debt overhang and secular stagnation - institute for … overhang and secular stagnation adair...

TRANSCRIPT

Debt Overhang and Secular

Stagnation

Adair TurnerSenior Fellow

Institute for New Economic Thinking

Cass Business School London, 25th March 2015

www.ineteconomics.org

300 Park Avenue South, New York, NY 10010 | 22 Park Street, London W1K 2JB

IMF Medium term growth projections

1

0

2

4

6

Advanced Economies Emerging Market &developing countries

World

Fall 2011 Spring 2012 Fall 2012 Spring 2013 Fall 2013 Spring 2014

Source: IMF World Economic Outlook, October 2014

US Payroll employment monthly increasesDecember 20112 – December 2014

2

0

50

100

150

200

250

300

350

400

20

12

-01

20

12

-02

20

12

-03

20

12

-04

20

12

-05

20

12

-06

20

12

-07

20

12

-08

20

12

-09

20

12

-10

201

2-1

1

20

12

-12

20

13

-01

20

13

-02

20

13

-03

20

13

-04

20

13

-05

20

13

-06

20

13

-07

20

13

-08

20

13

-09

201

3-1

0

20

13

-11

20

13

-12

20

14

-01

20

14

-02

20

14

-03

20

14

-04

20

14

-05

20

14

-06

20

14

-07

20

14

-08

201

4-0

9

20

14

-10

20

14

-11

20

14

-12

Source: US Bureau of Labor Statistics

%

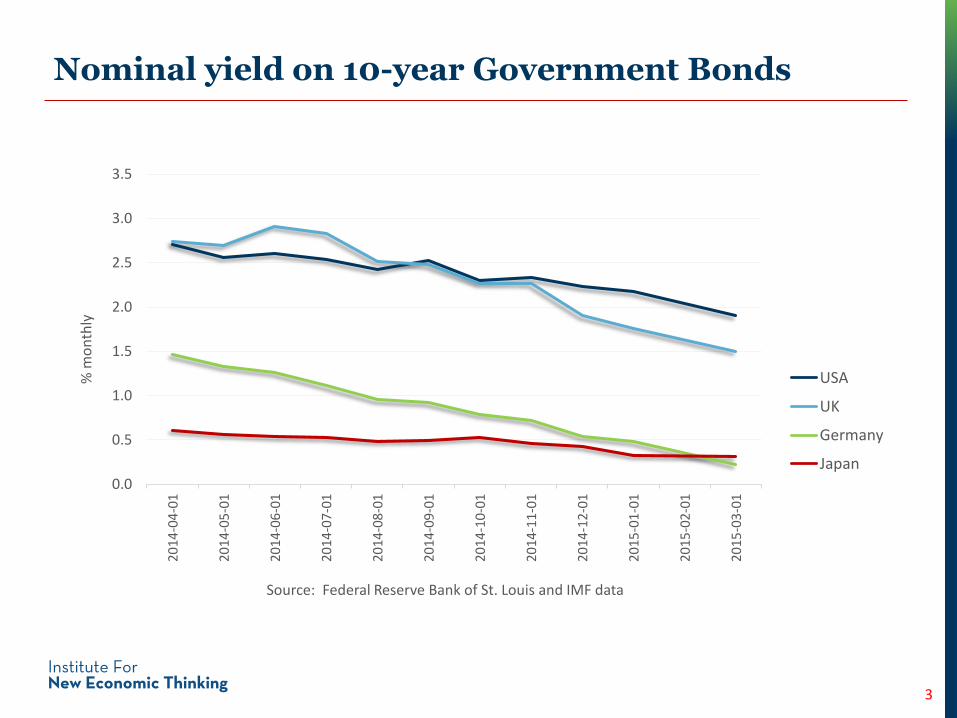

Nominal yield on 10-year Government Bonds

3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.520

14-0

4-0

1

2014

-05

-01

201

4-0

6-0

1

2014

-07

-01

2014

-08

-01

2014

-09

-01

2014

-10

-01

2014

-11

-01

2014

-12

-01

2015

-01

-01

2015

-02

-01

2015

-03

-01

USA

UK

Germany

Japan

% m

on

thly

Source: Federal Reserve Bank of St. Louis and IMF data

Consensus commentary still fails to reflect how deep

are the deflationary pressures created by

Debt overhang and deleveraging

Long-term secular trends

4

Private domestic credit as a % of GDP

5

Source: Financial and Sovereign Debt Crises: Some Lessons Learned and Those Forgotten, C. Reinhart & K. Rogoff, 2013

Advanced economies 1950 – 2011

Share of real estate lending in total bank lending

6

Source: The Great Mortgaging, Professor Alan Taylor, University of California, Davis

Ra

tio

of re

al e

sta

te le

nd

ing

to

to

tal le

nd

ing

0

0.1

0.2

0.3

0.4

0.5

0.6

0.71880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

10%

20%

30%

40%

50%

60%

70%

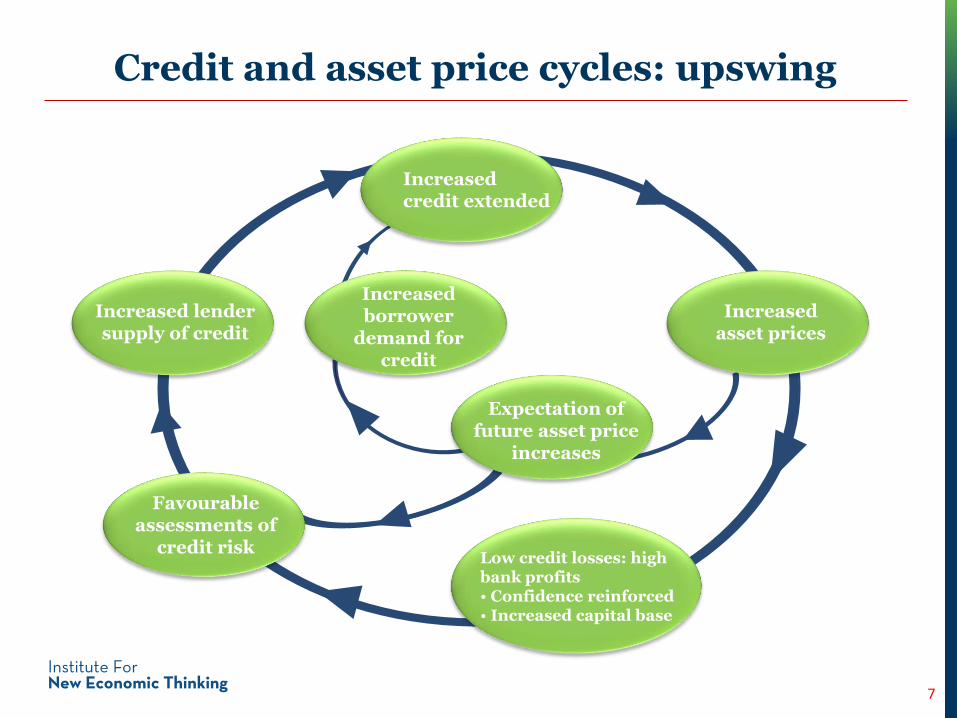

Credit and asset price cycles: upswing

7

Expectation of future asset price

increases

Increased credit extended

Low credit losses: high bank profits• Confidence reinforced • Increased capital base

Increased asset prices

Increased lender supply of credit

Favourable assessments of

credit risk

Increased borrower

demand for credit

Credit extension and house prices

House prices 2000 – 2007 Household debt as a % of GDP 2000 – 2007

Source: BEA; ONS; ECB

0

20

40

60

80

100

120

Q1 2000 Q1 2001 Q1 2002 Q1 2003 Q1 2004 Q1 2005 Q1 2006 Q1 2007%

GD

P

US UK Spain Ireland

0

50

100

150

200

250

Q1 2000 Q1 2001 Q1 2002 Q1 2003 Q1 2004 Q1 2005 Q1 2006 Q1 2007

Index:

2000 =

100

Spain US UK Ireland

Source: Ministry of Housing (Spain), S&P (US), DCLG

8

Credit and asset price cycles: downswing

9

Expectation of future asset price

falls

Less credit extended

High credit losses: low bank profits• Confidence dented• Reduced capital base

Falling asset prices

Restricted lender supply of credit

Cautious assessments of

credit risk

Reduced borrower

demand for credit

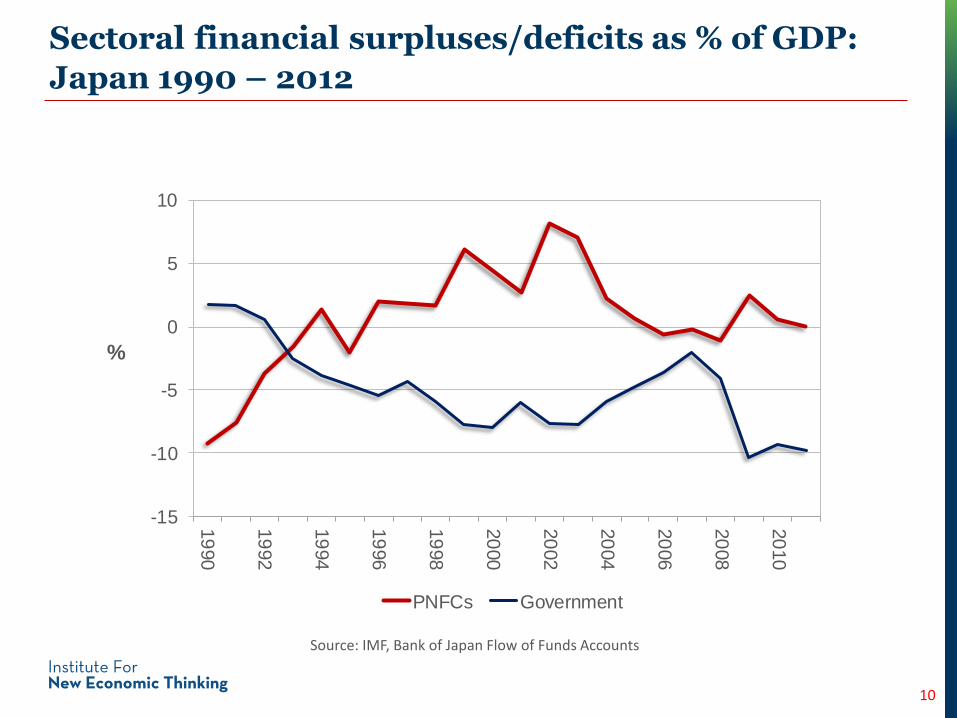

Sectoral financial surpluses/deficits as % of GDP:

Japan 1990 – 2012

10

Source: IMF, Bank of Japan Flow of Funds Accounts

-15

-10

-5

0

5

10

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

PNFCs Government

%

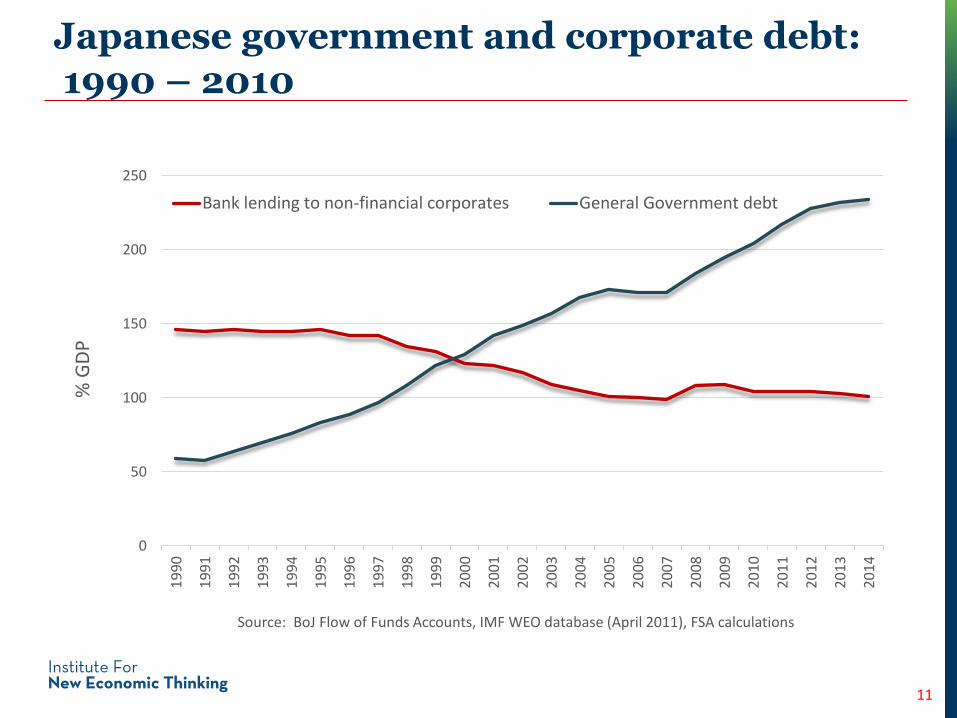

Japanese government and corporate debt:1990 – 2010

0

50

100

150

200

2501

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Bank lending to non-financial corporates General Government debt

11

Source: BoJ Flow of Funds Accounts, IMF WEO database (April 2011), FSA calculations

% G

DP

Shifting leverage: Private and public debt-to-GDP

12 12

50

65

80

95

110

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Household Non-financial Corp Public

% G

DP

Source: Geneva Report No 16 Deleveraging, What Deleveraging? ICMB / CEPR September 2014

Developed economies – Debt to GDP

13

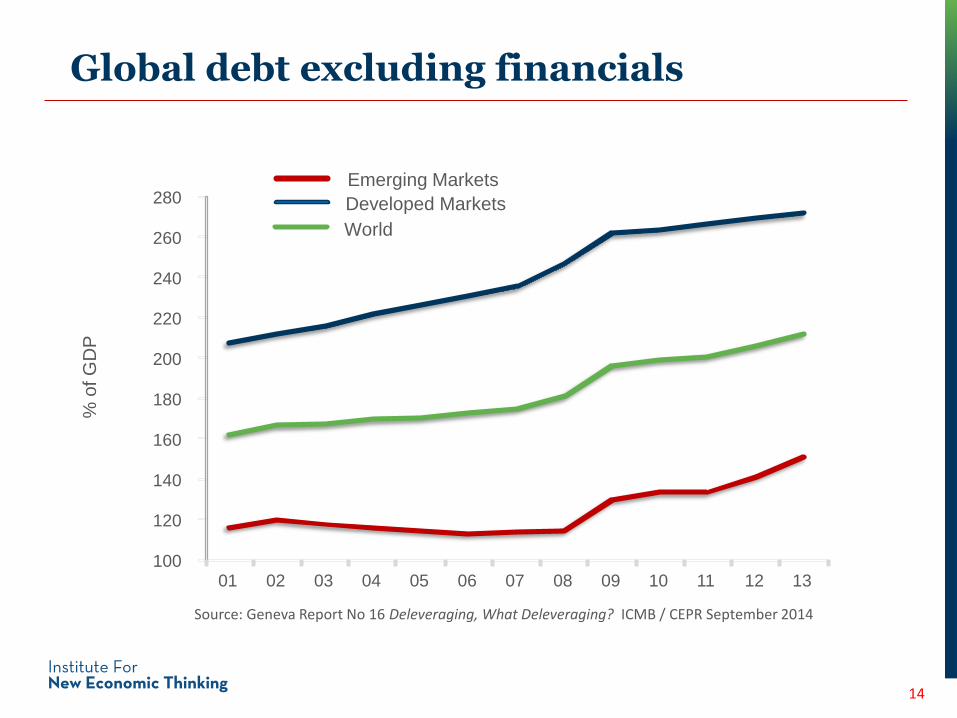

Global debt excluding financials

Source: Geneva Report No 16 Deleveraging, What Deleveraging? ICMB / CEPR September 2014

100

120

140

160

180

200

220

240

260

280

01 02 03 04 05 06 07 08 09 10 11 12 13

Developed Markets

Emerging Markets

World

% o

f G

DP

14

Emerging markets: total debt as % of GDP(excluding financial sector debt)

15

60

80

100

120

140

160

180

200

220

240

1 2 3 4 5 6 7 8 9 10 11 12 13

Series1 Series2 Series3 Series4 Series5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

ChinaChina

TurkeyBrazilIndia Emerging Markets

Source: Deleveraging, What deleveraging, The Geneva Report, 2014

China: debt as % of GDP

16

42 55

20

38

72

12524

65

2007 2014 Q2

Financial institutions

Non-Financial corporations

Households

Government

Source: McKinsey Global Institute

Total debt ($tr) 7.4 28.2

158

282

China’s debt exposure to property

17

Source: McKinsey Global Institute

$ trillion

Household Real estate Real estaterelated

Government Total exposureto property

As % of total non-financial debt 8 10-15 10-15 10 40-45

1.8

2.5-3

2-2.5

2.2 8.5-9.5

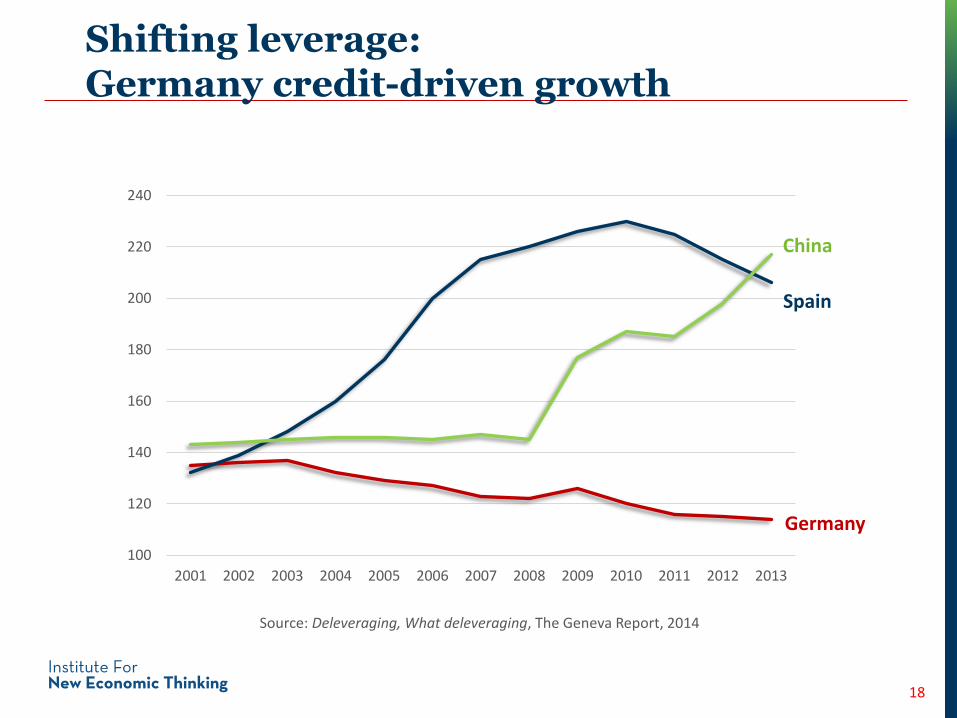

Shifting leverage: Germany credit-driven growth

18

Source: Deleveraging, What deleveraging, The Geneva Report, 2014

100

120

140

160

180

200

220

240

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Spain

China

Germany

General Government primary deficit

19

Eurozone

Japan

UK

US 7.2

6

7.8

1.6

Japan

Eurozone

Source: International Monetary Fund Fiscal Monitor, October 2014

% of GDP, average 2008- 2013

-6

-5

-4

-3

-2

-1

0

1

2

3

4

2008 2009 2010 2011 2012 2013

Net Exports as % of GDP

UK

USA

Japan

Eurozone

70

80

90

100

110

120

130

2008 2009 2010 2011 2012 2013 2014

Nominal GDP, 2008=100UK

USA

Japan

Eurozone

Sources: (IMF WEO, WB WDI)

70

80

90

100

110

120

130

2008 2009 2010 2011 2012 2013

UK

USA

Japan

Eurozone

Domestic Demand (GDP - Net Exports) 2008=100

20

Nominal demand growth 2008 – 2014

21

Raising actual and potential growth must remain a priority.

In advanced economies, this will require continued support

from monetary policy

The extended period of monetary accommodation and the

accompanying search for yields are leading to credit mispricing and asset

price pressures, and increasing the chance that financial stability risks

could derail the recovery.

IMFGlobal Financial Stability Review

October 2014

IMF World Economic Outlook October 2014

Shifting leverage: back to private again

22

UK Public net debt as % of GDP: 2009 - 2019

40

45

50

55

60

65

70

75

80

85

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

UK Household gross debt as % of income: 2009 - 2020

% P

erce

nt

140

145

150

155

160

165

170

175

180

185

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

Q1

20

20

Q1

Source: Office of Budget Responsibility, Economic and Fiscal Outlook, December 2014

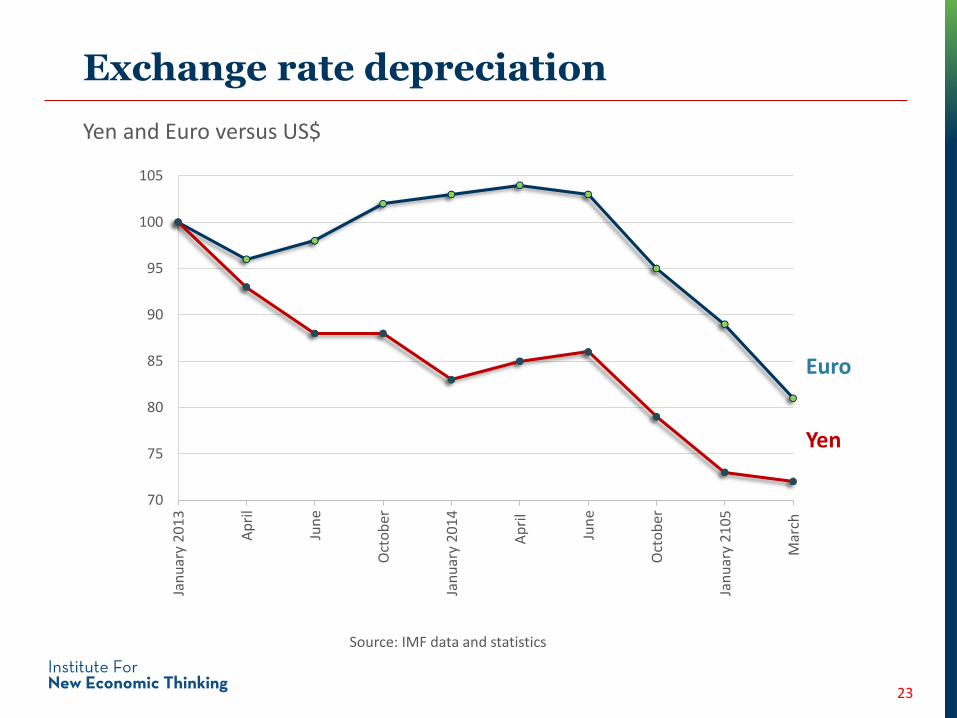

Exchange rate depreciation

23

70

75

80

85

90

95

100

105Ja

nu

ary

201

3

Ap

ril

Jun

e

Oct

ob

er

Jan

uar

y 20

14

Ap

ril

Jun

e

Oct

ob

er

Jan

uar

y 21

05

Mar

ch

Euro

Yen

Yen and Euro versus US$

Source: IMF data and statistics

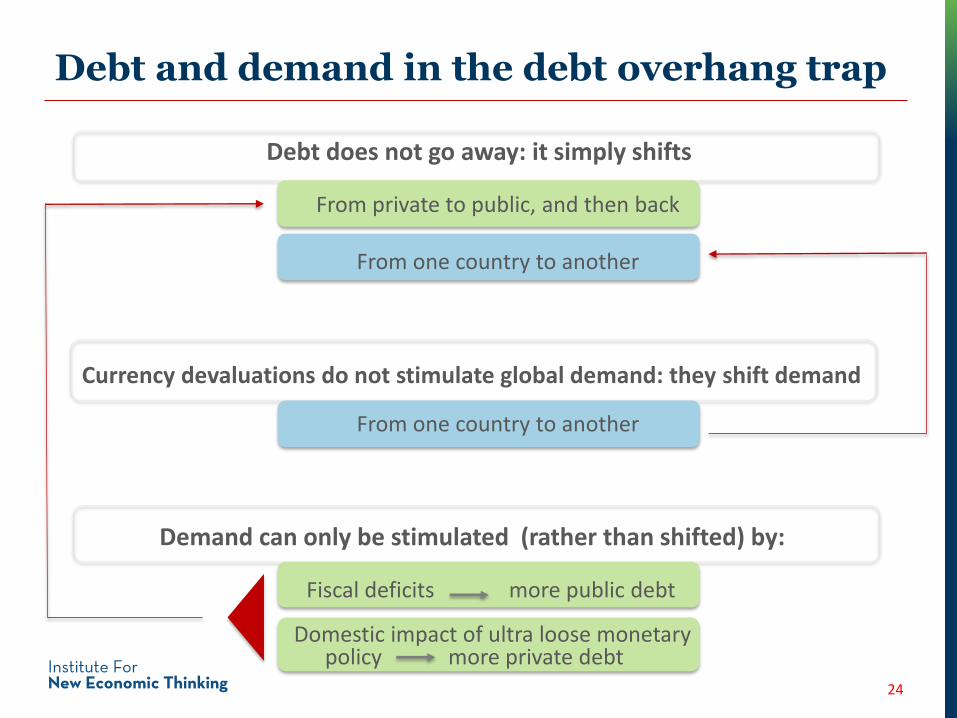

Debt and demand in the debt overhang trap

24

Domestic impact of ultra loose monetary policy more private debt

Debt does not go away: it simply shifts

Currency devaluations do not stimulate global demand: they shift demand

Demand can only be stimulated (rather than shifted) by:

From one country to another

Fiscal deficits more public debt

From private to public, and then back

From one country to another

Global debt excluding financials

Source: Geneva Report No 16 Deleveraging, What Deleveraging? ICMB / CEPR September 2014

100

120

140

160

180

200

220

240

260

280

01 02 03 04 05 06 07 08 09 10 11 12 13

Developed Markets

Emerging Markets

World

% o

f G

DP

25

26

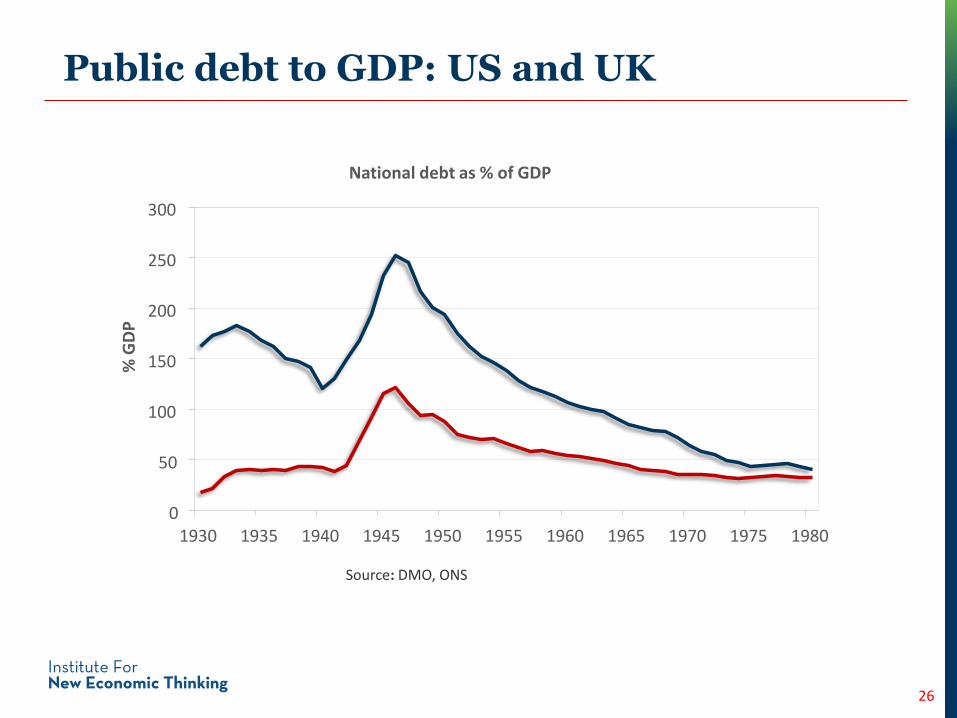

Public debt to GDP: US and UK

Source: DMO, ONS

National debt as % of GDP

0

50

100

150

200

250

300

1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980

% G

DP

Ensuring long-term Japan debt sustainability: IMF scenarios

27

Required cyclical changes in adjusted primary balance% of GDP

2010 2014 2020

Continuous surplus thereafter to reach

• 80% net debt• 200% gross debt

by 2030October 2014Fiscal Monitor

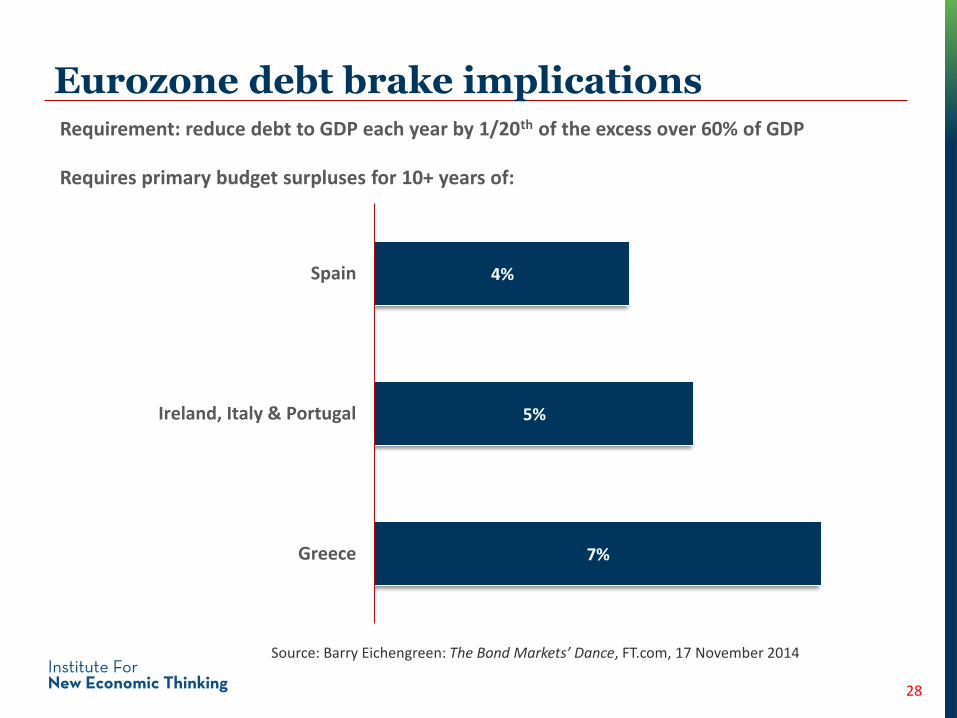

- 6.5 + 6.4

- 6.0 + 5.6

November 2010Fiscal Monitor

7%

5%

4%

Greece

Ireland, Italy & Portugal

Spain

28

Eurozone debt brake implications

Source: Barry Eichengreen: The Bond Markets’ Dance, FT.com, 17 November 2014

Requirement: reduce debt to GDP each year by 1/20th of the excess over 60% of GDP

Requires primary budget surpluses for 10+ years of:

Debt overhang: the unavoidable choice

29

Debt

Debt write-off,

default, restructuring

Debt erosion

via inflation, monetisation

Sustained slow

growth and low deflation

Stimulating yet

more credit

Debt overhang and deleveraging

Long-term secular trends

30

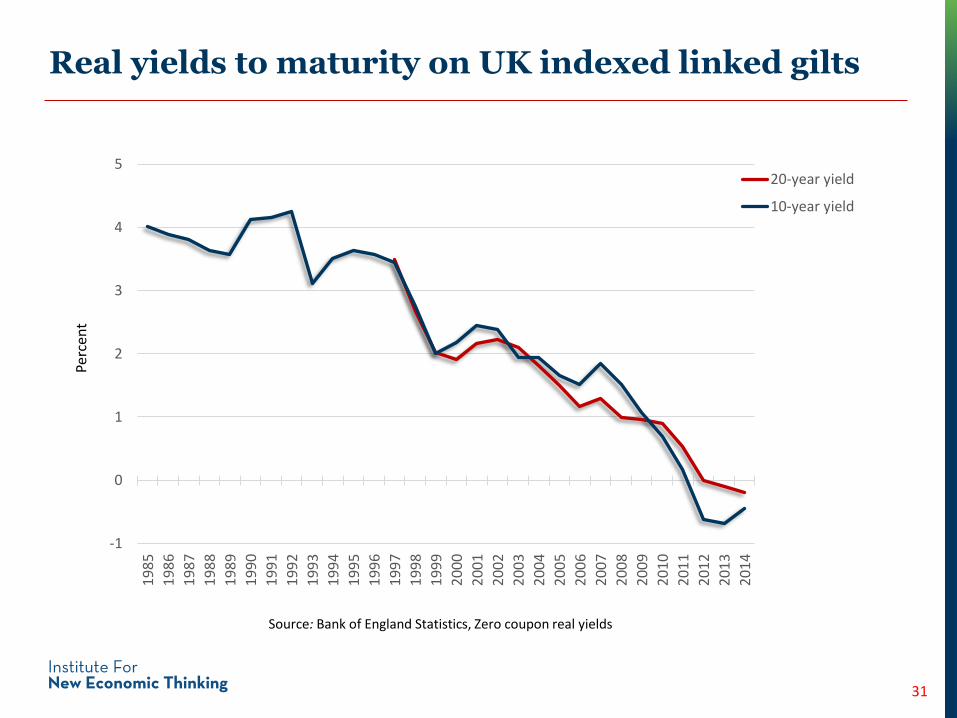

Real yields to maturity on UK indexed linked gilts

Source: Bank of England Statistics, Zero coupon real yields

31

Perc

ent

-1

0

1

2

3

4

51

98

5

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20-year yield

10-year yield

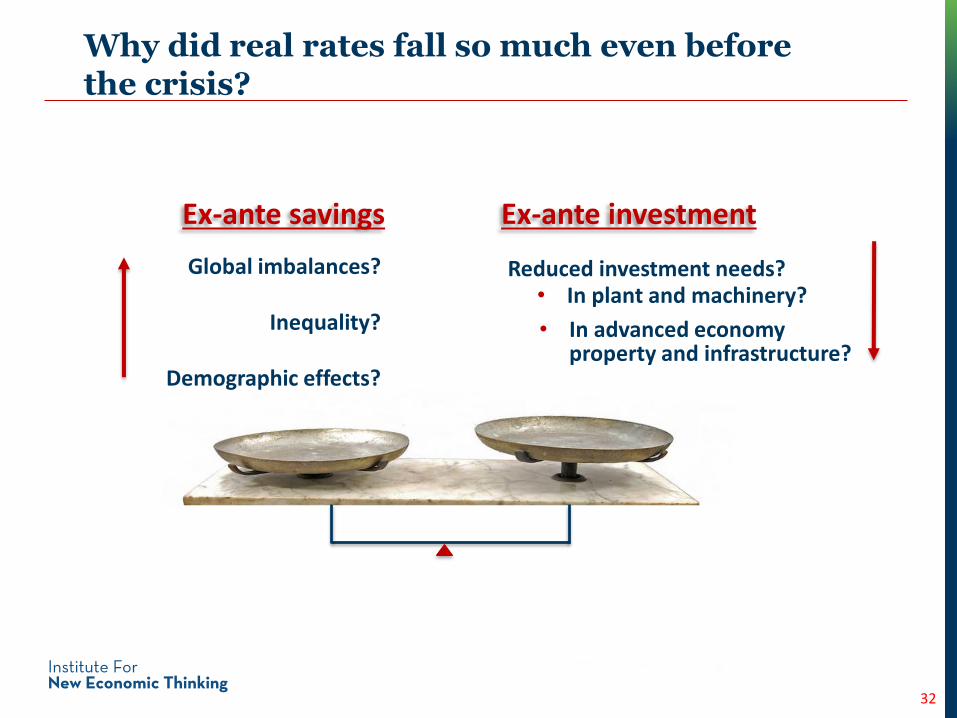

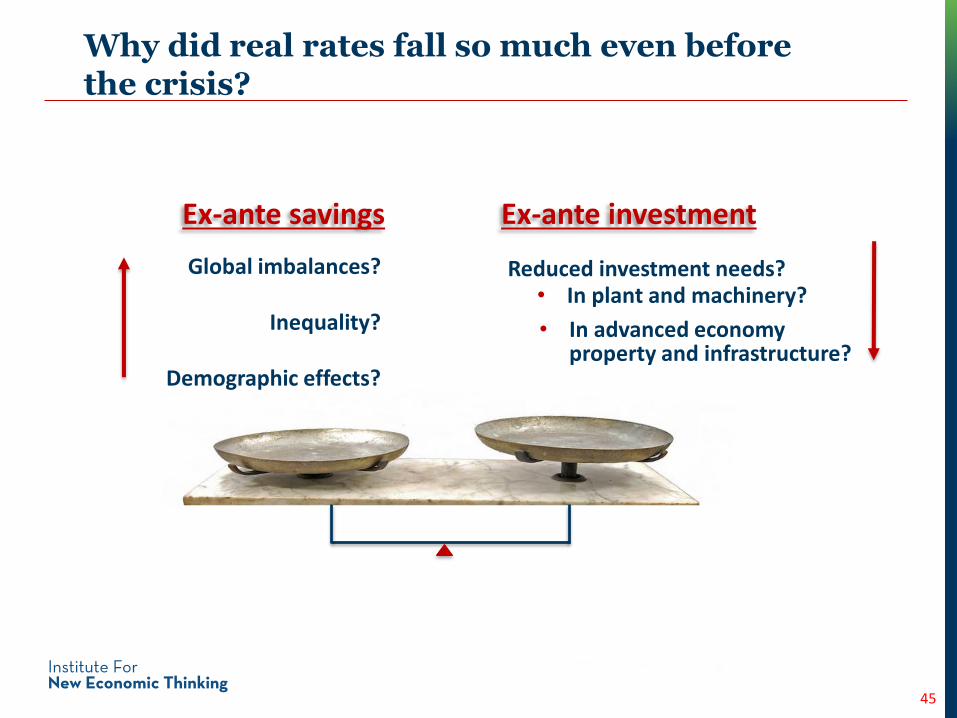

Why did real rates fall so much even before the crisis?

32

Reduced investment needs?• In plant and machinery?

Ex-ante savings Ex-ante investment

Global imbalances?

Inequality?

Demographic effects?

• In advanced economy property and infrastructure?

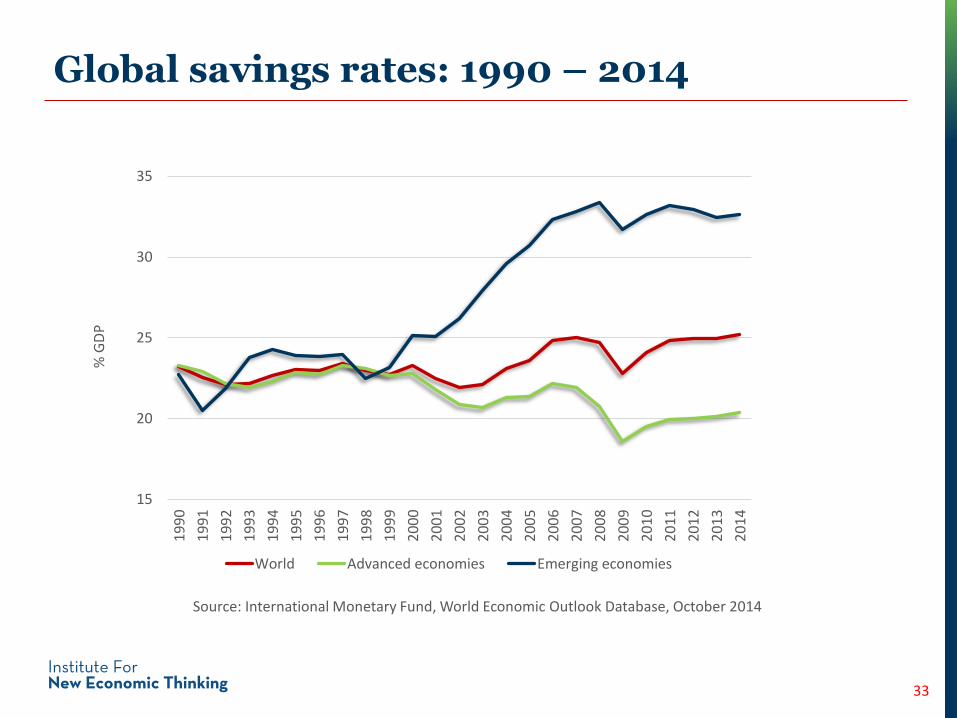

Global savings rates: 1990 – 2014

33

15

20

25

30

351

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

World Advanced economies Emerging economies

Source: International Monetary Fund, World Economic Outlook Database, October 2014

% G

DP

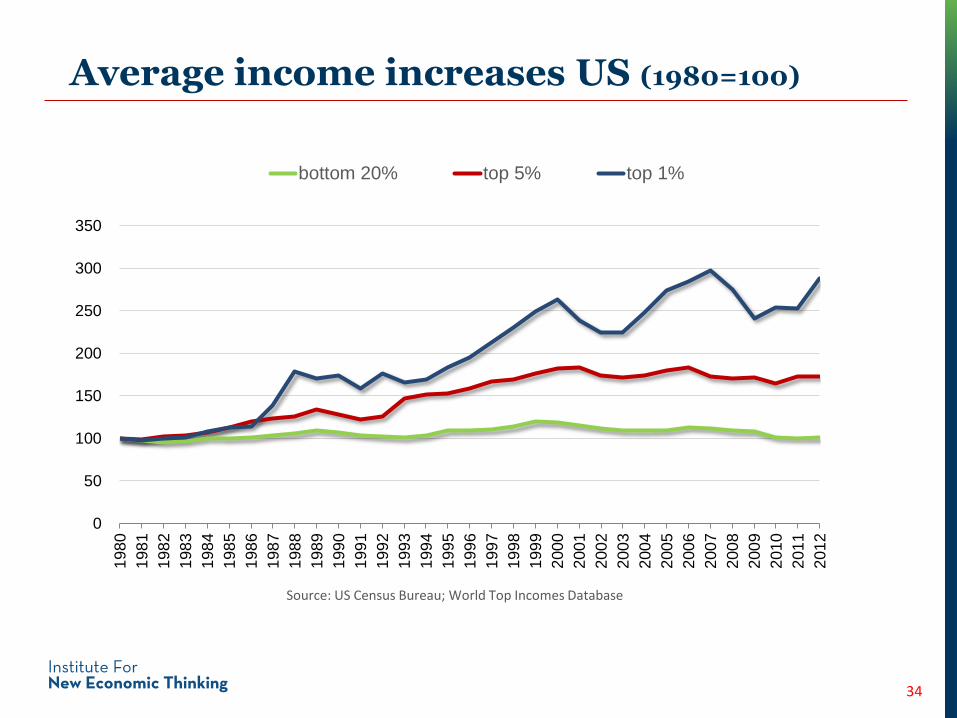

Average income increases US (1980=100)

0

50

100

150

200

250

300

350

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

bottom 20% top 5% top 1%

S

Source: US Census Bureau; World Top Incomes Database

34

Why did real rates fall so much even before the crisis?

35

Reduced investment needs?• In plant and machinery?

Ex-ante savings Ex-ante investment

Global imbalances?

Inequality?

Demographic effects?

• In advanced economy property and infrastructure?

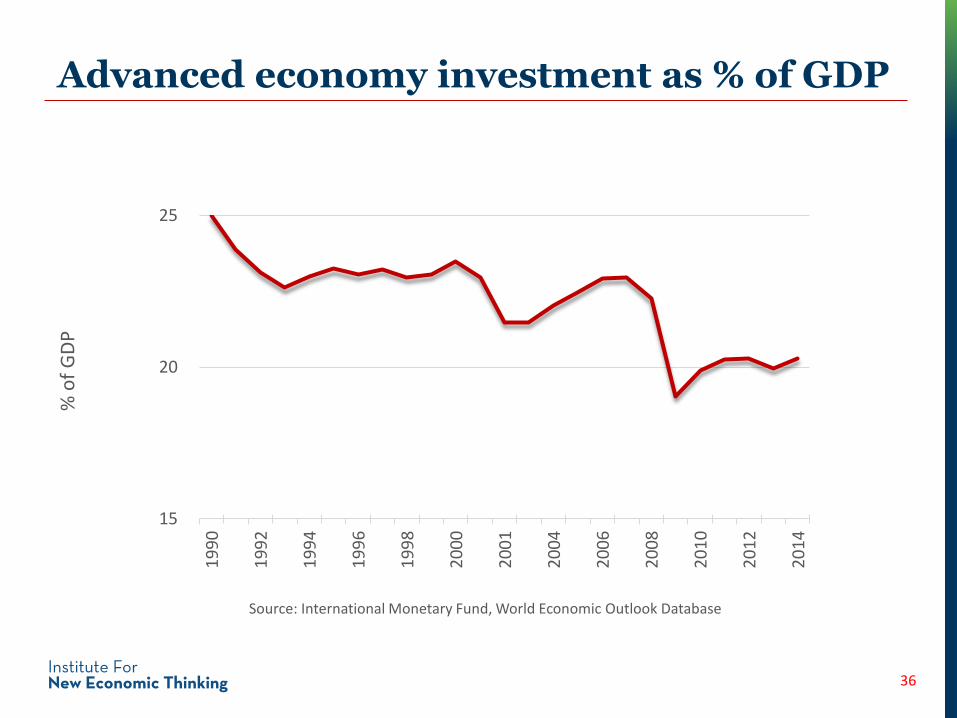

Advanced economy investment as % of GDP

36

15

20

251

99

0

19

92

19

94

19

96

19

98

20

00

20

01

20

04

20

06

20

08

20

10

20

12

20

14

% o

f G

DP

Source: International Monetary Fund, World Economic Outlook Database

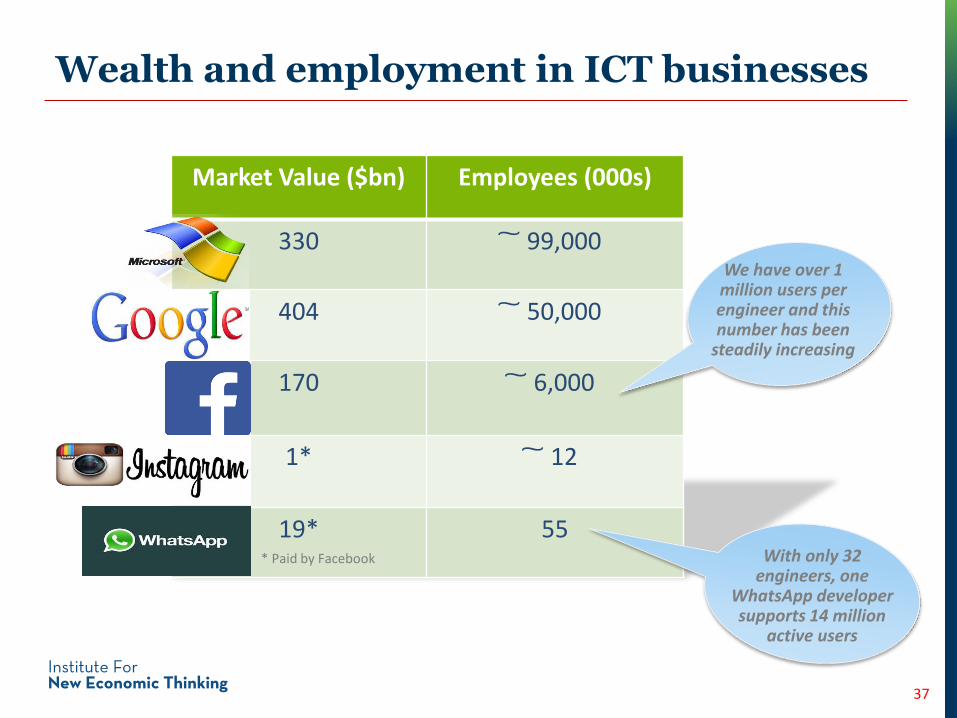

Wealth and employment in ICT businesses

Market Value ($bn) Employees (000s)

330 99,000

404 50,000

170 6,000

1* 12

19* 55

37

We have over 1 million users per engineer and this number has been

steadily increasing

* Paid by Facebook With only 32 engineers, one

WhatsApp developer supports 14 million

active users

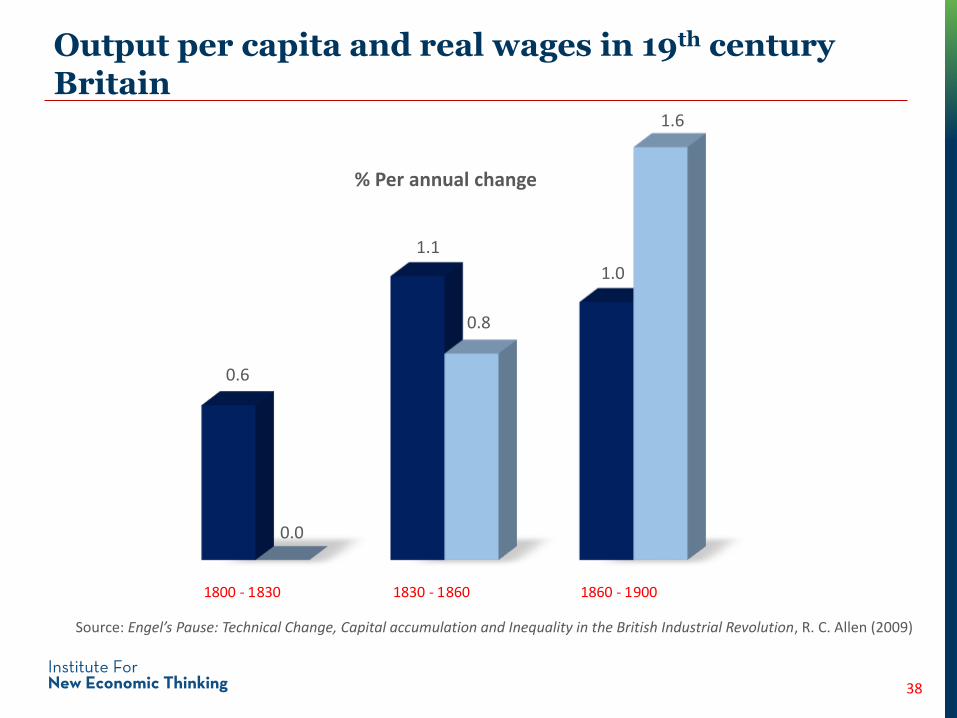

Output per capita and real wages in 19th century Britain

1800 - 1830 1830 - 1860 1860 - 1900

Source: Engel’s Pause: Technical Change, Capital accumulation and Inequality in the British Industrial Revolution, R. C. Allen (2009)

% Per annual change

0.6

0.0

1.1

1.6

1.0

0.8

38

Probability that computerisation will lead to job losses 2010 – 2030

OCCUPATION PROBABILITY

(1=certain)

Recreational Therapists 0.003

Personal Trainers 0.007

Firefighters 0.17

Economists 0.43

Machinists 0.65

Retail salesperson 0.92

Accountants & auditors 0.94

Telemarketers 0.99

Source: The Future of Employment: How Susceptible are Jobs to Computerisation? C. Frey and M. Osborne (2013)

39

US Jobs growth forecast, 2012 – 2022

40

20

65

21

21

18

24

32

30

22

30

19

90

1

2

3

4

5

6

7

8

9

10

19

26

Median annual wage ($000s)

Occupational categories by speed of job growth

Forecast job growth (000s)

1 Personal care aides 580

2 Registered nurses 527

3 Retail sales persons 435

4 Home health aides 424

5 Food preparation and serving aides 422

6 Nursing aides 312

7 Secretaries and administrative assistants

308

8 Customer services reps 299

9 Janitors and cleaners 280

10 Construction labourers 260

19 Maids and house keeping cleaners 183

26 Software developers, applications 140

Source: Bureau of Labor Statistics, www.bls.gov All sector average: 35

Growth in average wages and labour productivity

41

Real wage index

Labour productivity index

100

103

106

109

112

115

118

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Developed economies, 1999 – 2013

Source: Global Wage Report 2014/15, International Labour Organisation

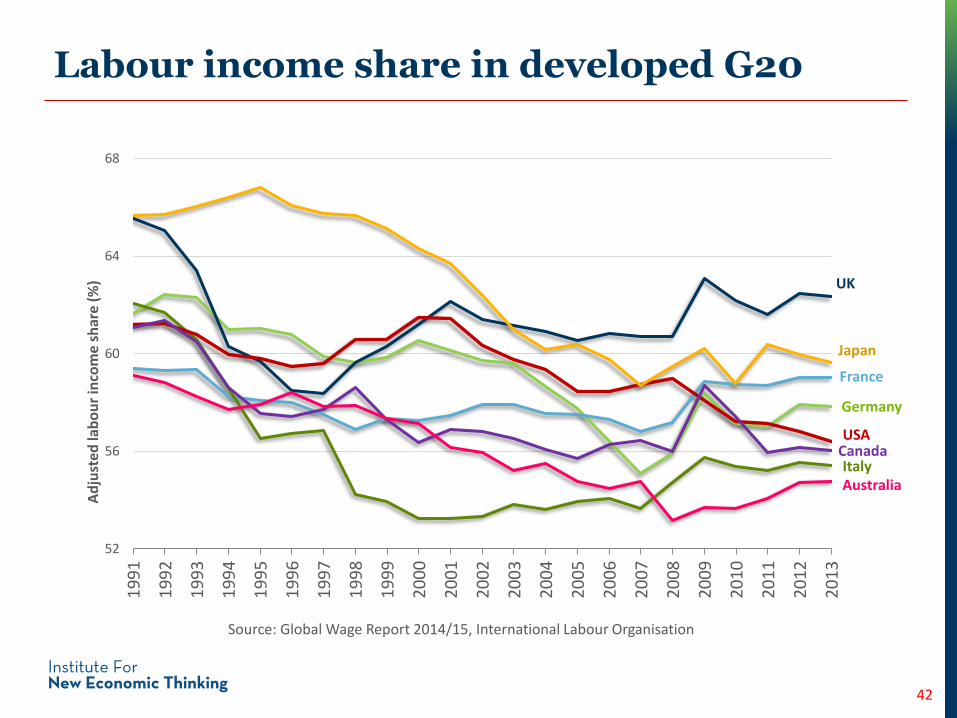

Labour income share in developed G20

42

Germany

France

Italy

UK

USA

Japan

Canada

Australia

52

56

60

64

68

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ad

just

ed la

bo

ur

inco

me

shar

e (%

)

Source: Global Wage Report 2014/15, International Labour Organisation

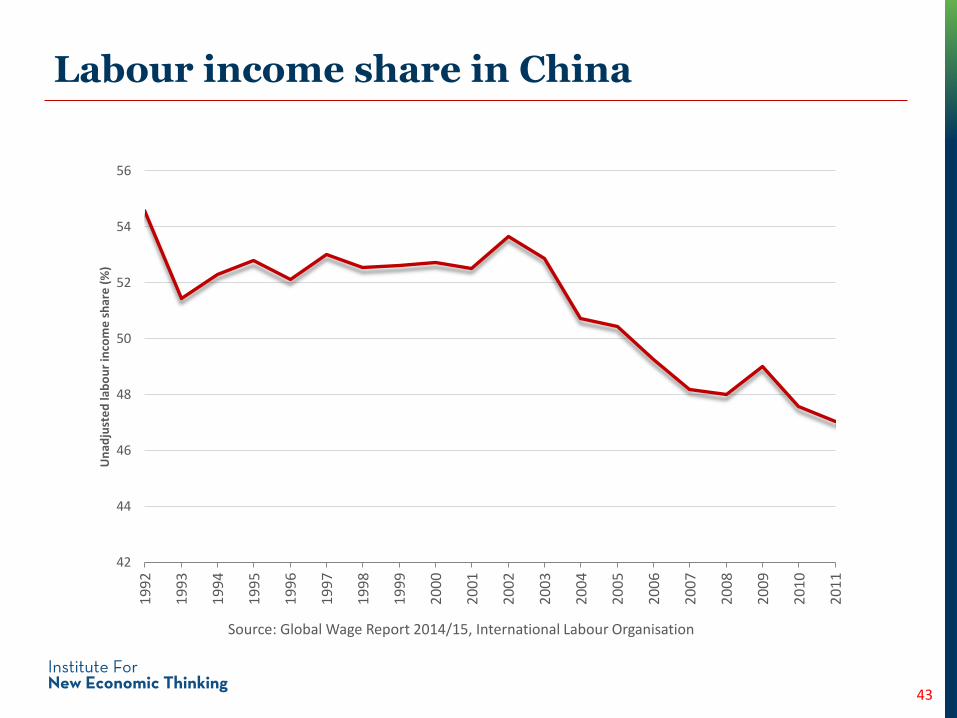

Labour income share in China

43

42

44

46

48

50

52

54

56

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Un

adju

ste

d la

bo

ur

inco

me

sh

are

(%

)

Source: Global Wage Report 2014/15, International Labour Organisation

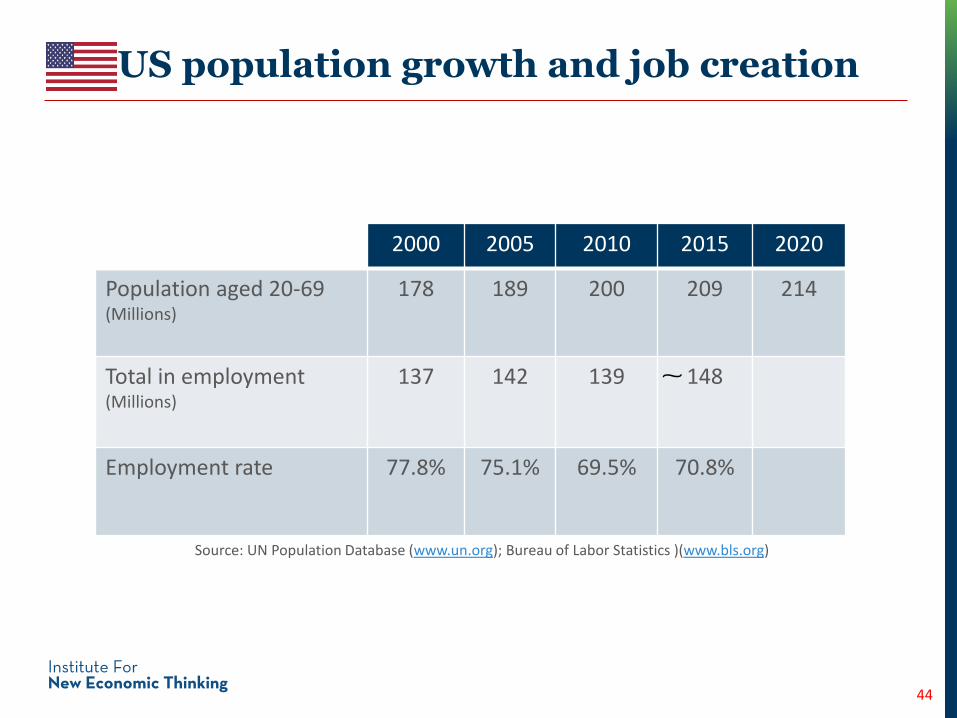

US population growth and job creation

44

2000 2005 2010 2015 2020

Population aged 20-69(Millions)

178 189 200 209 214

Total in employment(Millions)

137 142 139 148

Employment rate 77.8% 75.1% 69.5% 70.8%

Source: UN Population Database (www.un.org); Bureau of Labor Statistics )(www.bls.org)

Why did real rates fall so much even before the crisis?

45

Reduced investment needs?• In plant and machinery?

Ex-ante savings Ex-ante investment

Global imbalances?

Inequality?

Demographic effects?

• In advanced economy property and infrastructure?

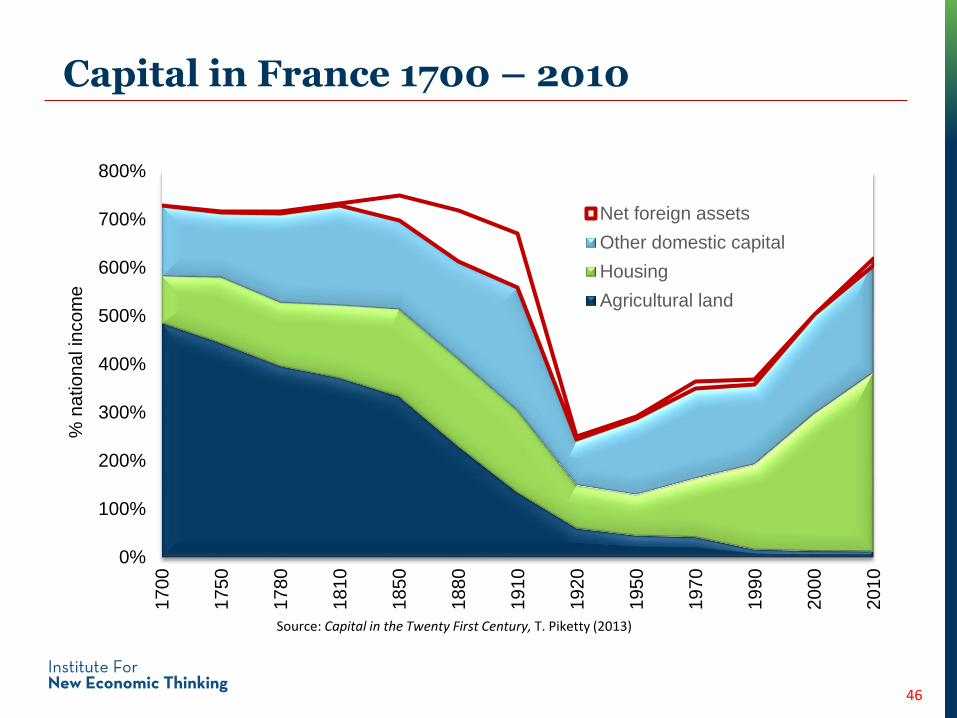

Capital in France 1700 – 2010

46

0%

100%

200%

300%

400%

500%

600%

700%

800%1700

1750

1780

1810

1850

1880

1910

1920

1950

1970

1990

2000

2010

% n

atio

na

l in

co

me

Net foreign assets

Other domestic capital

Housing

Agricultural land

Source: Capital in the Twenty First Century, T. Piketty (2013)

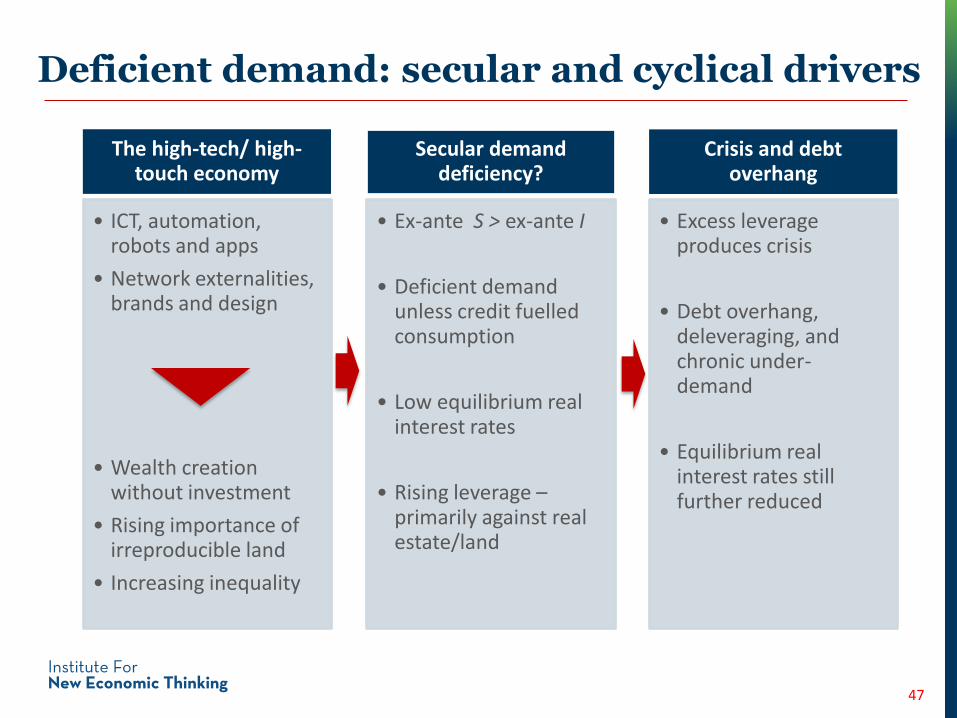

Deficient demand: secular and cyclical drivers

47

The high-tech/ high-touch economy

• ICT, automation, robots and apps

• Network externalities, brands and design

• Wealth creation without investment

• Rising importance of irreproducible land

• Increasing inequality

Secular demand deficiency?

• Ex-ante S ˃ ex-ante I

• Deficient demand unless credit fuelled consumption

• Low equilibrium real interest rates

• Rising leverage –primarily against real estate/land

Crisis and debt overhang

• Excess leverage produces crisis

• Debt overhang, deleveraging, and chronic under-demand

• Equilibrium real interest rates still further reduced

What will happen

48

No crisis, but big slowdown

The helicopter money end game: no big deal?

Playing with social and political fire

OK but unbalanced growth

Robust but not as good as hoped