dairy 2009 – situation & outlook industry briefing 22 may 2008 (final) 1 western victoria...

TRANSCRIPT

Dairy 2009 – Situation & Outlook

Industry briefing

22 May 2008 (final)

1

Western Victoria Roadshow

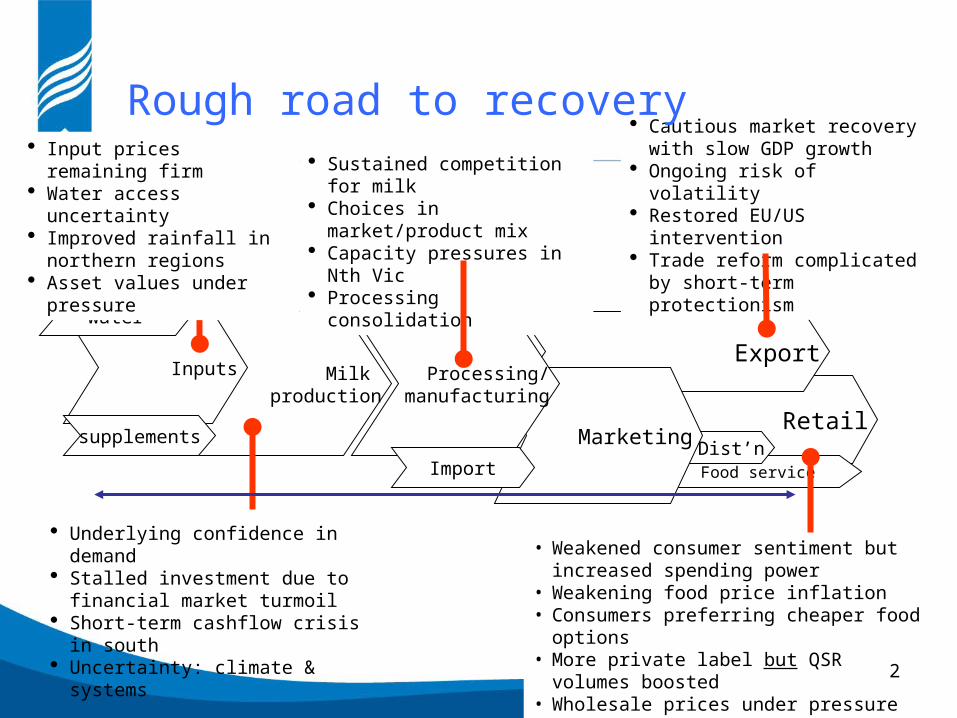

Retail

ExportMilk

production

Food serviceDist’n

Marketing

Processing/manufacturing

Import

Inputs

supplements

water

Sustained competition for milk

Choices in market/product mix

Capacity pressures in Nth Vic

Processing consolidation

• Weakened consumer sentiment but increased spending power

• Weakening food price inflation• Consumers preferring cheaper food

options • More private label but QSR volumes

boosted• Wholesale prices under pressure from

falling commodity prices

Cautious market recovery with slow GDP growth

Ongoing risk of volatility Restored EU/US intervention Trade reform complicated by

short-term protectionism

Rough road to recovery

Underlying confidence in demand

Stalled investment due to financial market turmoil

Short-term cashflow crisis in south

Uncertainty: climate & systems

Input prices remaining firm

Water access uncertainty Improved rainfall in

northern regions Asset values under

pressure

2

Effect of the GFC on global dairy market

3

DemandEconomic climate Supply

Recession in developed economies

Consumers trading-down dairy spend

Crop plantings harder to fund in some countries

Reduced milk supply expansion

Reduced demand volumes

Tightened credit markets

Initial limits on trade credit

High risk exposures for major banks

Rebalancing of dairy markets

Lower disposable incomes in

developing world

Firm grain/feed prices due to crop limits

Squeezed milk production margins

Reduced product prices

Build-up in dairy stocks

Buyer caution on volume & price

Unreliable climates

Supply response to high 2008 dairy prices

EU/US intervention

restored

Currency exchange rate volatility

Retail

ExportMilk

production

Food serviceDist’n

Marketing

Processing/manufacturing

Import

Feed production

supplements

water

The world market Cautious market recovery

with slow GDP growth Ongoing risk of volatility Restored EU/US intervention Trade reform complicated by

short-term protectionism

4

Stabilising international prices

5

What’s driving world markets?Supply• Developing supply response

to lower prices • Declining output in EU/US• Feed prices remaining firm

• Market intervention restored• EU subsidies• EU resisting further support

• Low product stocks (except cheese)

• Limited export availability from emerging low cost suppliers

• NZ supply continues to grow

Demand• Weak demand growth in

developing markets• Recession affecting important

markets• Lower cheese demand in

Japan • Lower butter and cheese for

Russia• Buyer caution with weakened

demand • Global economy near the

bottom

6

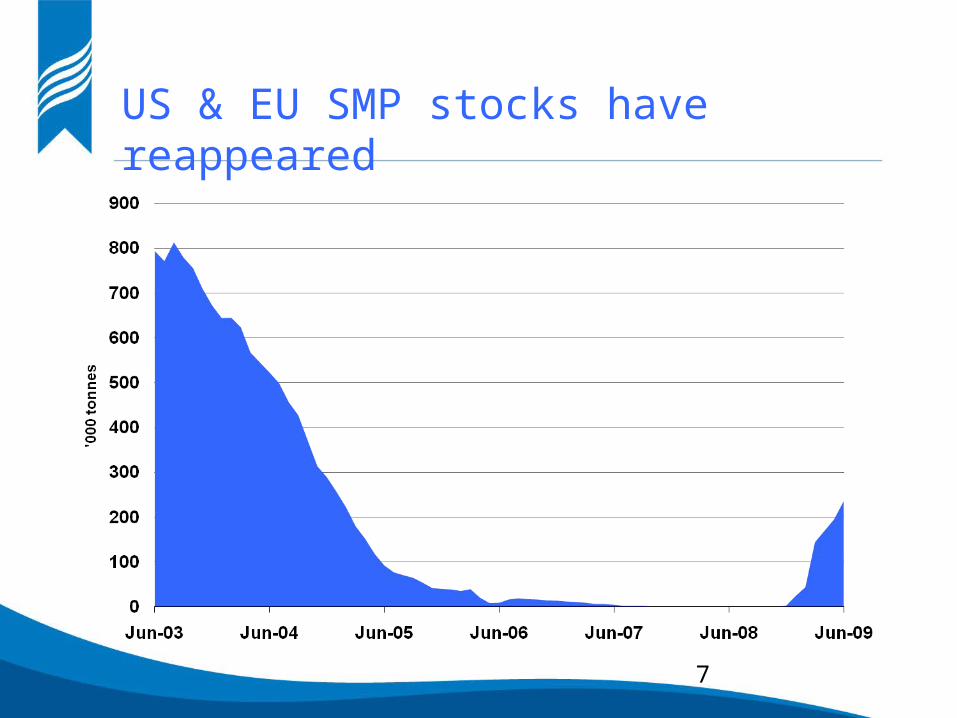

7

US & EU SMP stocks have reappeared

8

Impact of subsidiesClears domestic market•Support internal prices

Exporters seek a lower price•Returns topped up by subsidy•Limits ability of unsubsidised prices to rise in competition

Prevailing w

orld price

subsidy

Exporter offer price

New

world price

Major exporter production

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

EU

-27

US

NZ

Au

st

Arg

en

tin

a

Bra

zil

% c

hange

2007

2008

2009

World market outlookShort term• Short-term buyer caution

• Lack of transparency hinders stability

• Multiple influences on currency threaten returns

• Economic recovery in developing countries is crucial

• Supply response to low prices• Prices finding new levels

Medium term• Increased sources of volatility• Developing economies

underpin ongoing demand growth

• Outlook: Supply lower than demand growth

• Dairy maintains relativities with substitutes

Risks• Further intervention?• More protectionism?

10

Long range global outlook

Retail

ExportMilk

production

Food serviceDist’n

Marketing

Processing/manufacturing

Import

Feed production

supplements

water

The domestic market• Weakened consumer sentiment but

spending power boosted by better disposable incomes

• Weakening food price inflation• Consumers looking for value food

options • More private label but QSR sales

boosted

12

• Dairy sales proving resilient – good volume and value growth

• Wholesale prices under pressure from falling commodity prices

• Worsening economic conditions and rising unemployment encourage more “trading down”

• Value threatened but volume to remain stable

Domestic market a bright spot

13

0% 4% 8% 12% 16% 20%

Milk - Fresh

Milk - UHT

Cheese -cheddar

Cheese - Non-cheddar

Butter

Dairy blends

Volume

Value

Supermarket growth by categoryYr to May 2009

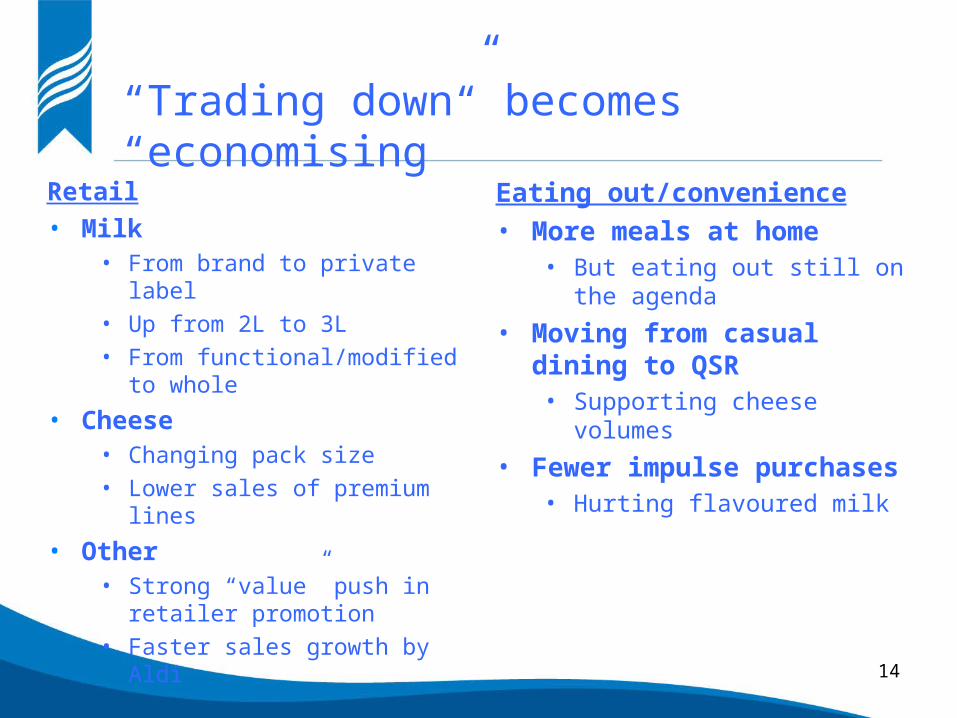

“Trading down” becomes “economising”

Retail• Milk

• From brand to private label

• Up from 2L to 3L

• From functional/modified to whole

• Cheese• Changing pack size

• Lower sales of premium lines

• Other • Strong “value” push in retailer

promotion

• Faster sales growth by Aldi

Eating out/convenience• More meals at home

• But eating out still on the agenda

• Moving from casual dining to QSR• Supporting cheese volumes

• Fewer impulse purchases• Hurting flavoured milk

14

Retail

ExportMilk

production

Food serviceDist’n

Marketing

Processing/manufacturing

Import

Feed production

supplements

water

Challenges from both sides

• Higher domestic share influencing milk value given price disparities

• Lack of milk growth sustains pressure on capacity

• Lower throughput will drive regional capacity restructuring

• Retailers driving supply chain cost reductions

Sustained competition for milk Choices in market/product mix Capacity pressures in Nth Vic Processing/marketing consolidation following

NatFoods merger with ACF

15

Shifting market mix• Home market more important with more of the milk?• Respective market/product returns evaluated

Australian industry market mix

16

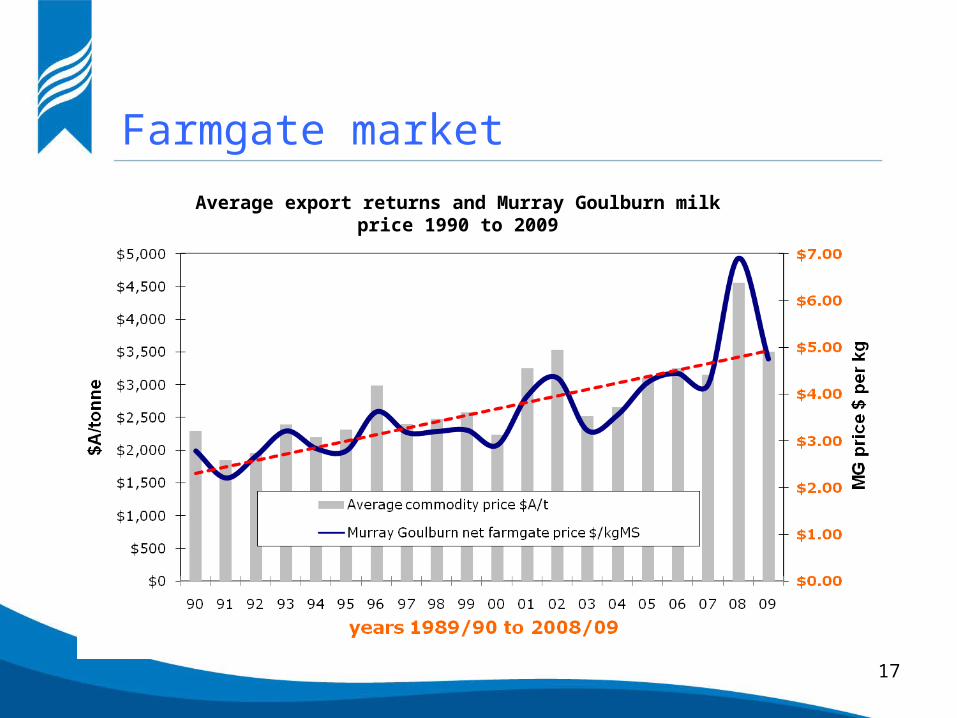

Farmgate market

Average export returns and Murray Goulburn milk price 1990 to 2009

17

Farmgate market outlook in 2009/10Southern:• Opening prices announced

• Indicative avge for Vic: $3.60kgMS, down 35%

• Lower end of DA forecast

• Full year outlook?• S & O forecast down by 10-15%

($4.00 to $4.60)• $A critical to final outcome,

commodity prices need to rise • Customers making shorter

commitments due to caution on market conditions

• Fresh milk processors will mark off manufacturers but conscious of supply risks

Fresh milk regions:• Security of year-round supply

remains the driver• Contract prices set in 2008

remain in place• Increased gap between

southern and NSW/Qld prices• Some prices under pressure

due to surplus milk at times• WA decline is stronger due to

production growth & market deterioration in commodities

18

Retail

ExportMilk

production

Food serviceDist’n

Marketing

Processing/manufacturing

Import

Feed production

supplements

water

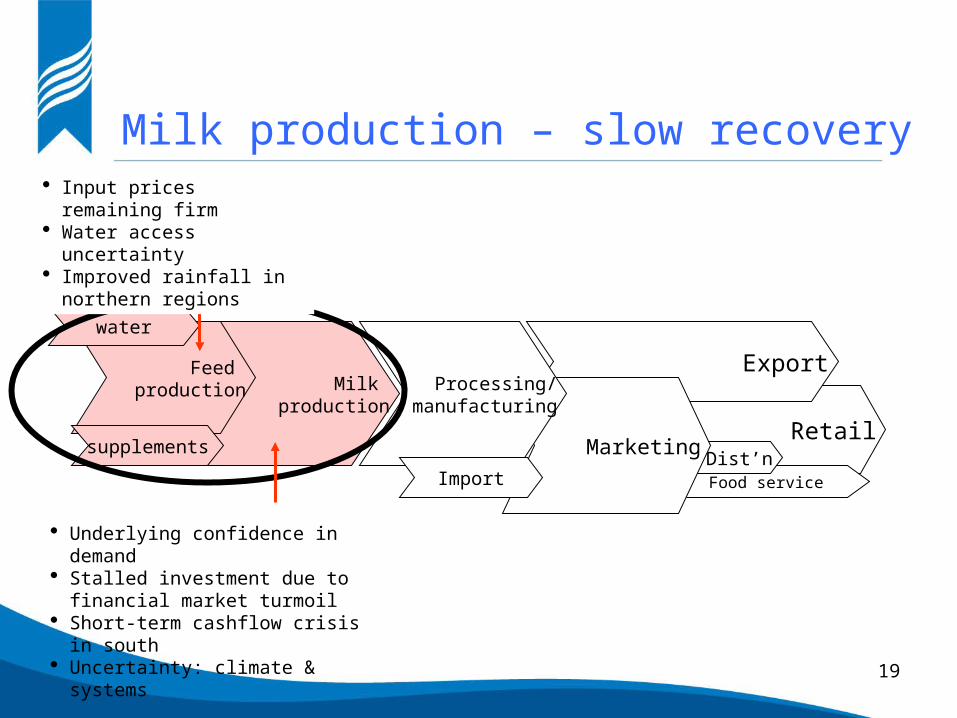

Milk production – slow recovery

Underlying confidence in demand

Stalled investment due to financial market turmoil

Short-term cashflow crisis in south

Uncertainty: climate & systems

Input prices remaining firm

Water access uncertainty Improved rainfall in

northern regions

19

National Dairy Farmer Survey• 6th year of NDFS survey

• 1,002 farmers interviewed• Similar to last year• 191 in Western Victoria

• Fieldwork conducted from mid-February to early March

• Response rate remained quite high at 72%

• 69% in 2008

• Follow-up survey planned for early September

0

50

100

150

200

250

NV

WV

Gip

ps

SE

Q

NS

W

FN

Q

Be

ga

SA

WA

Ta

s

20

Production sectoris a story of several industries

Where Short-term market outlook

Input costs Confidence

Southern Pasture

Gipps, West Vic, Tas, Sth SA, WA

** *** ***

Southern MDB

Nth Vic & Riverina, inland NSW, SA river

** ** **

Fresh milk supply

Sth Qld, NSW & other

***** *** ****

21

Farmer sentiment on these issues driven by nature of milk supply arrangements

and seasonal conditions

Attitude to the industry

Attitude towards the future of the dairy industry (% farms)

22

3 year outlook

Expected changes in production by region from 2008/09 to 2011/12 season (% of production)

23

Future challenges for growthOpportunity• Strong faith in medium to long

term prospects for the dairy industry

• Latent investment interest in the sector

• Land value impact of MIS failure

• Scope for gains from risk management

• Feed security

• Milk sales

Threat• Increasing volatility of

margins• Damage to herd capacity

from 2008/09 market slump• Uncertainty ahead

• Impact of CPRS

• Ongoing access to water + certainty of trading market regimes

• Labour & skills• Improved ability to compete

24