c.v.o. ca’s news & views vol. 20 no. 2 / august 2016 2016/chairmanaug16.pdf · convenor ca...

TRANSCRIPT

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

3

From the desk of ChairmanThe Biggest piece of Reform sees the light of the day……

NEWS BULLETINCOMMITEE

ChairmanCA Mulesh Savla

Office BearerCA Nilesh Dedhia

AdvisorCA Hiten Gada

ConvenorCA Rahul Nagda

Jt. ConvenorCA Harsh Dedhia

MembersCA Deepesh ChhedaCA Ameet Chheda

CA Paras MaruCA Sagar Maru

CA Niraj ChhedaCA Jeet Gala

CA Pratik ShahnandCA Jinit BhedaSp. Invitees

CA Arvind Nagda

C O N T E N T S

ASSOCIATION NEWS

Forth ComingEvents ....................... 4

Events Retrospect ..... 5

ManagingCommittee &Sub committee List .. 6

Annual Activity .......... 7

A R T I C L E S

Transfer PricingAssessments– A basic Overview .. 9

Corporate SocialResponsibility- An Insight ............ 13

Presentation onICDS andInd AS / ASDifferences .............. 19

The Reality ofVirtual Reality .......... 29

Technical updateKolkata ITAT (SB)Rules in favour ofthe Revenue bydirecting mandatoryALP determinationfor inboundinterest free loan ..... 30

New Membersenrolled ................... 34

“The most courageous act is still to think for yourself. Aloud.”

Dear Members,

The biggest reform, since an Independence, perhaps,not just the most transformative tax reform buta substantialpiece of business reform, the Goods and Service Tax Bill did sees the light of the day withthe Rajya Sabha passing the same unanimously, except the members of AIADMK walking out of thehouse under protest, paving way for the most awaited, destination based tax, replacing a raft ofdifferent state and local taxes with a single unified value added tax system to turn the country intoworld's biggest single market.

As we are aware, our Constitution gave powers to the Centre to levy taxes like Central Excise Duty,Service Tax and empoweredthe states to collect Sales Tax or VAT and few other local taxes like Octroi,which is amended now, as the 122nd Constitution Amendment Bill. This amendment gives concurrentpowers to the Centre and the States to make legislation on taxation of Goods and Services.

The Bill was passed in the Lok Sabha last year;however, due to series of changes suggested by variouscommittees at different levels, there have been major amendments to it. And therefore, it needs to getapproval of the Lower House again.

Once it is approved by both the houses, the final draftis required to be accepted or ratified by atleast50% of the 29 state assemblies before it can become the final Act.

Since now, about 13 states are ruled by the BJP and the finance ministers of few other states also havepublicly accepted the same; it may not be difficult to move forward for the ultimate implementationof GST. However, what is important is the time within which the same is ratified by the States.

The centre is ready with the draft norms to set up a GST council to finalise key things like the GSTrateand also some important debating point like the extent of the indirect taxes that will be subsumedunder GST,so on and so forth.

Though the government has time and again expressed its willingness to roll out GST by April 1, 2017,the experts have their own doubts about this aggressive deadline.

In fact a huge new IT system has to be set up. It has been announced that the contract to developand create the entire IT system to implement and administer GST law has already been assigned toa leading IT company of India. Even the tax collectors and the officials are required to be trained.

The administration of GST to be broken up in three segments being CGST, SGST and IGST and thesame will be administered by both the centre and the state governments. How these duel authoritieswill function is still a cause of confusion and concern.

On the other side, the tax payers, the Indian Inc., are also required to be geared up as there is goingto be a see change in the way Indian Inc was doing business hitherto.

Since the threshold limit isexpected to be much lower, most dealers from unorganised sectors aregoing to feel the heat and to pass on the appropriate input credits to their customers, they will bedrawn into the tax net. Incidentally this will enhance the, much needed, tax base for the government.Also, since there will be a levy of tax on the supply of goods and services, the dealers need to paytax even on their branch transfers, requiring them to jack up their working capital substantially. As about60% of the freight traffic in India is on the roads, logistic sector will have free play now to go acrossany states of the country, there by substantially reducing their time and consumption of fuel.

These and many more changes in the business landscape will create huge demand for the professionalsin the field and our members should gear up to take the fullest benefit of the same.

Warm regards, CA Mulesh Savla

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

4

Compiled by :CA. Rahul NagdaCA. Harsh Dedhia

ASSOCIATIONNEWS

FORTH COMING EVENTS

Student Committee has organsied Orientation for New article Students

Orientation course for newly joined article students is planned at D R Ghalla Memorial Hall, Dadar as perfollowing details:

Date Time Topic Speaker

22nd August 2016 4.00 to 6.00 Basics of Income Tax & TDS To be confirmed

(Monday) 6.15 to 7.30 Audit & Important clauses of Cos Act CA Harsh Dedhia

7.30 to 8.30 Email Management To be confirmed

23rd August 2016 4.00 to 6.00 Basics of VAT & Service Tax To be confirmed

(Tuesday) 6.15 to 7.30 Smart use of Excel at Work Place CA Vivek Gala

7.30 to 8.30 Three Years of Effective article ship CA Atul Bheda

Charges: Rs. 200/- per students.For Registration Contact Ms. Vaibhavi Shah 2410 5987

Study Circle Committee has organised study circle meeting on RECENT DEVELOPMENT IN TDS

Day & Date : Wedensday 24th August 2016

Time : 6.00 to 8.30 pm ( Snacks 5.30 to 6.00 pm)

Venue : D R Ghalla Memorial Hall, Dadar

Topic : Recent Development in TDS

Speaker : CA Mahendra Sanghvi

GST STUDY GROUP

Rajya Sabha on 3rd August, 2016 passed the much awaited Constitution amendment bill for Goods and ServiceTax (GST) with an absolute majority. The passing of the said legislation would result in newer and more complexchallenges. Accordingly, we have planned to form a "GST STUDY GROUP" to have an in-depth analysis ofGST Bill / Model Law.Particulars RemarksMeeting frequency Once in 15 days (can be modified according to interest of group)Timing 6.00 pm to 8.30 pmTentative Venue D. R. Ghalla Memorial Hall, 304, Jasmine Apt, DSP Road, Dadar (E) Mumbai - 14

(Kindly note that venue may be changed depending upon number of registrations)Investment Rs. 1000/- (For Member)

Rs. 2000/- (For Non Member)We request you to actively participate in the said Study Group and also provide your valuable to suggestion,if any to our Study Group Co-ordinator. For Registration contact:

Name Email TelephoneCA. Gautam Mota (Study Group Co-ordinator ) [email protected] 9594339945CA. Chintan Rambhia (Study Group Co-ordinator ) [email protected] 9867383060Vaibhavi Shah [email protected] 24105987

“How wrong is it for a woman to expect the man to build the world she wants, rather than to create it herself?”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

5

EVENTS RETROSPECT

PROGRAMME COMMITTEE

Seminar professionals on "Achieving ProfessionalExcellence"

The Association had organized Unique, Eye Openerand Thought Provoking Seminar for Professionals &Service based firms, on the topic "AchievingProfessional Excellence" by Dynamic Speaker Mr.Basesh Gala on 06th August 2016 at Damodar Hall,Parel TT. More than 350 participants had takenbenefit of the seminar. The speaker very aptly dealtwith major aspects which a service organizationfaces with case studies and also replied to thequestions raised by the participants. First time wehave make available online payment option whichwas received well

Membership and Recreation Committee

Career Guidance Panel Discussion for NewlyPassed CAs

MR Committee has planned Career Guidance PanelDiscussion for Newly passed CAs on Thursday 25thAugust 2016 at D R Ghalla Memorial Hall, Dadar,wherein successful Chartered AccountantsMembers in different fields like Practice, Audit, BigFour, Indirect Tax, Corporate, Equity analyst wouldguide participants through panel discussion and oneto one guidance. CAPITAL MARKET COMMITTEE has planned ameeting on Capital Market on Thursday, 25thAugust, 2016. The details are as follows:-

Venue: - IMFS 8th Floor, Diamond Destiny,Chabildas Road, Near Chabildas School,Dadar (West). Mumbai – 400 028

Time: - 7:00 p.m. to 9:00 p.m.

Fees: - Free for all CVO CA Association members

Prior Registration is compulsory; participation is onfirst come first serve basis.

Convener CA Parin Gala - 9967052078Vaibhavi Shah - 24105987

Members in Industry and Youth CommitteeWhite River Rafting at KoladIn the midst of hectic schedule let’s experience theexciting adventure of *WHITE WATER RAPIDS* andenjoy the natural beauty of *KUNDALIKA RIVER ATKOLAD*

MIYC of CVOCA organizes White Water RiverRafting for CVOCA Members and their familyDay & Date : Sat, 27th Aug, 2016Venue : Kolad, MaharashtraAge limit : Above 13 YearKey Attractions : White Water Rafting along with

Commondo Bridge,Burma Bridge, Volleyball.

Cost : Rs. 2,000 per pax.Cost includes Travelling, Breakfast, Lunch, High Teaand adventure filled White Water Rafting

Enrollment on First Come First Served basisFor Registration Fill Link:

http://goo.gl/forms/kTiQlnSRp2K9bjKy1For any further enquiries:Dadar CVO Office - 022-24105987Vinit Gada - 8655840598Heenal Shah - 9819758647Mittal Gala - 9819521665

FORTH COMING EVENTS

Student Committee

Student Study Circle on "Tax Audit Report andE-filing of Income Tax Returns

Study circle for students on the topic Tax AuditReport and E filing of Income Tax Returns wasorganized on 02nd August 2016 at D R GhallaMemorial Hall, where in student member HarshMaru and Jekin Dedhia lead the topics respectively.CA Gautam Mota chaired the session and guidedthe group leaders. In all 37 students have attendedthe study circle.

STUDY CIRCLE COMMITTEE

Study circle on the topic "IT and Social Media forCAs - Opportunities and Risks" was organized on09th August 2016 at D R Ghalla Memorial Hall whichwas lead by CA Maitri Savla. She explainedupcoming opportunities for CAs due to evolving ofnew technology which is changing dynamics of thebusiness. In all around 25 participants haveattended the study circle

“I hate to hear you talk about all women as if they were fine ladies instead of rational creatures.None of us want to be in calm waters all our lives.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

6

CVO CHARTERED AND COST ACCOUNTANTS' ASSOCIATIONLIST OF OFFICE BEARERS, MANAGING AND SUB COMMITTEE MEMBERS 2016-17

OFFICE BEARERS &MANAGING COMMITTEE

CA Ketan N. Gada President

CA Nilesh T. Dedhia Vice- President

CA Sunil V. Dedhia Secretary

CA Sanjay V. Chheda Jt. Secretary

CA Jigar R. Gogri Treasurer

CA Priti P. Savla Member

CA Jigar C. Chheda Member

CA Rahul T. Nagda Member

CA Ameet M. Chheda Member

CA Jeenal Sangoi Savla Member

CA Vinit D. Gada Member

CA Mehul T. Gala Member

CA Harsh H. Dedhia Member

CA Gautam R. Mota Member

CA Parin D. Gala Member

Committees Program Study Circle News Bulletin RRC & PDCommittee Committee Committee Committee

1 2 3 4

Chairman CA Himanshu Chheda CA Rajesh Shah CA Mulesh Savla CA Ketan SaiyaConvenor CA Jigar Chheda CA Gautam Mota CA Rahul Nagda CA Jeenal SawlaJt. Convenor CA Rahul Nagda CA Siddhart Karani CA Harsh Dedhia CA Ameet ChhedaAdvisor CA Haresh Chheda CA Mahendra Gala CA Hiten Gada CA Manoj ShahOB in Charge CA Nilesh Dedhia CA Jigar Gogri CA Nilesh Dedhia CA Sunil DedhiaSpecial Invitee CA Paresh Vora CA Rakesh Vora CA Arvind Nagda CA Jasmine SawlaMembers CA Vinit Gada CA Tansukh Chheda CA Ameet Chheda CA Anil Hariya

CA Mehul Gala CA Virav Dedhia CA Deepesh Chheda CA Prashant VoraCA Anil Haria CA Jiger Saiya CA Paras Maru CA Sanjay SavlaCA Nilesh Saiya CA Dharmi Kenia CA Sagar Maru CA Mayank GadaCA Vishesh Sangoi CA Hetal Maru CA Neeraj Chheda CA Shreyas SangoiCA Hetal Nandu CA Chintan Rambhia CA Jeet Gala CA Neerav GalaCA Umang Soni CA Hemant Shah CA Pratik Shahnand CA Zalak Savla

CA Jinit Bheda CA Kruti Sangoi

Students Members in Indstry Capital Market Membership & Publication, Website &Committee Committee and Youth Committee Recreation Representation IT Committee

Committee Committee & PR Committee

5 6 7 8 9 10

Chairman CA Bharat Gala CA Atul Bheda CA Navin Shah CA Dinesh Shah CA Paras Savla CA Paras Savla

Convenor CA Vinit Gada CA Priti Savla CA Parin Gala CA Ameet Chheda CA Mehul Gala CA Harsh Dedhia

Jt. Convenor CA Girish maru CA Vinit Gada CA Manish Dedhia CA Harshvardhan Shah CA Kiran Nandu

Advisor CA Navin Shah CA Atul Bheda CA Hasmukh Dedhia

OB in Charge CA Sanjay Chheda CA Sunil Dedhia CA Jigar Gogri CA Jigar Gogri CA Nilesh Dedhia CA Sanjay Chheda

Special CA Jayesh Salia CA Sanjeev Lalan CA Vignesh Bheda CA Ketan Mamania CA Dilip Gosar CA Ashwin Shah

Invitee CA Bharat Nagda CA Jayesh Gogri

Members CA Hitesh Pasad CA Chintan Karani CA Anil Haria CA Sanjay Savla CA Harsh Dedhia CA Rupal Haria

CA Gautam Mota CA Kewal Satra CA HarshvardhanShah CA Girish maru CA Namrata Dedhia CA Harshvardhan Shah

CA Poojan Dedhia CA Kimi Nagda CA Nilesh Chhadva CA Jayesh Chheda CA Bhavin Dedhia CA Hardik Maru

CA Mitul Furia CA Shrenik Shah CA Umang Soni CA Shrenik Shah CA Kruti Sangoi CA Jeet Gala

CA Jay Dinesh Gala CA Hetal Nandu CA Kushal Dedhia CA Shreyas Sangoi CA Kishor Gada CA Nimesh Dedhia

CA Deepa Pasad CA Mittal Gala CA Nikita Gogri CA Neha Vira

CA Viral Satra CA Jay Gosar CA Jay Gosar

CA Disha Dedhia CA Herin Mota CA Siddharth Karani

CA Heenal Shah

CCA Course Group

Convenor CA Rupal Haria

Member CA Namrata Dedhia

CA Kaushik Gada

CA Nisha Gala

CA Smit Shah

CA Dimpall Chheda

MEMBERSHIP DRIVE GROUPCA Atul BhedaCA Sanjeev LalanCA Priti SavlaCA Sanjay ChhedaCA Neha ViraCA Ketan MamaniaCA Girish Maru

With Youth Committee

“When I discover who I am, I’ll be free.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

7

ANNUAL ACTIVITYPROGRAMME COMMITTEEz Programme on Cheritable Trust

z Budget Seminar

z Local Budget meetings

z Seminar on GST

z Local meetings on GST

z Succession Planning – taking business fromFamily Driven to Public Driven

z Professional Development & Branding

z Success Stories of persons who have becomeiconic from zero.

NEWS BULLETIN COMMITTEEz To Publish Monthly Bulletin covering

Communication from chairman/President.Articles from members/Students/ members inIndustry. Issues on specific topics like StatutoryAudit, Internal Audit, Transfer Pricing, FEMA,International Taxation, etc.

z New members photo & Congratulation Column,Representation etc

z Articles and write-ups on legal maxims, judicialinterpretations, doctrine and meaning of legalterms

z Forthcoming Events & Events in restrospectshall preferably be noted on the cover page inbullet points

z Considering present costing structure, it hasbeen decided to appeal to all members to getnews and views circulated to client place. Thiswill help to brand news and views with morereach.

z It is decided to obtain more advertisement andneed be insert 4 additional colour pages in themiddle of journal.

RRC & PD COMMITTEEz Members RRC in the month of February 2017

with topics of GST Law, IndAS, IFC, Income Taxand rother topics related to ProfessionalDevelopment at location like Alibaug,Ahmendabad, Manor etc

STUDY CIRCLE COMMITTEEz Seminar on drafting, deeds & documentation

with special emphasis on LLP

z Seminar on labour laws

z Securities Law

z Stamp duty - applicability, procedure

z Bank audits

z Recent amendments in Company Act

z Tax implication for LLP - Business reorganisationetc.

z Recent judgements under direct tax

z Taxation of HUF and family arrangement

z Recent developments in TDS alongwith judicialprecedents

z Income Declaration Scheme - CCIT

z Direct/Indirect Tax Provisions of Finance Bill,2017

z Power Yoga

z RTI - relevance for Income Tax

z various funding alternative available to SME -Listing at SME exchange, Term Loan etc.

z Recent judgements under Indirect tax

z Important provisions of DTAA

z Taxation for Non Resident Indian, FATCAprovisions, FEMA Compliance

z Withholding of taxes u/s 195 on foreignremittances

z Role of Technology at work, Email and calendarmanagement, use of google

z Professional opportunities to CA wrt CSR

Workshop / Study groupz FEMAz GSTz Ind-AS

CAPITAL MARKET COMMITTEEz Two Days Technical Course for members

z Meeting for Members / Group Discussions

z Budget Program for Public

z Two Days RRC

“There is a stubbornness about me that never can bear to be frightened at the will of others.My courage always rises at every attempt to intimidate me.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

8

MEMBERS IN INDUSTRY & YOUTHCOMMITTEE PROGRAMMEz River Rafting at Kolad

z Movie Pre-Release Screening

z Members in Industry Meet

z Car Treasure hunt

z Youth RRC with Skill Development and FurtureOriented Topics

z Technical Session shall be conductedby Study Circle Committee & Supported byY & MI

z Mission 1500 Members

STUDENTS COMMITTEEz Study Circle for Students

E-filing of Income Tax ReturnsE-filing of MVAT ReturnsImportant clauses of Tax Auditors ReportRoC E-filingE-filing TDSVAT Audits

z Orientation Programme for newly joined Articles

z Student RRC/NRRC

z Seminar - How to Prepare for CA Exams ?

z Student Education Assistance

z Membership Drive for Student

PUBLICATION, REPRESENTATION &PR COMMITTEEz Cofee Table Book of Cvoca

z Representation before Government on GSTDraft law.

z Publication on GST and on any other topic.

z Budget Booklet

z FAQ'S on Various Issues for General Public inPatrika/ Pagdandi / Magazines

MEMBERSHIP AND RECREATIONCOMMITTEE

z Mega Membership Drive for enrolling newmembers.

z 3 day / 2 night Picnic for member at Saputara

z One Day picnic for new members in December

z Annual Sports in January 2017

WEBSITE & IT COMMITTEE

Website Related

z A new URL to be taken for our website. We havealready bought 2 URL's "www.cvoca.org" and"www.cvoca.in"

z To be ready with the content of Wesbite within 2months which can be given to web developer

z Check out options for another website provider.Not comfortable with the service of the existingWeb service provider

z Database of CVOCA Members and their familyand the area of expertise to be accessible onneed basis from website

z Creating event on Facebook and CVOCAwebsite including the payment gateway onCVOCA website for E-receipts

z Uploading of Powerpoint Presentations ofPublic Programs on the wesbite with thepermission of Speaker

z Website access ID and Password to be mappedwith Mobile number and Email ID for one timepassword.

Other IT/ Social Media Related

z Keeping only 1 Facebook Group of CVOCA andto eliminate all the other groups.

z Work on a detailed page on Wikipedia aboutCVOCA on approval basis

z A calender of CVOCA activities to be madewhich will get automatically merged with Googlecalender. Initially to be tried for 1 month withinthe Committee members

z Uploading the Video Recording on Youtubeunder CVOCA channel of Public Programs andStudy Circle Seminars.

z Creation of CVOCA Membership Loyalty Cards.

z Website Committee or Study Circle Committeecan keep workshops/ training programs on MSOffice, Effective use of Social Media, MobileApps.

“Don't be satisfied with stories, how things have gone with others. Unfold your own myth.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

9

IntroductionTransfer pricing provisions were introduced in Indiain the Finance Bill 2001. Since then the transferpricing assessments have been a talk of the town forthe difficulties faced by assesses and various positionsadopted by the Revenue during the course ofassessment proceedings. A typical transfer pricingassessment deals with the Revenue determining thearm’s length price (“ALP”) of the transactions beinginternational transaction as per Section 92B of theIncome-tax Act, 1961 (“the Act”) and / or specifieddomestic transaction as per Section 92BA of the Act.The arm’s length price is determined in accordancewith the detailed functional, asset and risk analysisand adopting the most appropriate method out of thesix specified methods.

The arm’s length value of the transactions coveredunder the transfer pricing regulationscan, as per theprovisions of the Act, be determined by the assessingofficer (“AO”) or the said AO can make a reference tothe experts called as transfer pricing officers (“TPO”).The AO and TPO form the first level of theassessment proceedings under the Indian transferpricing regulations while the Dispute ResolutionPanel (“DRP”) apart from the Commissioner Appeals(“CIT(A)”)forms the alternative first level of appellateproceedings.

The transfer pricing assessment ideally is a mixtureof economics and taxation wherein the TPOs areexpected to understand the revalent industryscenario before determining the Arm’s Length Price(“ALP”) of the international transaction(s) / specifieddomestic transaction(s) (“SDT”) as case may be. Adetailed summary on the assessment proceedings isprovided in the ensuing paragraphs.

Assessment before the AO:Section 92C(3) of the Act bestows the AO with thepower to determine the ALP of the international anddomestic transactions undertaken by the assesseeduring the year under review. The Central Board ofDirect Taxes (“CBDT”) lays down the criteria andprocedure for manual selection of the returns/casesfor scrutiny for transfer pricing matters. The CBDThas been issuing instructions to the AOs at regularintervals guiding them on the process of selecting thecases and making reference to the TPOs to determine

TRANSFER PRICING ASSESSMENTS– A BASIC OVERVIEW

Contributed by :CA Virav Dedhiaa member of the association

he can be reached [email protected]

the ALP1. The CBDT has moved from dropping thethreshold limit for selection of the cases for transferpricing scrutiny to adopting a risk based approach.Apart from these, the cases involving an addition inthe past assessment year on account of transferpricing or proceedings pending before any appellateauthority are also selected for the purpose of transferpricing assessment.

Accordingly, the AO makes a reference to the TPOunder Section 92CA of the Act after providing anopportunity of being heard to the assessee for makingsuch a reference. On the basis of various judicialprecedents, it is understood that making a referenceto the TPO under the said Section as read with theinstructions of the CBDT is mandatory in naturerather than optional (as may be understood from thepure reading of the Section 92CA of the Act).

The TPO during the course of assessmentproceedings may call for various documents,information, supporting calculations, etc. Thesedocuments primarily comprise of the documents andinformation as maintained by the assessee inaccordance with the provisions of Rule 10D of theIncome-tax Rules, 1962 (“the Rules”). However, theTPO may call for certain additional documentsduring the course of assessment proceedings as hemay deem required to determine the ALP of thetransaction. Further, based on practical experience, itis noted that the TPOs to determine the apt ALP, mayseek information under the provisions of Section133(6) of the Act from independent third partycompanies who are engaged in the similar line ofbusiness as that of the assessee. In such cases, if theTPO wishes to place its reliance on the saidinformation the same must then be shared with theassessee by making available a copy of the saidinformation to the assessee for its reference andconsequently an opportunity of being heard must beprovided to the assessee on such information.

Further, during the course of assessment, the TPOcan suo motto take cognizance of the transaction notreported by the assessee or not referred by the AOto determine the ALP as per Section 92CA (2A)and (2B).1 Instruction no. 03/2016 dated 10 March 2016 which has replaced

the Instruction no. 15/2015 dated October 2015.

“I care for myself. The more solitary, the more friendless, the more unsustainedI am, the more I will respect myself.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

10

The TPO, based on the various information,documents and calculations gathered during thecourse of assessment proceedings, will issue an orderunder Section 92CA(3) determining the ALP. It is tobe noted that the time limit to pass an order as perSection 92CA(3A) is 60 days prior to the date oflimitation referred to in Section 153 of the Act.

The AO, before making an adjustment (if any), basedon such order will provide an opportunity of beingheard to the assessee. The assessee may submit itsreply before the AO; the AO may consider the replyor may proceed with the adjustment provided by theTPO in its order.

The AO, in case where it is making an adjustment oran addition to the total income wherein transferpricing matter is involved, will have to issue a draftorder to the assessee as per the provisions of Section144C of the Act. The Draft Order can be acceptable orunacceptable to the assessee. In case the variationsmade in the draft order are acceptable to the assessee,he/she can file his acceptance to the Draft Order withthe AO within thirty days of the receipt of the DraftOrder. If no acceptance is filed within thirty days, theAO completes the assessment on the basis of the DraftOrder and passes the assessment order, within onemonth from the end of the month, in which, theacceptance is received or the period of filing ofobjections expires.

Assessment Procedure before the DRP:The DRP under the Act is an Alternative DisputeResolution (“ADR”) mechanism for resolving thedisputes relating to Transfer Pricing. Section 144C ofthe Act governs the provisions relating to DRP anddefines DRP as a collegium comprising of threeCommissioners of Income Tax constituted by theCBDT for this purpose. As stated, Section 144C comesinto picture when the AO proposes to make anyvariation in the income or loss stated in the returnfiled by the assessee and such variation is prejudicialto the interest of the assessee and the AO forwards adraft of the proposed assessment order to the assesseein order to invite his acceptance or objections to thesame. An assessee under Section 144C refers to aForeign Company and/or any person in where theAO proposes to make any variation in the returnedincome or loss as a consequence of the order passed bythe Transfer Pricing Officer under Sub Section (3) ofSection 92CA of the Act.

Section 144C was inserted in the Act by the FinanceAct, 2009 and came into effect from 1st October,2009. The DRP was formed with a view to provide

speedy and appropriate directions to the assesses atthe first level of appeal itself. Thus, the DRP has tocomplete the hearing and give its final Directionswithin a period of 9 months from the end of themonth in which the draft order was served to theassessee.

Prior to the formation of DRP, the assessee had toapproach the CIT (A) against the Assessment Orderif the assessee wanted to raise objections against theAssessment Order. The CIT(A) does not have anyspecified time limits to complete the assessment,however, CIT(A) may dispose of the appeal within aperiod of 1-2 years from the end of the financial yearin which appeal was filed.

After receiving Objections in Form 35A, the DRP goesthrough the Draft Order, objections filed by theassessee, the evidences furnished by the assessee inpaperbook; report, if any, of the Assessing Officer,Valuation Officer or Transfer Pricing Officer or anyother authority; records relating to the draft order;evidence collected by, or caused to be collected by, it;and result of any enquiry made by, or caused to bemade by, it and issue such directions, as it thinks fit,for the guidance of the AO to enable him to completethe assessment.

The DRP has the powers to confirm, reduce orenhance the variations proposed in the draft order,however, it shall not set aside any proposed variationor issue any direction for the guidance of the AO forfurther enquiry and passing of the assessment order.It is pertinent to note that if the members of the DRPdiffer in opinion on any point, the point shall bedecided according to the opinion of the majority of themembers.

The Directions to the AO will be given only after theassessee and the AO have been given an opportunityto present their case. After receiving the Directions inthe nature of guidance from the DRP, the AO shall,in conformity with the directions, complete theassessment without providing any furtheropportunity of being heard to the assessee, withinone month from the end of the month in which suchdirection is received.

The Directions given by DRP are binding on the AO,however, the said Directions can be challenged by theassessee before the Income Tax Appellate Tribunal(“ITAT”), being the second level of appeal andconsequently before the High Court (“HC”) andSupreme Court (“SC”).Presently there are 10 DRP inIndia having Jurisdiction over different States andTerritories.

“I'd rather die my way than live yours.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

11

Graphically the process of the appeal can be represented as under for easy reference:

Abeyance of tax demand:Under the CIT(A) route, there is no provision of automatic stay of demand as an appeal is filed only after theAO issues the final assessment order. Thus the assessee is required pay the tax demand before appeal. Theassessee may file a stay application with the AO seeking a stay of demand. CBDT via its instruction has clarifiedthat the quantum of stay would depend on the discretion of the AO.

With the objective of streamlining the process of grant of stay and standardising the quantum of demand, theafore said instruction was recently revised2. The said instruction provides that where the demand is disputedbefore CIT(A), the AO shall grant the stay till the disposal of the appeal by CIT(A) on payment of 15% ofdisputed demand unless the AO is of the view that:

(a) the payment of lump sum amount higher than 15% is warranted, for instance: if an addition on the sameissue has been confirmed by the ITAT in assessee’s own case or jurisdictional HCs or SCs decision is in the favourof revenue or addition is based upon evidence collected in a search or survey operation, etc.)

Or(b) the payment of lump sum amount less than 15% is warranted: for e.g. if an addition on the same issue hasbeen deleted by the ITAT or judgment has been passed by the jurisdictional HC or SC is in the favour of theassessee etc.

The said instruction does not provide the exhaustive list of cases which would fall in exceptions to the mandatedlimit of stay of demand.

If the AO grants a stay of 15% of disputed demand, the aggrieved assessee may approach the jurisdictionaladministrative Principal CIT/CIT for review of AO’s decision.

In a scenario where the AO proposes to vary the quantum of payment of demand such variation would berequired to be supported by detailed reasoning. Furthermore, where the assessee applies for payment of demandless than 15%, the burden of convincing the AO would vest on the assessee.

2 Instruction no. 1914 dated 21.03.1996 being revised through an office memorandum dated 29.02.2016

“I do not think, sir, you have any right to command me, merely because you are older than I, or because you have seen more ofthe world than I have; your claim to superiority depends on the use you have made of your time and experience.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

12

However, AO’s thorough knowledge of the appeal’ssubject matter before expressing views on thequantum of stay to be granted may reduce theassessee’s burden of demand. For instance, if theappeal involves transfer pricing matter, AO’s opinionofincreasing / decreasing the demand to be paidwould be based solely on TP principles and judicialprecedents. Accordingly, the revised instructionrestricts the discretionary power of the AO to someextent.

Further, the appellate powers of the CIT(A) alsoinclude the power to grant stay in relation to theappealpending before it. However, this is not asubstitute to the powers of the AO. CIT(A) is notbound by theafore said instruction and therefore, thequantum of stay would be dependent on CIT(A)’sjudgement.

Issues not raised before lower level:The assessee can raise any matter before the DRPirrespective of the fact that such an issue was notraised before the AO. In plethora of judgments it hasbeen upheld that though the powers of CIT(A) is co-terminus to the power of the AO, still it has nojurisdiction over the matters, which were not raisedor processed before the AO.

Conclusion:Tax litigation is a scourge for a tax friendly regimeand creates an environment of distrust in addition to

increasing the compliance cost of the assessees andadministrative cost for the Government. It is one ofthe road blocks in the growth of the economy as thisaffects the investment climate in the country. TheGovernment has acknowledged that the existinglitigation process is time consuming and neededrestructuring.

In a nutshell, aassessee looking for a fast track routeof appealing before the ITAT may opt for the DRProute. The CIT(A) route, though a time consumingprocess, may provide a better opportunity of beingheard. Also, the assessee might get the benefit of therevised instruction on stay matter. Needless to say,one needs to properly weigh all factors beforeselecting a particular litigation path, i.e. CIT(A) orDRP as the same will bevery fact specific.

In the current year, the Government has taken stepfor reducing litigation by taking away the power ofthe AO to appeal against the directions of the DRP.This would provide assurance to the assessee inrelation to the relief (if any) granted by the DRP.Furthermore, the revised instruction in relation tostay of demand may acts as an added advantage forthe assessee’s to opt for CIT(A) route. However, themanner of implementation of this instruction by theAO would have significant impact on assessee’sdecision.Note:- Views expressed are personal and readers mayseek specific professional advice based on their facts.

FOR ATTENTION OF MEMBERS/SUBSCRIBERS❑ Members are requested to come forward and contribute

their articles in CVO CA’s News & Views, the mouthpiece ofour Association. Best Article contributed by new comershall be awarded with a special prize.

❑ While sending Articles for News & Views, pleaseconfirm that the same are not published/not given forpublishing elsewhere. No correspondence shall bemade in respect of Art ic les not accepted forpublication; nor will they be sent back.

❑ The views and opinion expressed or implied in theNews and Views are those of the authors and do notnecessarily reflects those of the association. Theopinion expressed herein should not be construed aslegal or professional advice. Neither the Associationnor the authors/contributors are responsible in anymanner for any personal or professional liability arisingdue to the decisions taken by readers on the basis ofthese views. The association is also not in any wayresponsible for the result of any action taken on thebasis of the advertisement published in the journal.

❑ This is “YOUR” magazine. Please give your feedback/suggestions etc. Kindly intimate change of your

address by sending the necessary intimation to theAssociations’ Office.

❑ Non receipt of News & Views may be intimated to :CA Rahul Nagda - 9821552234Email Id - [email protected]

❑ Rates for Advertisements in CVO CA’s News & Views(per insertion) are as under:Inside Full Page (Single color printing) Rs. 8,000/-Inside Half Page (Single color printing) Rs. 5,000/-Inside Quar ter Page (Single color ptg.) Rs. 3,000/-(More than one insertion at time entitles for discount)Classified Advertisements rate Rs. 400/- for 100 words.

❑ CVO CA's News & View Subscription charges for 1 yearRs. 500 & 3 years Rs. 1200 for Non members of theassociation.

❑ Members are requested to register themselves to CVOCA Yahoo Group by sending E-mail to “cvoca-subscribe@ yahoogroups.co.in” to quickly receive thelatest updates and communicat ion from theAssociation.

“Freedom (n.): To ask nothing. To expect nothing. To depend on nothing.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

13

INTRODUCTIONWhile there may be no single universally accepteddefinition of Corporate Social Responsibility (CSR),each definition that currently exists underpins theimpact that businesses have on society at large andthe societal expectations of them. Although the rootsof CSR lie in philanthropic activities (such asdonations, charity, relief work, etc.) of corporations,globally, the concept of CSR has evolved and nowencompasses all related concepts such as triple bottomline, corporate citizenship, philanthropy, strategicphilanthropy, shared value, corporate sustainabilityand business responsibility.

CSR in India has traditionally been seen as aphilanthropic activity. And in keeping with theIndian tradition, it was an activity that wasperformed but not deliberated. As a result, there islimited documentation on specific activities related tothis concept. However, what was clearly evident thatmuch of this had a national character encapsulatedwithin it, whether it was endowing institutions toactively participating in India’s freedom movement,and embedded in the idea of trusteeship.

As some observers have pointed out, the practice ofCSR in India still remains within the philanthropicspace, but has moved from institutional building(educational, research and cultural) to communitydevelopment through various projects. Also, withglobal influences and with communities becomingmore active and demanding, there appears to be adiscernible trend, that while CSR remains largelyrestricted to community development, it is gettingmore strategic in nature (that is, getting linked withbusiness) than philanthropic, and a large number ofcompanies are reporting the activities they areundertaking in this space in their official websites,annual reports, sustainability reports and evenpublishing CSR reports.

India is the first country in the world to have aregulatory framework for CSR by law. The

Companies Act, 2013 has introduced the idea of CSR.Schedule VII of the Act, which lists out the CSRactivities, suggests communities to be the focal point.On the other hand, by discussing a company’srelationship to its stakeholders and integrating CSRinto its core operations, the rules suggest that CSRneeds to go beyond communities and beyond theconcept of philanthropy.

APPLICABILITY & COMPLIANCEREQUIREMENTSEvery Company including its holding or subsidiary,and a foreign company (as defined under section2(42) of the Act) having its branch office or projectoffice in India, which fulfils the criteria specifiedunder section 135(1) of the Act shall comply with theprovisions of section 135 and the Rules.

Criteria given under section 135(1) of the Act, whichprovides, during any financial year, a company iseither having:-z Net worth of Rs. 500 Crores or more; orz Turnover of Rs. 1,000 Crores or more; orz Net profit of Rs. 5 Crores or more.

Every company which falls under the criteriamentioned under section 135(1) shall:-z Constitute a Corporate Social Responsibility

Committee of the Board (CSR Committee);z Formulate Corporate Social Responsibility Policy

(CSR Policy);z Spend, in every financial year, at least two

percent of the ‘Average Net Profits’ of thecompany made during the three immediatelypreceding financial years, in pursuance of its CSRPolicy;

z Include in Board’s Report (pertaining to financialyear commencing on or after 1st April 2014) anAnnual Report on CSR, containing particulars

CORPORATE SOCIAL RESPONSIBILITY- AN INSIGHT

Contributed by :CS Bhavik Gala(a member of the association)

he can be reached [email protected]

DISCLAIMER:This write up is the personal property of the author to this article. If this write-up is circulated, content of thisdisclaimer and credit to CS Bhavik Gala shall be retained.The content of this write up is purely academic and is intended to provide a general guide to the subject matter andnot intended to be a professional advice and should not be relied upon for real life facts and the views are ofpersonal opinion in nature. Specialist advice should be sought about your specific circumstances, if any.

“I am not an angel,' I asserted; 'and I will not be one till I die: I will be myself. Mr. Rochester, you must neither expect nor exactanything celestial of me - for you will not get it, any more than I shall get it of you: which I do not at all anticipate.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

14

specified under the Rules (In case of foreigncompany, the balance sheet shall contain anannexure regarding report on CSR) .

z Display the contents of CSR Policy in Board’sReport and also place on company’s website, ifany.

The company shall give preference to the local areaand areas around which it operates, for spending theamount earmarked for the CSR Activities.

CSR Committee of Board shall consist of three or moredirectors, out of which at least one director shall be anindependent director. However, there are followingexemptions:z An unlisted company or private company [not

required to appoint an independent directorpursuant to section 149(4)] shall have CSRCommittee without such director.

z A private company having only two directorsshall constitute CSR Committee with two suchdirectors.

z CSR Committee of a foreign company shallcomprise of at least two persons of which one shallbe a person authorised to accept any notice orother documents from Registrar and anotherperson nominated by the foreign company.

CSR: PLANNING AND STRATEGISING

Clause 135 of the Companies Act, 2013 requires aCSR committee to be constituted by the board ofdirectors. This is an excellent starting point for anycompany new to CSR.

Functions of Committee:

z Formulate and recommend to the Board CSRPolicy indicating activities to be undertaken (asspecified under Schedule VII to the Act).

z Recommend amount of expenditure to beincurred on CSR projects, programs or activities(CSR Activity).

z Monitor CSR Policy from time to time.

z To ensure that all the income accrued to thecompany by way of CSR activities is credited backto the CSR corpus.

For effective implementation, the CSR committeemust also oversee the systematic development of a setof processes and guidelines for CSR to deliver itsproposed value to the company, including:

z one-time processes such as developing the CSRstrategy and operationalizing the institutionalmechanism

z repetitive processes such as the annual CSRpolicy, due diligence of the implementationpartner, project development, project approval,contracting, budgeting and payments,monitoring, impact measurement and reportingand communication

CSR Policy shall inter alia, include the following:

z CSR Activity which company plans to undertakespecifying modalities of execution andimplementation schedules

z Monitoring process for CSR Activities

z Declaration that any surplus arising out of theCSR Activity shall not form part of the businessprofit of the Company

Provided that, (i) CSR Activity does not include theactivities undertaken in pursuance of normal courseof business of company; and (ii) the Board shallensure that CSR Activities are related to the activitiesincluded in Schedule VII to the Act.

A set of such enabling processes, their inter-relationships and the sequence in which they need tobe developed have been identified below:

PERMISSIBLE CSR ACTIVITIES AS PERSCHEDULE VII OF THE ACT:

CSR Activities would mean any one or more of theareas, as specified under Schedule VII to the Act,which are to be pursued/undertaken by theCompany.

The companies may pursue CSR Activity by takinginto account the following:

a) the activities undertaken in pursuance of normalcourse of business shall not be treated as CSRActivity.

b) the company may undertake CSR Activitiesthrough a registered trust or society or company,established by the company or its holding orsubsidiary or associate company. Provided that, iftrust, society or company is not established bycompany or its holding or subsidiary or associatecompany, it shall have an established track recordof three years in undertaking similar programs orprojects.

To find yourself, think for yourself.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

15

c) the company shall specify project or programs tobe undertaken through said entities and also themodalities of utilization of funds and have systemof monitoring and reporting the same.

d) collaborate with other companies for undertakingCSR Activities in such manner that the CSRCommittee of respective companies can reportseparately on CSR Activities.

e) the programs or activities undertaken in Indiaonly shall amount to CSR expenditure.

f) the projects, programs or activities that benefitonly the employees of the company and theirfamilies shall not be considered CSR Activity.

g) contribution of any amount directly or indirectlyto any political party shall not be considered asCSR Activity.

h) companies may build CSR capacities of their ownpersonnel as well as those of their implementingagencies through Institutions with establishedtrack records of at least three financial years butsuch expenditure shall not exceed five percent oftotal CSR expenditure in one financial year.

i) In case of foreign owned and controlledcompanies, CSR contribution can be made only tothose trust/NGO’s, etc. who hold FCRA license. Italso pertinent to note that such restriction hasbeen proposed to be removed retrospectively inthe Union Budget of 2016 but we need to waitand watch till the same is being effectivelynotified and comply with the currently effectiveprovisions.

CERTAIN CLARIFICATIONS ONREGULATORY FRAMEWORK OF CSR1. It is further clarified that CSR activities should be

undertaken by the companies in project/programme mode [as referred in Rule 4 (1) ofCompanies CSR Rules, 2014]. One-off eventssuch as marathons/ awards/ charitablecontribution/ advertisement/ sponsorships of TVprogrammes etc. would not be qualified as part ofCSR expenditure.

2. Expenses incurred by companies for thefulfilment of any Act/ Statute of regulations (suchas Labour Laws, Land Acquisition Act etc.) wouldnot count as CSR expenditure under theCompanies Act.

3. Salaries paid by the companies to regular CSRstaff as well as to volunteers of the companies (inproportion to company’s time/hours spentspecifically on CSR) can be factored into CSRproject cost as part of the CSR expenditure.

4. “Any financial year” referred under Sub-Section(1) of Section 135 of the Act read with Rule 3(2)of Companies CSR Rule, 2014, implies ‘any of thethree preceding financial years’.

5. Expenditure incurred by Foreign HoldingCompany for CSR activities in India will qualifyas CSR spend of the Indian subsidiary if, the CSRexpenditures are routed through Indiansubsidiaries and if the Indian subsidiary isrequired to do so as per section 135 of the Act.

6. ‘Registered Trust’ (as referred in Rule 4(2) of theCompanies CSR Rules, 2014) would includeTrusts registered under Income Tax Act 1956, forthose States where registration of Trust is notmandatory.

7. Contribution to Corpus of a Trust/ society/ section8 companies etc. will qualify as CSR expenditureas long as (a) the Trust/ society/ section 8companies etc. is created exclusively forundertaking CSR activities or (b) where thecorpus is created exclusively for a purpose directlyrelatable to a subject covered in Schedule VII ofthe Act.

8. There is no specific exemption given to section 8companies with regard to applicability of section135, hence section 8 companies are required tofollow CSR provisions in case such companies arefalling in the criteria specified under Section135(1) and the same has been clarified by MCA.

9. It has MCA has clarified that amount spent by co.towards CSR cannot be claimed as ‘businessexpenditure’;

10. With respect to ‘average net profit’ criteria u/s135(5), MCA clarifies that computation of netprofit is as per section 198, which is primarily‘profit before tax’;

11. MCA states that no specific tax exemptions thathas been extended to CSR expenditure per se,however clarifies that spending on certainactivities prescribed in Schedule VII alreadyenjoy exemptions under different provisions ofIncome Tax Act;

12. Clarifies on activities which would not qualify asCSR,which includes: (i) Projects only foremployees’ benefit, (ii) one-off events, (iii)expenses incurred for compliance of any otherAct/Regulation, (iv) Contribution to politicalparty, etc.;

13. MCA States that if any excess CSR amount spent,same cannot be carried forward to subsequentyears;

“Marriage is a fine institution, but I'm not ready for an institution.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

16

TAX BENEFITS FOR EXPENDITURE ON CSRTax benefits for expenditure on CSR Firms spending money on Corporate Social Responsibility (CSR), which hasbeen made mandatory under the new Companies Act, have more reasons to cheer.

Though CSR provisions do not offer any great tax savings, companies can claim deductions specifically allowedunder Sections 30 to 36 of the Income Tax (IT) Act, 1961.

1. Section 30 of the IT Act allows deductions against expenditure incurred on repairs and insurance in respectof machinery, plant and furniture used for CSR activities.

2. Rent, rates, taxes and repairs incurred on buildings or other assets taken on lease earmarked for CSRactivity would also qualify for deductions.

3. Deduction towards depreciation on assets used for CSR purposes can be claimed.

4. Funds spent on Skill Development projects gives the assesse the benefit of claiming 150% deduction intheir books.

5. Installing water filter in schools at various places allows to claim expenditure on repairs, maintenance,insurance, besides deduction towards depreciation if the asset is shown in its books of account.

These are enabling provisions to incentivise companies to spend on welfare activities.

The following chart tabulates the activities as prescribed under Schedule VII to the 2013 Act and the allowabilityof expenditure incurred on the said activities under the Act:

No. Specific CSR Activities referred Expenditure allowed under the relevantunder Schedule VII to the 2013 Act provisions of the Income-tax Act, 1961

1 Activities concerning basic necessities of life - Section 35AC read with Rule 11K(i)(f).- Eradication of poverty, hunger and malnutrition - Section 35AC r/w Rules11k(i)(a),(f),(j)- Promoting Sanitation and health care andmakingavailable safe drinking water

2 Activities concerning Education- Promoting Education, including special education Section 35AC r/w11K(i)(c),(i),(o),(p),(s)and employment enhancing vocational skills especially - Section 35AC r/wRules 11K(i)(j),(s)among children, women and elderly and thedifferently abled- Livelihood enhancement programs

3 Activities addressing inequality and gender Section 35AC r.w. Rule11K(i)(n),(i)discrimination- Promoting gender equality of the 1962Rules- Empowering women- Setting up of homes andhostels for women and orphans- Setting up old age homes, day care centre

4 Activities concerning Care for environment Section 35AC r/w Rules11K(i)(d),(h),(l),(q),(r)- Ensuring environmental sustainability and ecologicalbalance- Preservation of flora and fauna, animalwelfare, agro forestry- Conservation of naturalresources and maintainingquality of soil, airand water

5 Activities concerning protection of National Heritage, Section 35AC r/w Rule11KArt and Culture- Protection of national heritage, artand culture including restoration of building andsites of historical importance and works of art- Setting up public libraries- Promotion of traditionalarts and handicrafts and itsDevelopment

“Then, one stupid person, no different from any other stupid person, wanders into your stupid life...you give them a piece of you.They don't ask for it. They do something dumb one day like kiss you or smile at you, and then your life isn't your own anymore.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

17

6 Activities concerning benefit to Armed Forces, Section 80G(2)(a)(i)and 80G(2)(a)(iii)(h)(c)veterans, war widows and their dependants- Measures for the benefit of armed forces, veterans,war widows and their dependents

7 Activities concerning Sports- Training to promote Section 35AC r/w Rule11K(i)(g)rural sports, nationally recognised sports,Paralympics sports andOlympic sports

8 Activities concerning national relief and welfare - Section 80G(2)(a)(iiia)of Economicallybackward class of Society - Section 35AC r/wRules 11K(i)(b),(c)- Contribution to PM National relief fund or any and 11K(ii).other fund- Relief and welfare of the SchedulesCasts, SchedulesTribes/Other backward castes,minorities and women

9 Activities concerning Technologyincubators Section 35(2AA)/80G(2)(iihi)- Contributions or funds provided to technologyincubators located within academicinstitutionswhich are approved by Central Government

10 Activities concerning Rural Development (Projects) Section 35AC/35CCA

Explanation II to sub-section (1) of Section 37 of Income Tax Act, 1961 says that any expenditure incurred byan assessee on the activities relating to corporate social responsibility referred to under Section 135 of theCompanies Act, 2013 shall not be deemed to be an expenditure incurred by the assesse for the purposes of thebusiness or profession. This is effective from 1st April, 2015 and accordingly applies to the assessment year (AY)2015-16 and subsequent years. In this scenario, resulting percentage spent by companies on CSR activitieswould be higher than the required 2% of the average three years’ net profits. It is understood that the aggregatecorporate taxation is 33.9% (taking a surcharge of 10%). Since the CSR spend is not included while calculatingthe net profit, the actual CSR spending percentage can be derived from the following formula: 2% / 1 – 33.9%.Thus the actual CSR spend of companies come to about 3.02% of the net profits, which is much higher thanthe required 2%.

It has been perceived by many industrialists that 2% of average net profit of the three preceding financial yearsis a huge spending for companies apart from other mandatory legal obligations. Corporates are already sharingthe 30-35% of its net profit with government by corporate taxes as compared to the global average of 24%, sothe government should not be diffident for allowing tax sops to CSR spending. If the present tax treatment ofCSR continues, then it results in companies only inclined to give funds to those organizations under sections 35or 80 where they get maximum tax benefit.

CONSEQUENCES OF DEFAULT IN CASE PRESCRIBED COMPANIES FAIL TO SPEND THEMANDATORY CSR AMOUNT AS PER THE ACT

The concept of CSR is based on the principle ‘comply or explain’. Section 135 of the Act does not lay down anypenal provisions in case a company fails to spend the desired amount. Second proviso to sub-section (5) of section135 provides that if the company fails to spend such amount, the Board shall in its report specify the reasonsfor not spending the amount.

However, sub-section 8 of section 134 relating to Board’s Report provides that in case the company contravenesthe provisions of the section i.e. in case it does not disclose the reasons for not spending in the Board’s report,the company shall be punishable with fine which shall not be less than fifty thousand rupees but which mayextend to twenty- five lakh rupees and every officer of the company who is in default shall be punishable withimprisonment for a term which may extend to three years or with fine which shall not be less than fifty thousandrupees but which may extend to five lakh rupees, or with both.

“The greatest thing in the world is to know how to belong to oneself.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

18

The CSR provisions were notified with clarity aroundthe regulations that govern them, but thestakeholders continue to threadbare discussions on itsapplicability, calculation of net profit and on theamount of CSR expenditure. What makes CSRprovisions so significant amongst many other criticalprovisions of the Act? There is no one answer to thisquestion. There are wide-ranging responses given bystakeholders and experts. Few believe that, itcontributes to the overall growth of the country andfew categorise it as a ‘return on the investment’—which may be in terms of land, manpower, resources(tangible or otherwise) used by the companiesregistered in India. However, the peculiarity of theprovisions of section 135 are such that the Actmandates certain class of companies to comply withthe provisions of the section, and on the other handpermits the companies violating the provisions toprovide necessary explanations in its Boards report—making it a comply or explain concept. Theexplanations shield the company from the penalconsequences, i.e., the defaulting companies andofficers of the company need not pay any penalty andwill not be charged for the default. Interestingly, inthe recent past the ministry of corporate affairs(MCA) seems to have taken the CSR mantra veryseriously and has directed all the Registrar ofCompanies (RoC) to send show cause notices, in theirrespective jurisdiction to those companies who fallunder the ambit of the provisions of the section of thelaw.

By virtue of section 206 of the law—power to call forinformation, inspect the books and conduct inquiries,the RoCs have been sending out notices to thecompanies seeking information on the (i) annualreport for the financial year FY15; (ii) informationpertaining to net profits, average net profits, of thethree immediate preceding financial years; (iii) 2% ofthe prescribed CSR expenditure; (iv) completeinformation on the CSR expenditure, if any; (v)further details for not meeting the CSR requirementsor on explanations provided in the Board’s report.

With the enthusiasm shown by the RoCs under thedirections of the MCA, one can infer that thecompanies may expect to receive notices even for thefinancial year FY16. As there are no stringent penalprovisions provided for non-compliance of section 135,numerous companies have not complied withprovisions and the rules framed thereunder and havebeen claiming defence by providing necessaryexplanations in the Board’s report for not meeting theCSR requirements.

In view of such non-compliances, it is clear that theRoCs have been very enthusiastic in having rightamount of checks and balances in CSR compliance bythe companies who fall under the ambit of CSR andalso to create a distress on the companies who fail tocomply and take advantage of the shield of providingnecessary explanations in the Board’s report.

On a separate note, there may be a possibility that,MCA may consider CSR compliance for a period ofthree years, i.e., from the date of notification of theCSR provisions, thereafter may decide to amend theprovisions and the rules made thereunder, so as to fitin the necessary penal provisions for the companiesand its officers for the non-compliance or partialcompliance of section 135 of the Act. In which case, adiligent compliance of the CSR provisions, will replacethe explanations in the Board’s report.

CONCLUSIONThe business sector is faced with new responsibilities,new challenges and new opportunities to be exploredin order to make poverty and squalor a thing of thepast. Philanthropy among businesses has alwaysexisted. In India, all leading corporate houses areinvolved in programs covering areas like education,health, livelihood creation, skill development, andempowerment of weaker sections of society. CSR is thecontinuing commitment by business houses to behaveethically and contribute to economic developmentwhile improving the quality of life of the workforce.

Though there are published analysis which revealsthat there is a positive relationship between CSR andfinancial performance and the descriptive measuresshows that Corporate social expenditure dependsupon the financial performance of the Company butat the same time, we can conclude that some of the topIndian companies are not spending the prescribedamount on part of their social responsibilities. 5 Out of10 companies spent lesser amount on social projectsthan recommended, 3 companies spent more than therecommended budget. The country’s top 75 companiesspent more than Rs 4,000 crore towards corporatesocial responsibility in the last fiscal, i.e. the first yearafter the government mandated bigger companies togive away a part of their profits for social work.

Big CSR spenders include Reliance Industries with Rs760 crore, ONGC with Rs 495 crore, Infosys with Rs239 crore, NTPC with Rs 205 crore and TCS with Rs220 crore. Wipro, ITC, Mahindra & Mahindra andHindustan Unilever are among the 28 companies thatmet the mandatory CSR spending norm of at least 2%

Continued on page no. 30

“I had rather hear my dog bark at a crow, than a man swear he loves me.”

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

19

Introduction to Income Computation andDisclosure Standards

Income Computation and Disclosure Standardsnotified for computation of taxable income

On 31st March 2015, the Central Board of DirectTaxes (“CBDT”) notified the Income Computationand Disclosure. Standards (“ICDSs”) which will comeinto effect from 1 April 2016 and shall accordinglyapply for assessment year 2017-18 onwards.

A Roadmap of ICDS – A look at the journey

A draft of 14 Tax Accounting Standards were firstissued in August 2012. However, these were revisedfurther and 12draft ICDSs were issued in January2015 for public comments. By way of abovenotification, 10 ICDSs were finalised –excluding thestandards on ‘Leases’ and ‘Intangible Assets’. ICDSshave been notified by the Government as per powersgranted under section 145(2) of the Income-tax Act,1961. The notified ICDSs shall supersede the existingaccounting standards notified by the CBDT on 25January 1996(‘existing tax AS’) relating to disclosureof accounting policies and disclosure of prior periodand extraordinary items and changes in accountingpolicies.ICDSs apply to all taxpayers followingaccrual system of accounting for the purpose ofcomputation of income under theheads of ‘Profits andgains of business / profession’ and ‘Income from othersources’. Further, the method of accountingprescribed in ICDSs is mandatory – else, as persection 145(3) of the Act, income can be recomputedby tax officer.

It has been specifically stated in the Preamble to allthe ICDSs that they are only for income computationand not formaintenance of books of account. ThePreamble also mentions that in case of conflictbetween the provisions of the Act andICDS, the Actshall prevail to that extend.

ICDS provides standards in various areas forcomputation of taxable income. In case of conflictsbetween the provisions ofthe Act and ICDS, Actwould prevail. However, in case the Act is silent orambiguous, the interplay between ICDS and existingphilosophy of law needs to be evaluated. Also, while

PRESENTATION ON ICDS ANDIND AS / AS DIFFERENCES

Contributed by :Jekin Dedhiaa student member of theassociation

he can be reached [email protected]

ICDS applies to prospective income computation fortax purposes, it is not clear whether ICDS impactseven existing litigation.The new Indian Accounting Standards (Ind AS) arebeing made mandatory for certain class of companieswith effect from 1April, 2016.Accordingly, differencesbetween ICDS and Ind AS must be mapped bycompanies to assessthe impact on taxable incomeincluding book profits as well as maintenance ofrelevant documentation.

Introduction to IndianAccounting Standards

Recently, the Indian Accounting Standards (“IndAS”) were notified on 16 February 2015 by theMinistry of CorporateAffairs (“MCA”). MCA notifiedthe Companies (Indian Accounting Standards)Rules, 2015 (pending publication inthe Gazette ofIndia) which specify the Ind AS applicable to certainclass of companies and set out the datesofapplicability.

Voluntary adoption

Companies may voluntarily adopt Ind AS forfinancial statements for accounting periodsbeginning on or after 1 April2015, with thecomparatives for the periods ending 31 March 2015or thereafter. Once a company opts to followthe IndAS, it will be required to follow the same for all thesubsequent financial statements.

Mandatory adoption

For the accounting periods beginning on orafter

� 1 April 2016

o Companies whose equity and/or debtsecuritiesare listed or are in the process of listingon anystock exchange in India or outside India(listedcompanies) and having net worth of Rs.500 crores or more.

o Unlisted companies having a net worth of Rs.500crores or more.

o Holding, subsidiary, joint venture orassociatecompanies of the listed and unlistedcompaniescovered above.

“If you truly want to be respected by people you love, you must prove to them that you can survive without them.”

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

20

ICDS and Ind AS Comparison

ICDS Particulars IND AS AS

I Accounting Policies 1 & 8 1

II Valuation of Inventories 2 2

III Construction Contract 11 7

IV Revenue Recognition 18 9

V Tangible Fixed Asset 16 10

VI Effects of changes in foreign exchange rates 21 11

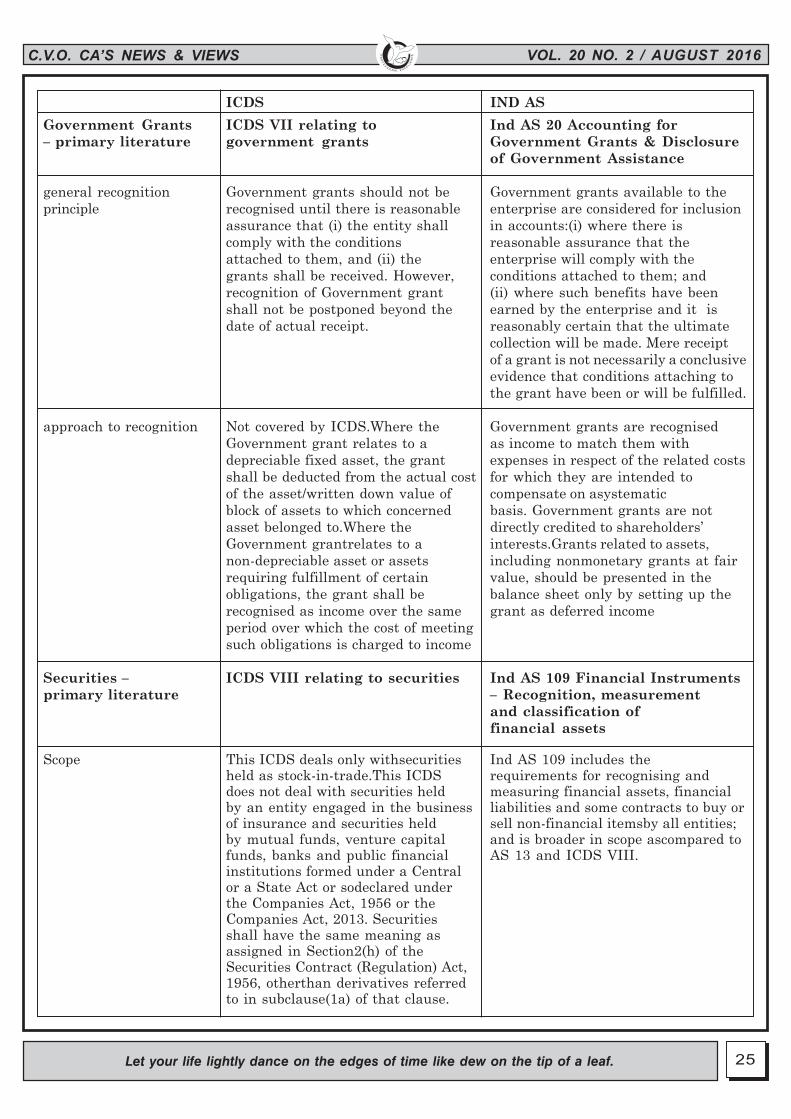

VII Government Grants 20 12

VIII Securities 32 30

IX Borrowing Costs 23 16

X Provisions, contingent liabilities and contingent assets 37 29

The table on the following pages set out some of the key differences between ICDS and IndASICDS IND AS

Accounting Policies, ICDS I relating to Ind AS 1 Presentation of FinancialChanges in accounting policies Statements Ind AS 8 AccountingAccounting Estimates Policies, Changes in Accountingand Errors Estimates and ErrorsChanges in Changes in accounting policy will not Requires retrospective application ofaccounting policies be done unless for a ‘reasonable changes in accounting policies by

cause’. However, ‘reasonable cause’ adjusting the opening balance ofis not defined. each affected component.

Errors Not covered by ICDS Material prior period errors arecorrected retrospectively by restatingthe comparative amounts for priorperiods presented in which the erroroccurred or if the error occurred beforethe earliest period presented, byrestating the opening balance sheet.

Inventories – ICDS II relating to valuationprimary literature of inventories Ind AS 2 Inventories

This Standard shall be applied for Measurement requirements of Ind AS 2valuation of inventories, except: do not apply to inventories held by��Work-in-progress arising under commodity broker-traders who

‘construction contract’ measure their inventories at fair valueWork-in-progress which is dealt less costs to sell and producers ofwith by other ICDS; agricultural and forest products,

� Shares, debentures and other agricultural produce after harvest andfinancial instruments held as minerals and mineral products to thestock-in-trade which are dealt extent that they are measured at netwith by the ICDS relating to realisable value in accordance withsecurities;etc well-established practices in those

industries. The standard also scopes

The laws of science do not distinguish between the past and the future.

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

21

out the biological assets related toagricultural activity and agriculturalproduce at the point of harvest.Changes in fair value less costs to sell/changes in net realisable value arerecognised in profit or loss in the periodof the change.

How to calculate The Cost of inventories of items Requires an entity to use the samecost of inventory. (i) that are not ordinarily cost formula for all inventories having

interchangeable; and a similar nature and use to the entity.(ii) goods or services produced and For inventories with a different

segregated for specific projects nature or use, different cost formulasshall be assigned by specific may be justified. Techniques for theidentification of their individual measurement of cost is similar tocosts. Cost of inventories, other Indian GAAPthan the inventory dealt withabove, shall be assigned by usingthe First-in First-out(FIFO), orweighted average cost formula

Allocation of fixed Allocation of fixed production Allocation of fixed productionproduction overheads overheads is based on normal overheads is based on normal capacity

capacity of production facilities. of production facilities. The actualThe actual level of production level of production may be used, if itshould be used, if it approximates approximates normal capacity.normal capacity.

Revenue from ICDS III relating to construction Ind AS 115 Revenue from ContractsContracts with contracts ICDS IV relating to with Customers Ind AS 109Customers – primary revenue recognition Financial Instrumentsliterature

Applicability ICDS III and ICDS IV are similar to Ind AS 115 applies to contract with aAS 7 and AS 9 respectively. customer and establishes principles on

reporting the nature, amount, timingand uncertainty of revenue and cashflows arising from a contract withcustomer.

What is revenue Revenue is the gross inflow of cash, Revenue is defined as income arisingreceivables or other consideration in the course of an entity’s ordinaryarising in the course of the ordinary activities. Income is defined asactivities from the sale of goods, from increases in economic benefits duringthe rendering of services, and from the accounting period in the form ofthe use by others of resources inflows or enhancements of assets oryielding interest, royalties and decreases of liabilities that result individends. Further, it is specified that an increase in equity, other thanin an agency relationship, the those relating to contributions fromrevenue is the amount of commission equity participants.and not the gross inflow of cash,receivables or other consideration.

ICDS IND AS

Time and tide wait for no man.

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

22

recognition Similar to Indian GAAP however The core principle under Ind AS 115completed service method to is that an entity should recogniserecognise revenue is not permitted revenue to depict the transfer ofunder ICDS IV. Under ICDS III, promised goods or services topercentage of completion method is customers in an amount that reflectsapplicable, except during early stages expects to be entitled in exchange forof a contract when the outcome of those goods or services. To achievethe contract cannot be estimated that core principle, the following stepsreliably. In this case, revenue is are applied: 1) Identify the contract(s)recognised to the extent of costs with a customer. 2) Identify theincurred. This is possible only when performance obligations in theup to 25% of the work is completed contract (account for a ‘distinct’ goodotherwise proportionate method will or service). 3) Determine theapply. Thus, profit recognition has transaction price. 4) Allocate theto start compulsorily once 25% stage transaction price to the performanceis completed. Contract costs are to be obligations in the contract.recognised as an expense in the 5) Recognise revenue when (or as) theperiod in which they are incurred. entity satisfies a performanceExpected loss should be recognised obligationin proportion of work completed.

time value of money Revenue is not adjusted for the Transaction price is adjusted for thetime value. time value of money when a

significant financing component exists.

Property, Plant and ICDS I relating to Ind AS 1 Presentation ofEquipment – primary accounting policies Financial StatementsInd AS 8literature Accounting Policies, Changes in

Accounting Estimatesand Errors

Identification of The tangible fixed asset is anyasset Fixed asset is an asset held with theFixed Assets being land, building,machinery, intention of being used for the purpose

plant or furniture held with the of producing or providing goods orintention of being used for the services and is not held for sale in thepurpose of producing goods or normal course of business. Howeverservices and is not held for sale in an enterprise maydecide to expensethe normal course of business.There an item which could otherwise haveis no option of expensing off of been included as fixed asset, becauseimmaterial assets resulting in onerous the amount of the expenditure is notcompliances and record keeping. material.

Costs to becapitalised Similar to Indian GAAP. However, Directly attributable costs may beexpenses incurred in the interval capitalised only until the asset iswhen the project is ready to “capable of operating in the mannercommence commercial production intended bymanagement”. If an asset isand when it actually commences purchased or constructed and canproduction may also be required to operate in that manner immediately,be capitalised costs incurred whilst the asset is

standing idle may not be capitalised.

Replacement costs Replacement cost of an item ofproperty, plant and equipment isgenerally expensed when incurred.

ICDS IND AS

Money is not gained by losing time.

C.V.O. CA’S NEWS & VIEWS VOL. 20 NO. 2 / AUGUST 2016

23

Only expenditure that increases Replacement cost of an item ofthe future benefits from the property, plant and equipment isexisting asset beyond its capitalised if replacement meets thepreviously assessed standard of recognition criteria. Carrying amountperformance is capitalised. of item sreplaced is derecognised.From financial years commencingon or after 1 April 2015, ScheduleIImandates fixed assets to becomponentised for the purposes ofdepriciation and therefore,theposition will be similar to that underInd AS.

Revaluation Not covered by ICDS. However, If an entity adopts the revaluationunder the Act, income / expense model, revaluations are required to berecognised only on actual realisation. made with sufficient regularity to

ensure that the carrying amount doesnot differ materially from that whichwould be determined using fair valueat the end of the reporting period.

Depreciation Depreciation on a tangible fixed Property, plant and equipment areasset shall be computed in accordance componentised and are depreciatedwith the provisions ofthe Act and separately. There is no concept ofthe Rules thereunder minimum statutory depreciation

under Ind AS.

Foreign Exchange– ICDS VI relating to the effects Ind AS 21 The Effects of Changesprimary literature of changes in foreign in Foreign Exchange Rates

exchange rates Ind AS 109 Financial Instruments

Effects of Changes in “Foreign currency” is a currency other Functional currency is the currency ofForeign Exchange Rates than the reporting currency. the primary economic environment infunctional and "Reporting currency” means Indian which the entity operates. Foreignpresentation Currency currency except for foreign operations currency is a currency other than the

where it shall mean currency of the functional currency.Presentationcountry where the operations are currency is the currency in which thecarried out. financial statements are presented.

Definition of foreign Foreign operation is a branch, by Foreign operation is an entity that isoperation whatever name called, the activities a subsidiary, associate, joint

of which are based or conducted in arrangement or branch of a reportinga country other than India. entity, the activities of which are based

on currency other than those ofthe reporting entity

Conversion at period Non-monetary foreign currency Non-monetary foreign currency itemsend for non-monetary items shall be converted into which are carried in terms of historicalforeign currency items reporting currency by using the cost denominated in a foreign currency

exchange rate at the date of the are reported using the exchange rate attransaction. Exchange differences the date of the transaction; andarising shall not be recognised as Those which are carried at fair valueincome orexpense in that year. or other similar valuation denominated

ICDS IND AS

I have yet to hear a man ask for advice on how to combine marriage and a career.

VOL. 20 NO. 2 / AUGUST 2016 C.V.O. CA’S NEWS & VIEWS

24

Recognition of exchange difference in a foreign currency are reportedshall be subject to provisions of using the exchange rates that existedsection 43A of the Act or Rule 115 when the values were determined.of the Rules, as the case may be.