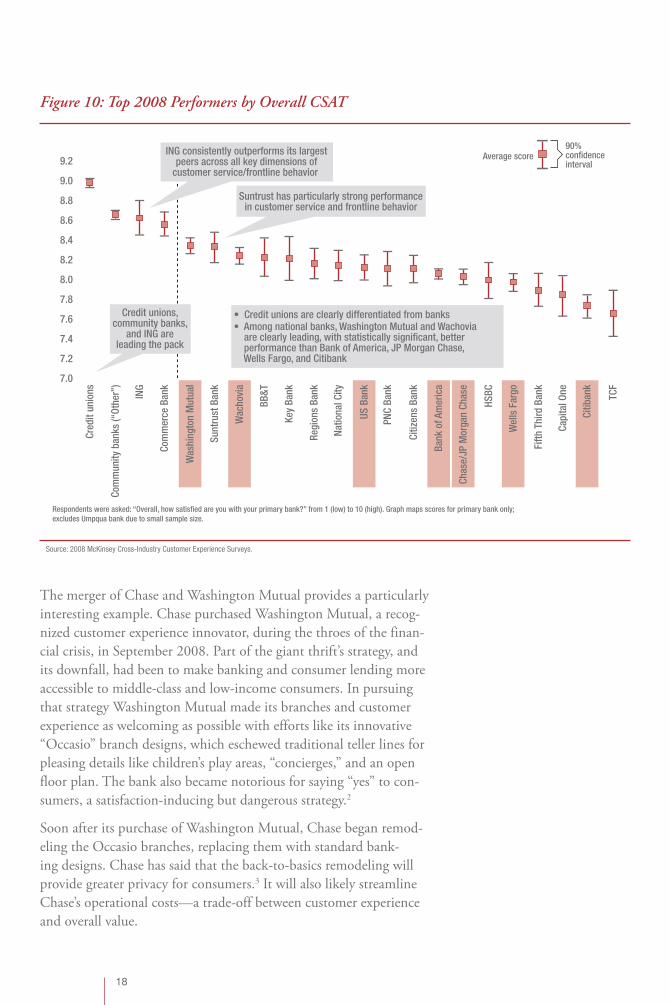

Choosing “Good Enough”Credit unions consistently rank at the top of any banking survey of customer satisfaction. That’s good on its face, but it may actually contribute to their struggles, Stone argues. For-profit and publicly traded banks have to answer to shareholders who are much more interested in bottom-line profits, so they have learned to settle for “good enough” customer satisfaction, while driving aggressively for efficiency and value.

In McKinsey’s 2008 survey, Wachovia and Washington Mutual were among the highest-ranked national banks in overall customer satis-faction, but that obviously didn’t protect them from the downturn. “The survivors seem to have said ‘good enough,’ and then focus[ed] on execution, on efficiency and tightness,” Stone says.

Figure 10 provides strong evidence for the idea that customer satisfaction isn’t always driven by personal connections or by hands-on service. ING Direct, the best performer after credit unions and community banks, got its superior scores despite the fact that it maintains virtually no person-to-person interaction with customers. Instead, it has set clear expectations for how customers will interact with it through its Internet channels.

The three national banks on the lowest side of the 2008 customer satisfaction scale—Bank of America, JP Morgan Chase, and Citi-bank—have each passed through the financial crisis scathed (and subsidized) but intact. Their customer philosophy is summed up by Stone as: “ ‘It’s going to be good enough, and then we’re going to execute like hell. And if I put a little bit less of a smile on one person’s face than others, that’s okay.’ They tend to remain actually stronger in areas like [overall] value.”

Best Practice

Survey members to determine which “magnet products” attracted them to the credit union in the first place, urges McKinsey’s Kurt MacAlpine. Figuring out which products are most competitive and attractive among your membership allows you to better position the credit union and attract similar members.

18

The merger of Chase and Washington Mutual provides a particularly interesting example. Chase purchased Washington Mutual, a recog-nized customer experience innovator, during the throes of the finan-cial crisis, in September 2008. Part of the giant thrift’s strategy, and its downfall, had been to make banking and consumer lending more accessible to middle-class and low-income consumers. In pursuing that strategy Washington Mutual made its branches and customer experience as welcoming as possible with efforts like its innovative “Occasio” branch designs, which eschewed traditional teller lines for pleasing details like children’s play areas, “concierges,” and an open floor plan. The bank also became notorious for saying “yes” to con-sumers, a satisfaction-inducing but dangerous strategy.2

Soon after its purchase of Washington Mutual, Chase began remod-eling the Occasio branches, replacing them with standard bank-ing designs. Chase has said that the back-to-basics remodeling will provide greater privacy for consumers.3 It will also likely streamline Chase’s operational costs—a trade-off between customer experience and overall value.

7.6

7.4

7.2

7.0

ING consistently outperforms its largestpeers across all key dimensions of

customer service/frontline behavior

Credit unions,community banks,

and ING areleading the pack

Suntrust has particularly strong performancein customer service and frontline behavior

are clearly leading, with statistically significant, better

Respondents were asked: “Overall, how satisfied are you with your primary bank?” from 1 (low) to 10 (high). Graph maps scores for primary bank only;excludes Umpqua bank due to small sample size.

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

ING

Com

mun

ity b

anks

(“Ot

her”

)

Cred

it un

ions

Com

mer

ce B

ank

Sunt

rust

Ban

k

BB&T

Key

Bank

Regi

ons

Bank

Natio

nal C

ity

US B

ank

Citiz

ens

Bank

HSBC

Capi

tal O

ne

Citib

ank

90%confidenceinterval

Figure 10: Top 2008 Performers by Overall CSAT

Source: 2008 McKinsey Cross-Industry Customer Experience Surveys.

19

Increased balance39 80

53 15

5 10

9 2

Customers whoexperienced positivemoment of truth

Question: “Since the last issue, which of the following are true?”% of respondents

Customers whoexperienced negative

moment of truth

Decreased balance

Opened new accounts*

Closed accounts

* Includes opening a new account (e.g., checking, CD, investment account) and taking out a new loan (including refinancing)

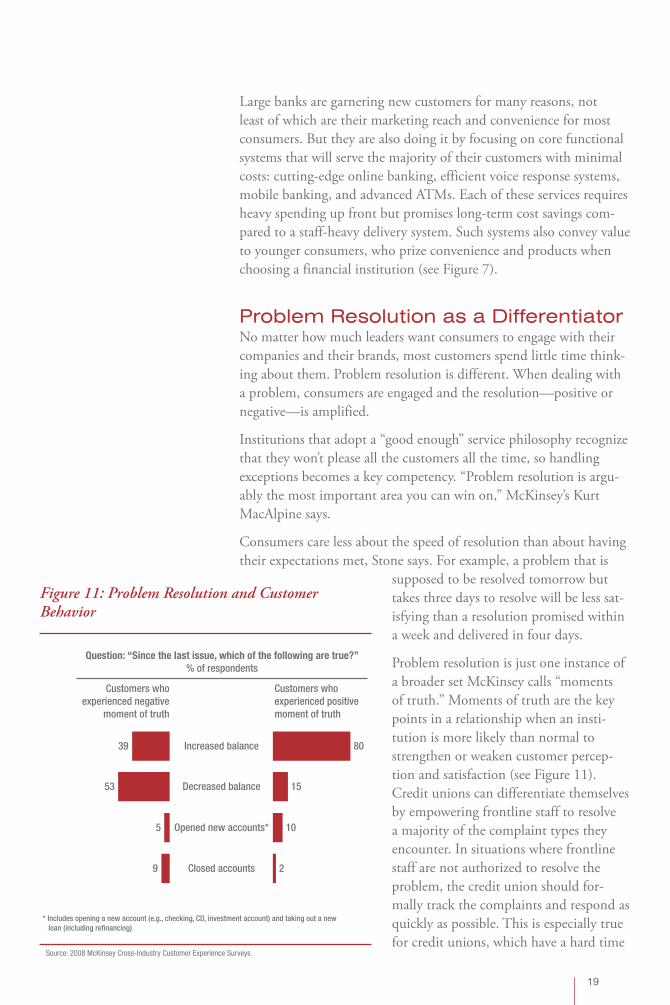

Figure 11: Problem Resolution and Customer Behavior

Source: 2008 McKinsey Cross-Industry Customer Experience Surveys.

Large banks are garnering new customers for many reasons, not least of which are their marketing reach and convenience for most consumers. But they are also doing it by focusing on core functional systems that will serve the majority of their customers with minimal costs: cutting-edge online banking, efficient voice response systems, mobile banking, and advanced ATMs. Each of these services requires heavy spending up front but promises long-term cost savings com-pared to a staff-heavy delivery system. Such systems also convey value to younger consumers, who prize convenience and products when choosing a financial institution (see Figure 7).

Problem Resolution as a DifferentiatorNo matter how much leaders want consumers to engage with their companies and their brands, most customers spend little time think-ing about them. Problem resolution is different. When dealing with a problem, consumers are engaged and the resolution—positive or negative—is amplified.

Institutions that adopt a “good enough” service philosophy recognize that they won’t please all the customers all the time, so handling exceptions becomes a key competency. “Problem resolution is argu-ably the most important area you can win on,” McKinsey’s Kurt MacAlpine says.

Consumers care less about the speed of resolution than about having their expectations met, Stone says. For example, a problem that is

supposed to be resolved tomorrow but takes three days to resolve will be less sat-isfying than a resolution promised within a week and delivered in four days.

Problem resolution is just one instance of a broader set McKinsey calls “moments of truth.” Moments of truth are the key points in a relationship when an insti-tution is more likely than normal to strengthen or weaken customer percep-tion and satisfaction (see Figure 11). Credit unions can differentiate themselves by empowering frontline staff to resolve a majority of the complaint types they encounter. In situations where frontline staff are not authorized to resolve the problem, the credit union should for-mally track the complaints and respond as quickly as possible. This is especially true for credit unions, which have a hard time

20

improving across the board on already good customer satisfaction surveys.

SummaryGarner better management insights, not just by polling members, but by tracking customer satisfaction responses to new initiatives. The specific type of customer satisfaction metric used is less impor-tant than consistent tracking and identifying what causes satisfaction to move.

National banks seem to choose “good enough” customer service for the majority of interactions while heavily investing in problem reso-lution and exception handling. Rather than striving for ever-better member satisfaction as a goal unto itself, credit unions should seek to maintain satisfaction while introducing functional improvements that make them more competitive.

Frontline employees are the face of the credit union. Their own engagement hinges on intan-gible factors, but it can make or break the member experience.

CHAPTER 3Frontline Performance and

Customer Experience

22

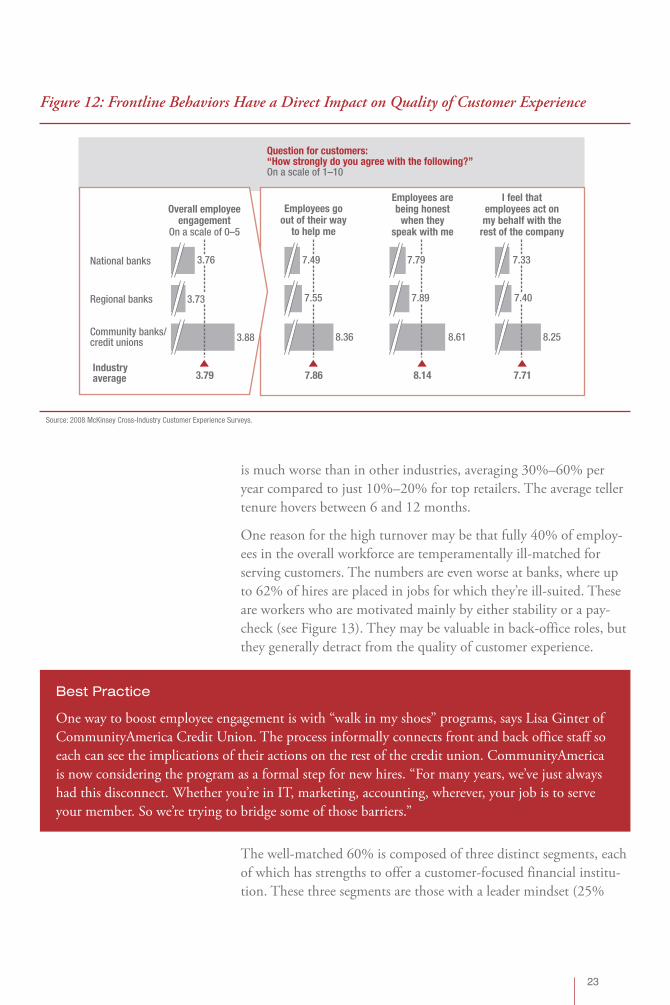

Nowhere is the connection between customer experience and the credit union more tangible than when an employee interacts with a member, whether in a branch, on the phone, through e-mail, or in an office. Yet credit unions don’t always hire who they should and are slow to fire those they should.

Employee engagement is one of the strongest drivers of good customer satisfaction. And credit unions together with community banks clearly outperform larger regional and national banks. Employee engagement at the smaller institutions is better—3.88 out of 5 as opposed to 3.73 (regional banks) and 3.76 (national banks).

The engagement differences play out clearly when customers are asked to rate employees on specific attitudes and perceptions. In each case, size seems to play a decisive role, with the smaller credit unions and community banks performing better than regional banks and regional banks performing better than national banks (though to a lesser degree).

On “Employees go out of their way to help me,” credit unions • and community banks are rated 9.7% higher than their closest competitors.On “Employees are being honest when they speak with me,” • credit unions and community banks are rated 8.8% higher than their closest competitors.On “I feel that employees act on my behalf with the rest of the • company,” credit unions and community banks are rated 11.0% higher than their closest competitors.

Banks in general struggle to sustain high levels of engagement at the front line, according to McKinsey. Attrition in the banking sector

Best Practice

Consider making individual employee performance metrics public for all employees. Doing so can encourage best practice sharing from top to bottom and is a cheap way to recognize top performers.

23

is much worse than in other industries, averaging 30%–60% per year compared to just 10%–20% for top retailers. The average teller tenure hovers between 6 and 12 months.

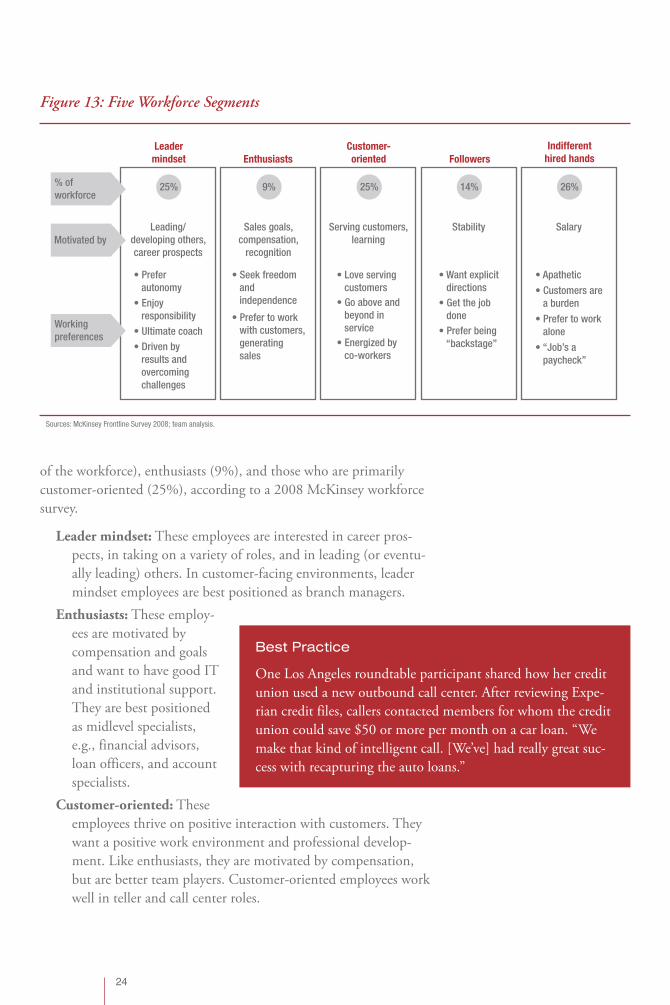

One reason for the high turnover may be that fully 40% of employ-ees in the overall workforce are temperamentally ill-matched for serving customers. The numbers are even worse at banks, where up to 62% of hires are placed in jobs for which they’re ill-suited. These are workers who are motivated mainly by either stability or a pay-check (see Figure 13). They may be valuable in back-office roles, but they generally detract from the quality of customer experience.

The well-matched 60% is composed of three distinct segments, each of which has strengths to offer a customer-focused financial institu-tion. These three segments are those with a leader mindset (25%

Question for customers:“How strongly do you agree with the following?”On a scale of 1–10

National banks 3.76

3.73 7.55

3.88

Overall employeeengagement

On a scale of 0–5

Employees goout of their way

to help me

Employees arebeing honest

when theyspeak with me

I feel thatemployees act onmy behalf with the

rest of the company

Industryaverage 3.79

Regional banks

Community banks/credit unions

7.49

8.36

7.89

7.79

8.61

7.40

7.33

8.25

7.86 8.14 7.71

Figure 12: Frontline Behaviors Have a Direct Impact on Quality of Customer Experience

Source: 2008 McKinsey Cross-Industry Customer Experience Surveys.

Best Practice

One way to boost employee engagement is with “walk in my shoes” programs, says Lisa Ginter of CommunityAmerica Credit Union. The process informally connects front and back office staff so each can see the implications of their actions on the rest of the credit union. CommunityAmerica is now considering the program as a formal step for new hires. “For many years, we’ve just always had this disconnect. Whether you’re in IT, marketing, accounting, wherever, your job is to serve your member. So we’re trying to bridge some of those barriers.”

24

of the workforce), enthusiasts (9%), and those who are primarily customer-oriented (25%), according to a 2008 McKinsey workforce survey.

Leader mindset: These employees are interested in career pros-pects, in taking on a variety of roles, and in leading (or eventu-ally leading) others. In customer-facing environments, leader mindset employees are best positioned as branch managers.

Enthusiasts: These employ-ees are motivated by compensation and goals and want to have good IT and institutional support. They are best positioned as midlevel specialists, e.g., financial advisors, loan officers, and account specialists.

Customer-oriented: These employees thrive on positive interaction with customers. They want a positive work environment and professional develop-ment. Like enthusiasts, they are motivated by compensation, but are better team players. Customer-oriented employees work well in teller and call center roles.

Leading/developing others,career prospects

Leader

mindset

autonomy

responsibility

results and overcoming challenges

25%

Enthusiasts

Sales goals,compensation,

recognition

and independence

generating sales

9%

Customer-

oriented

Serving customers,learning

customers

beyond in service

25%

Followers

Stability

directions

done

14%

Indifferent

hired hands

Salary

a burden

alone

26%

Motivated by

Figure 13: Five Workforce Segments

Sources: McKinsey Frontline Survey 2008; team analysis.

Best Practice

One Los Angeles roundtable participant shared how her credit union used a new outbound call center. After reviewing Expe-rian credit files, callers contacted members for whom the credit union could save $50 or more per month on a car loan. “We make that kind of intelligent call. [We’ve] had really great suc-cess with recapturing the auto loans.”

25

Sales: Not a Four-Letter Word“I have never found a specific industry so averse to sell-ing,” says McKinsey’s Kurt MacAlpine. “You’re not selling tobacco. You’re selling financial solutions for people and making their financial lives better. Don’t shy away from sales.”

One prevalent credit union bar-rier to building a frontline sales culture is staff fears that selling

will detract from member service and member relationships. Yet, McKinsey analysis shows that selling does not materially affect cus-tomers’ perceptions of their financial institutions, McKinsey’s Dorian Stone says. “People actually appreciated what was perceived as aggres-sive selling,” he says. Customers are, of course, welcome to decline products, but when they accept the offered product, their satisfaction improves because the bank offered a product the consumer didn’t know he or she needed.

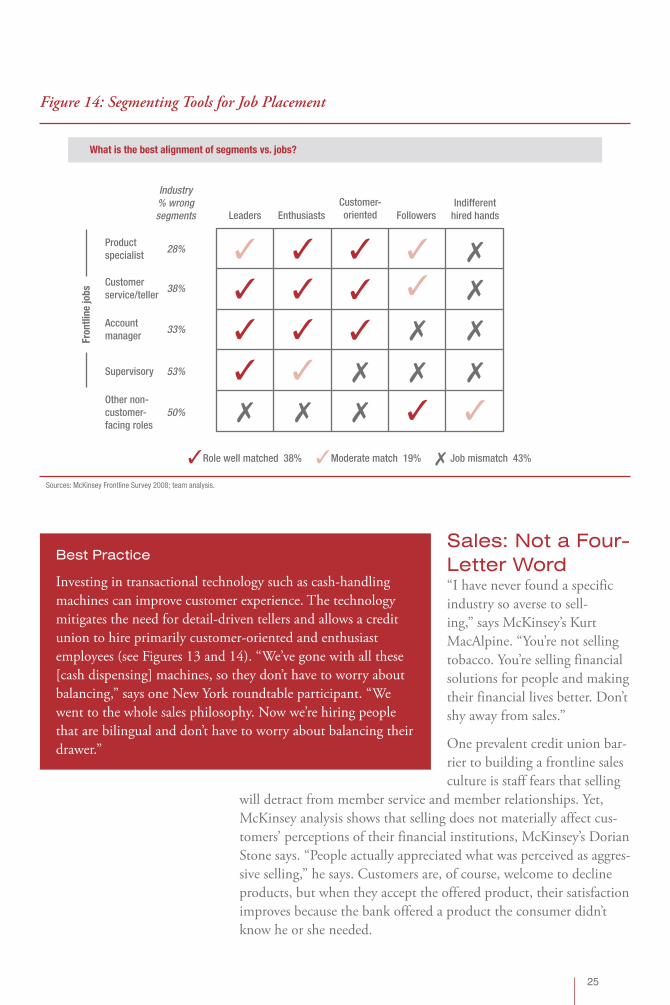

Fron

tline

jobs

Productspecialist

Industry% wrongsegments

28%

38%

33%

53%

50%

Accountmanager

Supervisory

Other non-customer-facing roles

Customerservice/teller

EnthusiastsLeaders

Role well matched 38% Moderate match 19% Job mismatch 43%

FollowersIndifferent

hired handsCustomer-oriented

What is the best alignment of segments vs. jobs?

Figure 14: Segmenting Tools for Job Placement

Sources: McKinsey Frontline Survey 2008; team analysis.

Best Practice

Investing in transactional technology such as cash-handling machines can improve customer experience. The technology mitigates the need for detail-driven tellers and allows a credit union to hire primarily customer-oriented and enthusiast employees (see Figures 13 and 14). “We’ve gone with all these [cash dispensing] machines, so they don’t have to worry about balancing,” says one New York roundtable participant. “We went to the whole sales philosophy. Now we’re hiring people that are bilingual and don’t have to worry about balancing their drawer.”

26

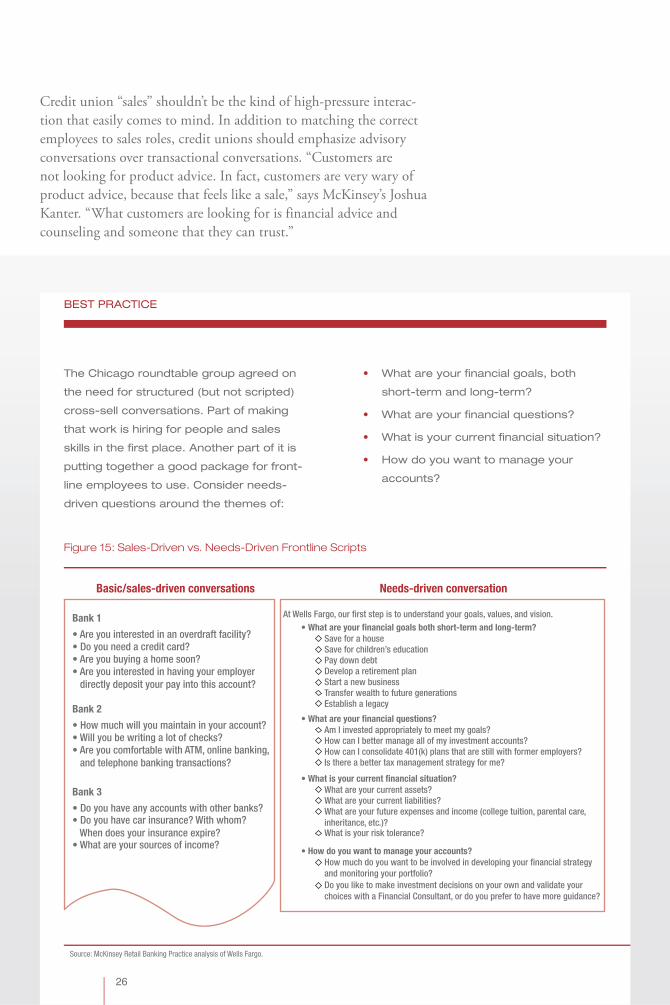

BEST PRACTICE

The Chicago roundtable group agreed on

the need for structured (but not scripted)

cross-sell conversations. Part of making

that work is hiring for people and sales

skills in the first place. Another part of it is

putting together a good package for front-

line employees to use. Consider needs-

driven questions around the themes of:

What are your financial goals, both •

short-term and long-term?

What are your financial questions?•

What is your current financial situation?•

How do you want to manage your •

accounts?

Bank 1

Basic/sales-driven conversations Needs-driven conversation

Bank 2

Bank 3

Figure 15: Sales-Driven vs. Needs-Driven Frontline Scripts

Source: McKinsey Retail Banking Practice analysis of Wells Fargo.

Credit union “sales” shouldn’t be the kind of high-pressure interac-tion that easily comes to mind. In addition to matching the correct employees to sales roles, credit unions should emphasize advisory conversations over transactional conversations. “Customers are not looking for product advice. In fact, customers are very wary of product advice, because that feels like a sale,” says McKinsey’s Joshua Kanter. “What customers are looking for is financial advice and counseling and someone that they can trust.”

BEST PRACTICE

Push organization-wide goals down to the

branch and individual levels. Cathy Rios of

Travis Credit Union in Vacaville, California,

shares how her credit union operations

team visits each branch and specifies its

expected contribution to the overall credit

union goals. From there, branch managers

are allowed to decide how to pursue their

goals. The message to branch managers:

“You’re the captain of your ship, and we

expect you to drive business. And we’re

here to help you,” Rios says. “Now [we’re]

seeing them call marketing because they

want to do an event. That never happened.

We were pushing the event to them. Now

they’re calling us.”

Consider cascading branch targets to

balances and numbers of accounts per

individual teller, McKinsey’s Kurt MacAlpine

suggests. It allows every employee and

manager to track tangible individual per-

formance and, correspondingly, to identify

individual ways to improve.

That perspective is bolstered by an anecdote from one CEO at the Los Angeles roundtable: “I actually had a [member service represen-tative] who came, sat in my office and cried, and said, ‘Take away $2 an hour just so I don’t have to sell. I don’t want to sell. I can’t sell,’ ” the CEO recounts. “She absolutely is our top producer, and

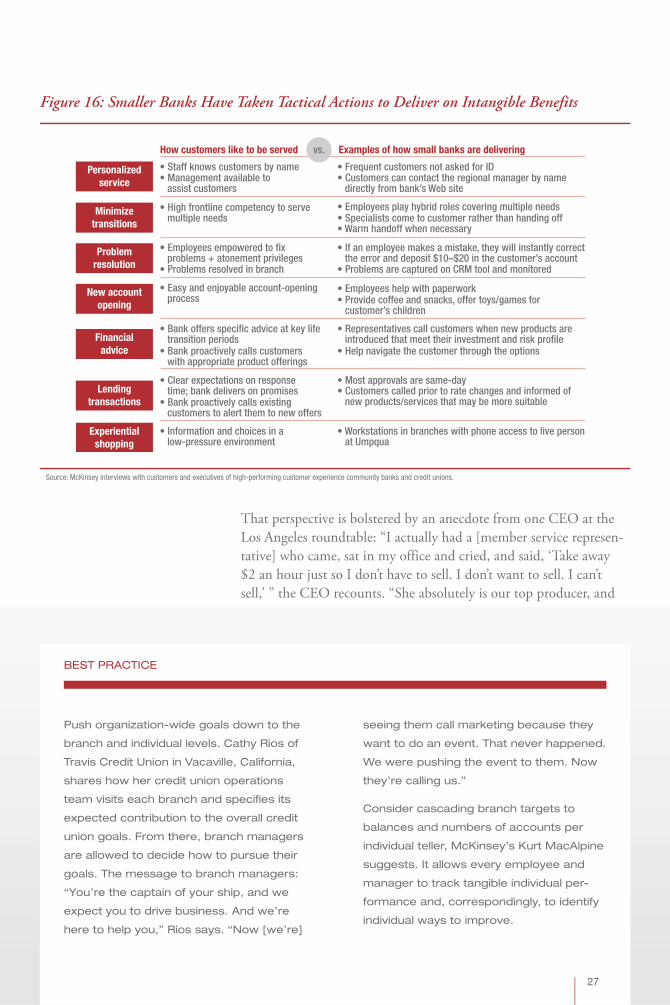

How customers like to be served Examples of how small banks are delivering

Personalizedservice

Experientialshopping

Lendingtransactions

Financialadvice

New accountopening

Problemresolution

Minimizetransitions

Figure 16: Smaller Banks Have Taken Tactical Actions to Deliver on Intangible Benefits

Source: McKinsey interviews with customers and executives of high-performing customer experience community banks and credit unions.

27

28

we talked about, ‘What is your definition of selling? I’m not asking you to sell a car; I’m asking you to prevent this person from going to Wells [Fargo] and getting charged 29% on their credit card.’ And immediately it clicked.” The takeaway: “If you hire people who like to be liked, you can’t call it sell-ing, because they don’t like that word.”

One way to encourage a mindset shift on the front line, MacAlpine argues, is to move customer satisfaction down to a secondary metric for frontline employees. Instead prioritize metrics like cross-sells or increased balances. High customer satisfaction will usu-ally get customers to the consideration stage, but sales-oriented staff matched with sales targets bring them through to purchase.

“To the extent that you can get customer experience to bring them in the door, to help set them up for a better financial future, don’t shy away from the sales,” MacAlpine says.

Hiring for ResultsForget training for passion, urges one Chicago roundtable partici-pant; it’s too expensive. Even the best training will probably not turn a hired hand into an enthusiast. And doing so will cost much more over the life of the employee than the cost of hiring correctly in the first place.

“What we find across financial institutions is the branch manager is the single biggest leverage point for performance,” Stone says. “This doesn’t necessarily mean that to make sure our branch manager is doing well, let’s go give them all raises. What it does mean is let’s work really hard to find that good branch manager. They’re the big-gest swing vote in terms of sales performance.”

One downside of credit unions’ historical focus on service over sales is that that approach limits the possibility of hiring top sales talent, Stone says. “We did a major piece of work on recruiting talent for a mutual insurance company. In the spirit of trying to be fair and give people one more chance, they were holding onto [poor] performers, and the highest performers in the company, and the ones that they

Best Practice

Develop a factually correct explanation of why each of your products is better than (or competitive with) that of your near-est competitor. And it shouldn’t be “Because you’re a member, and you own the credit union,” says McKinsey’s Dorian Stone. “That’s nice to have, but it misses the foundation of what you are there for.” Formulating the comparison will force managers to define the benefits of the credit union’s product set and give frontline staff effective sales tools.

29

were trying to attract from outside the company, they just didn’t have respect for the system,” he adds.

Employees who are excellent on the front line of a credit union are also attractive to other employers, so retaining them is important.

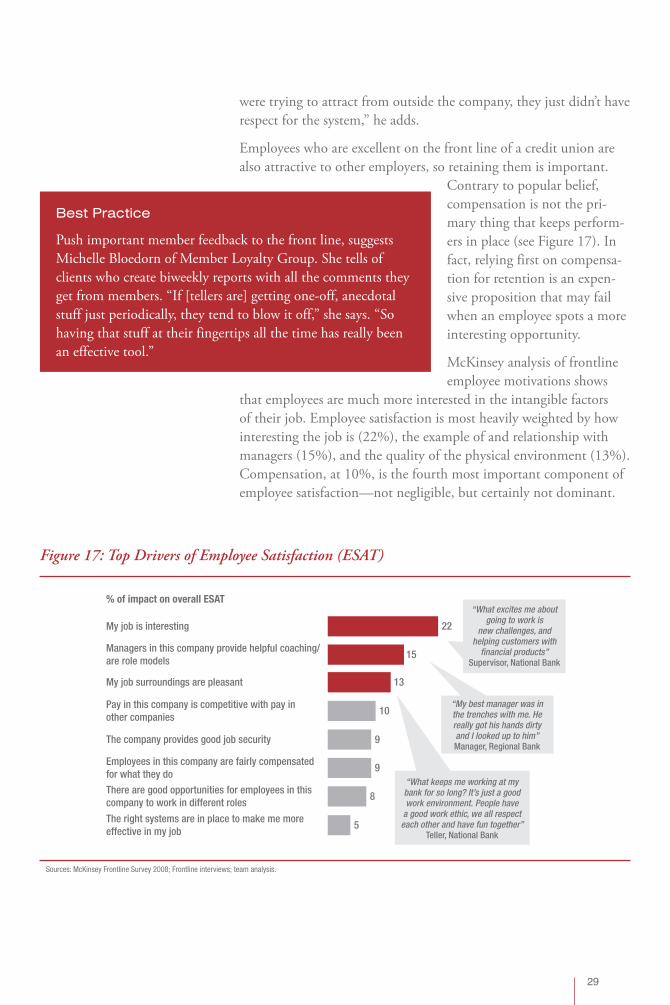

Contrary to popular belief, compensation is not the pri-mary thing that keeps perform-ers in place (see Figure 17). In fact, relying first on compensa-tion for retention is an expen-sive proposition that may fail when an employee spots a more interesting opportunity.

McKinsey analysis of frontline employee motivations shows

that employees are much more interested in the intangible factors of their job. Employee satisfaction is most heavily weighted by how interesting the job is (22%), the example of and relationship with managers (15%), and the quality of the physical environment (13%). Compensation, at 10%, is the fourth most important component of employee satisfaction—not negligible, but certainly not dominant.

% of impact on overall ESAT

My job is interesting

Managers in this company provide helpful coaching/are role models

My job surroundings are pleasant

Pay in this company is competitive with pay inother companies

The company provides good job security

Employees in this company are fairly compensatedfor what they do

There are good opportunities for employees in thiscompany to work in different roles

The right systems are in place to make me moreeffective in my job

“What excites me aboutgoing to work is

new challenges, andhelping customers with

financial products”Supervisor, National Bank

“My best manager was inthe trenches with me. Hereally got his hands dirtyand I looked up to him”Manager, Regional Bank

“What keeps me working at mybank for so long? It’s just a goodwork environment. People have

a good work ethic, we all respecteach other and have fun together”

Teller, National Bank

22

15

13

10

9

9

8

5

Figure 17: Top Drivers of Employee Satisfaction (ESAT)

Sources: McKinsey Frontline Survey 2008; Frontline interviews; team analysis.

Best Practice

Push important member feedback to the front line, suggests Michelle Bloedorn of Member Loyalty Group. She tells of clients who create biweekly reports with all the comments they get from members. “If [tellers are] getting one-off, anecdotal stuff just periodically, they tend to blow it off,” she says. “So having that stuff at their fingertips all the time has really been an effective tool.”

30

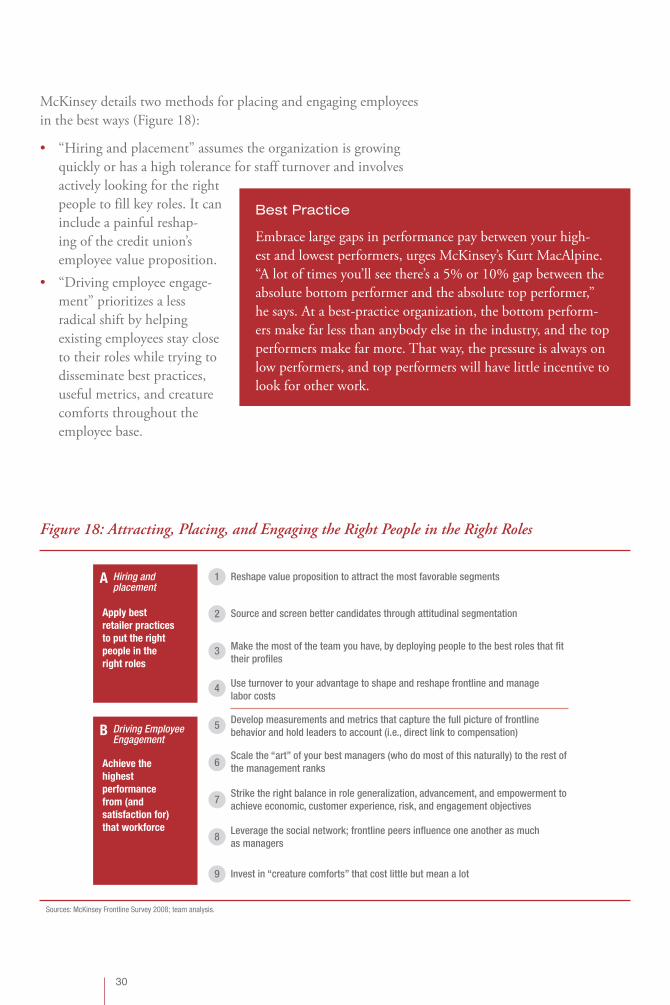

McKinsey details two methods for placing and engaging employees in the best ways (Figure 18):

“Hiring and placement” assumes the organization is growing • quickly or has a high tolerance for staff turnover and involves actively looking for the right people to fill key roles. It can include a painful reshap-ing of the credit union’s employee value proposition.“Driving employee engage-• ment” prioritizes a less radical shift by helping existing employees stay close to their roles while trying to disseminate best practices, useful metrics, and creature comforts throughout the employee base.

Reshape value proposition to attract the most favorable segments1

Source and screen better candidates through attitudinal segmentation2

Make the most of the team you have, by deploying people to the best roles that fittheir profiles

3

Use turnover to your advantage to shape and reshape frontline and managelabor costs

4

Develop measurements and metrics that capture the full picture of frontlinebehavior and hold leaders to account (i.e., direct link to compensation)

5

Scale the “art” of your best managers (who do most of this naturally) to the rest ofthe management ranks6

Strike the right balance in role generalization, advancement, and empowerment toachieve economic, customer experience, risk, and engagement objectives

7

Leverage the social network; frontline peers influence one another as muchas managers

8

Invest in “creature comforts” that cost little but mean a lot9

Hiring andplacement

Apply best retailer practicesto put the rightpeople in theright roles

A

Driving EmployeeEngagement

Achieve thehighestperformancefrom (andsatisfaction for)that workforce

B

Figure 18: Attracting, Placing, and Engaging the Right People in the Right Roles

Sources: McKinsey Frontline Survey 2008; team analysis.

Best Practice

Embrace large gaps in performance pay between your high-est and lowest performers, urges McKinsey’s Kurt MacAlpine. “A lot of times you’ll see there’s a 5% or 10% gap between the absolute bottom performer and the absolute top performer,” he says. At a best-practice organization, the bottom perform-ers make far less than anybody else in the industry, and the top performers make far more. That way, the pressure is always on low performers, and top performers will have little incentive to look for other work.

31

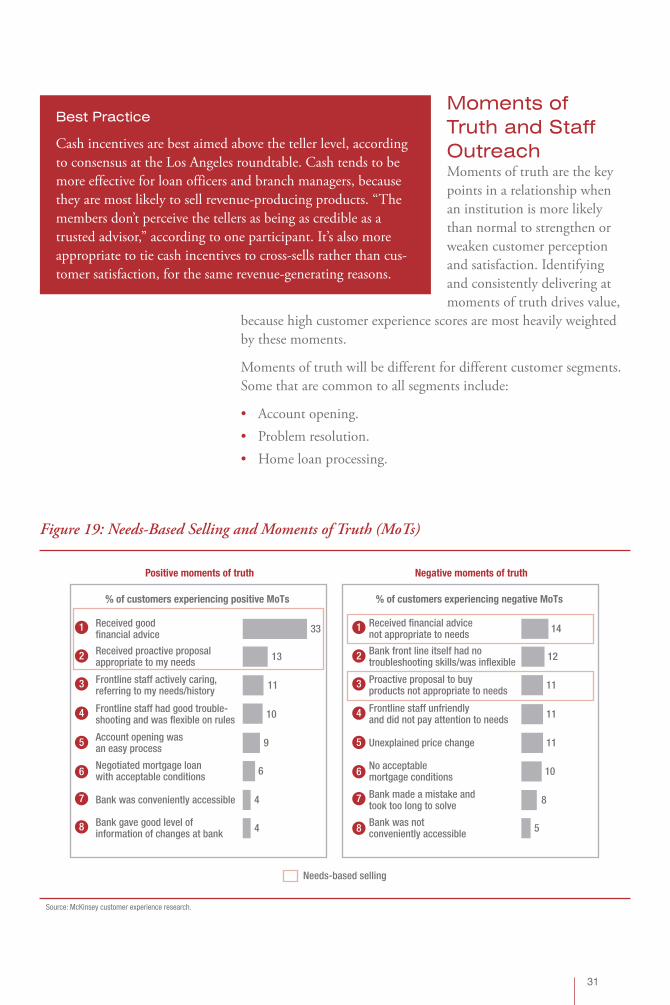

Moments of Truth and Staff OutreachMoments of truth are the key points in a relationship when an institution is more likely than normal to strengthen or weaken customer perception and satisfaction. Identifying and consistently delivering at moments of truth drives value,

because high customer experience scores are most heavily weighted by these moments.

Moments of truth will be different for different customer segments. Some that are common to all segments include:

Account opening.• Problem resolution.• Home loan processing.•

Received goodfinancial advice

Positive moments of truth

% of customers experiencing positive MoTs

Received proactive proposalappropriate to my needs