debits, credits, & the relationship between the income statement & the balance sheet

TRANSCRIPT

Debits, Credits, & The

Relationship between the Income Statement & the

Balance Sheet

Your Basic Financial Accounting Guide

by

Dr. Tanae W. Acolatse

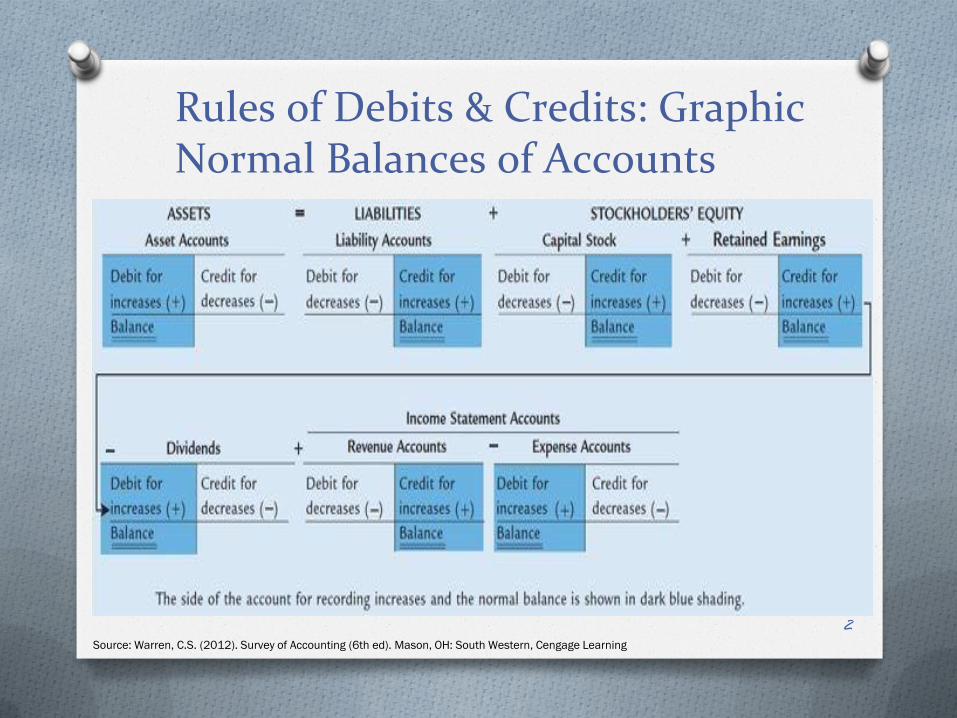

Rules of Debits & Credits: Graphic Normal Balances of Accounts

2 Source: Warren, C.S. (2012). Survey of Accounting (6th ed). Mason, OH: South Western, Cengage Learning

Rules of Debits & Credits Normal Balances of Accounts

O The normal balance of an account is the side

of the account used to record increases

O The normal balance of an asset account is a debit balance, while the normal balance of a liability account is a credit balance

O Useful in detecting errors in the recording process.

If an account normally having a debit balance actually has a credit balance, or vice versa, an error has occurred or an unusual situation exists.

3

Asset Accounts

Asset Accounts: Increased by debits and have a normal

debit balance (on the left side of the accounting equation)

O Exception: Some asset accounts, called contra asset

accounts, are increased by credits and have normal credit

balances.

O As the words contra asset imply, these accounts offset the

normal debit balances of asset accounts

Example: Accumulated depreciation, an offset to plant assets,

is increased by credits and has a normal credit balance.

Thus, accumulated depreciation is a contra asset account 4

Liability & Stockholders’ Equity Accounts

O Liability and stockholders' equity

accounts (on the right side of the

accounting equation)

O Increased by credits and have

normal credit balances

5

Dividend Accounts

O Dividend accounts appear on the right side of the accounting equation and decrease stockholders' equity (retained earnings)

O Increased by debits and have a normal debit balance

O Can be thought of as a type of contra account to retained earnings

6

Revenue Accounts

O Revenue accounts appear on the right side of the accounting equation and increase stockholders' equity (retained earnings)

O Increased by credits and have normal credit balances

7

Expense Accounts

O Expense accounts appear on the

right side of the accounting equation

and decrease stockholders' equity

(retained earnings)

O Increased by debits and have a

normal debit balance

O Can be thought of as a type of

contra account to revenues

8

Summary O The rules of debit and credit require that for each transaction, the

total debits equal the total credits

O Each transaction must be recorded so that the total debits for the

transaction equal the total credits.

Example: Assume that a company pays cash of $500 for supplies.

Asset Account: Supplies is debited (increased) by $500

Asset Account: Cash is credited (decreased) by $500

Example: If the company provides services and receives $2,000

from customers

Asset Account: Cash is debited (increased) by $2,000

Revenue Account: Fees Earned is credited (increased) by $2,000

transactions. 9

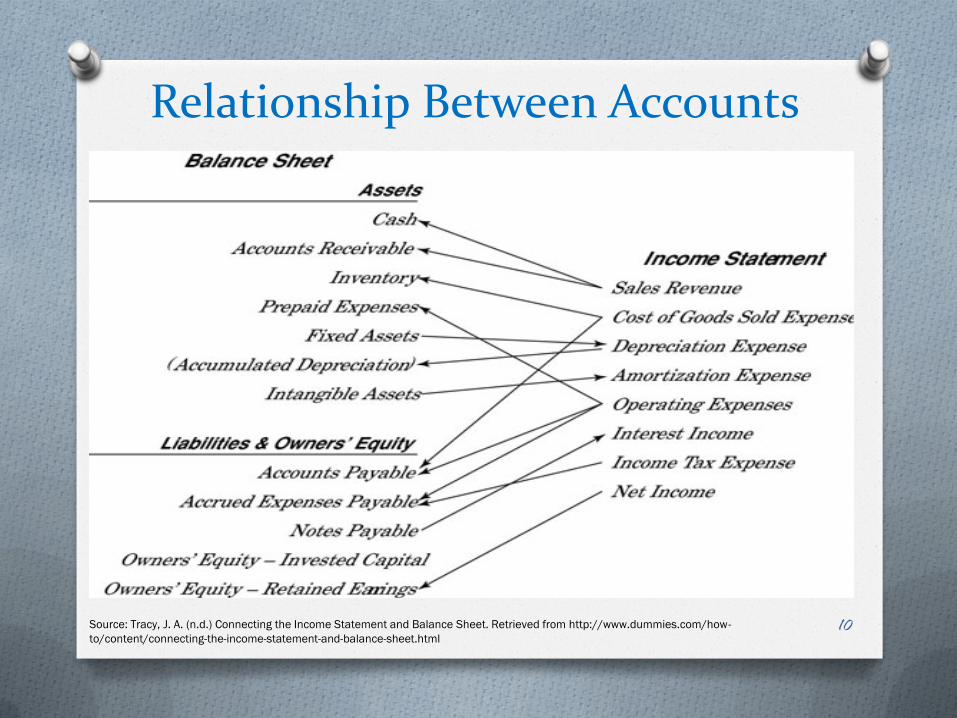

Relationship Between Accounts

10 Source: Tracy, J. A. (n.d.) Connecting the Income Statement and Balance Sheet. Retrieved from http://www.dummies.com/how-

to/content/connecting-the-income-statement-and-balance-sheet.html

Relationship Between Accounts (continued)

Accounts are connected as follows beginning with Sales:

O Making sales (and incurring expenses for making sales)

requires a business to maintain a working cash balance.

O Making sales on credit generates accounts receivable.

O Selling products requires the business to carry an

inventory (stock) of products.

11

Relationship Between Accounts (continued)

O Acquiring products involves purchases on credit that generate accounts payable.

O Depreciation expense is recorded for the use of fixed assets (long-term operating resources).

O Depreciation is recorded in the accumulated depreciation contra account (instead decreasing the fixed asset account).

O Amortization expense is recorded for limited-life intangible assets. 12

Relationship Between Accounts (continued)

O Operating expenses is a broad category of costs

encompassing selling, administrative, and general

expenses:

O Some of these operating costs are prepaid before the

expense is recorded, and until the expense is

recorded, the cost stays in the prepaid expenses

asset account.

O Some of these operating costs involve purchases on

credit that generate accounts payable.

O Some of these operating costs are from recording

unpaid expenses in the accrued expenses payable

liability.

13

Relationship Between Accounts

O Borrowing money on notes payable causes interest expense.

O A portion (usually relatively small) of income tax expense for the year is unpaid at year-end, which is recorded in the accrued expenses payable liability.

O Earning net income increases retained earnings.

14

References

Tracy, J. A. (n.d.). Connecting the income

statement and balance sheet. Retrieved

from http://www.dummies.com/how-

to/content/connecting-the-income-

statement-and-balance-sheet.html.

Warren, C.S. (2012). Survey of Accounting

(6th ed). Mason, OH: South Western,

Cengage Learning.

15