day 2 - welcome to united nations escap rebel applied ppp... · • internal “business case” of...

TRANSCRIPT

1

DAY 2

Applied Workshop on Preparing Infrastructure Projects

21th - 25th March Bangkok

2

Recap of Day 1

3

Applying central concepts to structuring PPP projects

• S1: Project screening

• S2: Defining project characteristics

• S3: Output specification

• S4: Risk allocation

• S5: Project structuring

• S6: PPP Contract

• S7: Contract Management Plan

• S8: Procurement Planning

4

Session 2: Project Characteristics and PPP Financing

5

Basic Characteristics

• What is the public service (infrastructure) ?

• Who are the users ?

• Greenfield (new) or brownfield (existing) ?

• What is involved in the service? (e.g. station, infra, trains, signaling, etc…; generation / transmission / distribution, etc…)

• What assets are involved (e.g. buildings, facilities, equipment, etc.) ? – Large, small; complex, simple; etc… – What scale of investment? – How long do these assets last?

• Project life-cycle costs – initial investment versus operation & maintenance ?

• How does the funding / payment work ? (next slide…)

6

• Need to consider the full Project Lifecycle – all costs and revenues over project life (e.g. 25 yrs)

• Lifecycle optimization (e.g. capex-maint. balance) • NPV

• Increase value by decrease investment costs or operating costs, increase revenues during and after operation , pull revenues forward in time and push costs back.

Project Life Cycle Optimization / Perspective

Koste

nO

pbre

ngste

n

Tijd

Capital expenditure

Operational expenditure

Operational revenues

Post-operational value

Exp

en

se

s

Reve

nu

es

7

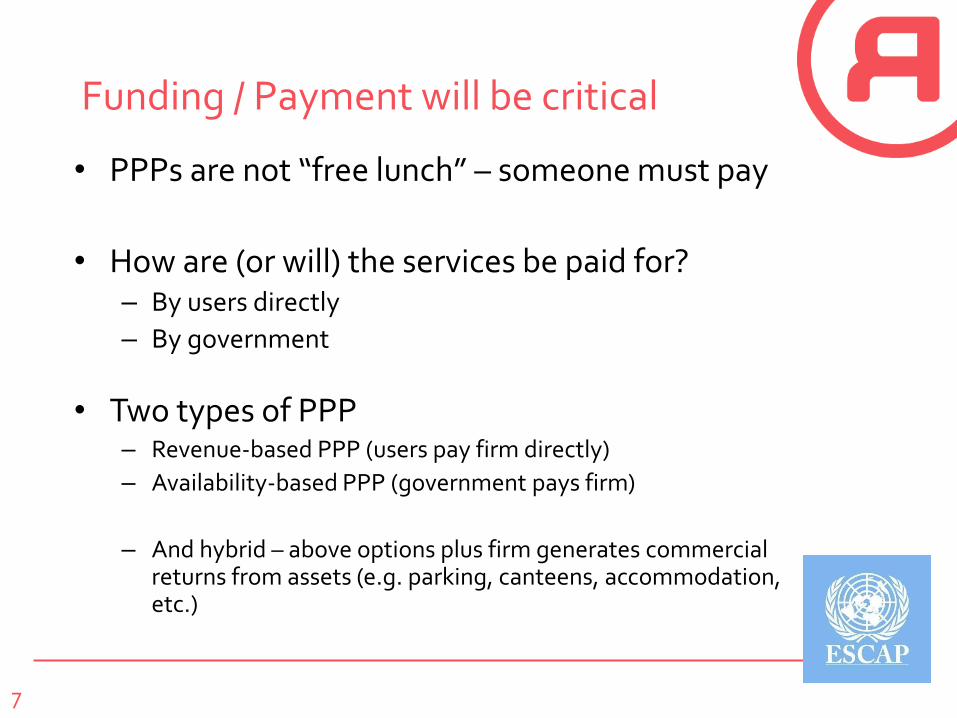

Funding / Payment will be critical

• PPPs are not “free lunch” – someone must pay

• How are (or will) the services be paid for? – By users directly

– By government

• Two types of PPP – Revenue-based PPP (users pay firm directly)

– Availability-based PPP (government pays firm)

– And hybrid – above options plus firm generates commercial returns from assets (e.g. parking, canteens, accommodation, etc.)

8

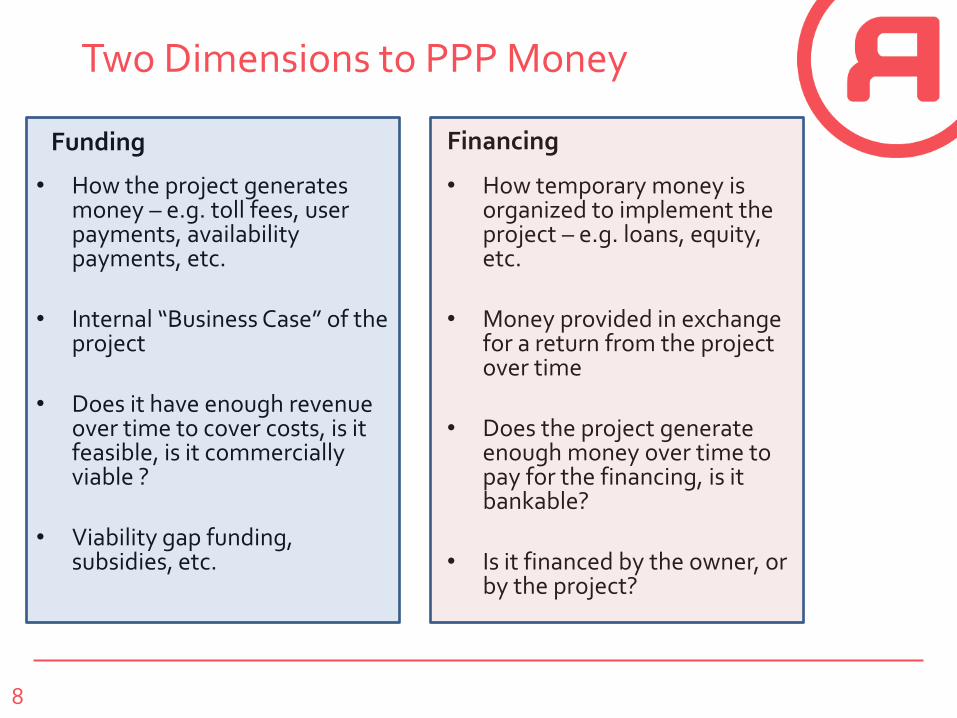

Two Dimensions to PPP Money

Funding

• How the project generates money – e.g. toll fees, user payments, availability payments, etc.

• Internal “Business Case” of the project

• Does it have enough revenue over time to cover costs, is it feasible, is it commercially viable ?

• Viability gap funding, subsidies, etc.

Financing

• How temporary money is organized to implement the project – e.g. loans, equity, etc.

• Money provided in exchange for a return from the project over time

• Does the project generate enough money over time to pay for the financing, is it bankable?

• Is it financed by the owner, or by the project?

9

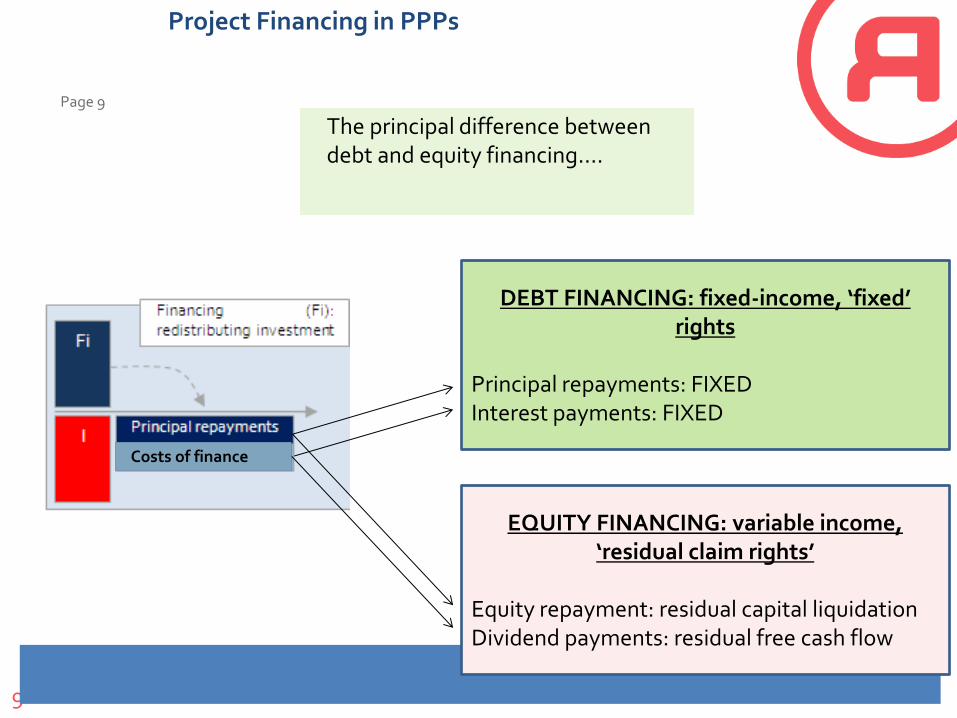

Page 9

Project Financing in PPPs

DEBT FINANCING: fixed-income, ‘fixed’ rights

Principal repayments: FIXED Interest payments: FIXED

EQUITY FINANCING: variable income, ‘residual claim rights’

Equity repayment: residual capital liquidation Dividend payments: residual free cash flow

Costs of finance

The principal difference between debt and equity financing….

10

Two Main Forms of Financing

Corporate Finance

• The ‘company’ borrows

• Multiple projects

• All company assets at risk

• Balance sheet financing

• Risk is an input

• Exit not clearly defined

• ‘On balance sheet’ of the

company

Project Finance

• The ‘project’ borrows

• One project, one cash flow

• Non or limited recourse

• Focus on project risks

• Limited life span / clearly defined exit

• ‘Off balance sheet’ of the company

11

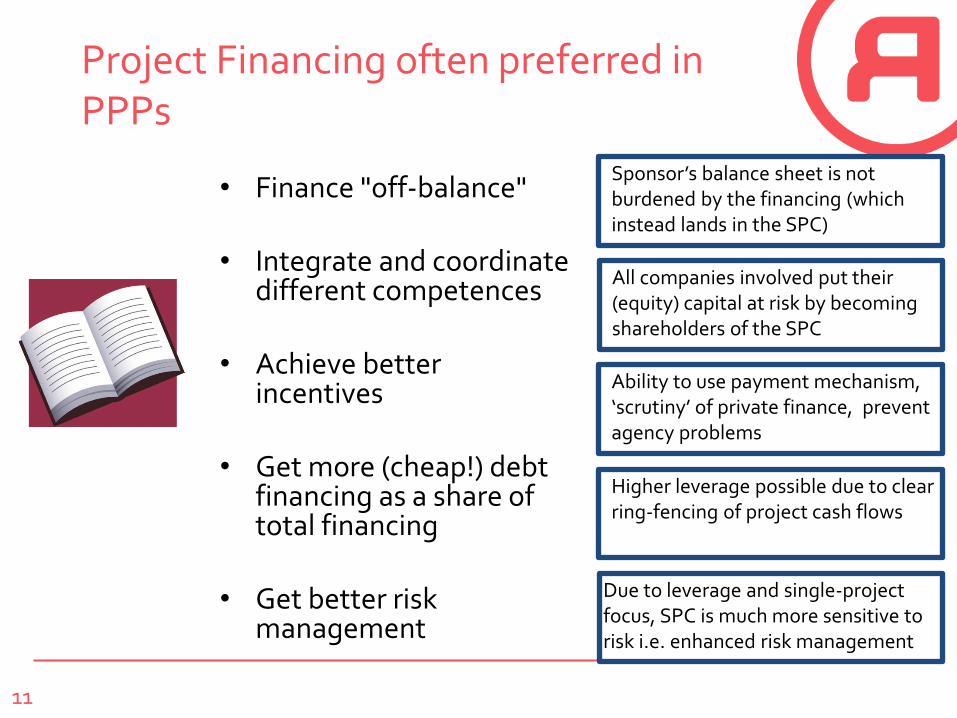

Project Financing often preferred in PPPs

• Finance "off-balance"

• Integrate and coordinate different competences

• Achieve better incentives

• Get more (cheap!) debt financing as a share of total financing

• Get better risk management

Sponsor’s balance sheet is not burdened by the financing (which instead lands in the SPC)

All companies involved put their (equity) capital at risk by becoming shareholders of the SPC

Ability to use payment mechanism, ‘scrutiny’ of private finance, prevent agency problems

Higher leverage possible due to clear ring-fencing of project cash flows

Due to leverage and single-project focus, SPC is much more sensitive to risk i.e. enhanced risk management

12

Page 12

Project Financing in PPPs

-2,000,000

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

Operational Taxes Investment Financing Dividend Cash

• A typical (but fictional) project finance cash flow

13

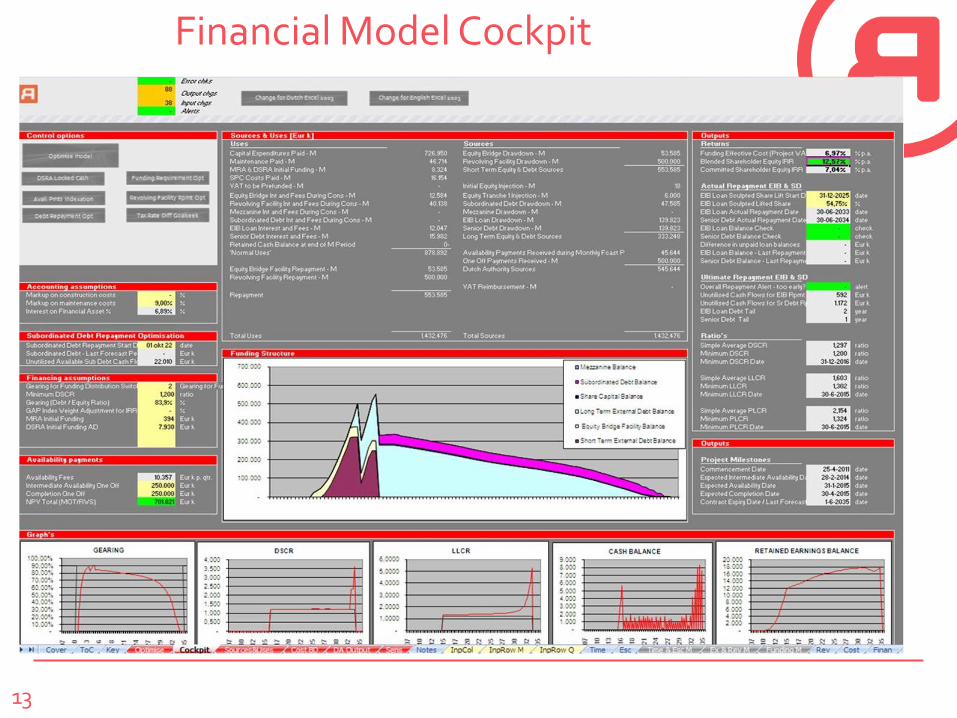

Financial Model Cockpit

14

Financial Flows

Often used measures:

• NPV (net present value): Total of all future cash flows in terms of todays’ money. (should be a positive number)

• IRR (internal rate of return): What is the return the investor makes?(should be higher than you get at the bank, because the project is probably riskier)

• Pay back period: how long does it take to pay the investor back? (should be shorter than the project duration)

• DSCR (debt service coverage ratio): will there be enough money to pay the interest and repayment of the bank ?(in the case that a bank supplies part of the financing) (should be (much) larger than 1 in every year)

15

Effects of Private Financing on Projects and the Market

• De facto cost of financing higher than pure public financing BUT

• Discipline from the financial markets – and market ‘memory’

• High scrutiny of the underlying project characteristics (performance, risks, revenues, etc.)

• Strong focus on capacity of the participating firms

• Close scrutiny and performance pressure on the public partner (e.g. Dabhol Power Plant effect)

• Continuous pressure from debt providers on private operator performance (ultimately with step in rights)

• Requirement for longer term (equity and debt) providers – opening especially role of institutional investors

16

• Government budget often lacks capital expenditure to invest in:

– Proper maintenance

– Rehabilitation

– New projects

Public Budget Project / Investment Constraints

- $$

(Budget

Spending)

1 2 3 4 5 6 7 8 9 10

Years

Capital Expenditure

“Hurdle”

17

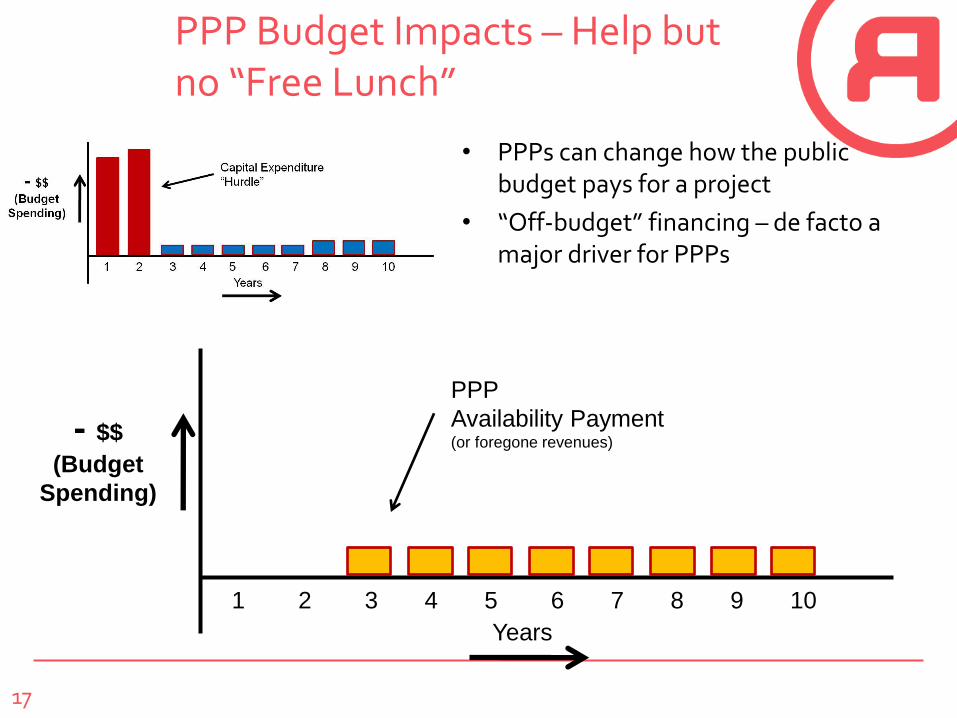

• PPPs can change how the public budget pays for a project

• “Off-budget” financing – de facto a major driver for PPPs

PPP Budget Impacts – Help but no “Free Lunch”

- $$

(Budget

Spending)

1 2 3 4 5 6 7 8 9 10

Years

PPP

Availability Payment (or foregone revenues)

18

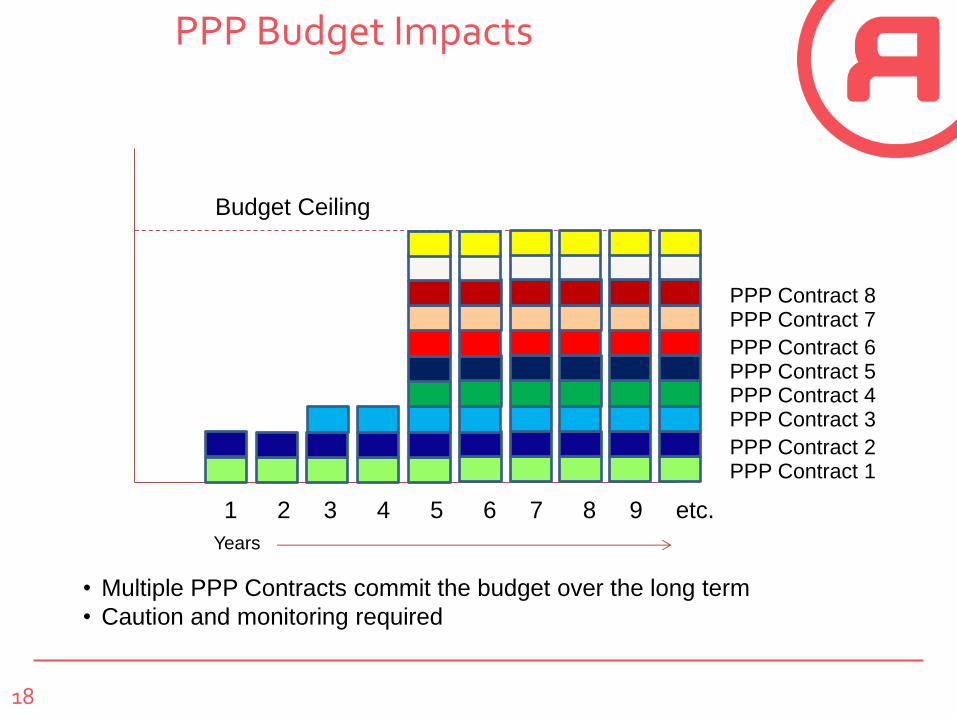

PPP Budget Impacts

Budget Ceiling

1 2 3 4 5 6 7 8 9 etc.

• Multiple PPP Contracts commit the budget over the long term

• Caution and monitoring required

PPP Contract 1 PPP Contract 2

PPP Contract 3 PPP Contract 4 PPP Contract 5 PPP Contract 6

PPP Contract 7 PPP Contract 8

Years

19

Viewing effects in financial model

• Variables affecting basic business case (“funding”): – Capex

– Opex / maintenance

– Traffic

– Tariffs

• Variables affecting financing costs (“financing”): – Debt interest rates

– Leverage

• Importantly, keep financing and the basic business case NPV separate – “if I can get financing cheaper than you, that says nothing about the project itself…”

20

Case Work

• Review and discuss your project

• Discuss and describe project characteristics: – Service

– Users

– Greenfield / brownfield

– Assets / scale of investment

– Duration of assets

– Lifecycle costs – initial investment versus operational

– Funding

• Be prepared to make a brief report back to plenary

21

Session 2 Plenary Group Report Back

22

Session 3: Output Based Specification

23

Applying central concepts to structuring PPP projects

• S1: Project screening

• S2: Defining project characteristics

• S3: Output specification

• S4: Risk allocation

• S5: Project structuring

• S6: PPP Contract

• S7: Contract Management Plan

• S8: Procurement Planning

24

Output Specification

• A central part of the RfP / ToR for the project

• What service must the project deliver?

25

What is Input Specification?

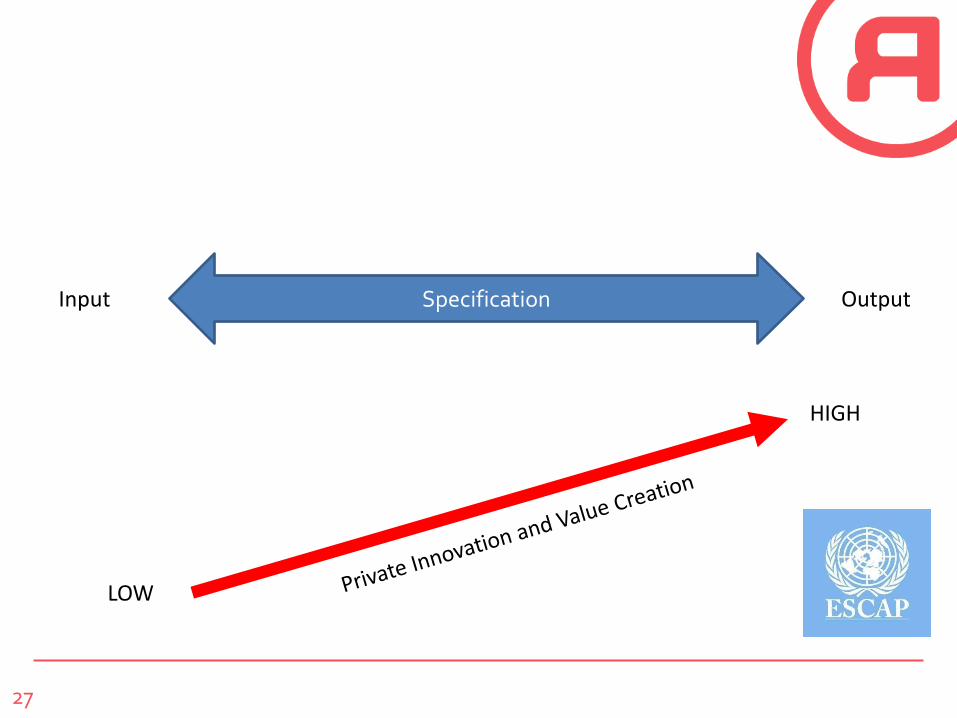

• EXAMPLE OF A BRIDGE CROSSING A RIVER

• Government prepares detailed specification for a bridge (input)

• Government determines exactly how it should be built, what materials used, and makes the detailed plan and design (input)

• Construction company is hired to build the bridge (usually based on cheapest price) – construction contract

• If the bridge does accommodate the traffic (or could have been better or cheaper) it is the government’s problem

• Consequence of Input Specification:

• Limited private innovation (they just build what government asks for)

• All design, operation and maintenance risk stays with government

26

What is Output Specification?

• Government specifies it wants traffic to cross the river (output)

• Government invites companies to propose the best solution (this could be a bridge, a ferry or a tunnel)

• Government hires the company with the best solution to provide that solutions – PPP Contract where company only gets paid over future years if their solution works

• Consequence of Output Specification: – Space for private companies to innovate and determine best solution

– Company is at risk over time if their solution does not work (hence they will get it right)

27

Specification Input Output

LOW

HIGH

28

Minimum Standards

• Output specification in conjunction with minimum standards

• Minimum standards, for example: – Environmental norms – Transport safety requirements – ISO certification / accreditation – Health and safety standards – Labour and employment standards – Civil Aviation Authority (CAA) regulations – And so on…

• Specify minimum standards as a compliance requirement (e.g.

must comply with applicable road safety standards), or a performance / output requirement (e.g. must obtain relevant accreditation within xyz period)

• Minimum standards requirements can still leave scope for the private partner to determine the best way for these to be achieved

29

Output Specification is a BIG CHANGE for government

• Usually new approach, with consequences

• Can be more difficult to do than input specification

• Should cover ouputs required as well as minimum standards (e.g. environmental requirements, etc.) that must be met

• Should be able to be monitored and measured in practice:

– Contract compliance manager – External agencies (e.g. regulators, oversight bodies, ISO certifiers)

30

Case Work

• Discuss your project

• Define a few main possible output specifications for the project

• Indicate whether and how each one will allow for private innovation

• Indicate how the output could be monitored and measured

• Identify if any minimum standards would apply to the project

• Be prepared to make a short report back to the plenary

31

Session 3 Plenary Group Report Back

REBELGROUP.COM

Rebel Wijnhaven 23 3011 WH Rotterdam Nederland

Rolf Dauskardt [email protected] +31 612506624 (mobile)

Patrick Rosales [email protected] +63 916 532 6768 (mobile)