daily fantasy sports (dfs) notes

TRANSCRIPT

Why DFS?

• Unlawful Internet Gambling Enforcement Act (UIGEA) passes in 2006– Prohibits online gambling except for fantasy sports and horse

racing– Cripples US online poker and sportsbook markets, many

businesses stop accepting US customers

• Apr 15 2011, “Black Friday” – Feds seize domains of largest online poker sites still accepting US-based players

• DFS explodes in popularity in 2013 with first $1M single-winner prize (similar to Chris Moneymaker winning 2003 WSOP)

• Now the fastest growing segment of the digital and interactive gaming space

Market Size & Demographics

• ~50M traditional (season-long) fantasy uniques• DFS only has ~1.5M uniques (3%)

– Penetration rate is small as industry is young– Whether rates will approach/exceed much higher levels

remains to be seen once early-adopter phase has passed– Debate is whether DFS will remain a niche product due to

its more technical nature– Life-Time Value (LTV) of players currently high (~$750) but

potentially overvalued and unsustainable

• DFS players primarily millennials (tech-savvy) and overwhelmingly male (est. 95%+)– Significant interest from leagues and media outlets

The Current Players

• FanDuel & DraftKings

• Everybody else

DFS Formats

• Person-to-person (P2P), roster-based, salary caps:– FanDuel (team sports), DraftKings (team and individual

sports)

• Simplified P2P, reduced rosters:– TopLine Game Labs (DailyMVP, FanNation)

• Against the House, lineup:– BetAmerica HomeRun predictions– Game Sports Network (GSN) HotRoster

• Event-based, P2P, market makers:– ScoreStreak (ran out of $)– Tradesports (Yes/No preditions)

Two-Horse Race: FanDuel & DraftKings

• FanDuel & DraftKings estimated combined market share 97%+

• Estimated split:– FanDuel: 75%– DraftKings: 25%

• Split is highly sensitive to time of year and offerings:– NFL dominates revenues and traffic; FanDuel has clear lead

in NFL– DraftKings has official MLB tie-in and offers Golf,

MMA/UFC, and NASCAR DFS competitions, which FanDueldoes not

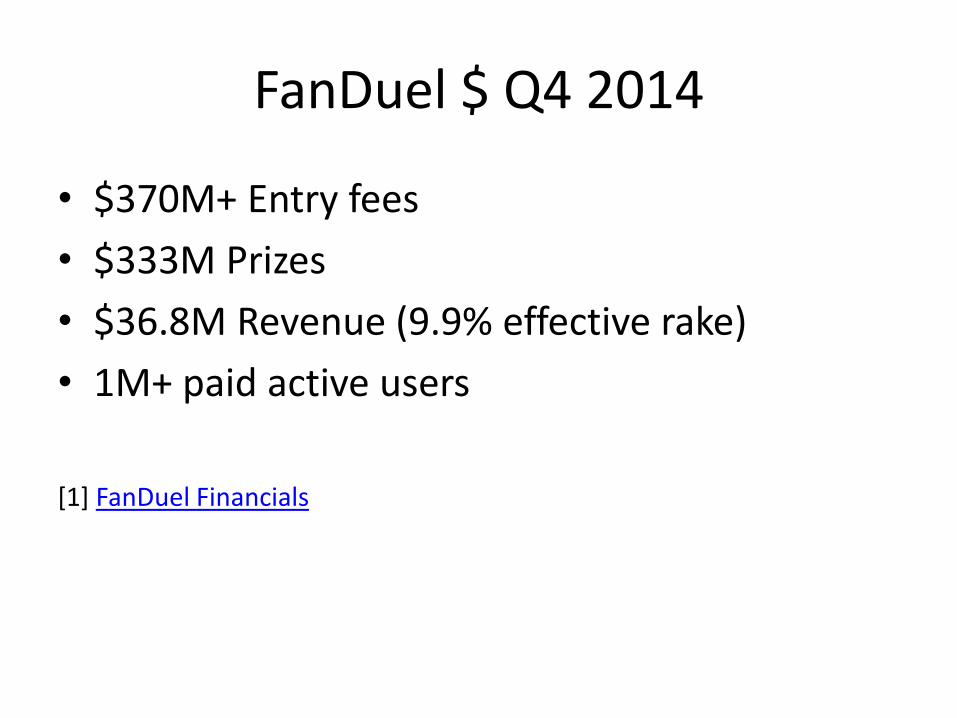

FanDuel $ Q4 2014

• $370M+ Entry fees

• $333M Prizes

• $36.8M Revenue (9.9% effective rake)

• 1M+ paid active users

[1] FanDuel Financials

FanDuel $ Q4 2014

• 300%+ YoY Revenue growth– 2013: $14.3M– 2014: $57.3M

• 424% YoY growth in active paid customers– Q4 2013: 193k– Q4 2014: 1.01M

• However, YoY avg. revenue per user decreased (-5.3%), and effective rake increased (9.1% to 9.9%)

[1] FanDuel Financials

DraftKings $

• DraftKings do not disclose as much investor information as FanDuel

• Site has quoted

– “$30M in revenue in 2014”

– “350K monthly active paid users in 4Q 2014”.

Venture Funding: FanDuel

• $86.2M in 6 rounds incl. $70M Series D (Q3 2014)

• Investors include Shamrock, NBC Sports, KKR among others

• Multi-year NBA partnership included equity stake for NBA in FanDuel

• Suggested valuation $1.0B to $1.5B

Venture Funding: DraftKings

• $75M in 5 rounds incl. $41M Series C (Q3 2014)• Investors include Raine Group, Atlas, GGV,

Redpoint among others• $250M Disney investment (Q2 2015) was

cancelled/postponed (reason not entirely clear)– Deal allegedly included agreement for $500M

marketing spend by DraftKings on ESPN properties– DraftKings will have exclusive DFS advertising rights on

ESPN starting 2016

• Official partnerships with MLB and NHL• Suggested valuation ~$1B

Current DFS Business Behavior

• “Land grab” currently:– Rush to partner with teams, leagues and media

outlets– Significant marketing expenditures driven by venture

capital– Aggressive courting of former online poker and

sportsbook players

• Lack of regulation and online, data-driven business model results in negligible barriers to entry

• Neither FanDuel nor DraftKings are profitable

The Future Players

• Amaya (AMYGF)– New owner PokerStars and Full Tilt Poker ($5B acquisitions),

already has casino gaming, testing sportsbook and prepping DFS site for 2015/16 NFL season

– Highly profitable (40%+ EBIDTA margins) and experienced in about monetizing online gaming users

– Could either build in-house or seek M&A opportunties

• Yahoo (YHOO)– Largest traditional season-long fantasy operator– Season-long and daily fantasy cross-over opportunities, large

existing user-base and technology/media powerhouse (see exclusive NFL game streaming deal)

– Prepping DFS site for 2015/16 NFL season or Q4 2015– Likely to be developed in-house

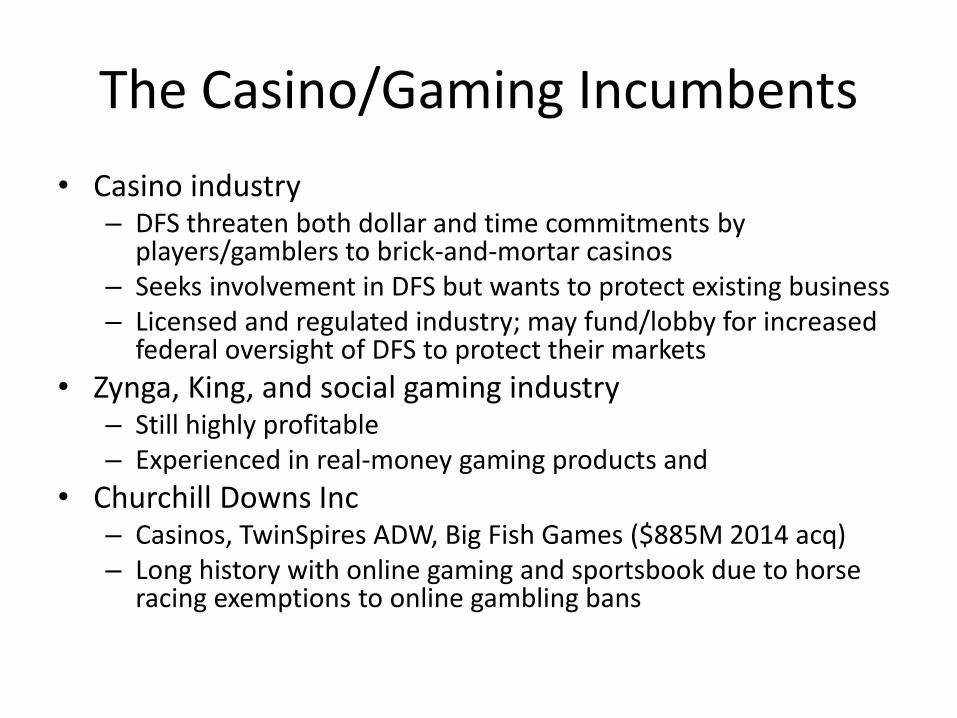

The Casino/Gaming Incumbents

• Casino industry– DFS threaten both dollar and time commitments by

players/gamblers to brick-and-mortar casinos– Seeks involvement in DFS but wants to protect existing business– Licensed and regulated industry; may fund/lobby for increased

federal oversight of DFS to protect their markets

• Zynga, King, and social gaming industry– Still highly profitable– Experienced in real-money gaming products and

• Churchill Downs Inc– Casinos, TwinSpires ADW, Big Fish Games ($885M 2014 acq)– Long history with online gaming and sportsbook due to horse

racing exemptions to online gambling bans

Kingmakers: NFL

• Historically the biggest beneficiary of fantasy sports

• FanDuel’s growth and dominance has been directly tied to daily fantasy football

• League has been taking a watching brief

• Leadership has been adverse to gambling connections

• However, some team owners are investors (e.g. Robert Kraft in DraftKings)

Kingmakers: ESPN

• Dominant sports media outlet

• Has prominently featured traditional and daily fantasy sports within its properties, broadcasts and publications

• DraftKings exclusive DFS advertising deal with ESPN may be inspired if growth continues at current pace and DFS becomes mainstream during sports broadcasts

Princemaker: PGA

• One of the hottest new verticals

• DraftKings offers golf, FanDuel does not

• Significant media exposure with 2015 US Open due to Dustin Johnson’s final hole 3-putt handing first-time DFS money-game player a ~$1M prize

Engagement: DFS, Leagues, Media

• Media: DraftKing and FanDuel user surveys stated:– 47% “started following 1+ new sports” due to DFS– 35% consume “a little more live sports content”, 43%

consume “a lot more live sports content”– 40% increase in time spent consuming sports media

• Leagues: Driving attention when fan interest has historically been at its lowest– Regular season games– Blowouts– Unfashionable/small-market games/events

Risks: Legal

I am not a lawyer (IANAL)

• ~45+ States “permit” DFS• Post-UIGEA, significant risks still possible for DFS to be

deemed “gambling”• Poker’s “Black Friday” showed Government can move to

shut down online businesses/markets overnight• Casino and gaming advisor industries have increased calls

for DFS to be regulated and licensed• Should a DFS-related gambling scandal occur in a

professional or college team or individual sport event, political support for non-regulated DFS sites may be impacted negatively

Risks: Reality

• For the format that has proven most popular (P2P, roster-based games), the number of gaming opportunities tends to be much lower than casino, poker or even sportsbook gambling e.g. NFL DFS

• Acquisition costs are high and continue to rise; financial viability of industry run as it is today may not be possible

• Far more than poker and horse racing gambling, daily fantasy is significantly more conducive to players using automated software to optimize investments; may drive casual players away

Risks: Attrition

• DFS sites, like other online properties highly sensitive to network and liquidity effects (eBay, poker), will tend to compete entirely on customer acquisition spend until one company “wins”

• Both poker and horse racing have shown that bad players (the “fish”, due to the skill gap vs. the good players) cannot and will not sustain losing large sums of money forever

• Good players must have enough of an edge over the competition to compensate for any effective rakes.

• Attrition takes place when the bad players leave, leaving a proportionally larger pool of higher-skill players whose competitiveness cannot compensate for the rake.

• DFS may accelerate this attrition due to the nature of it being primarily a data-driven competition, conducive to automated, technical tooling for placing highly-optimal investments.

• Bad/casual players will not be able to compete; either the rake would need to be reduced (affecting revenue) or handle decreases (as volume players reduce investments, also impacting revenue)