dbs group research may 2020 china e-commerce platforms

TRANSCRIPT

DBS Group Research • May 2020

DBS Asian Insights86SECTOR BRIEFING

China E-Commerce Platforms Who Will Make Money in Lower-Tier Cities?

19

DBS Asian Insights SECTOR BRIEFING 8602

China E-Commerce PlatformsWho Will Make Money in Lower-Tier Cities?

Produced by:

Asian Insights Office • DBS Group Research

go.dbs.com/research

@dbsinsights

Geraldine Tan EditorMartin Tacchi Art Director

Susanna CHUI [email protected]

Tsz-Wang [email protected]

19

DBS Asian Insights SECTOR BRIEFING 86

03

04

05

09

23

29

35

51

11

Executive Summary

E-commerce’s Share of China’s Retail Pie to Grow

Understanding Different Tiered Cities’ e-Commerce Customers

Analysing e-Commerce Platforms’ 4P Marketing Mix in Lower-Tier CitiesWhy Do We Use 4P Marketing Mix?

E-commerce Platforms’ Market Share Change in Terms of GMVMarket Share in Next Three Years

E-commerce Platforms’ Monetisation RateMonetisation Rate in Next Three Years

E-commerce Business ProfitabilityE-commerce Business Profitability in Next Three Years

Appendix

We expect China’s e-commerce retail GMV to deliver 26% CAGR during 2019-2021F, accounting for 35% of China’s retail sales in 2021F from 25% in 2019. To ride on this growth, China’s e-commerce platforms are raising e-commerce penetration rate in lower-tier cities with low online penetration. There are currently three dominant players in this space, namely Alibaba, JD and Pinduoduo. We spoke to industry experts and used the 4P marketing mix to assess how they will fare in the next three years.

E-commerce platforms that can secure users with demand for high-traffic necessities in lower-tier cities will gain market share in terms of GMV. Price advantage is most important for high-traffic necessities in lower-tier cities, which is Pinduoduo’s advantage.

Pinduoduo is a rising star in our eyes, with GMV share to increase from 10% in 2019 to 16% in 2021. We expect Alibaba to be a dominant player, with GMV share to remain relatively steady at 64% by 2021 from 66% in 2019, given its user advantage. Meanwhile, JD’s logistics advantage is less important for high-traffic necessities in lower-tier cities. Hence, we expect JD to lose ground, with GMV share to drop from 21% in 2019 to 19% in 2021.

E-commerce platforms that can raise GMV portion of high-profitability apparel products could increase monetisation rate. Promotion advantage is most important for apparel, which is an advantage enjoyed by Alibaba and Pinduoduo. We expect Alibaba’s and Pinduoduo’s monetisation rate to increase from 3.6% and 3.0% in 2019 to 3.8% and 3.5% in 2021F. Meanwhile, logistics, which is JD’s advantage, is less important for apparel. JD’s monetisation rate is expected to decline from 4.5% in 2019 to 4.0% in 2021F.

E-commerce platforms that can lift monetisation rate led by increasing high-profitability apparel GMV proportion could be profitable in lower-tier cities. We expect Alibaba’s and Pinduoduo’s non-GAAP net margin to rise from 78.7% and -14.6% in 2019 to 81.4% and 14.1% in 2021F, on increasing monetisation rate from increasing apparel GMV proportion. JD’s is projected to decline from 2.5% in 2019 to 1.8% in 2021F, with decreasing monetisation rate and decreasing apparel GMV proportion.

Executive SummaryChina’s e-commerce retail GMV to deliver

26% CAGR during 2019-2021F

Key to securing users in lower-tier cities

Pinduoduo is a rising star; JD set to lose

ground

Increase monetisation rate by raising GMV

portion of high-profitability apparel

products

E-commerce platforms could be profitable in

lower-tier cities

DBS Asian Insights SECTOR BRIEFING 8604

E-commerce’s Share of China’s Retail Pie to Grow

China’s e-commerce retail GMV to expand at 26% CAGR during

2019-2021F

DBS Asian Insights SECTOR BRIEFING 86

05

We expect China’s e-commerce retail gross merchandise volume (GMV) to deliver 26% CAGR during 2019-2021F, accounting for 35% of China’s retail sales in 2021F from 25% in 2019.

China’s e-commerce retail GMV as percentage of total retail sales grew from 9% in 2014 to 21% in 2018, which is high relative to key developed countries. Therefore, China’s e-commerce platforms are raising e-commerce penetration rate in (1) product categories with low online penetration and (2) lower-tier cities.

China’s e-commerce retail GMV

Global retail e-commerce penetration (2018)

Source: National Bureau of Statistics of China, DBS HK

Source: National Bureau of Statistics of China, eMarketer, DBS HK

6,200 8,000 10,165 12,413 16,221

30,426 30,09931,000 30,975

29,98716.9%21.0%

24.7%28.6%

35.1%

-15%

-5%

5%

15%

25%

35%

45%

05,000

10,00015,00020,00025,00030,00035,00040,00045,000

2017 2018 2019F 2020F 2021F

Rmb bn

Offline retail GMV (LHS)E-commerce retail GMV (LHS)E-commerce as % of China's retail sales (RHS)

21.0% 20.6%

17.5%

9.8%

7.3%

0%

5%

10%

15%

20%

25%

China UK SouthKorea

US Australia

Raising e-commerce penetration rate in

product categories with low online penetration

Raising e-commerce penetration rate of

lower-tier cities

Higher tier cities Lower-tier cities

City-tier classification

Tier 1 Tier 2 Tier 3 Tier 4

GDP >US$300bn US$68-299bn US$18-67bn <US$17bn

Political administration of the city

Directly controlled municipalities and leading provincial

capital cities

Directly controlled municipalities, provincial

capital cities, and economically important cities

Provincial capital cities and prefecture-level

cities

Prefecture-level cities and county-

level cities

Population >15m 3-15m 0.15-3m <0.15m

Number of cities

4 30 138 480

Lower-tier cities will deliver 34% CAGR

during 2019-2021F, accounting for 43% of

China’s e-commerce retail GMV in 2021F.

DBS Asian Insights SECTOR BRIEFING 8606

As a percentage of retail sales, computer, communication & consumer electronics (3C) products, and apparel & shoes, recorded high online shopping penetration rates of 32-45% in 2018. But homewares and home furnishings, and food & drinks have low online penetration rates of 10-11% due to perishability, logistics and involvement issues.

To bridge this, China’s e-commerce platforms have launched new retail initiatives which takes the best of both online and offline worlds to address perishability, logistics and involvement issues, to help product categories with low online penetration to go online. (For details, please refer to Asian Insights SparX: China Internet Sector: Who will be the winners in new retail?)

Another key driver is growth from lower-tier cities, which will deliver 34% CAGR during 2019-2021F, accounting for 43% of China’s e-commerce retail GMV in 2021F from 38% in 2019. This is driven by (a) rising online penetration and (b) rising consumption power.

Online penetration of key product categories in China (2018)

China’s city-tier classification by GDP, political administration, and population

Source: Euromonitor, DBS HK

Source: DBS HK

44.8%38.3%

31.8%27.4%

22.2%

11.1% 10.2%

0%

10%

20%

30%

40%

50%

Cons

umer

ele

ctro

nics

Cons

umer

App

lianc

es

Appa

rel &

Foot

wea

r

Beau

ty &

per

sona

l car

e

Cons

umer

Hea

lth

Food

& d

rinks

Hom

ewar

es a

nd H

ome

Furn

ishin

gs

Low online penetration

Rural online penetration rate was 38% in 2018, versus urban’s 75%, according to China Internet Network Information Center (CNNIC). This was because some of the rural population do not own or use PCs/smartphones.

The gap has widened from 32% in 2013 to 36% in 2016 but stabilised since 2016. This was because mobile phone makers Oppo and Vivo, which focus on tier 3 or below cities, have become popular since 2016. Their low-end smartphones with average selling price (ASP) of c.Rmb1,000 are affordable to the rural population. Their offline franchise stores can reach non-online rural population and provide face-to-face instruction on how to use smartphones.

There is a discrepancy between consumption in tier 1-2 cities and tier 3 or below cities. According to QuestMobile, tier 3 or below cities accounted for 55% of the total mobile Internet users in 2018, but they made up only 36% of China’s e-commerce retail GMV.

Rising online penetration

Rising consumption power

DBS Asian Insights SECTOR BRIEFING 86

07

Tier 1-2 cities and Tier 3 or below cities’ mobile Internet users and e-commerce retail GMV (2018)

China’s e-commerce retail GMV breakdown China’s online penetration

Source: iResearch, National Bureau of Statistics of China, DBS HK

Source: National Bureau of Statistics of China, DBS HK Source: CNNIC, DBS HK

45.3%64.1%

54.7%35.9%

0%

20%

40%

60%

80%

100%

Mobile Internet users E-commerce retail GMVTier 1-2 cit ies Tier 3 or above cit ies

4,174 5,126 6,291 7,208 8,8432,0262,874

3,8744,839

6,569

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

2017 2018 2019F 2020F 2021F

Rmb bn

Tier 1-2 cit ies Tier 3 or below cities

60.3% 62.8% 65.8% 69.1% 71.0%74.6%

28.1% 28.8% 31.6% 33.1% 35.4% 38.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2013 2014 2015 2016 2017 2018Urban area Rural area

4,174 5,126 6,291 7,208 8,8432,0262,874

3,8744,839

6,569

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

2017 2018 2019F 2020F 2021F

Rmb bn

Tier 1-2 cit ies Tier 3 or below cities

This can be attributed to lower per capita disposable income in lower-tier cities. According to National Bureau of Statistics of China, per capita disposable income in rural areas was Rmb14,617 in 2018, which was 37% of urban’s Rmb39,251. However, the gap has been narrowing, with per capita disposable income in rural areas expanding by 9% CAGR during 2013-2018, versus urban’s CAGR of 8%. The per capita disposable income growth in rural areas is outpacing urban’s, which can translate to rising consumption power in lower-tier cities.

Consumption power in lower-tier cities set

to rise as per capita disposable income

grows in rural areas.

DBS Asian Insights SECTOR BRIEFING 8608

China’s per capita disposable income

Source: National Bureau of Statistics of China, DBS HK

31,19533,616

36,39639,251

42,359

11,422 12,363 13,432 14,617 16,021

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2015 2016 2017 2018 2019

Rmb

Urban area Rural area

End customersPrice sensitivity of end customers in lower-tier cities is higher, with their lower income level. They are less aware of brands and demand is usually towards more targeted recommendations, compared to higher-tier cities.

Logistics service providersKey logistics service providers are similar in lower- and higher-tier cities, and include (i) express logistics platforms, (ii) warehouse service providers, and (iii) express delivery service providers. There are concerns that logistics costs will increase due to lower order density and higher last-mile delivery cost in sparsely populated lower-tier cities. However, logistics service providers have expressed that logistics cost per order in lower-tier cities is close to that in higher-tier cities.

Understanding Different Tiered Cities’ e-Commerce Customers

Higher-tier cities Lower-tier cities

Warehouse costs

Warehouse costs are mostly due to rental. Rental cost per sqm is 30%+ cheaper in lower-tier cities versus higher-tier cities.

(c.50% of total logistics cost)

Higher warehouse costs Lower warehouse costs

Delivery costs

(50% of total logistics cost)

Delivery cost is mostly labour cost. Despite per capita disposable income in rural areas being c.60% lower than urban areas, labour cost per order will be higher in lower-tier cities versus higher-tier cities due to lower order density and higher last-mile delivery cost. Population density is c.5-200 people per

square kilometre in lower-tier cities versus c.200-4,000 per square kilometre in higher-tier cities. At the same time, purchase frequency in lower-tier cities is around 30% below that of higher-tier cities.

However, pick-up and drop-off points for parcel delivery could be concentrated at one point and hence, lower last-mile delivery costs in sparsely populated lower-tier cities.

Lower delivery cost Higher delivery cost

Total logistics cost

Similar total logistics cost Similar total logistics cost

DBS Asian Insights SECTOR BRIEFING 86

09

Logistics costs in lower-tier cities versus higher-tier cities

Source: DBS HK

MerchantsMerchants targeting lower-tier cities are those selling unbranded products at lower prices and focusing on a few stock-keeping units (SKUs). Meanwhile, merchants targeting higher-tier cities are inclined toward branded products involving numerous SKUs.

Value chain for e-commerce platforms

DBS Asian Insights SECTOR BRIEFING 8610

Source: DBS HK

Merchants Pickup outlets

Regional sorting hubs

Regional sorting hubs

Delivery outlets

End customers

Firstmile

Shorthaul

Shorthaul

Linehaul

Lastmile

(2) Logistics service providers

Analysing e-commerce platforms’ 4P marketing mix in lower-tier cities

Analysing e-Commerce Platforms’ 4P Marketing Mix in Lower-Tier Cities

We interviewed industry experts and analysed e-commerce platforms’ 4P marketing mix in fast growing lower-tier cities. 4P refers to: (1) products, (2) price, (3) place, and (4) promotions. We compared the importance of these four factors in lower-tier cities versus higher-tier cities, and e-commerce platforms’ strengths and weaknesses in respect of these four factors.

In the following sections, we did an analysis to determine e-commerce platforms’ (a) market share in terms of GMV, given the different competitive landscape between lower- and higher-tier cities; (b) monetisation rate; (c) e-commerce business profitability in the next three years.

&"'()*+,

-

(1) Compare importance of 4P marketing mix in lower tier cities

Products Price Place Promotion

(a) GMV (b) Monetisation (c) Profitability

(2) Compare e-commerce platforms' strengths and weaknesses

(3) Analysis of e -commerce platforms' GMV share, monetisation, and profitability for next three years

Products Price Place Promotion

DBS Asian Insights SECTOR BRIEFING 86

11

Source: DBS HK

Sales of key product categories in China (2018)

Source: Euromonitor, DBS HK

Why Do We Use 4P Marketing Mix?

Jack Ma, founder of China’s largest e-commerce platform Alibaba, emphasised that there is no market that is the same, e.g. New York and Chicago are different. But e-commerce business is the same as it focuses on the customer. This is the reason why the 4P framework is one of the most commonly used frameworks for analysing marketing strategies (products, price, place and promotion centred around the customer) in targeted lower-tier cities.

1. ProductsProducts means “what are the products”. E-commerce platforms’ product strategies are important to gain market share in terms of GMV, monetisation rate, and profitability in both higher- and lower-tier cities. We analyse the three largest product categories in China’s retail sales market: (i) necessities, (ii) apparel, and (iii) computer, communication & consumer electronics products (3C products). Product categories can be classified into two dimensions, namely traffic and profitability.

(i) Necessities. Necessities (i.e. food and fast-moving consumer goods or FMCG) are high traffic products with purchase frequency estimated at 52 times per user per year, but with mid-level profitability and monetisation rate of 3-4%.

(ii) Apparel. Apparel are high profitability items with estimated monetisation rate of 4-8% but are mid traffic products with purchase frequency of 12 times per user per year.

(iii) 3C products. These products are low traffic with estimated purchase frequency at 1 time per user per year, and low profitability with monetisation rate of 1-3%.

DBS Asian Insights SECTOR BRIEFING 8612

2,1261,906

1,594

712351 220

0

500

1,000

1,500

2,000

2,500

Appa

rel &

Foot

wea

r

Food

& d

rinks

Com

pute

r,Co

mm

unica

tion

and

Cons

umer

Ele

ctro

nic

Hom

ewar

es a

ndHo

me

Furn

ishin

gs

Beau

ty &

pers

onal

care

Cons

umer

Heal

th

Rmb bn

Key product categories’ purchase frequency and revenue

Source: DBS HK

Source: DBS HK

As such, industry experts expect e-commerce platforms to focus on high-traffic necessities (i.e. food and FMCG) first to gain users and lock in user stickiness from lower-tier cities, before introducing high-profitability apparel to monetise users.

The other marketing mix parameters help to determine the success of e-commerce platforms in these product categories.

2. PricePrice means “at what price to sell various products”. Price advantage is important in lower-tier cities as price sensitivity is high, given the lower income level. On the top of these factors, price strategies are more important for necessities, compared to apparel and 3C products. Price sensitivity is high for necessities due to its nature of frequent purchases.

Comparison of e-commerce platforms:

(i) Price difference between products with different positioning. Pinduoduo focuses on unbranded products with lower prices, as demonstrated by its portfolio made up of only 100 brands. Meanwhile, JD and Alibaba are inclined towards branded products with price premium, as they have around 0.2m brands each on their platforms.

"Necessities (i.e. food and FMCG)"

Apparel 3C products

Retail sales (Rmb m) 1,905,799 2,125,552 1,593,792

Online penetration Low (11.1%) High (31.8%) High (42.1%)

Online retail sales (Rmb m) 211,544 675,925 671,514

Purchase frequency (times / year) 52 12 1

Ticket size 40 200 1,000

GMV/user/year 2,080 2,400 1,000

Advertising budget as of paying merchants' GMV

10-15% 15-30% 5-10%

Paying ratio 25%+ 25%+ 25%+

Monetisation rate 3-4% 4-8% 1-3%

Revenue/user/year (lower range) 62 360 50

Revenue/user/year (upper range) 83 720 100

Usage High traffic and mid profitability

High profitability and mid traffic

Low profitability and low traffic

DBS Asian Insights SECTOR BRIEFING 86

13

E-commerce platforms’ sales and marketing expenses as % of GMV (2019)

Source: Company, DBS HK

(ii) Price difference between the same SKU. We discovered that for the same SKUs, Pinduoduo’s products are priced at discounts of 1-15% to Alibaba and JD based on sample checks to compare prices of major product categories across e-commerce platforms.

The market may attribute the lower price to higher subsidies (i.e. coupons). Pinduoduo’s sales and marketing expenses as a percentage of GMV was relatively high at 3% in 2019, versus 1% for Alibaba and JD. However, even we assume all sales and marketing expenses are related to coupons, we consider the subsidy to be small versus product price discounts of 1-15%.

We attributed the lower price to Pinduoduo’s differentiated recommendation feed-based business model, which focuses on recommending top-selling SKUs to targeted users to gain better economies of scale. While Alibaba ‘s and JD’s search-based business model offers numerous SKUs through users’ searches. Therefore, Pinduoduo has a price advantage in lower-tier cities, especially for high-traffic necessities with high price sensitivity.

Alibaba and JD introduced recommendation feeds in 2018 and 2019 respectively, but industry experts believe they are not able to completely replicate Pinduoduo’s business model. This is because Pinduoduo has a narrower SKU selection, providing better economies of scale, while Alibaba has numerous SKUs, as indicated by its tie-ups with 10m merchants versus Pinduoduo’s 3.6m merchants and JD’s 0.2m.

0.7%

1.0%

2.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Alibaba JD Pinduoduo

Alibaba and JD unlikely to be able to completely replicate

Pinduoduo’s business model

Price advantage is important in lower-tier

cities as price sensitivity is high, given the lower

income level.

DBS Asian Insights SECTOR BRIEFING 8614

Alibaba JD Pinduoduo

Price comparison across e-commerce platforms

Source: BP PLC, DBS Bank

Corou tissue paper – 120 sheets x 10 packs

HLA oxford Shirt (male) HSTYLE printing t-shirt (female)

iPhone 11

Alibaba Rmb69.8 Rmb98 Rmb38 Rmb5,499

JD Rmb69.8 Rmb98 N.A. Rmb5,499

Pinduoduo Rmb59.6 Rmb97 Rmb37.5 Rmb5,099

3. PlacePlace means “how do they sell their products” (i.e. via e-commerce platforms with high traffic, such as those with a large number of [i] customers and [ii] merchants) and “how do they deliver products?” (i.e. e-commerce platforms with strong [iii] logistic capabilities).

(i) Number of customers. The number of customers is important for all three product categories (necessities, apparel, 3C products) in both higher- and lower-tier cities.

Comparison of e-commerce platforms: Alibaba is the clear leader in terms of annual active customers in both higher- (340m in 2019) and lower-tier (336m) cities. JD (190m) and Pinduoduo (236m) are neck and neck in higher-tier cities, but Pinduoduo (276m) has substantially more than JD (142m) in lower-tier cities.

DBS Asian Insights SECTOR BRIEFING 86

15

(ii) Number of merchants. The number of merchants is less important in lower-tier cities, versus higher-tier cities. E-commerce platforms tend to focus on recommending top-selling SKUs from a smaller merchant base to users in lower-tier cities, versus offering numerous SKUs from a larger number of merchants to users in higher-tier cities via searches.

Comparison of e-commerce platforms: Alibaba and Pinduoduo are leading in number of merchants with c.10m and c.3.6m merchants as of 2019, while JD has only c.0.2m.

(iii) Logistics capabilities. E-commerce platform’s logistics capabilities are less important in lower-tier cities, versus higher-tier cities. This is because (a) user demand in lower-tier cities for timely delivery is less; (b) necessity goods and apparel merchants targeting lower-tier cities are usually small and focus only on a few SKUs, while merchants targeting higher-tier cities need to

China’s e-commerce platforms – Annual active customers (m, 2019)

China’s e-commerce platforms – Number of merchants (2019)

Source: Jiguang Big Data, DBS HK

Source: Company, DBS HK

340190 236

336

142

276

0

100

200

300

400

500

600

700

800

Alibaba JD Pinduoduo

Tier 1 and 2 cities Tier 3 or below cities

10

0.2

3.6

0

2

4

6

8

10

12

Alibaba JD Pinduoduo

(m)

Alibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8616

Alibaba JD Pinduoduo

Logistics requirements are less in lower-tier cities for key product categories

Source: DBS HK

handle logistics involving numerous SKUs; (c) logistics services in lower-tier cities for unbranded 3C products do not require serial number management. The 3C merchants targeting higher-tier cities need to handle logistics services involving serial number management, in order to ensure that products are delivered to the correct warehouses and customers.

Comparison of e-commerce platforms: There are three ways for e-commerce platforms to set up their logistics systems: (a) building their own logistics network (i.e. JD); (b) creating a third-party logistic platform which connects third-party logistic service providers (i.e. warehouse service providers, express delivery service providers) with real-time logistic data sharing (i.e. Alibaba, Pinduoduo); and (c) employing third-party express delivery service providers.

JD, which has set up its own logistics network, could have significantly better inventory and sales forecasts with real-time logistic data, enabling it to optimise its self-built logistics network using a higher level of logistics technology and automation. As such, JD should be able to offer better fulfilment (i.e. high on-time rate, low error rate, and low damage rate) to differentiate itself from other e-commerce platforms.

Alibaba’s Cainiao Logistics, a third-party logistics platform, has strategically invested in integrated logistics services providers (i.e. warehouses and express delivery) such as BEST (百世), and express delivery partners such as ZTO (中通), YTO (圓通), and STO (申通), which are China’s three largest express delivery service providers. Third-party logistics platforms may help to enhance real-time logistics data sharing between Alibaba’s Cainiao Logistics and its logistic partners to improve fulfilment efficiency, but would not be able to optimise the latter’s logistics network at their discretion like a self-built logistics network.

Pinduoduo had employed third-party express delivery service providers until 1Q19. It found that it was unable to obtain real-time logistics data from third-party express delivery service providers to share with its clients and improve fulfilment efficiency. To tackle this, Pinduoduo set up a third-party logistics platform like Alibaba in 1Q19, with seven logistics partners including BEST, ZTO, YTO, STO, Yunda, SF, and EMS. But Pinduoduo’s network is different from Alibaba’s

Food and drinks Apparel 3C products

Higher-tier cities

Lower-tier cities Higher-tier cities

Lower-tier cities Higher-tier cities

Lower-tier cities

Timely delivery ***** *** ***** *** ***** ***

SKU management

***** * *** * * *

Serial number management

* * * ***** ***

DBS Asian Insights SECTOR BRIEFING 86

17

as it does not plan to invest in warehouses and express delivery service providers. However, industry experts expressed that collaboration between Pinduoduo and its logistic partners may be weak without investments made in their logistic partners, versus that between Alibaba and its strategic investments in logistics partners.

In conclusion, as e-commerce platforms’ logistics capabilities are less important in lower-tier cities versus higher-tier cities, JD’s logistics advantage over Alibaba and Pinduoduo is diminishing in lower-tier cities.

E-commerce platforms’ logistics capabilities are less important in lower-tier cities versus higher-

tier cities.

Three ways for e-commerce platforms to build their logistics systems

Source: Company, DBS HK

Self-built logistic network Third-party logistic platform Third-party logistic providers

Representatives JD Alibaba, Pinduoduo Other smaller e-commerce platforms

Advantages Self-built logistic networks could have significantly better inventory & sales forecasts with real-time logistic data.

Self-built logistics network can be optimised using human-less logistics technology. Offer better fulfilment (i.e. high on-time rate, low error rate, and low damage rate).

Light asset model. Third-party logistics platforms able to enhance real-time logistic data sharing between Alibaba’s Cainiao Logistics and its logistic partners to improve fulfilment efficiency.

Light asset model.

Disadvantages Heavy asset model Third-party logistics platforms may not be able to optimise their logistic partners’ logistics network at their discretion unlike having a self-built logistics network. Collaboration between third-party logistics platforms and their logistic partners may be weak without making investments in their logistic partners.

E-commerce platforms cannot have real-time logistic data from third-party express delivery service providers to share with clients and improve fulfilment efficiency.

DBS Asian Insights SECTOR BRIEFING 8618

Promotion is more important for apparel,

compared to necessities and 3C products.

4. PromotionPromotion means “how they promote products”. Promotion through user data analytics capabilities for product recommendations is more important in lower-tier cities, as users are less aware of brands and targeted recommendations could drive demand.

On the top of these, promotion is more important for apparel, compared to necessities and 3C products. Apparel are unstandardized and fragmented with the top 10 brands garnering a 10% market share. Accurate targeted recommendations could help users to decide what they want to buy among the various fragmented brands and numerous apparel SKUs, and thus increase customers’ purchase probability.

Despite fragmentation being high in the necessity goods market with the top 10 brands garnering 14% of the market, most customers are indifferent to brands for necessities. It is thus easier for users to decide what to buy in terms of necessities. For 3C products, the market is concentrated with the top 10 consumer electronics/consumer appliance brands having 74%/53% market share. Buying 3C products is less difficult given the narrower selection of brands and SKUs.

Comparison of e-commerce platforms:We analyse e-commerce platforms’ user data analytics capabilities in three dimensions: (i) data history, (ii) data variety, and (iii) network data.

(i) Data volume. Alibaba and JD, which were established in 2003 and 2004 respectively, are leading in this area, while Pinduoduo was established only in 2015. However, according to industry experts, Pinduoduo’s annual number of orders per buyer was 49x in 2019 versus Alibaba’s 50x and JD’s 16x, and the sample size is enough to obtain sufficient statistical power.

Market share of top 10 brands (2018)

Source: Euromonitor, DBS HK

9.6%14.4%

74.0%

52.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apparel Food anddrinks

Consumerelectronics

Consumerappliances

DBS Asian Insights SECTOR BRIEFING 86

19

(ii) Data variety. Alibaba, which is an Internet conglomerate, has a variety of data sources from its wide ecosystem of e-commerce, new retail, services e-commerce, logistics, payment, cloud computing, and digital media & entertainment, etc. Meanwhile, JD and Pinduoduo, which focus on e-commerce businesses, mainly have consumption data on their e-commerce platforms.

(iii) Network data. Pinduoduo has interactive consumption data of users and their family and friends, while Alibaba and JD only have consumption data of individual users. This is because Pinduoduo’s users tend to invite their family and friends to make a “team purchase” on WeChat (China’s largest social e-commerce platform), which further improves the accuracy of targeted recommendations and promotions. Alibaba and JD introduced “team purchase” in 2019, but industry experts believe they are not able to completely replicate Pinduoduo’s business model. This is because the success of Pinduoduo’s “team purchase” is attributed to the support of Tencent, which is its second-largest shareholder with a 16.9% stake. Alibaba and JD are unable to replicate this. Alibaba’s users are not able to share Alibaba’s links on Tencent’s WeChat. Meanwhile, JD has Tencent’s support as its largest shareholder with a 17.8% stake. However, JD‘s low traffic and 3C product focus fail to match traffic in lower-tier cities despite sharing the “team purchase” link on WeChat.

The market believes Alibaba is invincible in user data analytics capabilities with its wide data variety from its extensive ecosystem. However, industry experts have expressed that Pinduoduo could narrow the gap with Alibaba, with its network data (i.e. interactive consumption data) from its “team purchase” business model.

E-commerce platforms’ user data analytics capabilities

Source: DBS HK

Alibaba JD Pinduoduo

Data volume Established in 2003 Annual number of orders per buyer: 50

Established in 2004 Annual number of orders per buyer: 16

Established in 2015 Annual number of orders per buyer: 49

***** ***** ***

Data variety A variety of data from its wide ecosystem of e-commerce, new retail, services e-commerce, logistics, payment, cloud computing, and digital media & entertainment, etc.

Mainly consumption data on its e-commerce platforms

Mainly consumption data on its e-commerce platforms

***** * *

Network data Individual consumption data Individual consumption data Individual consumption data + interaction consumption data between users and their family and friends

* * *****

DBS Asian Insights SECTOR BRIEFING 8620

Comparing importance of 4P marketing mix in lower-tier cities versus higher-tier cities

Source: DBS HK

4P marketing mix Importance in lower-tier cities versus higher-tier cities

Product E-commerce platforms’ product strategies are important for market share in terms of GMV, monetisation rate and profitability in both higher- and lower-tier cities.

Price Price advantage is important in lower-tier cities, as price sensitivity is high. On the top of these, price sensitivity is high for necessities, as these products are frequently purchased.

Place (i) Number of customers. The number of customers is important for these three categories in both higher- and lower-tier cities. (ii) Number of merchants. E-commerce platforms focusing on recommending top-selling SKUs from a concentrated base of merchants to users in lower-tier cities, versus offering numerous SKUs from numerous merchants through users’ search in higher-tier cities. (iii) Logistics capabilities. Logistics capabilities are less important for 3C, necessities, and apparel products in lower-tier cities. There is more demand for unbranded 3C products in lower-tier cities, and this does not require serial number management services. Necessity and apparel merchants targeting lower-tier cities are small and focus on a few SKUs, which does not require SKU management services.

Promotion Promotion (i.e. user data analytics capabilities for product recommendations) is more important in lower-tier cities, as users are less aware of brands and demand for targeted recommendations. On top of this, promotion is more important for apparel, due to market fragmentation, compared to necessities and 3C products.

DBS Asian Insights SECTOR BRIEFING 86

21

E-commerce platforms’ strengths and weaknesses in 4P marketing mix in lower-tier cities:

Alibaba JD Pinduoduo

Product Alibaba’s user advantage is important for high-traffic necessities in lower-tier cities Promotion advantage is most important for apparel, a high profitability product

JD’s logistics advantage is less important for high-traffic necessities and high-profitability apparel

Pinduoduo’s price advantage is important for high-traffic necessities in lower-tier cities Promotion advantage is most important for high-profitability apparel products

***** * *****

Price Alibaba‘s search-based business model - offering numerous SKUs through users’ searches - does not have economies of scale

JD’s search-based business models - offering numerous SKUs through users’ searches - does not have economies of scale

Pinduoduo’s differentiated recommendation feed-based business model focuses on recommending top-selling SKUs to targeted users, offering better economies of scale

* * *****

Place (i) Number of customers: 336m (ii) Number of merchants: 10m (iii) Logistics capabilities: Third-party logistic platform

(i) Number of customers: 142m (ii) Number of merchants: 0.2m (iii) Logistics capabilities: Self-built logistics network

(i) Number of customers: 276m (ii) Number of merchants: 3.6m (iii) Logistics capabilities: Third-party logistic platform

*** *** ***

Promotion A variety of data from its wide ecosystem of e-commerce, new retail, e-commerce services, logistics, payment, cloud computing, and digital media & entertainment, etc.

Mainly individual consumption data on its e-commerce platform

Individual consumption data + interaction consumption data between users and their family & friends

***** * ***

Source: DBS HK

DBS Asian Insights SECTOR BRIEFING 8622

Alibaba, JD and Pinduoduo accounted for 97% of market share in terms of GMV in 2019. Alibaba and JD are China’s largest and second-largest e-commerce platforms with 66% and 21% market share, respectively, in terms of GMV in 2019. Established in 2015, Pinduoduo is catching up as China’s third-largest e-commerce platform, with 10% market share in terms of GMV, while its number of annual active customers and merchants stood at 512m and c.4m merchants as of 2019, higher than JD’s 332m annual active customers, and c.0.2m merchants.

E-commerce Platforms’ Market Share Change in Terms of GMVPinduoduo catching up

with Alibaba and JD

Market share of China’s e-commerce platforms in terms of GMV (2019)

Annual active customers on China’s e-commerce platforms (2019)

Source: National Bureau of Statistics of China, DBS HK Source: Company, DBS HK

Alibaba66%

JD21%

Pinduoduo10%

Others3%

676

333

512

0

100

200

300

400

500

600

700

800

Alibaba JD Pinduoduo

(m)

Alibaba JD Pinduoduo

Pinduoduo

DBS Asian Insights SECTOR BRIEFING 86

23

Market Share in Next Three Years

We interviewed industry experts and analysed e-commerce platforms’ 4P marketing mix in lower-tier cities. We have done an analysis to determine the market share of various e-commerce platforms in terms of GMV in next three years, given the different competitive landscapes between lower- and higher-tier cities.

(1) Annual active customers. Based on analysing e-commerce platforms’ 4P marketing mix in lower-tier cities, we believe those that are able to gain users who purchase high-traffic necessities in lower-tier cities will be able to increase their market share in terms of GMV.

Price advantage is most important for high-traffic necessities in lower-tier cities, which is Pinduoduo’s advantage. Pinduoduo is a rising star, with fast growing annual active customer CAGR of 25% to 805m during 2019-2021F.

User advantage is also important for high-traffic necessities in lower-tier cities, and Alibaba has an advantage in this aspect. We expect Alibaba to be a dominant player, with annual active customer CAGR of 14% to 880m in 2019-2021F.

Meanwhile, logistics advantage is less important for high-traffic necessities in lower-tier cities. JD had an advantage in logistics. However, we expect JD to be losing ground, with annual active customer CAGR of 11% to 409m in 2019-2021F.

China’s e-commerce platforms – Number of merchants (2019)

Source: Company, DBS HK

10

0.2

3.6

0

2

4

6

8

10

12

Alibaba JD Pinduoduo

(m)

Alibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8624

Source: Jiguang Big Data, DBS HK

Source: Jiguang Big Data, DBS HK

Source: Jiguang Big Data, DBS HK

Alibaba - annual active customers

JD - annual active customers

Pinduoduo - annual active customers

236 319 346 373 399

245272

336405

481

0100200300400500600700800900

1,000

2017 2018 2019 2020 2021

m

Tier 1 and 2 cities Tier 3 or above cit ies

153 187 193 209 224

111120 140

161185

050

100150200250300350400450

2017 2018 2019 2020 2021

m

Tier 1 and 2 cities Tier 3 or below cities

51173 236 286 324

91

188

276373

481

0100200300400500600700800900

2017 2018 2019 2020 2021

m

Tier 1 and 2 cities Tier 3 or below cities

DBS Asian Insights SECTOR BRIEFING 86

25

153 187 193 209 224

111120 140

161185

050

100150200250300350400450

2017 2018 2019 2020 2021

m

Tier 1 and 2 cities Tier 3 or below cities

(2) Average annual spending per customer. We expect Pinduoduo’s average annual spending per buyer in lower-tier cities to deliver 2019-2021F CAGR of 27%, driven by a narrowing purchase frequency gap between low- and high-tier cities, with its price advantage in necessities and promotion advantage in apparel.

We expect Alibaba’s purchase frequency gap between low- and high-tier cities to narrow as well, with its user advantage in necessities and promotion advantage in apparel. However, we expect Alibaba to deliver a relatively moderate rise in average annual spending per buyer of 9% CAGR in 2019-2021F, as increasing purchase frequency will be partly offset by low ticket sizes in lower-tier cities.

Source: Company, DBS HK

Source: Jiguang Big Data, DBS HK

Pinduoduo - Average annual spending per customer

Alibaba - Average annual spending per customer

1,5321,813

2,743

3,410

4,364

687 8421,336

1,746

2,361991

1,308

1,9672,468

3,167

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

13,22612,368

13,427 13,887

15,825

5,927 5,7436,503 7,030

8,418

9,503 9,3209,989 10,302

11,774

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

DBS Asian Insights SECTOR BRIEFING 8626

We expect JD’s purchase frequency gap between low- and high-tier cities to narrow but at a moderate rate, as its logistics advantage is less important for necessities and apparel in lower-tier cities. We expect JD to deliver relatively moderate rise in average annual spending per buyer of 11% CAGR in 2019-2021F.

(3) GMV. Driven by growth in annual active customers and average annual spending per buyer, we expect Pinduoduo’s GMV to expand by 58% CAGR in 2019-2021F. Meanwhile, due to moderate growth of annual active customers and average annual spending per buyer, we expect Alibaba’s and JD’s GMV to moderately increase by 24% and 23% CAGR in 2019-2021F.

Source: Jiguang Big Data, DBS HK

Source: National Bureau of Statistics of China, DBS

JD - Average annual spending per customer

Alibaba - GMV

6,3976,915

8,0438,481

9,586

2,867 3,2113,820 4,120

4,800

4,9145,470

6,270 6,5797,422

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

3,116 3,949 4,568 5,1356,309

1,4531,562

2,1822,849

4,051

0

2,000

4,000

6,000

8,000

10,000

12,000

2017 2018 2019F 2020F 2021F

Rmb bn

Tier 1 and 2 cities Tier 3 or below cities

DBS Asian Insights SECTOR BRIEFING 86

27

Source: National Bureau of Statistics of China, DBS

Source: National Bureau of Statistics of China, DBS

Source: National Bureau of Statistics of China, DBS

JD - GMV

Pinduoduo - GMV

Market shares of China’s e-commerce platforms in terms of GMV

9771,293 1,552 1,847

2,228317384

533694

921

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2017 2018 2019F 2020F 2021F

Rmb bn

Tier 1 and 2 cities Tier 3 or below cities

63 158 368652

1,136

79 314

648

976

1,414

0

500

1,000

1,500

2,000

2,500

3,000

2017 2018 2019F 2020F 2021F

Rmb bn

Tier 1 and 2 cities Tier 3 or below cities

74% 69% 66% 65% 64%

21%21% 21% 20% 18%

2% 6% 10% 14% 17%3% 4% 3% 2% 1%

0%10%20%30%40%50%60%70%80%90%100%

2017 2018 2019F 2020F 2021F

Alibaba JD Pinduoduo OthersAlibaba JD OthersPinduoduo

DBS Asian Insights SECTOR BRIEFING 8628

55%

100%

45%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Alibaba JD Pinduoduo

1P 3P Source: Company, DBS

Source: DBS HK

GMV breakdown (2019)

Monetisation avenues of China’s e-commerce platforms

There are first-party (1P) e-commerce platforms and third-party (3P) e-commerce platforms. (1) 1P e-commerce platforms procure products from suppliers and sell them to customers on a cost-plus basis, with low gross profit margin (GPM) of 6-8%. (2) 3P e-commerce platforms are platforms through which merchants sell their products to customers. 3P e-commerce platforms mainly monetise through online advertising and transaction-based commission, with high GPM of 80-90%. Online advertising and transaction-based commission are thus major high-margin monetisation avenues of e-commerce platforms’ GMV.

Alibaba and Pinduoduo are 3P e-commerce platforms (3P: 100% of 2019 GMV). JD is hybrid e-commerce platform (1P: 55% of 2019 GMV, 3P: 45% of 2019 GMV).

E-commerce Platforms’ Monetisation Rate

Business models Description Monetisation ways Gross profit margin

First-party (1P) e-commerce platforms

1P e-commerce platforms procure products from suppliers and sell them to customers on cost-plus basis

Price spread 6-8%

Third-party (3P) e-commerce platforms

3P e-commerce platforms are platforms through which merchants sell their products to customers

Online advertising and transaction-based commission

80-90%

DBS Asian Insights SECTOR BRIEFING 86

29

Current Monetisation Rate

JD’s, Alibaba’s, and Pinduoduo’s monetisation rate (commission and advertising revenue as percentage of 3P GMV) were 4.5%, 3.6%, and 3.0% respectively in 2019.

Monetisation Rate in Next Three Years

We interviewed industry experts, such as advertising agents and merchants, and analysed advertising budgets of merchants. Market is concerned that penetrating lower-tier cities will drag down the monetisation rate, however we believe e-commerce platforms could increase monetisation rate if they are able to increase the proportion of apparel in terms of GMV.

(1) Advertising budget as % of paying merchants’ GMV. According to industry experts, apparel merchants spend 15-30% of GMV on e-commerce ads, 10-15% for necessity merchants, 5-10% for 3C merchants. Merchants with a higher scale and profitability will tend to spend a higher percentage of GMV on e-commerce ads.

Source: Company, DBS HK

Source: Company, DBS HK

E-commerce platforms’ monetisation rate in 2019

Advertising budget as % of GMV on different product categories

3.6%

4.5%

3.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Alibaba JD Pinduoduo

10%

15%

5%

15%

30%

10%

0%

5%

10%

15%

20%

25%

30%

35%

Necessit ies (i.e.food and FMCG)

Apparel 3C products

Alibaba

Necessities (i.e. food and FMCG)

JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8630

Source: DBS HK

Alibaba’s GMV mix

35% 32% 29% 28%

10% 9% 8% 8%

35% 36% 38% 38%

20% 23% 25% 26%

0%

20%

40%

60%

80%

100%

2018 2019 2020 2021Necessit ies (i.e. food and FMCG)ApparelComputer, Communication and Consumer ElectronicOthers

Therefore, e-commerce platforms that are able to increase the proportion of GMV from high-profitability apparel would have a higher advertising budget as a percentage of GMV from paying merchants who place advertisements.

E-commerce platforms’ promotion advantage is most important for high-profitability apparel, which is Alibaba’s advantage. As a percentage of total GMV, we expect Alibaba’s contribution from necessities to rise from 23% in 2019 to 26% in 2021, as it gains users and user stickiness from lower-tier cities, while apparel’s is projected to rise from 36% in 2019 to 38% in 2021, as it increasingly monetises an already large user base from lower-tier cities. Meanwhile, we expect GMV contribution from low-traffic and low-profitability 3C and other products to drop from 41% in 2019 to 36% in 2021.

E-commerce platforms’ promotion advantage is most important for high-profitability apparel, which is Pinduoduo’s advantage. As a percentage of total GMV, Pinduoduo’s necessities contribution is projected to rise from 34% in 2019 to 38% in 2021, as it continues to gain users and user stickiness in lower-tier cities, while apparel’s contribution is estimated to rise from 34% in 2019 to 38% in 2021, as it increasingly monetises its already large user base in lower-tier cities. Meanwhile, we expect GMV contribution from low-traffic and low-profitability 3C and other products to drop from 31% in 2019 to 34% in 2021.

Necessities (i.e. food and FMCG)

DBS Asian Insights SECTOR BRIEFING 86

31

Logistics advantage, which is JD’s advantage, however, is less important for high-profitability apparel. As a percentage of total GMV, we expect JD’s necessities contribution to rise from 21% in 2019 to 24% in 2021, as it continues to gain users and user stickiness in lower-tier cities, while apparel’s contribution keeps at 20% from 2019 to 2021, as monetisation of its growing user base in lower-tier cities is moderate. Meanwhile, we expect GMV contribution from low-traffic and low-profitability 3C and other products to drop from 59% in 2019 to 55% in 2021.

(2) Paying ratio. We estimate JD’s paying ratio (merchants, which spend ad dollar on its e-commerce platform, as % of total merchants) to be c.55%, Alibaba c.32%, Pinduoduo c.25%. This means e-commerce platforms with a large merchant size (in terms of annual GMV per merchant) will have higher profitability and thus, higher paying ratio.

Source: Company, DBS HK

Source: Company, DBS HK

Pinduoduo’s GMV mix

JD’s GMV mix

30% 24% 20% 19%

10%8% 6% 5%

30%34% 37% 38%

30% 34% 37% 38%

0%

20%

40%

60%

80%

100%

2018 2019 2020 2021Necessit ies (i.e. food and FMCG)ApparelComputer, Communication and Consumer ElectronicOthers

5% 5% 5% 5%

55% 54% 52% 50%

20% 20% 20% 20%

20% 21% 23% 24%

0%

20%

40%

60%

80%

100%

2018 2019 2020 2021Necessit ies (i.e. food and FMCG)ApparelComputer, Communication and Consumer ElectronicOthers

Necessities (i.e. food and FMCG)

Necessities (i.e. food and FMCG)

DBS Asian Insights SECTOR BRIEFING 8632

We expect JD’s paying ratio to decrease from c.55% in 2019 to c.48% in 2021, with an increasing base of small and medium merchants with lower profitability offering value-for-money products.

Meanwhile, we expect Alibaba’s/Pinduoduo’s paying ratio to increase from c.32%/c.27% in 2019 to c.33%/c.30% in 2021. We expect Pinduoduo to expand towards large merchants with higher profitability to meet demand from users in lower-tier cities led by rising consumption power in the long term.

(3) Monetisation rate. We estimate Alibaba’s monetisation rate (commission and advertising revenue as a percentage of 3P GMV) to increase from 3.6% in 2019 to 3.8% in 2021F, led by a rise in advertising budget as a percentage of paying merchants’ GMV, with higher GMV contribution from higher-profitability apparel.

Source: Company, DBS HK

Source: Company, DBS HK

E-commerce platforms’ merchant paying ratio and annual GMV per merchant

E-commerce platforms’ paying ratio

0.7

10.4

0.3

32%

55%

27%

0%

10%

20%

30%

40%

50%

60%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Alibaba JD Pinduoduo

Annual GMV per merchant (Rmb m)

Annual GMV per merchant (Rmb m, LHS)Paying ratio (RHS)

31.8% 32.1% 32.5% 33.0%

54.6% 54.9%51.4%

47.7%

25.3% 26.9% 28.4% 30.0%

10%

20%

30%

40%

50%

60%

2018 2019 2020 2021

Alibaba JD PinduoduoAlibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 86

33

We estimate Pinduoduo’s monetisation rate to increase from 3.0% in 2019 to 3.5% in 2021F, led by an increase in advertising budget as a percentage of paying merchants’ GMV, due to: (i) higher GMV contribution from higher-profitability apparel, as well as (ii) increasing paying ratio, as Pinduoduo includes larger merchants on its platform to meet demand from users in lower-tier cities in the long term.

In contrast, we estimate that JD’s monetisation rate will decrease from 4.5% in 2019 to 4.0% in 2021F, on (i) decreasing paying ratio with an increase in the number of small and medium merchants with lower profitability offering value-for-money products, as well as (ii) flattish advertising budget as a percentage of paying merchants’ GMV, due to a shift in GMV mix to small- and medium-scale merchants in the necessity product category to gain traffic in lower-tier cities.

Source: Company, DBS HK

E-commerce platforms’ monetisation rate

3.3%3.6% 3.6% 3.7% 3.8%

4.6% 4.5% 4.5%4.3%

4.0%

1.2%

2.8%3.0%

3.3%3.5%

0%

1%

2%

3%

4%

5%

2017 2018 2019 2020 2021Alibaba JD PinduoduoAlibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8634

Source: Company, DBS HK

E-commerce platforms’ non-GAAP core e-commerce net margin (2019)

78.7%

2.5%

-14.6%-20%

0%

20%

40%

60%

80%

100%

Alibaba JD Pinduoduo

E-commerce Business Profitability

There are concerns on profitability of e-commerce platforms in lower-tier cities. Therefore, we have done an analysis on e-commerce platforms’ cost structure and profitability.

Current e-commerce business profitability

E-commerce platforms’ current core business profitability varies. Alibaba and JD are profitable with non-GAAP marketplace-based core e-commerce (1P + 3P [online advertising and commission]) net margin of 78.7% and 2.5% respectively in 2019, while Pinduoduo, which focuses on lower-tier cities, was loss making with non-GAAP core e-commerce net margin of -14.6%.

E-commerce platforms’ e-commerce cost structure E-commerce platforms’ marketplace-based core e-commerce profitability is largely dependent on (1) their business models (i.e. JD’s estimated 1P non-GAAP net margin: -2.9%; estimated 3P non-GAAP net margin: 67.4%) and (2) whether their commission and advertising revenue is able to offset corresponding operating expenses.

We have broken down e-commerce platform’s cost structure. Sales and marketing expenses accounted for 19-99% of Alibaba’s and Pinduoduo’s core e-commerce revenue, while other

Alibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 86

35

operating expenses (i.e. general & administrative expenses and research & development expenses) was 2-27%. Cost of revenue accounted for 85% of JD’s core e-commerce revenue, while sales and marketing expenses was only 4%, due to its low margin 1P business, while sales and marketing expenses was 23% of JD’s 3P core e-commerce revenue.

Sales and marketing expenses is thus a major cost item. Sales and marketing expenses as a percentage of revenue is one of the critical factors affecting the profitability of 3P e-commerce platforms.

2019

Alibaba JD - 1P Pinduoduo

As % of 1P GMV

1P direct sales revenue 0.0% 44.6% 0.0%

- Cost of revenue 0.0% -41.3% 0.0%

- Fulfilment cost 0.0% -3.2% 0.0%

- Sales and marketing expenses 0.0% -1.0% 0.0%

- Other operating expenses 0.0% -0.5% 0.0%

= Non-GAAP operating income 0.0% -1.3% 0.0%

As % of 1P revenue

1P direct sales revenue 0.0% 100.0% 0.0%

- Cost of revenue 0.0% -92.5% 0.0%

- Fulfilment cost 0.0% -7.1% 0.0%

- Sales and marketing expenses 0.0% -2.3% 0.0%

- Other operating expenses 0.0% -1.0% 0.0%

= Non-GAAP operating income 0.0% -2.9% 0.0%

Source: Company, DBS HK

E-commerce platforms’ marketplace-based core e-commerce cost structure - 1P

DBS Asian Insights SECTOR BRIEFING 8636

Cost of revenue is major cost item and one of the critical factors affecting the profitability of 1P e-commerce platforms

2019

Alibaba JD - 3P Pinduoduo

As % of 3P GMV

3P online advertising and commission revenue

3.6% 4.5% 3.00%

- Sales and marketing expenses -0.7% -1.0% -2.60%

- Other operating expenses -0.1% -0.5% -0.80%

= Non-GAAP operating income 2.9% 3.1% -0.40%

As % of 3P revenue

Online advertising and commission revenue

100.0% 100.0% 100.00%

- Sales and marketing expenses -19.2% -22.5% -87.30%

- Other operating expenses -1.8% -10.0% -27.30%

= Non-GAAP operating income 79.0% 67.4% -14.60%

Source: Company, DBS HK

E-commerce platforms’ marketplace-based core e-commerce cost structure - 3P

E-commerce Business Profitability in Next Three YearsAs discussed above, sales and marketing expenses as a percentage of revenue is one of critical factors impacting the profitability of 3P e-commerce platforms. We have interviewed industry experts, such as advertising agents, to help us analyse whether (1) an increase in sales and marketing expenses per annual active customer could be offset by (2) a rise in marketplace-based core e-commerce revenue per annual active customer (1P + 3P [online advertising and commission]), which is factor of (i) average annual spending per customer and (ii) monetisation rate, to determine (3) e-commerce platforms’ profitability.

1. Sales and marketing expenses per annual active customerThe market has concerns on the profitability of e-commerce platforms in lower-tier cities due to market perception of heavy sales and marketing expenses (i.e. subsidies) in underpenetrated markets.

However, advertising agents have indicated that sales and marketing expenses per annual active customer in lower-tier cities is c.Rmb50, which is around 50% lower than c.Rmb100 in higher-tier cities. This is because costs per thousand impressions (CPM) are similar in different tier cities, but the conversion rate is lower in higher-tier cities with a higher e-commerce penetration rate.

DBS Asian Insights SECTOR BRIEFING 86

37

Sales and marketing expenses is a major cost item and a critical factor impacting 3P e-commerce platform’s profitability

Assuming that user acquisition cost in lower-tier cities is at a 50% discount to that in higher-tier cities, we estimate Alibaba’s sales and marketing expenses per annual active customer was Rmb95 in tier 1-2 cities and Rmb47 in tier 3 or below cities in 2019, which is close to the market average.

With c.5% p.a. increase in CPM, we expect Alibaba’s sales and marketing expenses per annual active customer to increase by 5% p.a. to Rmb104 in tier 1-2 cities and 17% p.a. to Rmb64 in tier 3 or below cities in 2021F.

Source: DBS HK

Source: DBS HK

E-commerce platforms’ acquisition costs per annual active customer (2019)

E-commerce platforms’ acquisition costs per incremental annual active customer (2019)

100

50

0

20

40

60

80

100

120

Tier 1-2 cit ies Tier 3 or below cities

Rmb

95

8170

4741

35

7164

51

0102030405060708090

100

Alibaba JD Pinduoduo

Rmb

Tier 1-2 cit ies Tier 3 or below cities OverallAlibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8638

We estimate Pinduoduo’s acquisition costs per annual active customer is much lower at Rmb70 in tier 1-2 cities and Rmb35 in tier 3 or below cities in 2019, which is c.70% of the market average. This is because Pinduoduo occupies one of the “online shopping” portals on WeChat’s mobile wallet (with other e-commerce platforms, JD, Vipshop and Mogu), leveraging WeChat’s user base. Besides, Pinduoduo’s traffic could come from sharing of the “team purchase” link among buyers’ existing social networks (i.e. buyers’ family and friends) on social communication platforms, such as Tencent’s WeChat. The sharing of this link also promotes Pinduoduo’s products as well as its platform to more potential buyers without incurring additional expenses. The benefit will be “buying one user, getting more users free”. That is why Pinduoduo’s acquisition costs per incremental annual active customer is c.20% of market average. The success of its “team purchase” link is attributed to support from Tencent, its second largest shareholder with 16.9% stake. This cannot be replicated by Alibaba as buyers are not able to share Alibaba’s links on Tencent’s WeChat.

With c.5% p.a. increase in CPM, we expect Pinduoduo’s acquisition costs per annual active customer to increase moderately by 17% p.a. to Rmb96 in tier 1-2 cities and 5% p.a. to Rmb39 in tier 3 or below cities in 2021F.

Source: DBS HK

Source: DBS HK

Alibaba - sales and marketing expenses per annual active customer

Pinduoduo - sales and marketing expenses per annual active customer

E-commerce platforms’ acquisition costs per incremental annual active customer (2019)

8395 100 104

41 4755

6464

71 7683

0

20

40

60

80

100

120

2018 2019 2020 2021

Rmb

Tier 1-2 cit ies Tier 3 or below cities Overall

49

7082

96

2435 37 39

3651 57 62

0

20

40

60

80

100

120

2018 2019 2020 2021

Rmb

Tier 1-2 cit ies Tier 3 or below cities Overall

Pinduoduo’s acquisition costs per annual active

customer is much lower

DBS Asian Insights SECTOR BRIEFING 86

39

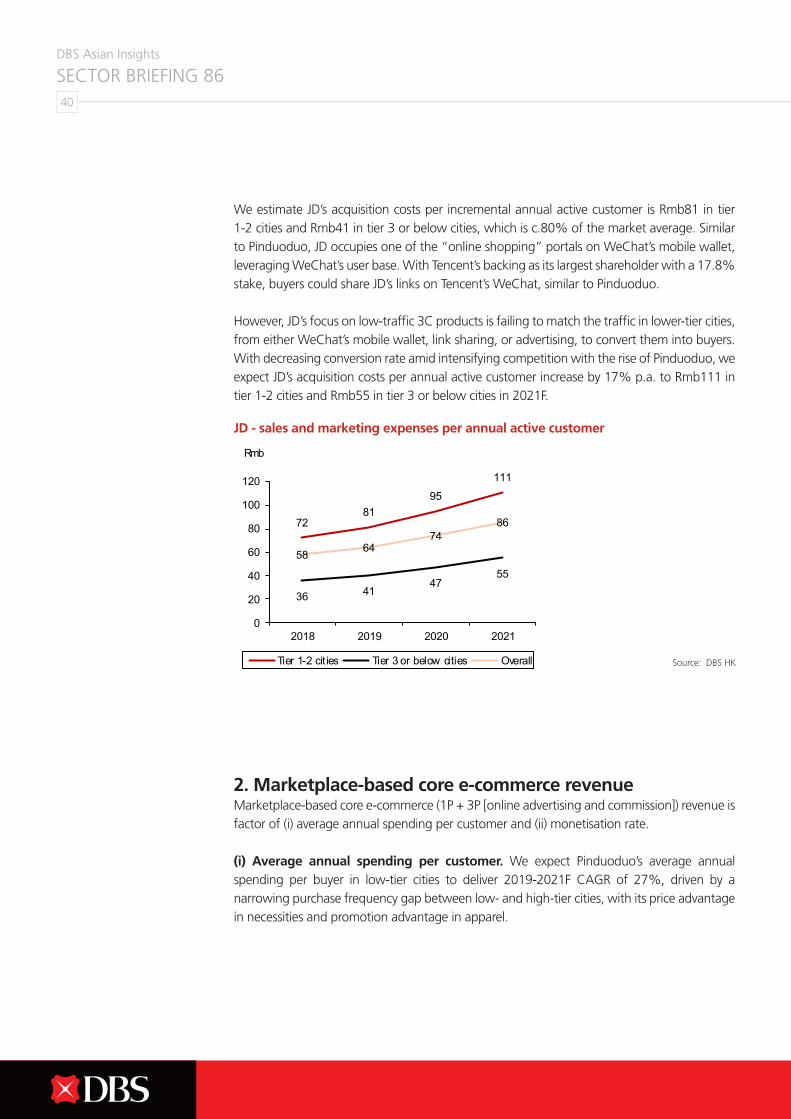

We estimate JD’s acquisition costs per incremental annual active customer is Rmb81 in tier 1-2 cities and Rmb41 in tier 3 or below cities, which is c.80% of the market average. Similar to Pinduoduo, JD occupies one of the “online shopping” portals on WeChat’s mobile wallet, leveraging WeChat’s user base. With Tencent’s backing as its largest shareholder with a 17.8% stake, buyers could share JD’s links on Tencent’s WeChat, similar to Pinduoduo.

However, JD’s focus on low-traffic 3C products is failing to match the traffic in lower-tier cities, from either WeChat’s mobile wallet, link sharing, or advertising, to convert them into buyers. With decreasing conversion rate amid intensifying competition with the rise of Pinduoduo, we expect JD’s acquisition costs per annual active customer increase by 17% p.a. to Rmb111 in tier 1-2 cities and Rmb55 in tier 3 or below cities in 2021F.

2. Marketplace-based core e-commerce revenueMarketplace-based core e-commerce (1P + 3P [online advertising and commission]) revenue is factor of (i) average annual spending per customer and (ii) monetisation rate.

(i) Average annual spending per customer. We expect Pinduoduo’s average annual spending per buyer in low-tier cities to deliver 2019-2021F CAGR of 27%, driven by a narrowing purchase frequency gap between low- and high-tier cities, with its price advantage in necessities and promotion advantage in apparel.

Source: DBS HK

JD - sales and marketing expenses per annual active customer

7281

95

111

36 4147

55

58 6474

86

0

20

40

60

80

100

120

2018 2019 2020 2021

Rmb

Tier 1-2 cit ies Tier 3 or below cities Overall

DBS Asian Insights SECTOR BRIEFING 8640

We expect Alibaba’s purchase frequency gap between low- and high-tier cities to narrow as well, with its user advantage in necessities and promotion advantage in apparel. However, we expect Alibaba to deliver a relatively moderate rise in average annual spending per buyer of 9% CAGR in 2019-2021F, as increasing purchase frequency will be partly offset by low ticket sizes in lower-tier cities.

We expect JD’s purchase frequency gap between low- and high-tier cities to narrow but at a moderate rate, as its logistics advantage is less important for necessities and apparel in lower-tier cities. We expect JD to deliver relatively moderate rise in average annual spending per buyer of 11% CAGR in 2019-2021F.

Source: Company, DBS HK

Source: Company, DBS HK

Pinduoduo - Average annual spending per customer

Alibaba - Average annual spending per customer

1,5321,813

2,743

3,410

4,364

687 8421,336

1,746

2,361991

1,308

1,9672,468

3,167

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

13,22612,368

13,427 13,887

15,825

5,927 5,7436,503 7,030

8,418

9,503 9,3209,989 10,302

11,774

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

DBS Asian Insights SECTOR BRIEFING 86

41

(ii) Monetisation rate. We estimate Alibaba’s monetisation rate (commission and advertising revenue as a percentage of 3P GMV) to increase from 3.6% in 2019 to 3.8% in 2021F, aided by increasing advertising budget as a percentage of paying merchants’ GMV, and shift in GMV mix to higher margin apparel category to monetise traffic from lower-tier cities.

We estimate Pinduoduo’s monetisation rate to increase from 3.0% in 2019 to 3.5% in 2021F, supported by an increase in the advertising budget as a percentage of paying merchants’ GMV and increasing paying ratio, with a shift in mix to larger merchants and apparels.

We estimate JD’s monetisation rate to decrease from 4.5% in 2019 to 4.0% in 2021F, with decreasing paying ratio and flattish advertising budget as a percentage of paying merchants’ GMV, with a shift in the merchant mix to small and medium scale and necessity category to gain traffic from lower-tier cities.

Source: Company, DBS HK

Source: Company, DBS HK

JD - Average annual spending per customer

E-commerce platforms’ monetisation rate

6,3976,915

8,0438,481

9,586

2,867 3,2113,820 4,120

4,800

4,9145,470

6,270 6,5797,422

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2017 2018 2019 2020 2021

Rmb

Tier 1 and 2 cities Tier 3 or below citiesOverall

3.3%3.6% 3.6% 3.7% 3.8%

4.6% 4.5% 4.5%4.3%

4.0%

1.2%

2.8%3.0%

3.3%3.5%

0%

1%

2%

3%

4%

5%

2017 2018 2019 2020 2021

Alibaba JD PinduoduoAlibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 8642

We expect Alibaba’s/Pinduoduo’s sales and marketing expenses as a percentage of marketplace-based core e-commerce revenue to decrease from 19.6%/87.3% in 2019 to 16.9%/55.6% in 2021 led by: (1) a moderate increase in sales and marketing expenses per annual active customer (3%/10% CAGR for each player during 2019-2021), offset by (2) rising marketplace-based core e-commerce revenue (11%/37% CAGR during 2019-2021) driven by (i) an increase in average annual spending per customer and (ii) higher monetisation rate, supported by Alibaba’s/Pinduoduo’s advantage in necessities and apparel.

However, JD’s sales and marketing expenses as a percentage of marketplace-based core e-commerce revenue is expected to increase from 2.1% in 2019 to 2.3% in 2021 as (1) the increase in sales and marketing expenses per annual active customer by 16% CAGR during 2019-2021 is unlikely to be fully offset by (2) a slower increase in marketplace-based core e-commerce revenue (10% CAGR during 2019-2021). Therefore, JD’s marketplace e-commerce revenue growth will be led by (i) a moderate increase in average annual spending per customer and (ii) a decrease in monetisation rate, as its logistics advantage is less important for necessities and apparel in lower-tier cities.

Source: DBS HK

Alibaba - Sales and marketing expenses as % of marketplace-based core e-commerce revenue

2018 2019 2020 2021

Tier 1-2 cities

Sales and marketing expenses per annual active customer

83 95 100 104

Average annual spending per customer 12,368 13,427 13,887 15,825

Sales and marketing expenses as % of GMV 0.7% 0.7% 0.7% 0.7%

Monetisation rate 3.9% 3.9% 4.0% 4.0%

Online advertising and commission revenue per annual active customers

478 527 554 638

Sales and marketing expenses as % of revenue 17.4% 18.0% 18.0% 16.4%

Tier 3 or below cities

Sales and marketing expenses per annual active customer

41 47 50 52

Average annual spending per customer 5,743 6,503 7,030 8,418

Sales and marketing expenses as % of GMV 0.7% 0.7% 0.7% 0.6%

Monetisation rate 2.8% 3.1% 3.3% 3.5%

Online advertising and commission revenue per annual active customers

163 199 232 295

Sales and marketing expenses as % of revenue 25.4% 23.8% 21.5% 17.7%

Overall

Sales and marketing expenses per annual active customer

64 71 73 76

Average annual spending per customer 9,320 9,989 10,302 11,774

Sales and marketing expenses as % of GMV 0.7% 0.7% 0.7% 0.6%

Monetisation rate 3.6% 3.6% 3.7% 3.8%

Online advertising and commission revenue per annual active customers

333 364 386 451

Sales and marketing expenses as % of revenue 19.2% 19.6% 19.1% 16.9%

DBS Asian Insights SECTOR BRIEFING 86

43

JD - Sales and marketing expenses as % of marketplace-based core e-commerce revenue

2018 2019 2020 2021

Tier 1-2 cities

Sales and marketing expenses per annual active customer

72 81 95 111

Average annual spending per customer 6,915 8,043 8,846 9,934

Sales and marketing expenses as % of GMV 1.0% 1.0% 1.1% 1.1%

1P monetisation rate 44.6% 44.6% 44.6% 44.6%

3P monetisation rate 4.5% 4.5% 4.5% 4.6%

Direct sales, Online advertising and commission revenue per annual active customers

1,889 2,171 2,356 2,612

Sales and marketing expenses as % of revenue 3.8% 3.7% 4.0% 4.2%

Tier 3 or below cities

Sales and marketing expenses per annual active customer

36 41 47 55

Average annual spending per customer 3,211 3,820 4,297 4,975

Sales and marketing expenses as % of GMV 1.1% 1.1% 1.1% 1.1%

1P monetisation rate 44.6% 44.6% 44.6% 44.6%

3P monetisation rate 4.5% 4.5% 3.5% 2.5%

Direct sales, Online advertising and commission revenue per annual active customers

877 1,030 1,121 1,254

Sales and marketing expenses as % of revenue 4.1% 3.9% 4.2% 4.4%

Overall

Sales and marketing expenses per annual active customer

58 64 74 86

Average annual spending per customer 5,470 6,270 6,862 7,692

Sales and marketing expenses as % of GMV 1.1% 1.0% 1.1% 1.1%

1P monetisation rate 44.6% 44.6% 44.6% 44.6%

3P monetisation rate 4.5% 4.5% 4.3% 4.0%

Direct sales, Online advertising and commission revenue per annual active customers

1,467 1,664 1,793 1,977

Sales and marketing expenses as % of revenue 4.0% 3.9% 4.1% 4.3%

Source: DBS HK

DBS Asian Insights SECTOR BRIEFING 8644

Pinduoduo - Sales and marketing expenses as % of marketplace-based core e-commerce revenue

2018 2019 2020 2021

Tier 1-2 cities

Sales and marketing expenses per annual active customer

49 70 82 96

Average annual spending per customer 1,813 2,743 3,410 4,364

Sales and marketing expenses as % of GMV 2.7% 2.6% 2.4% 2.2%

Monetisation rate 2.8% 3.0% 3.3% 3.5%

Online advertising and commission revenue per annual active customers

50 82 112 152

Sales and marketing expenses as % of revenue 96.9% 85.7% 73.4% 62.9%

Tier 3 or below cities

Sales and marketing expenses per annual active customer

24 35 37 39

Average annual spending per customer 842 1,303 1,746 2,361

Sales and marketing expenses as % of GMV 2.9% 2.7% 2.1% 1.6%

Monetisation rate 2.8% 3.0% 3.3% 3.5%

Online advertising and commission revenue per annual active customers

23 39 58 83

Sales and marketing expenses as % of revenue 104.3% 90.2% 64.1% 46.6%

Overall

Sales and marketing expenses per annual active customer

36 51 57 62

Average annual spending per customer 1,308 1,967 2,468 3,167

Sales and marketing expenses as % of GMV 2.8% 2.6% 2.3% 1.9%

Monetisation rate 2.8% 3.0% 3.3% 3.5%

Online advertising and commission revenue per annual active customers

36 59 81 111

Sales and marketing expenses as % of revenue 99.4% 87.3% 69.7% 55.6%

Source: DBS HK

Source: DBS HK

Sales and marketing expenses as % of marketplace-based core e-commerce revenue

19.2% 19.6% 19.1% 16.9%3.9% 3.9% 4.1% 4.3%

99.4%87.3%

69.7%55.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2018 2019 2020 2021

Alibaba JD PinduoduoAlibaba JD Pinduoduo

DBS Asian Insights SECTOR BRIEFING 86

45

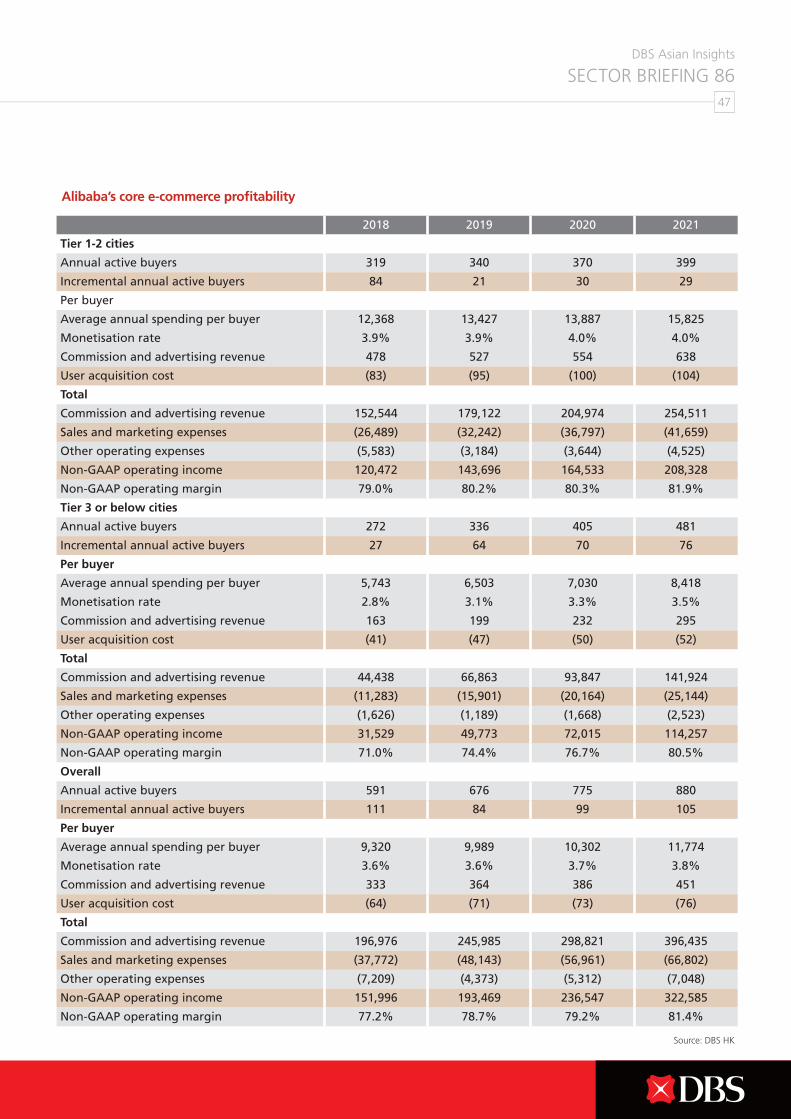

3. E-commerce platforms’ core e-commerce profitabilityAs discussed above, sales and marketing expenses as a percentage of revenue is one of critical factors impacting the profitability of 3P e-commerce platforms. With decreasing sales and marketing expenses as a percentage of marketplace-based core e-commerce revenue, we expect Alibaba’s/Pinduoduo’s non-GAAP core e-commerce net margin to increase from 78.7%/-14.6% in 2019 to 81.4%/14.1% in 2021F aided by a higher monetisation rate due to Alibaba’s/Pinduoduo’s advantage in necessities and apparel.

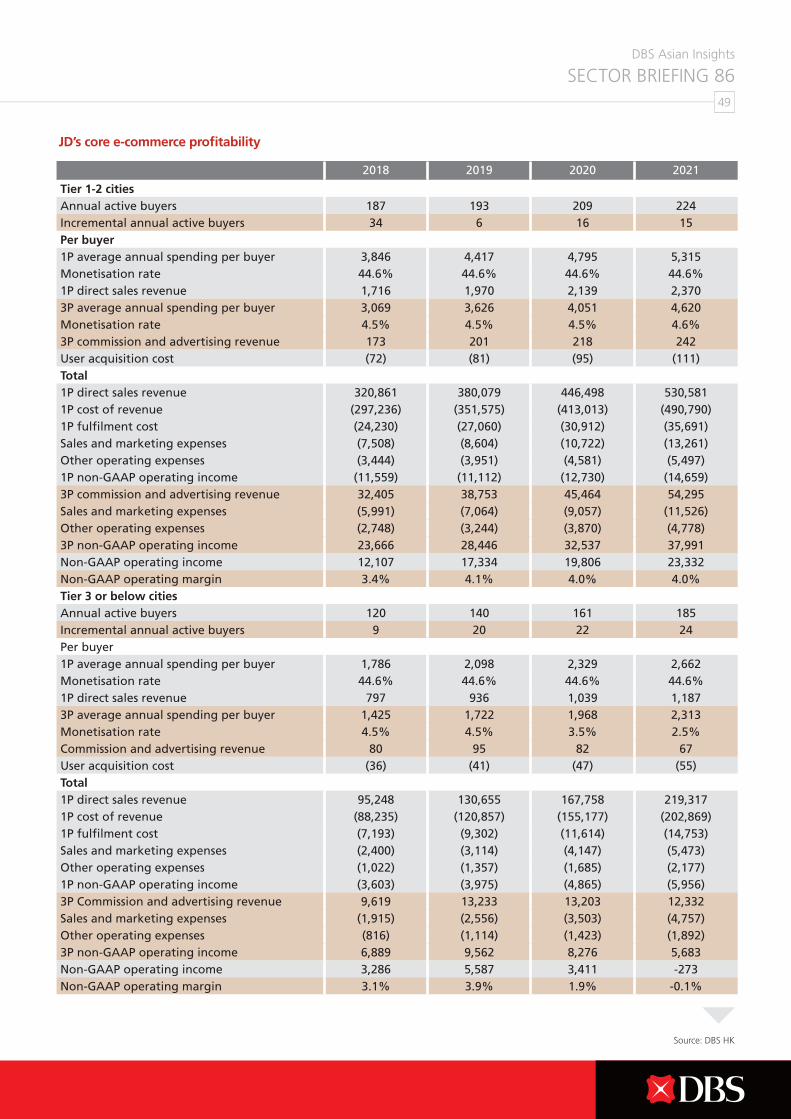

We expect JD’s non-GAAP core e-commerce net margin to decrease from 2.5% in 2019 to 1.8% in 2021F, on a decreasing monetisation rate as its logistics advantage is less important for necessities and apparel in lower-tier cities.

DBS Asian Insights SECTOR BRIEFING 8646

Alibaba’s core e-commerce profitability

2018 2019 2020 2021

Tier 1-2 cities

Annual active buyers 319 340 370 399

Incremental annual active buyers 84 21 30 29

Per buyer

Average annual spending per buyer 12,368 13,427 13,887 15,825

Monetisation rate 3.9% 3.9% 4.0% 4.0%

Commission and advertising revenue 478 527 554 638

User acquisition cost (83) (95) (100) (104)

Total

Commission and advertising revenue 152,544 179,122 204,974 254,511

Sales and marketing expenses (26,489) (32,242) (36,797) (41,659)

Other operating expenses (5,583) (3,184) (3,644) (4,525)

Non-GAAP operating income 120,472 143,696 164,533 208,328

Non-GAAP operating margin 79.0% 80.2% 80.3% 81.9%

Tier 3 or below cities

Annual active buyers 272 336 405 481

Incremental annual active buyers 27 64 70 76

Per buyer

Average annual spending per buyer 5,743 6,503 7,030 8,418

Monetisation rate 2.8% 3.1% 3.3% 3.5%

Commission and advertising revenue 163 199 232 295

User acquisition cost (41) (47) (50) (52)

Total

Commission and advertising revenue 44,438 66,863 93,847 141,924

Sales and marketing expenses (11,283) (15,901) (20,164) (25,144)

Other operating expenses (1,626) (1,189) (1,668) (2,523)

Non-GAAP operating income 31,529 49,773 72,015 114,257

Non-GAAP operating margin 71.0% 74.4% 76.7% 80.5%

Overall

Annual active buyers 591 676 775 880

Incremental annual active buyers 111 84 99 105

Per buyer

Average annual spending per buyer 9,320 9,989 10,302 11,774

Monetisation rate 3.6% 3.6% 3.7% 3.8%

Commission and advertising revenue 333 364 386 451

User acquisition cost (64) (71) (73) (76)

Total

Commission and advertising revenue 196,976 245,985 298,821 396,435

Sales and marketing expenses (37,772) (48,143) (56,961) (66,802)

Other operating expenses (7,209) (4,373) (5,312) (7,048)

Non-GAAP operating income 151,996 193,469 236,547 322,585

Non-GAAP operating margin 77.2% 78.7% 79.2% 81.4%

Source: DBS HK

DBS Asian Insights SECTOR BRIEFING 86

47

Pinduoduo’s core e-commerce profitability

2018 2019 2020 2021

Tier 1-2 cities

Annual active buyers 173 236 286 324

Incremental annual active buyers 122 63 50 38

Per buyer

Average annual spending per buyer 1,813 2,743 3,410 4,364

Monetisation rate 2.8% 3.0% 3.3% 3.5%

Commission and advertising revenue 50 82 112 152

User acquisition cost (49) (70) (82) (96)

Total

Commission and advertising revenue 8,729 19,390 32,009 49,349

Sales and marketing expenses (8,456) (16,615) (23,503) (31,027)

Other operating expenses (2,355) (5,300) (9,300) (14,931)

Non-GAAP operating income -2,082 -2,524 -794 3,392

Non-GAAP operating margin -23.8% -13.0% -2.5% 6.9%

Tier 3 or below cities

Annual active buyers 188 276 373 481

Incremental annual active buyers 96 88 98 108

Per buyer