dcg tech summit - opening remarks

TRANSCRIPT

OCTOBER 27 , 2017

Digital Currency Group3rd Annual Tech Summit

2

WELCOME

At Digital Currency Group, we believe we are uniquely positioned to provide a platform to support the industry’s

growth and evolution.

An important part of this is building a robust ecosystem of investors, corporations, institutions, and other stakeholders who

can be advocates, investors, and customers for companies.

OCTOBER 27 , 2017

DCG Tech SummitYear in Review

Barry Silbert, Founder & CEO

4

We believe that digital currencies and blockchain technology are going to transform our financial markets and drive positive

global economic and social change

OUR MISSION

It is our mission to accelerate the development of a better financial system

We do this by building and supporting digital currency and blockchain companies and leveraging our insights,

network, and access to capital

5

DCG TODAY

SUBSIDIARIES INVESTMENT PORTFOLIO DIGITAL CURRENCIES

110 companies across 28 countries; 50% IRR

$200+ million in value$40 million annualized revenue;

130% growth year-over-year

6

• C-Corp structure provides us with:

• Flexibility

• Opportunity to build a new investing/operating model

• Permanent capital

• Ability to raise money from strategic investors

• Potential to take DCG public

WE ARE NOT A VC FUND

7

OUR INVESTORS

8

• Target 2-5% ownership at seed stage (invest up to $200k)

• Focus on strategic life cycle investments (invest up to $500k in Series A, $1 mm in Series B)

• Join syndicates with other professional investors

• Back the very best teams in our target markets

• Minimize conflicts of interest; no board seats

• Opportunistically invest in tokens (up to $5 mm)

OUR INVESTING STRATEGY

9

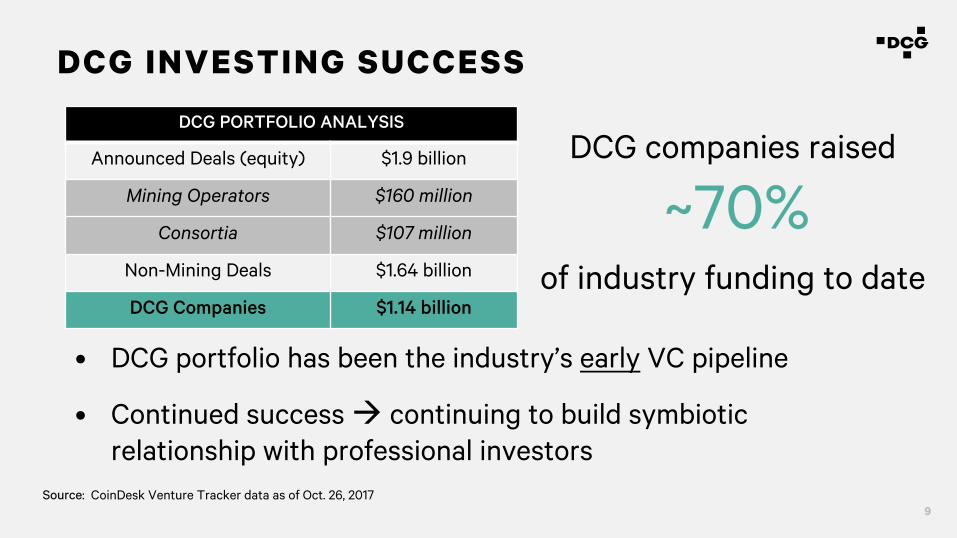

• DCG portfolio has been the industry’s early VC pipeline

• Continued success à continuing to build symbiotic relationship with professional investors

DCG PORTFOLIO ANALYSIS

Announced Deals (equity) $1.9 billion

Mining Operators $160 million

Consortia $107 million

Non-Mining Deals $1.64 billion

DCG Companies $1.14 billion

DCG companies raised

~70% of industry funding to date

DCG INVESTING SUCCESS

Source: CoinDesk Venture Tracker data as of Oct. 26, 2017

10

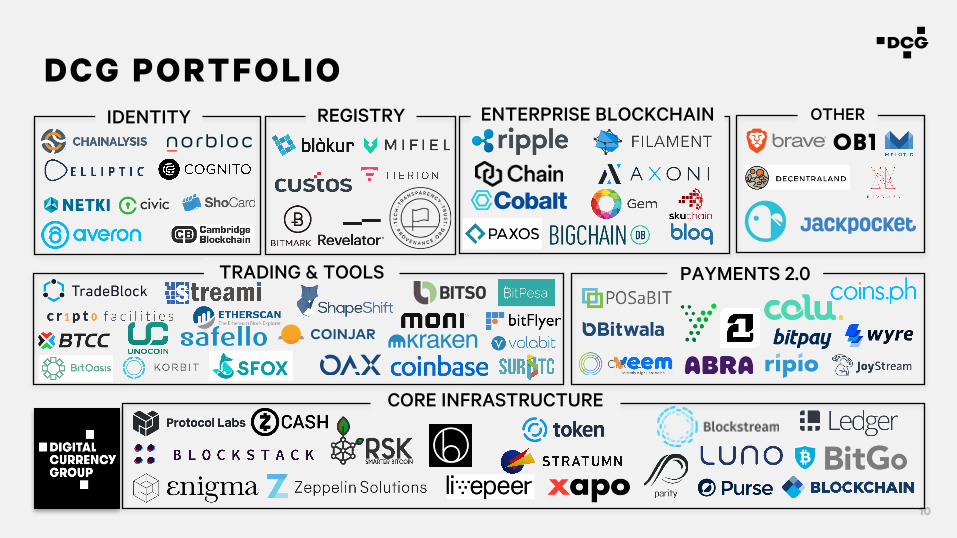

DCG PORTFOLIO

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

11

1. Core Infrastructure

2. Trading & Tools

3. Payments 2.0

4. Identity & Compliance

5. Blockchain Registry

6. Enterprise Blockchain

7. Other - Emerging Themes

KEY INVESTMENT AREAS

12

2017 PORTFOLIO ADDITIONS

Core Infrastructure

Trading & Tools

Payments 2.0

Identity & Compliance

BlockchainRegistry

Enterprise Blockchain

Other

Blockchain Coinjar POSaBIT norbloc Blokur Cobalt Nivaura

Basecoin* SFOX Provenance OB1

Ledger

Livepeer*

Parity

Stratumn

13

• Trading infrastructure (“picks and shovels”)

• Vaulting, custody, and compliance solutions

• Cross border payment infrastructure

• Digital currency as a speculative investment

WE ARE EXCITED ABOUT

14

CROSS BORDER PAYMENTS - ON/OFF RAMPS

15

CROSS BORDERS PAYMENTS VIA BITCOIN

Cumulative Volume

Source: Data provided by BitPesa, Bitso, Bitwala, and Wyre

$0

$250

$500

Aug-15 Feb-16 Aug-16 Feb-17 Aug-17

Mill

ions

16

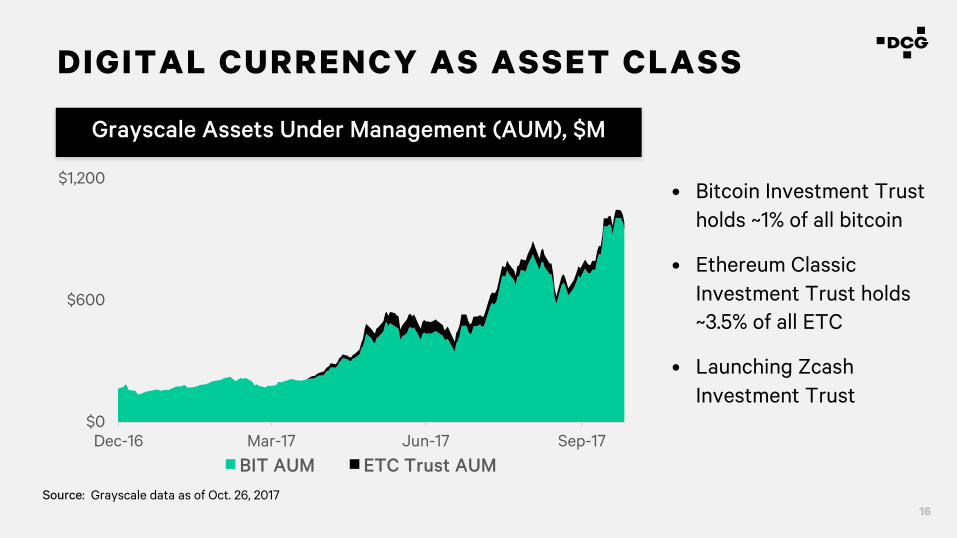

• Bitcoin Investment Trust holds ~1% of all bitcoin

• Ethereum Classic Investment Trust holds ~3.5% of all ETC

• Launching ZcashInvestment Trust

DIGITAL CURRENCY AS ASSET CLASS

Grayscale Assets Under Management (AUM), $M

Source: Grayscale data as of Oct. 26, 2017

$0

$600

$1,200

Dec-16 Mar-17 Jun-17 Sep-17BIT AUM ETC Trust AUM

17

• ICOs

• 99% of the digital assets currently being traded

• Decentralized token exchanges

• Crypto funds

WE ARE NOT EXCITED ABOUT…YET

18

• China crackdown on bitcoin (yes, again) and ICOs

• Scaling debate rages on

• Everybody is making money -> everybody is a trading/investing genius

• Over 100 crypto funds in the market raising capital

• ICO overload – greed and reckless investing permeates the space

• Huge disconnect in valuations between ICOs and seed/Series A financings

• First Unicorns built – Coinbase & Ripple

• “Experts” weigh in and declare bitcoin is [pick one: fraud/Enron/ponzi/bubble/tulip]

• Massive transaction volume growth in South Korea, Japan, Mexico

• Futures and derivatives markets opening up

• Institutional investors starting to dig in, but not investing yet

INDUSTRY STATE OF AFFAIRS

19

REVIEWING 2017 PREDICTIONS1. Bitcoin as a store of value re-emerges as key theme ü

2. Bitcoin becomes more accessible to retail and institutional investors via ETF(s) û

3. Cross border payments/remittance using bitcoin hits a $1 billion run rate û

4. Exponential bitcoin transactional growth in India, Japan & Middle East ü

5. Explosion of blockchain POCs focusing on supply chain ü

6. Identity solution competition heats up…but no leader emerges ü

7. SEC comes down hard on ICOs û

8. First >$50 mm M&A transaction ü

9. Micropayment models materialize ü

10. Bitcoin price on 12/31/17 = higher ü

20

TOP TEN PREDICTIONS FOR 2018

1. Crypto funds raise over $1 billion

2. First IPO on a major global exchange

3. No ETFs get approved in the U.S.

4. First U.S. brokerage firm offers bitcoin access to customers

5. Large number of ICO tokens deemed to be securities by regulators -> rescission rights triggered

6. Regulators go after certain crypto exchanges for trading token “securities”

7. ICO market collapses (number of issuances, valuations)

8. Corporates start to abandon “blockchain” projects

9. Aggregate market value of digital currencies/assets exceeds $250 billion

10. Jamie Dimon capitulates and walks back his “bitcoin is a fraud” comment

OCTOBER 27 , 2017

DCG Tech SummitICOs and Token Sales

Travis Scher, Investment Associate

22

WHAT IS AN ICO/TOKEN SALE?

23

WHAT IS AN ICO/TOKEN SALE?

The sale, typically a crowdsale, of a blockchain-native digital asset (a “token”), which confers the right to participate in a

network or use a product or service

Tokens typically do not represent equity in a business or explicitly provide any legal rights to the holder (though a

token may still be deemed a “security” by regulators)

24

BLOCKCHAIN VC V. TOKEN SALES

$0

$700,000

$1,400,000

2016 2017Q1 2017Q2 2017Q3

Thou

sand

s

BlockchainVC TokenSales

• TheamountraisedintokensaleshaveblownpasttheamountraisedbyblockchaincompaniesintraditionalVC

• InQ3,~$1.25bnwasinvestedintokensalescomparedto$155mminblockchainventuredeals

25

TOKEN SALES V. GLOBAL SEED FUNDING

$0

$700,000

$1,400,000

$2,100,000

$2,800,000

$3,500,000

$4,200,000

$4,900,000

$5,600,000

$6,300,000

$7,000,000

$7,700,000

$8,400,000

2016 2017Q1 2017Q2 2017Q3

Thou

sand

s

TokenSales GlobalSeedFunding

• Tokensalesareapproachingglobalangel/seedfundinglevels

• InQ1-Q3,tokensaleshaveraised~$2bnversus~$6bnforangel/seedfunding

• That’sin165salesversusnearly11,000angel/seedround

26

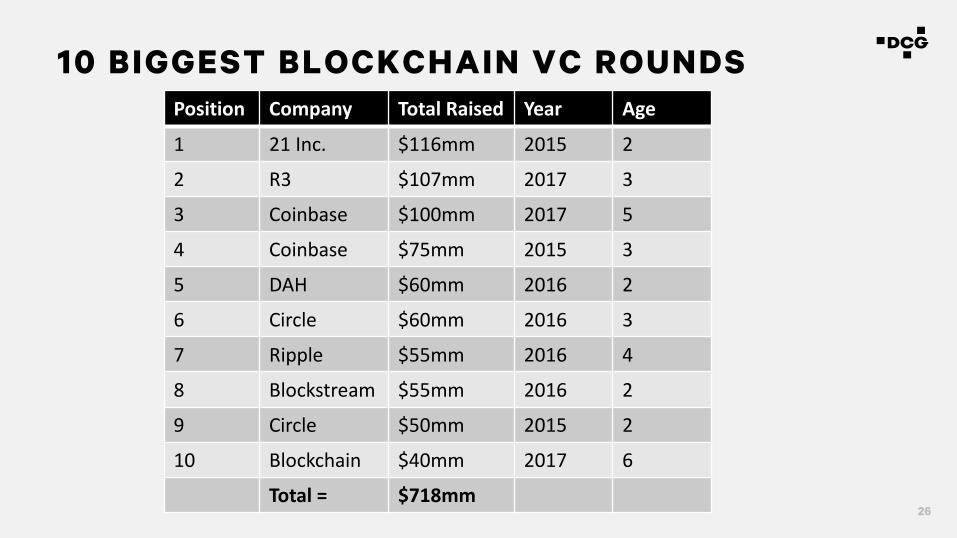

10 BIGGEST BLOCKCHAIN VC ROUNDSPosition Company TotalRaised Year Age

1 21Inc. $116mm 2015 2

2 R3 $107mm 2017 3

3 Coinbase $100mm 2017 5

4 Coinbase $75mm 2015 3

5 DAH $60mm 2016 2

6 Circle $60mm 2016 3

7 Ripple $55mm 2016 4

8 Blockstream $55mm 2016 2

9 Circle $50mm 2015 2

10 Blockchain $40mm 2017 6

Total= $718mm

27

10 BIGGEST TOKEN SALESPosition Project TotalRaised Year Age

1 Filecoin $257mm 2017 3

2 Tezos $232mm 2017 3

3 EOS $185mm 2017 <1

4 Bancor $153mm 2017 <1

5 TheDAO $150mm 2016 <1

6 Kin $97mm 2017 <1

7 Status $90mm 2017 <1

8 TenX $64mm 2017 <1

9 MobileGo $53mm 2017 <1

10 Kyber $48mm 2017 <1

Total= $1,329mm

28

WOW• The ten largest token sales have raised $1.33 billion, almost twice as much

as the ten largest blockchain venture rounds

• Eight of ten of the largest token sales were under development for less than one year at the time of the ICO (compared to 3.2 years for the venture rounds)

• These eight raised an average of $105 million – more than 3x the median US growth equity round!

29

DCG PORTCO TOKEN SALES - COMPLETED• 5 DCG portfolio companies (5.6% of active portfolio) have completed token

sales

• Collectively, those companies previously raised just $18mm in VC funding

• Each raised at least $25mm, and together a total of $395mm

30

DCG PORTCO TOKEN SALES – IN PROCESS• 12 more DCG portfolio companies are in the midst of or planning to do a

token sale (13.5% of active portfolio)

• These 17 companies (19.1% of active portfolio) are spread across 7 countries and 4 continents – it’s a global phenomena

31

WHY IS THIS HAPPENING?• It’s cheaper and easier to create tokens using Ethereum and the ERC20

standard

• Bitcoin and Ethereum have gained $100bn+ in market cap, and people are re-investing profits

• Political trends around decentralization, privacy, and autonomy

• Macro environment with lack of other attractive asset classes

Also:Hype,Mania,HerdMentality,andMadness!

33

IMPLICATIONS FOR VC’S• Displacement/Disruption/Loss of Opportunity?

• Should you invest in tokens?

• Should you invest in a crypto fund?

• Should your portfolio company do an ICO?

• What happens if your portfolio company ICOs?

34

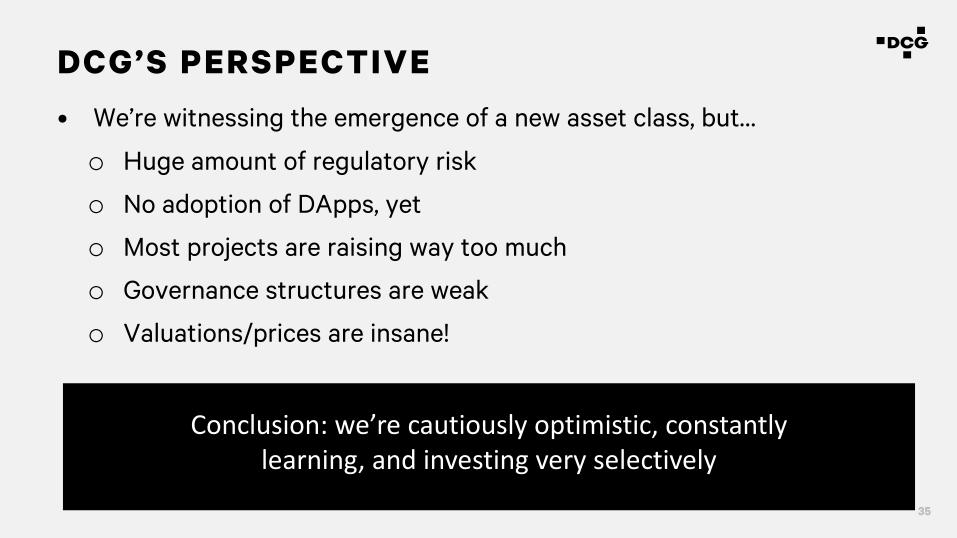

DCG’S PERSPECTIVE• We’re witnessing the emergence of a new asset class, but…

o Huge amount of regulatory risk

o No adoption of DApps, yet

o Most projects are raising way too much

o Governance structures are weak

o Valuations/prices are insane!

35

DCG’S PERSPECTIVE• We’re witnessing the emergence of a new asset class, but…

o Huge amount of regulatory risk

o No adoption of DApps, yet

o Most projects are raising way too much

o Governance structures are weak

o Valuations/prices are insane!

Conclusion:we’recautiouslyoptimistic,constantlylearning,andinvestingveryselectively

36

TYPES OF PROJECTS• Global Currency/Store of Value (e.g., Bitcoin, Zcash)

• Smart Contract Platforms (e.g., ETH, ETC, Tezos)

• Decentralized Compute Resources (e.g., Filecoin, Livepeer)

• Decentralized Exchange/Parachains (e.g., 0x, Cosmos, Polkadot)

• Currency for Internal Commerce or Access (e.g., Decentraland, OAX)

37

DCG’S TOKEN INVESTMENT FRAMEWORK• Mission-driven, high-integrity team

• Benefits from being decentralization/being on a blockchain

• Strong case for new token

• Token distribution done compliantly

• No uncapped notes, reasonable “implied market cap”

38

TEN THINGS TO WATCH IN 20181. Real use cases – what will be first widely DApp/Appcoin?

2. Infrastructure development – decentralized exchange, custody, PoS, scaling

3. Stablecoin that works?

4. Valuation methodologies – any progress?

5. Projects that raised “endowment fund” – can they deliver on expectations?

6. Projects that stall – can they pivot? What happens to $$ if they give up?

7. User/partner/developer growth pools – do they work?

8. Enterprise adoption – will they touch tokens?

9. Security tokens – any benefit besides calling it an “ICO”?

10. Regulation – will the SEC pull the punch bowl?

OCTOBER 27 , 2017

DCG Tech SummitPortfolio Growth & Development

Meltem Demirors, Director of Development

40

41

42

43

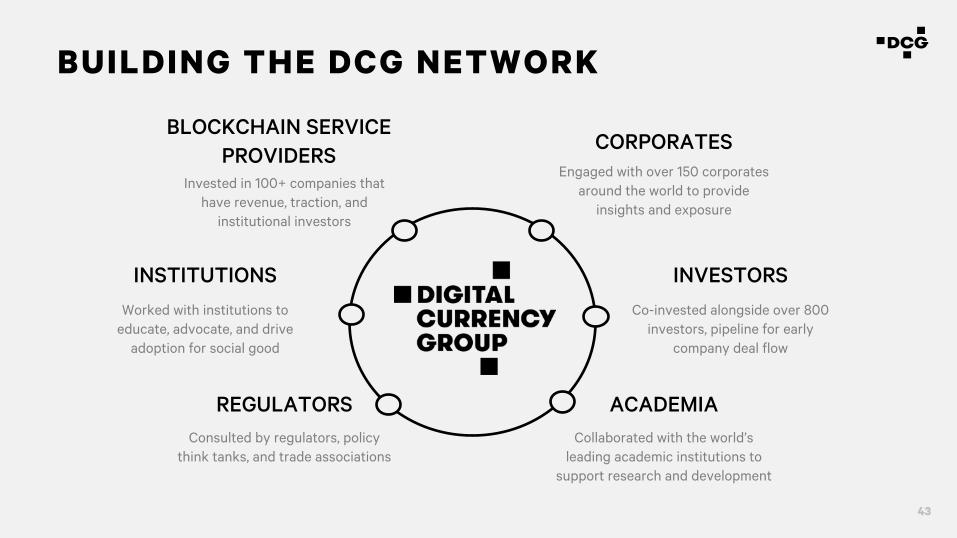

BUILDING THE DCG NETWORK

CORPORATES

ACADEMIA

INVESTORS

REGULATORS

INSTITUTIONS

BLOCKCHAIN SERVICE PROVIDERS

Invested in 100+ companies that have revenue, traction, and

institutional investors

Co-invested alongside over 800 investors, pipeline for early

company deal flow

Engaged with over 150 corporates around the world to provide

insights and exposure

Collaborated with the world’s leading academic institutions to

support research and development

Worked with institutions to educate, advocate, and drive

adoption for social good

Consulted by regulators, policy think tanks, and trade associations

44

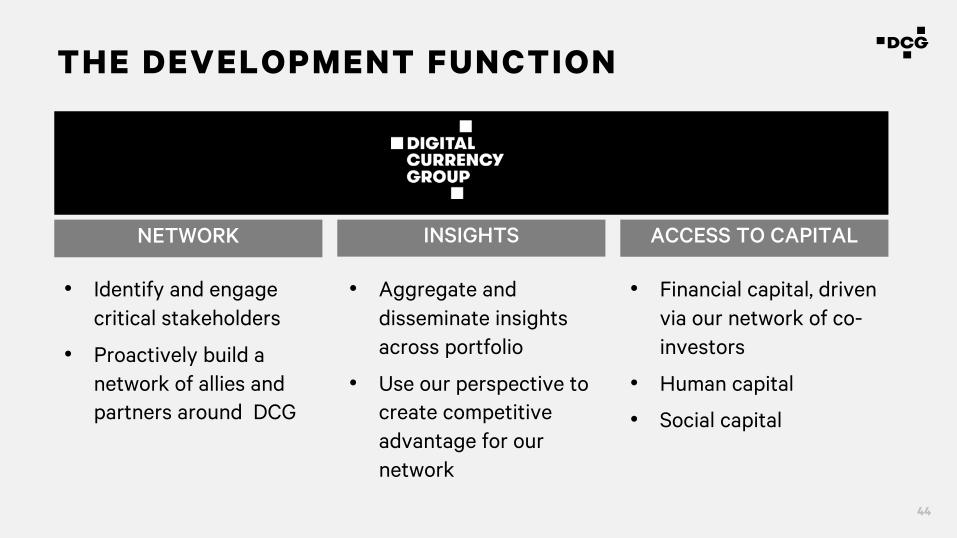

THE DEVELOPMENT FUNCTION

NETWORK INSIGHTS ACCESS TO CAPITAL

• Identify and engage critical stakeholders

• Proactively build a network of allies and partners around DCG

• Financial capital, driven via our network of co-investors

• Human capital

• Social capital

• Aggregate and disseminate insights across portfolio

• Use our perspective to create competitive advantage for our network

45

OVERVIEW

• Data from across the DCG Portfolio

• Insights on evolving digital currency and blockchain business models

• What we’ve done and what’s next

46

A GLOBAL PORTFOLIO

• The DCG Portfolio represents businesses in 28 countries

• Portfolio operations span over 40 countries and continue to spread as companies open subs

• US-based companies represent over 50% of the portfolio, but % has been declining over time

• 9 of 15 new investments in 2017 were outside of US

Africa3%

South America7%

North America

54%

Europe21% MENA

2%

Asia13%

Geographic Distribution Interesting Facts

47

STILL EARLY STAGE

0

20

40

Pre-Seed Seed Series A Series B Series C Series D

• Portfolio 65% seed-stage last year, now less than 45%

• More than 50% of the portfolio has raised follow-on capital

• Increasing number of late stage deals – many based in US, but a handful in Asia and Europe

• Majority of late stage companies are bitcoin focused – only 1 pure blockchain co past Series A

Portfolio by Stage Interesting Facts

48

A LOT OF HUMAN CAPITAL

0

25

50

<15 15 - 50 50 - 150 150 +

Portfolio Employee Distribution Interesting Facts

• 2,475 employees in portfolio– over 2,500 including DCG + subs

• 50% of portfolio is still under 15 employees – lean and mean teams!

• Only 9 companies with more than 50 employees – mix of later stage (Series B and beyond) B2B and B2C companies

• Very few sole founders – strong affinity for founding teams

49

GENERATING FINANCIAL CAPITAL

0

16

32

Pre-product Pre-revenue Revenue Breakeven Profit

Portfolio Performance Interesting Facts

• 68% of companies are making money, but relatively new trend

• Most companies were not profitable 9 months ago – high correlation between profit and digital currency market cap

• Companies that are not yet making money are mostly private blockchain / non digital currency companies

50

GENERATING FINANCIAL CAPITAL

Number of Employees

<15 15 - 50 50 - 150 150 +

Pre-product 7 1

Pre-revenue 11 7

Revenue 15 16

Breakeven 5 1

Profit 4 7 5 4

Portfolio Performance by Company Size Interesting Facts

• Doesn’t take a lot of people or capital to be profitable right now

• All companies over 50 employees are profitable, and directly interact with digital currencies

• Most pre-revenue and pre-product companies focused on enterprise blockchain where sales cycles last 18 – 24 months

51

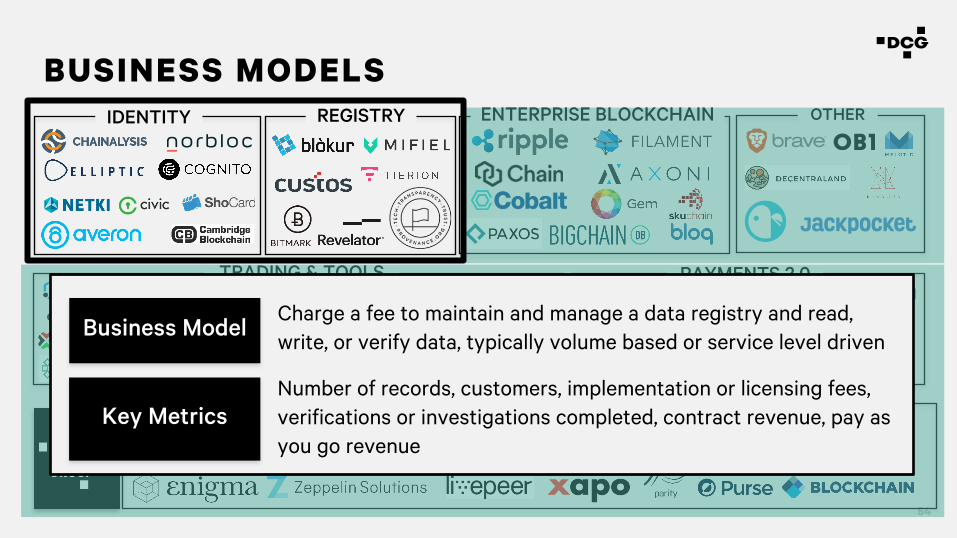

BUSINESS MODELS

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

Business Model

Key Metrics

Build broadly adopted software networks and software tools, become the standard for networking or services

Number of users or nodes, market penetration or adoption, developer ecosystem, applications, git pulls, token distribution

52

BUSINESS MODELS

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

Business Model

Key Metrics

Charge a fee to provide a product or service, typically volume based or service level driven

Number of customers, trading volume, trading revenue, trading profit, margin on traded volume

53

BUSINESS MODELS

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

Business Model

Key Metrics

Charge a fee to provide a payment product or payment service, typically volume based or service level driven

Number of customers / transactions, retention, payment volume, payment revenue, profit margin

54

BUSINESS MODELS

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

Business Model

Key Metrics

Charge a fee to maintain and manage a data registry and read, write, or verify data, typically volume based or service level driven

Number of records, customers, implementation or licensing fees, verifications or investigations completed, contract revenue, pay as you go revenue

55

BUSINESS MODELS

CORE INFRASTRUCTURE

IDENTITY REGISTRY ENTERPRISE BLOCKCHAIN

TRADING & TOOLS PAYMENTS 2.0

OTHER

Business Model

Key Metrics

Uncertain – often resembles enterprise SaaS but with higher degree of up front consultation, design, and integration work

Project-based revenues, implementation costs, licensing fees, volume based fees

56

CONSISTENT TRENDS

• Companies starting to find a useable business model and growing and scaling this model

• Revenue across business models is growing 5-20% MoM, but reliance on key partners can set back progress

• Most companies heavily focused on building and scaling customer acquisition strategies

• Converting enterprise sales pipeline into revenue is an expensive and slow process

57

BIGGEST CHALLENGES FOR COMPANIES

• Banking partnerships

• Regulation and compliance

• Making long term strategic decisions in an environment with a high degree of noise

• Converting sales pipeline into ARR

• Hiring at all levels of the organization

• Changing the narrative around the industry / companies

58

KEY EFFORTS IN 2017

• Scaled portfolio management process from 70 companies to now over 100, including companies raising ICO funds

• Conducted multiple events with banks, regulators, and companies focused on driving collaboration

• Grew enterprise partnership strategy, especially with IBM, AWS, and key corporate partners to accelerate sales cycles

59

KEY GOALS FOR 2018

• Begin building ecosystems around protocols and their associated tokens leveraging broader DCG network

• Focus on building banking alliance to help portfolio companies find, engage, and maintain banking relationships at scale

• Further expand the DCG platform to maximize human, social, and financial capital accessible to our network