customer lifecycle value & relationship marketing

DESCRIPTION

clv and relationship marketing explainedTRANSCRIPT

Customer Lifetime Value & Relationship exercise in Retail

BankingPresented By:Ankur Ashok B009Anshul Gupta B023Ganesh Padhi B047Richansh Kumar B038Iravatee Chitte D010Sagnik Niyogi D043Arihant Jain D024

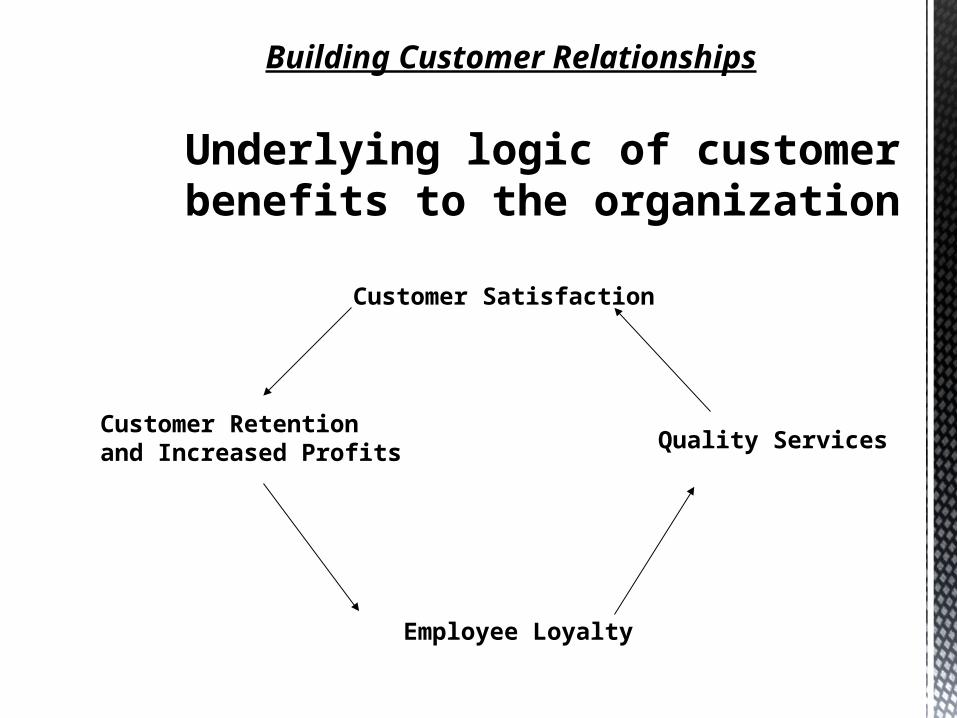

Underlying logic of customer benefits to the organization

Customer Satisfaction

Customer Retention and Increased Profits Quality Services

Employee Loyalty

Building Customer Relationships

CLV attempts to determine the economic value customers bring over their “lifetime” with the business

At the heart of understanding CLV lies the recognition that a customer does not represent a single transaction but a relationship that is far more valuable than any one time exchange.

What is Customer Lifetime Value (CLV) and Why is it important ?

Because if you don’t know what a client is worth, you don’t know what you should spend to get one or what you should spend to keep one

Understanding CLV is incredibly important for customer service

professionals and for businesses of all types.

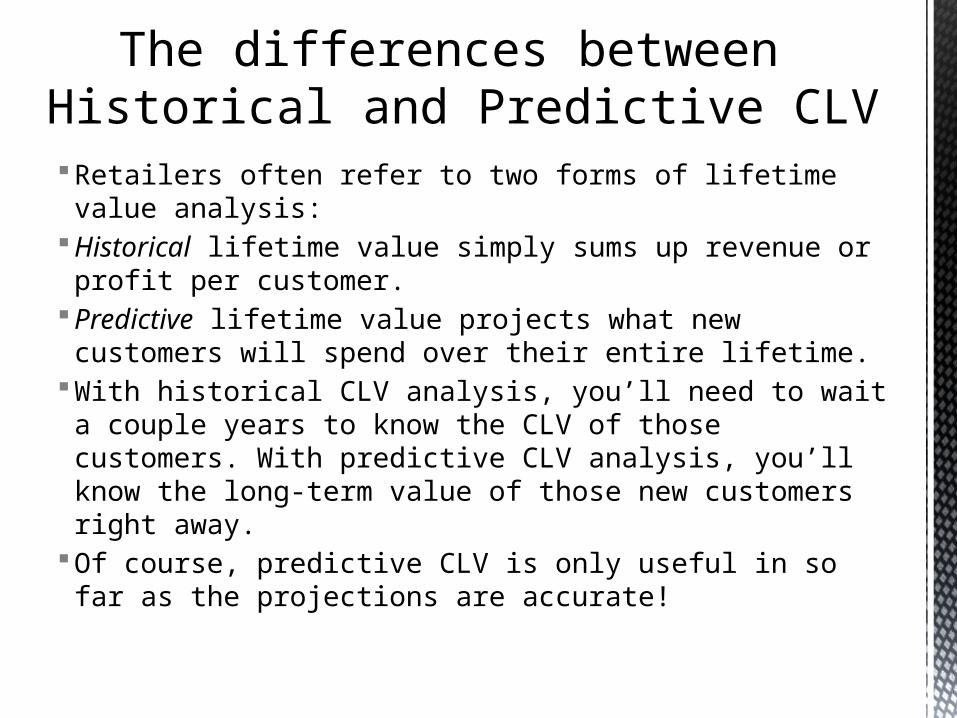

Retailers often refer to two forms of lifetime value analysis:Historical lifetime value simply sums up revenue or profit per

customer.Predictive lifetime value projects what new customers will

spend over their entire lifetime.With historical CLV analysis, you’ll need to wait a couple years

to know the CLV of those customers. With predictive CLV analysis, you’ll know the long-term value of those new customers right away.

Of course, predictive CLV is only useful in so far as the projections are accurate!

The differences between Historical and Predictive CLV

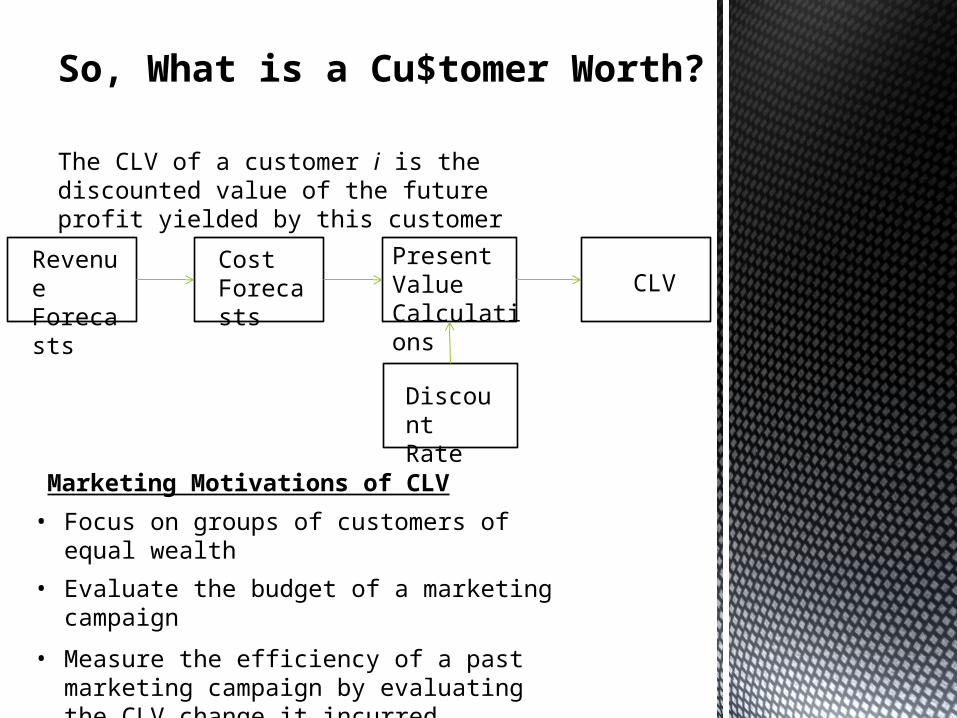

The CLV of a customer i is the discounted value of the future profit yielded by this customer

Revenue Forecasts

Present Value Calculations

Cost Forecasts CLV

Discount Rate

Marketing Motivations of CLV

• Focus on groups of customers of equal wealth

• Evaluate the budget of a marketing campaign

• Measure the efficiency of a past marketing campaign by evaluating the CLV change it incurred

So, What is a Cu$tomer Worth?

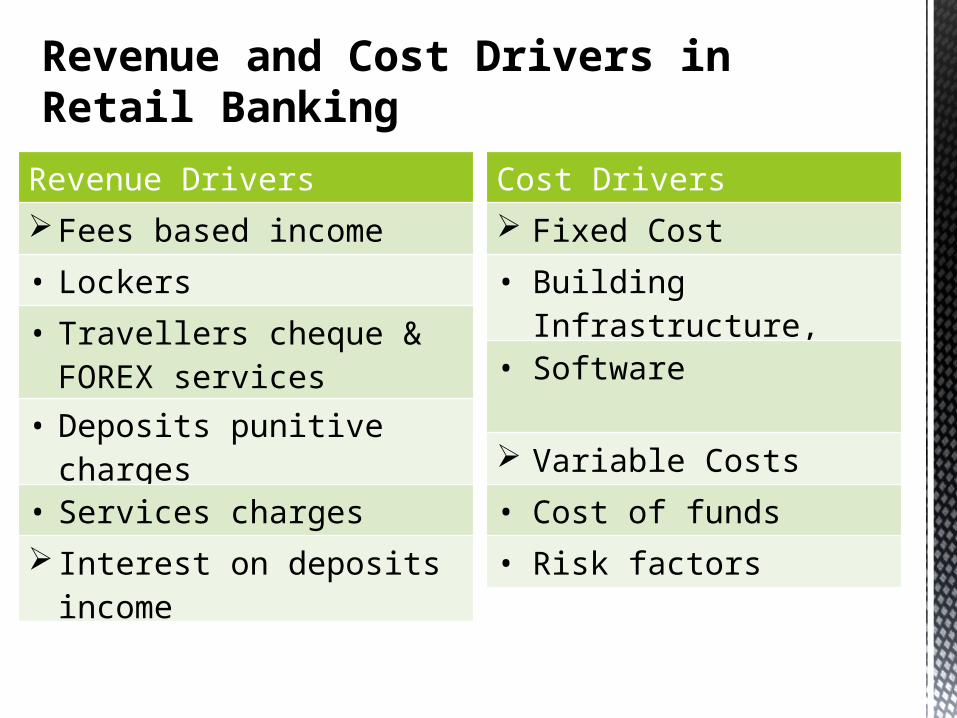

Revenue and Cost Drivers in Retail Banking

Cost Drivers

Fixed Cost

• Building Infrastructure,

• Software

Variable Costs

• Cost of funds

• Risk factors

Revenue Drivers

Fees based income

• Lockers

• Travellers cheque & FOREX services

• Deposits punitive charges

• Services charges

Interest on deposits income

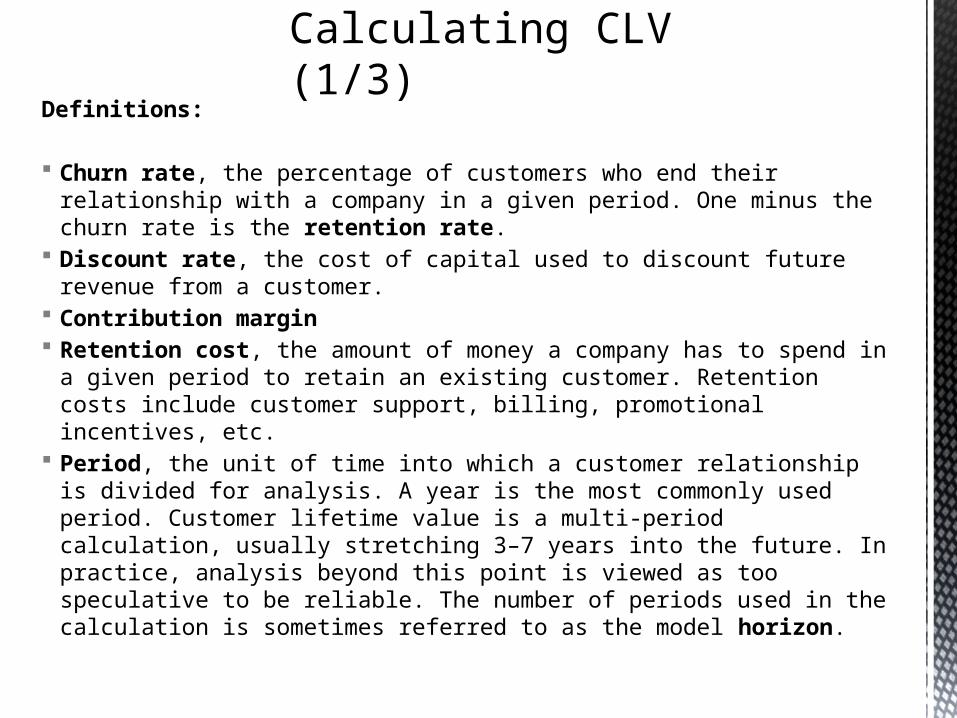

Definitions:

Churn rate, the percentage of customers who end their relationship with a company in a given period. One minus the churn rate is the retention rate.

Discount rate, the cost of capital used to discount future revenue from a customer. Contribution margin Retention cost, the amount of money a company has to spend in a given period to

retain an existing customer. Retention costs include customer support, billing, promotional incentives, etc.

Period, the unit of time into which a customer relationship is divided for analysis. A year is the most commonly used period. Customer lifetime value is a multi-period calculation, usually stretching 3–7 years into the future. In practice, analysis beyond this point is viewed as too speculative to be reliable. The number of periods used in the calculation is sometimes referred to as the model horizon.

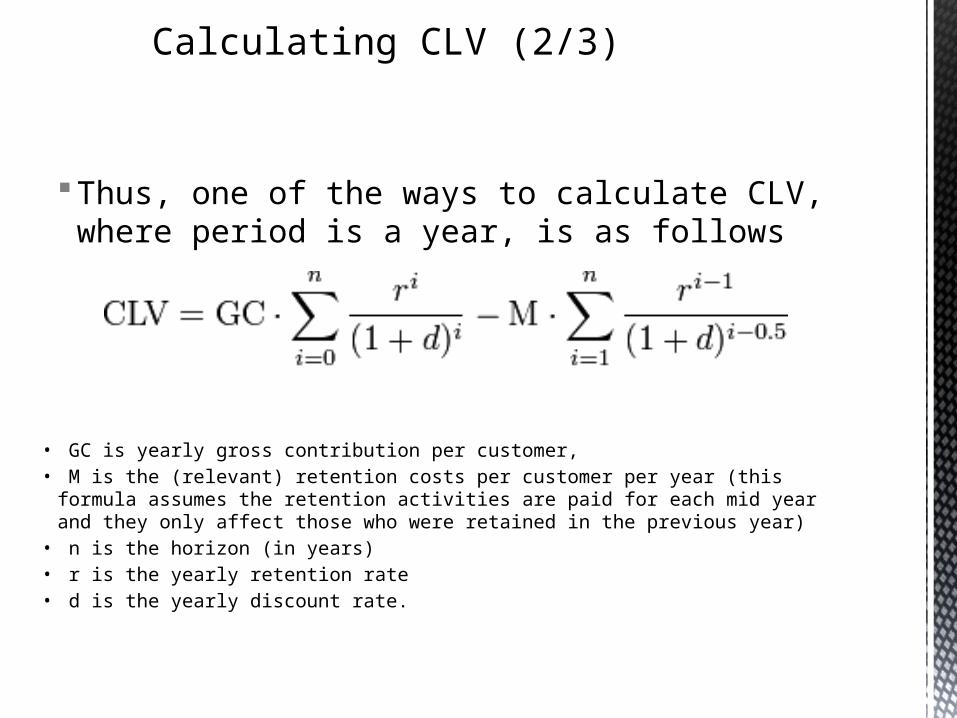

Calculating CLV (1/3)

Thus, one of the ways to calculate CLV, where period is a year, is as follows

Calculating CLV (2/3)

• GC is yearly gross contribution per customer, • M is the (relevant) retention costs per customer per year (this formula assumes the

retention activities are paid for each mid year and they only affect those who were retained in the previous year)

• n is the horizon (in years)• r is the yearly retention rate• d is the yearly discount rate.

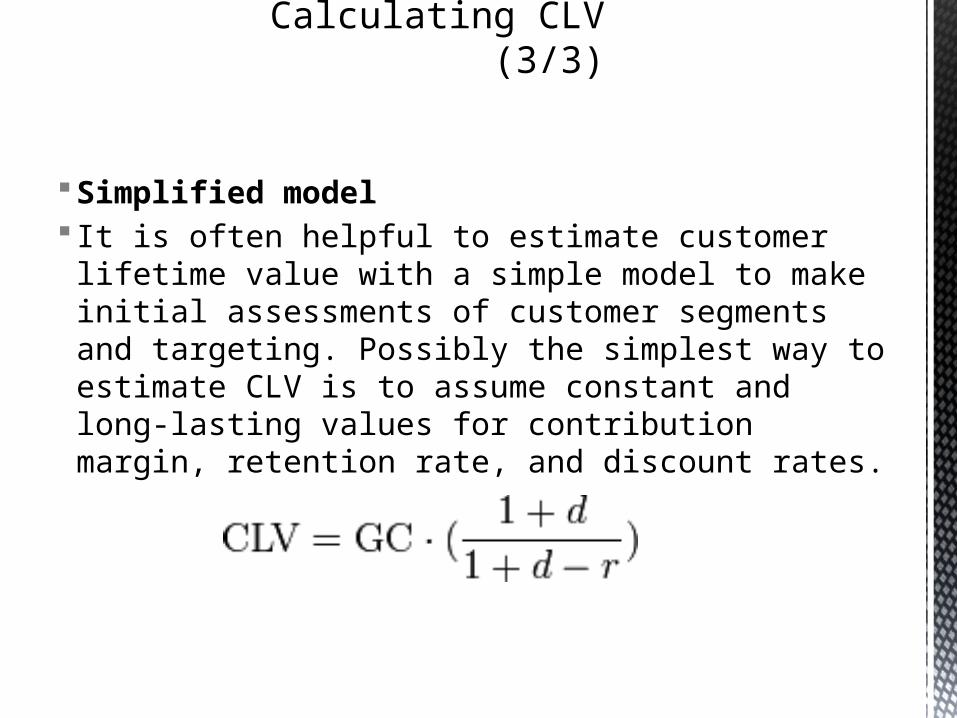

Simplified model It is often helpful to estimate customer lifetime value with a

simple model to make initial assessments of customer segments and targeting. Possibly the simplest way to estimate CLV is to assume constant and long-lasting values for contribution margin, retention rate, and discount rates.

Calculating CLV (3/3)

Getting Retaining Satisfying Enhancing

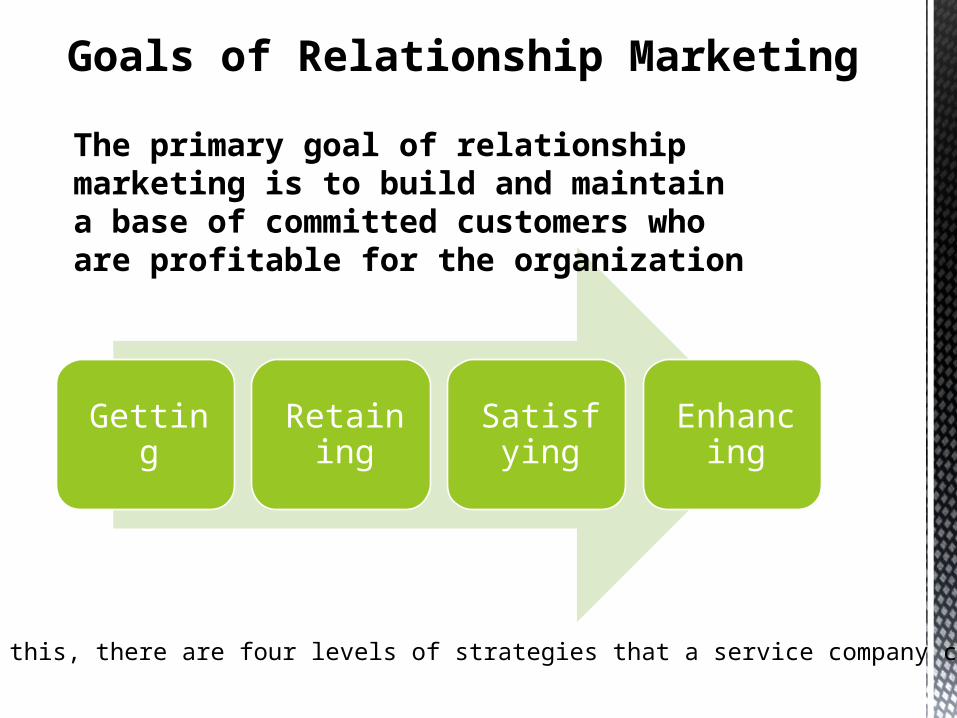

To achieve this, there are four levels of strategies that a service company can employ.

Goals of Relationship Marketing

The primary goal of relationship marketing is to build and maintain a base of committed customers who are profitable for the organization

12

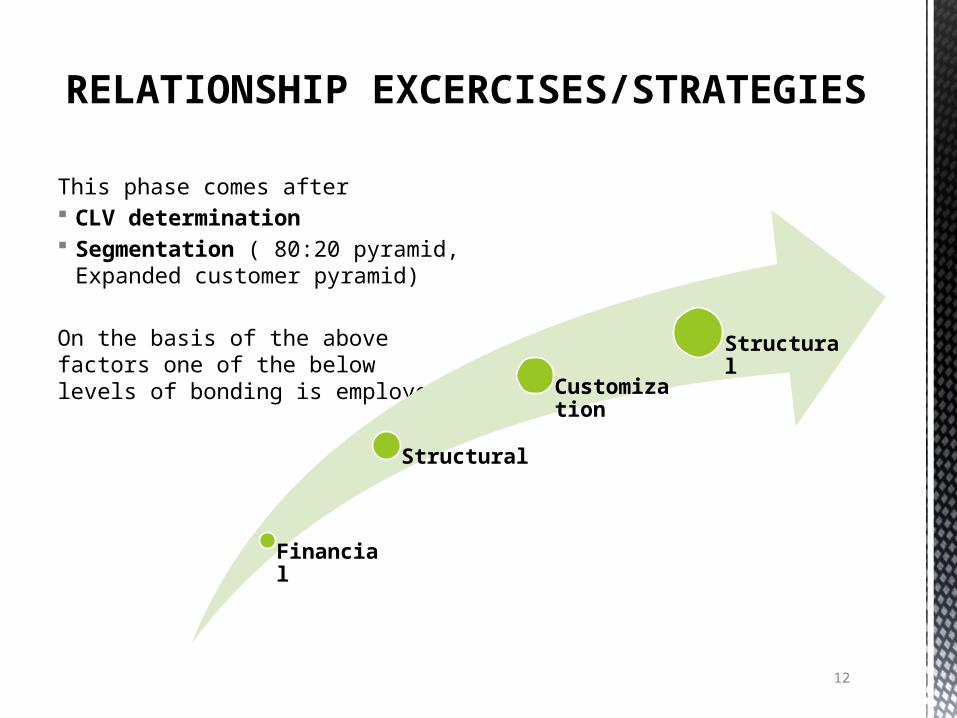

This phase comes after CLV determination Segmentation ( 80:20 pyramid,

Expanded customer pyramid)

On the basis of the above factors one of the below levels of bonding is employed.

RELATIONSHIP EXCERCISES/STRATEGIES

Financial

Structural

Customization

Structural

13

Provide financial incentivesUsed in most situationsMost easy to imitateShort terms gainsEasy for competitors to imitateCustomer tend to switch whenever better

deal arises

Level 1: Financial Bonds

Low rates on Demat AccountPayback Loyalty CardEMI optionsPre-qualification for loan eligibilityPreferential interest rates and/or processing

fees on Loan productsDiscounts on Locker facility and preferential

allotmentPreferential pricing on purchase of gold,

sale/purchase of forex

Financial Bonds by ICICI

15

Price is important but social bonds go furtherMany not tie customers permanentlyMore difficult for competitors to imitate than financial bondsCan encourage longer relationship with consumersWith financial incentives become very effective

Level 2: Social Bonds

Dedicated Relationship Manager is assigned who acts like a single POC to service varied needs like buying property and seeking loans

These experts bring to the table ICICI Bank's expertise across various financial products, offering you

Enhanced service levels Quicker responses End-to-end solution

More than anything, this Relationship Manager becomes the face of ICICI for the customer and he understands the needs of the customer due to repeated interactions

Social Bonds by ICICI

17

Make your processes flexibleCustomized to individual requirementsTwo important aspects

Mass customization Personalized Customer interaction

Even more difficult to imitate than financial and social bonds

Level 3: Customization Bonds

Needs of every individual investing is different. Some want growth, others want stability

ICICI creates, reviews and rebalances your investment plan to meet your needs.

A 5 stage process is followed, where your Relationship Manager and a team of experts will work closely with you to customize your investment.

Step 1: Understanding your Risk Profile Step 2: Asset AllocationStep 3: Investment AdvisoryStep 4: Review your InvestmentsStep 5: Matching your changing needs

Customization bonds in ICICI

19

Level 4- Structural Bonds Looks in to customers processesUse of technology and expertise Improve customer processesTotally customized according to requirementsMost difficult to imitate

Level 4: Structural Bonds

ICICI provides services that help strengthen business relationships by ensuring reliability and speed in your business documentation and payments

Provides credit facilities smoothen your cash flows, ensuring business never suffers. These require close collaboration and data sharing

ICICI systems are interlinked with L&T’s payroll for automatic credit of salaries

Structural Bonds in ICICI

Thank you!