daily score region visit report sarawak visit

TRANSCRIPT

PP10551/09/2012 (030567) 12 September 2012

See important disclosures at the e

OSK Research | See important disclosures at the end of this report 1

nd of this publication

OSK Research

MALAYSIA EQUITY Investment Research

Daily

SCORE Region Visit Report Ng Sem Guan, CFA +60 (3) 9207 7633 [email protected]

SARAWAK VISIT Ahmad Maghfur Usman +60 (3) 9207 7654 [email protected]

SCORE Thrives on Renewable Power

Kong Heng Siong +60 (3) 9207 7666 hengsiong.kong@ my.oskgroup.com

The inception of the “Sarawak Corridor of Renewable Energy” (SCORE) in 2008

has transformed the state. As a major initiative to develop the state’s central

region, SCORE aims to propel the state’s ambition to become a developed state

by 2020. Its goal is to accelerate the state's economic growth as well as improve

its people’s quality of life by capitalising on renewable energy. Last week (5-7

Sept 2012), we brought 18 clients on a trip to “Ground Zero” – Bintulu in

Sarawak – as well as Samalaju Industrial Park. The visit was an eye-opener as

we witnessed the region’s rapid development, confirming our view that

opportunities abound in the energy-rich state, particularly in renewable energy.

Gan Jian Bo +60 (3) 9207 7621 jianbo.gan@ my.oskgroup.com

Jerry Lee +60 (3) 9207 7622 jerry.lee@ my.oskgroup.com

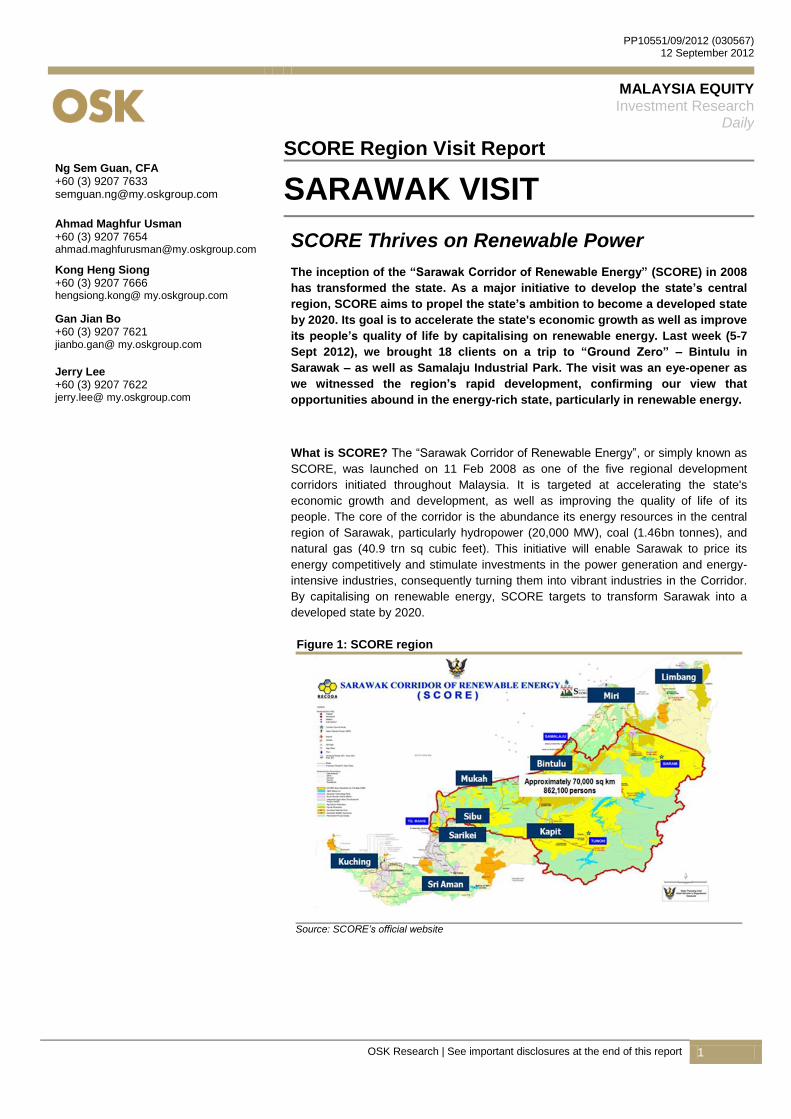

What is SCORE? The “Sarawak Corridor of Renewable Energy”, or simply known as

SCORE, was launched on 11 Feb 2008 as one of the five regional development

corridors initiated throughout Malaysia. It is targeted at accelerating the state's

economic growth and development, as well as improving the quality of life of its

people. The core of the corridor is the abundance its energy resources in the central

region of Sarawak, particularly hydropower (20,000 MW), coal (1.46bn tonnes), and

natural gas (40.9 trn sq cubic feet). This initiative will enable Sarawak to price its

energy competitively and stimulate investments in the power generation and energy-

intensive industries, consequently turning them into vibrant industries in the Corridor.

By capitalising on renewable energy, SCORE targets to transform Sarawak into a

developed state by 2020.

Figure 1: SCORE region

Source: SCORE’s official website

OSK Research

OSK Research | See important disclosures at the end of this report 2

A focus on private investment. Private investments in priority industries and their associated

downstream value-added economic activities will be the driving force behind SCORE‟s growth and

development. Chief among these are the energy-intensive industries, which will spur investments from an

early stage to become an advanced industrial base in the Corridor. Ten priority industries have been

indentified, namely aluminium, glass, steel, oil-based, palm oil, fishing & aquaculture, livestock, timber-

based, marine, and tourism.

Five growth nodes. Tanjung Manis, Mukah, Samalaju, Baram and Tunoh have been selected as the five

New Growth Nodes with different focus areas:

i. The Mukah Node will be developed into a Smart City and serve as the nerve centre for the

Corridor.

ii. The Tanjung Manis Node will be developed into an Industrial Port City and Halal Hub.

iii. The Samalaju Node will become the new Heavy Industry Centre.

iv. Baram and Tunoh will focus on the tourism and resource-based industries.

The spatial development of the entire region, as well as the development of these New Growth Nodes, will

also benefit the Corridor‟s Secondary Growth Centres, such as Semop, Balingian, Selangau, Samarakan,

Bakun and Ng. Merit.

Bintulu central to our event. The once sleepy fishing village of Bintulu has swiftly transformed into a

booming industrial centre and a soon-to-be capital for energy-intensive industries in Malaysia. The

Samalaju Industrial Park, being only an hour and a half‟s drive away from Bintulu Airport, led us to decide

to host our SCORE corporate event there.

OSK Research

OSK Research | See important disclosures at the end of this report 3

Day 1: The journey begins

A three-day excursion to Bintulu. Inspired by SCORE‟s prospects and eager that the investment

community witnesses Sarawak‟s abundant energy resources, particularly in renewable energy, we took 18

of OSK‟s clients on a three-day excursion to “Ground Zero”, i.e. Bintulu, in Sarawak. The following

chronicles our journey through the 5-7 Sept outing, as well as the new discoveries we made during the trip.

Samalaju, here we come. On 5 Sept 2012, we left for Bintulu, which took 2 hours of flight time from the

Kuala Lumpur International Airport. We were greeted by an OSK East Malaysia representative and boarded

a coach towards Samalaju Industrial Park. Our ride which passed through oil palm estates was on

reasonably well-paved two-lane tar roads. Although telecommunications reception was intermittent, we

were amazed with the strength of our 3G connection as we approached the industrial park.

Figure 2: Samalaju Industrial Park

Source: SCORE Official Website

Two nearly ready, two still in progress. As we entered Samalaju Industrial Park, we were surprised to

find that the first phase of Tokuyama Corp‟s polycrystalline plant producing silicon for solar panels was

almost complete though it is only scheduled for commissioning in 2Q13. Moreover, structural works on the

second phase of the plant seemed to have begun. Tokuyama is the Park‟s first foreign investor. We also

caught sight of Press Metal‟s aluminium smelting plant, which also looked ready judging from the outer

facade though a source on the ground told us that it is only scheduled for commissioning next year. Aside

from these, the Australian Securities Exchange-listed OM Holdings Ltd (OMH) and Asia Mineral Ltd have

each separately planned to set up a manganese smelter under the SCORE initiative. As we passed by two

adjacent sites, we noticed that land clearing was well in progress on both and structural works could

commence soon. Meanwhile, we also understand that the water supply and power grids connecting Bakun

Dam to Samalaju are now ready.

Company Investment

(RMbn) Product

Construction

Schedule

Production

Schedule Jobs Land (ha)

Electricity

(MW)

Press Metal 2.00 Aluminium ingots & billets Q1 2011 Q4 2012 2000 194 480

Tokuyama Corporation 6.60 Polycrystalline Silicon Q1 2011 Q3 2013 660 200 360

Asia Minerals Ltd 0.49 Silicone Manganese Q32011 Q4 2012 300 200 350

OM Holdings Ltd 1.50 Silicone Manganese Q2 2011 Q22013 1000 60 500

TOTAL 10.6 3960 654 1690

Source: RECODA

OSK Research

OSK Research | See important disclosures at the end of this report 4

Figure 3: Construction sites at Samalaju Industrial Park

Tokuyama Plant- Phase 1

Tokuyama Plant – Phase 2

Press Metal Plant

OM Holdings

Source: OSK Research

Quick tour of Cahya Mata Sarawak (CMS) Workers’ camp. Our first stop was at Samalaju Property

Development‟s (SPD) Samalaju Workers Camp. Its General Manager Mr. Goh Chii Yew showed us around

the RM40m site, touted as the best of its kind in Malaysia. It accommodates about 5,000 people, with a

majority working for Tokuyama. Accommodation costs vary from RM1,000 per month to as high as

RM5,000 per month. According to management, expansion plans are already in place to cope with rising

demand from Tokuyama, which will require 8,000 site workers at the peak of its construction cycle.

Meanwhile, we understand that the OM Materials and AML manganese ferro alloy plants were currently in

its land-clearing stage. We were impressed by the facilities and services provided at this camp,

notwithstanding the temporary unpaved road linking the site to the main road as proper road connections

are supposed to provided by the Government.

Figure 4: CMS workers’ camp

Executive lounge

Construction workers‟ camp

Source: OSK Research

OSK Research

OSK Research | See important disclosures at the end of this report 5

Samalaju Port. The opportunities in broadening the Corridor‟s industrial and economic base are in the

resource-based industries and the provision of modern services. Samalaju Port SB was established to

facilitate the cargo handling needs of Samalaju‟s industrial development, which may give rise to demand

for 13m-14m in tonnage by 2015. The visit kicked off with a briefing from Samalaju Port, followed by a

tour of the actual prospective site, on which some dredging works are currently being carried out.

Figure 5: Samalaju Port construction site

Construction site

Dredging works

Construction site

Construction site

Source: OSK Research

End of Day 1. Our road trip back to Bintulu town was rather smooth, taking slightly more than an hour.

There were numerous vehicles, including some buses, travelling in the same direction. We believe the

buses may be ferrying workers returning to Bintulu. We think it is just a matter of time before the

Government is forced to upgrade the road. The expansion of the Kidurong-Samalaju road is already in the

pipeline, with four new “no overtaking” lanes (each stretching 1km and located at every 5km interval), at a

total estimated cost of RM20m. Finally, after a long and tiring day, the entire party checked into the New

World Suites Hotel for a quick change of clothes before proceeding to a seafood dinner near the hotel.

OSK Research

OSK Research | See important disclosures at the end of this report 6

Day 2: The SCORE conference

A successful conference. On the second day, we held a conference at New World Suites Hotel. We were

deeply appreciative of the participation from RECODA CEO Datuk Amar Wilson Baya Dandot, who gave

our clients first-hand insights into SCORE, including its latest developments and challenges. Six public

corporations directly or indirectly involved in SCORE also made presentations at our conference. These

included Cahya Mata Sarawak, Sarawak Oil Palms (SOP), Sarawak Cable and Shin Yang Shipping. Our

party asked questions relating to business opportunities, SCORE‟s viability and its implications on the

corporates showcased at the conference. The key takeaways from the companies‟ presentations are

included in the last section of this report.

Figure 6: Snapshots of the conference

RECODA

Cahya Mata Sarawak

Sarawak Oil Palms

Shin Yang Shipping Corporation

Sarawak Cable

The attendees

Source: OSK Research

OSK Research

OSK Research | See important disclosures at the end of this report 7

Day 3: The adventure continues

Visit to Bintulu Port. Day 3 (7 Sep 2012) began with us checking out from our hotel. Our visit to Bintulu

Port kicked off with a quick presentation and Q&A session hosted by the company secretary of Bintulu Port

Holdings En. Nik Abd Rahman Nik Ismail, who briefed us on the group‟s operations, its future expansion

plans and latest corporate developments.

Figure 7: Bintulu Port visit

A meeting session

Aerial view of Bintulu Port

Source: OSK Research

Getting up close by boat. In order to experience and view the port operation up-close, Bintulu Port

graciously arranged a ride on the company‟s tug boat. From the vessel, we watched the loading of LNG

onto a MISC-owned vessel while being served light refreshments. Before the tour ended, our boat took us

close to the general cargo terminal, where we saw a few cargo container vessels berthed at the wharf.

Figure 8: Boat ride tour

The visiting party

On board

View from the boat

A view of Bintulu Port

Source: OSK Research

OSK Research

OSK Research | See important disclosures at the end of this report 8

Last stop - a palm oil refinery. Our group also visited SOP‟s palm oil refinery plant located almost

adjacent to Bintulu Port. SOP‟s general plant manager and his crew brought us around the company‟s

1,500 tonne-per-day refinery and 500 tonne-per-day kernel crushing plant. Although the refinery was under

maintenance, the plant manager gave us a good description of the refining process – from CPO to refined

palm oil, refined palm olein and palm stearin. At the crushing plant, we saw palm kernels being transported

on a conveyor belt for processing into crude palm kernel oil and palm kernel meal, which are used as

substitutes for coconut oil and feedstock respectively.

Figure 9: SOP palm oil refinery plant visit

Kernel crushing plant

Palm oil refinery

Palm kernels

Inside the refinery

Inside the kernel crushing plant

Storage silos

OSK Research

OSK Research | See important disclosures at the end of this report 9

RECODA

Bringing it together. RECODA‟s role is defined by the Regional Corridors Development Authorities

Ordinance 2006, which was passed by the Sarawak State Legislative Assembly on 11 Dec 2006. It is tasked

to manage, facilitate and promote SCORE‟s development and service investors. We felt honoured indeed that

RECODA‟s management graciously delivered the conference‟s keynote address.

Figure 10: Institutional framework and role of RECODA

Source: SCORE Official Website

A clear role. RECODA is organised and managed with a clear commercial mindset focused on providing

world-class customer service by minimising public service bureaucracy. It operates as a one-stop agency for

investors. Its role includes:-

Managing and promoting the development of SCORE.

Ensuring more expeditious and efficient mobilisation of the State's natural resources, which include

water and hydro power, and optimising the use of these resources to facilitate the development of

SCORE.

Planning SCORE‟s development and implementing the corridor‟s plans and projects.

Servicing investor clients.

Strong commitment and vision. Datuk Amar Wilson is proud of the approximate RM24.6bn worth of private

investments that SCORE has attracted despite having only RM1.8bn of total public funding spent to date. This

represents a private:public investment ratio of 94:6, on top of the 14,000 jobs it has created. According to

Datuk Amar Wilson, by 2030 the central region of SCORE Corridor is envisioned become the state's primary

economic powerhouse and Sarawak will have achieved the level of development and quality of life of a

developed country. However, his presentation focused on the medium term, with 2008- 2015 as the

foundation-laying phase for the corridor. RECODA will focus on building critical mass and momentum to

stimulate development, implementing high-priority infrastructure projects and attracting high-priority trigger

projects. Meanwhile, the Government is committed to upgrading existing infrastructure, utilities and amenities

as well as constructing new ones to meet the needs and requirements of investors within the Corridor.

The Tanjung Manis Halal Hub – another area of development. RECODA also highlighted that some

77,000 ha of landbank in Tanjung Manis have been earmarked for upstream and downstream aquaculture

and agriculture investments, a development that we find interesting. This delta region is suitable for a wide

range of aquacultural and agricultural activities throughout the year, due to its moderate, warm climate with

minimal seasonal changes. There is also sufficient area to expand into or build a new port to ship produce.

Some 13 bridges have been built, cutting the Sibu-Tanjung Manis road travelling time from many hours

previously to only 45 minutes. Thus, we expect to see a hive of economic activity emerge in the upcoming

years.

OSK Research

OSK Research | See important disclosures at the end of this report 10

No fancy investment incentives, only cheaper power! We were stunned, and believed that many of our

clients felt the same way, when Datuk Amar Wilson said there are no specific incentives lined up for SCORE.

Nevertheless, applications for general incentives such as the Investment Tax Allowance (ITA) and Pioneer

Status (PS) can be sought from the Malaysia Industrial Development Authority (MIDA). Besides that, we

believe the cheap renewable energy made available to investors is competitive and compelling enough to

attract investments from heavy industry players to Sarawak.

OSK Research

OSK Research | See important disclosures at the end of this report 11

MALAYSIA EQUITY Investment Research

Daily Post-Visit Update

Kong Heng Siong +60 (3) 9207 7666 hengsiong.kong@ my.oskgroup.com Cahya Mata Sarawak

The Prodigal Son Returns

NOT RATED

Price RM3.28

BUILDING MATERIALS

Cahya Mata Sarawak manufactures building materials and offers construction services and software.

Stock Statistics

Bloomberg Ticker CMS MK Share Capital (m) 330.3 Market Cap (RMm) 1,083.4 52 week H│L Price (RM) 3.50 1.70 3mth Avg Vol („000) 279.9 YTD Returns 56.9 Beta (x) 0.92

Major Shareholders (%)

Alwee Alsree Syed Ahmad 13.8 Majaharta SB 13.6 Lejla Taib 11.2

Share Performance (%)

Month Absolute Relative 1m 11.9 14.1 3m 41.1 29.1 6m 41.7 28.7 12m 71.7 44.1

6-month Share Price Performance

2.30

2.50

2.70

2.90

3.10

3.30

3.50

Mar-12 Apr-12 May-12 Jun-12 Jul-12 Jul-12 Aug-12

Cahya Mata Sarawak (CMS), one of Sarawak’s largest public-listed

conglomerates, began as a cement manufacturer in 1974. It has diversified into

sectors such as building materials, construction, road maintenance, property

development, financial services and education. The company’s major

shareholders linked to Sarawak Chief Minister Pehin Sri Haji Abdul Taib

Mahmud’s family (42.7%) and Sarawak Economic Development Corp (8.2%).

Given its dominance in Malaysia’s largest state, we expect CMS to play a crucial

role in driving SCORE’s developments, where its involvement is via 51%-owned

Samalaju Property Development (SPD) and a 20%-owned OM Materials Ltd plant.

Workers camp an eye-opener. We visited SPD‟s Samalaju Workers Camp and were

shown around by its General Manager Mr. Goh Chii Yew. Touted as the best of its kind

in Malaysia, the RM40m site now accommodates 5,000 people. The majority of these

work with Tokuyama Corp, which has invested USD2.5bn in a polycrystalline silicon

plant, to be built in two phases in Samalaju Industrial Park (SIP). Accommodation

charges range from RM1,000 per month for a site worker to RM5,000 per month for an

executive. Expansion plans are already in place to cope with rising demand from

Tokuyama, which will need 8,000 workers at the peak of its construction cycle.

Meanwhile, the construction progress at OM Materials‟ and AML‟s manganese

ferroalloy plants is also gaining pace.

Best proxy to Samalaju’s property play. Tipped to be the master developer of the

planned Samalaju township, SPD is currently looking at developing over 3,300 acres of

land about 12km away from SIP. Although the project‟s GDV is not known for now, we

understand that the construction of its first phase, done over 1,300 acres, will likely kick

off next year. This township is targeted to have a population of at least 45,000 by 2018.

20% share in OM Minerals. CMS holds a 20% stake in OM Materials‟ proposed

USD600m manganese ferroalloy plant in SIP, with the remaining 80% held by

Australia‟s OM Holdings, one of the world‟s largest manganese ore producers. Upon

completion, the plant is expected to produce 575,000mt of manganese and ferroalloy

p.a. Site preparation works for the manganese and ferroalloy smelter is nearing

completion and construction works will commence in 3Q12 with operations expected to

come on-stream by 1Q14.

FYE Dec (RMm) FY07 FY08 FY09 FY10 FY11

Turnover 2,552.5 893.0 874.6 943.5 1,012.6 Net Profit 388.2 95.8 41.0 65.8 120.0 % chg YoY 5554.3 -75.3 -57.2 60.5 82.5 Consensus - - - - - EPS (sen) 117.8 29.1 12.4 20.0 36.4 DPS (sen) 15.0 5.0 5.0 10.0 15.0 Div Yield 4.6% 1.5% 1.5% 3.1% 4.6% ROE 31.3% 7.7% 3.2% 5.0% 8.5% ROA 13.9% 4.1% 1.8% 3.1% 5.7% PER (x) 2.8 11.2 26.1 16.3 8.9 BV/ share 3.76 3.79 3.88 3.98 4.29 P/BV (x) 0.9 0.9 0.8 0.8 0.8

OSK Research

OSK Research | See important disclosures at the end of this report 12

Spill-over from SCORE projects. Although CMS is not actively involved in SIP‟s construction projects,

we see potential growth for its cement, clinker and concrete products as well as its construction

materials manufacturing divisions. It is the sole player in Sarawak for the former two industries and has

a 60% market share in the latter. In view of the increasing demand, CMS has proposed building a new

cement plant in Mambong by end-2014 and potentially, a second steel wires and mesh plant in Bintulu.

EARNINGS FORECAST

FYE Dec (RMm) FY07 FY08 FY09 FY10 FY11

Turnover 2,552.5 488.3 581.5 668.2 685.8 EBITDA 130.3 231.0 145.3 159.1 247.5 PBT 887.4 150.6 98.5 118.8 178.7 Net Profit 388.2 73.4 87.3 100.1 107.8 EPS (sen) 117.8 12.6 15.0 17.2 18.5 DPS (sen) 15.0 2.1 2.5 3.4 3.7 Margin EBITDA 5.1% 47.3% 25.0% 23.8% 36.1% PBT 34.8% 30.8% 16.9% 17.8% 26.1% Net Profit 15.2% 15.0% 15.0% 15.0% 15.7% ROE 31.3% 7.7% 3.2% 5.0% 8.5% ROA 13.9% 4.1% 1.8% 3.1% 5.7% Balance Sheet Fixed Assets 769.4 1,436.5 774.0 776.6 917.2 Current Assets 2,021.4 890.6 1,513.3 1,338.2 1,182.1 Total Assets 2,790.8 2,327.1 2,289.3 2,114.8 2,099.3 Current Liabilities 664.7 505.4 528.5 449.9 390.0 Net Current Assets 1,356.7 385.2 984.8 888.3 792.1 LT Liabilities 402.9 406.6 300.3 196.6 108.5 Shareholders Funds 1,238.2 1,248.8 1,278.0 1,312.7 1,414.8 Net Gearing 24.0% 24.2% 7.5% Net Cash 2.0%

OSK Research

OSK Research | See important disclosures at the end of this report 13

MALAYSIA EQUITY Investment Research

Daily Post-Visit Update

Gan Jian Bo +60 (3) 9207 7621 jianbo.gan@ my.oskgroup.com Sarawak Oil Palms

Set to Reap Future Rewards

BUY

Fair Value RM9.37 Previous RM9.37 Price RM6.41

PLANTATION

Sarawak Oi l Palms is primarily involved in oil palm plantations, with all its production area based in the state of Sarawak.

Stock Statistics

Bloomberg Ticker SOP MK Share Capital (m) 436.5 Market Cap (RMm) 2,797.9 52 week H│L Price (RM) 7.04 3.73 3mth Avg Vol („000) 115.9 YTD Returns 14.7 Beta (x) 0.85

Major Shareholders (%)

Shin Yang Group 36.2 PELITA Holdings 28.9

Share Performance (%)

Month Absolute Relative 1m -4.2 -2.3 3m 7.3 3.9 6m 10.2 7.1 12m 53.2 38.5

6-month Share Price Performance

5.50

5.70

5.90

6.10

6.30

6.50

6.70

6.90

7.10

7.30

7.50

Mar-12 Apr-12 May-12 Jun-12 Jul-12 Jul-12 Aug-12

SOP recently built its fourth palm oil refinery in Bintulu as it seeks to move across

the value chain. The facility will help ease the company’s CPO backlog as refining

capacity remains inadequate in Sarawak. While Malaysia’s refining landscape

remains challenging, we believe that an integrated business model like SOP’s will

better position the company in weathering any difficulties, as opposed to being

downstream-heavy. SOP remains our top Malaysian plantation pick, with its young

tree age profile and strong management expertise as the key drivers of growth for

the next few years. Maintain BUY, with a FV of RM9.37.

Solely Sarawak-focused. Sarawak Oil Palms (SOP) is a Sarawak-based oil palm

producer with the majority of its plantations located near Miri and Bintulu. Previously, the

company only focused on cultivating and harvesting oil palms and processing fresh fruit

bunches into crude palm oil and palm kernel. It has now ventured downstream,

beginning with the construction of a 1,500-tonne per day refinery and a 500-tonne per

day kernel crushing plant in Bintulu, Sarawak. The company has a sizeable planted area

of 62,948 ha, with 68.2% of its trees at or below 10 years old.

Going downstream in the state’s deepest port. SOP‟s Bintulu refinery commenced

operations in June, processing its own CPO as well as those from neighbouring millers

into refined, edible palm olein and stearin. Following a briefing on the refinery‟s structure,

the plant managers gave us a quick tour of the company‟s automated refinery and

mechanical kernel crushing plant. The processing of crude to its ultimate refined form at

temperatures of as high as 260ºC takes approximately 1.5 hours. It takes a full day to

warm up the refinery and another day to shut down the plant. The refinery, thus, runs

around the clock, with scheduled periodic shutdowns for maintenance.

Buying over minorities. SOP‟s strategy is to venture upstream in collaboration with its

major stakeholders Shin Yang and PELITA, a Sarawak state agency. The company

currently owns 60%-85% stakes in the estates under its care. Plans are now under way

for it to buy over the minority stakes, which will help reduce the minority interest leakage

on its profits. SOP prefers to transact in cash, although some parties prefer to be paid in

shares in order to remain invested in the company.

Maintain BUY. We value SOP at a FV of RM9.37, based on 13.0x FY13 PE. SOP

remains our top Malaysian plantation pick given its young tree age profile,

attractive valuations and strong management expertise. The stock is trading at

undemanding 12.8x and 9.1x FY12f and FY13f PEs.

FYE Dec (RMm) FY09 FY10 FY11 FY12f FY13f

Revenue 533.3 725.4 1166.3 2120.1 3171.8 Net Profit 100.0 147.2 243.0 222.6 314.1 % chg y-o-y -30.1 47.1 65.1 -8.4 41.1 Consensus 223.5 290.5 EPS (sen) 23.4 34.3 56.1 51.1 72.0 DPS (sen) 3.0 4.0 5.0 4.5 6.4 Dividend yield (%) 0.5 0.6 0.8 0.7 1.0 ROE (%) 12.1 15.1 20.1 15.7 18.5 ROA (%) 7.1 8.8 11.8 9.2 10.7 PER (x) 27.4 18.7 11.4 12.6 8.9 BV/share (RM) 1.9 2.2 2.8 3.2 3.9 P/BV (x) 3.4 2.9 2.3 2.0 1.6

OSK Research

OSK Research | See important disclosures at the end of this report 14

EARNINGS FORECAST

FYE Dec (RMm) FY09 FY10 FY11 FY12f FY13f

Turnover 533.3 725.4 1166.3 2120.1 3171.8 EBITDA 178.9 269.7 417.6 395.5 541.6 PBT 134.8 219.6 362.4 326.2 460.2 Net Profit 100.0 147.2 243.0 222.6 314.1 EPS (sen) 23.4 34.3 56.1 51.1 72.0 DPS (sen) 3.0 4.0 5.0 4.5 6.4 Margin EBITDA (%) 33.5 37.2 35.8 18.7 17.1 PBT (%) 25.3 30.3 31.1 15.4 14.5 Net Profit (%) 18.8 20.3 20.8 10.5 9.9 ROE (%) 12.1 15.1 20.1 15.7 18.5 ROA (%) 7.1 8.8 11.8 9.2 10.7 Balance Sheet Fixed Assets 1017.7 1184.2 1386.8 1583.8 1835.6 Current Assets 395.6 480.5 665.2 843.3 1091.5 Total Assets 1413.3 1664.7 2052.0 2427.1 2927.1 Current Liabilities 163.1 197.7 230.4 360.4 535.1 Net Current Assets 232.5 282.8 434.8 483.0 556.4 LT Liabilities 326.7 370.5 480.7 501.0 509.0 Shareholders Funds 828.8 974.2 1211.2 1414.1 1700.2 Net Gearing (%) net cash net cash net cash net cash net cash

OSK Research

OSK Research | See important disclosures at the end of this report 15

MALAYSIA EQUITY Investment Research

Daily Post-Visit Update

Ng Sem Guan, CFA +60 (3) 9207 7633 [email protected]

Sarawak Cable

Cabling New Territory

NOT RATED

Price RM1.57

BUILDING MATERIALS

Sarawak Cable manufactures power cables and wires and also hybrid power inverters.

Stock Statistics

Bloomberg Ticker SRCB MK Share Capital (m) 135.0 Market Cap (RMm) 212.0 52 week H│L Price (RM) 2.24 1.48 3mth Avg Vol („000) 27.2 YTD Returns -20.3 Beta (x) 0.84

Major Shareholders (%)

Sarawak Energy Bhd 21.6 Bekir Taib Mahmub Abu 19.4 Leader Universal Holdings 15.5

Share Performance (%)

Month Absolute Relative 1m -9.8 -8.0 3m -5.8 -9.7 6m -19.2 -22.0 12m -16.1 -25.6

6-month Share Price Performance

1.50

1.60

1.70

1.80

1.90

2.00

2.10

Mar-12 Apr-12 May-12 Jun-12 Jul-12 Jul-12 Aug-12

Sarawak Cable (SCB) is transforming from a pure cable and wire manufacturer

into a one-stop centre, which enables it to access the power transmission

industry’s value chain and to tap into SCORE’s abundant but under-utilised

energy resources. The company has acquired STSB, which offers exposure to

fabricating and galvanising transmission towers and other steel products, as well

as TISB, a contractor for transmission lines. SCB also expects a new income

stream from mini hydro power generation starting 2014 via 65%-owned PT Inpola

Mitra Elektrindo.

Laying cables across East Malaysia. SCB, listed on Bursa Malaysia‟s Main Board on

25 May 2010, is a manufacturer of aluminium and copper cables and wires based in

Kuching, Sarawak. Given its high exposure in the East Malaysian market, the company

controls roughly a third of the region‟s market share and offers products that include low

voltage power cables and high voltage bare conductors.

A one-stop power transmission centre. Post-listing, SCB acquired 75% of Sarwaja

Timur SB (STSB) and is now in the midst of acquiring the remaining 25% for RM11.3m.

Separately, SCB has also proposed to acquire full interest in Trenergy Infrastructure SB

(TISB) for RM65m. STSB is involved in the fabrication of transmission towers and other

steel products and also provides galvanising services, while TISB is an EPC contractor

for transmission lines. The acquisition will benefit SCB in terms of synergy and also

facilitate the creation of a one-stop centre for power transmission projects. The company

is also expanding overseas by acquiring a 65% stake in PT Inpola Mitra Elektrindo

(IME), which has been awarded a 20-year Power Purchase Agreement (PPA) for a 11

MW mini hydro power plant. Construction is expected to begin this year and complete in

2014.

More from SCORE. Other than the 2,400MW Bakun dam that has its power

transmission line and substation at Samalaju Industry park, there are many untapped

energy resources amounting to 28,000 MW in the corridor. With SCORE‟s development

picking up speed, the region is expected to be a hive of activity going forward. SCB, a

homegrown player, is likely to be a frontrunner for any power transmission projects, as

its new one-stop centre gives the group access to the power transmission industry‟s

entire value chain. The company‟s orderbook, including that of TISB‟s (whose acquisition

is expected to be completed by end-2012), totals RM292m.

FYE Dec (RMm) FY07 FY08 FY09 FY10 FY11

Revenue 104.07 135.7 89.8 129.5 368.3 Net Profit 11.3 8.78 8.1 5.5 15.6 % chg y-o-y - -22.3 -7.7 -32.1 183.6 Consensus - - - - - EPS (sen) 0.11 0.08 0.08 0.05 0.12 DPS (sen) 0.00 0.00 0.00 0.00 0.028 Dividend yield (%) 0.00 0.00 0.00 0.00 1.8% ROE (%) n.m. n.m. n.m. 5.90 13.80 ROA (%) n.m. n.m. n.m. 3.30 6.00 PER (x) 14.3 19.6 19.6 31.4 13.1 BV/share (RM) n.m. n.m. 0.74 0.79 0.89 P/BV (x) n.m. n.m. 2.12 1.99 1.76

OSK Research

OSK Research | See important disclosures at the end of this report 16

EARNINGS FORECAST

FYE Dec (RMm) FY07 FY08 FY09 FY10 FY11

Turnover 104.1 135.7 89.8 129.5 368.3

EBITDA 11.6 9.5 13.9 8.1 8.1

PBT 11.0 10.9 10.5 7.9 24.3

Net Profit 11.3 8.8 8.1 5.5 15.6

EPS (sen) 0.11 0.08 0.08 0.05 0.12

DPS (sen) n.m. n.m. 0.03 0.03 n.m.

Margin EBITDA (%) 11.1% 7.0% 15.5% 6.3% 2.2%

PBT (%) 10.6% 8.0% 11.7% 6.1% 6.6%

Net Profit (%) 10.9% 6.5% 9.0% 4.2% 4.2%

ROE (%) n.m. n.m. n.m. 5.9 13.8

ROA (%) n.m. n.m. n.m. 3.3 6.0

Balance Sheet Fixed Assets n.m. n.m. 34.7 55.2 56.5

Current Assets n.m. n.m. 53.39 177.5 210.2

Total Assets n.m. n.m. 90.88 241.7 274.6

Current Liabilities n.m. n.m. 9.0 117.9 135.8

Net Current Assets n.m. n.m. 44.43 59.6 74.4

LT Liabilities n.m. n.m. 2.2 5.9 6.0

Shareholders Funds n.m. n.m. 53.5 78.1 78.1

Net Gearing (%) n.m. n.m. n.m. Net Cash 21.2

OSK Research

OSK Research | See important disclosures at the end of this report 17

MALAYSIA EQUITY Investment Research

Daily Post-Visit Update

Jerry Lee +60 (3) 9207 7622 jerry.lee@ my.oskgroup.com Shin Yang Shipping Corp

On Expansion Mode

NOT RATED

Price RM0.405

TRANSPORT

Shin Yang Shipping Corp (SYS) is a leading integrated shipping and shipbuilding company based in Sarawak.

Stock Statistics

Bloomberg Ticker SHIN MK Share Capital (m) 1,200.0 Market Cap (RMm) 486.0 52 week H│L Price (RM) 0.68 0.40 3mth Avg Vol („000) 297.1 YTD Returns -8.0 Beta (x) 0.56

Major Shareholders (%)

Shin Yang Holdings SB 55.0

Share Performance (%)

Month Absolute Relative 1m -4.7 -4.0 3m -8.9 -13.0 6m -18.0 -20.8 12m -13.9 -25.5

6-month Share Price Performance

0.40

0.42

0.44

0.46

0.48

0.50

0.52

0.54

Mar-12 Apr-12 May-12 Jun-12 Jul-12 Jul-12 Aug-12

Shin Yang Shipping Corporation (SYSCorp) is well-positioned to benefit from the

busy transportation route between East and West Malaysia. It has expanded to the

Middle East by entering into joint ventures with local partners. Having secured an

order book of 36 vessels worth RM800.6m, the company’s growth outlook is

positive. SYSCorp has also acquired eight container vessels from Swee Joo to

expand its shipping routes.

Venturing beyond borders. A part of Shin Yang Group, SYSCorp is involved in

shipping and shipbuilding. It was listed on Bursa Malaysia‟s main market on 23 June

2010, with an IPO market cap of RM1.32bn. Its shipping divisions have a total of 297

vessels and a total gross registered tonnage of 460,100 tonnes. The company has

expanded to the Middle East by entering into joint ventures with several companies in

Qatar, Sharjah, Abu Dhabi and Dubai. Its shipbuilding division has an orderbook to build

36 vessels worth RM800.6m, which should keep it busy for the next two years.

Consistent business growth. Apart from the vessels contract, SYSCorp has also

secured 7.7m tonnes of aggregate in UAE with Steven Rock LLC and inked a 20-year

contract with CMS Cement SB to transport cement. The company has new shipping

routes for its container vessels, transporting construction materials and household goods

to China, Bangkok and Penang. To date, it has 18 existing container vessels. Of this, six

will service routes between Peninsular Malaysia and Borneo; meanwhile, two vessels

are dedicated to intra-Asia (including China) routes but are not yet in operation as some

renovation needs to be done to cater for longer journeys.

Opportunities from SCORE. The extensive need to transport in- and out-bound raw

materials to and from the SCORE region will definitely present positive opportunities for

SYSCorp. Aside from that, Samalaju Port‟s construction works offer SYSCorp

opportunities to tap into the business of transporting raw materials from Bintulu Port to

Samalaju Industrial Park. As such, we think SYSCorp may be able to achieve new „high

scores, thanks to its strong presence in the corridor.

FYE Jun (RMm) FY07 FY08 FY09 FY10 FY11

Revenue 486.7 595.1 673.5 320.9 593.9 Net Profit 98.0 159.0 101.8 152.5 74.7 % chg y-o-y - 62.3 -36.0 49.9 -51.0 Consensus - - - - - EPS (sen) 0.1 0.16 0.1 0.23 0.06 DPS (sen) n.m. n.m. n.m. 0.03 0.02 Dividend yield (%) n.m. n.m. n.m. 13.5 20.25 ROE (%) n.m. n.m. n.m. 11.4 5.45 ROA (%) n.m. n.m. n.m. 8.8 3.45 PER (x) n.m. n.m. n.m. 1.8 6.8 BV/share (RM) n.m. n.m. 1.1 1.13 1.16 P/BV (x) n.m. n.m. 0.37 0.36 0.35

OSK Research

OSK Research | See important disclosures at the end of this report 18

EARNINGS FORECAST

FYE Jun (RMm) FY07 FY08 FY09 FY10 FY11

Turnover 486.7 595.1 673.5 320.9 593.9 EBITDA n.m. n.m. n.m. 211.1 169.0 PBT 103.5 156.6 112.7 156.4 71.6 Net Profit 98.0 159.0 101.8 152.5 74.7 EPS (sen) 0.1 0.16 0.1 0.23 0.06 DPS (sen) n.m. n.m. n.m. 0.03 0.02 Margin EBITDA (%) n.m. n.m. n.m. 65.8 28.5 PBT (%) n.m. n.m. n.m. 48.7 12.1 Net Profit (%) n.m. n.m. n.m. 47.5 12.6 ROE (%) n.m. n.m. n.m. 11.4 5.45 ROA (%) n.m. n.m. n.m. 8.8 3.45 Balance Sheet Fixed Assets n.m. n.m. n.m. 1406.2 1682.7 Current Assets n.m. n.m. n.m. 589.5 482.1 Total Assets n.m. n.m. 1323.1 2142.9 2190.5 Current Liabilities n.m. n.m. n.m. 481.41 423.5 Net Current Assets n.m. n.m. n.m. 108.1 58.6 LT Liabilities n.m. n.m. n.m. 294.1 366.7 Shareholders Funds n.m. n.m. 1323.1 1350.9 1390.2 Net Gearing (%) n.m. n.m. n.m. 19.8 29.9

OSK Research

OSK Research | See important disclosures at the end of this report 19

MALAYSIA EQUITY Investment Research

Daily Post-Visit Update

Ahmad Maghfur Usman +60 (3) 9207 7654 [email protected] Bintulu Port Holdings

Rising With Samalaju

NEUTRAL

Fair Value RM7.10 Previous RM7.10 Price RM7.01

LOGISTICS

Bintulu Port is a world class LNG port which also operates as a multipurpose port.

Stock Statistics

Bloomberg Ticker BPH MK Share Capital (m) 400.0 Market Cap (RMm) 2,808.0 52 week H│L Price (RM) 7.32 6.43 3mth Avg Vol („000) 69.9 YTD Returns 4.4 Beta (x) 0.37

Major Shareholders (%)

Petroliam Nasional Bhd 32.8 State Fin Secretary Sarawak 30.7 KWAP 9.8

Share Performance (%)

Month Absolute Relative 1m -0.4 1.5 3m 1.4 -2.1 6m 3.5 -1.7 12m 12.3 -3.9

6-month Share Price Performance

6.80

6.90

7.00

7.10

7.20

7.30

Mar-12 Apr-12 May-12 Jun-12 Jul-12 Jul-12 Aug-12

The hive of industrial development in Samalaju creates opportunities for players

to cater to increasing demand for cargo handling in the immediate to long term for

both the Samalaju and Bintulu ports. The two ports are expected to see increases

in cargo demand of 13m-14m tonnes and 100,000-TEUs by 2015. However, the

issue of cutting tariffs for its LNG berthing and lease payments is unresolved

while the terms of Samalaju’s concession are yet to be finalised. We maintain a

NEUTRAL call on Bintulu Port, with an unchanged FV of RM7.10, based on DDM.

On track. Samalaju Port‟s development is on track, with the construction of its two-barge

berths and a Ro Ro ramp targeted to be completed by June 2013, before the completion

of the port‟s first phase in 2016. Bintulu Port is allocating an initial capex of RM193m for

the two barge berths. While the combined development could exceed RM1bn, the bulk

of its capex will be used for land reclamation and dredging the water depth deeper from

7m-12m, in order to cater to Panamax vessels‟ requirements. The barge berths will be

able to handle a capacity size of 4m tonnes p.a. Phase 1 of Samalaju‟s development,

which is expected to complete by 1Q16, will see an additional three Panamax berths and

one barge berth and an additional capacity of 14m tonnes. Upon completion of Phase 1,

Samalaju will be able to accommodate a combined capacity of 18 million tonnes.

Capital structure and concession terms. Management will announce the concession

terms from Samalaju Port in due course. The capex funding is understood to be from

bond issuances, in addition to Bintulu Port receiving a RM500m grant from the federal

government.

Ongoing negotiations. The long-drawn negotiations on tariff reduction for LNG berthing

and annual leases are still inconclusive. At the same time, management is also lobbying

for tariff increases for both Bintulu and Samalaju ports to cushion the decline in revenue

from LNG berthing. Management expects a solution to be reached by the end of the

year. There are indications of a revenue downside of RM50m from the c. 17% reduction

in LNG berthing tariffs, but this may be offset by a c. 20% jump in revenue of RM20m

arising from the cuts in rental and port tariffs. Despite the reductions, management

intends to maintain the current dividend payout.

FYE Dec (RMm) FY10 FY11 FY12f FY13f FY14f

Revenue 455.0 483.9 506.4 531.8 594.9 Core Net Income 120.9 122.8 128.2 132.3 159.2 % y-o-y 1.58 4.42 3.17 20.39 Consensus 171.7 176.3 186.5 EPS (sen) 30.2 30.7 32.1 33.1 39.8 DPS (sen) 37.5 37.5 37.5 37.5 37.5 Dividend yield (%) 5.3 5.3 5.3 5.3 5.3 Core ROE (%) 18.9 18.6 19.1 19.2 21.8 Core ROA (%) 6.0 6.3 6.5 6.9 8.4 Core PER (x) 23.2 22.8 21.9 21.2 17.6 BV/share (RM) 1.6 1.7 1.7 1.7 1.8 P/BV (x) 4.4 4.2 4.2 4.1 3.8 EV/ EBITDA (x) 8.4 8.2 7.9 7.8 7.1

OSK Research

OSK Research | See important disclosures at the end of this report 20

Cargo flow. As only two barge berths will be completed by mid-2013, cargo flows into Samalaju Port will

mostly be via barges, and Bintulu Port will act as an import and export hub of raw materials and finished

goods respectively with truck haulage also playing a major role in moving cargo on land. Samalaju‟s

need for industrial cargo throughput in the near term (by 2014) is expected to be in the range of 8m

tonnes and roughly 30,000 TEUS of imports. Exports are expected to see an annual throughput of 3.5m

tonnes and 45,000 TEUS, which is smaller in tonnage size as most of these finished products are high-

value goods. The combined import and export tonnage from Samalaju‟s development alone is expected

to handle up to 14m-15m tonnes and 100,000 additional TEUS per annum by 2015. We understand that

that Bintulu Port will continue with container handling in the immediate and longer term as management

wishes to avoid any duplication. Come 2016 and upon the completion of Phase 1, the cargo flow from

Samalaju will mostly shift to Samalaju Port as its berths can accommodate Panamax vessels.

Maintain NEUTRAL. While we like Bintulu Port‟s prospects, there are still uncertainties in relation to its

tariff negotiations and the concession agreement for Samalaju Port. We maintain our NEUTRAL stance

on Bintulu Port, with an unchanged FV of RM7.10, based on DDM at 7.5% required return.

EARNINGS FORECAST

FYE Dec (RM’m) FY10 FY11 FY12f FY13f FY14f

Revenue 455.0 483.9 506.4 531.8 594.9

EBITDA 301.1 311.2 321.2 332.3 375.4 Depreciation and amortization -103.9 -110.9 -117.5 -123.4 -129.6 EBIT 197.2 200.4 203.7 209.0 245.9 Interest income 13.4 12.9 11.6 12.9 10.1 Finance costs -47.2 -44.6 -42.2 -42.4 -39.7 EI 1.3 -1.5 0.0 0.0 0.0 PBT 164.7 167.1 173.1 179.5 216.3 Tax -43.8 -10.9 -11.5 -13.7 -23.5 PAT 120.9 156.3 161.7 165.8 192.7 Core PAT excl tax credit 120.9 122.8 128.2 132.3 159.2

Core EPS 30.2 30.7 32.1 33.1 39.8 DPS 37.5 37.5 37.5 37.5 37.5 Margin (%) EBITDA 66.2 64.3 63.4 62.5 63.1 Core PBT 35.9 34.8 34.2 33.7 36.4 Core PAT 26.6 25.4 25.3 24.9 26.8 Core ROE (%) 18.9 18.6 19.1 19.2 21.8 Core ROA (%) 6.0 6.3 6.5 6.9 8.4 Assets Non Current Assets 1651.8 1569.2 1562.1 1567.7 1614.6 Current assets 378.5 366.0 396.6 340.3 270.7 Total assets 2030.3 1935.3 1958.7 1908.0 1885.3 Equity and liabilities Total equity 639.5 660.2 671.9 687.7 730.4 Non-current liabilities 1213.3 1133.9 1136.1 1059.0 980.7 Current liabilities 177.5 141.2 150.6 161.4 174.2 Total liabilities 1390.7 1275.0 1286.8 1220.4 1154.9 Total equity and liabilities 2030.3 1935.3 1958.7 1908.0 1885.3 Net Gearing Net Cash Net Cash Net Cash Net Cash Net Cash CFO 158.1 132.2 273.8 205.2 239.4 CFI -48.1 -8.1 -96.5 -115.2 -168.0 CFF -150.0 -150.0 -150.0 -150.0 -150.0 End Cash 273.7 247.8 275.2 215.2 136.5

OSK Research

OSK Research | See important disclosures at the end of this report 21

OSK Research Guide to Investment Ratings

Buy: Share price may exceed 10% over the next 12 months Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain Neutral: Share price may fall within the range of +/- 10% over the next 12 months Take Profit: Target price has been attained. Look to accumulate at lower levels Sell: Share price may fall by more than 10% over the next 12 months Not Rated (NR): Stock is not within regular research coverage

All research is based on material compiled from data considered to be reliable at the time of writing. However, information and opinions expressed will be subject to change at short notice, and no part of this report is to be construed as an offer or solicitation of an offer to transact any securities or financial instruments whether referred to herein or otherwise. We do not accept any liability directly or indirectly that may arise from investment decision-making based on this report. The company, its directors, officers, employees and/or connected persons may periodically hold an interest and/or underwriting commitments in the securities mentioned.

Distribution in Singapore

This research report produced by OSK Research Sdn Bhd is distributed in Singapore only to "Institutional Investors", "Expert Investors" or "Accredited Investors" as defined in the Securities and Futures Act, CAP. 289 of Singapore. If you are not an "Institutional Investor", "Expert Investor" or "Accredited Investor", this research report is not intended for you and you should disregard this research report in its entirety. In respect of any matters arising from, or in connection with, this research report, you are to contact our Singapore Office, DMG & Partners Securities Pte Ltd ("DMG").

All Rights Reserved. No part of this publication may be used or re-produced without expressed permission from OSK Research. Published by OSK Research Sdn. Bhd., 6th Floor, Plaza OSK, Jalan Ampang, 50450 Kuala Lumpur Printed by Xpress Print (KL) Sdn. Bhd., No. 17, Jalan Lima, Off Jalan Chan Sow Lin, 55200 Kuala Lumpur

OSK RESEARCH SDN. BHD. (206591-V) (A wholly-owned subsidiary of OSK Investment Bank Berhad)

Kuala Lumpur Hong Kong Singapore

Malaysia Research Office

OSK Research Sdn. Bhd.

6th Floor, Plaza OSK

Jalan Ampang

50450 Kuala Lumpur

Malaysia

Tel : +(60) 3 9207 7688

Fax : +(60) 3 2175 3202

OSK Securities

Hong Kong Ltd.

12th Floor,

World-Wide House

19 Des Voeux Road

Central, Hong Kong

Tel : +(852) 2525 1118

Fax : +(852) 2810 0908

DMG & Partners

Securities Pte. Ltd.

10 Collyer Quay

#09-08 Ocean Financial Centre

Singapore 049315

Tel : +(65) 6533 1818

Fax : +(65) 6532 6211

Jakarta Shanghai Phnom Penh

PT OSK Nusadana

Securities Indonesia

Plaza CIMB Niaga,

14th Floor,

Jl. Jend. Sudirman Kav. 25,

Jakarta Selatan 12920

Indonesia

Tel : (6221) 2598 6888

Fax : (6221) 2598 6777

OSK (China) Investment

Advisory Co. Ltd.

Room 6506, Plaza 66

No.1266, West Nan Jing Road

200040 Shanghai

China

Tel : +(8621) 6288 9611

Fax : +(8621) 6288 9633

OSK Indochina Securities Limited

No. 1-3, Street 271,

Sangkat Toeuk Thla, Khan Sen Sok,

Phnom Penh,

Cambodia

Tel: (855) 23 969 161

Fax: (855) 23 969 171

Bangkok

OSK Securities (Thailand) PCL 10th Floor ,Sathorn Square Office Tower,

98, North Sathorn Road,Silom, Bangrak, Bangkok 10500

Thailand Tel: +(66) 862 9999 Fax : +(66) 108 0999