d3 banking digital banking the way it should be · pdf filed3 banking digital banking the way...

TRANSCRIPT

D 3 B A N K I N G

DIGITAL BANKING THE WAY IT SHOULD BE

Why Good Enough Isn’t In Digital BankingNo matter how you look at the results from a recent JD Power online survey measuring the level of consumer satisfaction with banks, if you are a regional or midsized institution it should be a wake up call. According to the data collected in the survey, the biggest banks — specifically Chase, Citi, Wells, BoA, PNC and US Bank — have a higher consumer satisfaction ranking than regional ($33B to $108BB in deposits) and midsized ($2B to $33B in deposits) institutions.

This is the first time since this research was first conducted in 2006 that big banks have outperformed the regional and midsized banks. According to Rocky Clancy, vice president of the financial services practice at J.D. Power, the reason big banks are outperforming the others has to do with them “putting their money where their mouths are” when it comes to investing in customer facing technology, specifically digital banking.

Good enough, “me too” solutions are no longer viable as strategies for institutions that want to be competitive in their markets. We have reached a pivotal moment in digital banking when regional and midsized financial institutions must look for new partners to help them deliver digital banking solutions that help them compete successfully.

D3 BANKING OFFERS:

• Single omnichannel solution• Consistent user experience• Automatic transaction categorization• Embedded financial management• Aggregation• Pro forma financials• Predictive cash flow• View and do dashboards• Biometrics security• Remote deposit capture• Innovative money movement• Expedited payments• Contextual functionality• Data visualization• Comprehensive alerting• iOS and Android apps• Mobile only and/or mobile first• Control of user data• 1:1 Marketing• Shadow assist• Least cost routing• Multi-tenancy• Configuration not customization• Maximum control of entitlements

www.d3banking.com

For the first time in the history of the survey, JD Powers records a higher customer satisfaction rates among the largest bank over midsized/regional banks.

Digital Banking The Way It Should BeD3 Banking’s solutions for consumer and small business digital banking are the newest, most modern products in the marketplace. Leading institutions including Arvest Bank, First Tennessee Bank, IBERIABANK and others have selected our products to be the foundation for their digital banking strategies. Some of the reasons why these blue chip institutions have partnered with D3 Banking include:

One Solution, All Digital Devices: D3 Banking delivers a comprehensive set of banking services from a single code base to laptops, smartphones, tablets and wearables eliminating the inconsistent user experience as well as the complexity and costs associated with using disparate solutions from multiple vendors to meet the needs of digital customers. Our API-driven architecture allows us to easily incorporate new services as the needs of digital consumers evolve.

Scalable and Configurable: D3 Banking’s products were built to meet the needs of regional and mid-sized financial institutions. In the past year we have successfully completed several of the largest legacy product replacements in more than a decade in the industry. In addition, our solutions are built to be highly configurable. This means that banks and credit unions control their own destiny rather than being held hostage by vendors whose solutions require expensive and time-intensive customization.

Data Driven Personalization: D3 Banking offers solutions built with powerful data analytics capabilities that allow customers to assess and monitor their financial health without requiring heavy lifting on their part. In addition, the information concerning a customer’s financial health is provided to the institution, allowing banks or credit unions to personalize the advice, products and services they offer to each individual.

Choose Your Deployment Model: D3 Banking’s products can be operated on premise or hosted for a financial institution. Regardless of which model suits a bank or credit union better, each institution receives the same value added features, including scalability, configurability, availability, data analytics and reduced costs and complexity, that have made D3 banking a provider of choice for leading institutions

During a day, 98 percent of consumer use more than one of their digital devices while 90 percent start a task on one device and complete it on another. (Google: The New Multi-Screen World)

www.d3banking.com

D3 Consumer BankingD3 Consumer Banking was developed in response to an industry-wide problem that exists today. The harsh reality is that most financial institutions have lost control of their digital customers. They’ve outsourced control of the user’s experience, lost control of digital data needed to deepen their customer relationships, and diluted their brand, all the while driving up the costs and complexity of their digital operations. D3 Consumer Banking returns control of the user experience and associated data to financial institutions. The unique features offered in D3 Consumer Banking include the following:

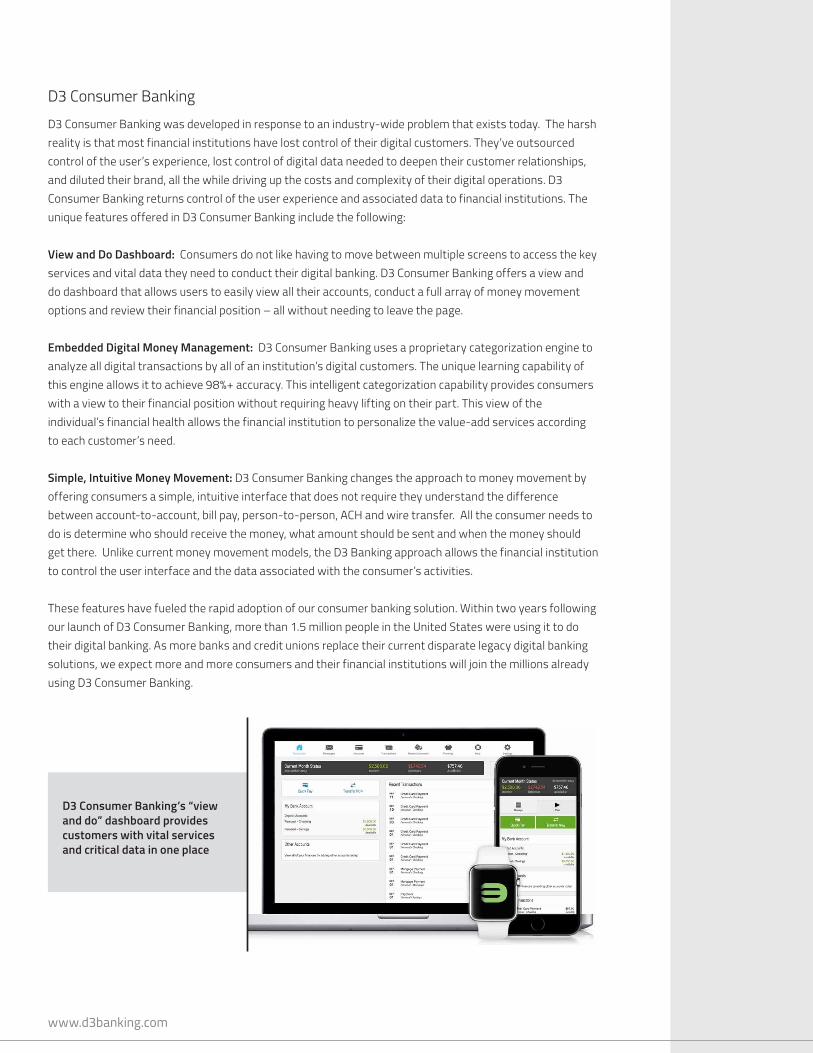

View and Do Dashboard: Consumers do not like having to move between multiple screens to access the key services and vital data they need to conduct their digital banking. D3 Consumer Banking offers a view and do dashboard that allows users to easily view all their accounts, conduct a full array of money movement options and review their financial position – all without needing to leave the page.

Embedded Digital Money Management: D3 Consumer Banking uses a proprietary categorization engine to analyze all digital transactions by all of an institution’s digital customers. The unique learning capability of this engine allows it to achieve 98%+ accuracy. This intelligent categorization capability provides consumers with a view to their financial position without requiring heavy lifting on their part. This view of the individual’s financial health allows the financial institution to personalize the value-add services according to each customer’s need.

Simple, Intuitive Money Movement: D3 Consumer Banking changes the approach to money movement by offering consumers a simple, intuitive interface that does not require they understand the difference between account-to-account, bill pay, person-to-person, ACH and wire transfer. All the consumer needs to do is determine who should receive the money, what amount should be sent and when the money should get there. Unlike current money movement models, the D3 Banking approach allows the financial institution to control the user interface and the data associated with the consumer’s activities.

These features have fueled the rapid adoption of our consumer banking solution. Within two years following our launch of D3 Consumer Banking, more than 1.5 million people in the United States were using it to do their digital banking. As more banks and credit unions replace their current disparate legacy digital banking solutions, we expect more and more consumers and their financial institutions will join the millions already using D3 Consumer Banking.

D3 Consumer Banking’s “view and do” dashboard provides customers with vital services and critical data in one place

www.d3banking.com

D3 Small Business BankingSince 1995, two-thirds of our job growth has come from small business. However, while half a million small businesses are launched each month, more than that number fail. One of the primary reasons that small businesses fail is an inability to manage their finances. Financial institutions have neglected to provide these organizations with the kind of financial services and support they need to succeed. At the same time, banks and credit unions have missed a huge opportunity to unlock potential revenue by providing these services to small businesses.

D3 Small Business Banking addresses the needs of these under-served small businesses allowing financial institutions to help these organizations survive and thrive.

One Stop Information Rich View: Accessing D3 Small Business Banking is as simple as toggling between an owner’s personal and business accounts. No additional login required. The D3 Small Business Banking Dashboard presents summary information regarding all the accounts held by a small business and allows an owner to conduct a full array of money movement services without leaving the page. In addition, from within the dashboard, the owner can quickly and easily review and evaluate the financial health of his or her business with information provided in graphical form automatically, using D3 Banking’s powerful data analytics engine.

Intuitive Analytics and Automated Reporting: D3 Small Business Banking turns this data into actionable information by automatically creating pro forma budgets, income statements, balance sheets and a statement of cash flow for the small business owner. This is done without requiring heavy lifting from the owner. We provide a graphical representation of the data as well as line item versions that are downloadable.

More Control, Less Complexity, Improved Planning: D3 Small Business Banking’s entitlements functionality allows an owner to assign or limit access across accounts and activities. A timeline presentation of money movement activities is provided in order to present all transactions (transfers, bill pays, etc.) past and present in one simple view. Based on the predictive analytics used by our solution, the owner can easily configure the timeline to identify if there may be a cash shortage in the future. Similarly, the financial institution has visibility to this information and can use it to engage with the small business to proactively offer relevant advice, products or services.

D3 Small Business Banking addresses the need of organizations that lack consistent access to the financial expertise they need to succeed. In addition, our small business solution provides financial institutions with a way to provide the products, services and advice that small business owners need through any digital channel, establishing a partnership that is advantageous to both parties.

FOR MOREINFORMATION:

D3 Banking is Data Driven Digital™ banking. The D3 Banking product family is built for financial institutions that want a digital banking solution that lowers costs, reduces complexities, delivers a consistent user experience and drives new revenue opportunities with personal-ized services and products. For more information, visit www.D3Banking.com.

Omaha Office

11837 Miracle Hills DriveSuite 101Omaha, Nebraska 68154

Phone: +1 (402) 933-0541

www.d3banking.com

D3 Small Business Banking provides predictive cash flow and a robust entitlement capabilities giving owners better control of finances.