d&b us economic health briefing (feb. 2014)

TRANSCRIPT

Paul Ballew, Chief Data & Analytic Officer, D&B

February 6, 2014

Introducing A New Way To Assess U.S. Economic Activity

Follow us on Twitter #DnBEconomy

#DnBEconomy

Introducing D&B’s Economic Health TrackerA multi-dimensional view of the economy

3

Small Business Health Index

The Small Business Health has been remarkably stable for the first time post recession

Some signs of modest softening but the US is still positioned to grow above 2%

4Source: D&B Proprietary Data

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 201370

75

80

85

90

95

100

105

Overall Small Business Health Index: Past 3 years

2011 2012 2013

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Overall Small Business Health Index: YOY Changes

The recovery process for small businesses remains uneven

Industries which seemed to be lagging behind in the recovery process are gradually accelerating

5

Manufacturing Transportation Personal Services-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Small Business Health Index by Vertical: YOY Changes

2011 2012 2013

Source: D&B Proprietary Data

…. And a few sectors that bounced back quickly have leveled off

On the other hand, industries which were initially leading the recovery have slowed down in the past year

6

Retail Real Estate Business Services Construction-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Small Business Health Index by Vertical: YOY Changes

2011 2012 2013

Source: D&B Proprietary Data

Credit growth has accelerated for small businesses

Post recession, the small businesses have experienced more credit growth through the more conventional avenues, although credit card loans have also been on the upturn in the past two years

7

2010 Q1

2010 Q2

2010 Q3

2010 Q4

2011 Q1

2011 Q2

2011 Q3

2011 Q4

2012 Q1

2012 Q2

2012 Q3

2012 Q4

2013 Q1

2013 Q2

2013 Q3$17,200

$17,600

$18,000

$18,400

$18,800

$19,200

Credit Card Current Balances ($M)

2% decline

4% rise in the

past 2 years

2010 Q1

2010 Q2

2010 Q3

2010 Q4

2011 Q1

2011 Q2

2011 Q3

2011 Q4

2012 Q1

2012 Q2

2012 Q3

2012 Q4

2013 Q1

2013 Q2

2013 Q3$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

$75,000

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

Loans Current Balances

Commercial & Industrial Loans, All Commercial Banks ($Bn, left)Small Business Loans, D&B Database ($Mn, right)

44 % growth

Overall credit usage and availability has improved

Although still falling short of pre-recession levels, access to credit for US businesses is on an upturn

8Source: D&B Proprietary Data

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Card Utilization Index

Y/Y

Perc

enta

ge C

hg.

9

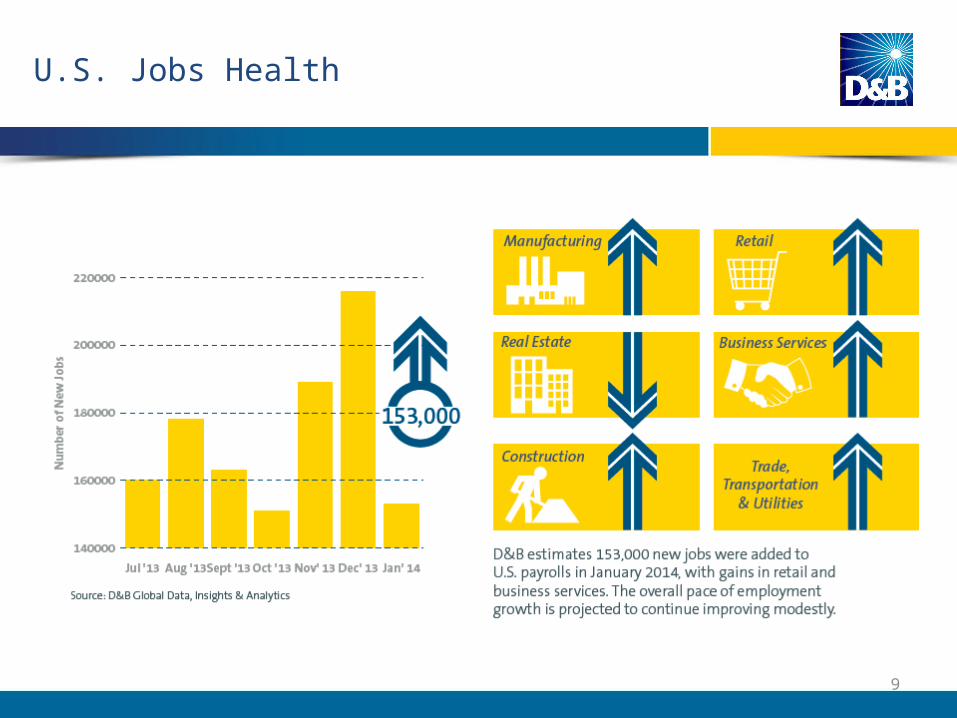

U.S. Jobs Health

10

U.S. Business Health Index

U.S. Business Health Index

11

Dec-10

Feb-11

Apr-11

Jun-11

Aug-11

Oct-11

Dec-11

Feb-12

Apr-12

Jun-12

Aug-12

Oct-12

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

44

46

48

50

52

54

56

Overall

• The overall US business health index improved in January for the fourth-consecutive month—reaching 52.8%.

• This was the highest level recorded since the inception of the index in December 2010.

U.S. Business Health Index

12

• On a year-over-year basis the overall index increased 5.9 percentage points (pp.)—the strongest growth since June 2012.

• Viability (+14.8 pp.), Total Loss Predictor (+2.2 pp.) and the Delinquency (+0.9 pp.) components all increased on a 12-month basis.

May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Overall Viab Delinq TLP

Y/Y

Perc

ent C

hg.

Strong growth in Viability helped to lift the overall indicator

Summary

13

• The Small Business Health Index declined modestly in the current month and warrants tracking going forward. A number of factors including the weather may be influencing so D&B remains confident in our economic outlook

• The recovery for small business remains uneven although there are signs that some lagging sectors are gaining momentum. One important driver of growth is credit availability and usage and there are improving signs on this front

• Based on the Small Business Health Index, D&B expects economic growth in excess of 2.5% and improvement in nonfarm payroll employment

• As 2014 begins, composite risk and balance sheets among U.S. businesses continue to improve. The overall index was once again above the “no change” threshold continuing its trend higher. January’s reading bodes well for the future of U.S. businesses health.

Join us every month on the Tuesday prior to the first Friday at 8:30 AM EST for the latest economic update

14#DnBEconomy

Follow us on Twitter for up to the minute information and analysis

15

For more information, visit www.dnb.com/tracker

And follow the conversation on Twitter at

@DnBEconomy