dallas coffin company building (constructed 1909) … · source: nps statistical report and...

TRANSCRIPT

Dallas Coffin Company Building (Constructed 1909) NYLO South Dallas (2012)

• Panel Introductions

• Tax Credit Introduction

• Federal

• Non-refundable credit that can offset corporatefederal income tax of non-closely held C-Corporations, as well as certain individual federalincome tax

• 20% of the qualified rehabilitation expenditures

• Or 10% of the qualified rehabilitation expenditures

• Texas

• Non-refundable credit against Texas Franchise Tax

• 25% of the qualified rehabilitation expenditures

• Texas Historical Commission

• Case Study (2101 Church Street) Wilson Building, Dallas

•Federal •Non-refundable credit that can offset corporate federal income tax of non-closely held C-Corporations, as well as certain individual federal income tax•20% of the qualified rehabilitation expenditures•Or 10% of the qualified rehabilitation expenditures

WHY HISTORIC TAX CREDITS?

• The federal Historic Tax Credit (HTC) Program is an alternative financingcomplement to conventional capital sources that can be used in therehabilitation and re-use of historic buildings

• HTC financing can provide approximately 10% - 20% of the necessary capital• A $10 million project that contains a $8 million of Qualified

Rehabilitation Expenditures (“QREs”) can anticipate approximately$1.4 million in gross HTC equity at closing

• Fill a gap in a capital stack

TIMELINE OF FEDERAL AND TEXAS

HTC

• 1976 – Congress creates tax deduction for Qualifiedrehabilitation expenditures ("QREs") for historic buildings

• 1982 – Congress adopts IRC Section 47 creating 10% tax creditfor "certified historic structures" as part of economic stimulus

• 1986 – Congress amends IRC Section 47 increasing tax creditto 20% for "certified historic structures" and creating 10%credit for non-historic buildings older than 1936

• 2013 – Texas Legislature adopts 25% historic tax credit

• 2014 – IRS provides safe harbor guidance in response toHistoric Boardwalk Hall

• 2015 – Texas historic tax credit becomes effective

• The objective of the Federal HTC program is to encourage private sector investment in the rehabilitation and re-use of historic buildings

• The National Park Service (NPS) and the IRS administer the federal program in partnership with State Historic Preservation Offices• The NPS manages all national parks, many national monuments, and other conservation

and historical properties• The NPS is an agency of the Department of the Interior• NPS works with State Historic Office of Preservation

• By the Numbers –• According to the National Park Service, since 1977 federal HTCs have:

• Supported 40,384 rehabilitation projects• Generated $73.8 billion in historic preservation• Rehabilitated 255,994 housing units• Supported the development of 248,303 new housing united• Contributed to the development of 137,978 LMI units• Created an estimated 2.47 million jobs

FEDERAL HTC PROGRAM

REGIONAL USE OF THE FEDERAL HTC

2012 2013 2014 2012 - 2014 2012 - 2014

State Pt 3 A QRE @ Pt 3 Pt 3 A QRE @ Pt 3 Pt 3 A QRE @ Pt 3 3 Yr Total QRE at Pt3 Rank

LA 72 $173,488,505 73 $193,241,315 64 $228,237,249 $594,967,069 8

FL 9 $82,136,973 4 $6,288,540 12 $77,531,993 $165,957,506 16

TX 3 $37,856,910 3 $33,802,168 9 $70,662,842 $142,321,920 18

GA 15 $16,785,130 29 $26,195,596 17 $30,356,140 $73,336,866 28

MS 21 $27,319,684 12 $15,971,513 14 $20,117,603 $63,408,800 29

AL 3 $4,394,338 5 $6,674,385 7 $11,423,841 $22,492,564 41

Source: NPS Statistical Report and Analysis for Fiscal Year 2012 -2014

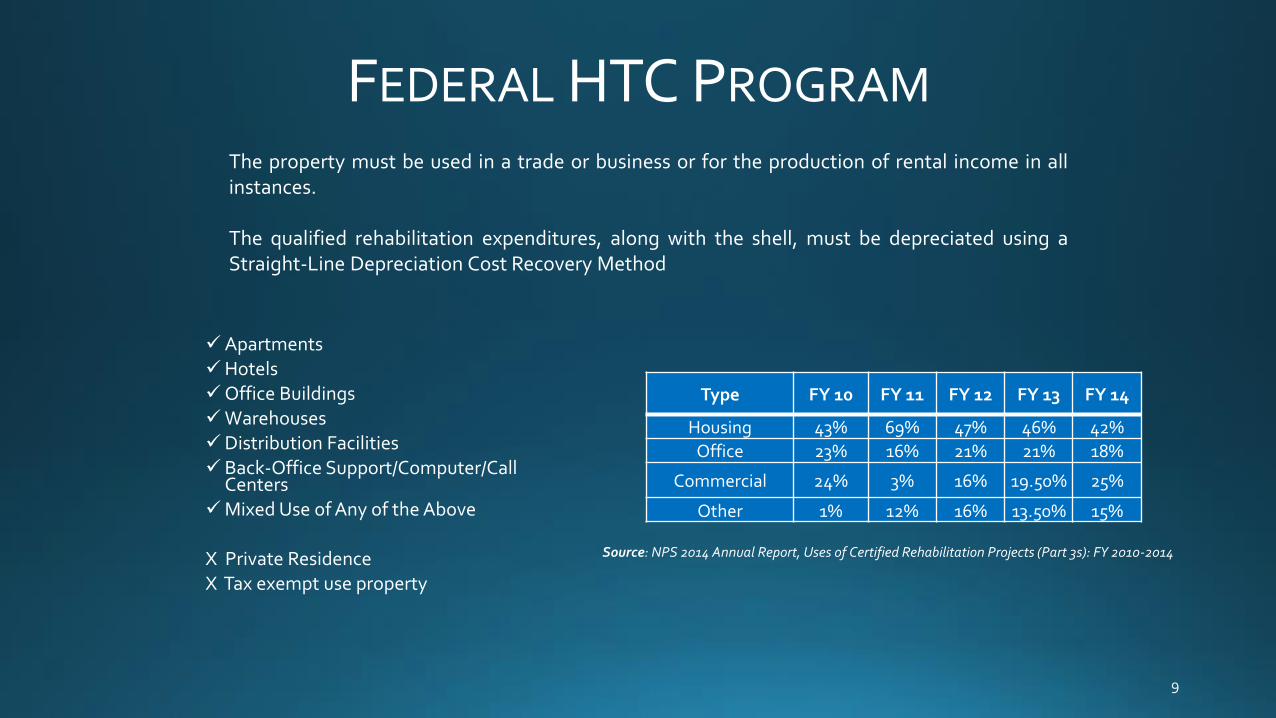

Source: NPS 2014 Annual Report, Uses of Certified Rehabilitation Projects (Part 3s): FY 2010-2014

Type FY 10 FY 11 FY 12 FY 13 FY 14

Housing 43% 69% 47% 46% 42%

Office 23% 16% 21% 21% 18%

Commercial 24% 3% 16% 19.50% 25%

Other 1% 12% 16% 13.50% 15%

FEDERAL HTC PROGRAM

The property must be used in a trade or business or for the production of rental income in allinstances.

The qualified rehabilitation expenditures, along with the shell, must be depreciated using aStraight-Line Depreciation Cost Recovery Method

ApartmentsHotelsOffice BuildingsWarehousesDistribution FacilitiesBack-Office Support/Computer/Call

CentersMixed Use of Any of the Above

X Private ResidenceX Tax exempt use property

QUALIFIED REHABILITATION

EXPENDITURESQualified Rehabilitation Expenditures are defined in Treas. Reg. 1.48-12(c) and generallyinclude costs chargeable to a capital account and made in connection with the rehabilitation ofa qualified building. Land costs are NOT a qualified costs. Special rules exist for costs incurredby a prior owner and assumed through purchase by a new owner.

For purposes of the substantial rehabilitation test, adjusted basis is the cost of the property(excluding land) plus or minus adjustments to basis and is determined as of the first day of the24-month period selected by the taxpayer.

Qualified:

• Construction and construction-related costs

• Construction period interest

• Architectural and engineering fees

• Site survey fees

• Legal expenses

• Insurance premiums

• Development fees

• Property taxes

NOTQualified:

• Costs related to the acquisition or enlargement of thebuilding

• Furniture, fixtures and equipment

• Expenses incurred for building-related areas:

• Sidewalks

• Parking lots

• Landscaping

• Three Part Federal Process:

• Part 1 – Confirming the Building Qualifies

• Part 2 – Plans for the Rehabilitation

• Part 3 – Confirmation the Rehabilitation was consistent with the architectural standards

FEDERAL PROGRAM

HTC PROGRAM COMPARISONTo date, 35 states in the country have adopted laws creating credits against state taxes toprovide incentives for the appropriate rehabilitation of historic buildings. In most cases thesetax credits take the form of the very successful federal income tax credit for historicrehabilitation contained in Section 47 of the Internal Revenue Code.

Federal Alabama Louisiana TexasApplication

Process Part I, Part II, Part III Lottery, Part A, Part B, Part C Part I, Part II, Part III Part A, Part B, Part C

Credit % 20% 25% 25% 25%

Recapture 5 years from PIS, 25% burned

off annually Same as federalOwner prohibited to sell

within 5 years None

Credit Type Allocated Allocated or Certificated Allocated or Certificated Allocated or Certificated

Transferability None Single transfer or

disproportionate allocation Directly transferable Directly Transferable

Transaction Cap None $5 million None None

Annual Aggregate Cap None $20 million None None

Offset Corporate Excise, Corporate, Personal Income, Franchise Franchise

Carry Forward 20 years 10 years 5 years 5 years

Parties to an HTC Transaction

Federal:• Direct Structure

• Also known as a single tier structure• Developer has a 1% interest in the entity that owns the building• Investor has a 99% interest in the entity that owns the building

• Master Tenant Structure• Also know as lessee pass-through• The entity that owns the building leases the building to the Master

Tenant• The Master Tenant leases the building to the actual occupants• Developer owns 1% of the Master Tenant• Investor owns 99% of the Master Tenant

STRUCTURING THE DEAL

Federal

Historic Tax

Credits

State Historic

Tax Credits Combined

Project Size 12,000,000 12,000,000 12,000,000

Eligible Basis (QRE) 10,000,000 10,000,000 10,000,000

Tax Credits 20.0% 2,000,000 25.0% 2,500,000 4,500,000

Equity Price 100.0% 2,000,000 2,000,000

Sales Price 80.0% 2,000,000 2,000,000

Gross Proceeds at Close 2,000,000 2,000,000 4,000,000

Estimated Fees & Closing Costs (170,000) (150,000) (320,000)

Net Proceeds at Close/Certification 1,830,000 1,850,000 3,680,000

Estimated Aggregate Annual Distributions 2.0% (200,000) (200,000)

Exit/Put Price 10.0% (200,000) (200,000)

Net Benefit (Before Tax) 1,430,000 1,850,000 3,280,000

Income Tax Liability 39.0% (721,500) (721,500)

After Tax Net Benefit 1,430,000 1,128,500 2,558,500

CHARACTERISTICS OF INVESTMENT CANDIDATES Property type - Multi-family, mixed use, special use, hospitality, office, retail Developer has site control of property Construction and permanent debt has been identified NPS Part I completed; Part II submitted Experienced HTC architect and contractor

INVESTMENT PREFERENCES Development cost > $1 million Development period < than 24 months Qualified Rehabilitation Expenditures (QREs) > $2 million Catalyze further redevelopment

INVESTMENT STRUCTURES Widely accepted structuring options have been developed with and approved by market leading accounting firms and legal counsel, but will vary by state. Options include:

Master Tenant Partnership Flip Purchase & Sale

Stonehenge Capital is actively seeking historic rehabilitation projects that generate state historic tax credits

STONEHENGE – TEXAS HTC STRATEGY

STONEHENGE CAPITAL COMPANY OVERVIEW

• Stonehenge’s business Gr0ups include:

• A nationally recognized specialty finance company with expertise in tax credit finance, structured finance, and private equity.

− Principals: senior managers within Bank One (now JPMorgan Chase) investment banking, merchant banking, investment

advisory, securities brokerage, and insurance operations.

− 45+ professional employees in seven states; Executive oversight in LA and OH; additional production offices in AL, FL, NY, CT

and TX.

Tax Credit Products: Stonehenge has extensive experience structuring and financing over $2.5 billion in premium tax, income tax,

and franchise state tax credits across the United States generated by film, historic rehabilitation, renewable energy, and brownfield

projects.

Community Development: $545 million federal New Markets Tax Credit (NMTC) allocation, a program administered by the USTreasury to encourage investment in low income communities. In addition, Stonehenge manages $491 million in state NMTC funds inAlabama, Arkansas, Florida, Illinois, Kentucky, Maine, Missouri, Nebraska, Nevada, Ohio, and Oregon and syndicates state credits inMissouri and Louisiana.

Venture Capital & Private Equity: Stonehenge manages approximately $630 million in regionally-targeted funds focused onmezzanine/growth investments in small businesses.

Whitney LaNasa 236 Third Street

Baton Rouge, LA 70801(O) 225-408-3265

CONTACT INFORMATION