dalata hotel group january 2018 ise: dhg lse:...

TRANSCRIPT

Dalata Hotel Group January 2018 ISE: DHG LSE: DAL

Disclaimer

The presentation contains forward looking statements. These statements have been made by the

Directors in good faith based on the information available to them up to the time of their approval of this

presentation.

Due to inherent uncertainties, including both economic and business risk factors underlying such

forward looking information, actual results may differ materially from those expressed or implied by

these forward looking statements. The Directors undertake no obligation to update any forward looking

statements contained in this presentation, whether as a result of new information, future events or

otherwise.

Page 2

Dalata | Contents

Group Overview

Market Update

UK Research & Strategy

2018

Page 3

Group Overview

Dalata | Strong, Complementary Brand Proposition

Brand Proposition

Maldron is all about providing a fun, relaxed time for all who arrive through our doors. Our great-value hotels arefound in convenient locations close to local attractions -

ensuring there’s always plenty to see and do. With friendly, helpful staff, good food and excellent facilities, it’s the

perfect place to enjoy good times with family and friends

Rest assured, it’s a Maldron

You can always depend on Clayton Hotels to deliver exactly what you need, whether that’s a weekend

away, a family break or an important business meeting. From the comfort of our bedrooms to the quality of

our facilities and the warm, helpful attitude of our staff - every detail is handled with care

Where every moment matters

BedroomsGenerally standard rooms, with family and executive rooms

in some locationsStandard, superior and executive rooms

Food and Beverage

Integrated bar and restaurant in some locations. Simplemenus made from fresh quality produce

Modern bar, restaurant and coffee dock. Food and beverage offering based on local influences and freshly

sourced premium ingredients

Conference Facilities

Meeting room facilitiesExtensive choice of modern meeting rooms and events

facilities

Target Customers

Both leisure and corporate with main focus on leisure guests and family

Focus on corporate and conference midweek. Leisure, functions and weddings at weekend

Page 5

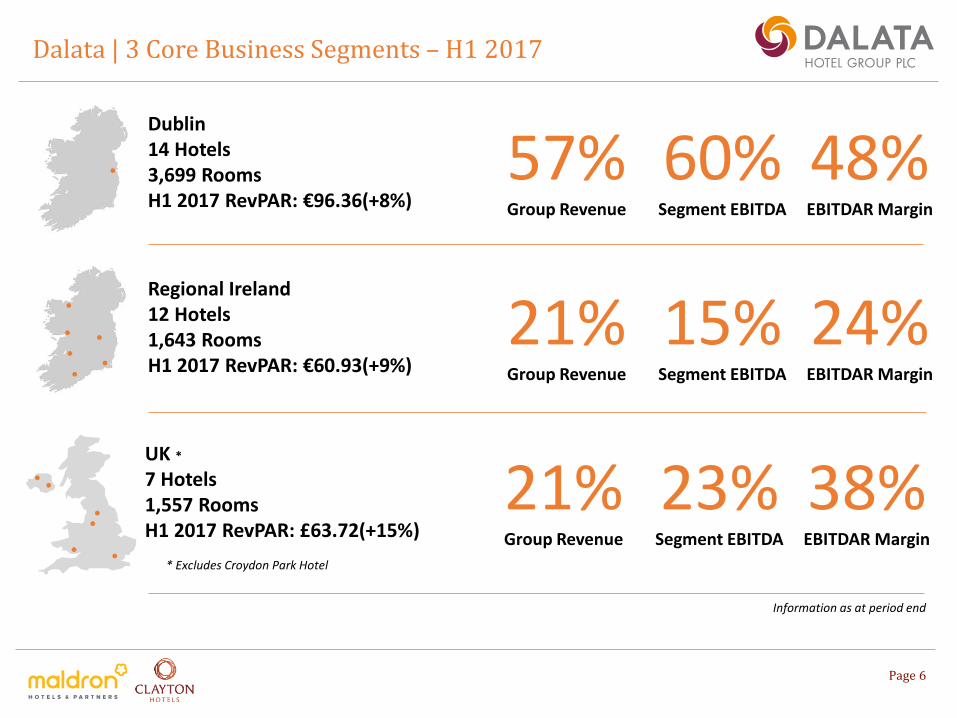

Dalata | 3 Core Business Segments – H1 2017

Dublin14 Hotels 3,699 RoomsH1 2017 RevPAR: €96.36(+8%)

57%Group Revenue

60%Segment EBITDA

48%EBITDAR Margin

Regional Ireland12 Hotels 1,643 RoomsH1 2017 RevPAR: €60.93(+9%)

21%Group Revenue

15%Segment EBITDA

24%EBITDAR Margin

UK *

7 Hotels 1,557 RoomsH1 2017 RevPAR: £63.72(+15%)

21%Group Revenue

23%Segment EBITDA

38%EBITDAR Margin

Page 6

* Excludes Croydon Park Hotel

Information as at period end

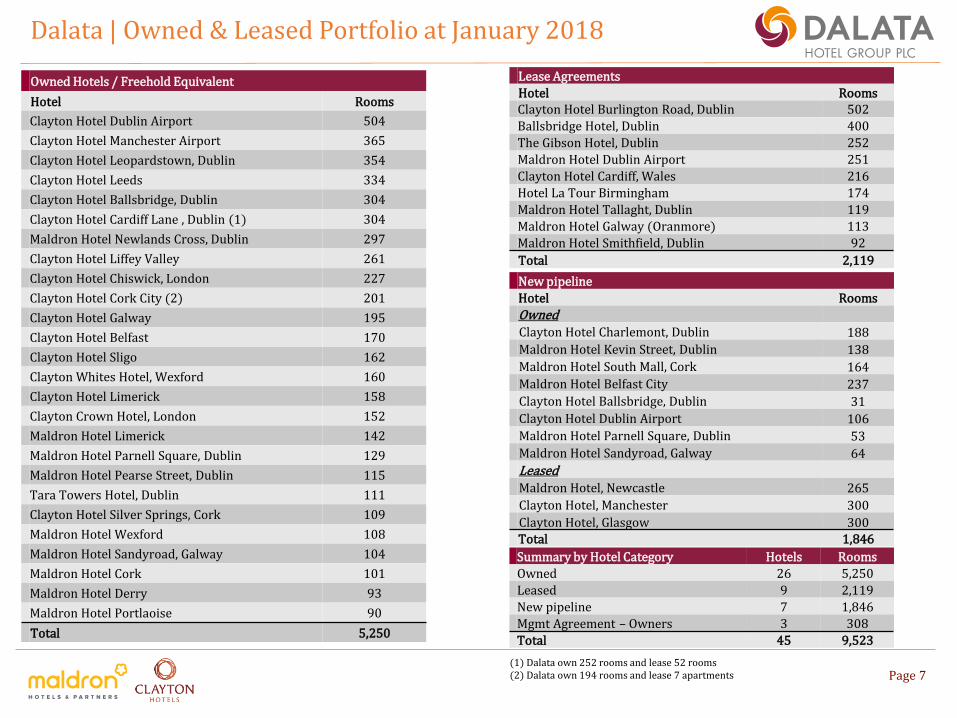

Dalata | Owned & Leased Portfolio at January 2018

Owned Hotels / Freehold Equivalent

Hotel Rooms

Clayton Hotel Dublin Airport 504

Clayton Hotel Manchester Airport 365

Clayton Hotel Leopardstown, Dublin 354

Clayton Hotel Leeds 334

Clayton Hotel Ballsbridge, Dublin 304

Clayton Hotel Cardiff Lane , Dublin (1) 304

Maldron Hotel Newlands Cross, Dublin 297

Clayton Hotel Liffey Valley 261

Clayton Hotel Chiswick, London 227

Clayton Hotel Cork City (2) 201

Clayton Hotel Galway 195

Clayton Hotel Belfast 170

Clayton Hotel Sligo 162

Clayton Whites Hotel, Wexford 160

Clayton Hotel Limerick 158

Clayton Crown Hotel, London 152

Maldron Hotel Limerick 142

Maldron Hotel Parnell Square, Dublin 129

Maldron Hotel Pearse Street, Dublin 115

Tara Towers Hotel, Dublin 111

Clayton Hotel Silver Springs, Cork 109

Maldron Hotel Wexford 108

Maldron Hotel Sandyroad, Galway 104

Maldron Hotel Cork 101

Maldron Hotel Derry 93

Maldron Hotel Portlaoise 90

Total 5,250

Lease Agreements

Hotel RoomsClayton Hotel Burlington Road, Dublin 502

Ballsbridge Hotel, Dublin 400

The Gibson Hotel, Dublin 252

Maldron Hotel Dublin Airport 251

Clayton Hotel Cardiff, Wales 216

Hotel La Tour Birmingham 174

Maldron Hotel Tallaght, Dublin 119

Maldron Hotel Galway (Oranmore) 113

Maldron Hotel Smithfield, Dublin 92

Total 2,119

New pipeline

Hotel Rooms

OwnedClayton Hotel Charlemont, Dublin 188

Maldron Hotel Kevin Street, Dublin 138

Maldron Hotel South Mall, Cork 164

Maldron Hotel Belfast City 237

Clayton Hotel Ballsbridge, Dublin 31

Clayton Hotel Dublin Airport 106

Maldron Hotel Parnell Square, Dublin 53

Maldron Hotel Sandyroad, Galway 64

LeasedMaldron Hotel, Newcastle 265

Clayton Hotel, Manchester 300

Clayton Hotel, Glasgow 300Total 1,846

(1) Dalata own 252 rooms and lease 52 rooms(2) Dalata own 194 rooms and lease 7 apartments Page 7

Summary by Hotel Category Hotels Rooms

Owned 26 5,250

Leased 9 2,119

New pipeline 7 1,846

Mgmt Agreement – Owners 3 308

Total 45 9,523

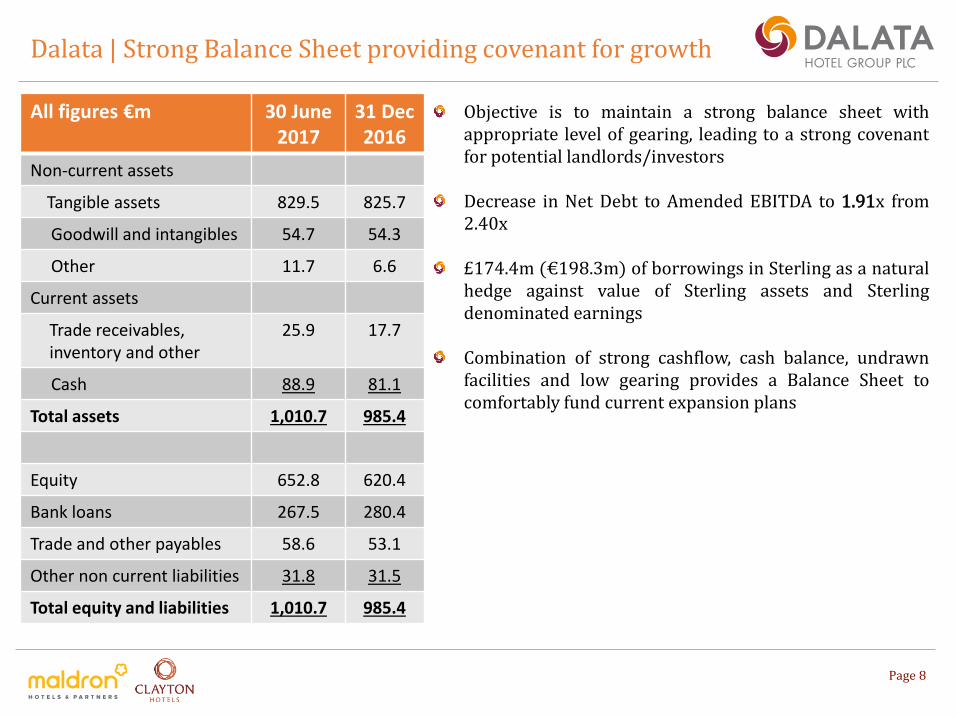

Dalata | Strong Balance Sheet providing covenant for growth

Objective is to maintain a strong balance sheet withappropriate level of gearing, leading to a strong covenantfor potential landlords/investors

Decrease in Net Debt to Amended EBITDA to 1.91x from2.40x

£174.4m (€198.3m) of borrowings in Sterling as a naturalhedge against value of Sterling assets and Sterlingdenominated earnings

Combination of strong cashflow, cash balance, undrawnfacilities and low gearing provides a Balance Sheet tocomfortably fund current expansion plans

All figures €m 30 June 2017

31 Dec2016

Non-current assets

Tangible assets 829.5 825.7

Goodwill and intangibles 54.7 54.3

Other 11.7 6.6

Current assets

Trade receivables, inventory and other

25.9 17.7

Cash 88.9 81.1

Total assets 1,010.7 985.4

Equity 652.8 620.4

Bank loans 267.5 280.4

Trade and other payables 58.6 53.1

Other non current liabilities 31.8 31.5

Total equity and liabilities 1,010.7 985.4

Page 8

Dalata | “The Difference with Dalata”

Our decentralised operational approach

Dalata’s decentralised structure is core to our management philosophy

Hotel General Managers are critical players – we continually develop them

A strong multi-functional team at the centre setting direction, seeking growth opportunities,supporting the hotels, and reporting to our stakeholders

We grow our own – training and development a major focus as there is a need to have a strong pipelineof key people coming through

Having people we know taking up key roles de-risks our business

We focus on what we are good at

Operating 3 star and 4 star modern well-maintained hotels in cities with strong mix of corporate andleisure demand

Executing transactions to grow our owned and leased portfolio

Identifying strong locations and developing new hotels on them

Decentralised revenue management – our revenue managers are informed by systems but always makethe decisions themselvesInvesting in systems to support our approach to cost control

Owner/Operator Model

Control of our brand standardsSecurity of tenure allows us to build a central team to effectively support and scale our decentralisedstructure

Page 9

Ireland: Portfolio Objectives

Complete existing development pipeline of 744 rooms and deliver on earnings potential when theyopen in 2018

Reach the optimum market share in each of the key urban centres – Dublin, Cork, Limerick and Galway

Drive Portfolio Growth | Ireland

Page 10

Dalata | Over 1,840 new rooms across Ireland and UK

Dublin

2 New Hotels

3 Extensions

516 rooms

Regional Ireland

1 New Hotel

1 Extension

228 Rooms

UK

1 New Owned Hotel

3 New Leased Hotels

1,102 Rooms

Property New Extension Rooms Planning Construction Completion

Granted Started

Clayton Hotel Charlemont x 188 x x Nov 2018

Maldron Hotel Kevin Street x 138 x x June 2018

Clayton Hotel Ballsbridge x 31 x x Aug 2018

Clayton Hotel Dublin Airport x 106 x x May 2018

Maldron Hotel Parnell Square x 53 x x Dec 2018

Property New Extension Rooms Planning Construction Completion

Granted Started

Maldron Hotel South Mall, Cork x 164 x x Dec 2018

Maldron Hotel Sandyroad, Galway x 64 x x June 2018

Property New Extension Rooms Planning Construction Completion

Granted Started

Maldron Hotel Belfast City x 237 x x Mar 2018

Maldron Hotel, Newcastle* x 265 x x Feb 2019

Clayton Hotel, Manchester* x 300 Q3 2020

Clayton Hotel, Glasgow* x 300 Q4 2020

*35 year operating lease

Page 11

Markets Update

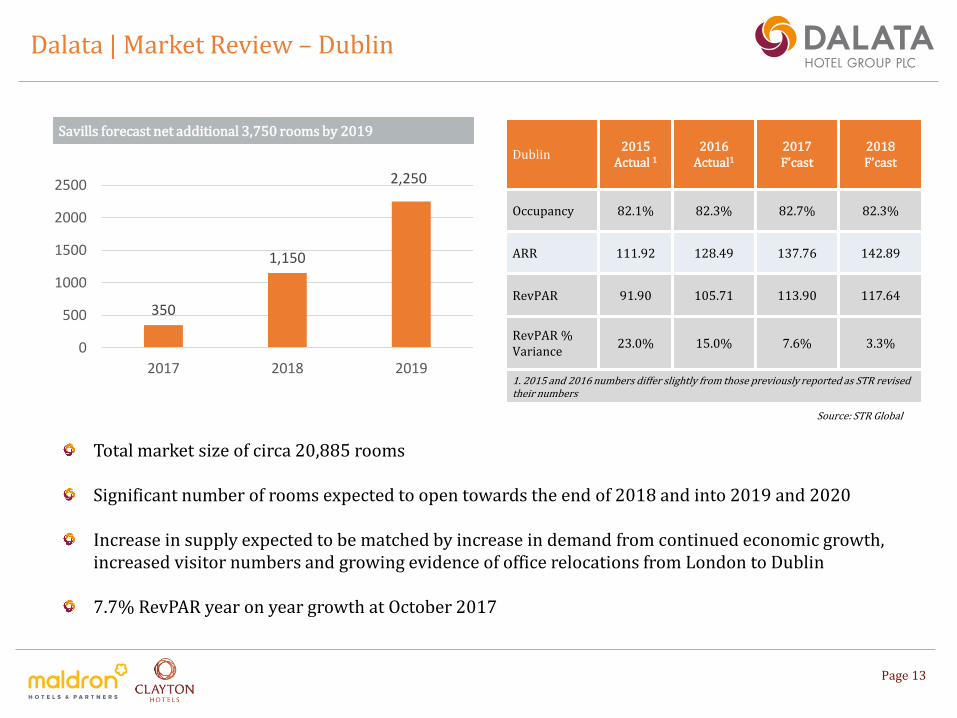

Dalata | Market Review – Dublin

350

1,150

2,250

0

500

1000

1500

2000

2500

2017 2018 2019

Savills forecast net additional 3,750 rooms by 2019

Dublin2015

Actual 12016

Actual1

2017F’cast

2018F’cast

Occupancy 82.1% 82.3% 82.7% 82.3%

ARR 111.92 128.49 137.76 142.89

RevPAR 91.90 105.71 113.90 117.64

RevPAR % Variance

23.0% 15.0% 7.6% 3.3%

1. 2015 and 2016 numbers differ slightly from those previously reported as STR revised their numbers

Page 13

Total market size of circa 20,885 rooms

Significant number of rooms expected to open towards the end of 2018 and into 2019 and 2020

Increase in supply expected to be matched by increase in demand from continued economic growth, increased visitor numbers and growing evidence of office relocations from London to Dublin

7.7% RevPAR year on year growth at October 2017

Source: STR Global

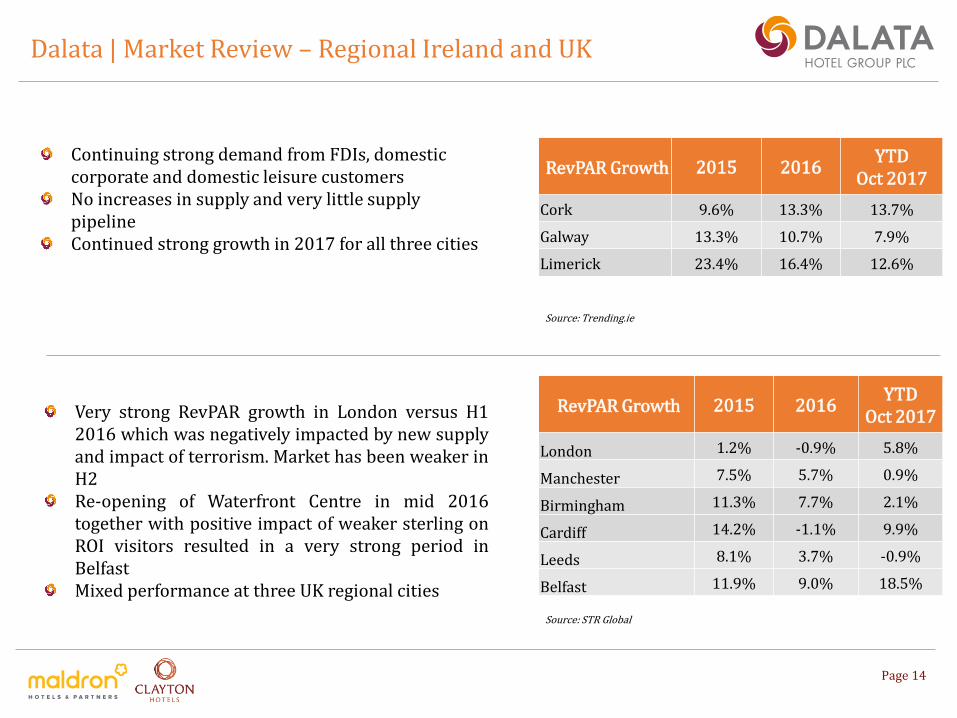

Dalata | Market Review – Regional Ireland and UK

RevPAR Growth 2015 2016YTD

Oct 2017

Cork 9.6% 13.3% 13.7%

Galway 13.3% 10.7% 7.9%

Limerick 23.4% 16.4% 12.6%

Continuing strong demand from FDIs, domestic corporate and domestic leisure customersNo increases in supply and very little supply pipeline Continued strong growth in 2017 for all three cities

Source: STR Global

Source: Trending.ie

Page 14

RevPAR Growth 2015 2016YTD

Oct 2017

London 1.2% -0.9% 5.8%

Manchester 7.5% 5.7% 0.9%

Birmingham 11.3% 7.7% 2.1%

Cardiff 14.2% -1.1% 9.9%

Leeds 8.1% 3.7% -0.9%

Belfast 11.9% 9.0% 18.5%

Very strong RevPAR growth in London versus H12016 which was negatively impacted by new supplyand impact of terrorism. Market has been weaker inH2Re-opening of Waterfront Centre in mid 2016together with positive impact of weaker sterling onROI visitors resulted in a very strong period inBelfastMixed performance at three UK regional cities

UK Research & Strategy

Dalata | 20 Target Cities Identified From Research

Page 16

1 Edinburgh2 Manchester3 Glasgow4 Brighton5 Bristol6 Leeds7 Liverpool8 Oxford9 Belfast10 Reading

11 Birmingham12 York13 Cambridge14 Southampton15 Milton Keynes16 Cardiff17 Portsmouth18 Newcastle19 Bournemouth20 Exeter

Following extensive research management have identified 20 provincial UK cities with strongopportunities for Maldron or Clayton hotels

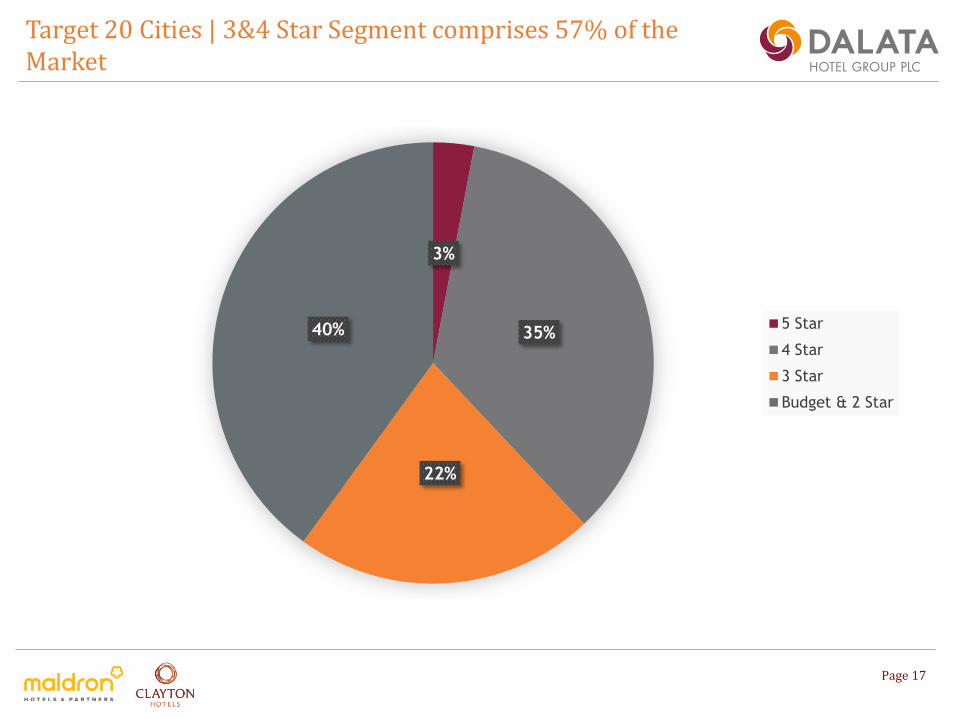

Target 20 Cities | 3&4 Star Segment comprises 57% of the Market

Page 17

3%

35%

22%

40% 5 Star

4 Star

3 Star

Budget & 2 Star

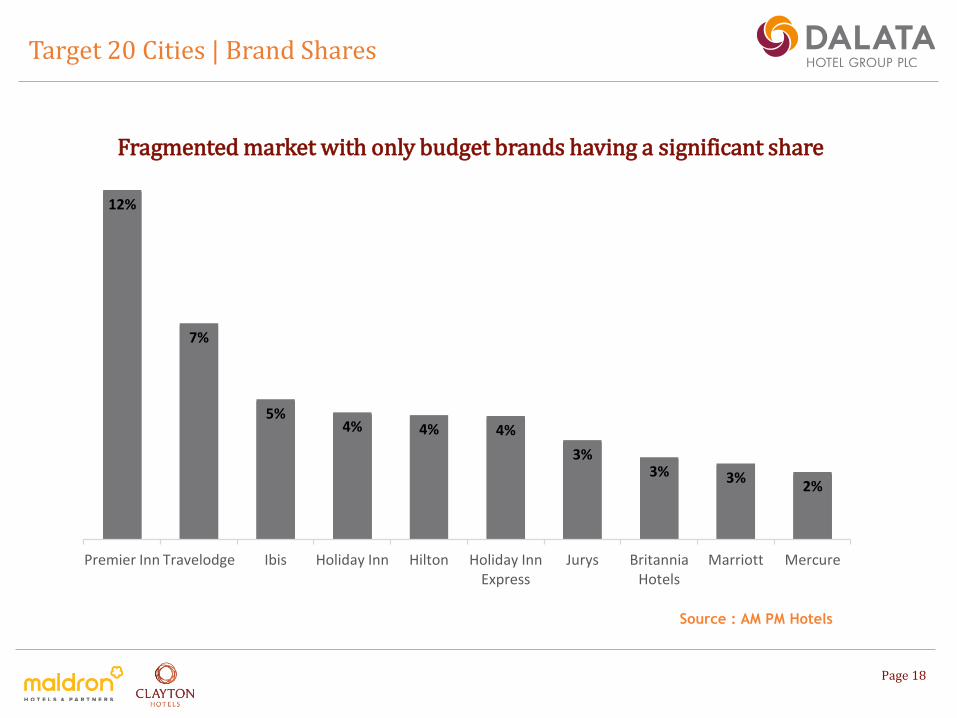

Target 20 Cities | Brand Shares

Page 18

12%

7%

5%4% 4% 4%

3%3% 3%

2%

Premier Inn Travelodge Ibis Holiday Inn Hilton Holiday Inn Express

Jurys Britannia Hotels

Marriott Mercure

Fragmented market with only budget brands having a significant share

Source : AM PM Hotels

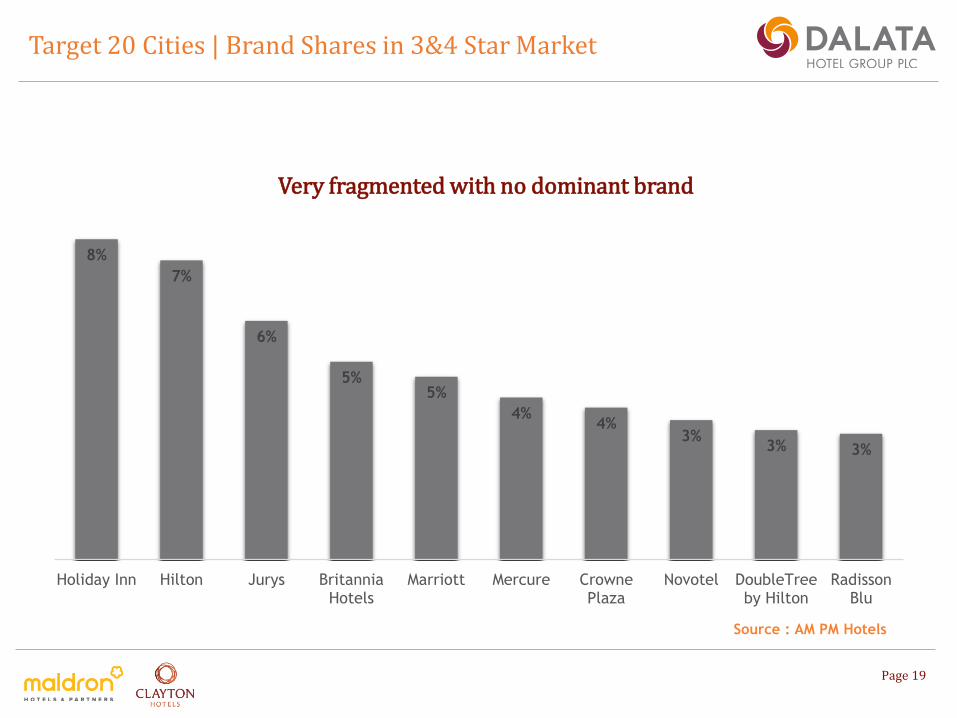

Target 20 Cities | Brand Shares in 3&4 Star Market

Page 19

Very fragmented with no dominant brand

8%

7%

6%

5%5%

4%4%

3%3% 3%

Holiday Inn Hilton Jurys BritanniaHotels

Marriott Mercure CrownePlaza

Novotel DoubleTreeby Hilton

RadissonBlu

Source : AM PM Hotels

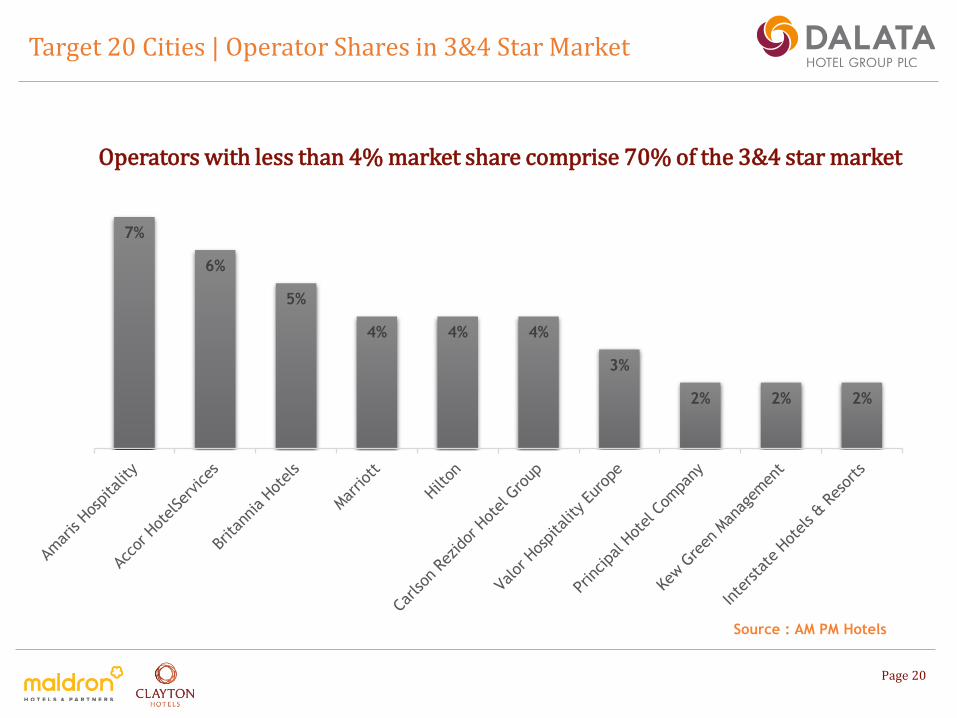

Target 20 Cities | Operator Shares in 3&4 Star Market

Page 20

Operators with less than 4% market share comprise 70% of the 3&4 star market

Source : AM PM Hotels

7%

6%

5%

4% 4% 4%

3%

2% 2% 2%

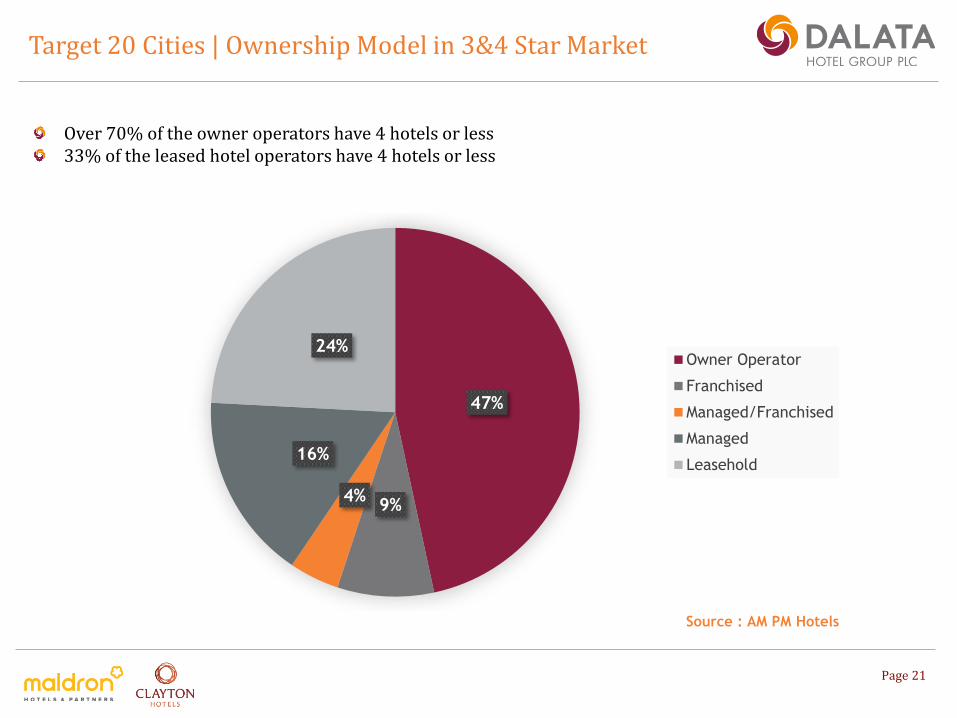

Target 20 Cities | Ownership Model in 3&4 Star Market

Page 21

Over 70% of the owner operators have 4 hotels or less33% of the leased hotel operators have 4 hotels or less

Source : AM PM Hotels

47%

9%4%

16%

24%Owner Operator

Franchised

Managed/Franchised

Managed

Leasehold

Target 20 Cities | International Brands moving away from operating hotels

Page 22

Source : AM PM Hotels

HiltonMarriott/Starwood

IHG Accor

Franchised 72% 43% 70% 33%

Managed 24% 52% 30%67%*

Owned/Leased 3% 2% 0%

Worldwide Rooms by Ownership Model

*Accor do not disclose separately no. rooms managed, owned and leased

Target 20 Cities | Age Profile in 3&4 Star Market

Page 23

Source : AM PM Hotels

19%18%

20%

18%

24%

Not Stated Under 10 years 10 - 20 years 20 - 40 Years 40 + years

Target 20 Cities | Fragmented Market offering Compelling Opportunity

Page 24

Dalata’s management team believe that a large structural opportunity has emerged in the 3 and 4 starhotel markets in certain regional cities in the UK. Key drivers of this structural opportunity are:

International brands are increasingly evolving to a franchise model leaving a shortage of operatorswith any scale

The specific 3 and 4 star market in certain large regional cities is very fragmented and there are nodominant brands in this market segment

Ownership model is also very fragmented

Close to 50% of the 3 & 4 star market comprises owner/operators and 70% of these operate 4hotels or less

The stock of 3 and 4 star hotels is considerably older than the age profile of the Budget sector

Opportunity now exists for a hotel operator with a strong balance sheet and operational focus to become the market leader in fragmented 3 and 4 star hotel markets

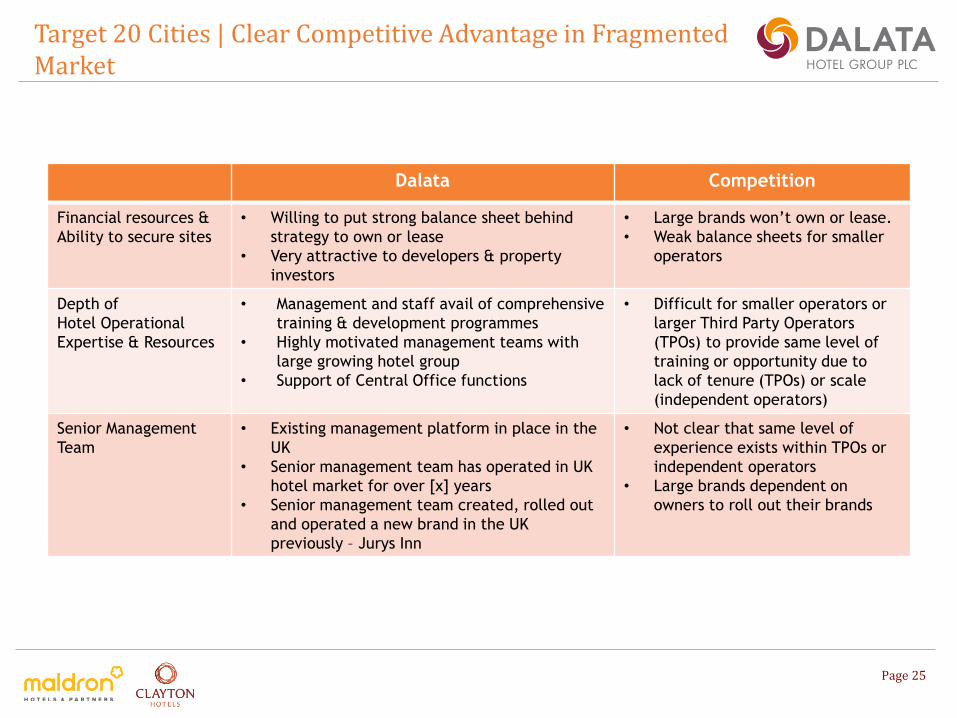

Target 20 Cities | Clear Competitive Advantage in Fragmented Market

Page 25

Dalata Competition

Financial resources &

Ability to secure sites

• Willing to put strong balance sheet behind

strategy to own or lease

• Very attractive to developers & property

investors

• Large brands won’t own or lease.

• Weak balance sheets for smaller

operators

Depth of

Hotel Operational

Expertise & Resources

• Management and staff avail of comprehensive

training & development programmes

• Highly motivated management teams with

large growing hotel group

• Support of Central Office functions

• Difficult for smaller operators or

larger Third Party Operators

(TPOs) to provide same level of

training or opportunity due to

lack of tenure (TPOs) or scale

(independent operators)

Senior Management

Team

• Existing management platform in place in the

UK

• Senior management team has operated in UK

hotel market for over [x] years

• Senior management team created, rolled out

and operated a new brand in the UK

previously – Jurys Inn

• Not clear that same level of

experience exists within TPOs or

independent operators

• Large brands dependent on

owners to roll out their brands

Target 20 Cities | Key Objectives in Target UK 20 cities

Page 26

Our objective is to become the leading 3/4 star operator in our target city markets

Target range of 10% to 15% market share of 3/4 star market in each city

Translates to additional circa 8,000 rooms (assuming a 12.5% market share in achieved) in 5– 7 years

Further opportunities are likely to exist in the Greater London area and adjacent to UKairports but Dalata will look to address those opportunities in a more bespoke manner as andwhen they arise

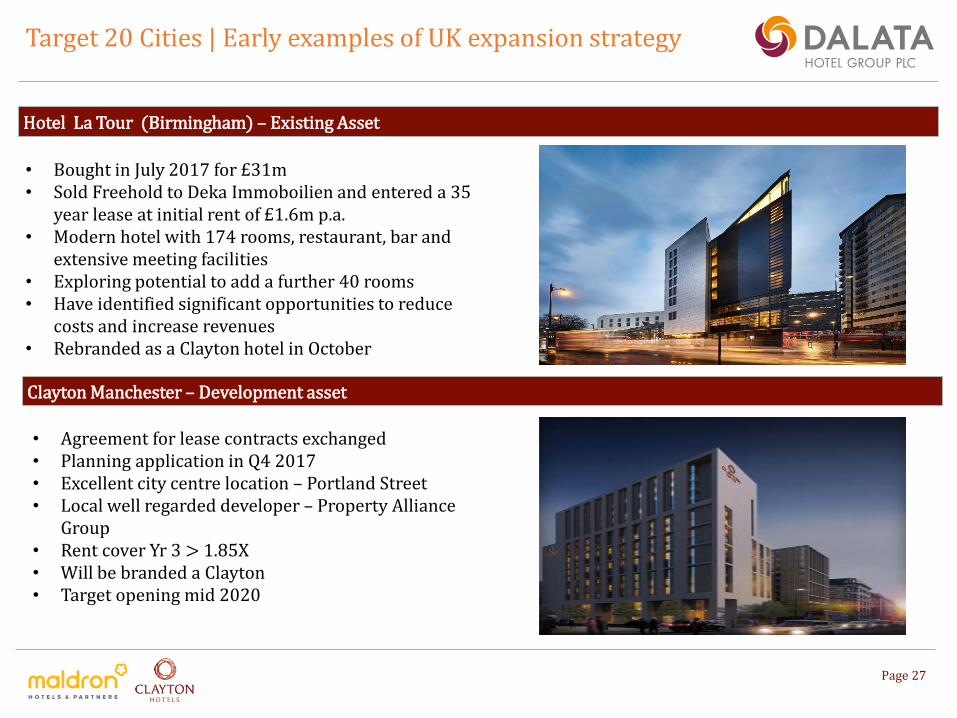

Target 20 Cities | Early examples of UK expansion strategy

Page 27

Hotel La Tour (Birmingham) – Existing Asset

• Bought in July 2017 for £31m • Sold Freehold to Deka Immoboilien and entered a 35

year lease at initial rent of £1.6m p.a. • Modern hotel with 174 rooms, restaurant, bar and

extensive meeting facilities • Exploring potential to add a further 40 rooms • Have identified significant opportunities to reduce

costs and increase revenues• Rebranded as a Clayton hotel in October

Clayton Manchester – Development asset

• Agreement for lease contracts exchanged • Planning application in Q4 2017• Excellent city centre location – Portland Street• Local well regarded developer – Property Alliance

Group • Rent cover Yr 3 > 1.85X • Will be branded a Clayton • Target opening mid 2020

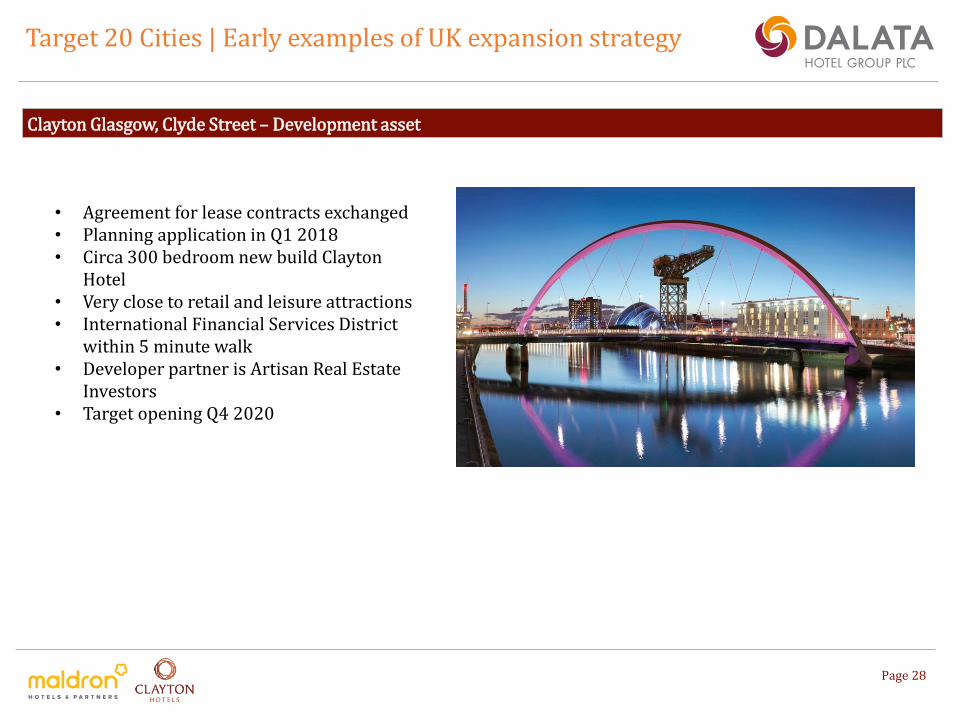

Target 20 Cities | Early examples of UK expansion strategy

Page 28

Clayton Glasgow, Clyde Street – Development asset

• Agreement for lease contracts exchanged • Planning application in Q1 2018• Circa 300 bedroom new build Clayton

Hotel• Very close to retail and leisure attractions• International Financial Services District

within 5 minute walk• Developer partner is Artisan Real Estate

Investors• Target opening Q4 2020

Outlook

Dalata | Another Busy Year in store in 2018

Continued focus on operational requirements of our hotels through training/development programmes, investment in technology and interaction with our customers

Confirmed pipeline of 1840 rooms across the three regions – 975 of these to open in 2018

Planning to commence construction in our two new Clayton hotel projects in Glasgow and Manchester.

Seeking to secure a further 1200 rooms in our development pipeline

Planning to complete the current investment programme in technology across our property management, revenue management and procurement systems.

Page 30