day eaic daily - asia insurance revie€œas of today, brexit: ... the very real threat of emerging...

TRANSCRIPT

EAIC Daily3Day

Thursday, 13 October 2016

Sponsors:

EAIC Chief Delegates alongside the 28th EAIC Organising Committee at the opening ceremony.

Changing consumer expectations and demo-graphics require insurers to remain dynamic and

innovative in adapting their products and distribution to current needs, said Mr Anselmo Teng Lin Seng, Chairman of the Board of Directors of the Monetary Authority of Macao.

He noted that changing customer expectations will have implications for both product design and service delivery, and insurers will have to constantly remodel their propositions to keep up with the evolving consumer outlook.

One example is how life insurers have changed their marketing to focus on the pursuit of healthy lifestyles, he said. Digital technology

Be ever-responsive to changing needs

Mr Anselmo Teng Lin Seng

Continued on page 2

also requires insurers to improve their level of engagement and ac-cessibility online.

But in the era of technology, insurers should step up their risk management efforts in the face of cyber threats.

“It’s become more of a challenge to secure data, so I encourage market participants to balance your risk while pursuing new niches,” he said.

Turning to Macau, he said the market will continue to strengthen its supervisory regime by remaining vigilant on IAIS guidelines. He added Macau is currently in the process of raising the standard of insurance intermediaries and will soon launch a professional training scheme for this segment.

Brexit is arguably one of the biggest developments in 2016, a decision which reverberated around the world. But what does this mean for the insurance industry and what are the

lessons for the region here? Mr Kent Chaplin, CEO, Lloyd’s, Asia Pacific, cited a

recent KPMG report on the implications of Brexit in ASEAN. It suggests that companies in ASEAN need to examine the implications of a potential loss of access to the Single Market via subsidiaries in the UK.

However, they should also consider the potential upside of new trade deals between the UK and ASEAN states as a result of the UK’s new-found status. Once the UK is free to do so outside the EU, the UK’s new Department for International Trade will be seeking to conclude free trade agreements quickly. “Malaysia’s Prime Minister has also said he sees Brexit as an opportunity to improve relations, especially in trade and investment,” he added.

It is probably too early to tell what will eventually happen. Even though UK Prime Minister Theresa May declared her intent to start the two-year process of leaving the EU in March next year. “As of today,

Brexit: Implications and lessons learnt

Mr Kent Chaplin

Market players should continue to cultivate the dynamism of Asia’s insurance sector in order

to support the region’s rapid economic growth, said Mr Jiang Yi Dao, President of the Macau Insurance Association at yesterday’s opening ceremony.

“In the next decade or two, Asia will become the global economic growth engine and the region’s insur-ance industry can be propelled by this growth, so we need to look after our insurance environment in order to support economic growth,” he said.

A critical element in the sustainability of the sector is the development of new talent and in that regard, the EAIC’s latest initiative to launch the “Young Insurance Practitioners Programme” is a timely move, said Mr Steve Chen, President of the EAIC.

Member cities of EAIC nominated two insurance practitioners under-35 to attend this year’s conference, as both a means to mark Insurance Day, but also crucially

Mr Jiang Yi Dao

Mr Steve Chen

Securing future of the industry

EAIC Chief Delegates at the traditional “Dotting the Lion’s Eye“ ceremony

believed to usher in good luck.

nothing has changed. The UK is still very much a full member of the EU,” said Mr Chaplin.

Benefits of market harmonisation As to what Asia can learn from it, he said that the case of the EU has shown the benefits of greater market harmonisation. It enables the industry to be closer to its customer to better cater to their needs and provide greater value.

“At Lloyd’s we support the importance of building integrated agree-ments and access to trade and services freely across the region. From an insurance perspective, this permits insurance clients unrestricted access to the growing capacity and expertise available across the region,” said Mr Chaplin.

On the regulatory front, he said that in the case of ASEAN with its

varying levels of economic development, it is important to proceed at the pace that the individual markets are comfortable with. In the ASEAN Economic Community (AEC), this may well translate into en-suring the local supervisors retain supervisory responsibility for local insurers.

A model worth looking at is the European Insurance and Occupa-tional Pensions Authority – the EU’s “super regulator”. He said that the Authority has the considerable responsibility for the form that insurance regulation takes in the EU. However, it does not have the day-to-day responsibility for the regulation of individual insurers within the EU, which remains with the national supervisors.

“The greater harmonisation of regulatory regimes across markets will drive improvements in local knowledge and technical expertise,” he said.

Brexit: Implications and lessons learnt from page 1

“Generation Y”, in some cases already the industry’s current generation of customers, are significantly more engaged.

“This is true across every channel and across every geography. This is an absolutely universal phenomenon, that we have a generation that is growing up wanting to be more empowered and more engaged with service and product providers,” said Mr Andrew Rear, Chief Executive of Digital Partners, Munich Re. Digital Partners is a global, multi-line business working with startups and other businesses which are disrupt-ing insurance.

What does the “chair” say? Consumer expectationsBut is the industry ready to engage them?

Figure 1 shows the three expectations that consumers have of providers.

Digital innovation is not about taking physical forms and sticking them on the internet, he said.

The empty chairTo meet these customers’ expectations and to improve customer centricity, he cited Jeff Bezos, founder of Amazon, who recognised the importance of keeping the customer in mind by having an empty chair during meetings and asking “What does the customer say?”

For the insurance industry, the “customer” in the empty chair is likely to tell us:

• We need to stop building propositions around our industry and our legacy system and start building propositions around the way customers perceive their own needs.

• We need to stop delivering products to suit our channel structure and start delivering products to suit the way our customers want to live their lives.

• We need to stop treating our customers like strangers that we need to question before we allow them into our club and start engaging customers through data that they are willing to share with us.

“I believe that as an industry we can do this and we can become a customer-centric industry,” he concluded.

to encourage more participation from younger insurance professionals at the EAIC conference in order to regenerate the industry.

The nominated delegates will also have the opportunity to submit suggestions to improve the EAIC conference, added Mr Chen.

Design how customers see the

world

Deliver how customers live

their lives

Build engagement

from customer data

Mr Andrew Rear

Figure 1: Three expectations consumers have of providers

In line with our mission “to be innovative in providing reinsur-ance solutions and prompt responses, always”, we continuously work towards strengthening our value proposition to our Busi-

ness Partners. Customer Centricity is key. One such way is by means of thought leadership. In the summer of

2016, we were pleased to partner with the renowned Dr. Schanz, Alms & Company AG in Switzerland to produce a research paper entitled “The Changing Global Energy Landscape: Opportunities and Chal-lenges for Energy Underwriters”. Here is a look at the key themes of the paper, as well as the growing importance of sound Enterprise Risk Management (ERM) practices. The latter are especially relevant given the very real threat of emerging risks such as terrorism and cyber.

Global energy demand by source, sector and supplyA number of factors, including economic, political, technological and societal, determine the development of the global energy market. Today’s largest oil consumer, the United States, will see its oil con-sumption decline by about 25% until 2040, due to higher efficiency standards for passenger as well as heavy duty vehicles. In contrast, India’s demand for oil will rise strongest, followed by China.

World oil production is predicted to grow by 15% - 30% until 2040, depending on the source of research and the underlying scenario applied. Other than oil, all sources for electricity generation are projected to increase, including nuclear. For the foreseeable future, fossil fuels will remain the dominant source of energy.

An overview of global energy and power insurance marketsIn upstream energy markets, from 2014 to 2015 alone, premium volumes have dropped from about US$3 billion to $2.3 billion; at the same time, overall losses whether insured or not, have risen. Likewise, in the downstream sector premium volumes are being eaten away fast, as a result of abundant capacity and increasing reliance on captives. Contrary to the upstream sector, however, losses recorded in downstream are much less.

Volatile oil prices have impacted the upstream and downstream sectors dif-ferently. In the former, an increasing number of clients have opted for lower programme limits and higher self-retentions despite the fact that the decline in oil

prices has reduced the scope for a “natural” hedging of exposures. Whereas in the latter, the contrary is true: the sharply reduced cost of feedstock has boosted refiners’ margins, with business interruption values up accordingly.

Further consolidation is very likely given the current turmoil af-fecting the global oil and gas industry, implying that the demand for energy insurance capacity will come under additional pressure.

A changing risk landscapeSound Enterprise Risk Management (ERM) practices are a further way in which reinsurers can add value to stakeholders. The risk landscape is changing fast, presenting both challenges and opportunities.

With reference to the energy sector, technological progress is of particular relevance. One example is the rise of subsea drilling, as opposed to traditional platform-based field drilling. Statistics reveal that such completions operate relatively smoothly after the initial installation. In addition, they are economically advantageous and offer environmental benefits.

Another relevant trend is risk concentration. It presents major un-derwriting challenges in most areas of energy and power insurance. A further development to monitor is supply chain risk, as exemplified by the Tohoku earthquake, the Thai floods and the Tianjin blasts.

Emerging risks: Terrorism and cyberBy now, terrorism has become a global phenomenon. Although particularly highly concentrated in a few countries, it is spreading to more. Terrorism continues to be a threat with the resulting growing need for, and uptake of, terrorism and political violence insurance by businesses as a risk mitigation measure. Trust Re provides Terrorism & Political Violence cover as part of its Specialty Lines reinsurance offering.

Cyber-attacks are placed within the top ten global risks in terms of likelihood and have become increasingly relevant for many compa-nies, especially due to the growth in use of cloud computing, social media and big data. The energy sector is certainly not immune to the threat of terrorism or cyber-attacks.

Against the backdrop of a rapidly changing operating environ-ment in the energy sector, those who embrace the opportunities of ERM as both a risk mitigation measure and value-added proposition are those most likely to weather the current storm. The same is surely true for the non-energy sector.

To read the full research paper, please refer to www.trustre.com/en/home/perspectives_details?id=21

Drivers of change in the energy market and risk landscapeMr Kamal Tabaja, Group Chief Operating Officer, Trust Re, shares the key findings of “The Changing Global Energy Landscape: Opportunities and Challenges for Energy Underwriters”, the research paper produced in partnership with Dr. Schanz, Alms & Company.

Mr Huy Vatharo,Phnom Penh

Mrs Esther C Tan,Manila

Growth, growth, growth

Those were the three keywords at yesterday’s City Reports by the chief delegates of the 12 member cities of the EAIC. The fact that Asia is growing economically is nothing new, but the

numbers shared yesterday spoke volumes of the potential lying latent in the insurance industry.

Each of the 12 member cities reported respectable growth in both life and non-life sectors, as well as not-inconsiderable growth in insur-ance penetration numbers, as eachchief delegate briefly shared the current market conditions and some future plans in their respective markets.

Even Indonesia, which had seen sluggish economic growth in the last two years, was able to report a 12% y-o-y growth in gross written premiums, for both the life and general insurance sectors. Cambodia, the smallest market amongst the 12, reported a massive 40% growth in gross written premiums for the general sector, and a 240% increase in premiums for the life market (bearing in mind that life insurance in Cambodia has only existed for a few years).

The Philippines boasted a 7% growth in their GDP in 2015, making them the fastest growing member, and in the same year also recorded a premium growth of 18.8% in life, and a 7% increase in general insur-ance premiums. This same success has them aiming for an insurance penetration of 3% of the national GDP by 2019 (up from the 2% it currently stands at).

Much of the growth for the general insurance field was driven, un-surprisingly, by motor insurance, most of which is mandatory in most markets. Standouts include Brunei, Thailand and Taiwan, where motor insurance accounted for at least 50% of the general insurance pie.

Within the life insurance sector, bancassurance proved to be a strong avenue of distribution, coming close to matching the efforts of the many life insurance agents that work across the region.

Always forwardMuch of the growth in the region was catalysed by government and industry initiatives to increase insurance awareness, enhance edu-cation and improve the perceived value of insurance amongst the general public. Malaysia has recently implemented the Life Insurance and Family Takaful Framework to increase penetration and consumer knowledge, while Japan has introduced several schemes to target the rapidly aging population with great results. Meanwhile, the Philippines insurance industry is developing a curriculum aimed at high school students to educate them on the value of insurance.

Japan’s measures to protect their elderly population – by 2040,

City Reports by Chief Delegates

Mr A K Cher, Singapore

Haji Osman Bin Haji Md Jair,

Bandar Seri Begawan

Mr Arnon Opaspimoltum,

Bangkok

Mr Ronnie Ng,Hong Kong

Mr Yasril Y Rasyid,Jakarta

Mr Antony Lee,Kuala Lumpur

Mr Chris Ma,Macau

Mr C M Jang,Seoul

Dr Cheng-Te Liang, Taipei

Mr Akio Negishi,Tokyo

it is estimated that one third of the population will be aged 65 and above – include service guidelines for the elderly implemented by the Life Insurance Association of Japan (LIAJ) and the General Insurance Association of Japan (GIAJ), rebranding life insurance as an inheritance tax-saving measure and an increased emphasis on healthcare and nursing care.

These initiatives have proven to be successful in capturing this rap-idly growing market segment (a segment that is also steadily growing in other parts of Asia, such as Hong Kong, Thailand and Singapore), with 19.6% of all life insurance policies being held by citizens aged 60 and over.

Laying the groundwork for the futureWhile Japan focused on its elderly, the ASEAN nations set their sights on cultivating their youth. Chief delegates of Singapore, Hong Kong and Malaysia spoke of youth internship programmes and their success in attracting and grooming the next generation of insurance talent.

Besides the education curriculum being developed in the Philip-pines, the Malaysian industry also innovated with the Youth Video Awards, capitalising on social media and video-sharing site Youtube to capture the attention of an entirely fresh and new customer-base.

Malaysia is not alone in utilising technology. Hong Kong, already well known for its strong FinTech presence, set up a task force in Sep-tember 2015 to further promote mobile and digital technology, with insurance being one of the industries set to benefit.

Taiwan’s FSC is also looking at implementing policies to develop a FinTech business model, as part of their long-term strategy to increase insurance penetration, and Macau is following closely on their heels.

Further, Korea, already the most connected city in the world, are poised to take advantage of their infrastructure to improve data col-lection and adapting the industry to technology and social media developments.

Chief Delegates

Although there is much that is still unknown about the Zika virus, which is spread primarily by the Aedes species of mosquito to humans primarily through infected insect bite,

the early research does not leave much room for optimism. In fact, top US health officials have stated that the Zika virus, and its link to birth defects and neurological disorders, is worse than they originally suspected. Given this information, we can anticipate that the strain on healthcare facilities will be significant.

The front line diagnosticians (primary care physicians, OB/GYNs, emergency room physicians, etc) have the first opportunity to iden-tify patients who have been exposed to the Zika virus. The Centers for Disease Control (CDC) in the US has produced testing algorithms related to pregnant women who have travelled or who reside in an area with Zika, as well as for infants who may have been exposed to the virus. And with the recent discovery of an “almost certain” link to Guillain-Barré syndrome, these clinicians need to be mindful of the signs and symptoms of that rare condition as well.

We can also anticipate that there will be an additional strain on laboratories as healthcare providers order blood tests to look for Zika. The CDC has a permanent lab set up in Puerto Rico, and recently has begun importing staff and equipment to conduct 100,000 blood tests a year (which is five times as many as it can do now). It is unclear whether this will even be enough, as top officials predict that over the next year more than four million people could be infected, but it is a start. All Zika testing is to be coordinated through the CDC, and the Federal Drug Administration has issued an Emergency Use Authorization (EUA) for a diagnostic tool for the Zika virus that will be distributed to qualified laboratories and, in the US, those that are certified to perform high-complexity tests.

Insurance risks linked to Zika Although the current focus is on research and prevention of the Zika virus and the health risks it poses to the population, we should also consider the risks it could pose to the business side of healthcare.

In the medical malpractice world, there may be claims for wrongful birth due to failed or inaccurate tests performed during pregnancy. The average cost of caring for one child with birth defects can be over US$10 million. There could also be claims alleging failure to diagnose where the damages could be equally severe. And what role might “batch” claims play in this scenario? Thirty claims all over $10 million each would exhaust most insurance towers.

These are admittedly hypothetical worst-case scenarios, but are worth consideration nonetheless. They also highlight the need for accurate and timely testing, which in a situation where the volume of ordered tests outpaces the labs equipped to handle them, can be precarious at best. As CDC director Thomas Frieden has said, at some point Zika cases will increase “not steadily, but dramatically.”

Healthcare facilities will also want to be mindful of their business continuity plans. And though many organisations purchase business interruption insurance, coverage for lost revenue arising out of a non-physical damage event (such as a quarantine of facilities or medical professionals) may not be available on some business interruption coverage forms.

Risk management strategies for Zika In talking with some of the most sophisticated healthcare organisa-tions about their approach to managing the Zika virus, it is evident that it is still early stages even for them. Thus, at this time, the risk manage-ment strategies for Zika are not unlike those for other pandemics. This may change as we continue to learn more about Zika.

In most healthcare organisations, pandemic preparedness is man-aged through an infection control plan. It is vital that an organisation’s infection control specialist have a close working relationship with the local health department, as they will be the first to receive information from the CDC about the early identification and management of any widespread disease.

For individuals, the focus must be on limiting exposure to areas with mosquitoes that are known to spread the Zika virus, wear long-sleeved shirts and pants, and use appropriate insect repellents. According to Mr Frieden, “There is nothing about Zika control that is quick or easy. The only thing quick is the mosquito bite that can give it to you.”

Impact of the Zika virus“Batch” claims all over US$10 million each are a hypothetical worst-case scenario but worth consideration nonetheless. Ms Kristen Kenst, AVP, Healthcare Underwriter for North America – Healthcare Division, Allied World, discusses insurance risks and risk management strategies in coping with the Zika virus.

It’s like spending quality time with an old friend...

if they were a specialist in designing creative marine reinsurance solutions.

Build a lasting partnership with Endurance Re.Anchored in deep marine expertise, we work closely with our clients to truly understand their exposures and develop creative risk solutions. Endurance Re is uniquely positioned to help navigate your marine risks. www.endurance.bm

ENDUR_Marine_Re_210mmx297mm_Ad_Due1006.indd 1 10/7/15 5:04 PM

Diary of events 2017

10th India Rendezvous18-20 JanuaryTaj Lands End, Mumbai, India

Asia CEO Insurance Summit21-22 FebruarySingapore

Asia Insurance Brokers’ Summit6-7 MarchSingapore

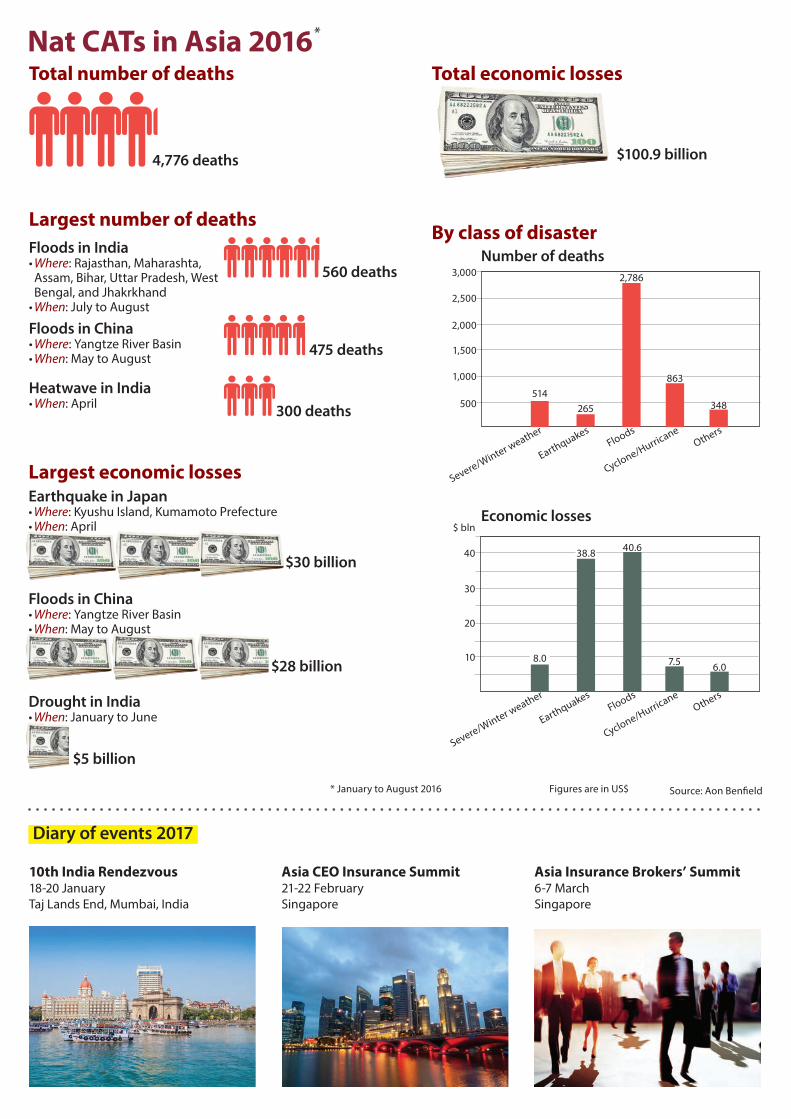

Nat CATs in Asia 2016*

$5 billion

$30 billion

$28 billion

Largest economic lossesEarthquake in Japan• Where: Kyushu Island, Kumamoto Prefecture• When: April

Floods in China • Where: Yangtze River Basin• When: May to August

Drought in India• When: January to June

Heatwave in India • When: April

Largest number of deathsFloods in India • Where: Rajasthan, Maharashta, Assam, Bihar, Uttar Pradesh, West Bengal, and Jhakrkhand

• When: July to August

Floods in China • Where: Yangtze River Basin• When: May to August

560 deaths

475 deaths

300 deaths

40

30

20

10

$ blnEconomic losses

Severe/Winter weather

Earthquakes

Floods

Cyclone/Hurricane

Others

8.0

38.8 40.6

7.5 6.0

Total number of deaths

4,776 deaths $100.9 billion

Total economic losses

Source: Aon BenfieldFigures are in US$* January to August 2016

By class of disaster

3,000

2,500

2,000

1,500

1,000

500

Number of deaths

Severe/Winter weather

Earthquakes

Floods

Cyclone/Hurricane

Others

514265

2,786

863

348

EAIC Daily newsletter team(L-R): Editor-in-Chief: Sivam Subramaniam • General Manager, Business Development: Sheela SuppiahEditorial Team: Benjamin Ang, Ridwan Abbas, Zaki Ahmad, Chia Wan Fen • Design & layout: Charles Chau www.asiainsurancereview.com • www.meinsurancereview.com

www.endurance.bmwww.aonbenfield.com www.swissre.comwww.scicollege.org.sgwww.moorestephensconsulting.com www.trustre.com www.awac.com

Sponsors

After a busy first day at the conference, it was time to wind down with cocktail parties dotted around the famous Macau strip as several market players played host to the delegates.

Winding down the night