czech republic - pkf · • czech resident individuals are subject to income tax on worldwide...

TRANSCRIPT

2015/16

Czech Republic

PKF Worldwide Tax Guide 2015/16 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2015/16 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 1 January 2015, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Czech Republic

PKF Worldwide Tax Guide 2015/16 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International is a family of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms. PKF INTERNATIONAL LIMITED JUNE 2015 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Czech Republic

PKF Worldwide Tax Guide 2015/16 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX VALUE ADDED TAX (VAT) OTHER TAXES

B. DETERMINATION OF TAXABLE INCOME

DEPRECIATION STOCK / INVENTORY DIVIDENDS INTEREST DEDUCTIONS LOSSES INCENTIVES

C. FOREIGN TAX RELIEF D. CORPORATE GROUPS E. RELATED PARTY TRANSACTIONS F. WITHHOLDING TAX G. EXCHANGE CONTROLS H. PERSONAL TAX I. TREATY AND NON-TREATY WITHHOLDING TAX RATES

Czech Republic

PKF Worldwide Tax Guide 2015/16 4

MEMBER FIRM For further advice or information please contact Oliver Grosse-Brauckmann, PKFI EMEI Regional Director on +44 203 691 2523 or email [email protected] BASIC FACTS Full name: Czech Republic Capital: Prague Main language: Czech Population: 10.538 million (2014) ) Major religion: 80% non-declared or non-religious, 10.3% Roman Catholic Monetary unit: Czech Koruna (CZK) Internet domain: .cz Int. dialling code: +420 KEY TAX POINTS • Czech resident companies are subject to tax on all their worldwide income. Non-resident

companies are subject to tax on Czech-source income. • Capital gains are not taxed separately but included within ordinary income. • Value added tax is applied to the provision of goods, transfer of real estate, provision of services

and imports. The basic rate is 21% although there is a lower rate of 15% and from 1 January 2015 a second lower rate of 10%.

• Transfer pricing rules apply to non-arm's length profit-sharing arrangements agreed between

related parties. • A real estate tax is levied on land and buildings. • Ordinary credits for foreign income tax on overseas income are available to Czech resident

taxpayers where a relevant double tax agreement exists. If there is no tax treaty, the overseas tax is included in the tax expenses for the following period.

• Czech resident individuals are subject to income tax on worldwide income, whereas non-

resident Individuals are only required to pay tax on Czech-sourced income. For 2015, the personal income tax rate is 15%, An additional 7 % “solidarity surcharge” applies to the part of the gross employment income (including taxable benefits) and tax base from business income which exceeds 48 times annual average salary (for 2015 CZK 1,277,328)

• In addition to income tax, employees also pay social security and medical insurance

contributions at the rate of 11% withheld by their employers from their gross wages. Employer´s part of social security and medical insurance represents additional cost of 34 %.

• Withholding tax applies to dividends, licence fees, interest and related income and royalties.

Czech Republic

PKF Worldwide Tax Guide 2015/16 5

A. TAXES PAYABLE FEDERAL TAXES AND LEVIES COMPANY TAX Company tax is payable by Czech resident companies on income derived from worldwide sources. Non-resident companies are required to pay the tax on income sourced in the Czech Republic. Resident companies are those which have their registered office, or place of management located, in the Czech Republic. The corporate income tax rate is 19% for 2015 and this is applied to all taxable profits of a business, including capital gains from the sale of shares (if not exempt under the participation exemption regime). A 5% and 0% tax rate applies to income from defined investments and pension funds respectively. A special tax rate of 15% applies to dividend income received by Czech tax resident entities from non-resident entities (unless a participation exemption applies). A company may choose either a calendar year or an accounting year as its tax year. Tax returns are due within three months of the end of the tax period (or within six months for audited entities or entities represented by recognized tax advisor). Tax is required to be paid within three months of the end of the tax period (or within six months for audited entities or represented by recognized tax advisor). Estimated company tax payments (advance tax payments) are paid semi-annually or quarterly. There is no CFC legislation in the Czech Republic. CAPITAL GAINS TAX Capital gains such as dividends, interest from owed securities, deposit accounts and deeds are subject to 15% withholding tax. Where capital gains are paid to residents of non-treaty countries the rate of withholding tax is 35%. Dividends income is exempt from withholding tax if paid to a resident of an EU territory in accordance with the EU Parent-Subsidiary Directive No 90/435/ EU. The Parent company must have a minimum of a 10% holding in the subsidiary's registered capital for an uninterrupted period of at least 12 months. The subsidiary company must have the form of the company indicated in the Parent-Subsidiary directive, be tax resident in EU Member State and be subject to corporate income tax in these States. Exemption applies under the same conditions also to dividends distributed by subsidiaries with their seats in Switzerland, Norway, Island or Lichtenstein. Moreover the similar exemption applies to the income arising from transfer of shareholdings by a parent company in its subsidiaries within the EU. The scope of exemption is extended to dividends distributed by qualified subsidiaries with their seats outside the EU where relevant DTT is applicable and that are subject to a rate of tax at a minimum of 12% the year of payment of distribution of dividends and previous year. The exemption also applies to income from the transfer of shareholdings by parent companies in subsidiaries outside the EU under the same conditions. Interest and royalties are tax exempt when transferred from a Czech company to a parent company in another state in EU or EEA (which is a shareholder of the Czech company and has held the shares

Czech Republic

PKF Worldwide Tax Guide 2015/16 6

for a period of at least 24 months). It is necessary to apply for this tax exemption with the Czech tax authority. The following documents must be generally provided: tax domicile certificate of the parent company, extract of the commercial register of the parent company, extract of commercial register of the Czech company, the title of the licence fees, and confirmation from the tax authority of parent company, that the parent company has its tax domicile in EU or EEA state. For companies, capital gains are included within ordinary income in the year they arise and taxed as part of their respective taxable profits for the period. Capital gains are not taxed separately in the Czech Republic except of those with their source abroad. BRANCH PROFITS TAX There is no separate branch profits tax in the Czech Republic. The income of a Czech branch of a foreign company is subject to taxation at the generally applicable, 19% rate for 2015. Attribution of profits to a branch if it does not result from its separately held bookkeeping is generally determined on the basis of the margins that are generally realised by resident companies undertaking similar activities. VALUE ADDED TAX (VAT) Value Added Tax (VAT) is imposed on the domestic provision of goods, transfer of real estate, provision of services, including the transfer or use of rights and importation of goods. There are three rates of VAT; basic rate 21% and lower rate 15% and from 2015 10 %. The 21% rate applies generally to supplies of goods and most services with some exceptions while the 15% rate applies to selected services and some goods such as foodstuffs accommodation, restaurant, and transport services. The 10 % rate applies namely to pharmaceutical products, printed books, to certain children nutrition and to qualified mill products. With effect from 1 January 2015, changes in the Value Added Tax (VAT) legislation were made which: (1) Implemented a 'mini one-stop shop regulation' for companies providing electronic,

telecommunication and broadcasting services to private customers; (2) Provided for additional categories of goods to be subject to the reverse charge mechanism; and, (3) Provided changes to the VAT treatment of a transfer of immovable property. Goods and services exported from the Czech Republic to non-EU countries are exempt from VAT. The principles of the Sixth Directive – VAT (771388/EU), have applied since 1 May 2004 to goods and services exported from the Czech Republic to EU countries. A group of related parties may register as a single VAT taxpayer. OTHER TAXES Tax on real estate property is levied on buildings, structures and land situated within the Czech Republic. The taxpayer is the actual owner or in limited cases the user of the property. The rate depends on size, quality, type and location of the property. This tax is deductible for corporate income tax purposes.

Czech Republic

PKF Worldwide Tax Guide 2015/16 7

Income from inheritance and gifts are not subject to a specific tax but are included within the income tax regime and subject to tax at a rate of 15% for individuals and 19 % for companies (broad exemptions apply to donations for individuals while income from inheritance is exempt for all taxpayers). From 2014 a separate law was introduced for real estate transfer tax which was broadly in line with the previous system. Property transfers are liable to real estate transfer tax at the rate of 4% on the official valuation or actual price, whichever is the higher. This tax is deductible for income tax purposes. The taxpayer is the seller or if agreed in the transfer agreement the acquirer. The employers' payment on behalf of their employees towards the workers' social security and medical insurance is at the rate of 34% of the gross payroll (social security premium payments are capped by CZK 1,277,328 in 2015). There is no Stamp Duty in the Czech Republic although the operation of a notarial fee may apply for certain documents. There is no net wealth/worth tax in the Czech Republic. B. DETERMINATION OF TAXABLE INCOME The company's taxable income is determined by ascertaining assessable income and then subtracting all allowable expenses. In general, to be tax deductible, all expenses must be related to the gaining or producing of assessable income and are not exempt pursuant to the law on income tax. DEPRECIATION The tax law prescribes six groups of tangible assets for tax depreciation purposes using depreciation periods ranging from three to 50 years. Either straight-line or accelerated depreciation methods are available. The choice of a method is made by the taxpayer and, once selected, cannot be changed for the remaining life of the asset.

Assets Depreciation group

Depreciation period (minimum years)

Office machines and computers, tools 1 3

Engines, motor vehicles, machines, audio-visual equipment 2 5

Elevators, escalators, turbines, air conditioning equipment, electric motors, and generators 3 10

Buildings made of wood and plastic, long-distance lines, and pipes 4 20

Buildings (except for those listed in groups 4 and 6), roads, bridges, tunnels 5 30

Administrative buildings, department stores, historical buildings, and hotels 6 50

Tangible assets with economic useful lives of longer than one year and acquisition prices higher than CZK 40,000 are subject to tax depreciation. Buildings are always considered as tangible assets.

Czech Republic

PKF Worldwide Tax Guide 2015/16 8

Intangible assets which are acquired for CZK 60,000 or more, have a useful life of longer than one year and were acquired from a third party or developed internally for the purpose of trading are also subject to tax depreciation. It includes software, valuable rights or the intangible results of research and development. For tax purposes, intangible assets are depreciated over the life of the license held by the taxpayer (if the licence is for a limited number of years) otherwise it depends on the category of intangible asset, for example, research and development and software are depreciated over 36 months and audio-visual works are depreciated over 18 months. STOCK / INVENTORY All trading stock is valued at purchase price, including ancillary costs incurred. Stock produced by the company's own operation is valued at internal costs. If a temporary reduction of stock value is non-tax deductible, corrective provisions are applied. Accepted valuation methods include the use of the arithmetical average cost and first in first out (FIFO) methods but not last in first out (LIFO) or the replacement-cost methods (except for livestock). DIVIDENDS If dividends are not tax exempt under the participation exemption regime, they are subject to a final withholding tax of 15% or the rate agreed in an applicable double taxation treaty if paid to tax non-resident. Tax exemption does not apply to a profit share paid out on the liquidation of a company. A withholding of 35% applies to dividends paid to resident entities of countries which are not part of the European Union or European Economic Area and do not have an enforceable double taxation treaty or tax information exchange agreement with the Czech Republic. INTEREST DEDUCTIONS Interest incurred for business purposes is broadly tax deductible, however, thin capitalisation rules apply which can restrict its deduction. Notably, financial costs (e.g. interest plus other related costs, such as bank fees) of credits and loans for the relevant tax period shall be considered non-deductible expenses for the proportion of related-party loans which exceed four times the accounting equity (based on Czech GAAP) of the borrower. The non-deductible expense is the amount of the interest connected to the part of the sum of credits and loans (including financing costs) from related parties by which it exceeds a 4:1 debt to equity ratio (6:1 for banks and insurance companies) in the period for which the tax return is submitted. LOSSES Tax losses may be carried forward for five years following the year when the tax loss has been declared. Losses may not be carried back. Losses arising (after 2004) may be transferred within the framework of common taxation of parent and daughter companies within the EU territory (transfers of enterprises, mergers and demerger of enterprises) under limited conditions.

Czech Republic

PKF Worldwide Tax Guide 2015/16 9

INCENTIVES Investment incentives including tax relief are governed by the Investment Incentives Act and apply only to Czech entities (including Czech subsidiaries of foreign companies). A variety of incentives are available including financial support for training or retraining of employees or the creation of new jobs, capital expenditure grants and income tax relief. There are also incentives to support technology centres, strategic services and the manufacturing industry of the Czech Republic. C. FOREIGN TAX RELIEF Ordinary credits for foreign income tax are available to resident taxpayers under Czech law where an international double taxation treaty exists and indicates tax credit as method of avoidance of double taxation. The clearance or exemption method is available, according to the particular double tax treaty. If there is no tax treaty, the legal entity will include the foreign tax paid as tax expense for the following period provided it was imposed on income which has been included within the Czech entities taxable income. D. CORPORATE GROUPS There is no group taxation in the Czech Republic. Each company is taxed as a standalone entity regardless of its ownership or control relationships. E. RELATED PARTY TRANSACTIONS Non-arm's length pricing arrangements between related parties are addressed by transfer pricing legislation which allows the tax authority to adjust the prices to reflect third party arm’s length values. Where such adjustment are made by the tax authority, which can be the result of an audit, additional tax liabilities and penalties can arise which can also affect a company’s ability to claim investment incentives. As of the tax period 2014 qualified companies are obliged to file a special form describing arrangements between related parties together with the corporate income tax return. The Czech Republic tax authorities follow OECD pricing guidelines and an Advance Pricing Agreement (APA) between a company and its related parties can be agreed. F. WITHHOLDING TAX Certain types of income of companies are subject to withholding tax at source. In the case of resident taxpayers, dividends from Czech sources are subject to final withholding tax at 15% whereas interest and royalties are not subject to withholding tax and are included in the general tax base. In the case of non-residents, dividends, interest and royalties are all subject to 15% withholding tax if exemption does not apply – see more precisely chapter Capital Gains Tax. Residents of countries outside the European Union or European Economic Area which do not have an enforceable double taxation treaty or tax information exchange agreement with the Czech Republic are subject to 35% withholding tax).

Czech Republic

PKF Worldwide Tax Guide 2015/16 10

G. EXCHANGE CONTROLS The Foreign Exchange Act allows the Czech currency to be used freely to pay for business and other costs, for direct investment and reinvestment and for purchase of real estate property abroad. Capital transfers have been deregulated but the reporting duty has been retained. Sales of foreign currency and gold are permitted where one of the parties is an entity holding a licence or foreign currency permit. H. PERSONAL TAX Income tax is payable by Czech resident individuals on income derived from worldwide sources. Non-resident individuals are only required to pay tax on Czech-sourced income. Tax residence is determined by reference to permanent home or where the individual has spent at least 183 days of the relevant calendar year in the Czech Republic. Income tax is payable on total tax base from different kinds of income. Taxable income of individuals includes employment income, business income, certain capital gains, dividend income, rental income, interest income; annuities and other income including benefits in kind related to such income. Generally the tax base is calculated as difference between assessable income and expenses and tax deductible expenses allowable deductions. Expenses cannot be claimed for employment income or capital gains (most of which are subject to withholding tax). Employment income cannot be reduced by losses of any other categories of income. Tax base for employment income is increased by the amount of social security and health insurance contributions to be paid by the employer (34%, so called super-gross wage). Income from business or rental operations can be reduced by losses deriving from other categories. Income from employment is taxable individually and is reduced for some deductible items and personal allowances. For 2015, the personal income tax rate is 15%. However income from employment and business income are also subject to “solidarity surcharge that represents additional 7% applied to the amount which in total exceeds 48 times annual average salary (for 2015 CZK 1,277,328). Employees hired under an employment contract under Czech law pay social security and medical insurance contributions at the rate of 11% withheld by their employers from their gross wages. This represents 6.5% for social security and 4.5% for health insurance. The contribution rates for the employer are 25% for social security and 9% for health insurance. Medical insurance and social security contributions are also paid by the self-employed individuals. The maximum annual social security contributions cap which applies to both employees and entrepreneurs is 48 times the average monthly wage per year (for 2015 this is CZK 1,277,328). • A deduction of up to CZK 12,000 per year is available for under certain conditions for private

contributions paid on private life insurance. A deduction is also available for up to CZK 12,000 per year (under certain conditions) for private contributions paid to a private pension insurance fund.

• A deduction is available for up to CZK 300,000 per year for interest paid on a mortgage for

taxpayer´s permanent home, although several strict conditions apply.

Czech Republic

PKF Worldwide Tax Guide 2015/16 11

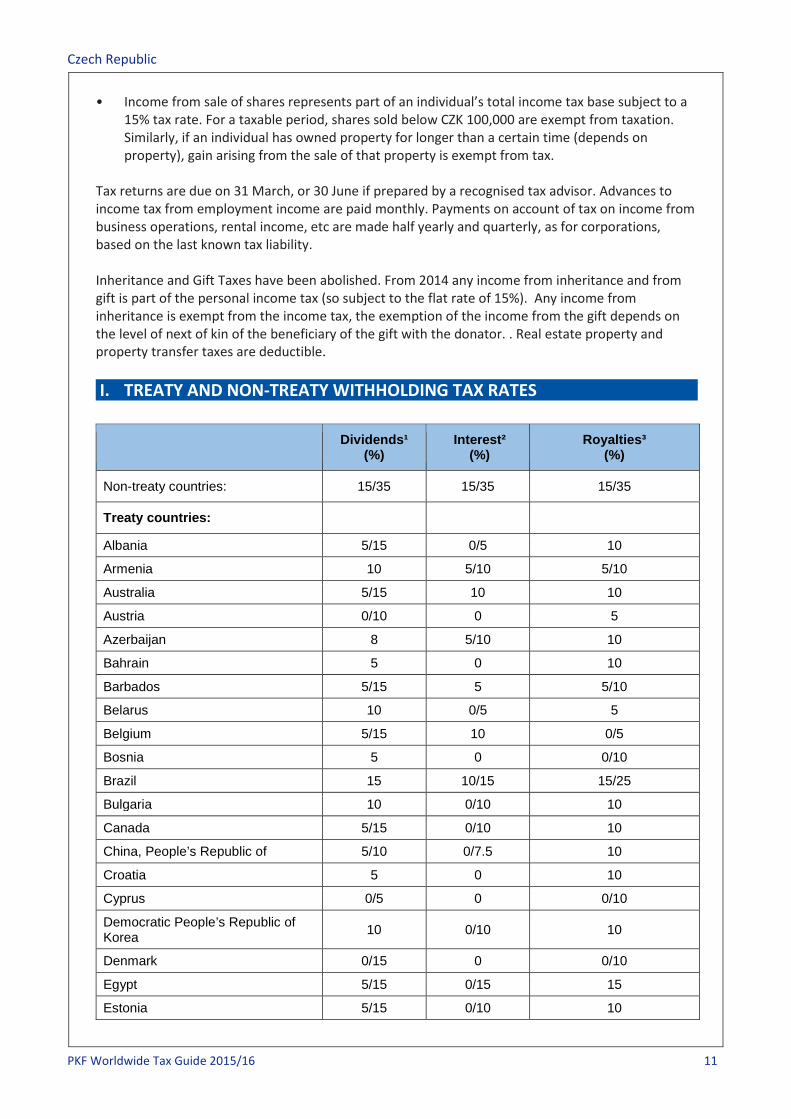

• Income from sale of shares represents part of an individual’s total income tax base subject to a 15% tax rate. For a taxable period, shares sold below CZK 100,000 are exempt from taxation. Similarly, if an individual has owned property for longer than a certain time (depends on property), gain arising from the sale of that property is exempt from tax.

Tax returns are due on 31 March, or 30 June if prepared by a recognised tax advisor. Advances to income tax from employment income are paid monthly. Payments on account of tax on income from business operations, rental income, etc are made half yearly and quarterly, as for corporations, based on the last known tax liability. Inheritance and Gift Taxes have been abolished. From 2014 any income from inheritance and from gift is part of the personal income tax (so subject to the flat rate of 15%). Any income from inheritance is exempt from the income tax, the exemption of the income from the gift depends on the level of next of kin of the beneficiary of the gift with the donator. . Real estate property and property transfer taxes are deductible. I. TREATY AND NON-TREATY WITHHOLDING TAX RATES Dividends¹

(%) Interest²

(%) Royalties³

(%)

Non-treaty countries: 15/35 15/35 15/35

Treaty countries:

Albania 5/15 0/5 10

Armenia 10 5/10 5/10

Australia 5/15 10 10

Austria 0/10 0 5

Azerbaijan 8 5/10 10

Bahrain 5 0 10

Barbados 5/15 5 5/10

Belarus 10 0/5 5

Belgium 5/15 10 0/5

Bosnia 5 0 0/10

Brazil 15 10/15 15/25

Bulgaria 10 0/10 10

Canada 5/15 0/10 10

China, People’s Republic of 5/10 0/7.5 10

Croatia 5 0 10

Cyprus 0/5 0 0/10

Democratic People’s Republic of Korea 10 0/10 10

Denmark 0/15 0 0/10

Egypt 5/15 0/15 15

Estonia 5/15 0/10 10

Czech Republic

PKF Worldwide Tax Guide 2015/16 12

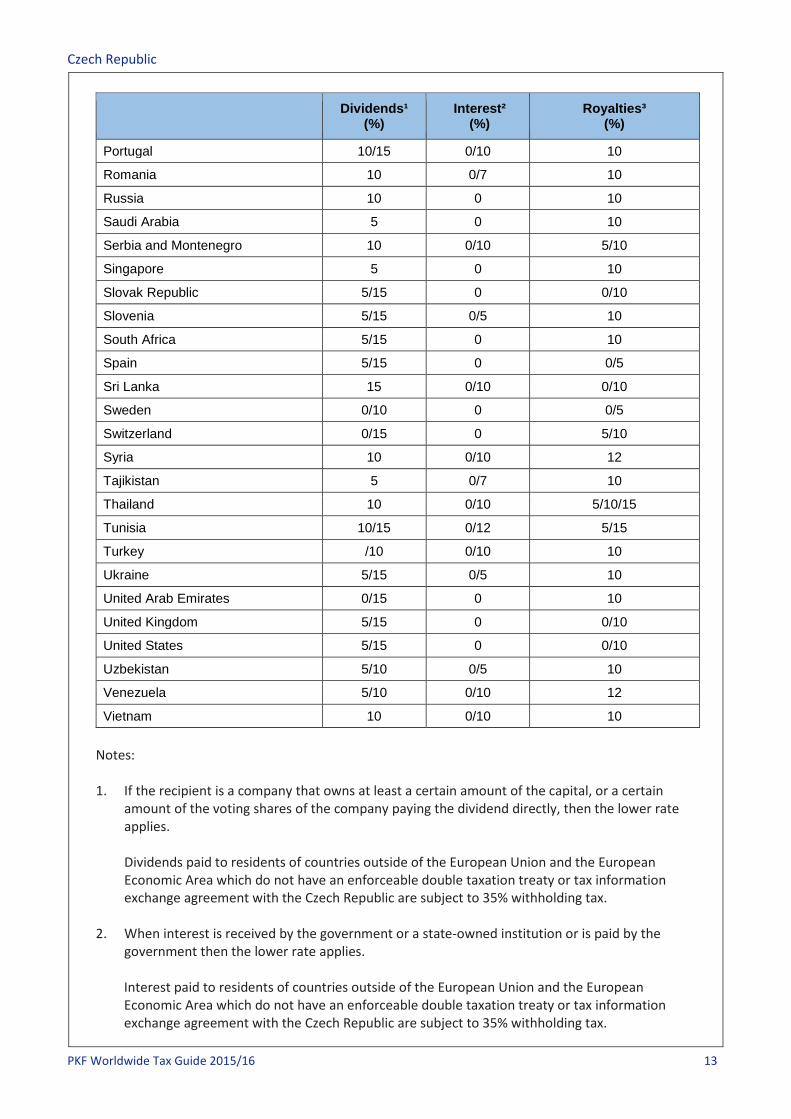

Dividends¹ (%)

Interest² (%)

Royalties³ (%)

Ethiopia 10 0/10 10

Finland 5/15 0 0/1/5/10

France 0/10 0 0/5/10

Georgia 5/10 0/8 0/5/10

Germany 5/15 0 5

Greece Local rates 0/10 0/10

Hong Kong 5 0 10

Hungary 5/15 0 10

Iceland 5/15 0 10

India 10 0/10 10

Indonesia 10/15 0/12.5 12.5

Ireland, Republic of 5/15 0 10

Israel 5/15 0/10 5

Italy 15 0 0/5

Japan 10/15 0/10 0/10

Jordan 10 0/10 10

Kazakhstan 10 0/10 10

Korea, Republic of 5/10 0/10 0/10

Kuwait 0/5 0 10

Latvia 5/15 0/10 10

Lebanon 5 0 5/10

Lithuania 5/15 0/10 10

Luxembourg 0/10 0 0/10

Macedonia 5/15 0 /10

Malaysia 0/10 0/12 12

Malta 5 0 5

Mexico 10 0/10 10

Moldova 5/15 5 10

Mongolia 10 0/10 10

Morocco 10 0/10 10

Netherlands 0/10 0 5

New Zealand 15 0/10 10

Nigeria 12.5/15 0/15 15

Norway 0/15 0 0/5/10

Panama 10 0/5/10 10

Philippines 10/15 0/10 10/15

Poland 5 0/5 10

Czech Republic

PKF Worldwide Tax Guide 2015/16 13

Dividends¹ (%)

Interest² (%)

Royalties³ (%)

Portugal 10/15 0/10 10

Romania 10 0/7 10

Russia 10 0 10

Saudi Arabia 5 0 10

Serbia and Montenegro 10 0/10 5/10

Singapore 5 0 10

Slovak Republic 5/15 0 0/10

Slovenia 5/15 0/5 10

South Africa 5/15 0 10

Spain 5/15 0 0/5

Sri Lanka 15 0/10 0/10

Sweden 0/10 0 0/5

Switzerland 0/15 0 5/10

Syria 10 0/10 12

Tajikistan 5 0/7 10

Thailand 10 0/10 5/10/15

Tunisia 10/15 0/12 5/15

Turkey /10 0/10 10

Ukraine 5/15 0/5 10

United Arab Emirates 0/15 0 10

United Kingdom 5/15 0 0/10

United States 5/15 0 0/10

Uzbekistan 5/10 0/5 10

Venezuela 5/10 0/10 12

Vietnam 10 0/10 10 Notes: 1. If the recipient is a company that owns at least a certain amount of the capital, or a certain

amount of the voting shares of the company paying the dividend directly, then the lower rate applies.

Dividends paid to residents of countries outside of the European Union and the European Economic Area which do not have an enforceable double taxation treaty or tax information exchange agreement with the Czech Republic are subject to 35% withholding tax.

2. When interest is received by the government or a state-owned institution or is paid by the

government then the lower rate applies.

Interest paid to residents of countries outside of the European Union and the European Economic Area which do not have an enforceable double taxation treaty or tax information exchange agreement with the Czech Republic are subject to 35% withholding tax.

Czech Republic

PKF Worldwide Tax Guide 2015/16 14

3. Cultural royalties are generally subject to the lower rate.

Royalties paid to residents of countries outside of the European Union and the European Economic Area which do not have an enforceable double taxation treaty or tax information exchange agreement with the Czech Republic are subject to 35% withholding tax.