decoding treasury and fintechs past and … treasury and fintechs past and forecasting the future...

TRANSCRIPT

Decoding Treasury and Fintech’s past and forecasting the futureEvan Smith, VP & Treasurer, CST BrandsMark Kirsch CTP, Treasury Practitioner Executive, Bank of AmericaApril 4, 2017

22

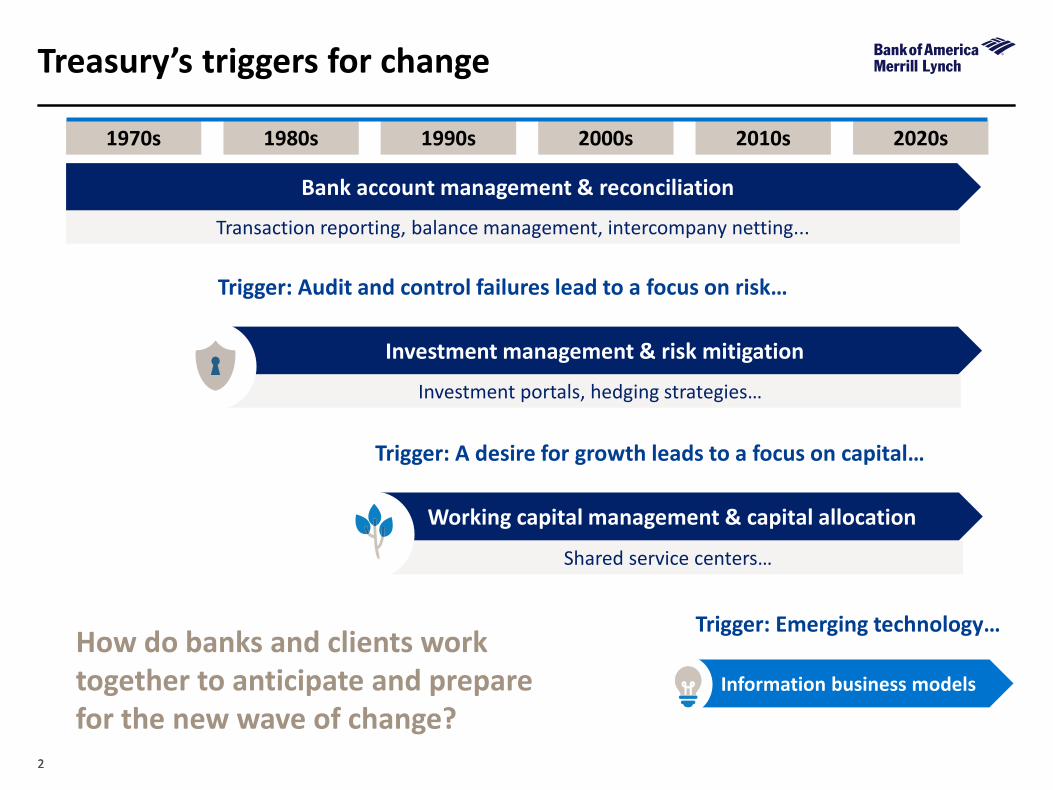

Treasury’s triggers for change

1970s 1980s 1990s 2000s 2010s 2020s

Bank account management & reconciliation

Investment management & risk mitigation

Working capital management & capital allocation

Information business models

Trigger: Audit and control failures lead to a focus on risk…

Trigger: A desire for growth leads to a focus on capital…

Transaction reporting, balance management, intercompany netting...

Investment portals, hedging strategies…

Shared service centers…

Trigger: Emerging technology…How do banks and clients work together to anticipate and prepare for the new wave of change?

33

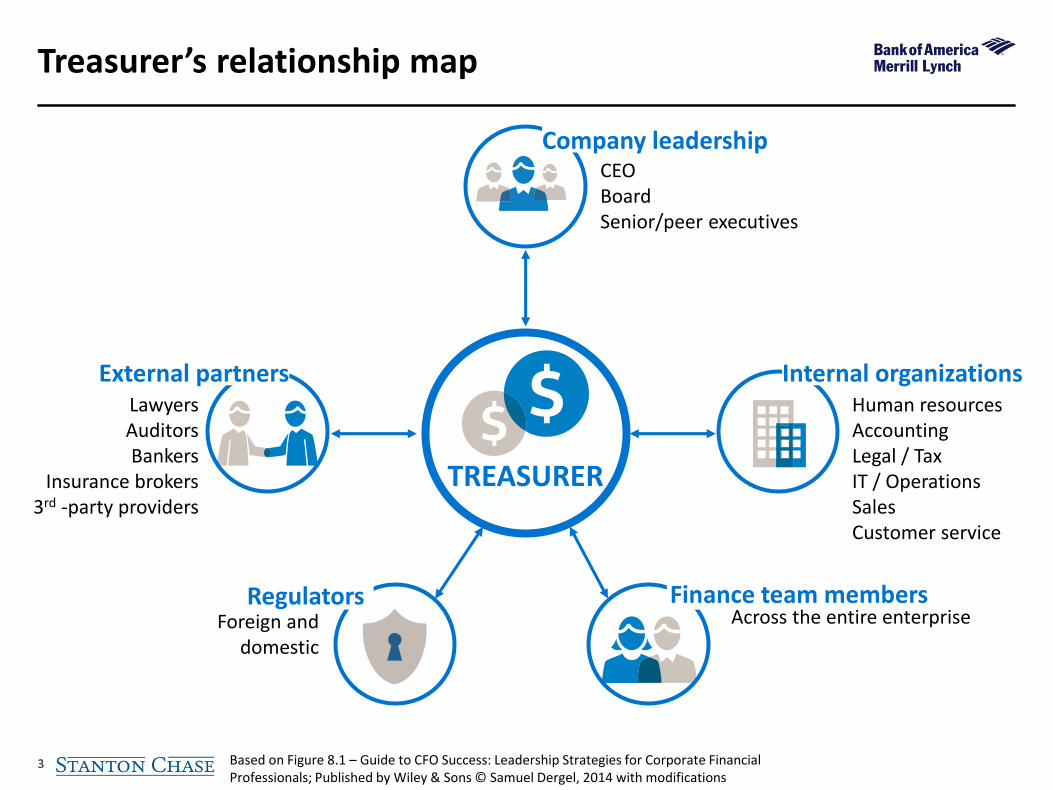

Treasurer’s relationship map

TREASURER

Based on Figure 8.1 – Guide to CFO Success: Leadership Strategies for Corporate Financial Professionals; Published by Wiley & Sons © Samuel Dergel, 2014 with modifications

LawyersAuditorsBankers

Insurance brokers3rd -party providers

External partnersHuman resourcesAccountingLegal / TaxIT / OperationsSalesCustomer service

Internal organizations

Across the entire enterpriseFinance team members

CEOBoardSenior/peer executives

Company leadership

Foreign and domestic

Regulators

44

Liquidity solutions, POBO/ROBO, shared service centers,virtual accounts

Payment factories, ZBA structures, TMS

In-house bank, multi banking, FX, trade finance

Intercompany netting, term deposits, banking workstation software

Daily transaction reporting, balances

Early 1980s to 2020s – Generational waves

Pri

nci

ple

pro

du

ct in

no

vati

on

s –

Mar

ket

mat

uri

ty

SEPA, FBAR, FATCA, fraud, EMV, Cyber security, cloud-based software, distributed ledger technology, the rise of FinTech firms, alternative lenders, e-Commerce, m-Commerce

Historically, innovation was driven solely by financial institutions. But now…..

Why it matters

• Treasury functions have bought into generational solutions as a group; however they have always sought the next big thing.

• Each wave of innovation has a long tail. 95% of today’s business will be 10% of the total in the future. The 5% is the innovation space.

• Risk management has evolved over time into one of the most critical responsibilities of the function. What is your risk appetite?

• Banks used to provide end-to-end industry wide solutions; however market disruptions and crisis's, as well as increased regulations has altered their business rules and the decisions based on those rules.

• The introduction of FinTech firms has significantly changed the landscape.

Treasury’s evolution has occurred in waves

55

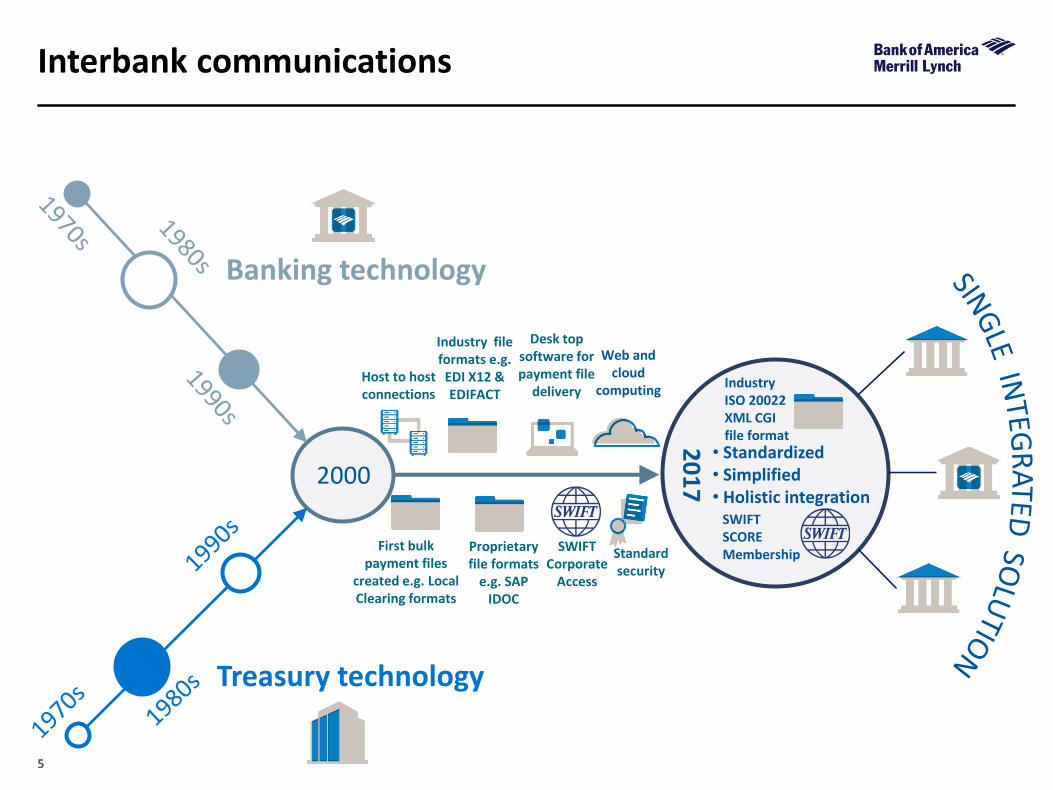

Interbank communications

20

172000

Banking technology

Treasury technology

First bulk payment files

created e.g. Local Clearing formats

Desk top software for payment file

delivery

Industry file formats e.g.

EDI X12 & EDIFACT

Proprietary file formats

e.g. SAP IDOC

Host to host connections

SWIFT Corporate

Access

Industry ISO 20022 XML CGI file format

Web and cloud

computing

SWIFT SCOREMembership

• Standardized• Simplified• Holistic integration

Standard security

66

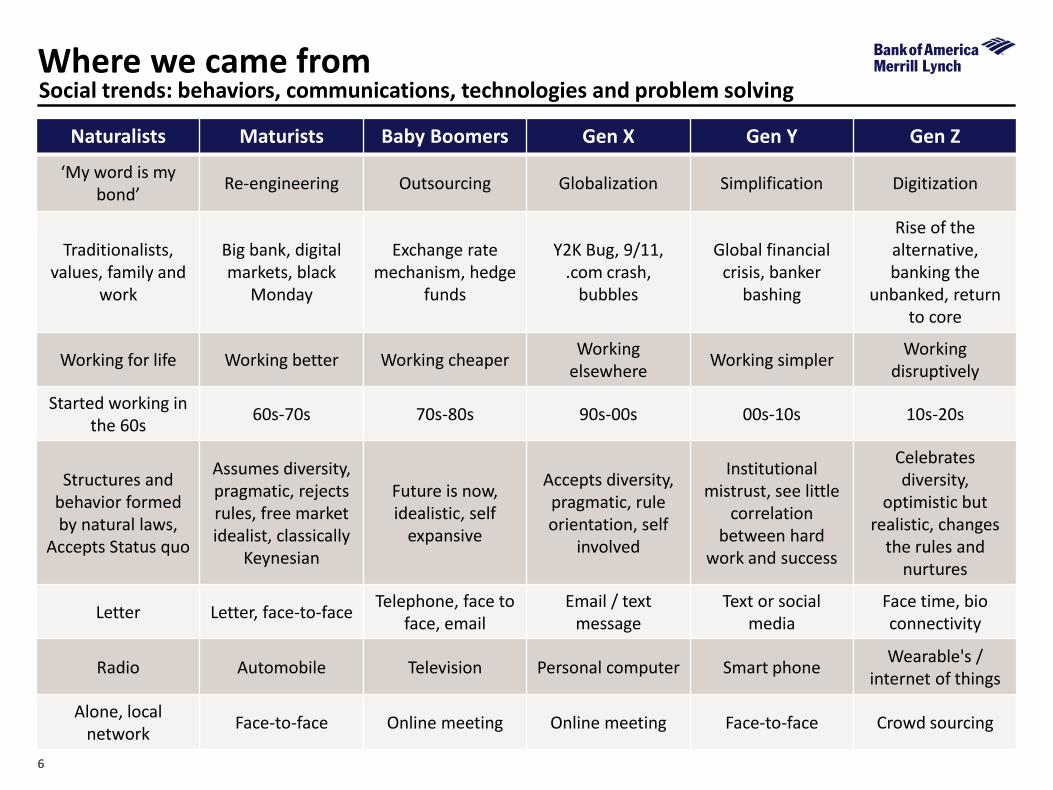

Where we came fromSocial trends: behaviors, communications, technologies and problem solving

Naturalists Maturists Baby Boomers Gen X Gen Y Gen Z

‘My word is my bond’

Re-engineering Outsourcing Globalization Simplification Digitization

Traditionalists, values, family and

work

Big bank, digital markets, black

Monday

Exchange rate mechanism, hedge

funds

Y2K Bug, 9/11, .com crash,

bubbles

Global financial crisis, banker

bashing

Rise of the alternative, banking the

unbanked, return to core

Working for life Working better Working cheaperWorking

elsewhereWorking simpler

Working disruptively

Started working in the 60s

60s-70s 70s-80s 90s-00s 00s-10s 10s-20s

Structures and behavior formed by natural laws,

Accepts Status quo

Assumes diversity, pragmatic, rejects rules, free market idealist, classically

Keynesian

Future is now, idealistic, self

expansive

Accepts diversity,pragmatic, rule orientation, self

involved

Institutional mistrust, see little

correlation between hard

work and success

Celebrates diversity,

optimistic but realistic, changes

the rules and nurtures

Letter Letter, face-to-faceTelephone, face to

face, emailEmail / text

messageText or social

mediaFace time, bioconnectivity

Radio Automobile Television Personal computer Smart phoneWearable's /

internet of things

Alone, local network

Face-to-face Online meeting Online meeting Face-to-face Crowd sourcing

77

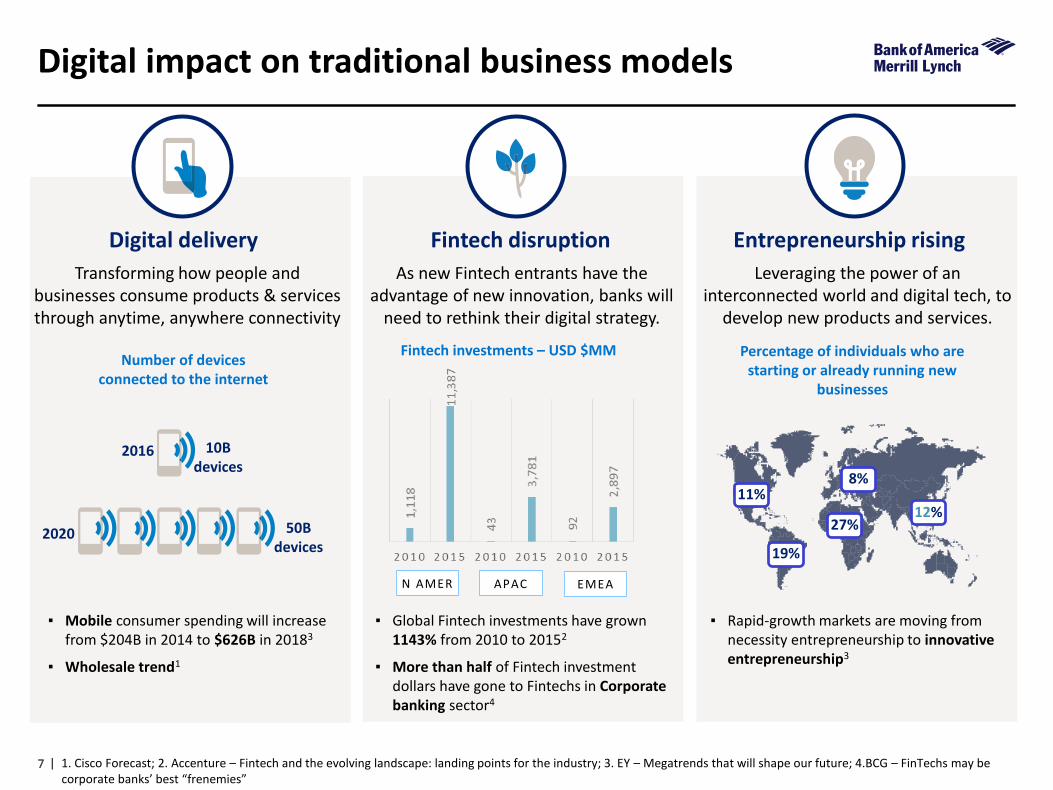

Digital impact on traditional business models

| 1. Cisco Forecast; 2. Accenture – Fintech and the evolving landscape: landing points for the industry; 3. EY – Megatrends that will shape our future; 4.BCG – FinTechs may be corporate banks’ best “frenemies”

Entrepreneurship rising

Leveraging the power of an interconnected world and digital tech, to

develop new products and services.

▪ Rapid-growth markets are moving from necessity entrepreneurship to innovative entrepreneurship3

11%

19%

27%

8%

12%

Percentage of individuals who are starting or already running new

businesses

▪ Global Fintech investments have grown 1143% from 2010 to 20152

▪ More than half of Fintech investment dollars have gone to Fintechs in Corporate banking sector4

Fintech disruption

As new Fintech entrants have the advantage of new innovation, banks will

need to rethink their digital strategy.

N AMER APAC EMEA

Fintech investments – USD $MM

▪ Mobile consumer spending will increase from $204B in 2014 to $626B in 20183

▪ Wholesale trend1

Digital delivery

Transforming how people and businesses consume products & services through anytime, anywhere connectivity

2016 10B devices

2020 50B devices

Number of devices connected to the internet

88

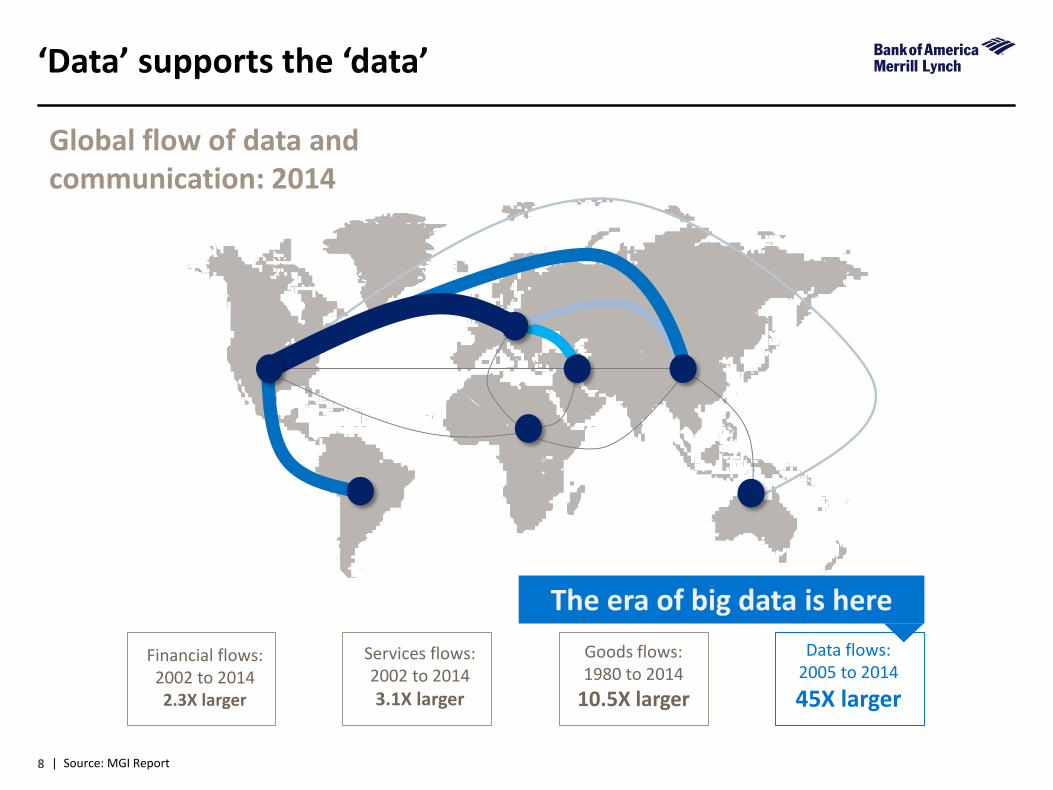

‘Data’ supports the ‘data’

Data flows:2005 to 2014

45X larger

Goods flows:1980 to 2014

10.5X larger

Services flows:2002 to 2014

3.1X larger

Financial flows:2002 to 20142.3X larger

| Source: MGI Report

Global flow of data and communication: 2014

The era of big data is here

9

Areas of focus

▪ Payments

▪ Creating/enhancing payment/securities clearing schemes

▪ Improving back office operational efficiencies

Areas of focus

▪ Payments/foreign exchange

▪ Acquiring

▪ Supply chain management

Areas of focus

▪ Challenger banks

▪ Payments/foreign exchange

▪ Lending/borrowing

▪ Investment advisory & brokerage

Fintech landscape

Consumer CorporateFinancial

institution

Represents 73% of total investment in Fintech

Represents 3% of total investment in Fintech

Represents 24% of total investment in Fintech

| Source: CB Insights, KPMG, Crunch Base & Citi Research. Financial Institution comprises of Asset Management (10%), Insurance (10%) and Investment Banking (4%)

Total investment in private Fintech companies increased >x10 in the last 5 years to $19bn in 2015

How are financial institutions coping with this disruption?

1111

– The Witch from Hansel & Gretel

Financial institutionsWill continue to be governed by two dominant philosophies

“If you can’t beat’em, eat’em” #1

*Also referred to asStrategic acquisitions

1212

Financial institutions

Pippen, Jordan… and Rodman

“The enemy of my enemy is my friend” – Kautilya, 4 BC#2

*Also referred to asStrategic alliances

Will continue to be governed by two dominant philosophies

1313

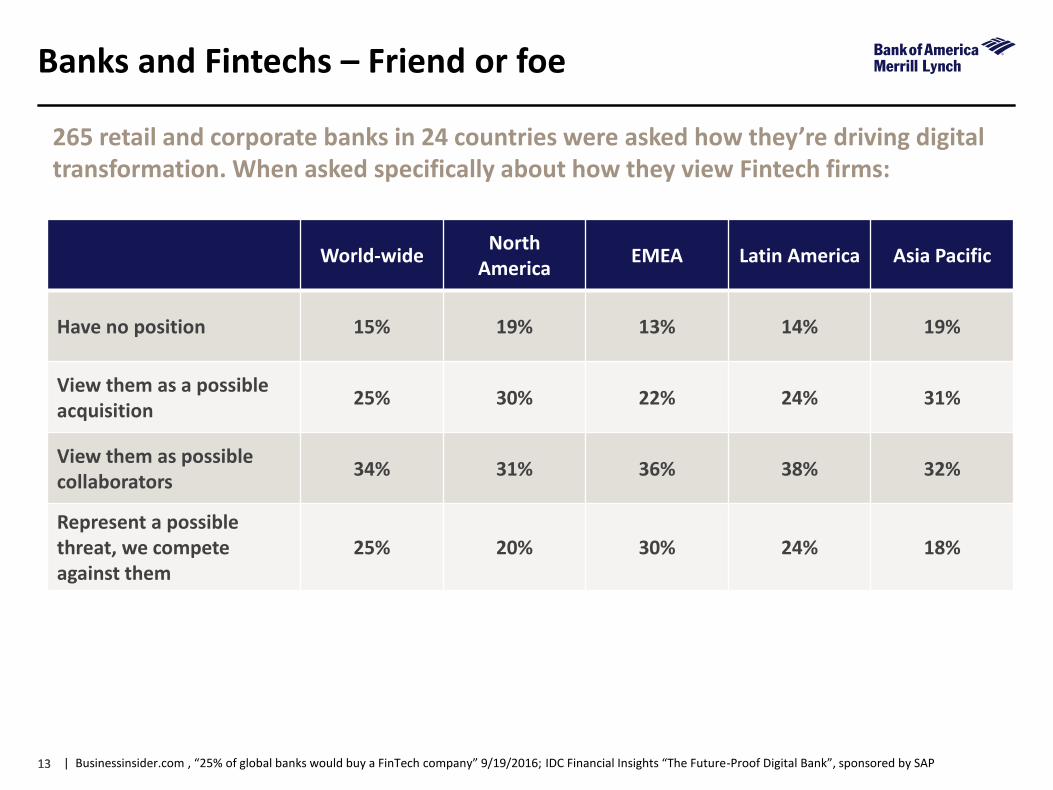

Banks and Fintechs – Friend or foe

World-wideNorth

AmericaEMEA Latin America Asia Pacific

Have no position 15% 19% 13% 14% 19%

View them as a possible acquisition

25% 30% 22% 24% 31%

View them as possiblecollaborators

34% 31% 36% 38% 32%

Represent a possible threat, we compete against them

25% 20% 30% 24% 18%

| Businessinsider.com , “25% of global banks would buy a FinTech company” 9/19/2016; IDC Financial Insights “The Future-Proof Digital Bank”, sponsored by SAP

265 retail and corporate banks in 24 countries were asked how they’re driving digital transformation. When asked specifically about how they view Fintech firms:

1414

Strategic alliances in the news

Forbes.com “DTCC Partners with IBM, Startups for Blockchain-based Credit Default Swaps Solution” 01/09/2017

Launching in early 2018, the solution has already had input from banks such as Barclays, Citi, Credit Suisse,

Deutsche Bank, JP Morgan, UBS and Wells Fargo as well as other infrastructure providers including IHS Markit

and Intercontinental Exchange…. The product will address one of the main problems with the current way that

transactions are processed post-trade, which is that it is entered into multiple databases in different ways….

To make sure that there’s one version of the trade, the DTCC must reconcile all these versions constantly.

Forbes.com “IBM’s Blockchain Consortium with The Seam Deploys ‘Hyperledger for Cotton Trading” 01/07/2017

US commodities trading and agribusiness software provider The Seam… is forming a blockchain consortium

in conjunction with IBM for the billion dollar global cotton industry deployed on the Hyperledger Fabric,

with the project kicking off early this year and poised to yield significant efficiencies. Working with IBM, the

company…revealed its intention to create an “industry-wide collaboration” to create a supply chain and

trading ecosystem built on IBM blockchain technology, specifically using the Hyperledger Fabric.

1515

So, what’s next?

1616

A national framework for Fintech development

The National Economic Council’s objectives for the financial services sector and the U.S. government entities that interact with the sector, as well as a principle framework policymakers and regulators should use to think about, engage with and assess the fintech ecosystem to meet these objectives.

Policy objectives for financial services

▪ Foster positive financial services innovation and entrepreneurship

▪ Promote safe, affordable, and fair access to capital

▪ Strengthen financial inclusion & health in the United States and abroad

▪ Address financial stability risks

▪ Further a 21st century financial regulatory framework

▪ Maintain national competitiveness

Statement of principles

▪ Think broadly about the financial ecosystem

▪ Start with the consumer in mind

▪ Promote safe financial inclusion and financial health

▪ Recognize and overcome potential technological bias

▪ Maximize transparency

▪ Strive for interoperability and harmonize technical standards

▪ Build in cyber security, data security, and privacy protections from the start

▪ Increase efficiency and effectiveness in financial infrastructure

▪ Protect financial stability

▪ Continue and strengthen cross-sector engagement

| National Economic Council, “A framework for FinTech” January 13, 2017

1717

Silicon Valley is coming. There are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking…..

Competitors are coming in the payments area. You have all read about Bitcoin, merchants building their own networks, PayPal and PayPal lookalikes …. But there is much for us to learn in terms of real-time systems, better encryption techniques, and reduction of costs and pain points for customers.

Having said that, we need to acknowledge our own flaws.

The new competitor

Jamie Dimon, Chairman and CEO letter to shareholdersJP Morgan Chase & Co. 2014 Annual Report

1818

Key themes for 2017 and beyond

End-to-end digitization of processes occurring rapidly to reduce or eliminate pain points.

▪ End-to-end digital account opening, KYC

▪ Dramatically streamlined documentation, real-time transparency on where the client and the bank are in the process

End-to-end digitization

1919

Regulation

2020

Key themes for 2017 and beyond

| 1.Greenwich Associates December 2016; 2. Bank of America Merrill Lynch “Global FinTech: 2017 YA: multiple themes drive attractive growth prospects” 01/09/2017

Blockchain for cash management has gone from immediacy and hype to more realistic longer runway timelines1

▪ Implementation of any meaningful volume for large corporates is 2 to 5 years away

▪ While more than 70 financial institutions are part of R3 consortium and some have working blockchain prototypes, the

▪ Lower frictional costs, shorter settlement time, and lower administrative costs are the most compelling benefits from Distributed Ledger Technology

More blockchain partnerships lead to more permissioned/private blockchain platforms2

▪ Discussions centered around standardization and ways to connect to existing financial services infrastructure2

Blockchain

2121

Market context

Market snapshot

Distributed ledger (“DL”)

Core functionality

▪ Ledger of asset ownership

▪ Enables assets transfer without central counterparty

Benefits

▪ Reduced costs & complexity, de-duplication

▪ Eliminates reconciliations

Current challenges

▪ Technology still in infancy

▪ Need for industry standards

▪ Competing technology protocols

Key components of distributed ledger

Distributed

▪ Single, shared record of asset ownership, transfer

▪ Resilient, no single point of failure

▪ Single, common shared ledger

▪ “Golden source” of asset ownership

Ledger

Uses cryptography to ensure: partner authentication, data privacy, data integrity and data origin authentication

Cryptographically secure

Other key terms

Permissioned vs. open

Closed group of authorized participants, vs. public anonymized network

Potential impact across entire capital markets value chain

~$85Bn of industry costs potentially in scope via improved technology, operational workflows and headcount rationalization

>800 bitcoin / DL companies globally1

>$1Bncumulative VC investment

into bitcoin & other DL companies2

~$494MM invested in 20152

~$160MMinvested in Q1 20163

>50 banks, financial institutions and infrastructure providers

analyzing DL

| 1. Source: Venture Scanner; 2. Source: CB Insights; 3. Source: Coindesk

Rules with source code freely available for modification and redistribution

Open source protocol Smart contract

Cryptographically assured business logic to update ledger

2222

Strategic alliances in the news

Financial News “Fintech startup launches platform for private bond placements” 01/09/2017

Origin Markets, a fintech startup that wants to simplify the way money is raised in the private

placement market for medium-term bonds, has teamed up with six investment banks and 20

borrowers on the introduction of the beta version of its platform.…launch partners on dealer

side are BNP Paribas, DekaBank, Bank of America Merrill Lynch, Societe Generale Corporate and

Investment Banking, Credit Suisse and Danske Bank. The borrowers include Hitachi Capital UK

and International Finance Corporation, a member of the World Bank.

PRNewsWire 12/19/2016

EuroClear and Paxos… are pleased to announce the successful completion of the first pilot for

EuroClear BankChain, the new blockchain settlement service for London bullion due to go live

in 2017. Over 600 OTC test bullion trades were settled on the EuroClear Bankchain platform….

2323

Unanswered questions

| Morgan Stanley “Big Banks try to harness the Blockchain” May 18, 2016

Faster isn’t always more profitable. A positive

return on invested capital is a must.

It must scale effectively from proof-of-concept

to succeed. Most proposals are looking at

a range of rules, including ones

restricting users or centralize all, or part, of

the blockchain.

Innovators need to share the cost of

building the infrastructure.

Different entities may have conflicting

priorities for a shared blockchain. Without

large groups of users, blockchains wouldn’t

be successful.

A governing body to decide who gets

access and manages its maintenance.

Regulating digital identities and cross-

border standards need to be addressed

during the build-out.

Can all parties leverage and

understand it?

Cost/benefit Cost mutualization Governance Simplicity

Users must be identifiable entities. Financial regulators would still enforce

“know your customer” and anti-money laundering rules.

ScalabilityIncentive alignment

Regulation Legal risks

Security

Is blockchain resilient against attack?

Users want to determine a standard ahead of any material

investments. Too many choices could

slow adoption.

Standards evolution

Questions that need to be answered if blockchain is to be used in the financial services industry.

2424

Key themes for 2017 and beyond (continued)

| 1. Greenwich Associates Dec 2016; 2. Bank of America Merrill Lynch “Global FinTech: 2017 YA: multiple themes drive attractive growth prospects” 01/09/2017

PSD2 opens consumer accounts held by banks to third parties who can provide multiple value added services in addition to payment related services1

▪ Rise of the payment initiation service providers (PISP)2

─ Can initiate payment from user’s payment account held at another payment service provider e.g. accountholder’s financial institution

─ Merchants can offer consumers option to pay with online credit transfer rather than credit card

EU payments services directive 2 (PSD2)

2525

Continued emergence of new players in FinTech

FACEBOOK TO OFFER C2B PAYMENT SERVICE

“Facebook has launched a payment method in Europe. They have obtained an e-payments license from the Central Bank of Ireland, signaling

that the ability to pay people through the Messenger app (already available in the US) which will probably be soon coming to Europe.

The Central Bank of Ireland's approval of the payments license authorized

Facebook Payments International (FBPIL) in October 2016 for ‘e-money issuance’ and ‘payment services’ As a member of the European Union, passporting rights means that the Irish license would apply throughout the other 27 EU member states.

Currently the payment service only works in the US. It allows customers to send money to friends via the Messenger app. But it has been reported

that the social network will soon be adding payments to businesses, as well as friends via the app. This could be huge because Facebook had 1.79 billion users at end of 3Q 2016 of which 1 bn+ were active in the last month.”

| CTMfile.com December 19, 2016

From unexpected places….

1.79USERSB I L L I O N

2626

Key themes for 2017 and beyond (continued)

| 1 Institute for Development and Research (established by The Reserve Bank of India), “Application of Blockchain Technology to Banking and Financial Sector in India” January 2017

A Central or Reserve Bank develops the infrastructure, security and controls which enables them to digitize their native currency1

Digitizing currency

2727

Potential benefits

Cost savings

Mitigation of FX volatility

Faster settlement

Greater efficiency

Reduced processing time

Improved KYC compliance

Automatic reconciliation

Increases the efficiency of treasury technology (e.g. TMS, account analysis and analytic software)

The Reserve Bank of IndiaConsiders digitizing the Rupee using blockchain

Institute for Development and Research (established by The Reserve Bank of India), “Application of Blockchain Technology to Banking and Financial Sector in India” January 2017

Blockchain holds the potential for all participants in a business network to share

a system of records, which will provide consensus, provenance, immutability

and finality around the transfer of assets with the business network.

PYMNTS.COM, “India's Reserve Bank wants to Digitize the Rupee on Blockchain” 01/11/2017

The Unified Payments Interface, an interbank system to facilitate

stream-lined payments saw more transactions pass through in the

first 9 days of December, than the entire month of November 2016.

2828 | 1. Greenwich Associates Dec 2016; 2. Bank of America Merrill Lynch “Global FinTech: 2017 YA: multiple themes drive attractive growth prospects” 01/09/2017

Key themes for 2017 and beyond (continued)

Artificial intelligence and the banking equivalent of “robo-advising” will be the next major breakthrough1

▪ IBM Watson-like advisory capabilities matched to company’s specific set of needs

▪ Will continue to rise in prominence as they offer easy, simple, inexpensive online access to portfolio management2

─ Focus on helping companies maximize cash flow efficiency, short-term investments, liquidity needs, multi-country tax efficiency, etc.

▪ Applications include digital self-service advice for clients as well as AI leveraged by bank sales force to be better informed advisors that are more efficient1

─ Wealth management for affluent and younger demographics, which traditional wealth managers view as uneconomical and unwilling to pay high service charges2

Artificial intelligence

2929

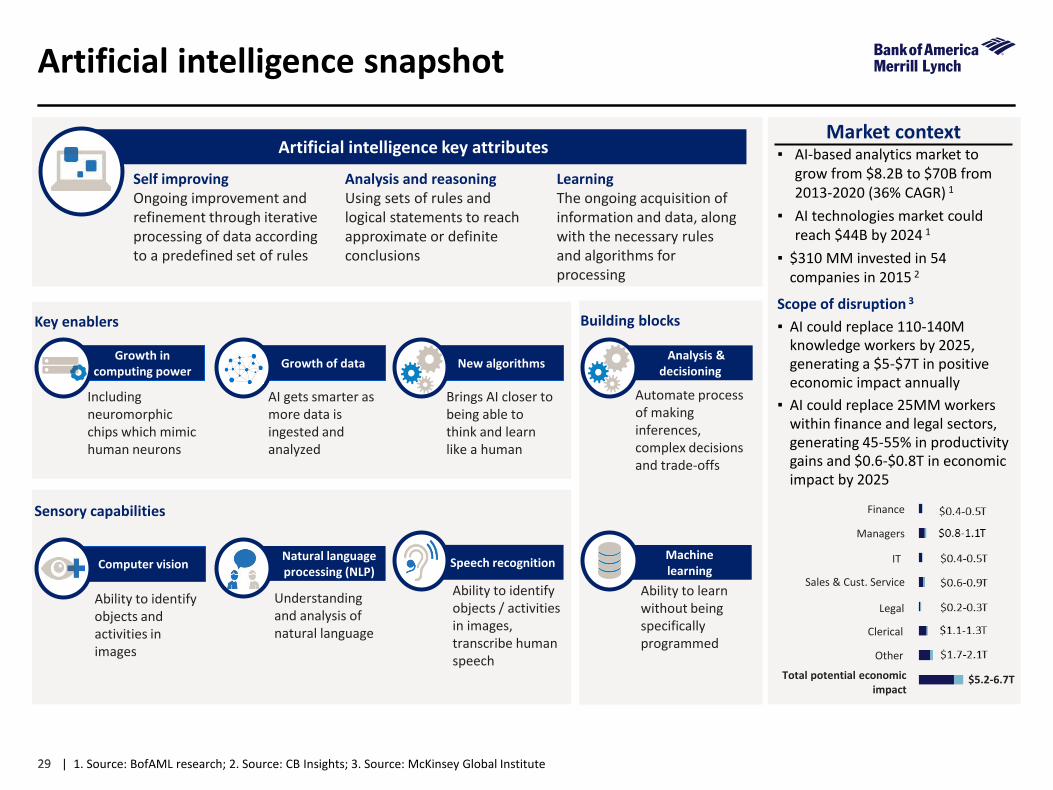

Artificial intelligence snapshot

▪ AI-based analytics market to grow from $8.2B to $70B from 2013-2020 (36% CAGR) 1

▪ AI technologies market could reach $44B by 2024 1

▪ $310 MM invested in 54 companies in 2015 2

Scope of disruption 3

▪ AI could replace 110-140M knowledge workers by 2025, generating a $5-$7T in positive economic impact annually

▪ AI could replace 25MM workers within finance and legal sectors, generating 45-55% in productivity gains and $0.6-$0.8T in economic impact by 2025

Market context

| 1. Source: BofAML research; 2. Source: CB Insights; 3. Source: McKinsey Global Institute 29

Artificial intelligence key attributes

Self improvingOngoing improvement and refinement through iterative processing of data according to a predefined set of rules

Analysis and reasoningUsing sets of rules and logical statements to reach approximate or definite conclusions

LearningThe ongoing acquisition of information and data, along with the necessary rules and algorithms for processing

Key enablers

New algorithms

Brings AI closer to being able to think and learn like a human

AI gets smarter as more data is ingested and analyzed

Growth of data

Computer vision

Ability to identify objects and activities in images

Growth in computing power

Including neuromorphic chips which mimic human neurons

Finance

IT

Sales & Cust. Service

Managers

Legal

Clerical

Other

Total potential economic impact

$5.2-6.7T

Sensory capabilities

Ability to learn without being specifically programmed

Machine learning

Natural language processing (NLP)

Understanding and analysis of natural language

Automate process of making inferences, complex decisions and trade-offs

Analysis & decisioning

Building blocks

Ability to identify objects / activities in images, transcribe human speech

Speech recognition

3030

Key early stage AI firms by area of focus

30

Fraud detection

Security / authentication

SalesPersonal assistant

Intelligencetools

Marketing HR / recruiting

Behavox,SiftScience,

Socure,ThreatMetrix,

Feedzai, Brighterion,

Verafin

Crossmatch, Conjur,

EyeVerify, Bitsight, Cylance

Preact, Aviso,RelateIQ, NGData,

Clarabridge, Framed Data,

Infer, Attensity,Causata

Siri, Google Now, Cortana,Clever Sense,

Tempo AI,Rebinlabs,

Kasisto,Fusemachines, Viv, Clara Labs

Adatao, Palantir,Quid, DigitalReasoning,

FirstRain

BrightFunnel,BloomReach,CommandIQ, AirPR, Radius,

TellApart,People Pattern,

Freshplum

TalentBin, Entelo, Predikt,

Connectifier, Gild, hiQ,

Concept Node

Finance Legal Adtech Agriculture Education Manufacturing Medical

FinGenius,AlphaSense,

Kensho, Dataminr,

Minetta Brook,ForwardLane

Lex Machina, Brighteaf,

Counselytics, Ravel, Judicata,

Brevia, Diligence Engine

Metamarkets, Dstillery, Rocket Fuel, YieldMo,

Adbrain

Blue River, TerrAvion

Declara, Coursera,Knewton, Kidaptive

Sight Machine,Microscan

Systems, Ivisys, Boulder Imaging

Parzival, Transcriptic,Genescient,

Zephyr Health, Grand RoundTable, Tute

Consumer finance

Oil and gasMedia / content

Philanthropy Automotive Diagnostics Retail

Affirm, inVenture, Zest

Finance, BillsGuard

Kaggle, BiotaTechnology,

TachyusSolutions,

Flutura

Outbrain, Newsie, Arria,Sailthru, Wavii,

Owlin, Narrative Science, Yseop

DataKind, Thorn, Data

Guild

Google Car,Continental,

Tesla,MobileEye,

Cruise

Enlitic, 3scan, Lumiata,Entopsis

Bay Sensors, Prism Skylabs, Celect, Euclid

Augmented reality Gestural computing Robotics Emotional recognition

Wearable Intelligence, APX, Blippar, Meta Intelligence,

Layar

Thalmic Labs, OmekInteractive, Flutter, LeapMotion, Eye Sight, 3Gear

Systems, GestureTek, Nod

Intel, Liquid Robotics, iRobot, SoftBank, Jibo, Boston

Dynamics, Anki, EvolutionRobotics

Affectiva, Beyond Verbal, Emotient, Cogito

| Source: BofAML Research

Artificial intelligence innovation is targeted across industries with a small portion of firms focused on finance sector

Enterprise level technology is a key focus for both innovative companies and large corporates

Rethinking enterprise

Rethinking industries

Rethinking human /

computer interactions

(HCI)

Relevant to financial services Other industries

31

Questions?

Comments?

32

Notice to recipient

“ Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Securities, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp., both of which are registered broker-dealers and Members of SIPC, and, in other jurisdictions, by locally registered entities. Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp. are registered as futures commission merchants with the CFTC and are members of the NFA. Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed. ©2016 Bank of America Corporation.

Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured * May Lose Value * Are Not Bank Guaranteed.

These materials have been prepared by one or more subsidiaries of Bank of America Corporation for the client or potential client to whom such materials are directly addressed and delivered (the “Company”) in connection with an actual or potential mandate or engagement and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with us. These materials are based on information provided by or on behalf of the Company and/or other potential transaction participants, from public sources or otherwise reviewed by us. We assume no responsibility for independent investigation or verification of such information (including, without limitation, data from third party suppliers) and have relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the managements of the Company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Company and are being furnished and should be considered only in connection with other information, oral or written, being provided by us in connection herewith. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Bank of America Corporation or any of its affiliates to provide or arrange any financing for any transaction or to purchase any security in connection therewith. These materials are for discussion purposes only and are subject to our review and assessment from a legal, compliance, accounting policy and risk perspective, as appropriate, following our discussion with the Company. We assume no obligation to update or otherwise revise these materials. These materials have not been prepared with a view toward public disclosure under applicable securities laws or otherwise, are intended for the benefit and use of the Company, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without our prior written consent. These materials may not reflect information known to other professionals in other business areas of Bank of America Corporation and its affiliates.

Bank of America Corporation and its affiliates (collectively, the “BAC Group”) comprise a full service securities firm and commercial bank engaged in securities, commodities and derivatives trading, foreign exchange and other brokerage activities, and principal investing as well as providing investment, corporate and private banking, asset and investment management, financing and strategic advisory services and other commercial services and products to a wide range of corporations, governments and individuals, domestically and offshore, from which conflicting interests or duties, or a perception thereof, may arise. In the ordinary course of these activities, parts of the BAC Group at any time may invest on a principal basis or manage funds that invest, make or hold long or short positions, finance positions or trade or otherwise effect transactions, for their own accounts or the accounts of customers, in debt, equity or other securities or financial instruments (including derivatives, bank loans or other obligations) of the Company, potential counterparties or any other company that may be involved in a transaction. Products and services that may be referenced in the accompanying materials may be provided through one or more affiliates of Bank of America Corporation. We have adopted policies and guidelines designed to preserve the independence of our research analysts. These policies prohibit employees from offering research coverage, a favorable research rating or a specific price target or offering to change a research rating or price target as consideration for or an inducement to obtain business or other compensation. We are required to obtain, verify and record certain information that identifies the Company, which information includes the name and address of the Company and other information that will allow us to identify the Company in accordance, as applicable, with the USA Patriot Act (Title III of Pub. L. 107-56 (signed into law October 26, 2001)) and such other laws, rules and regulations as applicable within and outside the United States.

We do not provide legal, compliance, tax or accounting advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by us to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. If any person uses or refers to any such tax statement in promoting, marketing or recommending a partnership or other entity, investment plan or arrangement to any taxpayer, then the statement expressed herein is being delivered to support the promotion or marketing of the transaction or matter addressed and the recipient should seek advice based on its particular circumstances from an independent tax advisor. Notwithstanding anything that may appear herein or in other materials to the contrary, the Company shall be permitted to disclose the tax treatment and tax structure of a transaction (including any materials, opinions or analyses relating to such tax treatment or tax structure, but without disclosure of identifying information or, except to the extent relating to such tax structure or tax treatment, any nonpublic commercial or financial information) on and after the earliest to occur of the date of (i) public announcement of discussions relating to such transaction, (ii) public announcement of such transaction or (iii) execution of a definitive agreement (with or without conditions) to enter into such transaction; provided, however, that if such transaction is not consummated for any reason, the provisions of this sentence shall cease to apply. ©2017 Bank of America Corporation.