debtfree digi spet 2012 thedci special edition

DESCRIPTION

Debtfree DIGI theDCI Special Edition. Special DCI content as well as all the latest news about debt review. The rise and fall of VDMS, Securitisation for dummies, Debt Vader and much, much moreTRANSCRIPT

www.debtfreedigi.co.za

DebtfreeSouth Africa’s debt counselling magazine

September 2012 Spring

Debt Counsellors and Consumers need to realise an important fact. The Debt Counselling industry has only one regulator: the National Credit Regulator. This important fact should be made known to all consumers and even to our attorneys and magistrates. If consumers or Debt Counsellors have problems with payment distribution agencies or credit providers they should talk to the National Credit Regulator. At this time there does not seem to be any mandate between the NCR and any other association or body to handle consumer, Debt Counsellor or Payment Distribution Agency issues.

The National Credit Regulator has a daunting task of regulating all aspects of the National Credit Act. You can imagine how vast a task that is. No wonder that they appreciate it greatly when consumers and Debt Counsellors bring their concerns to them so that they can find out what is happening in the current credit market. Consumers and Debt Counsellors find themselves dealing with market realities daily and so they should feel free to let the NCR know what is happening especially where they feel the NCA is being breached.

TheDCI has been invited to assist the Department of Trade and Industry in making

proposals for amendments to the National Credit Act. The last five years have given plenty of opportunities for the various national Courts to try and test different aspects of the National Credit Act. Now there is an opportunity for those who deal with different portions of the Act to have a say in areas they feel will benefit from slight changes.

After our first call for suggestions theDCI has already received over 300 different emails from Debt Counsellors in regard to proposed changes. This is great and will no doubt help the DTI immensely as they consider where amendments can be made to the Act.

Your voice is important and can make a difference. Lets work together to talk to the DTI and to the NCR about issues that face our industry.

United we stand.

We have ONE regulator

C O N T E N T S

5 Editors notes

7 News

12 DEBT VADER

18 The rise and fall of VDMS

22 Securitisation for dummies

28 Letter from a reader

Debt Review Software by

Bitech is recognised as the leading Debt Counsellor software system supplier.

Simplicity is rich in functionality and caters for all Debt Counsellor requirements e�ortlessly.

Simplicity is leading edge technology and Bitech stay at the forefront of development - we continue to lead the way!

The Simplicity system is fully integrated with Hyphen PDA, which provides you, the Debt Counsellor, with an uninterrupted and e�cient service with no manual intervention and in total control.

Some features of the Simplicity system are completely unique unique, amongst others is the ability to create customised legal documentation instantaneously.

Bitech prides itself on its after sales service and the support it provides to Debt Counsellors - this is as important as the excellence of the Simplicity product!

p d a

Hyphen Technology (Pty) Limited is a member of the FirstRand Group

Hyphen PDA is a division of Hyphen Technology (Pty) Limited, which is wholly-owned by the FirstRand Group - �nancial soundness is important when considering a PDA!

Hyphen PDA is at the top of its game and is unrivalled in the collections and payment space.

Hyphen PDA essentially operates with the use of banking systems (iSeries mainframe computers) and the PDA and Payments Engine are fully integrated - as a result you will seldom, if ever, query the status of your collections or payments.

The reports generated are everything a Debt Counsellor will need to manage the business - reporting is immediate, current and always available.

27(0)16 987 5004/27(0)16 987 5006/27(0)16 987 2369

Contact Bitech

www.bitechsystems.hypermart.net

27(0)11 303 0060 extension 2

Contact Hyphen

www.hyphen.co.za

Debt Review Software by

Bitech is recognised as the leading Debt Counsellor software system supplier.

Simplicity is rich in functionality and caters for all Debt Counsellor requirements e�ortlessly.

Simplicity is leading edge technology and Bitech stay at the forefront of development - we continue to lead the way!

The Simplicity system is fully integrated with Hyphen PDA, which provides you, the Debt Counsellor, with an uninterrupted and e�cient service with no manual intervention and in total control.

Some features of the Simplicity system are completely unique unique, amongst others is the ability to create customised legal documentation instantaneously.

Bitech prides itself on its after sales service and the support it provides to Debt Counsellors - this is as important as the excellence of the Simplicity product!

p d a

Hyphen Technology (Pty) Limited is a member of the FirstRand Group

Hyphen PDA is a division of Hyphen Technology (Pty) Limited, which is wholly-owned by the FirstRand Group - �nancial soundness is important when considering a PDA!

Hyphen PDA is at the top of its game and is unrivalled in the collections and payment space.

Hyphen PDA essentially operates with the use of banking systems (iSeries mainframe computers) and the PDA and Payments Engine are fully integrated - as a result you will seldom, if ever, query the status of your collections or payments.

The reports generated are everything a Debt Counsellor will need to manage the business - reporting is immediate, current and always available.

27(0)16 987 5004/27(0)16 987 5006/27(0)16 987 2369

Contact Bitech

www.bitechsystems.hypermart.net

27(0)11 303 0060 extension 2

Contact Hyphen

www.hyphen.co.za

Simplici ty

Spring has sprung! Summer is just around the corner. It is a great time of year as we push towards December and all that brings. The change of season gets us thinking about the fact that the end of the year is suddenly so much closer than we realised and that we better get ready to squeeze our winter bodies into our swimming costumes. I think mine must have shrunk in the wash or something! Well, if you are under debt review a diet (if that’s what you call just eating less) is a great way to cut down on the crazy raising food costs and exercise is a great form of entertainment that can be achieved for minimal costs. Prices are shooting up left, right and center; with fuel costs being a big factor and add to that issues in other parts of the world to do with wheat costs and it is a recipe for a very skinny December after all.

If however we put all that aside for a moment and think about what has been happening in SA with regard to debt review and the debt counselling industry there have been some interesting developments. The NCR have shown their teeth over the Voluntary Debt Mediation Solution (VDMS) which they decided was seemingly an unregulated form of debt review which undermines the statutory process that hundreds of thousands of South Africans are making use of. This issue you can

read more about the rise and fall of the VDMS system. More than that you can read about how the NCR have now withheld the carrot they were offering to the NDMA in the form of taking over the job of registering consumers under debt review with the various credit bureaus. It has not been a great month for the NDMA!

We feature articles from the Dark Sith Lord of debt review Debt Vader and legal opinions that will have you giggling but thinking about new ways of looking at things. It is great to see the regulator pushing credit providers to put their money where their mouth is and show increased support for the debt review process. Lets hope they take the advice to heart and that consumers under review will see increased co operation from their creditors. This would be a great weight off their backs ...now if only we could get the weight off our bellies we could actually hit the beach.

So keep up the good work and don’t lose momentum now. Start to plan for the end of the year right now and keep taking another step towards being debt free.

EDITOR’S NOTE

Debt review and distribution software.Proud Software provider to DC Partner, Payment Distribution Agency.

https://debtwisesolutions.co.za

Debt Wise Solutions

INDUSTRY CONSUMER

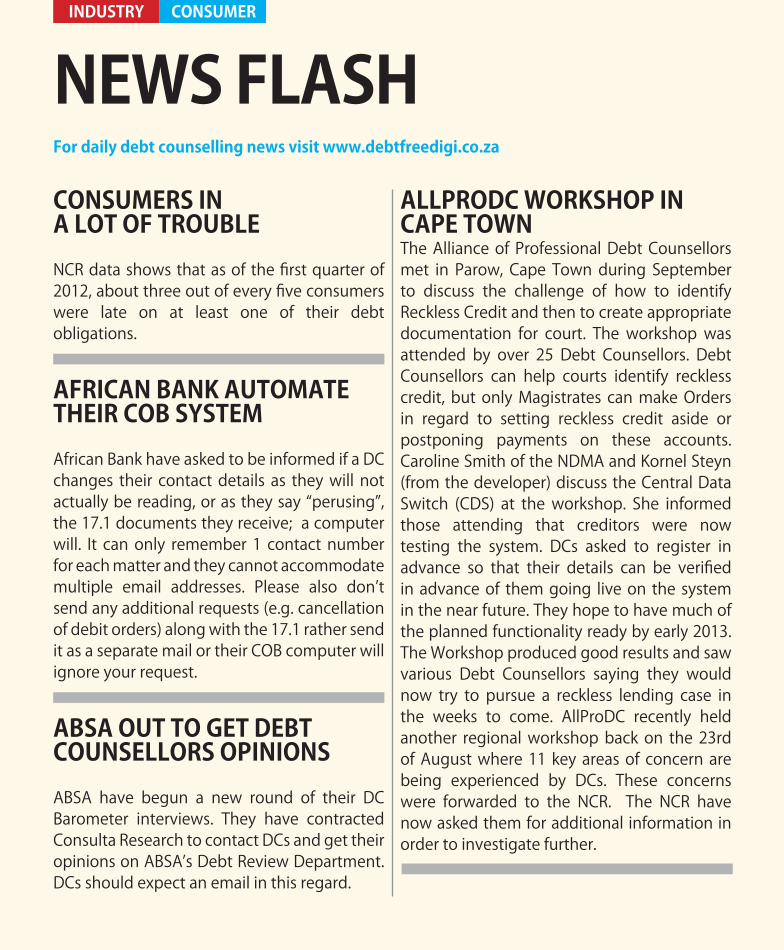

NEWS FLASHFor daily debt counselling news visit www.debtfreedigi.co.za

CONSUMERS IN A LOT OF TROUBLE

NCR data shows that as of the first quarter of 2012, about three out of every five consumers were late on at least one of their debt obligations.

ALLPRODC WORKSHOP IN CAPE TOWNThe Alliance of Professional Debt Counsellors met in Parow, Cape Town during September to discuss the challenge of how to identify Reckless Credit and then to create appropriate documentation for court. The workshop was attended by over 25 Debt Counsellors. Debt Counsellors can help courts identify reckless credit, but only Magistrates can make Orders in regard to setting reckless credit aside or postponing payments on these accounts. Caroline Smith of the NDMA and Kornel Steyn (from the developer) discuss the Central Data Switch (CDS) at the workshop. She informed those attending that creditors were now testing the system. DCs asked to register in advance so that their details can be verified in advance of them going live on the system in the near future. They hope to have much of the planned functionality ready by early 2013. The Workshop produced good results and saw various Debt Counsellors saying they would now try to pursue a reckless lending case in the weeks to come. AllProDC recently held another regional workshop back on the 23rd of August where 11 key areas of concern are being experienced by DCs. These concerns were forwarded to the NCR. The NCR have now asked them for additional information in order to investigate further.

AFRICAN BANK AUTOMATE THEIR COB SYSTEM

African Bank have asked to be informed if a DC changes their contact details as they will not actually be reading, or as they say “perusing”, the 17.1 documents they receive; a computer will. It can only remember 1 contact number for each matter and they cannot accommodate multiple email addresses. Please also don’t send any additional requests (e.g. cancellation of debit orders) along with the 17.1 rather send it as a separate mail or their COB computer will ignore your request.

ABSA OUT TO GET DEBT COUNSELLORS OPINIONS

ABSA have begun a new round of their DC Barometer interviews. They have contracted Consulta Research to contact DCs and get their opinions on ABSA’s Debt Review Department. DCs should expect an email in this regard.

NEWS CONT.

NCR AND VDMS

In their CIRCULAR No.06 of 2012 the NCR have informed the public that they are bringing the VDMS project to a halt. Here is an extract from the circular: ASSESSMENT FINDINGS ON VOLUNTARY DEBT MEDIATION SOLUTIONOur assessment has revealed that the implementation of the VDMS pilot would contravene the National Credit Act 34 of 2005 (“the Act”) and undermine statutory debt counselling. The VDMS pilot is in essence a masked form of debt counselling with attributes similar in nature to statutory debt counselling. It also weakens the protection afforded by the Act to consumers and undermines the spirit and purpose of the Act in respect of debt counselling.” The NCR has instructed the National Debt Mediation Association (NDMA) not to implement the VDMS pilot and also issued instructional letters to participating debt counsellors and Payment Distribution Agencies (PDAs) to withdraw participation with immediate effect. For more on this see our article this month called The Rise and Fall of VDMS.

NCR TO KEEP WWW.NCRDEBTHELP.CO.ZA RUNNING

The NCR had recently indicated that it would be handing over the function of informing the credit bureaus of consumers debt review status to the NDMA. They have now changed their minds and decided to keep the troubled web system running (at least for now). The NCR have said: The National Credit Regulator wishes to advise all debt counsellors and credit bureaus that it has no intention of handing over the NCR Debt Help System to any other party, including the NDMA. The NCR will continue to operate the said system and provide its function on a continuous basis to debt counsellors and credit bureaus until further notice. Debt Counsellors are requested to ensure that all debt review applications are registered and updated on the NCR Debt Help System.

DCASA CEO RESIGNS

DCASA ‘s CEO Wikus Olivier has resigned. The Debt Counsellors Association of South Africa’s Chief Executive Officer has handed in his resignation. He has told Debtfree DIGI that he will now be able “to follow other interests”. Wikus has been instrumental in bringing DCASA’s web and social presence up to date over the last few months. DCASA members will miss Wikus’ constant presence on the DCASA forum and at meetings. Ironically he has only just finished traveling the country to various regional DCASA meetings to introduce himself.Wikus will be missed and Debtfree wish him the best in his new venture.

NCA CHANGES - THE DTI WANT HELP

The DTI have approached theDCI and both Debt Counsellor associations (AllProDC and DCASA) for suggestions in regard to sections of the National Credit Act which might need some attention in possible amendments to the Act. theDCI report having received over 300 emails from DCs within the first week of calling for suggestions.

NEXT PAGE 18

RISE AND FALL OF VDMS

NEWS CONT.

DCASA CONFERENCE SUCCESS

August saw DCASA host their annual conference for Debt Counsellors and Creditors about the debt review industry. The theme was “tomorrow-today”. It was described by those attending as a “success” and “well put together”. Various speakers discussed current industry developments and plans for amendments to the NCA. A last minute change saw the NDMA presentation on VDMS moved to the morning session. No questions were taken in regard to the VDMS pilot project which the NCR has subsequently stopped. Many members were sad to hear of DCASA CEO Wikus’ resignation, but over all, the conference went off without a hitch. With nearly 100 extra attendees, it was a great success indeed.

ABSA’S SECTION 129 LETTER STATS

A Section 129 letter is a: ‘we are about to sue you, get help or pay up’ letter. During the period January to May 2012 ABSA dispatched some 5 195 section 129 letters in respect of unsecured loans. In the same period 19 555 Section 129 letters were sent out to consumers in respect of default on credit card debt. During 2012 ABSA’s computerised system has to date generated between 10 000 and 15 000 Section 129 letters per month in respect of asset and vehicle finance. In total that is around 40 000 Section 129 letters or 6500 letters a month.

NEXT PAGE 12

DEBT VADER

NEXT PAGE 18

RISE AND FALL OF VDMS

As the Debt Counselling industry itself has gone thorough changes so to have those companies who offer debt review related services. With many companies coming and going over the years, consumers are looking for stable, long lasting brands that can meet their needs.

In 2012 the DCM Group and its subsidiary brands have gone through a metamorphosis, the outcome of which is a fresh new look and feel. New branding accompanies this new perspective.

While in the past DCM has offered services under a variety of brands it seems that DCM’s acquisition of several different brands resulted in an organisation that was presenting a myriad images and messages to the various target markets which it services. As a result, some consumers where not aware of the range of services which DCM could offer or were confused about who owned these brands.

The new branding brings all these various brands under one recognisable parent company, namely DCM. The individual brands and logos have now been incorporated into the DCM Group of Companies with DCM Group as the lead brand.

This means that DCM Consumer Assist, DCM Care Premier and DCM Corporate are now sub-brands; and that the NPDA is being the endorsement brand for the whole Group.

When describing the ongoing changes in the industry and the performance of the various DCM brands Anton Viljoen CEO of the DCM Group says: “ We look forward to many more exciting times in the years ahead...the DCM Group will grow from strength to strength”

DCM are moving forward and are now positioned for even greater growth and success.

The DCM Group get a fresh new look

www.dcmgroup.co.za/brands

debtstar

Debt VaderVirtual arrears

CONSUMER

As the Debt Counselling industry evolves, it becomes more and more evident that credit providers treat Debt Re-arrangement Court Orders as inconsequential, even going so far as to ignore the court orders by refusing to update their internal computer systems to reflect the restructured debt as per the Debt Re-arrangement Court Order, and placing themselves intentionally in contempt of a valid and enforceable court order.

Thus the immergence of the “virtual arrears” which are arrears accumulated before the application for Debt Review and during the debt re-arrangement process. It is accepted that when a consumer enters the Debt Review process, any arrears that may have existed on their accounts is capitalised. The consumers are then expected to pay in respect of the Debt Re-arrangement Court Order, a specific amount of money to their Credit Providers, over a specific time and at a specific interest rate, all of which is documented and confirmed in the court order itself.

The unwillingness of the Credit Providers to change their internal computer systems to accommodate the new arrangement reflected on the Court Order, results in a deficit between the original contractual installment and the debt review installment (virtual arrears). This

deficit expresses itself as an arrears amount which accumulates during the existence of the Debt Review and upon which the bank charges interest (which they are not entitled to), thus creating debt out of “thin air”.

In the instance where a consumer wishes to withdraw from the Debt Review process, the Credit Providers request a withdrawal form (17.4) issued by a Debt Counsellor before they will entertain any request by the consumer. Once the withdrawal form has been issued, the consumer no longer enjoys the protection of the NCA and this places them in an unenviable bargaining position.

Some of the banks make ludicrous demands on consumers, they will demand that 50% of this “virtual arrears” be paid upfront, and that the other 50% is to be paid over 6 - 9 months, while the consumer continues to pay the normal contractual installment, thus making it impossible for a consumer to comply with the arrangement or to successfully exit Debt Review. The result being that the consumer could lose their property.

These “virtual arrears” seems to be how the banks calculate which consumer they are going to be harassing into higher installments (paid outside of the Debt Re-arrangement

Court Order) or withdrawing from the Debt Review process. This harassment takes the form of constant sms’s, letters threatening the consumer with enforcement action and even premature terminations, or attempts to rescind the Debt Re-arrangement Court Orders. The higher the “virtual arrears” become the more high risk that consumer becomes and the more pressure the banks will place on the consumer, in some instances going so far as to summons consumers.

From my understanding of the process, the Court Order varies the original contractual agreement between the parties. My reasoning is that in accordance with the original contract variation clauses, consensus has been reached between the parties and it is reduced to writing. When the Credit Provider receives the Debt Review proposal or the court application documents he has an opportunity to oppose and/or negotiate, thus creating consensus between the parties. If the Court Order is taken without opposition then the consensus on the part of the Credit Provider is tacit because of his omission to act. As long as the consumer pays in terms of the court order, there should be no arrears. Only when a consumer defaults in terms of the court order, then the credit providers may terminate the debt review but they are not entitled to the “ virtual arrears” which accrued during the debt review or the interest thereon.

Once a credit provider cancels a debt re-arrangement court order and proceeds with enforcement, he effectively cancels the entire

contract between the parties and thus cannot sue for foreclosure balances based on the terms of the same contract he just cancelled. This will require a new application as it arises from a new cause of action. Another concern is that if a debt re-arrangement court order has been granted, how does an employee of a credit provider get to make the unilateral decision that the consumer is in default (as no notice to the consumer is required in terms of S88 of the NCA) and proceed with enforcement action without first rescinding the debt re-arrangement court order.

At present, consumers who default are left in the situation where the banks demand unreasonable installments in respect of these arrears and the tacit underlying threat is that if the consumer does not pay these monies, the bank will proceed with enforcement action and execute against their property.

Once again the result has been that consumers who apply successfully for Debt Review are held to a stricter set of rules by the credit providers, and they victimize and capitalise on these consumers who are already in financial dire straits.

Mail your comments to Debt Vader on [email protected]

You can get insurance designed specifically for consumers under debt review?

Some credit insurance products will not pay out because you are under debt review?

You can get insurance for up to R1 000 000.00?

You can pay as little as R1.62 per R1000 insured?

This is the only product specially designed to cover your debt while you are under debt review?

This product is only available through your Debt Counsellor

DID U KNOW THAT

CONSUMER

DEBT COUNSELLOR

DID U KNOW THAT Your clients can save thousands of Rands over time by making use of the Debt Counselling Industry Group Scheme?

You can help your consumers get out of debt faster and still remain covered as required by their creditors?

Have the courts ever asked you to prove the clients insurance as stipulated on their budget ?

Now you will automatically get a copy of your clients policy as well as know their monthly payment status from the insurer directly. The creditors will not be able to argue risk of death or risk of no cover because for the first time you will know the truth first hand.

Email [email protected] for further information

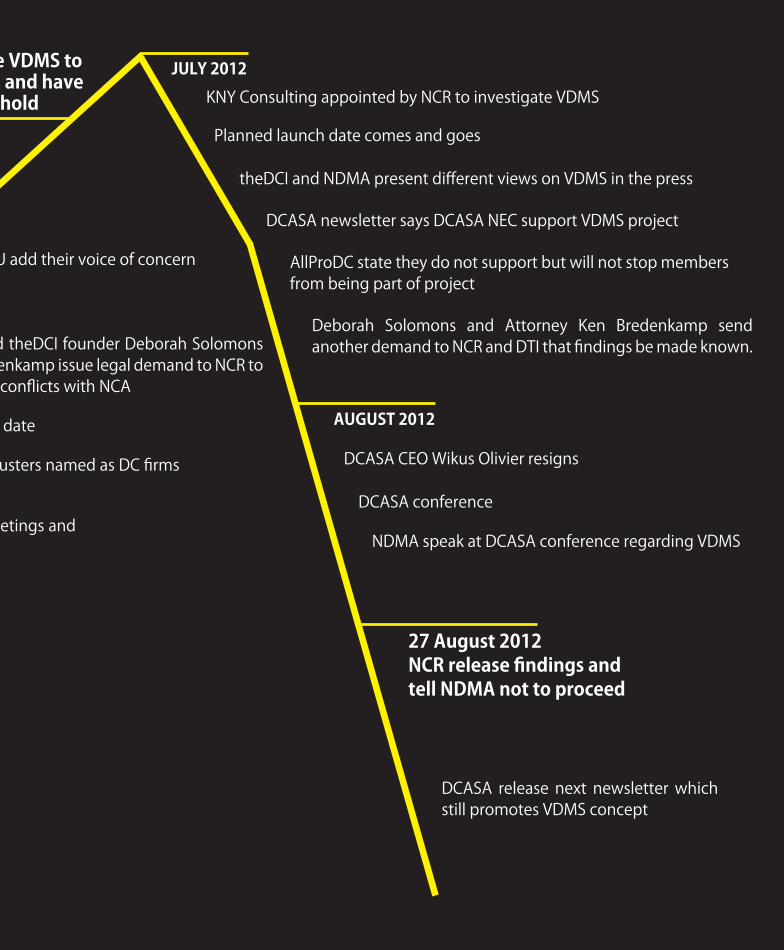

Recently the Banking Association of South Africa and the NDMA (a credit provider representative body) began to promote an alternative to debt review called VDMS. The system offered voluntary debt mediation rather than statutory debt review and debt restructuring through the courts. For several months the NDMA developed and promoted the project as a cheaper, easier alternative to debt review via the courts. At the last minute the National Credit Regulator told the NDMA to stop work on the pilot project.

The rise and fall of VDMS

MAY 2012

theDCI pushes NDMA for more info

COSATU add their voice of concern

NCR issue circular 04 of 2012 re VDMS to say they are now investigating and have asked NDMA to put project on hold

Debt Counsellor and theDCI founder Deborah Solomons and Attorney K Bredenkamp issue legal demand to NCR to investigate possible conflicts with NCA

AllProDC discuss VDMS at regional meetings

NDMA circular on VDMS issued

02 July 2012 named as starting date

Octogen, Consumer Assist and Debt Busters named as DC firms to be part of pilot project

DCASA members discuss VDMS at regional meetings and DCASA ask NDMA for more info

JUNE 2012

NDMA state that DCs will be chosen by creditors to assess & propose repayment plans

NDMA state that DCRS is to be used

KNY Consulting appointed by NCR to investigate VDMS

COSATU add their voice of concern

DCASA CEO Wikus Olivier resigns

NCR issue circular 04 of 2012 re VDMS to say they are now investigating and have asked NDMA to put project on hold

Debt Counsellor and theDCI founder Deborah Solomons and Attorney K Bredenkamp issue legal demand to NCR to investigate possible conflicts with NCA

Deborah Solomons and Attorney Ken Bredenkamp send another demand to NCR and DTI that findings be made known.

Planned launch date comes and goes

theDCI and NDMA present different views on VDMS in the press

DCASA newsletter says DCASA NEC support VDMS project

AllProDC state they do not support but will not stop members from being part of project

02 July 2012 named as starting date

Octogen, Consumer Assist and Debt Busters named as DC firms to be part of pilot project

DCASA members discuss VDMS at regional meetings and DCASA ask NDMA for more info

JULY 2012

DCASA release next newsletter which still promotes VDMS concept

27 August 2012NCR release findings and tell NDMA not to proceed

NDMA speak at DCASA conference regarding VDMS

DCASA conference

AUGUST 2012

The NCR have said that since the Debt Counsellors would get work from the credit providers and payment from them, this would be a conflict of interest and in breach of the National Credit Act. The PDAs are also not allowed to handle money for any other purpose than that allowed by the NCR namely: debt restructuring via debt review.VDMS would not be regulated by anyone other than the creditors themselves and would have no judicial oversight. there would be little legal protection for consumers if things went wrong. The NCR published a circular in which it stated: “...implementation of the VDMS pilot would contravene the National Credit Act 34 of 2005 (“the Act”) and undermine statutory debt counselling. The VDMS pilot is in essence a masked form of debt counselling with attributes similar in nature to statutory debt counselling. It also weakens the protection afforded by the Act to consumers and undermines the spirit and purpose of the Act in respect of debt counselling. The NCR has instructed the National Debt Mediation Association (NDMA) not to implement the VDMS pilot...” One NCR employee put it this way: “This is not an invitation to the [NDMA] to redesign the process - we are putting an end to it and will...make sure it has stopped”.

Debt Counsellors would be used to make proposals to creditors.

Debt Counsellor software called DCRS would be used to make proposals.

Creditors would allow for reduced debt repayments over longer periods.

Money would be distributed via the various debt review Payment Distribution Agencies.

See our dedicated VDMS webpage http://debtfreedigi.co.za/voluntary-debt-mediation/

How VDMS was similar to debt review

What the problems were

Securitisation

DUMMIESFOR

Recently you might have heard this term

“securitisation” being thrown around.

What does it mean?

to find out read on page 22

Recently you might have heard this term “securitisation” being thrown around. What does it mean?

What a pretty house

Mr Consumer goes to Big Bank to take a bond for his new house. The house is valued at R500 000.00 (+ - average bond amount in South Africa at the moment).

Big Bank grant Mr Consumer a bond and he purchases the house.

Yay! I own a house.

Mr Consumer moves into his new house.

During this time Big Bank lumps Mr Consumer’s bond together with a few other credit accounts and sells them to SPV.

SPV buy various accounts and give Big Bank money. They are actually buying the future earnings of these various accounts. But just in case something goes wrong SVP insure the payments to these accounts. SVP now sell these “securities” on the various local and international bond markets and stock exchanges. Investors buy them and hope to make profit over time.

A few months later Mr Consumer hits a rough patch and can no longer make his full bond repayments.

Oh, Oh!

Big Bank now start to call and email and sms Mr Consumer.

Securitisation FOR DUMMIES

Pay up!

Mr Consumer cant pay up, so Big Bank send him a Section 129 letter and then a summons.Next, they get a judgment against Mr. Consumer and get permission to sell the asset on auction. (But are they actually allowed to?)

The house gets sold on auction for R200 000.00

SPV now go to their insurance company and claim on their insurance policy. The investors get their money.

Yay, more money!

Big Bank now approach Mr Consumer from time to time over the next 30 years demand that Mr Consumer pay them the R300 000.00 shortfall (plus interest) as per the court judgment.

Yay, more money!

Homeless :-(

Fast Facts:

Securitisation has been around in SA for nearly 20 years. BASA say that they are securitising around R30 Billion each month. Consumer rights organisations like the NewERA want banks to be more transparent and tell consumers who it is that actually owns their bond. They also ask if Big Bank has sold Mr Consumer’s bond to someone else, can Big Bank sue the consumer and then sell the house on auction and still come back and collect on the shortfall? In law this issue is called “Locus Standi”

For more information, feel free to visit www.thebigcase.co.zawww.newera.org.za

Debt is a world-wide phenomenon, glorified by banks in the form of credit cards, personal loans, mortgage bonds and the like. Using media marketing as a launching pad for idealistic representations of the financial freedom that an overdraft, credit card or loan can bring, the banks publicise an “acquire now, pay later” mentality. Perhaps some may find that description a little disparaging, but the fact remains that we find ourselves in a world wide credit crisis. As Mark Twain said: “A banker is a fellow who lends you his umbrella when the sun is shining, but wants it back the minute it starts to rain”.To continue on the same tack, not only is the banker going to want his umbrella back, but he knows when the rain will start and how many people will be caught in the storm. Through experience, statistics, projections and financial analysis, the banks can accurately predict figures as to non-payers and defaulters, on an annual basis. This is how they assign a budget in the form of legal costs necessary to regain ownership of that metaphorical umbrella, be it a house, car, lounge suite or television.

It is at this point that the banks no longer ask: “How can we help you?”, but rather: “How can we help ourselves?” And the promise of: “Today, tomorrow, together” seems to fall away just as tomorrow begins to dawn, leaving the consumer to wonder why that family in the advert promoting personal loans looked so damn happy. That must have been the “today”, when they were enjoying their credit funded holiday, preceding the “tomorrow” when petrol prices rocketed and inflation leapt forward, making those interest drenched repayments incredibly difficult to maintain.I certainly believe that necessary debt is manageable. However, unforeseen and unpredictable financial burdens and occurrences such as job loss, retrenchments, death of a bread winner can thrust one into an unmanageable debt trap.This is the stage at which the bank’s seeming “nemesis”, the Debt Counsellor, steps in to offer that help and to see the consumer through that tomorrow, to weather the storm and salvage the umbrella. But what if the Debt Counsellor and the bank enjoyed a more harmonious

LETTER FROM A READER

www.newera.org.za

relationship? What if, instead of opposition to debt review applications the bank, upon receipt of the notice of motion, or even prior thereto were to approach the Debt Counsellor and quickly agree on a revised payment structure? What if the Debt Counsellor were to take the debt review order by consent on the first set down date at court?If the banks were to reform their infrastructure to link the foreclosure, repossession and debt collection departments with the Debt Review department, that for one would be a step in the right direction. I say this because whilst employed as an attorney at a bank panel firm, doing foreclosures and vehicle repossessions, I would often receive appearances to defend, the basis of the defence being that “the consumer is under Debt Review”. The bank would then instruct us to withdraw and tender costs. Had the foreclosure department been in closer communication with the debt review department, this would not have happened, and there would have been no cost implications.Building on this first step, if the banks had to revise their debt recovery budget and instead of instructing attorneys to foreclose or repossess in every instance, direct communication channels between the internal debt review department and Debt Counsellors could be established to facilitate a speedy, almost automatic debt

review process at a fraction of the cost of litigating.In order to establish the feasibility of such a proposal, an enormous study with many variables will have to be conducted: How many debtors are to be handed over to attorneys? How many will qualify for debt review? What percentage reduction on a monthly repayment amount as an average across the board, considering the length of the repayment period will be reasonably viable? What is the sustainable lifespan of this approach? Etc etc.The time and money required would no doubt be significant, but if the result has the potential to, in the long run, save the banks time, save them money and put them first, which will in turn put the consumers and Debt Counsellors first as well, why should it not be done?The big question is If this is a great Idea then how do we get the banks on board?

Keegan O’[email protected] 021 462 1663 FAX 0866 504 550303 Millborough, 70A Upper Mill Street,Vreedehoek, Cape Town, 8000

DEBT COUNSELLING

AA Debt Counselling CentreAnthea JohannesNCRDC531Tel: +27 (0) 21 982 0522Cell: +27 (0) 84 402 7032

Alan Watts NCRDC 962NCR registered Debt Counsellor Tel: 084 4448439 Fax: 086 6501954alan@active-debt-counselling.co.zawww.active-debt-counselling.co.za

Central SA Debt Counsellors082 950 7806Fax: 086 563 1621

Consumer AssistJohann VermeulenTel: 0861 628 628

Credit Matters021 431 [email protected]

CS Debt CounsellingBernidene Smith NCRDC 764057 352 4115/352 5000Welkom - Free state

Darran [email protected]

Debtbusters0861 663 328 (NO DEBT)

Debt BudgetTel: 021 824 8885

Debt Solve Debt CounsellorsOffice: 033 397 0945

DEBTINCNCRDC’s 1071, 1188, 1189.Tel: (022) 713-2021Fax: (022) 713-2028Share Call: 0861 20 21 20E-mail: [email protected]: www.debtinclusive.co.zaSMS: HELP to 35075

DebtSafe0861 100 999

Debt SeriousWe are serious about debtVida Scheepers NCRDC1792Po box 394, Garsfontein, Pretoria 0042Fax no: 086 553 [email protected]

Debt RehabColleen Van Wyk(BCom, LLB)Debt Counsellor NCRDC2619Tel: 083 290 0848Tel: 011 740 7374Fax: 086 716 9694Website: http://debtrehab.co.za

Debt eezyYour Debt Solution made EasyAshley Carstens NCRDC858 Tel: 021 839 2809 Fax: 083 512 4160 / 086 665 9125 Email: [email protected]: www.thedci.co.za

Debt RescueNeil RoetsNCR DC 474Cell: 083 644 7406Tel: 0861 800 009Fax: 086 523 0617E-mail: [email protected]

Debt Management & Counseling Services“The greatest glory in livinglies not in never falling,but in rising every time we fall.” - Nelson MandelaDerry Burge NCRDC108140 Irene Avenue, La Concorde,Somerset West, 7130 Tel: 021 855 5997 Cell: 074 177 5375 Fax: 021 855 1195 or 0865413200E-mail: [email protected]

Durban Debt Counselling ServicesSuite 112, 1st floor Union Club Building353 Sm ith StreetDurban, 4001Tel: 031 301-7893Fax: 031 [email protected]

SERVICE DIRECTORY

Debt Counselling South AfricaCape Town BranchTel: 021 919 66 94Rod De WittNCRDC831Visit: www.debtcounsellingsa.co.za Fincorp debt Counsellors ccCecilia Zwarts [email protected]

Holistic Debt [email protected]

Helpdesk Debt CounsellorsAllan HoffmanTel: 0861 000 754

Help-U-Debt (Vaal Triangle) WanineTel: 082 445 3967

Help-U-Debt (Potchefstroom)Madra083 390 3275

Help-U-Debt (Parys)Marilouise082 920 6249

Help-U-Debt (Vanderbijlpark)Herma083 320 8303

Incentive Debt Counselling“Paving the way to a Debt Free Tommorrow”Darran Manikam NCRDC704Tel: (031) 409 9379Fax: (031) 409 1327Cell: 0845898286Branches: Phoenix and Shallcross

Indigo debt counsellors CC

Tel: 087 808 9734 Fax: 086 580 8675 [email protected]

MG Consulting Strand - Helderberg AreaTelkom : 021 853 4537 Mobile Phone: 082 450 7459Fax Number: 0866 220 690E-Mail: [email protected]

NDA Debt CounsellorsYour Trusted Debt CounsellorsGary Williams (NCRDC 143)Tel: 034 315 3880 Fax: 086 612 [email protected] www.ndad.co.za

Rihanyo Debt Counselling(012) 804 50 57

Think Green Debt CounsellingSandi [email protected] : 012 991 6638Cell : 082 460 7800Fax : 086 219 2615

U-Win Debt CounsellorsCoreli Roos - NCR DC 509Aliwal North, Burgersdorp, Bethulie, GariepDam, Smithfield, SpringfonteinCell:079 626 [email protected]

Zuné Coetzer Debt CounsellorsNCRDC 159924 van der Stel Street, Dan PienaarBloemfonteinTel: 051-4364515Fax: 086 5870 845Email: [email protected]

SERVICE DIRECTORYThe best angle to approach debt is the Triangle

Caledon - Western CapeContact Person: Yolande8 Hoop Street, 7230 [email protected]: 028 212 2537

Ceres - Western CapeLeyll str 61, 683 [email protected]: 023 312 1292Fax: 023 312 2119

Worcester - Western Cape71 Porter Street 6850 Longitude: 19.44305Latitude: [email protected]: 0233420576Fax: 086656801

Bloemfontein - Free State94 Zastron, 9301 BloemfonteinContact Person: [email protected]: +27 51 448 2828Fax: +27 51 447 9481

Viljoenskroon - Free State35 Denyssen Street, 7230Contact Person: Johann [email protected]: +27 56 343 0352Fax: +27 56 343 035

Welkom – Free State329 Stateway, 9460 WelkomContact Person: Susan RouxEmail: [email protected]: +27 57 352 6117Fax: +27 57-352 2355

DEBT RESTRUCTURING SERVICES

BORDER REGION:

DRS BEACON BAYJohan PretoriusCell: 082 324 4038Office: 043 748 1139

DRS BUFFALO CITYHerman MariasCell: 082 378 3743Office: 043 7210652

DRS KING WILLIAMS TOWNHerman MaraisCell: 082 378 3743Email: [email protected]

DRS CRADOCKOffice: 043 721 0652

DRS QUEENSTOWNHerman Marais Cell: 082 378 3743 Email: [email protected]

DRS MTHATHAHerman Marais Cell: 082 378 3743 Email: [email protected]

EASTERN CAPE:

DRS ALBANYOffice: 041 373 9693Email: [email protected]

DRS ALGOAMarius WeyersCell: 083 497 3219Email: [email protected]

DRS BOND CHOICEAndrea AtkinsonOffice: 041 393 7000Email: [email protected]

DRS CENTRAL EXPRESSDerryn FishOffice: 041 373 9693586 2020Email: [email protected]

DRS DESPATCHIsabe LandmanCell: 072 337 3328Office: 041 933 1189Email: [email protected] HUMANSDORPMorne SteynCell: 083 298 8182Office: 042 291 0135Email: [email protected]

DRS NKONKOBE (Fort Beaufort)Bernadine von der DeckenCell: 083 2859289Office: 046 645 1898Email: [email protected]

DRS KIRKWOODKeith Le RouxCell: 073 207 1675Office: 041 451 0474Email: [email protected]

DRS PORT ELIZABETHDerryn FishCell: 084 515 6135Office: 041 453 8961Email: [email protected]

DRS SIDWELL EXPRESSKeith Le RouxCell: 073 207 1675Office: 041 451 0474Email: [email protected]

DRS SOMMERSET EASTLuther De BruynCell: 082 568 2970Office: 042 243 1107Email: [email protected]

DRS UTENHAGELynn LindoorCell: 083 7174 183Email: [email protected]

FREESTATE:

DRS GOLDFIELDS (Welkom)Irvin Billy (Derryn Fish)Cell: 072 114 4427Office: 081 319 0083Email: [email protected]

DRS MANGAUNGAmanda JohnsonOffice: 041 373 9693Email: [email protected]

DRS FOREISTATA EXPRESS (Bloemfontein)Derryn FishOffice: 041 373 9693Email: [email protected]

DRS SOUTH FREESTATENelmarie De langeCell: 079 236 3615Office: 053 591 0734Email: [email protected]

GARDEN ROUTE:

DRS DE AARVeronique Louw (Derryn Fish)Cell: 076 382 2020Office: 053 631 1189

SERVICE DIRECTORY

Email: [email protected] DRS GEORGEFrancois Van ZylCell: 079 522 1930Office: 044 874 2820Email: [email protected] EDEN (Hartenbos)Bruno MertschTel: 042 291 1083/4Email: [email protected]

GAUTENG:

DRS CENTURION EXPRESSAmanda JohnonOffice: 041 373 9693Email: [email protected]

DRS LYNNWOODJunique JuliusOffice: 012 807 4339Email: [email protected]

DRS PRETORIA EXPRESSBen VermeulenCell: 082 442 8654Office: 012 331 2145Email: [email protected]

DRS PRETORIA NOORDOffice: 041 373 9693Email: [email protected]

DRS ROODEPOORT EXPRESSDerryn FishOffice: 041 373 9693Email: [email protected]

DRS RUSTENBURG Amanda JohnsonOffice: 041 373 9693Email: [email protected]

KWA ZULU NATAL:

DRS GREYVILLEVyas JuggernathCell: 083 206 0300Office: 031 309 8716Email: [email protected]

DRS KOKSTAD Melanie LouwrensCell: 083 269 0424Office: 039 727 1430Email: [email protected]

DRS MORNINGSIDE DURBANErica Mtshali (Amanda Johnson)Cell: 076 578 8660 Office: 031 301 5990email [email protected]

DRS PHOENIXVyas JuggernathCell: 083 206 0300Office: 031 309 8716Email: [email protected]

DRS PIETERMARITZBURGSanele ZuluCell: 083 543 3487Office: 033 394 8319Email: [email protected]

WESTERN CAPE:

DRS BELLVILLEPatricia BekkerOffice: 021 948 8523 / 4Email: [email protected]

DRS DIAMONDClive PalmerOffice: 021 421 8563Email: [email protected]

DRS TYGERBERGCraig LakeyCell: 082 627 0957Office: 021 945 4062Email: [email protected]

DRS WEST COASTMarius CoetzeeCell: 082 978 4407Office: 022 713 3766Email [email protected]

DRS SALDANHAMarius CoetzeeOffice: 022 713 3766Email: [email protected]

DRS SOLUTIONSChristelle de VilliersCell: 084 586 5600Email: [email protected]

SERVICE DIRECTORY

SERVICE DIRECTORYSUPPORT SERVICES

Staff Line Ndizani Executive RecruitmentCell no: 083 3028163Direct Line: (011) 468 - 2150E- Mail: [email protected]

Information resources & serviceswww.thedci.co.za

DesigntimesSouth Africa’s creative resourcewww.designtimes.co.za

TRAINING

Compuscan Academy 0861 51 41 31www.compuscanacademy.co.za

You & Your MoneyWestern Cape: NCR Debt Counsellor Training: For a Cutting Edge Course with practical input contact: You & Your MoneyDawn [email protected]: 072 1769789(021) 761 3287

FINANCIAL

ABSA Customer Debt Repair Line0861 005 901

Credit Ombudsman0861 662837

Experian011 799-3400 [email protected]

Eric StresoFinancial PlannerB Juris LL B CFP MBATel: 0833273358Fax: 086 612 7912

Fair Debt0829019788 or [email protected]

PACFIN Financial Solutions Head OfficeTel: +27 11 9757445Fax: 086536878336 Van Riebeeck roadKempton Park [email protected] Carlo BuildingNo 8 VoortrekkerstreetKempton Park 1619

Kempton ParkContact: Reyno CoetzeeTel: +27 11 3945363Fax: 0866048002Cell: +27 73 [email protected] / GermistonContact: Armand PosthumusTel: +27 11 8921911Fax: 0865620378

NelspruitContact: Ann BakerTel: +27 13 7415559Fax: 0880 1374 15559Cell: +27 82 [email protected]

SpringsContact: Wynand MclachlanTel: +27 11 8113728Fax: +27 11 8113728Cell: +27 83 2754014/[email protected]

Gooseberry Business AdvisoryTel: 012 644 0589

NedbankDebt Rehabilitation & Recoveries Services0860 109 279

STD BankDebt review HelplineTelephone: 0861 111 402 TransUnion0861 482 482

ThinkmoneyFinancial comparison websiteContact: Gareth MountainTel: 079 0996 798www.thinkmoney.co.za

WIZARD Vereeniging Making Mortgage MagicWanine SmitTel:+27 16 454 1132Fax:+27 86 686 3678 Cell:+27 82 445 3967 www.wizard.za.com

FINANCIAL PLANNING Eric StresoFinancial PlannerB Juris LL B CFP MBATel: 0833273358Fax: 086 612 7912

LEGAL

Karen van Staden Tel: 012 998 9117 / 012 993 2132Fax: 086 721 6467 / 086 662 1153Email: [email protected]@hauptearle.co.zawww.hauptearle.co.za

LUCID AttorneysTel: 011 880 1100Fax: 011 880 1101Email: [email protected]/attorney

O’Connell & AssociatesAttorneys at LawKeegan O’[email protected] 021 462 1663Fax 0866 504 550303 Millborough, 70A Upper Mill Street, Vreedehoek, Cape Town,8000

Prinsloo & AssociatesAttorneys and conveyancersNanika Prinsloo Farm Bergamot, Paarl 7620P O Box 6199, Paarl 762014 Laing Street, Barrydale 6750Cell: 072-8558-106Fax: [email protected]

RM Brown and Associates 601 Pier House, 13 -17 Heerengracht, Cape TownDocex 138 Cape Town t: 021 431 9127, f: 021 425 0875 e: [email protected]

Scheepers AttorneysGerhard [email protected]

Agiliti CCColleen Van Wyk(BCom, LLB)Tel: 083 290 0848Tel: 011 740 7374Fax: 086 716 9694Website: http://agiliti.co.za

CREDIT BUREAUS

Compuscan 0861 514 131www.compuscan.co.za

Computer Profile Bureau0861 28 7328www.c-p-b.co.zaExperianwww.experian.co.zaBusiness- 0861 63 60 70 Consumer- 0861 10 5665

Micro Lenders Credit Bureau 0861 28 7328 www.mlcb.co.za

TransUnion 0861 886 466www.transunion.co.za

XDS 0860 937 000 www.xds.co.za

SERVICE DIRECTORY

Is it time to expand your Debt Counselling practice?

Do you need specialist Attorneys with a national footprint?

Do you need expert advice on how to protect your practice and your clients?

Are you informed about recent statutory and legal developments within the industry?

Attorneys servicing individual needs

Pretoria: +27(0)12 998 9117 www.hauptearle.co.za Nelspruit: +27 (0)13 752 7084

If you want to subscribe, advertise or be listed in our directory please contact us! [email protected]

Dont miss out on a single

issue!

http://debtfreedigi.co.za/sample-page/

Did you miss last months issue?