decoding the indas impact for indian companies the indas impact for indian companies 1 ... across...

TRANSCRIPT

Decoding the IndAS Impact for Indian Companies

Q1 Reporting Under the New IFRS Converged Framework

1Decoding the IndAS Impact for Indian Companies

Foreword

The prescribed listed companies in India have started reporting under the new Indian Accounting Standards (IndAS) from the current financial year (2016-17). IndAS are the IFRS converged finan-cial reporting standards and will have to be followed by all the listed companies and certain private companies going forward, in a phased manner. Listed companies with net worth of more than INR 500Cr have reported their Quarter 1 (Q1) results for 30 June 2016, under the new standards.

We at Protiviti, have followed the transition closely and analysed the impact of this significant change on most of the sectors. As part of our study, we have analysed the Q1 IndAS results of almost 125 companies, across all major sectors and attempted to decode the impact, in a simplified manner. The study includes selected companies that have declared the Q1 results under IndAS, up to 16 August 2016 and is based on publically available information. The last date for submission of Q1 results has been extended to 14 September 2016 by, The Securities & Exchange Board of India (SEBI).

The Q1 results reported by the companies are as per the prescribed format issued by SEBI, which requires companies to provide GAAP reconcilliation only of Profit after Tax (PAT) for the compara-tive quarter i.e., quarter ended 30 June 2015. As such, most companies have not provided GAAP reconcilliation, as at the transition date (1 April 2015) and some companies (approx. 40% of the companies selected) have included a PAT reconcilliation for the full year ended 31 March 2016 (comparative year).

In view of the above, our study and analysis is primarily based on the PAT reconcilliation reported by the companies, for the first quarter comparative period ended 30 June 2015. There could be material adjustments made to the equity/reserves at the transition date i.e. 1 April 2015, which could not be analysed in our study, due to inadequate number of companies providing the transi-tion date equity reconcilliation.

Considering that the number of companies that have reported under the new regime are only a very small percentage of the total companies that are yet to transition, we hope that the study will provide insights to the remaining companies on the transition impact, relevant to their business.

We have also included a section at the end of the study to enable companies to carry out an initial self-assessment of their preparedness, for the significant transition.

Vishal SethManaging Director and LeaderFinancial Reporting and Transaction Advisory

2 Decoding the IndAS Impact for Indian Companies

Index

1. Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2. Decoding the Impact on Various Sectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

– Automotive . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

– Energy, metals and mining . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

– Information technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

– Infrastructure and real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

– Manufacturing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

– Media and entertainment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

– Pharmaceutical and biotechnology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

– Retail and consumer goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

– Telecommunications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

3. Decoding the Major GAAP Adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

– Adjustments to fixed assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

– Consolidation related adjustments, including adjustments to past business combinations . . . . 16

– Share based payments and employee benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

– Adjustments to carrying value of financial instruments . . . . . . . . . . . . . . . . . . . . . . . . 18

– Derivatives and hedge accounting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

– Service concession arrangements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

– Intangible assets and goodwill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

– Lease related adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

– Revenue recognition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

– Adjustments related to foreign exchange gain or loss . . . . . . . . . . . . . . . . . . . . . . . . . 21

– Deferred taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

– Transition date exemptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4. Closing Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

5. Is Your Company Ready for the Transition? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

6. Appendix A: IndAS Preparedness Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

7. Appendix B: List of Companies Included in the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

8. About Protiviti . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3Decoding the IndAS Impact for Indian Companies

1. Executive Summary

As Indian companies declare the results for the first quarter of the 2016-17 financial year, under the new IndAS regime (IFRS converged accounting standards in India), we at Protiviti have analysed the impact of adopting IndAS by these companies. Our analysis has been carried on a sample of almost 125 companies, across all the major sectors and industries, except for the banking and financial service industry (BFSI), for which the transition shall commence from financial year 2018-19 onwards. This study has been performed based on the analysis of the quarterly results reported by the listed compa-nies, with the net worth of more than INR 500Cr (US$75mn).

The overall impact of GAAP adjustments made on the profit after tax (PAT) for 30 June 2015 is approximately INR 20bn (US$ 300mn) decrease in PAT (net of debit and credit adjustments of INR 57bn and INR 37bn respectively). The total absolute value of the GAAP adjustments made by the selected companies, ignoring debit or credit adjustments in 30 June 2015 quarter is approximately INR 94bn (US$ 1.5bn).

40% of the companies that are included in the study have provided a profit (PAT) reconcilliation, for the comparative financial year ended 31 March 2016. The total impact of adjustments made by these companies is of INR 8bn, increase in PAT (net of INR 121 bn and INR 113 bn credit and debit adjustments respectively).

Our analysis covers 26 of the 41 eligible Nifty 50 companies and 74% of the total companies included in our study are large cap and mid cap companies. 9 of the Nifty 50 companies represent the BFSI sector which is not required to transition to IndAS until financial year 2018-19.

Although, companies have reported the quarter 1 results under the IndAS framework, they will have time until 31 March 2017 to re-look at the transition adjustments, in light of any change in the regulation/s that take place before 31 March 2017, which will be the first annual reporting period under IndAS. For example, the ongoing amendments/clarifications to the recommendation by Central Board of Direct Taxes (CBDT), on the treatment of Minimum Alternative Tax (MAT) for the adjustments to retained earnings, could result in additional companies opting for the fair valuation exemption with respect to property, plant and equipment.

4 Decoding the IndAS Impact for Indian Companies

Highlights of selected high value adjustments made by individual companies include:

Nature of adjustment/s Magnitude of the impact (in INR)Company’s

sector

Change in the Functional Currency

3 bn adjustment recognised in the income statement for the quarter ended 30 June 2015 and 9.5bn adjustment recognised in the income statement for 31 March 2016 comparative year.

Oil&Gas

Fair value adjustment on transition date of company's fixed assets on opting for the deemed cost exemption

450bn adjustment to the reserves as at 31 March’16. The adjustment was net of increase in the value of land and reduction in value of some producing assets.

Oil&Gas

Restatement of past business combination/s with a reversal of goodwill amortisation

210bn adjustment made to the reserves as at 31 March 2016 with adjustment to profit/s for 30 June’15 quarter and 31 March 2016 financial year of 7bn and 27 bn respectively.

Telecom

Change in accounting policy on capitalisation of expenditure

A company changed it's accounting policy on capitalisation of exploration expenditure from full cost method to successful effort method.

Impact of 395bn adjustment to reserves for 31 March 2016 with some impact on profits for quarter ended 30 June’15 and comparative year ended 31 March 2016.

Oil&Gas

Change in accounting policy on depletion and amortisation of oil producing assets

12bn adjustment to the profits for the financial year ended 31 March 2016 and 800mn adjustment to profit for the quarter 30 June 2015.

Oil&Gas, Mining

Adjustment/s to the carrying value of fixed assets

A power company has increased the carrying value of it's fixed assets (reason undisclosed) with additional depreciation impact recognised.

Impact of 10bn adjustment to the profit for the quarter ended 30 June 2015.

Power

a. Sectoral split of companies: Our sample covered prescribed companies across all major sectors. In case of the Aviation sector, most of the companies are covered in phase 2 of the transition. BFSI companies shall start the transition from financial year 2018-19 onwards.

For further analysis on each of the sectors, refer to section 2 of our study.

7%Retail & Personal Care

15%Pharmaceuticals& Biotechnology

4%Media& Entertainment

8%Information Technology

30%Manufacturing

4%Telecommunication

7%Infrastructure

& Realty

13%Energy, Metals

& Mining

12%Automotive

Sector Split (%)

Refer to Appendix B for the complete list of companies covered by our study.

5Decoding the IndAS Impact for Indian Companies

b. Number of adjustments made by companies in the respective sectors: On this parameter, companies in manufacturing and information technology sectors had the maximum number of accounting adjustments, followed by the telecommunications, mining/metals and energy sectors. On an average, more than 50% of the companies have made more than 10 adjustments to the reported profits, for the quarter ended 30 June 2015.

15Retail &Personal Care

13Pharmaceuticals& Biotechnology

10Media& Entertainment

17Information Technology

22Manufacturing

10Infrastructure & Realty

18Energy, Metals

& Mining

12Automotive

13Telecommunication

Number of Adjustments

c. Major accounting adjustments made by companies: Almost all companies have made adjust-ments with respect to fair valuation of financial instruments, employee benefits and deferred taxes. Significant number of companies have made adjustments for consolidation, accounting for deriva-tives/embedded derivatives, restatement of past business combinations, revenue recognition and fixed assets. Adjustments related to intangible assets are primarily on account of restatement of past business combinations, as per IndAS.

15Lease related adjustments

21Revenue recognition

20Consolidation adjustments

83Impact on financial

instruments

17Derivatives andembedded derivatives

12Business combinations

12Intangible assets

83Tax expense

(including deferred tax)

85Employee benefits

19PPE and depreciation

Top 10 Adjustments (% of Companies)

6 Decoding the IndAS Impact for Indian Companies

Detail analysis on the key adjustments is discussed in sections 2 and 3 or our study.

d. Snapshot of the impact of the accounting adjustments: The following graph provides a split of the GAAP adjustments made by the companies. The impact (if INR 94bn) is in absolute value (ignoring the impact of debit or credit adjustments). Of the total adjustments made to the June 2015 PAT, more than 50% of the adjustments are on account of fair valuation of financial instru-ments, consolidation and fixed assets. 35% of the total adjustments represent restatement of past business combinations, forex gains and losses, tax adjustments and employee benefits.

Overall Impact absolute amounts, INR in Millions

366 Inventory

684 Lease related adjustments

94 Impairment of financial assets

91 Government grant

66 Dividend

65 Functional currency impact

56 Service concession

arrangement

23,006 Impact on

financial instruments

13,737 Consolidation adjustments

12,069 Tax expense

(including deferred tax)

7,810 Business combinations

5,656 Forex adjustments

3,126 Intangible assets

1,535 Accouting policy

7,275 Employee benefits

13,358 PPE and depreciation

1,663 Accounting for derivatives and

embedded derivatives

1,030 Revenue recognition

2,718 Others

7Decoding the IndAS Impact for Indian Companies

Capital intensive sectors, in particular, the telecommunications and metals/mining & energy sectors contributed nearly 70% of the total adjustments (in absolute value). These two sectors also include the top business groups that have significant global operations and a history of multiple business acquisitions.

Absolute Amt of Adjustments (%)

33%Telecommunication

2%Retail &Personal Care

8%Pharmaceuticals& Biotechnology

5%Infrastructure & Realty

4%Automotive

6%Manufacturing

1%Media & Entertainment

4%Information Technology

37%Energy, Metals

& Mining

8 Decoding the IndAS Impact for Indian Companies

2. Decoding the Impact on Various Sectors

The impact analysed is on the IGAAP PAT for 30 June 2015 and is in absolute value (i.e. it ignores the debit and credit adjustments). This section includes the discussion on the sector specific issues. Adjustments that are common to most companies such as, adjustments with respect to employee benefits or fair valuation of financial instruments etc. are discussed in section 3 of the study.

a. Automotive sector includes both the original equipment manufacturers (OEM) and the auto component suppliers (ACS). Sector specific impact includes adjustments to revenue recognition. In particular, there has been deferral of revenue in case of future performance obligation/s (such as service warranties), and also adjustment for recognition of cash/trade discounts. No material impact was noted on account of embedded lease arrangements in this sector.

Impact on Automotiveabsolute amount, INR in Millions

14PPE and depreciation

Impact on PAT: Increase Increase and decreaseDecrease

273Revenue recognition

286Employee benefits

271Tax expense

(including deferred tax)

45Accounting for derivatives and

embedded derivatives

37Business combinations

25Consolidation adjustments

16Forex adjustments

205Others

2,359Impact on

financial instruments

9Decoding the IndAS Impact for Indian Companies

b. Energy, metals and mining includes oil & gas companies, companies in mining of natural resources, power companies and steel manufacturing companies. Given the sector is capital inten-sive and exposed to the global commodity/currency markets, the sector noted some high value adjustments. These included forex gains and losses (particularly due to change in the functional currency of the company and of it’s foreign operations), restatement of past business combina-tions (including common control acquisitions), change in accounting policy (primarily for oil and mining companies) and adjustments to the carrying value of property, plant and equipment. The adjustments made to fixed assets include impact of INR 10bn of additional depreciation charged by a company as a result of significant increase in the carrying value of it's fixed assets (the specific reason for the increase has not been disclosed in the reconcilliation).

Sector specific impact included, impact of change in the functional currency (US$) by some companies, accounting for service concession arrangements (by power companies) and embedded lease arrange-ments (by power companies). In case of embedded finance lease arrangements, companies that had previously capitalised fixed assets on their balance sheet have de-capitalised the fixed asset/s, reversed the corresponding depreciation charged and recognised a finance lease receivable.

Impact on Energy, Metals & Miningabsolute amount, INR in Millions

3,970Tax expense

(including deferred tax)

2,313Intangible assets

7,792Impact on

financial instruments

2,844Forex adjustments

1,535Accouting policy

546Accounting for derivatives and

embedded derivatives

12,068PPE and depreciation

231Business combinations

386Lease related adjustments

179Inventory

1,942Employee benefits

65Functional currency impact

56Service concession

arrangement

712Others

Impact on PAT: Increase Increase and decreaseDecrease

10 Decoding the IndAS Impact for Indian Companies

c. Information technology sector was amongst the top sector with the maximum number of adjustments. Common adjustments made by the companies included share based payments, restatement of past business combinations and fair valuation of financial instruments. Given share based payments (stock options) are very common incentive for employees in this sector, multiple companies in the sector have made adjustments with respect to expense arising from share based payments. Indian GAAP provided an option to value the stock options using intrinsic value approach, whereas under IndAS, only fair value approach is permitted.

Impact on Information Technologyabsolute amount, INR in Millions

1,427Employee benefits

651Tax expense

(including deferred tax)

816Impact on

financial instruments

480PPE and depreciation

476Business combinations

124Forex adjustments

117Consolidation adjustments

40Impairment of financial assets

14Accounting for derivatives and

embedded derivatives

9Lease related adjustments

9Revenue recognition

6Intangible assets

32Others

Impact on PAT: Increase Increase and decreaseDecrease

11Decoding the IndAS Impact for Indian Companies

d. In case of the Infrastructure and Real Estate sector, no major sector specific adjustments were noted. However, given that some of the large infrastructure companies have yet to announce their Q1 results, we expect some adjustments related to, service concession arrangements, that could impact revenue recognition and recognised property, plant and equipment. Some of the real estate compa-nies that have reported under IndAS have made adjustments to revenue on account of either, change in the accounting policy for applying percentage completion method (POCM) or change to the costs considered for applying the POCM. For example, POCM based on cost, instead of the effort.

Impact on Infrastructure & Realtyabsolute amount, INR in Millions

1,702Impact on

financial instruments

1,244Employee benefits

863Tax expense

(including deferred tax)

180Revenue recognition

330Consolidation adjustments

181Others

Impact on PAT: Increase Increase and decreaseDecrease

12 Decoding the IndAS Impact for Indian Companies

e. In the Manufacturing sector, we have covered 37 companies, across various industries includ-ing chemicals, cements, food and beverages, textile and industrial products. Common adjustments made by companies are with respect to employee benefits, fair valuation of financial instruments, carrying value of PP&E and taxes (primarily deferred tax related).

Sector specific impact includes recognition of embedded lease arrangements (with impact on revenue from operations) and de-capitalisation of borrowing costs from inventory.

Impact on Manufacturingabsolute amount, INR in Millions

1,638Employee benefits

993Tax expense

(including deferred tax)

278Consolidation adjustments

1,464Impact on

financial instruments

188Inventory

146PPE and depreciation

140Intangible assets

131Revenue recognition

108Business combinations

87Government grant

54Impairment of financial assets

28Accounting for derivatives and

embedded derivatives

25Lease related adjustments

14Forex adjustments

182Others

Impact on PAT: Increase Increase and decreaseDecrease

13Decoding the IndAS Impact for Indian Companies

f. Media and Entertainment: Two of the five companies recognised share of losses for minority interest. No significant sector specific impact was noted for companies in this sector. Most of the adjustments made were common to companies in other sectors as well.

Impact on Media & Entertainmentabsolute amount, INR in Millions

995Impact on

financial instruments

208Consolidation adjustments

12Employee benefits

10Revenue recognition

16Lease related adjustments

8Forex adjustments

19Others

Impact on PAT: Increase Increase and decreaseDecrease

g. Pharmaceutical and Biotechnology sector also did not report significant adjustments except for fair valuation of financial instruments and reversal of goodwill amortisation. Tax adjustment was unusually high due to a deferred tax credit adjustment, made by one of the company, with-out adequate disclosure on the nature of the adjustment. Companies have made adjustments to revenue, taking impact of multiple element arrangements, netting off the cash/trade discounts and adjustment for expected sales returns.

Impact on Pharmaceuticals & Biotechnologyabsolute amount, INR in Millions

1,480Impact on

financial instruments

478Intangible assets

361Employee benefits

251Revenue recognition

141Accounting for derivatives and

embedded derivatives

50Business combinations

44PPE and depreciation

311Others

Impact on PAT: Increase Increase and decreaseDecrease

4,679Tax expense

(including deferred tax)

14 Decoding the IndAS Impact for Indian Companies

h. Companies in the Retail and Consumer Goods sectors noted some impact on revenue related to recognition of customer loyalty programmes by the retail sector. Adjustments on account of deriva-tives represent change in fair valuation of embedded derivatives (call/put options) recognised by one company.

Impact on Retail & Personal Careabsolute amount, INR in Millions

225Impact on

financial instruments

137Employee benefits

126Consolidation adjustments

66Dividend

43Business combinations

19Intangible assets

5Lease related adjustments

3Government grant

5Revenue recognition

17Others

Impact on PAT: Increase Increase and decreaseDecrease

226Tax expense

(including deferred tax)

754Accounting for derivatives and

embedded derivatives

15Decoding the IndAS Impact for Indian Companies

i. Companies in the Telecommunications sector primarily include the network operators and tele-com infrastructure companies. Telecom companies have made significant adjustments relating to forex gains/losses (due to change in functional currency of foreign operations), restatement of past business combinations (also resulting in a significant reversal of goodwill amortisation charge) and recognition of share of losses for minority interest.

Sector specific adjustments include adjustment related to service income. For example, reversal of straight lining of lease rentals to the extent related to inflationary increase in the rentals. The same is not required to be included in the straight lining computation under IndAS. Companies have also made significant adjustment for discounting of asset retirement obligations previously recog-nised, resulting in a lower depreciation charge.

6,172Impact on

financial instruments

2,650Forex adjustments

607PPE and depreciation

417Tax expense

(including deferred tax)

241Lease related adjustments

228Employee benefits

171Revenue recognition

169Intangible assets

136Accounting for derivatives and

embedded derivatives

1,169Others

Impact on PAT: Increase Increase and decreaseDecrease

6,865Business combinations

12,544Consolidation adjustments

Impact on Telecommunicationabsolute amount, INR in Millions

16 Decoding the IndAS Impact for Indian Companies

3. Decoding the Major GAAP Adjustments

The study has highlighted significant GAAP adjustments, some of which are common to various sectors. As companies align with the new framework that is closer to the global IFRS, we have analysed these GAAP adjustments in more detail.

a. Adjustments to fixed assets:

The key adjustments made to fixed assets include:

1. Upward fair valuation done by companies to take the benefit of the transition date exemption available to the companies, under IndAS 101. Companies primarily in the capital intensive sectors such as, manufacturing, oil/gas & mining and telecommunications have taken the fair value as deemed cost exemption, on the transition date. Under IndAS, any fair valuation change on the transition date is recognised in retained earnings and the fair value of the asset is treated as it’s deemed cost from such date. Depreciation is charged on the new carrying amount.

2. Companies have capitalised spare parts (capital spares) that were previously expensed under the Indian GAAP. Further, overhauling costs incurred on the fixed assets are required to be capital-ised under IndAS. These costs were usually expensed off under the Indian GAAP.

3. In some cases, companies that are lessees in an embedded finance lease arrangement have recognised a new asset on their balance sheet and charged depreciation on the carrying value of those assets. In case of lessors of such finance lease arrangement, companies have de-capitalised the existing asset, reversed the depreciation charge and recognised income/revenue from the sale of the leased asset.

4. In case of companies with service concession arrangements, the PP&E previously recognised is de-recognised with a corresponding recognition of an intangible asset or a financial asset.

5. Certain companies have made adjustments as a result of adopting a capitalisation/depreciation policy that was not permitted under IGAAP. For example, in case of oil & gas and mining industry, companies have adopted policies on capitalisation of certain expenses and depletion/depreciation, which were not available/permitted under the Indian GAAP.

b. Consolidation related adjustments, including adjustments to past business combinations:

Some major adjustments include:

1. Adjustment to the minority interest (non-controlling interest): IndAS mandates allocating the losses to minority shareholders (non-controlling interest). IGAAP only requires allocation of the losses to minority shareholders, if it is contractually agreed. Companies have recognised the share of losses incurred during the quarter attributed to the minority shareholders. IndAS 101 permits, to not allocate previously un-recognised losses on the transition date.

2. Definition of control under IndAS is much wider and requires a company to assess the contractual rights, de-facto control, and potential voting rights before determining

17Decoding the IndAS Impact for Indian Companies

control. The current Indian GAAP focuses more on majority voting rights and the board composition, while assessing control. Based on our study, new subsidiaries have been consolidated including, investments previously treated as a joint venture or an associate. Further, companies have consolidated employee welfare trusts and ESOP trusts. Interestingly, there are also companies which have de-consolidated some of the previously consolidated subsidiaries or associates and accounted for these as “investments in equity shares held at fair value through other comprehensive income (OCI)”.

3. The definition and accounting for joint arrangements has significantly changed under IndAS as compared to the current IGAAP. Under IndAS, joint arrangements are classified and accounted for as either, a Joint Venture (JV) or a Joint Operation (JO). Equity account-ing is permitted only in case of a JV, while a JO arrangement is accounted by consolidating the investor’s proportionate share in the assets/liabilities, income and expenses, in the investee company. As a result, companies have re-evaluated their existing joint arrangements and made the necessary adjustments.

4. Past business combinations: Most Indian companies record business combinations based on the carrying value approach. IndAS permits only “Purchase method” to account for all business combinations (except in case of common control business combination, for which Pooling of Interest method is required). Purchase method requires, the acquirer to fair value the consider-ation as well as the assets and liabilities acquired. Further, goodwill is the residual of the purchase consideration over the net assets acquired and is tested for impairment, at each reporting date. On the transition date, companies are given an option to either restate the past business combinations or grandfather the previous GAAP accounting treatment (subject to some prescribed adjustments).

On transition, companies that have taken the option to restate the past combinations have unlocked the value in goodwill, recognised new intangible assets and fair valued the net assets acquired, in those combination/s. Adjustments are also made as a result of recognising contingent and deferred consideration, at fair value. Further, significant credit adjustments are made by companies to reverse the amortisation of goodwill. Amortisation of goodwill is not permitted under IndAS and is only required to be tested for impairment regularly.

Also, companies that have previously recognised goodwill on common control business combinations have restated those acquisitions using the “Pooling of Interest method”. As a result, companies had to de-recognise the previously recognised goodwill and the subsequent impairment recognised on such goodwill under the Indian GAAP has been reversed, under IndAS.

c. Share based payments and employee benefits:

IndAS requires actuarial gains and losses on post-employment defined benefit schemes (such as gratuity) to be recognised in other comprehensive income (OCI). Such actuarial gains/losses are never transferred back to, the profit and loss account. Indian GAAP permits companies to recognise actuarial gains and losses in the profit and loss account. Further, there are some GAAP differences with respect to, recognition of past service costs between the two standards.

Almost all companies have reflected the accounting impact arising from the above GAAP difference in their quarterly results (including the comparative period/s).

In relation to the share based payments, IndAS mandates costs related to share based payments to be computed based on the fair valuation of the options, on the grant date. Indian GAAP also permits the use of intrinsic value. There is also difference in accounting treatment for options issued to employees under a graded vested scheme, whereby, IndAS treatment results in higher charge to the profit and loss account in the later years of the plan (Indian GAAP gives an option to straight line the charge). Companies that have share based schemes (primarily in the IT sector), have recognised the impact of the above GAAP difference, in their first quarter results and the comparative periods.

18 Decoding the IndAS Impact for Indian Companies

d. Adjustments to the carrying value of financial instruments:

Adjustments with respect to financial instruments account for almost 25% of the total value of adjust-ments made by the companies. As reflected in the executive summary above, most companies have had to adjust the carrying value of their financial instruments, on transition. IndAS introduces many new requirements with respect to classification, recognition and measurement principles, for financial instruments. The new framework also requires certain financial assets to be tested for impairment.

Some of the key requirements include:

a. Classification of an instrument as debt or equity;

b. Amortisation of transactions costs, in case of financial assets/liabilities other than those held at fair value through profit and loss account;

c. Fair valuation of all financial assets and liabilities at initial recognition and for some also on subse-quent re-measurement;

d. Categorisation of financial assets and liabilities into specific buckets, based on the nature and purpose of such instruments;

e. Recognition of fair value gains and losses on financial assets and liabilities either in the profit & loss account or in other comprehensive income, based on their classification; and

f. Impairment test for certain financial assets based on the expected credit loss (ECL) method.

Indian GAAP requires companies to carry current investments at the lower of cost of net realis-able value (NRV). As such, companies do not recognise the fair value gains in such investments (for example on mutual funds). In case of long term investments, these are carried at cost, unless there is a permanent diminution in the value of such investments. There is no specific requirement or guidance under Indian GAAP to fair value the financial instruments or to test them for impairment.

Almost 85% of the companies selected have made adjustments to the classification and carry-ing values of their financial instruments. In particular, adjustments have been made on account of fair valuation of investments, discounting of long term provisions (such as asset restoration liabilities), fair valuation of security deposits, amortisation of transaction costs (such as loan processing fees), and impairment losses on receivables/inter-corporate deposits. Fair value movements in the carrying values have significantly impacted the results, for the quarter.

Companies that have redeemable preference shares/debentures or have compound financial instruments (such as convertible preference shares) have recognised the impact on transition. For example, recognition of dividend cost as finance costs in case of redeemable preference shares and recognition of redemption premium in the profit and loss account. Indian GAAP permits adjust-ment of redemption premium with the securities premium account, without affecting the profit and loss account.

e. Derivatives and hedge accounting:

Except in case of voluntary adoption of Accounting Standards (AS) 30, 31, 32 by a company, Indian GAAP does not permit companies to recognise mark to market gains (only losses are recognised) on derivative contracts (other than, in case of foreign currency forward contracts, for which separate guidance is given under the GAAP). Under IndAS, derivative contracts need to be marked to market and resulting gains/losses are recognised in the profit and loss account. Further, there is difference in the accounting treatment for recognising foreign currency forward contracts between Indian GAAP and IndAS.

Companies have recognised the marked to market adjustments (in particular, gains) on their derivative contracts that were not previously recognised, under the Indian GAAP.

19Decoding the IndAS Impact for Indian Companies

Further, under IGAAP there is no concept of embedded derivatives (such as call/put options, prepay-ment options etc). IndAS mandates companies to identify embedded derivatives within normal executory contracts and measure such embedded derivatives separately, at fair value. On transition, companies have identified embedded derivatives (in particular call and put options) and recognised the subsequent fair value movement in the profit and loss account. For example, one of the companies has recognised a put option (as an obligation) with the minority shareholder to sell it’s remaining interest to the majority share-holders. A company has also recognised fair value gain or loss on the call and put options embedded within their share purchase agreements of overseas operations.

f. Service concession arrangements (SCA):

Under IndAS, companies operating through service concession arrangements may have to recognise revenue and profits earlier, than what is required under the Indian GAAP. The eligible companies would be required to recognise an intangible asset or a financial asset on their balance sheet, as opposed to property, plant and equipment (PP&E) under the Indian GAAP. Revenue is recognised during all the stages of the performance obligations including, construction, operation and mainte-nance of the asset. Under the Indian GAAP, revenue recognition usually commences on the start of commercial use of the asset. For example, in case of construction of toll road, no revenue is usually recognised until the completion of construction and the users start paying the toll charges.

On transition to IndAS, companies in the relevant sectors (particularly power, utility and infrastruc-ture) have recognised revenue during the construction stage, recognised intangible asset and/or a financial asset and de-recognised previously recognised PP&E. The recognition of revenue and profits during the construction stage would also have impact on the tax liability, particularly, if the company is covered by the Minimum Alterative Tax (MAT) provisions.

g. Intangible assets and goodwill:

Under IndAS, companies are required to account for business combinations using the Purchase method only. Under the purchase method, companies are required to fair value the consideration and also fair value the assets and liabilities acquired in the combination. The assets and liabilities acquired include assets and liabilities not previously recognised by the acquired company, for example intangi-ble assets such as customer list, intellectual property and other assets and liabilities such as contingent liabilities, fair value of operating leases etc.

On transition, some companies have decided to restate some of their past business combinations and unlock the value in goodwill by recognising the intangible assets. Intangible assets recognised are amortised/depreciated over their respective economic useful lives. Further, any previously charged amortisation on goodwill (permitted under IGAAP) has been reversed under IndAS resulting in a significant increase to the carrying value of goodwill for some companies as well as credit to the income statement to the extent of the amortisation charge.

Some companies have also recognised new intangible assets that were not permitted to be recog-nised under the previous GAAP.

Also refer to the discussion in point b) of this section above.

20 Decoding the IndAS Impact for Indian Companies

h. Lease related adjustments:

1. Composite lease arrangements: IndAS requires that in case of composite lease arrange-ments for land and buildings, companies are required to test the two components indepen-dently for classifying them as an operating or a finance lease. The separation of the lease rental is determined based on relative standalone fair values of the two components. Some companies that had composite lease arrangements have made adjustments on account of the new requirement and accounted for the two separately.

2. Embedded lease arrangements: IndAS also requires any embedded lease of assets within normal executory contracts to be separately accounted for, in particular where the customer controls the use/access of the underlying asset. Companies in the manufacturing, metals and power sectors have made adjustments by separating out embedded leases and have recog-nised the lease of the underlying asset as, an operating or a finance lease. In case of embedded finance lease arrangements, companies that had previously capitalised fixed assets on their balance sheet have de-capitalised the fixed asset/s, reversed the corresponding depreciation charged and recognised finance lease receivable. In case of embedded operating leases, compa-nies have carved out the rental income from the revenue amount recognised previously and recognised the same separately, as lease income.

3. Other adjustments on account of lease arrangements include fair valuation of interest free security deposits with amortisation of resultant prepaid rent over the lease period. The unwinding of the discount is recognised in the profit and loss account. Companies have also reversed any revenue or expense from straight lining of lease rentals, if the rental increase was linked to inflation index.

i. Revenue recognition:

IndAS has some very specific provisions that impact certain sectors and arrangements. For instance, revenue recognition would change in case of service concession arrangements (as discussed above). Further, there are some specific provisions on multiple element arrangements (or arrangements containing multiple performance obligations). In such cases, companies may have to defer a part of their revenue until the performance obligation is complete. This could be the case in automobile sector, telecommunication sector or some of the service sectors where a company has multiple performance obligations and have bundled arrangements with their customers.

Some adjustments made to revenue include:

a. Recognition of revenue from service concession arrangements;

b. Deferral of revenue in case of future performance obligations (for example over the service period, in case of extended service warranties);

c. Adjustments recognised with respect to cash and trade discounts expected to be transferred to customers/dealers;

d. Adjustment to revenue in case of embedded lease arrangements by segregating the total contract revenue into lease income and income from sale of goods or services;

e. Change in accounting policy for recognising revenue from operations. For example, in case of real estate sector, companies have re-assessed their policy on application of the POCM approach.

f. Gross up adjustments on reassessment of principal vs. agency relationship.

g. Reversal of the lease rentals straight lining impact to the extent related to inflation price index; and

h. Adjustments with respect to customer loyalty programmes, in the retail sector.

21Decoding the IndAS Impact for Indian Companies

In case of other income, companies have recognised interest income arising from unwinding of discount on fair valuation of financial assets (such as security deposits).

j. Adjustments made related to foreign exchange gain or loss include:

1. IndAS introduces a new concept of “Functional Currency” which is, the currency of the primary economic environment in which an entity operates and can be different from the company’s “Presentation Currency”, which is the currency in which the company prepares and reports it’s financial results. Every reporting entity is required to assess it’s functional and presentation currency and record it’s transactions in it’s functional currency. On transition, companies in specific sectors with significant foreign operations (for example oil companies, telecom companies) have determined their functional currency to be other than INR and recog-nised forex gains or losses from translation on foreign currency transactions to it’s functional currency, in the profit and loss account. For example, one of the oil companies has determined US$ as it’s functional currency.

2. Under IndAS all foreign currency gains and losses are recognised in the profit and loss account. Indian GAAP permitted companies to defer or capitalise the foreign currency gains and losses on long term monetary foreign currency items. Although, the transition provision allow companies to continue following the previous GAAP policy for outstanding balances, in case of new transactions, any forex gain or loss on restatement is recognised in the profit and loss account.

3. Further, the transition provisions requires, any existing balance in the foreign currency trans-lation reserve to be transferred to retained earnings on the transition date. Companies have made such adjustment to equity/reserves, at the transition date.

k. Deferred taxes:

Companies have recognised the incidental impact on deferred tax, of the various accounting adjust-ments (discussed above). In addition to the incidental impact, companies have recognised deferred tax liability for undistributed profits of joint ventures and associates, which is permitted to be recognised under IndAS, in case there is no doubt on the reversal of such deferred tax.

l. Transition date exemptions:

Based on the limited disclosures in the interim results, some key exemptions opted by the companies include a) restatement of the past business combinations (in part or all past business combina-tions) and b) deemed cost exemption with respect to the carrying value of fixed assets (both in terms of the option to either grandfather the previous GAAP carrying values or fair value such assets on the transition date). Many companies did not opt the fair valuation exemption for fixed assets due to potential MAT liability, based on the draft circular issued by the CBDT.

With some clarification/s issued by the CBDT, that provides relief to companies around, the impact of fair valuation adjustments on the transition date, on the MAT liability, it is likely that more companies would revisit their opening balance sheets and consider taking the transition date exemption on fair valuation of their fixed assets.

Some companies have also adjusted the carrying value of their investments in subsidiaries, associates and joint ventures in their standalone financial statements by opting for the fair value and deemed cost exemption under IndAS 101. For example, one of the companies in the telecom sector has exercised the option to fair value it’s investments in some of it’s subsidiaries.

22 Decoding the IndAS Impact for Indian Companies

Closing Comments

Based on our study of the quarter 1 results reported by the companies across sectors, it is clear that companies have put in tremendous effort to thoroughly analyse and examine the new accounting rules, which to a large extent are converged to the global IFRS standards.

IndAS standards are different from the existing Indian GAAP framework in three key aspects i.e.

a. Fair valuation

b. Substance over legal form and

c. Emphasis on the Balance Sheet.

Also, the new framework is principle based, as opposed to rule based.

Based on our analysis of the transition and the Q1 financial statements, covered in this study, it is quite evident that all the three fundamental changes have translated into significant financial impact, for the Indian companies. It is also interesting to see that the adjustments made by companies to the revenue has been relatively marginal, across all major sectors. Significant impact has been seen arising from the changes to carrying values of the assets and liabilities.

Given that the new rules emphasise on the substance of the transaction, it is imperative for the companies to properly understand and analyse the accounting implications when they enter into various business arrangements.

Although, the first quarter reporting has disclosed most of the expected impact areas, it would be interesting to see through the entire transition (including the first full year results), to be able to understand and analyse various other possible adjustments and in particular any innovative applica-tion of the new framework, by companies.

23Decoding the IndAS Impact for Indian Companies

Is Your Company Ready for the Transition?

Through this study, it is clear that more than 50% of the companies have made more than 8-10 adjustments in their first quarter results. We should also acknowledge that the interim results are only representing part of the year and carry very limited disclosures, explanations and reconcilliations on the transition. Given, that the first full year reporting is just a few months away for companies in the first phase, it is important that they put in the additional effort required, to meet the reporting requirements, under the new framework.

For private companies and companies in phase 2 of the transition, the ongoing IndAS reporting should provide adequate guidance and direction on how to approach this significant change, and how to use the transition window to the best advantage.

It is also critical that companies understand and start working on the non-accounting impact, since the transition is way beyond, just accounting adjustments. The transition will have multifold impact on company’s business processes, its contractual arrangements, IT systems, tax and treasury management.

We have attached a high level questionnaire for you to do an initial assessment of your company’s preparedness for the new global framework.

24 Decoding the IndAS Impact for Indian Companies

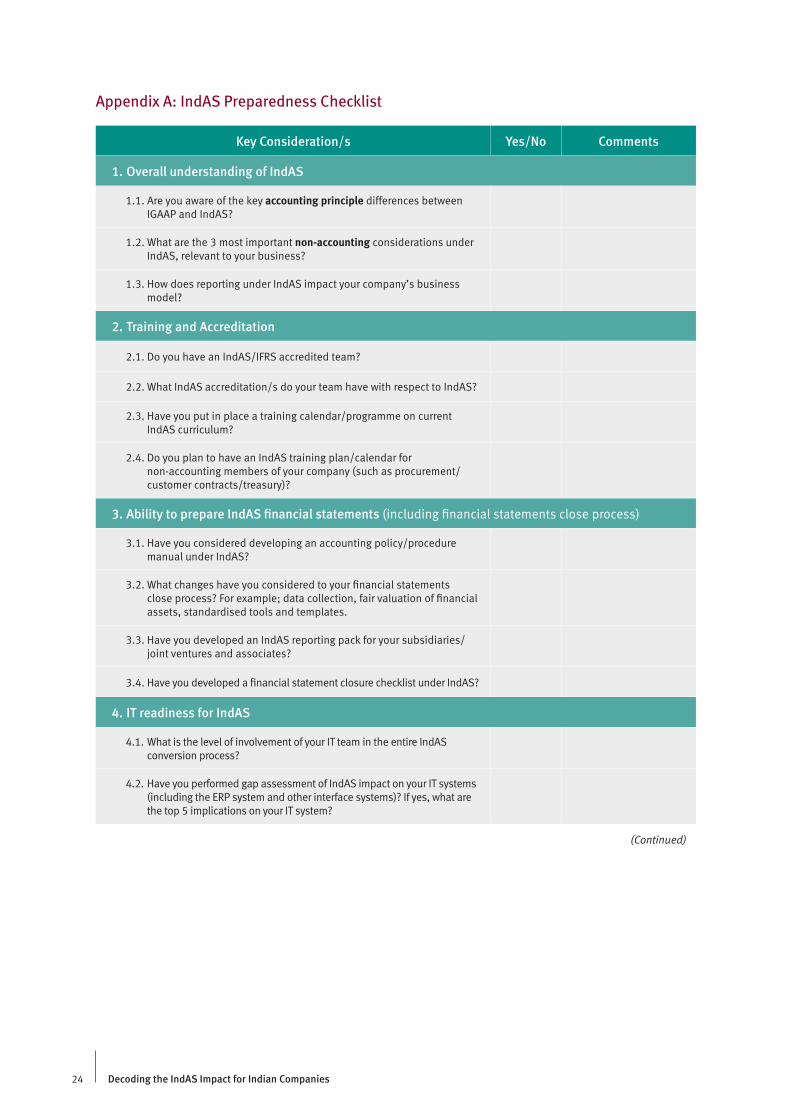

Appendix A: IndAS Preparedness Checklist

Key Consideration/s Yes/No Comments

1. Overall understanding of IndAS

1.1. Are you aware of the key accounting principle differences between IGAAP and IndAS?

1.2. What are the 3 most important non-accounting considerations under IndAS, relevant to your business?

1.3. How does reporting under IndAS impact your company’s business model?

2. Training and Accreditation

2.1. Do you have an IndAS/IFRS accredited team?

2.2. What IndAS accreditation/s do your team have with respect to IndAS?

2.3. Have you put in place a training calendar/programme on current IndAS curriculum?

2.4. Do you plan to have an IndAS training plan/calendar for non-accounting members of your company (such as procurement/customer contracts/treasury)?

3. Ability to prepare IndAS financial statements (including financial statements close process)

3.1. Have you considered developing an accounting policy/procedure manual under IndAS?

3.2. What changes have you considered to your financial statements close process? For example; data collection, fair valuation of financial assets, standardised tools and templates.

3.3. Have you developed an IndAS reporting pack for your subsidiaries/joint ventures and associates?

3.4. Have you developed a financial statement closure checklist under IndAS?

4. IT readiness for IndAS

4.1. What is the level of involvement of your IT team in the entire IndAS conversion process?

4.2. Have you performed gap assessment of IndAS impact on your IT systems (including the ERP system and other interface systems)? If yes, what are the top 5 implications on your IT system?

(Continued)

25Decoding the IndAS Impact for Indian Companies

5. Business process readiness for IndAS

5.1. What has been the level of involvement of various business owners and functional leads in the IndAS conversion process?

5.2. Have you performed a gap assessment of IndAS on your business processes? If yes, please share your understanding of the key changes.

5.3. Do you see a need for a SOP to determine the fair valuation of assets/liabilities and transactions?

5.4. Do you see a need to put in place a SOP to identify embedded derivatives within executory contracts?

5.5. Do you see a need to put in place a SOP for computing impairment loss on your financial assets based on expected credit loss (ECL) method?

5.6. Do you see a need to develop a SOP for identifying embedded lease arrangements?

5.7. What process have you put in place for hedge effectiveness testing and hedge accounting compliance?

5.8. What process have you put in place for identifying various performance obligations within revenue contracts?

26 Decoding the IndAS Impact for Indian Companies

Aban Offshore Limited

Adani Power Limited

Adlabs Entertainment Limited

Ajanta Pharma Limited

Akzo Nobel India Limited

Alembic Pharmaceuticals Limited

Alkem laboratories Limited

Apollo Tyres Limited

Ashok Leyland Limited

Asian Paints Limited

Atul Limited

Bajaj Auto Limited

Bajaj Corp Limited

Bayer Cropscience Limited

Berger Paints India Limited

Bharat Electronics Limited

Bharat Forge Limited

Bharti Airtel Limited

Bharti Infratel Limited

Biocon Limited

Bosch Limited

Brigade Enterprises Limited

Britannia Industries Limited

Cadila Healthcare Limited

Ceat Limited

Colgate Palmolive (India) Limited

Coromandel International Limited

Cyient Limited

Dabur India Limited

DB Corp Limited

Dr Reddys Laboratories Limited

Eicher Motors Limited

Elecon Engineering Company Limited

Emami Limited

Exide Industries Limited

Force Motors Limited

GHCL Limited

Glaxosmithkline Consumer Healthcare Limited

Glaxosmithkline Pharmaceuticals Limited

Glenmark Pharmaceuticals Limited

Godrej Consumer Products Limited

Godrej Properties Limited

Grasim Industries Limited

Greaves Cotton Limited

Greenply Industries Limited

Gujarat Narmada Valley Fertilizers Chemicals Limited

Gujarat State Fertilizers Chemicals Limited

Havells India Limited

HEG Limited

Heidelberg Cement India Limited

Hero Motocorp Limited

Hindalco Industries Limited

Hindustan Construction Company Limited

Hindustan Unilever Limited

Hindustan Zinc Limited

Honeywell Automation india Limited

Idea Cellular Limited

Indiabulls Real Estate Limited

Indian Metals Ferro Alloys Limited

Indoco Remedies Limited

Info Edge (India) Limited

Infosys Limited

Ingersoll Rand (India) Limited

ITC Limited

JK Paper Limited

JMC Projects (India) Limited

JSW Energy Limited

JSW Steel Limited

Kajaria Ceramics Limited

Kalpataru Power Transmission Limited

Kansai Nerolac Paints Limited

KEC International Limited

Larsen Toubro Limited

Lupin Limited

Mahindra and Mahindra Limited

Marico Limited

Maruti Suzuki India Limited

MINDTREE Limited

Motherson Sumi Systems Limited

MphasiS Limited

MRF Limited

Natco Pharma Limited

NCC Limited

Network 18 Media Investments Limited

NHPC Limited

Nilkamal Limited

Novartis India Limited

Orient Green Power Company Limited

Persistent Systems Limited

Pfizer Limited

PI Industries Limited

Pidilite Industries Limited

Piramal Enterprises Limited

Power Grid Corporation of India Limited

Rallis India Limited

Raymond Limited

Reliance Industries Limited

Shoppers Stop Limited

Sun Pharmaceutical Industries Limited

Syngene International Limited

Tata Communications Limited

Tata Consultancy Services Limited

Tech Mahindra Limited

The Phoenix Mills Limited

The Ramco Cements Limited

Thermax Limited

Tinplate Company of India Limited

Torrent Pharmaceuticals Limited

Torrent Power Limited

Trent Limited

TV18 Broadcast Limited

TVS Motor Company Limited

Ultratech Cement Limited

United Spirits Limited

UPL Limited

Vedanta Limited

Voltas Limited

Wabco India Limited

Welspun India Limited

Wipro Limited

Wockhardt Limited

Zee Entertainment Enterprises Limited

Zensar Technologies Limited

Appendix B: List of Companies Included in the Study

27Decoding the IndAS Impact for Indian Companies

About Protiviti

Protiviti (www.protiviti.com) is a global consulting firm that helps companies solve problems in finance, technology, operations, governance, risk and internal audit, and has served more than 60 percent of Fortune 1000® and 35 percent of Fortune Global 500® companies. Protiviti and our independently owned Member Firms serve clients through a network of more than 70 locations in over 20 countries. We also work with smaller, growing companies, including those looking to go public, as well as government agencies. In India, Protiviti’s member firm (Protiviti India Member Private Ltd.) is a leading provider of business consulting, internal audit, risk management, technology, tax and regulatory, financial reporting and IFRS advisory, forensic and fraud investigation, information management and transaction services. Protiviti member firms are separate and independent legal entities, are not agents of other firms in the Protiviti network, and have no authority to obligate or bind other firms in the Protiviti network.

Ranked 57 on the 2016 Fortune 100 Best Companies to Work For® list, Protiviti is a wholly owned subsidiary of Robert Half (NYSE:RHI). Founded in 1948, Robert Half is a member of the S&P 500 index.

Financial Reporting and Accounting Advisory

Protiviti’s Financial Reporting consultants help companies on various financial reporting matters. The conditions in today’s global business market, such as rapidly changing regulations, increased scrutiny of company financials, complex, nonrecurring business transactions, and complex accounting standards, strain the capabilities of many finance organisations. This amplified stress increases an organisation's exposure to mistakes, lost synergies and the inability to maintain base-level financial processes. The risk of these errors is typically higher during the adoption of new accounting standards; embarking on significant business transactions; implementation of new IT/enterprise resources planning (ERP) systems; restructurings, acquisitions and divestitures; and expansion into new markets or new businesses.

Our Financial Reporting professionals are qualified chartered accountants with extensive practical experience in financial reporting across multiple jurisdictions and under various accounting frameworks (including IFRS and US GAAP). Our financial reporting experts provide the critical functional and project management expertise necessary to cost-effectively prepare for and manage non-routine situations such as transition to new accounting standards, restatements, mergers and IPOs. We proactively monitor new accounting rules, alert our clients to changing requirements and offer assistance with addressing complex accounting or reporting challenges, including the conversion to International Financial Reporting Standards (IFRS).

Contacts

Vishal Seth +91.124.661.8650 [email protected]

Subrata Bagchi +91.124.661.8630 [email protected]

Disclaimer

This publication has been carefully prepared, but should be seen as general guidance only. You should not act or refrain from acting, based upon the information contained in this presentation, without obtaining specific professional advice. Please contact the persons listed in the publication to discuss these matters in the context of your particular circumstances. Protiviti India Member Private Ltd nor the shareholders, partners, directors, managers, employees or agents of any of them make any representation or warranty, expressed or implied, as to the accuracy, reasonableness or completeness of the information contained in the publication. All such parties and entities expressly disclaim any and all liability for or based on or relating to any information contained herein, or error, or omissions from this publication or any loss incurred as a result of acting on information in this presentation, or for any decision based on it.

© 2016 Protiviti Inc. An Equal Opportunity Employer. M/F/Disability/Veterans. PRO-0816-108164Protiviti is not licensed or registered as a public accounting firm and does not issue opinions on financial statements or offer attestation services.

* Protiviti Member Firm

THE AMERICAS

UNITED STATES

AlexandriaAtlantaBaltimoreBostonCharlotteChicagoCincinnatiClevelandDallasDenverFort LauderdaleHouston

Kansas City Los Angeles Milwaukee Minneapolis New York Orlando Philadelphia Phoenix Pittsburgh Portland Richmond Sacramento

Salt Lake City San Francisco San Jose Seattle Stamford St. Louis Tampa Washington, D.C. WinchesterWoodbridge

ARGENTINA*

Buenos Aires

BRAZIL*

Rio de Janeiro São Paulo

CANADA

Kitchener-WaterlooToronto

ASIA-PACIFIC

AUSTRALIA

BrisbaneCanberraMelbourneSydney

CHINA

BeijingHong KongShanghaiShenzhen

INDIA*

BangaloreHyderabadKolkata MumbaiNew Delhi

JAPAN

Osaka Tokyo

SINGAPORE

Singapore

CHILE*

Santiago

MEXICO*

Mexico City

PERU*

Lima

VENEZUELA*

Caracas

EUROPE/MIDDLE EAST/AFRICA

FRANCE

Paris

GERMANY

Frankfurt Munich

ITALY

Milan Rome Turin

THE NETHERLANDS

Amsterdam

UNITED KINGDOM

London

BAHRAIN*

Manama

KUWAIT*

Kuwait City

OMAN*

Muscat

SOUTH AFRICA*

Johannesburg

QATAR*

Doha

SAUDI ARABIA*

Riyadh

UNITED ARAB EMIRATES*

Abu Dhabi Dubai