david lamb consultant, target analytics february, 2009

TRANSCRIPT

David LambConsultant, Target Analytics

February, 2009

Part 1• Basic math - real estate research• Higher math - public company officers

Part 2• Advanced calculus - private company

officers • Tax math - foundations • Philanthropy capacity – making sense of

the math

Real Estate Research

First, a few observations:

Real estate appraisal is a discipline unto itself

The primary purpose of real estate research is not to get a gift of property (though that might happen)

It is often impossible to learn about all the real estate some prospects hold

Liabilities related to real estate are usually hidden from view

Real estate is often the only asset that a researcher learns about a potential prospect

Market Value – the price determined by a willing buyer and a willing seller

Assessed Value – the value determined for tax assessment purposes

Appraised Value – the value determined by an appraisal professional, usually based on more than one method of valuation (i.e. replacement cost or value as a rental property)

Taxpayer’s Name – usually the owner of the property, sometimes the same as the individual’s given name, but can be the name of a company, partnership, trust or other entity

Protection of the public To allow you to verify that I am being

taxed the same way you are

Property taxing authority Usually a county, but may be a township

• Many taxing authorities make the tax records searchable on their web sites

• No searching standards Might have to know the parcel number or the address Often name search is available Quality and detail of data varies widely from one county

to another Vendors and other providers obtain the

information and standardize it for searching• Lexis Nexis• DataQuick• KnowX

The tax value of a property set by the rules of the state or county

Source: http://www.pulawski.net/georgia.html

Source: http://www.pulawski.net/newyork.html

Source: Zillow.com

Record taxpayer name as someone other than the owner• Family trust• Spouse with a different last name

Send the tax bill to an address other than the owner’s home or business

Use a vendor• County by county search is inefficient• Counties may not allow name search• Vendors allow you to do national search by

taxpayer or owner name and mailing address• Trade-off: efficiency and convenience for cost• Common vendors

Lexis Nexis Dataquick

Use a realtor sales site • Corcoran (New York, Hamptons, Palm Beach)• Realtor.com

Shows the direction of national home prices

Based on repeat sales of single family homes – new construction not included

Includes 20 regional indexes All regions normalized to a value of 100

in January, 2000 For more detailed index, see the

National Association of Realtors website

Can be used as a way to gauge overall wealth

Can be the gift if not where the prospect lives

Can be given through a bequest

Free• Portico – directory of assessors with online access

indorgs.virginia.edu/portico/personalproperty.html• Christina Pulawski’s Tax Assessor Database –

www.pulawski.net • Zillow – market value estimates http://www.zillow.com

Vendor supplied• Lexis Nexis• Dataquick• KnowX (www.knowx.com)

Public Company Math

Definition• Top officer (policy making level)• Director• 5% shareholders

Must report their stock holdings and compensation

Easy to research Smallest part of your constituency

Direct and indirect stock holdings of insiders

Stock options Compensation of directors Compensation of top officers Other details (severance &

retirement plans & more) Current value of stock Current stock holdings

Yahoo!Finance• Current Stock Price• Insider Roster• Insider Transactions• SEC Filings

Public company databases• Free

Yahoo!Finance SEC Info MarketWatch

• Charge Hoovers 10K Wizard

Do you have…• More time than money?• More money than time?

Forms • 3 – Initial statement of

ownership• 4 – Record of a trade• 5 – Annual statement

of ownership• DEF 14A – Proxy

statement• S1 – Initial Public

Offering

Election of Directors – bios of all the directors

Beneficial Owners – stock holdings of all insiders

Executive Compensation – salary, bonus and other compensation

Option Awards and Exercises Director Compensation Retirement or pension provisions

Bio: HOWARD SCHULTZ, 55, is the founder of Starbucks and serves as our chairman, president and chief executive officer…

Stock ownership: 18,317,211 shares x $10.72 (2/9/09) = $196,360,502

Cash salary: $1,190,000 Other compensation: $764,366 Options

• Value of vested options: $62,759,150• Value of options expiring in 2009 (based on 2/9

price) : $5,257,937

Search for SEC Filings to find Recent Filings

Most recent Form 4 summarizes holdings

DIRECTLY HELD STOCK INDIRECTLY HELD STOCK

Personal property of the insider

Easily gifted Count as an asset

Legal owner is someone other than the insider• Spouse• Children• 401K• A trust

May or may not be gift-able

Do not count unless you understand the relationship

When your prospect is no longer with a public company

When your prospect sells her privately-held company to a public company

Free• U.S. Securities and Exchange Commission

(EDGAR)www.sec.gov/edgar.shtml Tutorial, description of forms, link to regulatory actions

• Yahoo!Financehttp://finance.yahoo.com

• MarketWatchhttp://www.marketwatch.com/tools/quotes/insiders.asp?siteid=mktw

Charge• 10K Wizard

www.10kwizard.com• Hoovers

www.hooovers.com

Private Company Math

When a company incorporates, it issues shares, known as “outstanding stock”

The value of the company is divided evenly among the shares

“Publicly held” stock vs. “closely held”

Finding the value of public company stock is easy

Finding the value of private company stock is difficult and expensive

Closely Held Stock

The value of a company is influenced by the reason you’re asking the question

Reasons to value a private company:• To measure progress• To sell it• To raise capital from investors• Part of a divorce settlement• For a management buyout• For estate planning• For an employee stock ownership plan• For taxation

Change the purpose of the valuation and you change the stock price

Only fundraisers ask how it affects a gift

Information typically is not available on private companies

The value of a company is not necessarily identical to the bottom line on the balance sheet

Companies with a negative cash flow can have a high value

Companies with a positive cash flow might have a modest value

To find out what a company is worth, sell it

Value is partly (sometimes mostly) subjective

Sometimes D&B provides a net worth figure

Read everything you can about your target company – it’s not just numbers

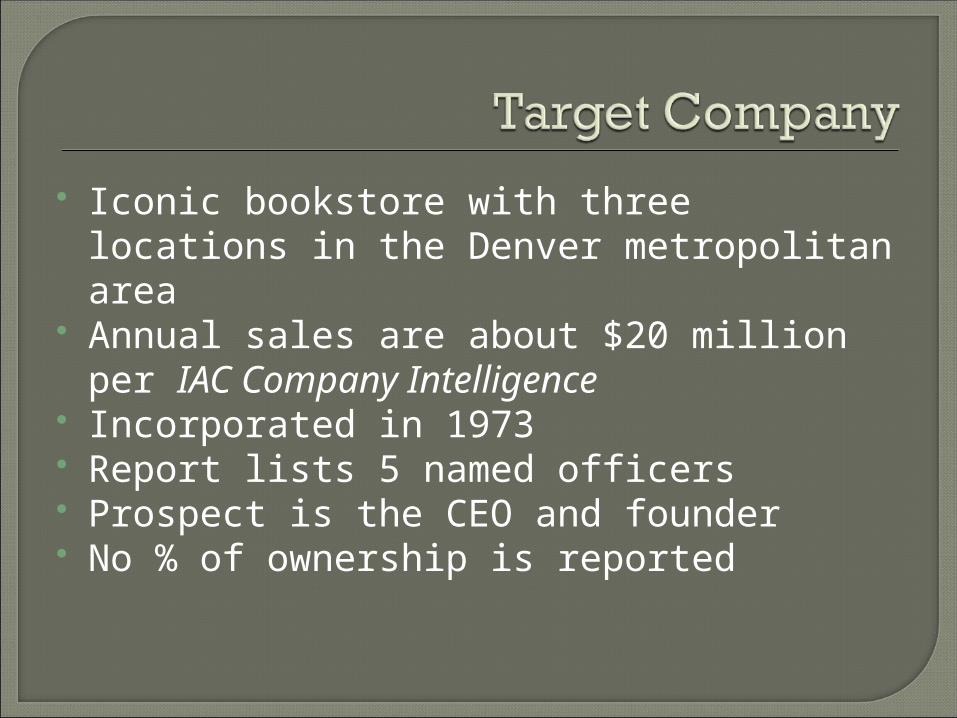

Iconic bookstore with three locations in the Denver metropolitan area

Annual sales are about $20 million per IAC Company Intelligence

Incorporated in 1973 Report lists 5 named officers Prospect is the CEO and founder No % of ownership is reported

Book value Price/earnings ratio (P/E) Discounted cash flow Comparison to similar companies of

known value• Multiple: Known value/known annual sales• Apply the multiple to target company’s

sales

Find a similar public company• Downside: a public company is almost

always valued higher than an otherwise equivalent private company would be

Find a similar private company that sold recently• Downside: the only commonly available

metric is sales, and value is not always clearly tied to sales or even profit

Comparison is only method that is possible if you have no access to the financial statements and appraisals of the assets is comparable companies

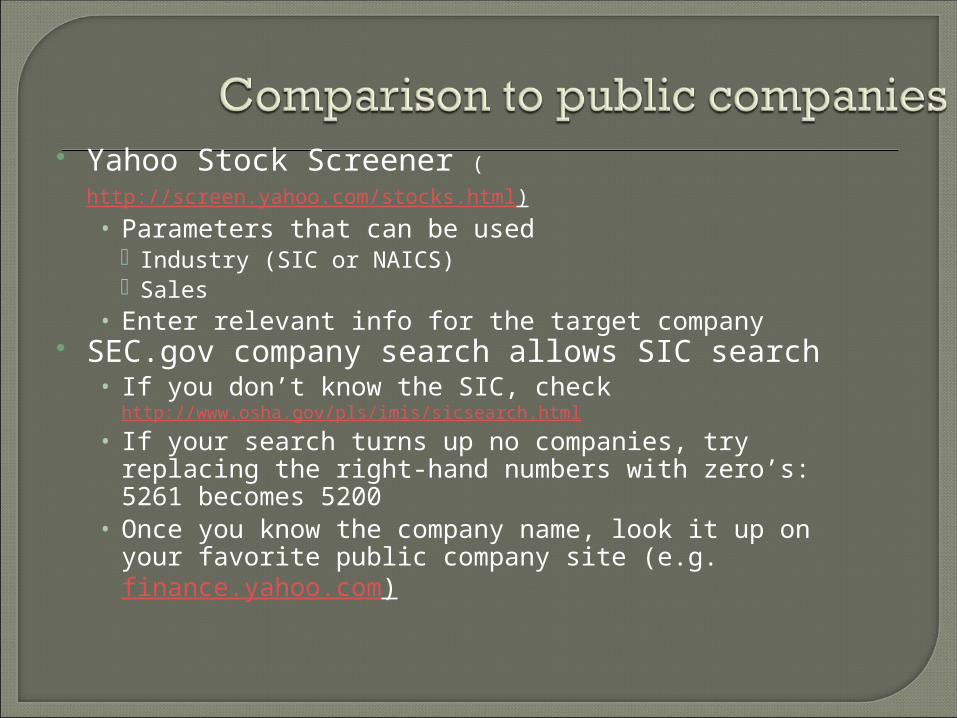

Yahoo Stock Screener (http://screen.yahoo.com/stocks.html) • Parameters that can be used

Industry (SIC or NAICS) Sales

• Enter relevant info for the target company SEC.gov company search allows SIC search

• If you don’t know the SIC, check http://www.osha.gov/pls/imis/sicsearch.html

• If your search turns up no companies, try replacing the right-hand numbers with zero’s: 5261 becomes 5200

• Once you know the company name, look it up on your favorite public company site (e.g. finance.yahoo.com)

Market Capitalization is one good measure of public company value

Your target company value is probably considerably less, even if otherwise equivalent

Public companies tend to be much larger than their private counterparts

Ratio of annual sales to market cap provides a multiple for the relevant industry

The more examples the better Read the profile to see if the comparison

company is similar in purpose to the target If the public company has flat or negative

earnings, it may still have value

Business Valuation Resources (www.bvmarketdata.com) • Pratt’s Stats

Database of over 9,500 private company sales from 1990 to present

Deal price ranges from $1 million to $14.4 billion Updated monthly with about 100 transactions added /

month $595

• Bizcomps Database of over 9,500 private company sales from 1993

to present 61% of the companies have gross revenues less than

$500K 18% of the companies have gross revenues over $1

million $395

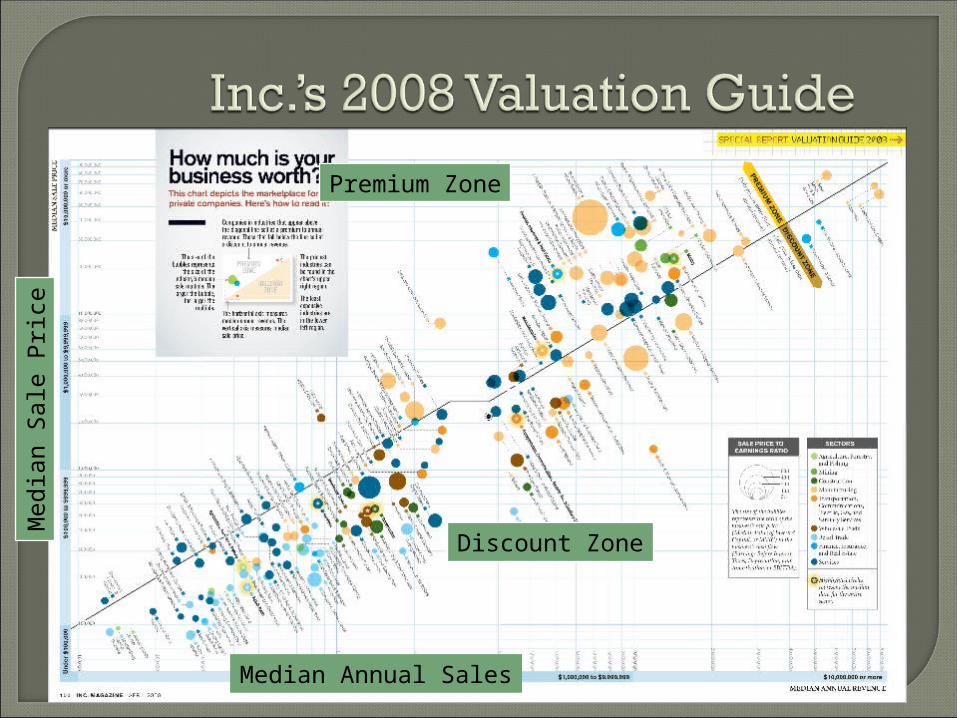

INC. Magazine’s Ultimate Valuation Guide

Premium Zone

Discount Zone

Med

ian

Sale

Pri

ce

Median Annual Sales

Med

ian

Sale

Pri

ce

Median Annual Sales

http://www.bizstats.com/reports/valuation-rule-thumb.asp

Bizbuysell.com GlobalBX.com

Company sales are reported to be $20 million The one classified found for a bookstore

supports a high ratio of value to sales Inventory is unknown, but classified add

suggests a possible inventory to sales ratio of 37.5%

Best guess of inventory: 37.5% x $20 MM = $7.5 MM

Alternate calculations:• Using BizStats (15% of sales + inventory)

$7.5 MM Inventory $3.0 MM 15% of sales $10.5 MM Total

• Using Inc. Valuation Guide (43% of sales) $8.6 MM

Company sales are reported to be $20 million The one classified found for a bookstore

supports a high ratio of value to sales Inventory is unknown, but classified add

suggests a possible inventory to sales ratio of 37.5%

Best guess of inventory: 37.5% x $20 MM = $7.5 MM

Alternate calculations:• Using BizStats (15% of sales + inventory)

$7.5 MM Inventory $3.0 MM 15% of sales $10.5 MM Total

• Using Inc. Valuation Guide (43% of sales) $8.6 MM

Gifts from people - individuals & bequests (about 83.2%±)

Gifts from corporations and foundations (16.8%±)

For more details, visit the Giving USA Foundation™ site at http://www.givingusa.org/

2005

GuideStar 990-PF tutorialhttp://www.guidestar.org/index.jsp

The Foundation Center 990-PF FAQshttp://fdncenter.org/learn/faqs/html/990pf.html

Form 4506-A: Request for Public Inspection or Copy of Exempt or Political Organization IRS Formhttp://www.irs.gov/pub/irs-pdf/f4506a.pdf

Tip: Go to the IRS Web site at http://www.irs.gov/pub/irs-pdf/f990pf.pdf Print a blank 990-PF and then highlight the lines and sections that matter to you.

Public charities file 990s Private foundations file 990 PFs

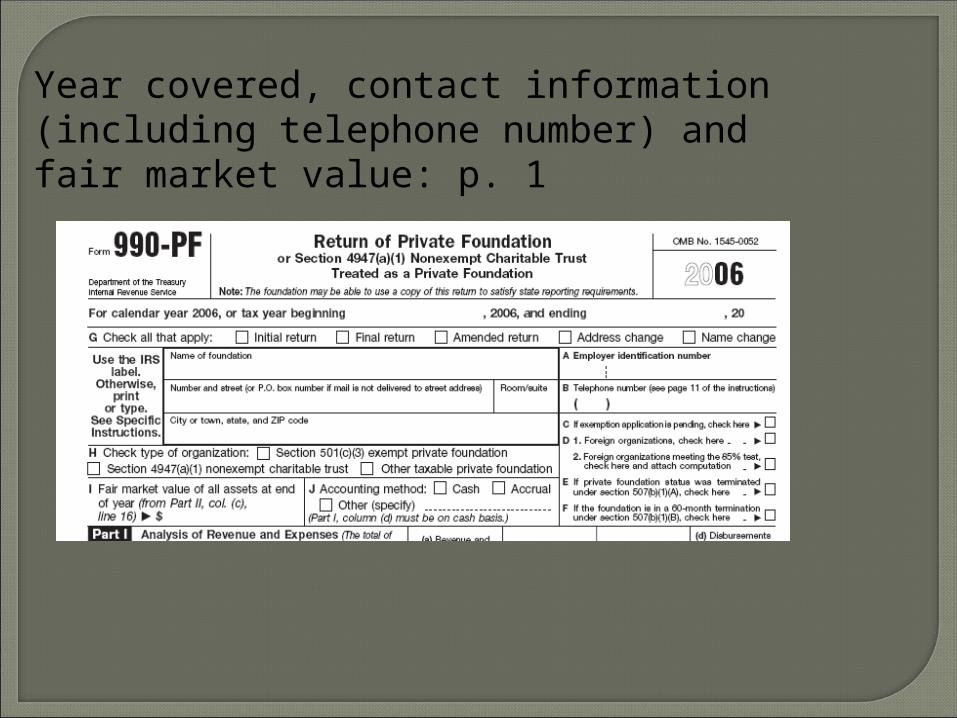

Year covered, contact information (including telephone number) and fair market value: p. 1

Gifts and grants total:p. 1, Part I, lines 25 and 26

Beginning of the year and year end assets: p. 2, Part III, lines 1 and 6

Officers, directors and trustees: Part VIII, line 1 (and look at line 2, too)

Future grants to be paid: Part IV, line 3, section b

GuideStar - http://www.guidestar.org IRS Search for Charities

http://www.irs.gov/charities/article/0,,id=96136,00.html

FundsNethttp://www.fundsnetservices.com/quick_links.htm

GrantSmart - http://www.grantsmart.org/ AG charities databases

http://www.searchsystems.net/ Your local library (see Foundation Center list of

cooperating collections at http://fdncenter.org/collections/)

CharityVillage (Canadian foundations) - http://www.charityvillage.com/

GuideStar UK http://www.guidestar.org.uk/

Philanthropic Capacity Rating

First, a few definitions (and a word or two about ranges) Total philanthropic capacity (TPC) is an estimate

of the amount an individual will or can give to all charities over 5 years.

Net worth is the value of an individual's assets minus their expenses or debts.

Known assets are the financial points of information available to prospect research. This term is often used in place of “net worth” since researchers never have enough information to accurately estimate net worth (all assets minus all expenses).

Ask Rating is the solicitation amount appropriate for a specific project, based on the conclusions of the development officer who has been cultivating the donor for that major gift.

"Salary represents 10 percent of net worth." "Stock holdings represent 30-35 percent of net

worth." "Real estate holdings represent 20-25 percent of

net worth." "Prospects have the capacity to give about 5

percent of net worth (or known assets) to charity (in a single gift or over five years)."

"An annual fund gift represents about 10-20 percent of a prospect’s major gift capacity."

"Prospects have the capacity to give 10 percent of the value of stock options of $1 million or more to charity."

Households with a net worth of $1.5M-$10M, 2004 IRS data, published in 2008[2] Includes cash and cash management accounts.[3] Includes all government bonds, bonds issued by corporations and foreign governments, mortgages and notes, cash value life insurance, and diversified mutual funds.[4] Includes Individual Retirement Accounts, annuities, and self-employed or Keogh plans.[5] Includes non-corporate businesses, farms, and limited partnerships.

Age Giving Rate

70+ 5%

60-69 4%

50-59 3%

40-49 2%

21-39 1%

Adjusting the estimate: • Is the prospect an entrepreneur?• How mature is the business?• Is the prospect a farmer?• Is the prospect an investor?

Your task: Develop a gut feel for the prospect’s situation and adjust appropriately• Past giving to your org• Past giving to other orgs• Strength of relationship• Prospect research• Anecdotal information

Try out different scenarios to find one that seems to fit the facts the best

Example: A 55-yr. old prospect is a 50% owner in a privately held company with an estimated value of $10 million

Estimated company value ($10 million)x ownership percentage (50%)÷ estimated proportion of net worth (10% (IRS

says 9%))x age multiplier (3%)-----------------------------------------------= Total Philanthropic Capacity of $1.5 million

Salary corresponds to cash on IRS chart but… Much of it is spent – doesn’t stay in portfolio Rule: net worth can be estimated at

10 times annual salary.

Annual Salary + Bonus x 10 x giving percentage (or age multiplier) ----------------------------------------------------= Total Philanthropic Capacity

Example: Prospect earned $250,000 in salary and a bonus of $50,000 last year.

($250,000 + $50,000) x 10 x 5% = $150,000

Example: A 58-yr. old with $17 million in directly held stock. $5 million of the indirectly held stock is owned by the spouse, and $5 million is owned by trusts for children and grandchildren

Stock holdings ($22 million) ÷ portion of estate (20% (IRS says 17%))x age multiplier (3%) --------------------------------------------------= Total Philanthropic Capacity of $3.3 million

Remember: the insider stock is probably only a part of the prospect’s portfolio!

Example: A 63-yr old owns home with an estimated value of $1.5 million, a vacation home worth $1 million, and business property valued at $500,000

Real estate value ($3 million) ÷ portion of estate from IRS (25% (actually 23%))x age multiplier (4%) --------------------------------------------------= Total Philanthropic Capacity of $480,000

Consistent annual giving x 10 or 20 = TPC Total private foundation giving x 5 (years) =

TPCExample: $100,000 gift x 5 (years) = $500,000 (TPC)

$5,000 in political campaign donations in a cycle = $100,000 in philanthropic capacity

Gift Calculators• Charity Navigator Giving Calculator:

http://www.charitynavigator.org/index.cfm?bay=content.view&cpid=40

• Hoosier Christian Foundation Giving Calculator:http://www.hoosierchristian.com/calculator.asp

• Ask Analyzer: https://www.askanalyzer.com/

Collections

Hobbies

Toys

Lifestyle

Philanthropies

Downsizers

Inheritors

Internationals

Who else?

Establish a philosophy. Share it with your team (via a white paper or a special meeting). Listen to their feedback. Make a plan for dealing with their objections.

Establish a capacity rating approach for your entire team. Decide which formulas work for your team.

Establish a process, including back-up. Be prepared to be challenged.

Prepare to review capacity ratings as new information emerges through contacts and cultivations.

Be consistent. Keep up with trends. Talk to other researchers. Adapt

as changes unfold.

“Capacity Ratings;” presented by Lisa Howley, 2004 APRA Conference.

“Understanding Compensation Practices & Estimating Income.” presented by Jill Meister and Debra Westerberg; 2005 APRA Conference.

“Assessing the Value of Real Estate;” by Cliff Anderson; 2005 APRA Conference.

“Estimating Net Worth: One Organization's Search for Truth;” University of Virginia Research Department; 1998; http://www.usc.edu/dept/source/NetWorth2.htm.

“How Much is that Donor in Your Records?” by Roger R. Millar;

CASE Currents; 1995.